Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Historical Data Period | 2020 - 2024 |

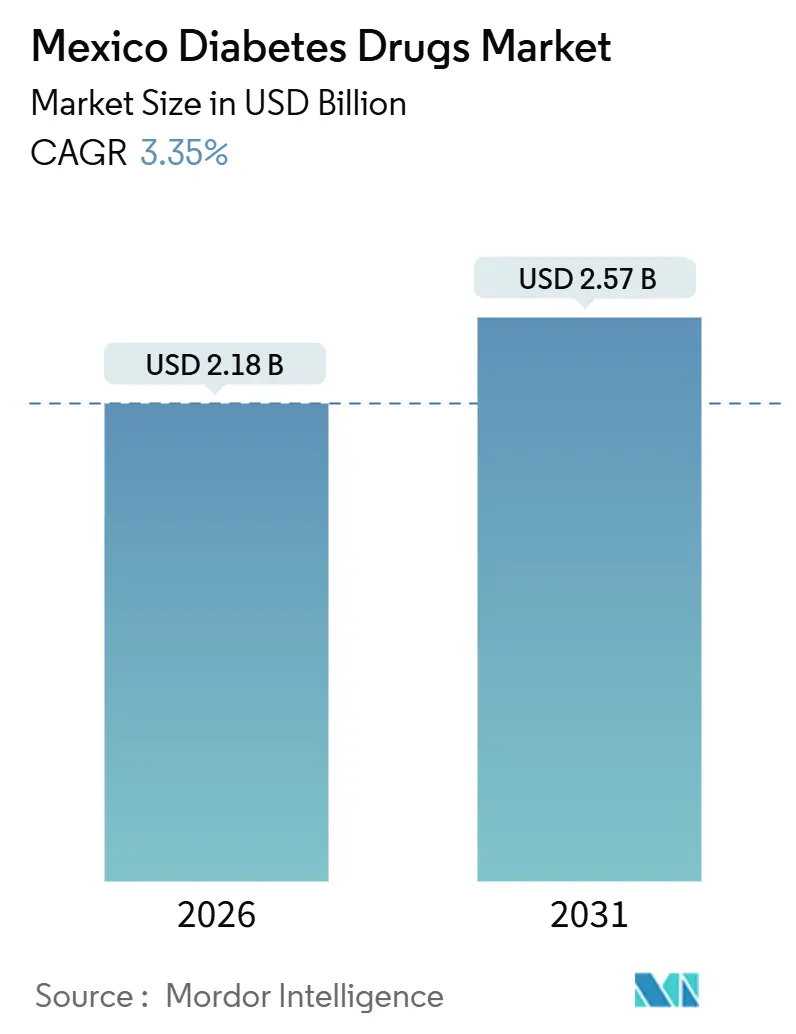

| Market Size (2026) | USD 2.18 Billion |

| Market Size (2031) | USD 2.57 Billion |

| Growth Rate (2026 - 2031) | 3.35% CAGR |

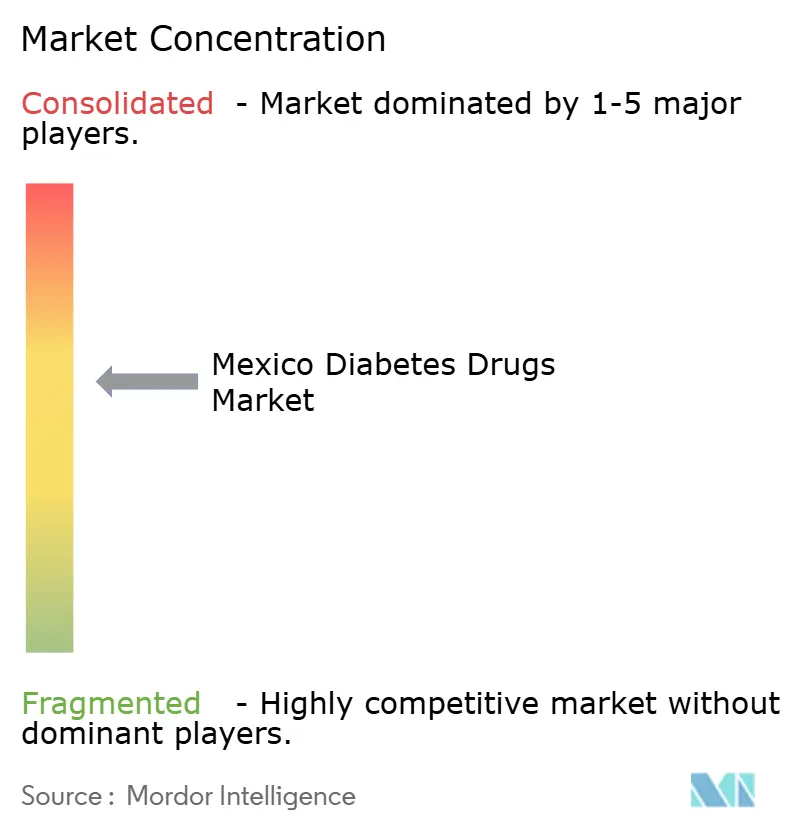

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Mexico Diabetes Drugs Market Analysis by Mordor Intelligence

The Mexico Diabetes Drugs Market size is estimated at USD 2.18 billion in 2026, and is expected to reach USD 2.57 billion by 2031, at a CAGR of 3.35% during the forecast period (2026-2031).

Persistent growth reflects the widening clinical burden, surging demand for modern therapies, and procurement policy reforms that favor price-competitive biosimilars. Adult diabetes prevalence climbed to 18.3% in 2024, while obesity reached 36.1%, broadening the treatment-eligible pool and driving steady prescriptions of metformin, basal insulin analogs, and GLP-1 receptor agonists. COFEPRIS approvals of three insulin glargine biosimilars between 2024 and 2025 accelerated tender savings, yet administrative delays under the new IMSS-led purchasing model caused intermittent stock-outs that redirected patients to higher-priced retail channels. Cardiovascular and renal outcome data for GLP-1 and SGLT-2 classes are also altering physician habits, with cardiologists and nephrologists issuing prescriptions that extend beyond glycemic control. Meanwhile, private insurers are broadening formularies for innovative drugs, creating premium niches that multinational firms are racing to serve.

Key Report Takeaways

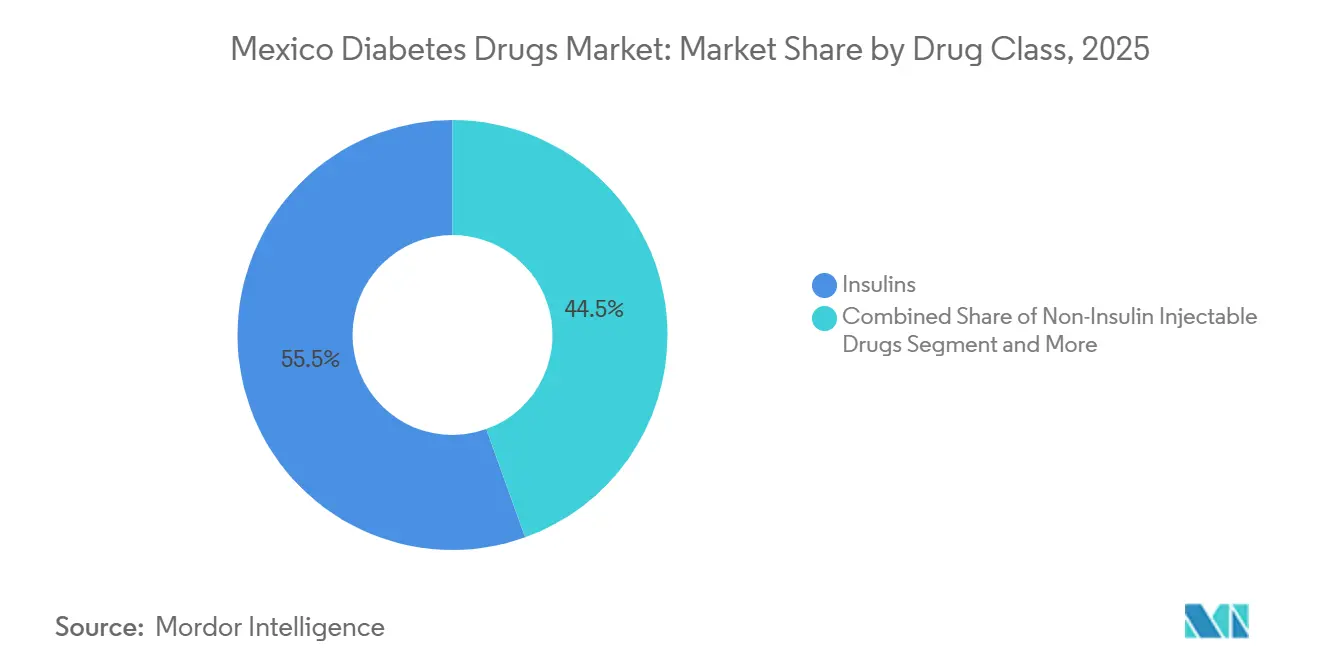

- By drug class, insulins led with 55.55% revenue share in 2025; non-insulin injectables are projected to expand at a 4.15% CAGR through 2031.

- By route of administration, subcutaneous formulations held 69.53% of the Mexico diabetes drugs market share in 2025, while oral therapies are set to grow at a 4.75% CAGR to 2031.

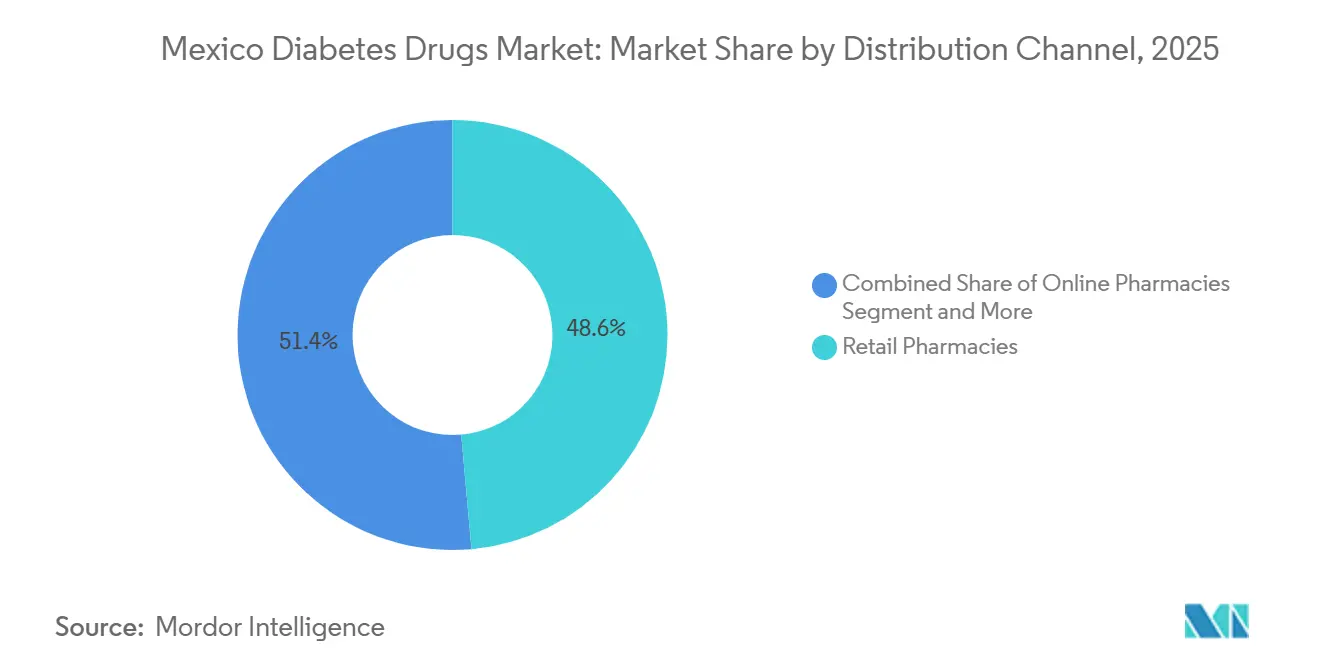

- By distribution channel, retail pharmacies commanded 48.63% of the Mexico diabetes drugs market size in 2025, whereas online pharmacies record the fastest projected CAGR at 5.87% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Mexico Diabetes Drugs Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising type-2 diabetes and obesity prevalence | +1.2% | Nationwide, strongest in northern states | Long term (≥ 4 years) |

| Government tender reforms expanding biosimilar insulin uptake | +0.8% | IMSS and ISSSTE beneficiary populations | Medium term (2-4 years) |

| GLP-1 adoption for dual diabetes-obesity and cardiovascular benefit | +0.9% | Large urban centers | Medium term (2-4 years) |

| Tele-prescription and e-pharmacy penetration in rural Mexico | +0.5% | Southern and central rural municipalities | Long term (≥ 4 years) |

| Growth of private insurance panels covering innovative therapies | +0.6% | Metropolitan labor markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Type-2 Diabetes and Obesity Prevalence

Mexico’s adult diabetes prevalence reached 18.3% in 2024 alongside obesity at 36.1%, trends most pronounced in northern border states where calorie-dense diets and sedentary lifestyles converge. The dual epidemic is adding roughly 400 000 new treatment-eligible adults each year, yet only 47% of diagnosed patients attain HbA1c below 7%. Lower control rates among adults aged 35–50 intensify demand for second-line injectables and propel volume growth across basal insulin and GLP-1 classes. Shortfalls in lifestyle change programs further entrench pharmacologic dependence, reinforcing steady expansion of the Mexico diabetes drugs market.

Government Tender Reforms Expanding Biosimilar Insulin Uptake

COFEPRIS cleared three insulin glargine biosimilars from 2024 to 2025, aligning with federal cost-containment mandates that emphasize interchangeable biologics. IMSS tenders in Q2 2025 assigned 38% of basal volume to biosimilars, creating MXN 420 million (USD 24 million) in annual savings[1]IMSS, “Informe de Compras y Licitaciones 2025,” imss.gob.mx. Clinics now juggle originator and biosimilar SKUs, stretching cold-chain capacity and raising counseling needs for safe switching. Price concessions from Biocon’s Basaglar undercut Lantus by 30-35% yet confusion over device differences occasionally triggers nocturnal hypoglycemia reports. Even with friction, biosimilars are cementing structurally lower procurement baselines, supporting mid-term CAGR uplift.

GLP-1 Adoption for Dual Diabetes-Obesity and CV Benefit

Cardiovascular-outcome trials reshaped GLP-1 positioning after liraglutide and dulaglutide showed 12-13% MACE reductions, prompting cardiologists to champion these agents for secondary prevention. COFEPRIS granted semaglutide a cardiovascular indication in March 2024, expanding clinical utility just as private insurers lift reimbursement ceilings[2]COFEPRIS, “Registro de Biosimilares 2025,” cofepris.gob.mx. Global supply shortages limited deliveries to 60% of distributor orders in early 2025, spawning gray-market arbitrage with markups near 40%. Even so, prescriber enthusiasm is lifting non-insulin injectable penetration and solidifying multispecialty uptake in the Mexico diabetes drugs market.

Tele-Prescription and E-Pharmacy Penetration into Rural Mexico

The December 2024 Digital Health Framework legalized electronic prescriptions for insulin and GLP-1 drugs. Partnerships between platforms such as Doctoralia and farmacias digitales expanded rural access, with Prixz posting a 210% jump in diabetes orders from towns under 50 000 residents in the year to Q1 2025. Delivery lead times average 48 hours, but only 34% of cold-chain shipments sustain 2-8 °C, risking insulin potency loss. Regulatory enforcement and investment in passive coolers will determine long-term penetration and thus incremental sales.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High price of innovative insulins and GLP-1 RAs limiting public reimbursement | -0.7% | National public institutions | Short term (≤ 2 years) |

| Supply-chain volatility and void tenders causing stock-outs | -0.5% | Rural and peri-urban clinics | Short term (≤ 2 years) |

| Illicit or counterfeit GLP-1 products via social media | -0.3% | Large cities with high social-media use | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Price of Innovative Insulins and GLP-1 RAs Limiting Public Reimbursement

Toujeo, Tresiba, Ozempic, and similar agents list at 4–6 times the cost of NPH insulin or metformin, straining IMSS and ISSSTE budgets that covered 12% of drug spend for GLP-1 agents in 2025. A 30-day supply of Ozempic costs MXN 3 200-4 500, about 40% of monthly minimum wage, leaving 85% of diabetics priced out when private insurance is absent[3]Secretaría de Salud, “Informe de Abasto de Medicamentos 2025,” salud.gob.mx. Physicians often fall back on sulfonylureas despite hypoglycemia risks, slowing the shift toward cardio-protective drugs integral to the Mexico diabetes drugs market.

Supply-Chain Volatility and Void Tenders Causing Stock-Outs

When UNOPS handed purchasing back to IMSS in 2024, bid qualification glitches triggered void tenders across 18% of insulin RFPs, leaving 23% of primary clinics without basal supply for over 30 days in Q1 2025. Long payment lags persuaded some incumbents to skip bids, shrinking competitive fields and exacerbating shortages, especially in rural areas where retail mark-ups reach 80%. Stock-outs distort prescribing behavior, erode adherence, and sharpen regional inequities.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Drug Class: Biosimilars Reshape Insulin Economics

Insulins accounted for 55.55% of 2025 revenue, propelled by basal analogs such as glargine and degludec that dominate IMSS and ISSSTE formularies. Non-insulin injectables, primarily GLP-1 receptor agonists, exhibit the fastest 4.15% CAGR forecast to 2031, reflecting multispecialty endorsement for cardiovascular protection. Basal agents captured 62% of insulin takings in 2025; bolus products added 23%, while human insulins filled the remaining 15% share, largely in rural clinics that favor room-temperature stable vials. Biosimilar glargine’s 38% tender volume in 2025 generated MXN 420 million savings and directly lowered the Mexico diabetes drugs market size for basal insulin while expanding unit throughput. Patient groups nonetheless flagged counseling gaps that caused dose mis-titration events after mandatory switches, illustrating ongoing adherence hurdles.

Therapeutic diversification continues as SGLT-2 inhibitors post robust cardioprotective evidence. Jardiance and Farxiga widened labels after EMPA-REG and DAPA-CKD trials, spurring cardiologists and nephrologists to co-prescribe with metformin, which is expanding oral drug revenue at a quicker clip than sulfonylureas. Combination injectables like Xultophy and Ryzodeg remain below 5% of insulin-treated patients owing to limited reimbursement, but they signal a future where simplified regimens underpin market differentiation within the Mexico diabetes drugs market.

By Route of Administration: Oral Formulations Gain Ground

Subcutaneous delivery retained 69.53% share in 2025, anchored by insulin and GLP-1 pens that remain indispensable for type-1 and advanced type-2 control. Oral drugs are projected to expand at 4.75% CAGR, the strongest route, thanks to SGLT-2 indications that transcend glycemia and to Novo Nordisk’s oral semaglutide Rybelsus launch in mid-2024. Persistent injection fatigue—42% of insulin users miss at least three monthly doses—reinforces interest in oral alternatives and connected-pen technologies that address adherence lapses.

Empagliflozin reduced heart-failure hospitalizations by 25% in EMPEROR-Reduced, solidifying its role even when HbA1c sits below target. Dapagliflozin’s 39% renal disease-progression reduction in DAPA-CKD further pushes oral adoption among nephrologists. Subcutaneous share will remain dominant, yet incremental shifts toward tablets will broaden therapeutic reach and reinforce patient autonomy in the Mexico diabetes drugs market.

By Distribution Channel: E-Pharmacies Disrupt Traditional Retail

Retail chains retained 48.63% of 2025 sales, buoyed by pharmacist counseling and loyalty discounts. Online pharmacies are on a 5.87% CAGR trajectory as the Digital Health Framework legitimizes electronic prescriptions for insulin and controlled injectables. Prixz’s order surge from small municipalities shows digital models can bridge geographic gaps, though cold-chain fulfillment for biologics is still inconsistent, creating a service-quality moat for players investing in refrigerated micro-hubs.

Hospital pharmacies, largely within IMSS and ISSSTE networks, dispensed 35% of volume in 2025 but face chronic stock-outs because of void tenders and budget caps. That volatility funnels patients to retail outlets where insulin costs are 60–80% higher, encouraging parallel importers to source biosimilars from Central America at 25–30% margins. As digital infrastructure matures and rural broadband improves, e-pharmacies are poised to siphon share from brick-and-mortar stores, especially for oral therapies that avoid cold-chain limits, reshaping the go-to-market calculus in the Mexico diabetes drugs market.

Geography Analysis

Northern states delivered 32% of market value in 2025 despite housing only 18% of the population, reflecting higher diabetes prevalence of 21.4% and stronger private insurance coverage among maquila workforces. Mexico City and adjoining Estado de México contributed 28% of revenue through dense networks of specialty clinics that stock GLP-1 and SGLT-2 brands in private cash segments. Southern regions such as Oaxaca, Chiapas, and Guerrero mustered just 12% share because endocrinologist density lags at one per 85 000 people, and public formularies still depend on metformin and NPH insulin.

Tele-prescription traction is beginning to close the gap. Sixty-eight percent of Prixz’s Q1 2025 diabetes orders came from towns under 100 000 people, confirming latent demand where physical pharmacies are sparse. Yet only 34% of rural insulin shipments meet temperature standards, underlining logistic hurdles that stall equitable access. Border states reveal cross-border leakage; roughly 15-20% of diabetic residents purchase insulin in the United States to secure consistent supply and brand familiarity, diverting an estimated USD 45 million annually away from domestic channels. Biosimilar penetration and licit e-commerce may gradually repatriate this outflow, but quality assurance and payment security will be decisive.

Competitive Landscape

Novo Nordisk, Eli Lilly, and Sanofi held a significant percentage of insulin sales in 2025, yielding a moderately concentrated field despite the rise of biosimilar challengers. Novo Nordisk committed USD 200 million in 2024 to scale its Querétaro site, aiming to localize fill-finish for Ozempic and Rybelsus and shorten lead times from 12 weeks to 4 weeks.

Sanofi is bundling glucometers and strips with Lantus in IMSS bids to blunt Basaglar’s 30-35% price edge, but the biosimilar still seized 18% of IMSS insulin volume by December 2025. AstraZeneca and Boehringer Ingelheim jointly detail cardiologists and nephrologists on Farxiga and Jardiance, lifting SGLT-2 scripts 34% in 2024. E-pharmacy entrants such as Prixz and Farmacias del Ahorro Digital leverage telehealth integration and last-mile networks to capture the 5.87% CAGR growth track in distribution. Technology is another differentiator: Novo Nordisk patented a connected insulin pen in March 2024, aiming to curb the 42% non-adherence rate by pushing dose reminders to smartphones.

Mexico Diabetes Drugs Industry Leaders

Boehringer Ingelheim

Eli Lilly and Company

AstraZeneca plc

Novo Nordisk A/S

Sanofi S.A.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: Boehringer Ingelheim’s Social Engagement Fund invested in Clínicas del Azúcar to open four affordable diabetes centers across Mexico.

- April 2025: Novo Nordisk launched semaglutide 2.4 mg to support weight loss among obese adults in Mexico.

Mexico Diabetes Drugs Market Report Scope

As per the scope of the report, Diabetes drugs are medications used to manage and treat diabetes mellitus, a chronic health condition characterized by high blood sugar levels. These drugs help regulate blood glucose levels, improve the body's ability to use insulin, or increase insulin production, depending on the type of diabetes and the specific medication.

The Mexico diabetes drugs market is segmented by drug class, route of administration, and distribution channel. By drug class, the market includes insulins, oral anti-diabetic medications, non-insulin injectable medications, and combination drugs. Insulins are further categorized into basal/long-acting insulins, bolus/rapid-acting insulins, traditional human insulins, and biosimilar insulins. Basal/long-acting insulins include Lantus (insulin glargine), Levemir (insulin detemir), Toujeo (insulin glargine), Tresiba (insulin degludec), and Basaglar (biosimilar insulin glargine). Bolus/rapid-acting insulins comprise NovoRapid/Novolog (insulin aspart), Humalog (insulin lispro), and Apidra (insulin glulisine). Traditional human insulins include Novolin/Actrapid/Insulatard, Humulin, and Insuman, while biosimilar insulins are segmented into insulin glargine biosimilars and human insulin biosimilars. Oral anti-diabetic medications are divided into biguanides, alpha-glucosidase inhibitors, dopamine-D2 receptor agonists, SGLT-2 inhibitors, DPP-4 inhibitors, sulfonylureas, and meglitinides. SGLT-2 inhibitors include Canagliflozin (Invokana), Empagliflozin (Jardiance), Dapagliflozin (Farxiga/Forxiga), and Ipragliflozin (Suglat). DPP-4 inhibitors consist of Sitagliptin (Januvia), Saxagliptin (Onglyza), Linagliptin (Tradjenta), Alogliptin (Nesina/Vipidia), and Vildagliptin (Galvus). Non-insulin injectable medications include GLP-1 receptor agonists such as Victoza (liraglutide), Byetta (exenatide), Bydureon (exenatide ER), Trulicity (dulaglutide), and Lyxumia (lixisenatide), along with amylin analogues. Combination drugs are segmented into insulin blends and oral drug combinations. Insulin blends include NovoMix (biphasic insulin aspart), Ryzodeg (insulin degludec + aspart), and Xultophy (insulin degludec + liraglutide). By route of administration, the market is segmented into oral, subcutaneous, and intravenous methods. By distribution channel, the market is divided into hospital pharmacies, retail pharmacies, and online pharmacies.

By Drug Class

| Insulins | Basal / Long-Acting Insulins | Lantus (Insulin Glargine) |

| Levemir (Insulin Detemir) | ||

| Toujeo (Insulin Glargine) | ||

| Tresiba (Insulin Degludec) | ||

| Basaglar (Insulin Glargine, biosimilar) | ||

| Bolus / Rapid-Acting Insulins | NovoRapid / Novolog (Insulin Aspart) | |

| Humalog (Insulin Lispro) | ||

| Apidra (Insulin Glulisine) | ||

| Traditional Human Insulins | Novolin / Actrapid / Insulatard | |

| Humulin | ||

| Insuman | ||

| Biosimilar Insulins | Insulin Glargine Biosimilars | |

| Human Insulin Biosimilars | ||

| Oral Anti-Diabetic Drugs | Biguanides | |

| Alpha-glucosidase Inhibitors | ||

| Dopamine-D2 Receptor Agonists | ||

| SGLT-2 Inhibitors | Canagliflozin (Invokana) | |

| Empagliflozin (Jardiance) | ||

| Dapagliflozin (Farxiga/Forxiga) | ||

| Ipragliflozin (Suglat) | ||

| DPP-4 Inhibitors | Sitagliptin (Januvia) | |

| Saxagliptin (Onglyza) | ||

| Linagliptin (Tradjenta) | ||

| Alogliptin (Nesina/Vipidia) | ||

| Vildagliptin (Galvus) | ||

| Sulfonylureas | ||

| Meglitinides | ||

| Non-Insulin Injectables | GLP-1 Receptor Agonists | Victoza (Liraglutide) |

| Byetta (Exenatide) | ||

| Bydureon (Exenatide ER) | ||

| Trulicity (Dulaglutide) | ||

| Lyxumia (Lixisenatide) | ||

| Amylin Analogue | ||

| Combination Drugs | Insulin Combinations | NovoMix (Biphasic Insulin Aspart) |

| Ryzodeg (Insulin Degludec + Aspart) | ||

| Xultophy (Insulin Degludec + Liraglutide) | ||

| Oral Combinations | ||

By Route of Administration

| Oral |

| Subcutaneous |

| Intravenous |

By Distribution Channel

| Hospital Pharmacies |

| Retail Pharmacies |

| Online Pharmacies |

| By Drug Class | Insulins | Basal / Long-Acting Insulins | Lantus (Insulin Glargine) |

| Levemir (Insulin Detemir) | |||

| Toujeo (Insulin Glargine) | |||

| Tresiba (Insulin Degludec) | |||

| Basaglar (Insulin Glargine, biosimilar) | |||

| Bolus / Rapid-Acting Insulins | NovoRapid / Novolog (Insulin Aspart) | ||

| Humalog (Insulin Lispro) | |||

| Apidra (Insulin Glulisine) | |||

| Traditional Human Insulins | Novolin / Actrapid / Insulatard | ||

| Humulin | |||

| Insuman | |||

| Biosimilar Insulins | Insulin Glargine Biosimilars | ||

| Human Insulin Biosimilars | |||

| Oral Anti-Diabetic Drugs | Biguanides | ||

| Alpha-glucosidase Inhibitors | |||

| Dopamine-D2 Receptor Agonists | |||

| SGLT-2 Inhibitors | Canagliflozin (Invokana) | ||

| Empagliflozin (Jardiance) | |||

| Dapagliflozin (Farxiga/Forxiga) | |||

| Ipragliflozin (Suglat) | |||

| DPP-4 Inhibitors | Sitagliptin (Januvia) | ||

| Saxagliptin (Onglyza) | |||

| Linagliptin (Tradjenta) | |||

| Alogliptin (Nesina/Vipidia) | |||

| Vildagliptin (Galvus) | |||

| Sulfonylureas | |||

| Meglitinides | |||

| Non-Insulin Injectables | GLP-1 Receptor Agonists | Victoza (Liraglutide) | |

| Byetta (Exenatide) | |||

| Bydureon (Exenatide ER) | |||

| Trulicity (Dulaglutide) | |||

| Lyxumia (Lixisenatide) | |||

| Amylin Analogue | |||

| Combination Drugs | Insulin Combinations | NovoMix (Biphasic Insulin Aspart) | |

| Ryzodeg (Insulin Degludec + Aspart) | |||

| Xultophy (Insulin Degludec + Liraglutide) | |||

| Oral Combinations | |||

| By Route of Administration | Oral | ||

| Subcutaneous | |||

| Intravenous | |||

| By Distribution Channel | Hospital Pharmacies | ||

| Retail Pharmacies | |||

| Online Pharmacies | |||

Key Questions Answered in the Report

What is the projected value of the Mexico diabetes drugs market by 2031?

The market is forecast to reach USD 2.57 billion by 2031.

Which drug class is growing fastest in Mexico?

GLP-1 receptor agonists are advancing at a 4.15% CAGR through 2031.

How big is biosimilar insulin's role in public tenders?

Biosimilar glargine captured 38% of basal insulin volume in IMSS tenders during 2025.

Why are online pharmacies gaining traction?

Tele-prescription rules finalized in 2024 permit electronic insulin scripts, enabling e-pharmacies to reach rural patients quickly.

Which region of Mexico spends most on diabetes drugs?

Northern states account for 32% of national spending due to higher prevalence and greater private insurance coverage.

What limits public access to innovative GLP-1 therapies?

High prices and budget caps mean only 12% of the public drug budget covered GLP-1 products in 2025.

Page last updated on: