Mexico Last Mile Delivery Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

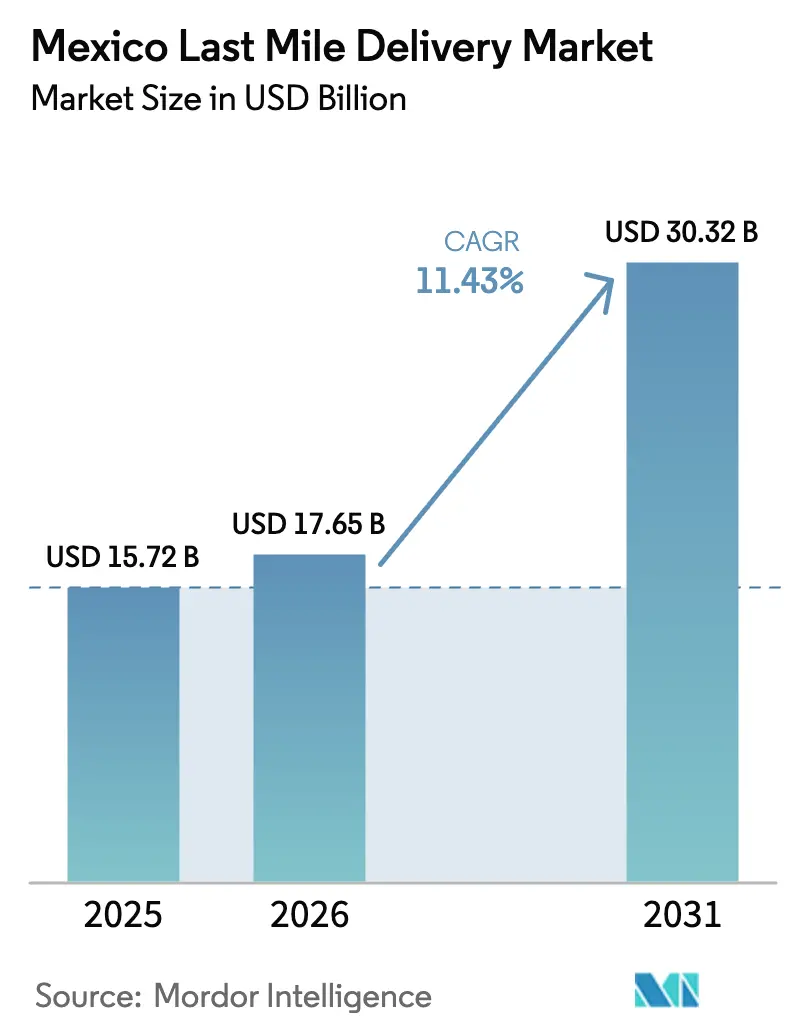

| Base Year Market Size (2025) | USD 15.72 Billion |

| Market Size (2026) | USD 17.65 Billion |

| Market Size (2031) | USD 30.32 Billion |

| Growth Rate (2026 - 2031) | 11.43% CAGR |

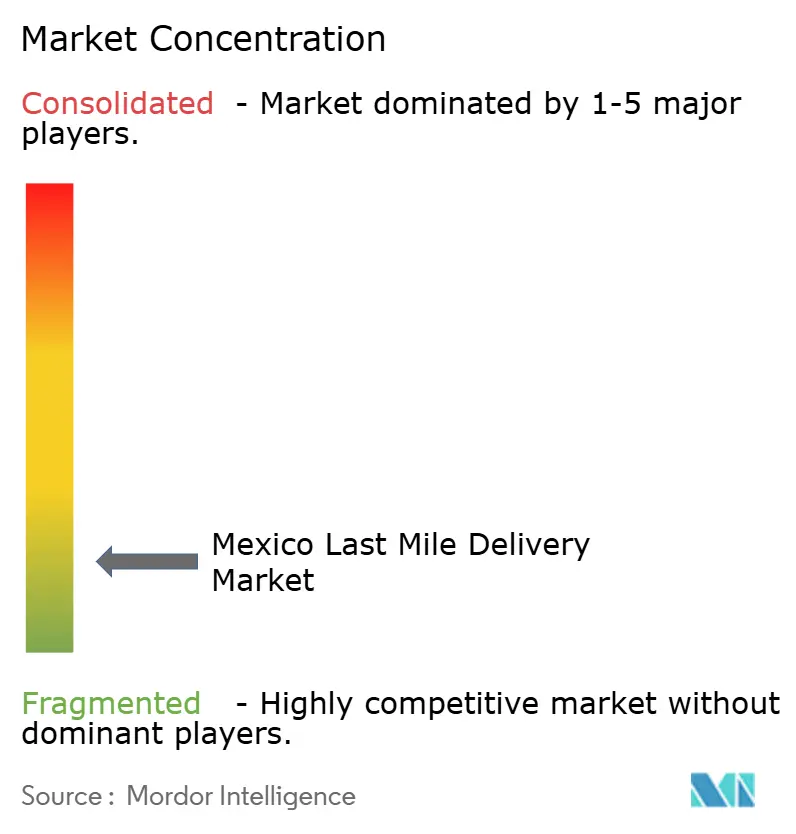

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Mexico Last Mile Delivery Market Analysis by Mordor Intelligence

The Mexico Last Mile Delivery Market size is expected to increase from USD 15.72 billion in 2025 to USD 17.65 billion in 2026 and reach USD 30.32 billion by 2031, growing at a CAGR of 11.43% over 2026-2031.

The Mexico last-mile delivery market is evolving rapidly as online retail penetration increases and consumers demand faster and more flexible delivery options. Logistics providers are expanding urban distribution hubs and technology-driven route optimization to improve delivery efficiency in dense metropolitan areas such as Mexico City and Monterrey. The market is also seeing the entry of digital delivery platforms and independent courier networks, enabling same-day and next-day delivery services. However, traffic congestion, urban infrastructure constraints, and cost pressures continue to influence delivery models. As competition intensifies, companies are focusing on fleet optimization, localized fulfillment, and partnerships with retailers to strengthen their last-mile capabilities.

Key Report Takeaways

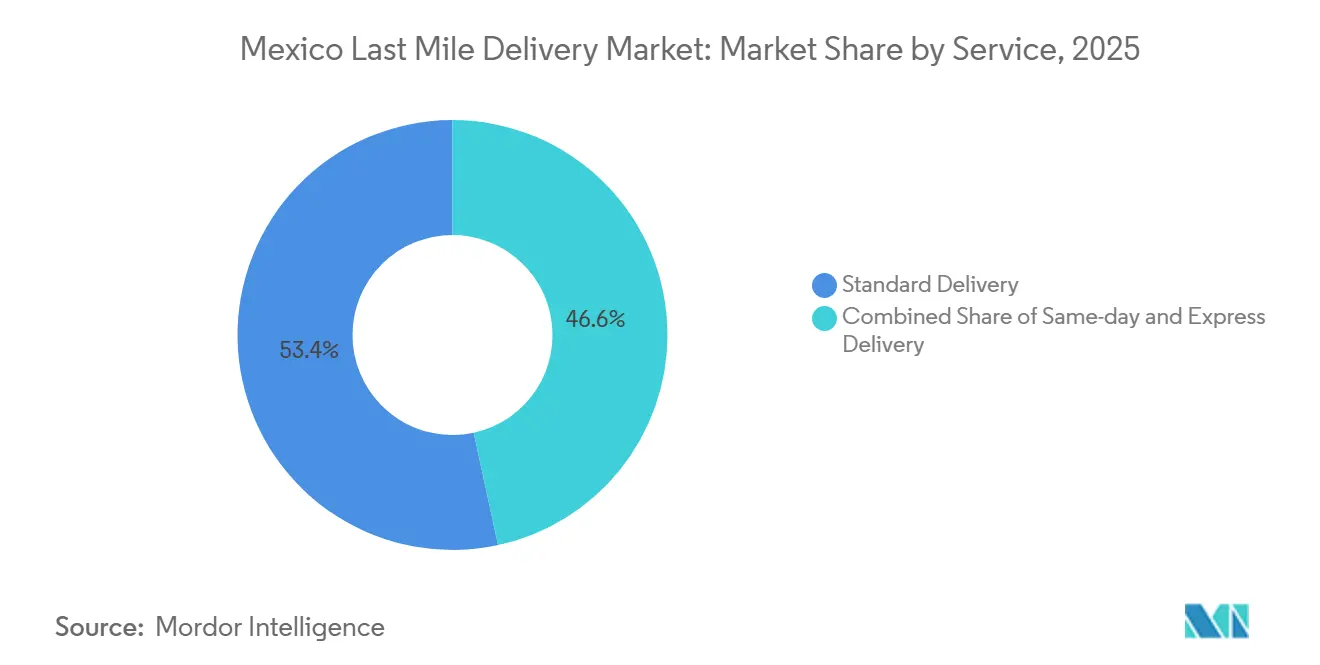

- By service, Standard Delivery led with 53.45% market share in 2025, while Same-Day is forecast to grow at a 12.45% CAGR through 2026-2031.

- By business model, B2C accounted for 61.12% of the Mexico last-mile delivery market share in 2025 and is projected to post the fastest CAGR at 12.67% during 2026-2031.

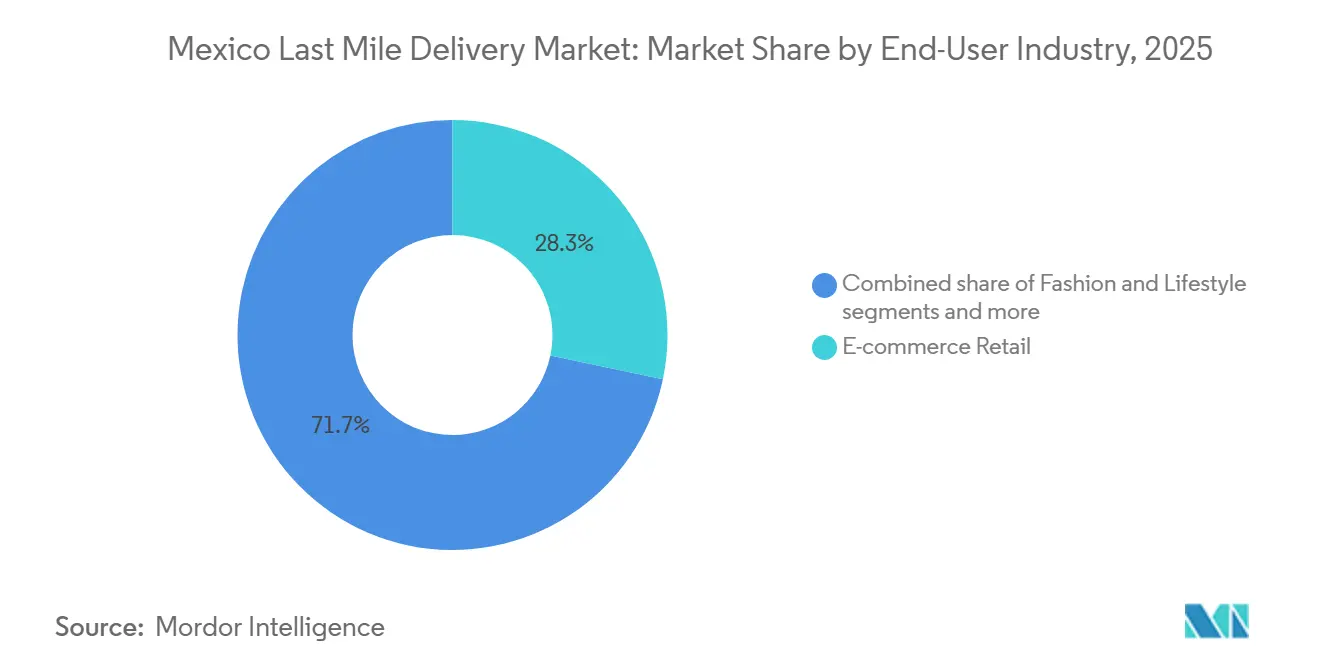

- By end-user industry, E-commerce Retail held a 28.30% share of the Mexico last-mile delivery market size in 2025, while Healthcare and Medical Supplies are expected to record a robust 12.23% CAGR through 2026-2031.

- By region, Central Mexico captured a 37.45% share in 2025, and North Mexico is projected to deliver the fastest growth with an 11.21% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Mexico Last Mile Delivery Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Middle-Class Purchasing Power Expanding Addressable Customer Base | +3.0% | National, with early gains in Mexico City, Monterrey, Guadalajara | Medium term (2-4 years) |

| USMCA Trade Facilitation Driving Parcel Volumes from US Cross-Border Fulfillment Centers | +2.4% | North Mexico (Nuevo León, Baja California), spill-over to Bajío | Long term (≥ 4 years) |

| High Mobile and Smartphone Penetration Enabling App-Based Delivery Tracking and Notifications | +2.2% | Mexico, highest adoption in urban centers | Short term (≤ 2 years) |

| Cold Chain Last-Mile Buildout for Online Grocery and Pharmaceutical Deliveries | +1.6% | Central Mexico, expanding to West and North hubs | Medium term (2-4 years) |

| Gig Economy Labor Pool Providing Flexible, Scalable Delivery Workforce | +1.9% | National, with concentration in metropolitan areas | Short term (≤ 2 years) |

| Parcel Locker and Pickup Point Networks Reducing Failed Delivery Costs | +1.3% | Urban Mexico, pilot expansion in semi-urban zones | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Middle-Class Purchasing Power Expanding Addressable Customer Base

Rising incomes and financial inclusion are expanding online consumers who value reliable delivery options in major metros. Increased purchasing power boosts order frequency, improving route density and delivery productivity in the Mexico last-mile delivery market. Higher demand for speed in urban areas supports premium services with shorter delivery windows. Mobile internet access bridges discovery and checkout gaps, linking purchasing power with fulfillment execution. New warehouses near industrial and residential zones enable carriers to meet demand with localized capacity and shorter linehauls, fostering scale economies and service-tier growth in the market.

USMCA Trade Facilitation Driving Parcel Volumes from US Cross-Border Fulfillment Centers

Deeper U.S.–Mexico supply-chain integration under USMCA strengthens cross-border e-commerce and B2B parcel flows, supporting just-in-time replenishment and returns management. USMCA simplifies compliance for express operators and encourages investment in warehousing and transport links, shortening order cycles in northern industrial corridors.[1]International Trade Administration, “Mexico Customs Law Reform,” U.S. Department of Commerce, trade.gov These corridors stage consumer and small-business parcels near U.S. markets and consolidated trucking lanes. Densified lanes improve outbound and reverse flows, enhancing pricing discipline and asset utilization in Mexico's last-mile delivery market. Stronger cross-border operations also enable specialized services for regulated categories, raising standards for speed, visibility, and domestic last-mile services.

High Mobile and Smartphone Penetration Enabling App-Based Delivery Tracking and Notifications

Smartphones are the primary internet access device in Mexico, making delivery notifications and tracking central to the post-purchase experience. Mobile adoption enables order-status alerts, flexible scheduling, and address validation, reducing failed deliveries and boosting repeat purchases. Platforms and carriers optimize mobile flows for low-bandwidth users and offer light data usage options. As digital payments grow, smartphone-native checkout and delivery orchestration streamline order creation to final handoff, improving lead times and first-attempt success.

Gig Economy Labor Pool Providing Flexible, Scalable Delivery Workforce

App-based work provides delivery platforms with a flexible labor pool to meet peak demand and adjust by zone. Many workers value flexibility and supplemental income, aligning with last-mile demand variability in Mexico.[2]United Nations Development Programme, “New Opportunities or Precarious Prosperity? The Two Faces of the Gig Economy in Latin America,” UNDP, undp.orgGig drivers enable services like same-day delivery without the fixed costs of permanent fleets. Platforms enhance retention and productivity through safety measures, financial tools, and route optimization. As payment systems improve, faster earnings and financial services boost workforce participation, supporting rapid service expansion while maintaining cost efficiency.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Peso Volatility and Fuel Price Fluctuations Increasing Operating Cost Unpredictability | -1.3% | National, acute in fuel-dependent long-haul routes | Short term (≤ 2 years) |

| Limited Urban Warehousing and Sortation Center Capacity Constraining Network Density | -1.1% | Central and North Mexico metro clusters | Medium term (2-4 years) |

| Persistent Cash-On-Delivery Preference Complicating Reconciliation and Working Capital | -0.8% | National, highest in rural and lower-income urban zones | Long term (≥ 4 years) |

| Inconsistent Regulatory Frameworks Across States Creating Compliance Complexity | -0.7% | National, with border states experiencing heightened customs scrutiny | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Peso Volatility and Fuel Price Fluctuations Increasing Operating Cost Unpredictability

Fuel expense and currency swings add uncertainty to unit economics for operators that lack hedging or fleet electrification pathways. Rapid input-cost changes are difficult to pass through in real time without harming customer retention, which compresses margins during price spikes. Larger incumbents that can deploy lower-emission vehicles and consolidate procurement enjoy relative insulation, which widens the gap with smaller carriers during volatile periods. Exchange-rate movements also affect imported equipment and parts, which can delay fleet renewal and facility upgrades in the Mexico last-mile delivery market. Operators that rely on independent contractors face a second-order effect when fuel costs reduce driver availability and route acceptance. Sustained cost-management discipline and diversified service tiers are needed to keep service reliability intact while maintaining competitiveness.

Limited Urban Warehousing and Sortation Center Capacity Constraining Network Density

High occupancy and land scarcity in key metros hinder adding high-grade sortation and cross-dock capacity within urban rings. Peripheral locations increase travel times and variability, weakening same-day and narrow-window services. Global players are adding multi-customer capacity near manufacturing and consumption hubs to enable denser delivery zones and faster cycles. Warehouse automation can boost throughput, though talent and power availability may delay urban deployments. A mix of micro-fulfillment nodes and larger hubs will balance proximity with economies of scale in the Mexico last-mile delivery market. The pace of zoned site development will impact service levels in fast-growth districts.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service: Same-Day Surge Challenges Standard's Volume Lead

Standard Delivery led the service mix with a 53.45% share in 2025, while Same-Day is projected to grow at a 12.45% CAGR from 2026-2031, driven by micro-fulfillment and tighter dispatch cycles in major metros. Express Delivery serves time-sensitive B2B replenishment and high-value consumer categories with predictable next-day service. The Mexico last-mile delivery market is segmenting by urgency, with value-conscious customers favoring Standard and time-sensitive purchases opting for premium tiers. Urban density, route optimization, and proximity to cross-docks are increasing throughput and enabling broader same-day coverage. Platforms and incumbents are refining zone designs to improve first-attempt success and support late cutoffs without compromising reliability.

Same-Day’s growth reflects mobile-driven behaviors and willingness to pay for speed in high-frequency categories like essentials and personal care. Standard Delivery remains key for larger baskets and diffuse routes where consolidation keeps costs low. Express Delivery supports ready-to-install appliances and just-in-time manufacturing, prioritizing reliability over speed. Operators are testing out-of-home drop density to boost Standard productivity and preserve premium capacity for Same-Day during peaks. Investments in sortation accuracy and address verification limit reattempts, protecting margins. As coverage and automation expand, Same-Day’s 12.45% CAGR is expected to narrow the gap with Standard while maintaining specialization.

By Business Model: B2C Dominance Anchored in Mobile-First Commerce

B2C held 61.12% of the Mexico last-mile delivery market share in 2025 and is expected to grow at a 12.67% CAGR, driven by smartphone shopping and embedded delivery options. Omnichannel adoption by retailers using stores as fulfillment hubs boosts B2C growth. B2B focuses on high-value shipments with time-certain windows for industrial and healthcare customers. C2C, though smaller, grows through tools simplifying prepaid labels, pickups, and returns. Expanding digital wallets and alternative payments improve B2C conversion in underbanked segments, reinforcing its market leadership.

B2C’s dominance reflects how user experience and logistics transparency drive repeat orders. Mobile tracking and flexible windows encourage premium tier adoption for urgent or high-value orders. B2B relies on service guarantees and specialized handling, supporting premium pricing for sensitive categories. C2C adds parcels but requires trust-building features like verified addresses and simplified claims. As platforms and carriers integrate further, B2C will extend its lead, while B2B focuses on reliability-first niches. C2C is expected to remain a complementary flow rather than a core network driver in the Mexico last-mile delivery market.

By End-User Industry: Healthcare’s Cold-Chain Imperative Disrupts E-Commerce Retail Inertia

E-commerce Retail held a 28.30% share in 2025, driven by electronics, fashion, and general merchandise aligned with rapid delivery in large metros. Healthcare and Medical Supplies is the fastest-growing segment due to temperature-sensitive handling and documented custody, supporting higher pricing. Fashion and Lifestyle add frequent orders and return flows requiring bidirectional planning. Beauty and Personal Care leverage predictable replenishment to boost route density. Home, furniture, and Consumer Electronics generate larger-ticket deliveries needing scheduled windows and special handling. These segments sustain utilization across zones in the Mexico last-mile delivery market.

Healthcare growth is driven by precision, traceability, and validated temperature control under certified frameworks. Packaging innovation extending cold-life without powered refrigeration lowers barriers for mid-tier operators. E-commerce Retail’s scale pressures service standards and returns management, intensifying cost control needs. Fashion and Lifestyle require effective reverse logistics and out-of-home paths for convenience. Electronics and large home goods favor scheduled windows to improve handoffs and reduce reattempts. Carriers are tuning services and capacity to match category seasonality and handling needs in the Mexico last-mile delivery industry.

Geography Analysis

Central Mexico’s 37.45% share in 2025 anchors network planning, with dense metro demand and mature fulfillment nodes supporting short-haul cycles and high-capacity cross-docks. New warehousing near Querétaro strengthens the Bajío corridor, improving access to highways and air links for faster dispatch. Mobile-first behavior sustains adoption of real-time tracking, flexible delivery windows, and out-of-home options to reduce reattempts.

North Mexico is forecast to lead regional growth with an 11.21% CAGR from 2026 to 2031, driven by cross-border integration and industrial hub expansion. Predictable lanes enable premium offerings and consistent reverse logistics. Operators now meet federal traceability and risk analysis obligations, enhancing compliance and operational readiness for peak cycles.

West, East, and South regions diversify the network with port-linked staging, inland distribution, and pickup-first designs. West Mexico’s ports support transload strategies for smoother imports. East Mexico balances industrial clusters with urban-to-rural connectivity, increasing the value of lockers and pickup points. South Mexico grows with store-based cash alternatives and digital wallets, improving last-mile conversion. Across regions, market dynamics depend on capacity placement, payment integration, and partner coordination with upstream fulfillment.

Competitive Landscape

The Mexico last-mile delivery market includes platform-integrated networks, global integrators, and regional specialists competing on speed, coverage, and cost. Global players are expanding vehicles, service points, and specialized handling to serve life sciences, e-commerce, and small-business flows with higher reliability and compliance.[3]DHL Group, “Capital Markets Day 2025,” DHL Group, group.dhl.com Multi-customer warehousing in strategic corridors aligns storage and sortation with consumption and manufacturing hotspots. Payment innovations and pickup partnerships are key to conversion and first-attempt success.

Top-tier operators are investing in automation, documentation systems, and compliance integration to meet traceability obligations introduced in 2026. These capabilities favor operators with robust IT systems and workflows that reduce inspection risks and delays. Carriers are extending cold-chain readiness to serve healthcare volumes requiring validated packaging and certified handling, supporting premium pricing. Network optimizations combining out-of-home delivery density with refined mobile flows improve on-time performance.

Market concentration is moderate, with platform-integrated networks and global logistics providers playing key roles, while regional specialists fill density gaps and deliver tailored services. Compliance and technology investments may drive deeper partnerships and selective consolidation. Premium tiers will rely on SLAs, certified handling, and traceability for growth. Operators embedding payment flexibility and pickup-point access into shopper journeys will gain an edge in conversion and delivery success. Leading players hold a significant share of capacity, with investments shaping service level convergence in the market.

Mexico Last Mile Delivery Industry Leaders

DHL Group

FedEx Corporation

United Parcel Service (UPS)

Paquetexpress

Mercado Libre (Mercado Envíos)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Mexico's Customs Law Reform requires courier and parcel operators to implement real-time risk-analysis systems, retain transaction documentation, and comply with stricter Carta Porte digital waybills for domestic goods movement.

- December 2025: DP World opened a 117,000-square-foot warehouse in La Bomba Industrial Park, El Marqués, Querétaro, near Highway 57 and Querétaro Intercontinental Airport to support nearshoring manufacturers in North America.

Mexico Last Mile Delivery Market Report Scope

Last-mile delivery refers to the final step of the logistics process, wherein a parcel is transported from a distribution hub to its ultimate destination.

Mexico last mile delivery market is segmented by Service (Standard Delivery, Same-Day, and Express Delivery), by Business Model (B2B, B2C, and C2C), by End-User Industry (E-commerce Retail, Fashion & Lifestyle, Beauty, Wellness & Personal Care, Home & Furniture, Consumer Electronics & Appliances, Healthcare & Medical Supplies, and Others), and Geography (North, Central, West, East, and South). The report offers market size and forecasts in values (USD) for all the above segments.

| Standard Delivery |

| Same-day |

| Express Delivery |

| Business-to-Business (B2B) |

| Business-to-Consumer (B2C) |

| Customer-to-Consumer (C2C) |

| E-commerce Retail |

| Fashion & Lifestyle |

| Beauty, Wellness & Personal Care |

| Home & Furniture |

| Consumer Electronics & Appliances |

| Healthcare & Medical Supplies |

| Others |

| North |

| Central |

| West |

| East |

| South |

| By Service | Standard Delivery |

| Same-day | |

| Express Delivery | |

| By Business Model | Business-to-Business (B2B) |

| Business-to-Consumer (B2C) | |

| Customer-to-Consumer (C2C) | |

| By End-user Industry | E-commerce Retail |

| Fashion & Lifestyle | |

| Beauty, Wellness & Personal Care | |

| Home & Furniture | |

| Consumer Electronics & Appliances | |

| Healthcare & Medical Supplies | |

| Others | |

| By Region (Mexico) | North |

| Central | |

| West | |

| East | |

| South |

Key Questions Answered in the Report

What is the current size and growth outlook for the Mexico last mile delivery market?

The Mexico last mile delivery market size was USD 15.72 billion in 2025 and is expected to reach USD 30.32 billion by 2031 at an 11.43% CAGR over 2026-2031

Which service types are leading and growing fastest in Mexico’s last mile context?

Standard Delivery led with 53.45% share in 2025, while Same-Day is projected to grow fastest at a 12.45% CAGR through 2031

How do payments and mobile usage influence last mile performance in Mexico?

Widespread smartphone access supports real-time tracking and flexible handoffs, while digital wallets and store-based cash alternatives reduce friction and improve first-attempt success

What regulatory changes are shaping last mile operations in 2026?

The 2026 Customs Law Reform requires real-time risk analysis systems and enhanced shipment data practices, favoring operators with strong IT and documentation capabilities

Which regions show the strongest momentum within Mexico?

Central Mexico holds the largest share, while North Mexico is forecast to post the fastest CAGR through 2031 due to cross-border integration and industrial growth

What strategies are market leaders using to compete in Mexico’s last mile space?

Leaders are expanding multi-customer warehousing, enhancing compliance and traceability systems, integrating payment options, and upgrading specialized handling for life sciences and temperature-controlled flows

Page last updated on: