Mexico MNVO Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

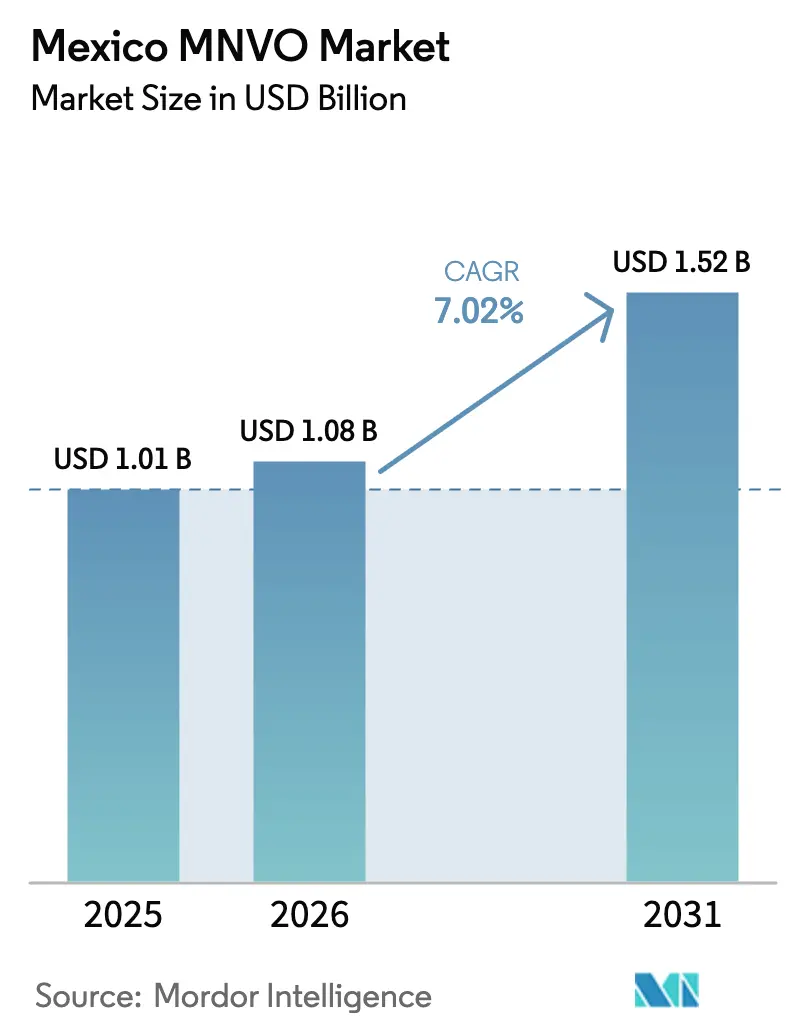

| Base Year Market Size (2025) | USD 1.01 Billion |

| Market Size (2026) | USD 1.08 Billion |

| Market Size (2031) | USD 1.52 Billion |

| Growth Rate (2026 - 2031) | 7.02% CAGR |

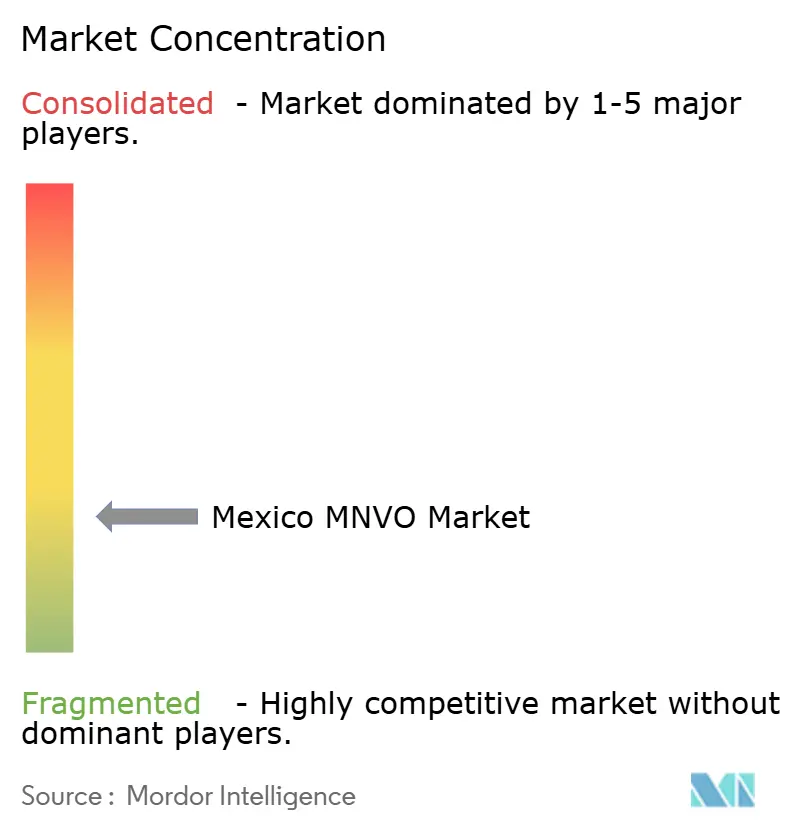

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Mexico MNVO Market Analysis by Mordor Intelligence

The Mexico MNVO Market size was valued at USD 1.01 billion in 2025 and estimated to grow from USD 1.08 billion in 2026 to reach USD 1.52 billion by 2031, at a CAGR of 7.02% during the forecast period (2026-2031).

Wholesale access to the Red Compartida network, rising price competition, and fast eSIM adoption are expanding the subscriber base and reshaping competitive dynamics. MVNOs collectively serve 11.9% of all mobile lines—up from 0.8% nine years earlier—underscoring their disruptive traction. Consumer demand for low-cost data, cloud-based operating models, and retail-integrated distribution strategies continue to accelerate revenue growth. Incumbents are responding with heavier capital spending, while regulatory uncertainty around the Federal Telecommunications Institute (IFT) could alter spectrum allocation rules and wholesale pricing. Overall, the Mexico MVNO market is poised to benefit from digital-only onboarding, IoT deployment, and cross-border service innovation over the forecast horizon.

Key Report Takeaways

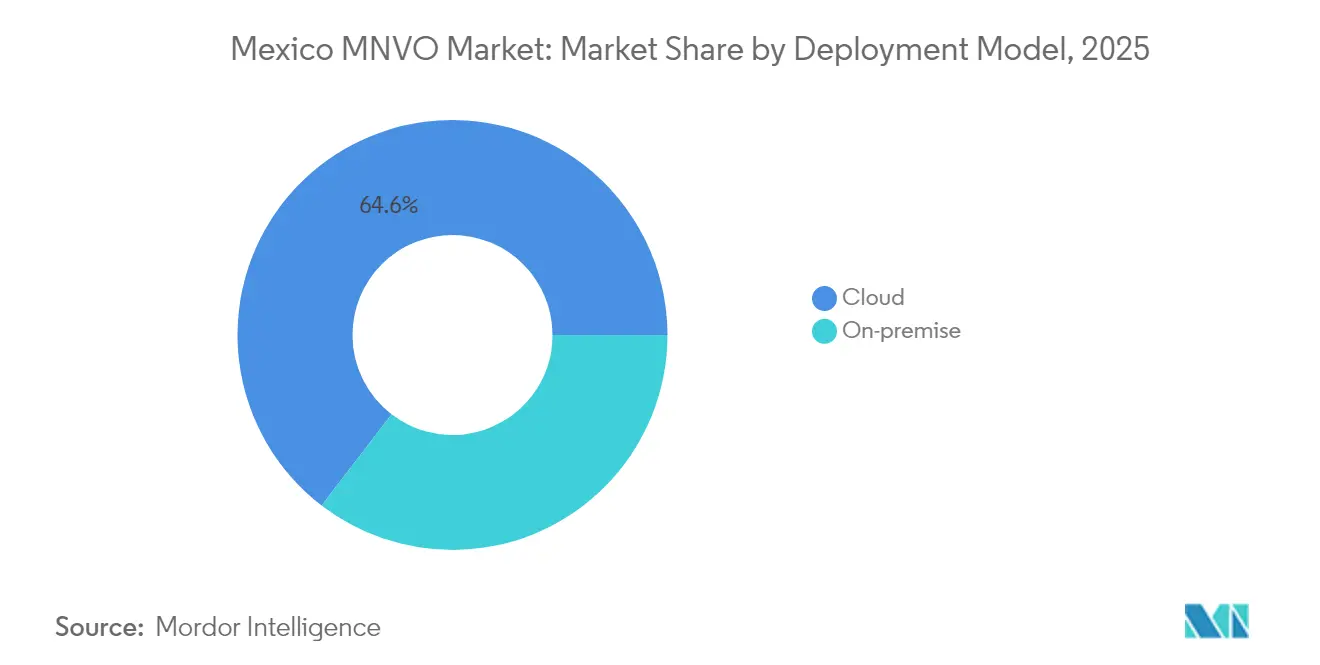

- By deployment model, the cloud segment captured 64.58% of Mexico MVNO market share in 2025; on-premise platforms are projected to grow at an 11.56% CAGR through 2031.

- By operational mode, full MVNOs accounted for 39.60% of Mexico MVNO market size in 2025 and are forecast to expand at a 11.88% CAGR to 2031.

- By subscriber type, consumer lines held 73.68% of Mexico MVNO market share in 2025, while IoT-specific subscriptions are advancing at a 21.34% CAGR over the same period.

- By application, discount services represented 39.45% of Mexico MVNO market size in 2025 and cellular M2M connections are growing at a 21.34% CAGR through 2031.

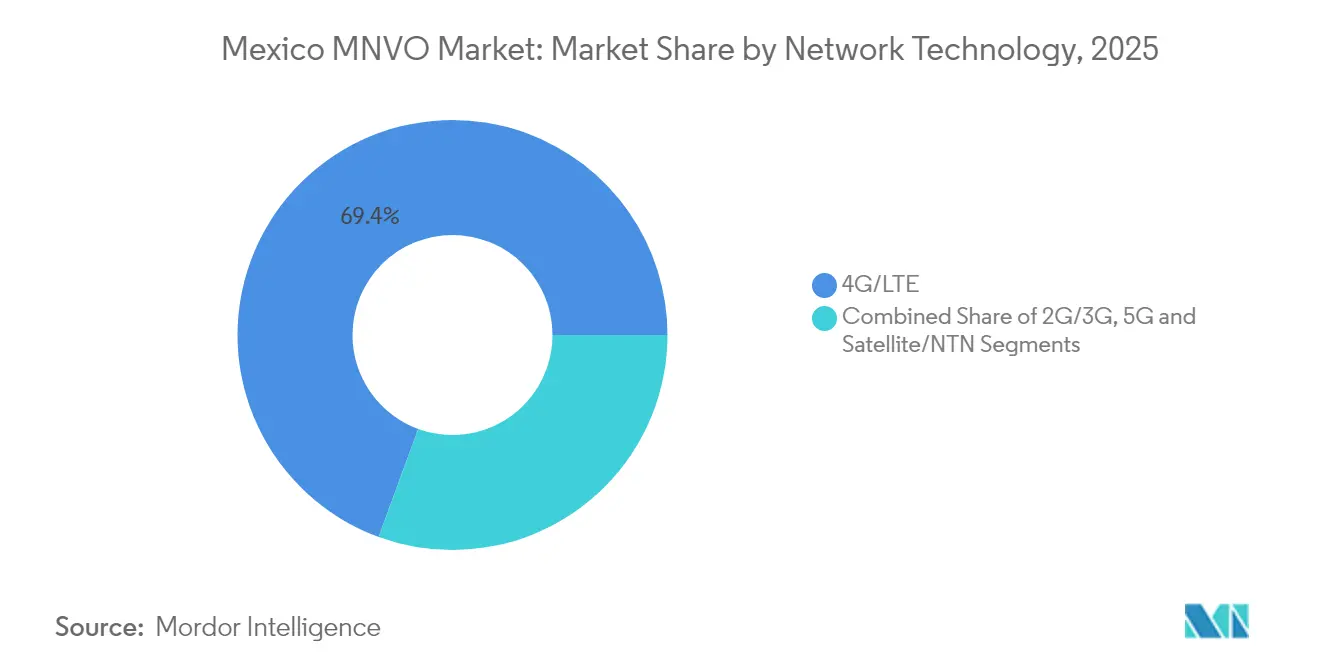

- By network technology, 4G/LTE commanded 69.42% of Mexico MVNO market share in 2025; satellite/NTN links are rising at a 64.12% CAGR.

- By distribution channel, online and digital-only sales secured 37.85% of Mexico MVNO market share in 2025 and are increasing at a 15.94% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Mexico MNVO Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Wholesale access to Red Compartida | +1.8% | Nationwide; strongest in rural zones | Medium term (2-4 years) |

| Price-sensitive prepaid users | +1.2% | Urban centers | Short term (≤ 2 years) |

| Retail-led bundling by large chains | +0.9% | National network of mass-merchandisers | Medium term (2-4 years) |

| Rapid eSIM uptake | +0.7% | High-penetration cities | Short term (≤ 2 years) |

| Cross-border migrant plans | +0.4% | Border states and key metros | Long term (≥ 4 years) |

| IoT-focused demand post-NOM-236 | +0.6% | Industrial corridors & smart-city initiatives | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Wholesale access to Red Compartida lowers entry barriers

Red Compartida’s open-access 4G footprint covers 92.4% of the population and supports more than 100 MVNOs, enabling cost-efficient nationwide reach for newcomers. [1]Altán Redes, “Red Compartida Cobertura Nacional,” altanredes.comWalmart-backed BAIT rapidly scaled to nearly 12% subscriber share by leveraging this infrastructure, prompting América Móvil to file pricing complaints with regulators.[2]América Móvil, “Informe Anual 2024,” americamovil.com The platform’s standardized wholesale rates reduce capital intensity, allowing virtual operators to expand rural coverage without owning spectrum. Regulatory scrutiny may adjust fee structures, yet the current model continues to underwrite aggressive MVNO growth. Future inclusion of 5G services remains a pivotal variable for sustained competitiveness.

Price-sensitive prepaid users boost low-ARPU growth

Prepaid connections account for 83% of Mexican mobile lines, and MVNO data prices can be six times cheaper than incumbent tariffs. GDP growth of only 1.12% in 2025 keeps household budgets tight, pushing millions toward lower-priced plans. BAIT gained 1.5 million customers in one year while Telcel lost 821,000 users, illustrating elasticity in a price-driven market. MVNOs able to operate on lean margins capture churn from premium operators by bundling generous data allowances with minimal overhead. This cost advantage is expected to endure as macroeconomic headwinds persist.

Retail-led bundling by giants expands reach

Nation-wide retailers use extensive store footprints and loyalty programs to distribute SIMs and bundle connectivity with everyday purchases. Walmart’s BAIT offers activation in 2,500 outlets, while OXXO sells AT&T-backed lines across 21,000 stores. Store associates guide first-time users through activation, lowering customer-acquisition costs and driving rapid subscriber uptake. Loyalty points redeemed for airtime strengthen stickiness and encourage repeat top-ups. The model’s success is prompting other retailers to explore similar ventures, broadening MVNO access to cash-preferred consumers.

Rapid eSIM uptake enables digital-only onboarding

Telcel, AT&T México, and Movistar support eSIM across 99% of the territory, letting MVNOs provide instant over-the-air activation without physical logistics. Digital sign-up reduces operating costs, allows multiple profiles per device, and appeals to cross-border travelers who switch carriers frequently. Over-the-air provisioning accelerates time-to-revenue and supports niche offerings such as temporary data passes. As smartphone replacement cycles shorten, eSIM readiness is becoming a baseline consumer expectation that virtual operators can leverage for differentiation. Regulatory frameworks around remote KYC continue to mature, further easing digital onboarding.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| MVNO exclusion from 5G wholesale | -1.4% | Nationwide | Medium term (2-4 years) |

| Low brand awareness & perceived quality gaps | -0.8% | Dense urban markets | Short term (≤ 2 years) |

| Rising Red Compartida wholesale fees | -0.6% | National | Medium term (2-4 years) |

| High satellite/NTN slicing costs | -0.3% | Remote regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

MVNO exclusion from 5G wholesale deals limits offerings

Mexico hosts 13 million 5G lines—9.1% of total connections—yet MVNOs cannot access next-generation wholesale capacity, constraining enterprise and IoT service propositions.[3]RCR Wireless News, “IFT-12 Spectrum Auction Details Announced,” rcrwireless.com Incumbents have invested more than USD 1.8 billion in 5G networks, widening the technology gap. The IFT-12 auction may not mandate open 5G wholesale, leaving MVNOs dependent on 4G for the foreseeable future. Enterprises seeking low-latency links could favor incumbent operators, limiting MVNO penetration into high-value segments. Unless regulators intervene, 5G exclusion will suppress premium-revenue growth for virtual players during the medium term.

Low brand awareness and perceived quality gaps curb adoption

Surveys show 41.8% of users remain unclear on newer mobile technologies and often equate low prices with lower quality. MVNO marketing budgets are modest compared with incumbents, reducing visibility in mainstream media. Concerns about network reliability persist despite MVNOs sharing the same underlying infrastructure. Regulatory enforcement of transparency mandates varies, allowing some providers to over-promise on speeds and eroding consumer trust. These perception barriers slow subscriber migration to MVNOs, particularly in competitive urban markets where brand recognition influences purchase decisions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment Model: Cloud infrastructure underpins rapid scale

Cloud platforms accounted for 64.58% of total MVNO revenue in 2025 and are on track for an 11.56% CAGR. Operators offload core network functions to the cloud to minimize capital expenditures and accelerate service launches. Google Cloud’s new region in Querétaro will boost capacity, lower latency, and support AI-driven service orchestration. On-premise solutions persist in security-sensitive niches such as financial services, yet they face slower adoption due to higher upkeep costs.

Cloud-native architectures align with national AI integration, where 90% of firms plan machine-learning deployments by 2026. Function virtualization enables MVNOs to roll out digital wallets and content bundles without hardware upgrades, sustaining differentiation against reseller-only competitors.

By Operational Mode: Full MVNOs capture margin and control

Full MVNOs commanded 39.60% of revenue in 2025 and are forecast for a 11.88% CAGR as brands seek end-to-end control over billing, customer experience, and product design. BAIT leverages integrated retail data to fine-tune tariffs and promote cross-selling. Light MVNO and service-operator models fit brands prioritizing distribution reach over network management but generate slimmer margins. Convergence strategies—bundling mobile with broadband—make full MVNO status appealing to cable and ISP players such as Megacable, which recorded a 22.3% rise in mobile subscribers during 2024.

By Subscriber Type: Consumer lines dominate while IoT surges

Consumer SIMs account for 73.68% of total MVNO lines in 2025, reflecting Mexico’s prepaid orientation. IoT-specific SIMs are expanding at 21.34% CAGR, propelled by NOM-236 telemetry mandates and smart-city rollouts. Enterprises are gradually increasing deployments but demand service-level agreements and management dashboards, keeping sales cycles lengthy. Northern manufacturing hubs adopt IoT for fleet management and predictive maintenance, opening high-density, low-data revenue streams for specialized MVNOs.

By Application: Discount services lead; M2M emerging fast

Discount bundles held 39.45% of revenue in 2025, confirming the price sensitivity of consumers. Cellular M2M lines are growing at a 21.34% CAGR as industrial automation and smart-metering gather pace. Cross-border plans targeting the USD 66.2 billion remittance corridor between Mexico and the United States create additional niche opportunities. Sustaining profitability in discount segments will require efficiency gains and diversification into higher-margin enterprise niches.

By Network Technology: 4G anchors operations; satellite growth accelerates

4G/LTE supports 69.42% of MVNO traffic in 2025 via Red Compartida and incumbent roaming deals. Satellite/NTN links are surging at a 64.12% CAGR thanks to Starlink’s rapid uptake and government subsidies for rural access. Without wholesale 5G access, MVNOs risk falling behind on enterprise latency requirements. Community-based networks such as Movistar’s Helium partnership showcase alternative densification tactics that could extend to virtual operators.

By Distribution Channel: Digital adoption lifts online sales

Digital-only channels generated 37.85% of 2025 revenue and are expanding at 15.94% CAGR, driven by eSIM activation and stronger e-commerce habits. Physical retailers retain strategic value: OXXO and Walmart together host more than 23,000 locations, onboarding cash-preferred users. Hybrid models pairing in-store SIMs with app-based top-ups optimize reach and cost. Streamlined e-KYC rules and biometric verification will further accelerate remote onboarding by 2026.

Geography Analysis

Nationwide Red Compartida coverage enables MVNOs to reach 92.4% of residents, yet Mexico City, Guadalajara, and Monterrey account for roughly one-third of traffic due to higher incomes and smartphone penetration. Border states such as Baja California and Nuevo León offer cross-border plan demand tied to 12.3 million yearly migrant crossings. Near-shoring has pumped USD 36.9 billion into northern manufacturing in 2024, spurring enterprise IoT connectivity needs.

Southern rural regions gain connectivity through satellite backhaul and community Wi-Fi nodes under Internet para Todos, shrinking the digital divide. While ARPU outside major metros trails national averages, wholesale fees are lower, preserving margins. Regulatory uniformity enforced by IFT standardizes quality, yet any move to dissolve the regulator could disrupt license renewal and spectrum fee policies.

Competitive Landscape

Thirty-seven MVNOs compete alongside three dominant network operators, producing moderate fragmentation. América Móvil still controls roughly 70% of total mobile lines, but MVNO share climbed to 11.9% in 2024. The top five providers hold close to 80% of combined subscriptions, leading to a market concentration score of 8. Incumbents defend their base with USD 6.7 billion in 2025 capex. BAIT leverages retail analytics to grow rapidly, while Megacable bundles fixed and mobile services. Telefónica’s USD 609 million divestiture talks with Beyond ONE hint at further consolidation. Technological agility—cloud cores, eSIM, AI chatbots—emerges as a key differentiator for nimble MVNOs lacking spectrum but able to pivot quickly.

Mexico MNVO Industry Leaders

BAIT

OXXO CEL

Virgin Mobile Mexico

FreedomPop Mexico

izzi Movil

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Telefónica began exclusive talks to sell its Mexican unit to Beyond ONE for USD 609 million.

- May 2025: BAIT forecast 21.4 million subscribers and 13% share by end-2025.

- April 2025: América Móvil announced USD 6.7 billion capex for 2025.

- March 2025: Starlink launched Mini hardware in Mexico via Liverpool and Home Depot.

Mexico MNVO Market Report Scope

Mobile virtual network operators (MVNOs) are wireless communication service providers that do not own the wireless network infrastructure but instead buy network capacity from existing MNOs to deliver services to their users. Operational models, such as resellers, service operators, full MVNO, and others, are considered part of the study. The study is structured to capture revenues accrued by MVNOs through various voice, data, and other services offered in Mexico.

The report covers the analysis of the Mexican mobile virtual network operator (MNVO) market. It is segmented by operating model (reseller, service operator, full MNVO, and other models) and end user (business and consumer). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| Cloud |

| On-premise |

| Reseller |

| Service Operator |

| Full MVNO |

| Light / Brand MVNO |

| Consumer |

| Enterprise |

| IoT-specific |

| Discount |

| Business |

| Cellular M2M |

| Others |

| 2G/3G |

| 4G/LTE |

| 5G |

| Satellite/NTN |

| Online / Digital-only |

| Traditional Retail Stores |

| Carrier Sub-brand Stores |

| Third-Party / Wholesale |

| By Deployment Model | Cloud |

| On-premise | |

| By Operational Mode | Reseller |

| Service Operator | |

| Full MVNO | |

| Light / Brand MVNO | |

| By Subscriber Type | Consumer |

| Enterprise | |

| IoT-specific | |

| By Application | Discount |

| Business | |

| Cellular M2M | |

| Others | |

| By Network Technology | 2G/3G |

| 4G/LTE | |

| 5G | |

| Satellite/NTN | |

| By Distribution Channel | Online / Digital-only |

| Traditional Retail Stores | |

| Carrier Sub-brand Stores | |

| Third-Party / Wholesale |

Key Questions Answered in the Report

How large is the Mexico MNVO Market opportunity in 2026? What CAGR is expected for virtual operators through 2031?

The Mexico MNVO Market size is USD 1.08 billion in 2026 and is forecast to reach USD 1.52 billion by 2031. Aggregate revenue is projected to grow at a 7.02% CAGR over the 2026-2031 period.

Which operational model is expanding fastest?

Full MVNOs are forecast to post a 11.88% CAGR as brands seek full control of billing and customer experience.

How important is cloud deployment for Mexico’s MVNOs?

Cloud infrastructure already underpins 64.58% of total revenue because it lowers capex and speeds service launches.

What role does eSIM play in customer acquisition?

ESIM enables instant, digital-only activation, cutting distribution costs and accelerating subscriber onboarding nationwide.

Why are IoT-specific SIMs gaining traction?

Regulatory telemetry mandates and industrial automation projects are driving IoT SIM connections at a 21.34% CAGR.

Page last updated on: