Mexico Customs Brokerage Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

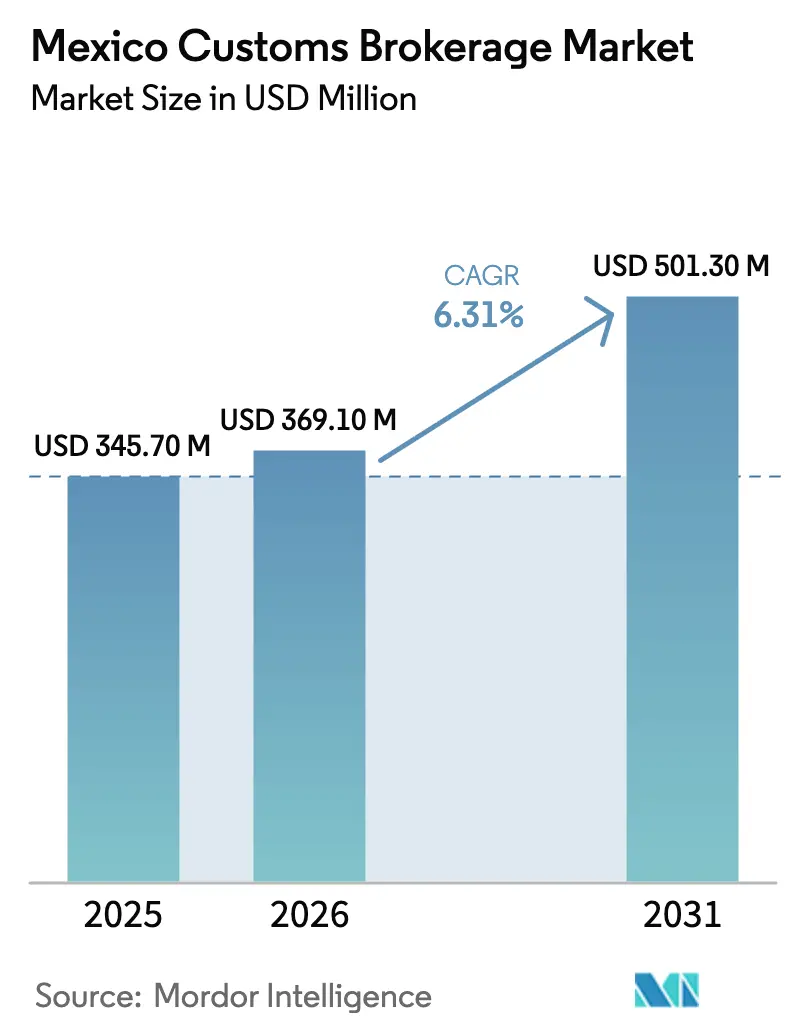

| Base Year Market Size (2025) | USD 345.70 Million |

| Market Size (2026) | USD 369.10 Million |

| Market Size (2031) | USD 501.30 Million |

| Growth Rate (2026 - 2031) | 6.31% CAGR |

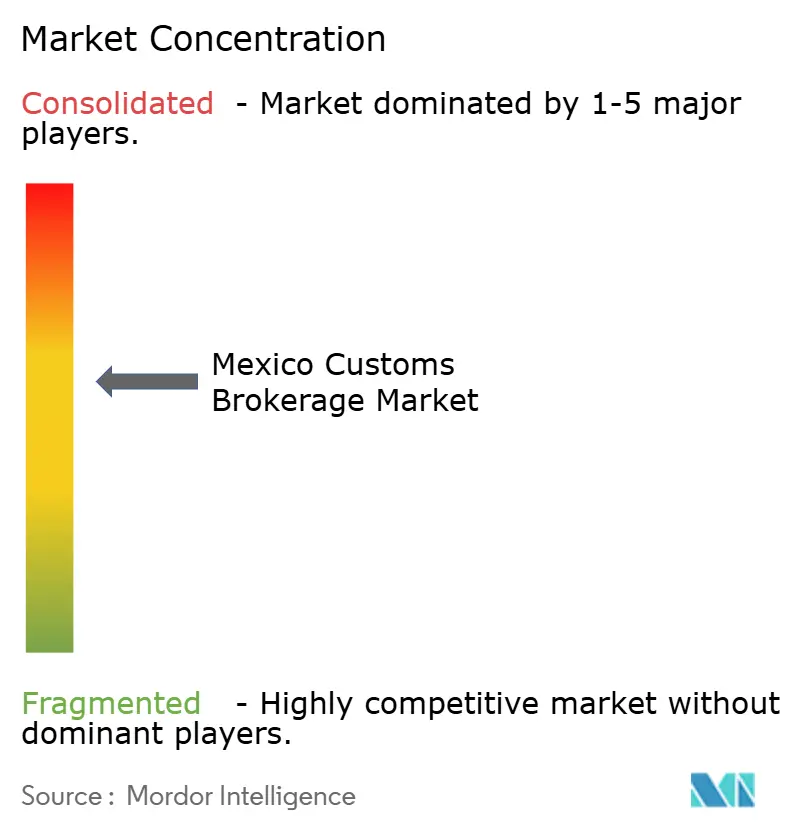

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Mexico Customs Brokerage Market Analysis by Mordor Intelligence

The Mexico Customs Brokerage Market size is expected to increase from USD 345.70 million in 2025 to USD 369.10 million in 2026 and reach USD 501.30 million by 2031, growing at a CAGR of 6.31% over 2026-2031.

Structural shifts in North American trade are shaping demand, as firms redesign supply chains under USMCA rules and deepen nearshoring commitments in Mexico’s manufacturing corridors. Rising customs digitalization, including mandatory electronic value manifest submissions, is changing how declarations are prepared and audited in 2026. Clearance complexity is increasing around valuation accuracy, rules-of-origin dossiers, and non-tariff compliance for sensitive goods that move through high-volume land ports and key maritime gateways. Sustained bilateral trade growth with the United States keeps transaction volumes on an upward path while policy predictability around USMCA’s 2026 review anchors planning cycles for exporters and brokers. These forces collectively define how the Mexican customs brokerage market evolves across volumes, service models, and technology investments in the current cycle.

Key Report Takeaways

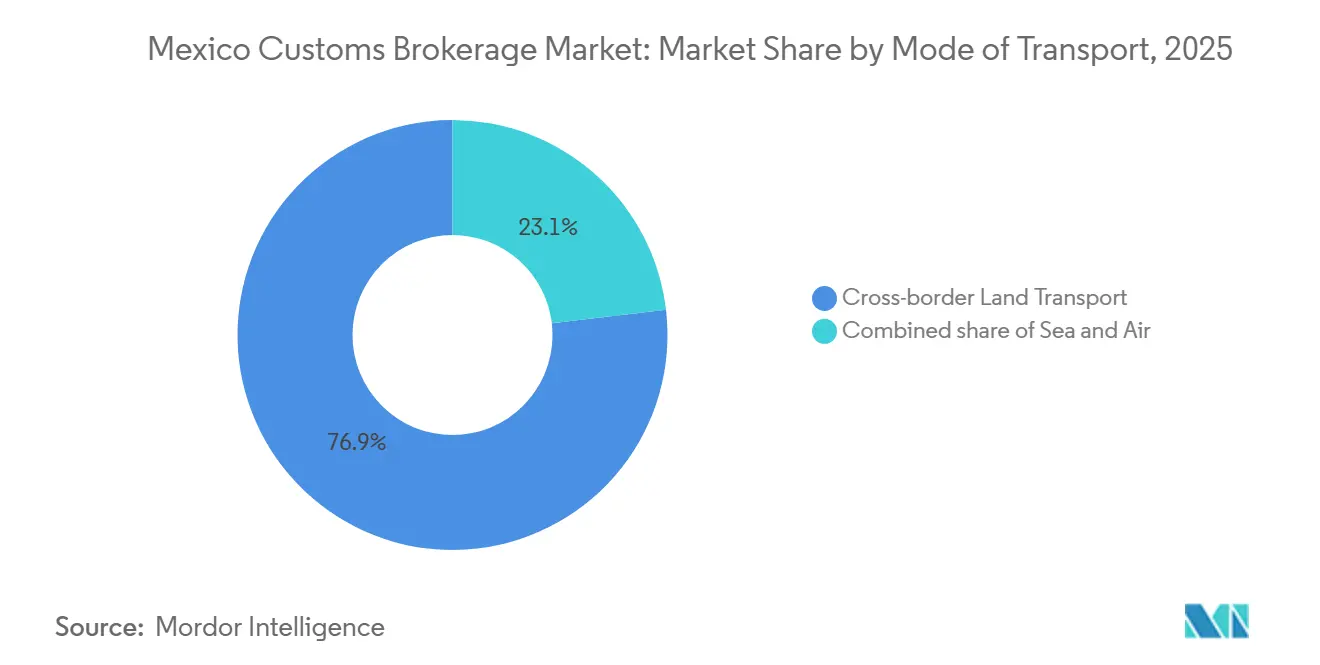

- By mode of transport, cross-border land transport led with 76.87% of Mexico customs brokerage market share in 2025, while air freight is forecast to post the fastest growth at 7.34% CAGR through 2026-2031.

- By end-user industry, manufacturing and automotive accounted for 54.23% of the Mexico customs brokerage market size in 2025, while consumer goods and retail are the fastest growing at a 7.86% CAGR through 2026-2031.

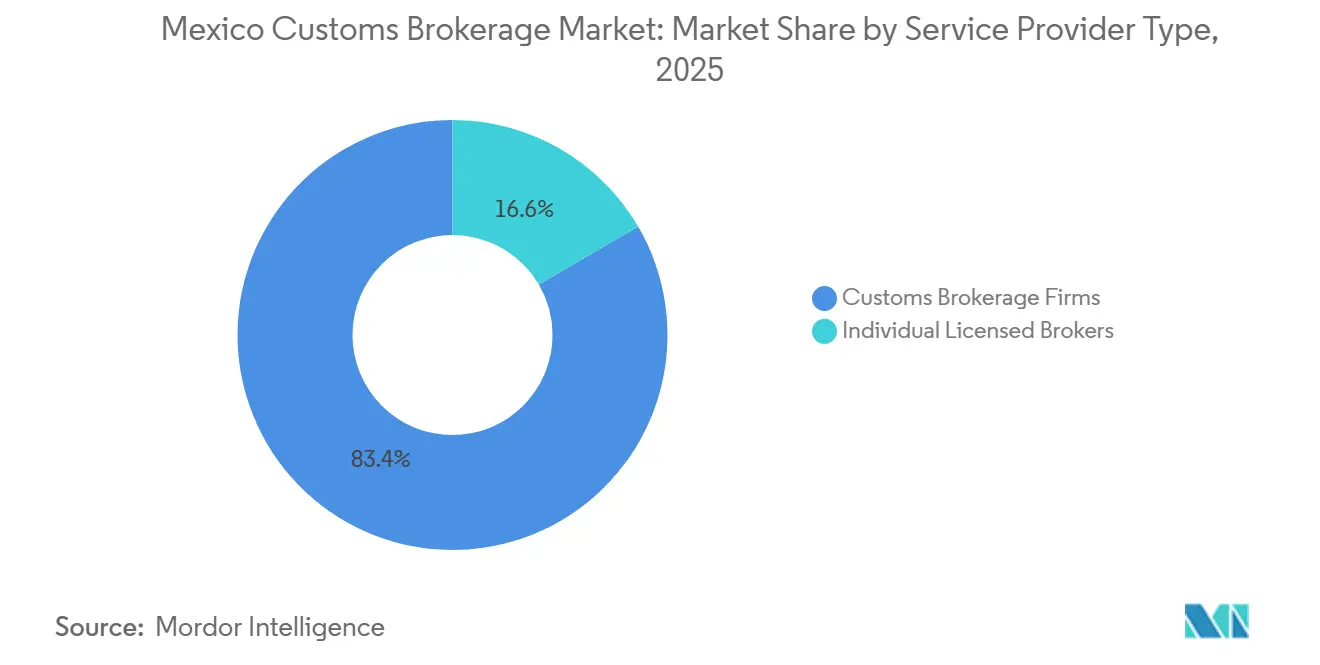

- By service provider type, customs brokerage firms held 83.41% of the Mexico customs brokerage market size in 2025 and are projected to expand at a 6.87% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Mexico Customs Brokerage Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| USMCA Trade Agreement Implementation | +1.2% | Global, with primary concentration in the United States-Mexico trade corridor (Nuevo León, Chihuahua, Tamaulipas) | Medium term (2-4 years) |

| Nearshoring and Reshoring Trends | +1.8% | Nuevo León, Guanajuato, Querétaro, San Luis Potosí, spill-over to Jalisco and the State of México | Medium term (2-4 years) |

| E-commerce and Cross-Border Parcel Growth | +0.9% | Mexico City, Monterrey metropolitan areas, and rising penetration in Guadalajara and border cities | Short term (≤ 2 years) |

| Automotive Industry Expansion | +1.1% | Central Mexico automotive corridor (Guanajuato, Aguascalientes, San Luis Potosí), Northern tier (Coahuila, Nuevo León) | Medium term (2-4 years) |

| Digital Customs Modernization Initiatives | +0.7% | National, with early implementation in major customs offices (Mexico City, Nuevo Laredo, Manzanillo) | Short term (≤ 2 years) |

| Foreign Direct Investment Inflows | +1.5% | National, especially industrial corridors in Nuevo León, Querétaro, State of México | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

USMCA Trade Agreement Implementation Accelerates Cross-Border Clearance Volumes

USMCA implementation is reshaping trade operations across North America and lifting customs-brokerage workloads along Mexico’s land borders and maritime gateways. The share of Mexican exports that applied USMCA preferences rose from 44.8% in early 2024 to 88.7% by late 2025, showing how preferential tariff treatment now guides clearance strategy and documentation sequencing for manufacturers that have reconfigured sourcing and production footprints under the agreement. Mexico’s exports to the United States reached USD 534.9 billion in 2025, equal to 15.7% of total United States imports, which placed Mexico ahead of both Canada and China for the year.[1]U.S. Census Bureau, “Trade Data on U.S. Goods Imports by Country,” U.S. Census Bureau, census.gov USMCA’s rules of origin require granular proof of regional content and labor value content for sensitive sectors, which increases the documentation duty for brokers that must assemble supplier certificates and keep comprehensive electronic files in compliance with Mexico’s updated customs law. The first USMCA review will occur on July 1, 2026, which keeps attention on potential rule updates while the agreement’s core framework continues to underpin nearshoring and trade flows in 2026.[2]U.S. Trade Representative, “USMCA Six-Year Review Timeline,” Office of the USTR, ustr.gov Land crossings remain central to this intensity, with Laredo alone handling USD 19.6 billion in November 2025, a level that concentrates high-value clearances where speed and documentation accuracy are closely monitored.

Nearshoring and Reshoring Trends Drive Industrial-Park Buildouts and Recurrent Clearance Activity

Mexico recorded USD 40.871 billion in foreign direct investment in 2025, which marked a fifth consecutive annual gain and reinforced the country’s role within North American production networks.[3]Secretaría de Economía, “Inversión Extranjera Directa 2025,” Government of Mexico, gob.mx New greenfield commitments rose to USD 7.38 billion, with a concentration in industrial assets that support automotive batteries, precision machining, and factory expansions that require continuous importation of equipment and inputs under temporary and definitive regimes. The United States was the largest investor, underscoring a deeper regional realignment that relies on quick border turns and predictable customs processing cycles tied to high-frequency trucking lanes. The composition of inflows, including a large share of reinvested earnings among established operators, signals that production nodes across Mexico are gaining scale and will generate steady declaration volumes for brokers in 2026. These inputs create recurrent paperwork around valuation, classification, and origin certification as more assembly nodes enhance in-house compliance while partnering with brokers to ensure traceable and audit-ready submissions that meet Mexico’s electronic-file requirements under the new law.

E-commerce and Cross-Border Parcel Growth Demands Expedited Clearance Under Simplified Procedures

Mexico’s e-commerce value increased by 19.2% in 2025 and reached 941 billion pesos, supported by 77.2 million digital buyers whose orders convert into high-frequency, small-parcel flows that pass through courier networks and simplified clearance profiles. The rising transaction count requires faster data capture, clean declarations, and precise valuation for consignments that arrive in tight windows and often require pre-clearance data transmission. As of April 1, 2026, the Electronic Value Manifest is mandatory through VUCEM, which moves more valuation elements into structured electronic fields that importers or their authorized brokers must complete before clearance. The manifest includes declared commercial value, valuation method, and supporting information such as freight and insurance, which reduces ambiguity and supports upstream risk analysis by customs in high-volume parcel channels. New 2026 requirements for courier and express-delivery authorization include risk systems with real-time customs access and documentation retention, which raises the operational baseline for expedited providers that serve cross-border retail and electronics flows.

Automotive Industry Expansion Generates Precision-Component Imports and EV-Supply-Chain Complexity

Mexico produced 3.95 million vehicles in 2025 and exported 87% of that output, with the United States as the primary destination, which reinforces the role of Mexico’s assembly hubs as anchors of high-volume customs activity. Auto parts supply chains involve frequent inbound shipments of precision components that must meet USMCA origin documentation, which increases the broker’s responsibilities for certificate validation and for maintaining an electronic trail that aligns with 2026 requirements. The shift toward electrified models elevates the documentation and permit profile for parts and materials such as lithium-ion batteries, power semiconductors, and thermal-management systems, which must satisfy additional non-tariff controls during clearance. As suppliers expand capacity in the central and northern corridors, the Mexican customs brokerage market needs specialized classification expertise and transparent valuation documentation to avoid under-declaration risk in parts with volatile pricing and dual-use scrutiny. High-value, time-sensitive electronics and modules that feed auto assembly programs also support a gradual shift toward more airfreight clearances where brokers manage tighter service windows and a higher level of document readiness at flight arrival.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory Uncertainty and Frequent Changes | -0.8% | National, heightened impact in manufacturing-intensive states such as Nuevo León, Guanajuato, and Coahuila | Short term (≤ 2 years) |

| Border Congestion and Delays | -0.6% | Primary land crossings such as Laredo, Ciudad Juárez, Tijuana, and the Manzanillo maritime gateway | Short term (≤ 2 years) |

| Technology Investment Requirements | -1.0% | National, especially for small-to-midsize customs agencies with limited capital reserves | Medium term (2-4 years) |

| Licensed Broker Shortage | -0.7% | National, with acute gaps in high-growth corridors such as Monterrey, Querétaro, and the Bajío | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Regulatory Uncertainty and Frequent Changes Elevate Compliance Costs and Legal Exposure

Mexico’s revised customs law is in force as of January 1, 2026, and introduces joint and several liability for brokers and importers, which intensifies exposure on valuation accuracy, tariff classification, and compliance with non-tariff measures. Penalties can reach 250% to 300% of the goods’ commercial value for issues such as undervaluation or misclassification, which raises the financial stakes for agencies and clients when documentation is incomplete or inconsistent. Broker licenses now have a 20-year validity and require recertification every three years, while a new Customs Council with tax and customs authorities oversees license issuance, suspension, or cancellation based on ongoing compliance. The law mandates robust electronic files for each client, including proof of operational infrastructure, sworn statements, and checks that clients are not listed under Article 69-B of the Federal Tax Code, which demands stricter onboarding and continuing diligence. USMCA’s July 1, 2026, review also keeps businesses attentive to potential rule refinements, which adds planning uncertainty for long-lead procurement and capital programs that intersect with customs rules.

Technology Investment Requirements Strain Capital Reserves of Small-to-Midsize Agencies

The Electronic Value Manifest requirement through VUCEM took effect on April 1, 2026, and requires e.firma credentials, compliant data-capture systems, and document-attachment standards that compel investment in document management and secure transmission. Regulatory updates in early 2026 require agencies to implement internal control procedures for foreign trade data and to enable interoperability with the Customs Electronic System for remote verification by authorities, which raises the IT and process-management baseline across the ecosystem. Inventory-control and real-time monitoring mandates for certain bonded operations increase the demand for systems integration, cybersecurity, and audit logs that smaller agencies must finance without dedicated technology budgets. The net effect is a higher fixed-cost profile to participate in the Mexico customs brokerage market, which encourages consolidation strategies among firms that seek to spread these costs over larger transaction volumes. Industry associations have noted that excessive complexity can undermine nearshoring attractiveness if not balanced with predictable rules and stable implementation timelines, which keeps stakeholder dialogue active in 2026.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Mode of Transport: Land Crossings Dominate While Air Freight Gains on Time-Sensitive Electronics

Land transport held 76.87% of Mexico's customs brokerage market share in 2025, an outcome that reflects the depth of Mexico–United States trucking lanes and the heavy concentration of bilateral trade moving through primary crossings such as Laredo, which processed USD 19.6 billion in November 2025. USMCA encourages regionalized sourcing and assembly, which supports routing through road corridors where shippers can synchronize plant-to-border cycle times with customs pre-documentation and inspection slotting. Maritime gateways continue to serve containerized flows from Asia and outbound shipments to third markets, while operational reliability at ports remains a point of focus for importers seeking to hedge against congestion risks. As manufacturing footprints expand in central Mexico, cross-dock networks and bonded facilities extend land-based efficiencies with integrated inventory-control and data capture that align with 2026 documentation mandates. These linkages support consistent declaration pipelines in the Mexico customs brokerage market as suppliers coordinate inbound components and outbound finished goods across predictable trucking timetables.

Air freight captured a low share in 2025 but is projected to grow at a 7.34% CAGR through 2031 as semiconductors, medical devices, and high-value electronics move on to tighter delivery expectations. Electronics shipments tied to the United States demand for electrical and electronic products are becoming a larger source of brokerage workload at airports, which calls for precise valuation documentation and quick origin-verification steps that meet USMCA thresholds. Brokers that invest in air-specific workflows, including data readiness at flight arrival and concierge resolution of data holds, can capture incremental share at Mexico City and regional airports that support fast-moving production schedules. Sea and rail remain important in trade with third markets and for bulk or heavy equipment, though their clearance profiles are steadier and less time critical than the high-touch air consignments. As land retains its lead and air accelerates, the mix shift supports higher-value service lines in the Mexico customs brokerage market, where documentation precision and systems connectivity define performance.

By End-User Industry: Automotive Retains Leadership as Consumer Goods Accelerate on E-commerce Surge

Manufacturing and automotive accounted for 54.23% of brokerage revenue in 2025, a position built on Mexico’s auto production of 3.95 million units and an export ratio of 87% that anchors cross-border parts and finished-vehicle flows. Assembly and tiered suppliers depend on recurrent importations of subassemblies, electronics, and metals, each of which requires correct tariff classification, valuation methods aligned with customs criteria, and comprehensive origin files in 2026. The evolution toward electrified platforms adds regulatory and documentation layers for batteries and power electronics, which increases reliance on brokers that can coordinate permits and confirm compliance with non-tariff measures for sensitive materials. These dynamics reinforce the central role of automotive within the Mexican customs brokerage market as suppliers broaden capacity in the northern and central corridors.

Consumer goods and retail are the fastest-growing end-user segments with a 7.86% CAGR, supported by e-commerce value growth of 19.2% in 2025 and a digital-buyer base of 77.2 million that drives frequent, small-parcel cross-border flows. The new manifest requirement in 2026 moves valuation fields into structured submissions and strengthens risk screening, which places higher expectations on brokers and express operators that serve this segment. Electronics and high-tech products also contribute to rising declaration counts, given Mexico’s strong role in the United States electrical and electronics sourcing that benefits from agile cross-border programs and precise documentation at the point of entry. Healthcare, chemicals, and agri-food maintain steady shares that require specialized sanitary, phytosanitary, and hazardous-material documentation, which keeps sector-specific brokerage expertise in demand within the Mexican customs brokerage market in 2026.

By Service Provider Type: Brokerage Firms Consolidate Market Share as Technology Mandates Favor Scale

Brokerage firms held 83.41% of the Mexico customs brokerage market size in 2025 and are projected to expand at a 6.87% CAGR through 2031 as 2026 regulatory and digital requirements raise baseline investment needs around systems, controls, and electronic recordkeeping. The law enforcers share joint responsibility for valuation and classification accuracy and mandate electronic files with documentary and photographic evidence for each client, which favors firms with stronger compliance infrastructure and dedicated IT teams. Individual brokers face a higher documentation and audit burden in 2026, including periodic recertification, and must either invest in technology or affiliate with larger entities to meet strict interoperability and verification standards. These changes push the Mexico customs brokerage market toward integrated models where brokers, warehousing, and transportation work from unified data and processes to reduce errors and accelerate release cycles.

Market participants with bilingual compliance teams and real-time visibility platforms are positioned to win share as shippers seek fewer handoffs and better control of end-to-end data. Cross-border specialists who update workflows to the 2026 profile, including manifest pre-submission and robust internal controls, provide tangible value in audit-readiness and dispute resolution. Firms that elevate training and codify best practices for valuation documentation can reduce penalty exposure for clients as enforcement tightens. These operating advantages underpin the growth outlook for scaled agencies in the Mexican customs brokerage market as technology, process discipline, and legal fluency become the primary differentiators in 2026.

Geography Analysis

Northern border states, including Nuevo León, Chihuahua, Tamaulipas, Coahuila, Baja California, and Sonora, account for a large share of land-clearance volumes due to proximity to the United States and the concentration of export-oriented manufacturing. Laredo functions as the most active commercial port of entry and processed USD 19.6 billion in November 2025, which reflects the concentration of high-value flows that depend on accurate, well-sequenced declarations to maintain cross-border rhythm. Border operations in cities such as Ciudad Juárez and Tijuana handle electronics, medical devices, and automotive components, and must manage periodic surges in inspections that extend crossing times and require contingency planning. The Mexico customs brokerage market in these corridors benefits from experienced brokers that can re-time entries and use pre-filed documentation to mitigate disruption.

Central Mexico, including Guanajuato, Querétaro, San Luis Potosí, Aguascalientes, and Jalisco, expanded its role in 2025 as a production base for automotive and high-value manufacturing, which increases inland declaration activity at bonded facilities and airports. Mexico City remains the primary air-cargo gateway where e-commerce and high-tech goods require rapid cycle times and clean valuation submissions under the 2026 manifest requirement. The Mexico customs brokerage market sees rising demand for providers that can coordinate inland clearances, link inventory systems to VUCEM workflows, and manage virtual transfers and temporary regimes for components that move between plants and cross-border lanes without friction. This inland concentration complements the northern border and creates a multi-node customs footprint that supports suppliers serving North American demand.

Maritime gateways on the Pacific and Gulf coasts handle containerized imports from Asia and outbound shipments to third markets and serve as alternatives when land ports face congestion. Brokers active in Manzanillo, Lázaro Cárdenas, Veracruz, and Altamira manage steady flows that require consistent classification and non-tariff compliance around time-sensitive or regulated goods. The Mexico customs brokerage market at seaports focuses on error-free documentation to prevent storage and demurrage risk, which keeps attention on pre-clearance accuracy and coordination with maritime agents. While land crossings retain the largest volume share, seaports add diversification for shippers that balance cost, service levels, and space availability over the planning horizon. This portfolio of gateways supports resilience in 2026 as nearshoring continues and USMCA sustains two-way flows that depend on efficient customs procedures.

Competitive Landscape

Innovation and Integration Drive Future Success

For established players to maintain and expand their market share, the focus must be on developing comprehensive digital solutions that integrate seamlessly with client systems while maintaining high compliance standards. Incumbent firms need to invest in specialized industry expertise, particularly in high-growth sectors like automotive, retail, and technology, while building robust risk management capabilities. The ability to offer value-added services beyond basic customs clearance, such as customs consulting and supply chain optimization, will become increasingly important for maintaining a competitive advantage in the evolving market landscape.

New entrants and smaller players can gain ground by focusing on niche industry segments or specific trade corridors where they can develop specialized expertise and superior service levels. Success factors include developing strong relationships with customs authorities, investing in modern technology platforms, and maintaining operational flexibility to adapt to changing market conditions. The relatively low threat of substitution from automated solutions and high customer loyalty to established providers creates a stable competitive environment, though regulatory changes and increasing digitalization of customs processes may reshape competitive dynamics in the longer term. The role of customs management in ensuring compliance and efficiency cannot be overstated, as it remains a critical component of successful operations.

Mexico Customs Brokerage Industry Leaders

Bollore Logistics Mexico

Tuscor Lloyds Mexico

Chapela Diaz

Montalvo y Montalvo S.C.

Global LogÃstica Aduanal S.C.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: WeShip Express relocated its headquarters to Austin, Texas, to scale compliance automation, temperature-controlled logistics, and e-commerce fulfillment capabilities that serve trade flows linked to Mexico’s fast-growing online retail segment.

- January 2026: Transport Capacity Services opened a new office in Monterrey, Mexico, to expand operational support for high-volume cross-border shipments and visibility for manufacturers navigating Mexico's 2026 customs enforcement profile.

- November 2025: On November 19, 2025, the Mexican Congress approved major Customs Law reforms, effective January 1, 2026. These changes end liability exemptions for customs brokers, making them jointly responsible with importers for valuation, tariff classification, and regulatory compliance. Fines for violations range from 250% to 300% of goods' value. Broker licenses, now limited to 20 years, require recertification every three years. A new Customs Council will oversee license issuance, suspension, and cancellation based on compliance.

- February 2025: Total Quality Logistics (TQL), North America's second-largest freight brokerage, has opened new offices in Laredo, Texas, and Monterrey, Mexico, to expand its Mexico Cross-Border services. The Laredo office partners with transloading facilities offering 200,000+ square feet of storage and 75+ dock doors to streamline freight and reduce customs delays. Since 2016, TQL has enhanced cross-border services, supporting nearshoring growth as Mexico becomes the U.S.'s top trading partner.

Mexico Customs Brokerage Market Report Scope

The customs brokerage market refers to the industry involved in facilitating the import and export of goods across international borders while ensuring compliance with the customs regulations and laws of the countries involved.

The Mexico Customs Brokerage Market Report is Segmented by Mode of Transport (Sea, Air, and Cross-Border Land Transport), by End-user Industry (Manufacturing and Automotive, Consumer Goods and Retail, High-Tech and Electronics, Healthcare and Pharmaceuticals, Chemicals and Petrochemicals, Agriculture and Food, and Others), by Service Provider Type (Customs Brokerage Firms, Individual Licensed Brokers), Forecasts are Provided in Terms of Value in USD.

| Sea |

| Air |

| Cross-border Land Transport |

| Manufacturing & Automotive |

| Consumer Goods & Retail |

| High-Tech & Electronics |

| Healthcare & Pharmaceuticals |

| Chemicals & Petrochemicals |

| Agriculture & Food |

| Others (Aerospace Components, Mining Equipment, etc) |

| Customs Brokerage Firms |

| Individual Licensed Brokers |

| By Mode of Transport | Sea |

| Air | |

| Cross-border Land Transport | |

| By End-User Industry | Manufacturing & Automotive |

| Consumer Goods & Retail | |

| High-Tech & Electronics | |

| Healthcare & Pharmaceuticals | |

| Chemicals & Petrochemicals | |

| Agriculture & Food | |

| Others (Aerospace Components, Mining Equipment, etc) | |

| By Service Provider Type | Customs Brokerage Firms |

| Individual Licensed Brokers |

Key Questions Answered in the Report

What is the current size and outlook of the Mexico customs brokerage market?

The Mexico customs brokerage market size was USD 345.7 million in 2025 and is forecast to reach USD 501.3 million by 2031 at a 6.31% CAGR over 2026-2031.

Which transport mode leads in the Mexico customs brokerage market, and which is growing fastest?

Cross-border land transport led with 76.87% share in 2025, while air freight is projected to record the fastest growth at 7.34% CAGR through 2031.

Which end-user segments are most important for customs-brokerage demand in Mexico?

Manufacturing and automotive represented 54.23% of revenue in 2025, while consumer goods and retail is the fastest growing at a 7.86% CAGR as e-commerce expands

How does USMCA affect customs-brokerage workflows in Mexico?

USMCA increases documentation around rules of origin and labor value content, which drives higher broker workload and stricter electronic files as the July 1, 2026 review approaches

What 2026 digital requirements change customs documentation in Mexico?

The Electronic Value Manifest through VUCEM is mandatory from April 1, 2026, requiring electronic submission of valuation and related data before clearance

Where are customs-clearance activities most concentrated geographically?

Northern border crossings such as Laredo handle high volumes, with Laredo processing USD 19.6 billion in November 2025, while Mexico City’s airport supports a growing share of time-sensitive shipments

Page last updated on: