Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

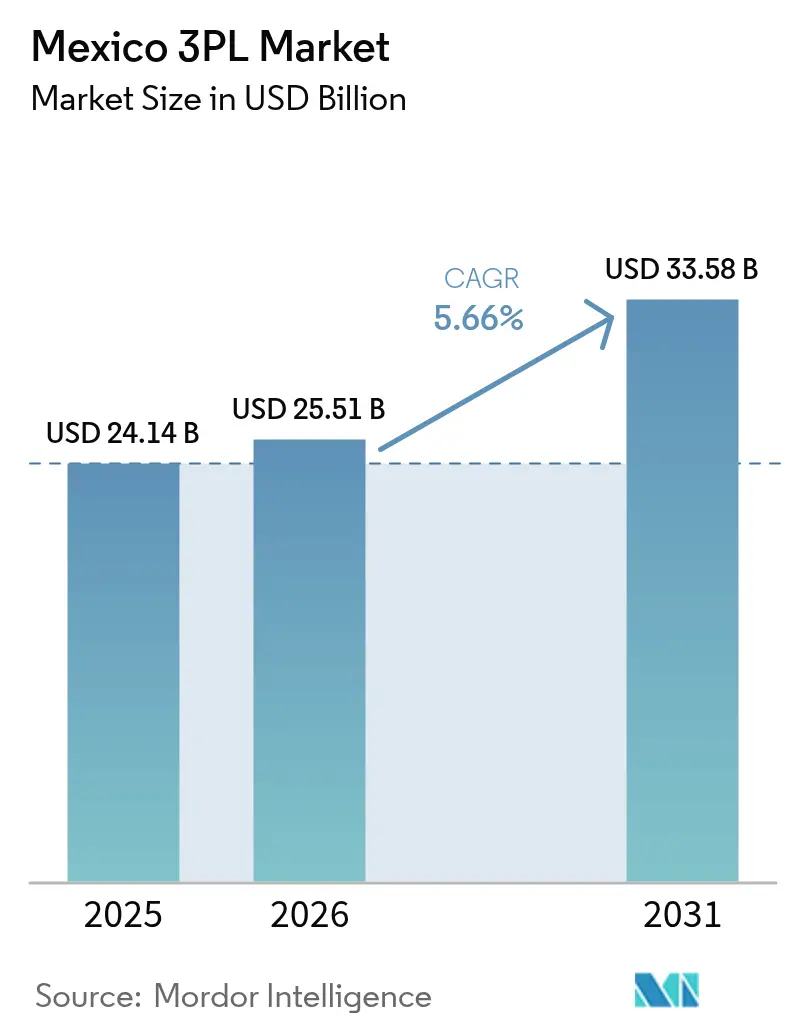

| Base Year Market Size (2025) | USD 24.14 Billion |

| Market Size (2026) | USD 25.51 Billion |

| Market Size (2031) | USD 33.58 Billion |

| Growth Rate (2026 - 2031) | 5.66% CAGR |

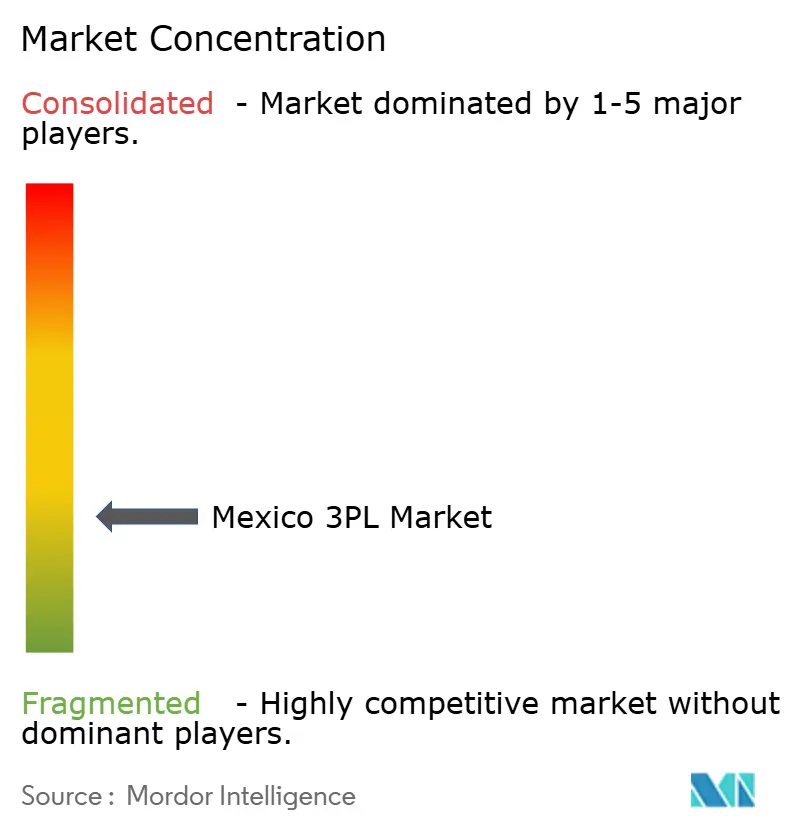

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Mexico 3PL Market Analysis by Mordor Intelligence

The Mexico 3PL market size in 2026 is estimated at USD 25.51 billion, growing from 2025 value of USD 24.14 billion with 2031 projections showing USD 33.58 billion, growing at 5.66% CAGR over 2026-2031.

The steady climb of the market is anchored in Mexico’s role as North America’s preferred near-shoring destination, rising bilateral trade with the United States, and the accelerated digitalization of freight networks. E-commerce parcel expansion, infrastructure upgrades such as the Interoceanic Corridor, and persistent inflows of foreign direct investment into automotive and electronics plants add momentum. However, the Mexico third-party logistics market navigates persistent security risks, driver-hours limits, and currency volatility, forcing providers to adopt technology-rich, asset-light models that lower fixed costs and spread risk. The interplay of these factors keeps pricing rational, promotes consolidation, and pushes the sector toward advanced visibility platforms and value-added warehousing services.

Key Report Takeaways

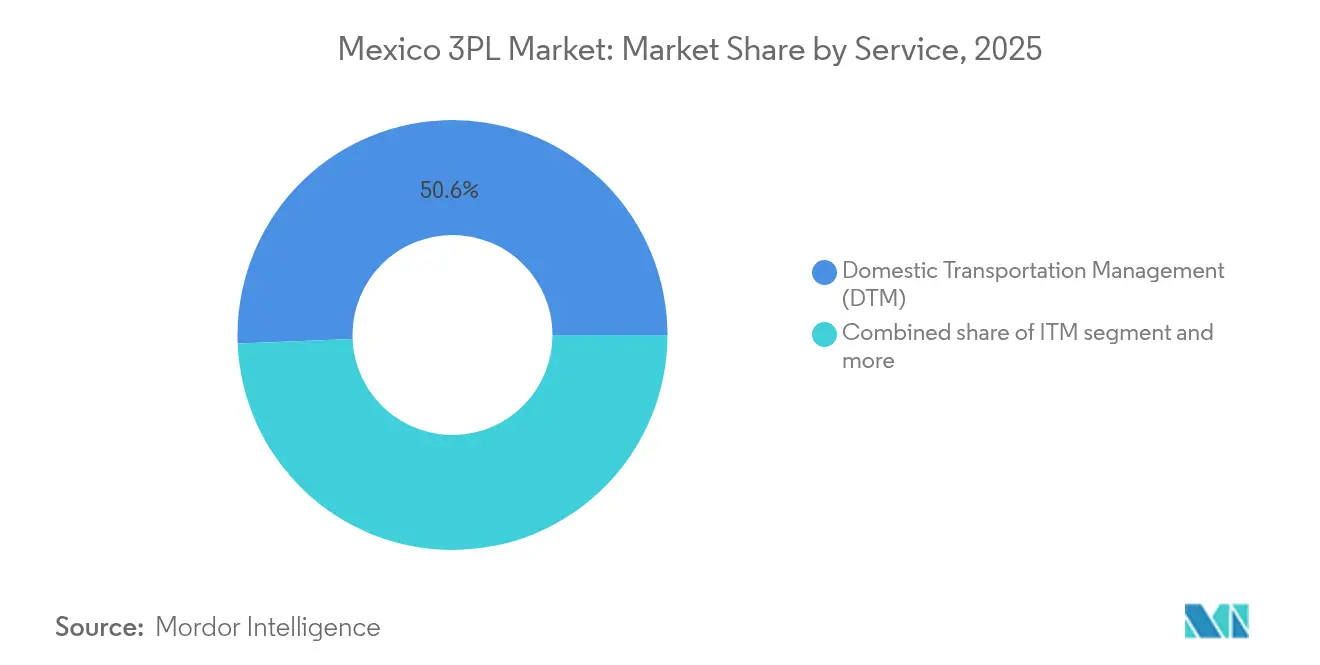

- By service, domestic transportation management led with 50.63% of Mexico's third-party logistics market share in 2025, while value-added warehousing and distribution are projected to advance at a 7.05% CAGR through 2031.

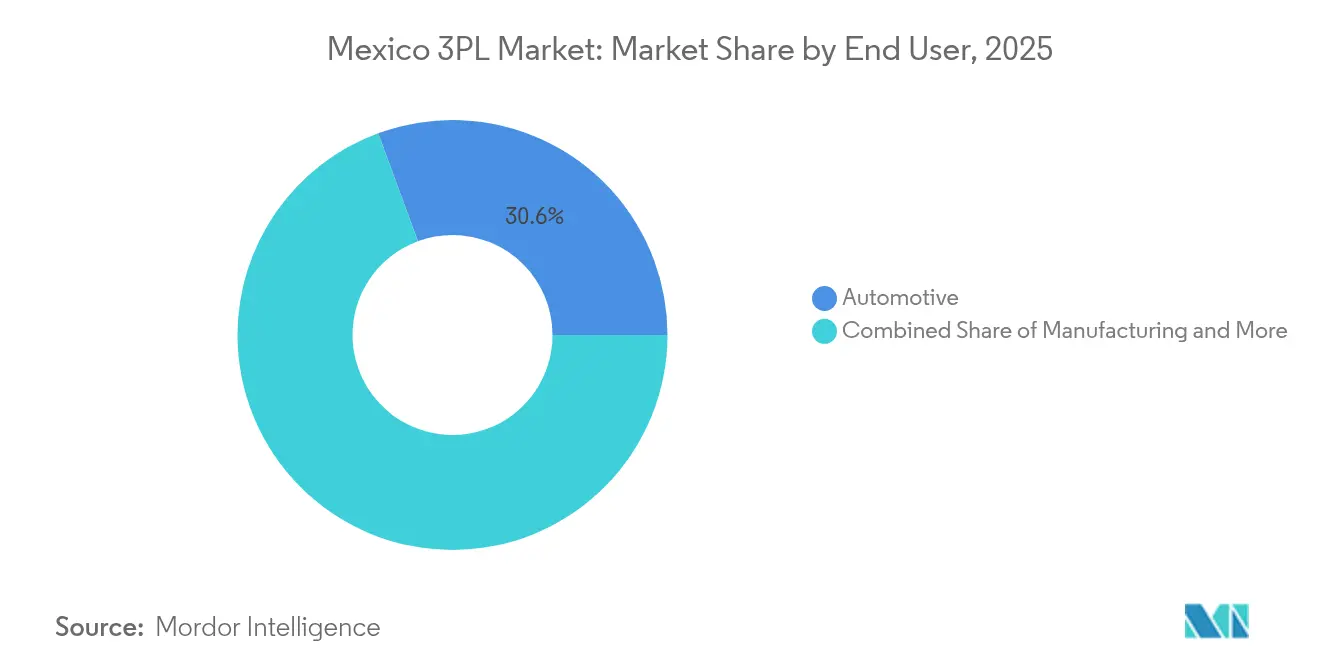

- By end user, automotive accounted for 30.62% of Mexico third-party logistics market size in 2025, and life sciences & healthcare is advancing at an 7.86% CAGR through 2031.

- By logistics model, asset-light providers captured 41.57% share of Mexico third-party logistics market size in 2025, and the same model is forecast to expand at an 6.03% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Mexico 3PL Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Near-shoring led re-routing of North American supply chains | +1.8% | Northern border states and Bajío region | Medium term (2-4 years) |

| E-commerce parcel volumes pushing same-day delivery expectations | +1.2% | Mexico City, Guadalajara, Monterrey | Short term (≤ 2 years) |

| Rebound in automotive production and cross-border component flows | +1.0% | Northern manufacturing corridors and central Mexico | Medium term (2-4 years) |

| Foreign pharma investment expanding GDP-linked cold-chain demand | +0.8% | Mexico City, Guadalajara, Tijuana | Long term (≥ 4 years) |

| Government incentives for agri-export cold logistics | +0.6% | Sinaloa, Sonora, Michoacán | Medium term (2-4 years) |

| Aduanas Digital customs-clearance program | +0.4% | Border crossings and major ports | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Near-shoring Led Re-routing of North American Supply Chains

Foreign manufacturers continue relocating capacity from Asia to Mexico, channeling USD 46 billion of planned investments into automotive, electronics, and pharmaceutical plants. Truck crossings into the United States have climbed 62.6% since 2000, magnifying demand for cross-border brokerage and multimodal coordination. As companies seek USMCA compliance without inflating landed costs, the Mexico third-party logistics market gains importance in orchestrating synchronized just-in-time flows that integrate value-added warehousing close to production nodes. Enhanced visibility platforms and unified customs data sets unlock cost savings, encouraging further outsourcing and sustaining the driver’s medium-term boost[1]Raúl Rodríguez, “2025 Mexican Automotive Industry Outlook,” Asociación Mexicana de la Industria Automotriz (AMIA), amia.com.mx.

E-commerce Parcel Volumes Pushing Same-day Delivery Expectations

Online retail now captures a rising share of Mexican consumer spending, led by platforms such as MercadoLibre, Temu, and Shein. MercadoLibre alone is investing USD 2.5 billion to lift its fulfillment centers from 90 to over 100, compressing delivery windows to under 24 hours in major cities. Logistics providers answer with micro-fulfillment hubs, dark stores, and crowdsourced rider fleets, all backed by AI-driven route engines that cut dwell time. The Mexico third-party logistics market must integrate same-day capabilities without eroding margins, further cementing the relevance of urban vertical warehouses that lower the last-mile cost curve.

Rebound in Automotive Production and Cross-border Component Flows

Automakers plan multibillion-dollar electrification bets, including BMW’s USD 870 million battery campus and Tesla’s projected USD 5 billion gigafactory[2]Olivier Zipse, “BMW Group Invests €870 Million in San Luis Potosí Battery Plant,” BMW Group Newsroom, bmwgroup.com. Component streams already benefit from Canadian Pacific Kansas City’s USD 100 million twin-track bridge at Laredo-Nuevo Laredo, boosting rail fluidity for tier-one part suppliers. Specialized handling for batteries and power electronics drives new contract logistics bids featuring temperature-managed transport and stringent ADR compliance. This high-value freight profile lifts revenue yield, reinforcing the sector as a durable growth engine for the Mexico third-party logistics market.

Foreign Pharma Investment Expanding GDP-linked Cold-chain Demand

DHL Supply Chain’s USD 200 million outlay in life-sciences facilities underscores a wave of pharmaceutical near-shoring that demands GDP-certified warehousing, 2-8 °C transport, and end-to-end traceability. Frialsa’s 125.7 million ft³ of Latin American freezer space demonstrates domestic capacity scaling, while federal clean-energy targets spur providers to adopt solar-powered refrigeration. Long-term contracts from multinational drug makers anchor predictable volumes, cushioning the Mexico third-party logistics market against cyclical swings.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Dilapidated road & rail infrastructure is inflating domestic haulage costs | -1.4% | Southern and rural regions | Long term (≥ 4 years) |

| Cargo-theft hotspots are raising insurance premiums and route detours | -1.0% | Estado de México, Puebla, Michoacán | Short term (≤ 2 years) |

| Driver-hours cap (NOM-087-SCT-2-2017) squeezing long-haul efficiency | -0.8% | Nationwide long-distance routes | Medium term (2-4 years) |

| Peso volatility & small-parcel documentation complexity | -0.6% | Cross-border corridors | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Dilapidated Road & Rail Infrastructure Inflating Domestic Haulage Cost

Roughly 85% of Mexican freight still moves by road, exposing shippers to bottlenecks on aging highways that require USD 18.9 billion to modernize by 2030. Although the MXN 157 billion (USD 8.45 billion) rail build-out and the USD 850 million Interoceanic Corridor promise relief, completion dates stretch beyond 2025. Until then, detours, vehicle wear, and congestion inflate operating costs that cascade into contract rates across the Mexico third-party logistics market. Providers respond by blending rail where available, but the restraint remains a long-term drag on margin.

Cargo-theft Hotspots Raising Insurance Premiums and Route Detours

More than 24,000 cargo robberies were logged in 2024, 83% involving violence, forcing shippers to pay higher insurance and schedule guarded convoys. Central corridors near Puebla and Estado de México are flashpoints, prompting lengthy bypasses that add fuel and labor hours. The National Guard’s “Balam” program trimmed highway robbery by 8.8%, yet risk remains elevated, particularly for food, beverage, and consumer electronics loads. The Mexico third-party logistics market invests heavily in telematics, geofencing, and driver training to counteract the short-term headwind[3]Miguel Silva, “National Guard ‘Balam’ Strategy Quarterly Report 2024,” Secretaría de Seguridad y Protección Ciudadana, gob.mx.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service: Transportation Dominance Amid Warehousing Acceleration

Domestic transportation management generated 50.63% of Mexico third-party logistics market size in 2025 as manufacturers relied on trucks to connect Bajío plants with border crossings. The corridor-heavy structure demands end-to-end orchestration, dynamic pricing, and compliance with driver-rest mandates. International transportation management, riding on USD 839.9 billion in bilateral trade, leverages integrated customs brokerage, bonded drayage, and rail interchanges to streamline USMCA cargo flows. Together, these services lock in predictable revenue streams that providers often hedge with multi-year contracts.

Value-added warehousing and distribution is scaling fastest at a 7.05% CAGR. Robotics-enabled centers, like Walmart’s AI-equipped hubs in Bajío, illustrate a pivot from basic storage to omnichannel fulfillment, returns processing, and kitting. Autonomous mobile robots deployed by GEODIS cut picking times, raising throughput without expanding footprint. As space near Mexico City tightens, vertical warehouses emerge, reinforcing the Mexico third-party logistics market as an innovation sandbox. Rail-linked facilities in San Luis Potosí and Monterrey integrate cross-dock zones that speed parts delivery to assembly plants, widening service stickiness.

By End User: Automotive Leadership Challenged by Healthcare Surge

Automotive contracts supplied 30.62% of Mexico third-party logistics market share in 2025, supported by 3.8 million vehicle exports and tier-one suppliers’ just-in-sequence schedules. Fleet expansions, such as TLE Automotive’s doubling of carrier units, underscore robust lane volumes into U.S. dealerships. Manufacturing, technology, and electronics combine near-shoring economics with duty-saving tariff structures, illustrated by Foxconn’s AI server expansion in Chihuahua.

Life sciences and healthcare, at an 7.86% CAGR, will erode automotive’s dominance by mid-decade. DHL’s USD 1.1 billion continent-wide upgrade introduces GDP-certified nodes, reversible temperature lanes, and real-time biologic tracking. Cold-storage specialists integrate solar arrays to meet environmental mandates while maintaining ±2 °C tolerances, boosting the value proposition of the Mexico third-party logistics industry. Consumer goods, FMCG, and food trade maintain stable trajectories but wrestle with theft-driven insurance surcharges that compress margins.

By Logistics Model: Asset-Light Strategy Drives Market Evolution

Asset-light operators held 41.57% of Mexico third-party logistics market size in 2025, expanding at 6.03% CAGR by leveraging partner fleets and orchestration software rather than owned trucks. Platforms like C.H. Robinson’s Navisphere offer API-fed visibility, exception management, and automated paperwork that cut overhead. In a high-theft landscape, dispersing equipment risk across subcontracted carriers lowers exposure and premiums.

Asset-heavy providers remain critical for sectors needing dedicated rigs, secured yards, and specialized equipment such as car carriers and GDP-certified trailers. Hybrid models fuse selective ownership with brokerage networks to optimize capacity swings while meeting stringent service-level agreements. NOM-087-SCT-2-2017 driver-hour limits tighten fleet utilization, pushing even asset-heavy players toward collaborative pooling via digital freight platforms. The Mexico third-party logistics market thus converges on data-rich ecosystems where physical assets and software symbiotically unlock scale.

Geography Analysis

Northern border states dominate volumes thanks to proximity to Texas gateways; Laredo-Nuevo Laredo alone processed nearly 3 million inbound trucks in 2023, equating to USD 320 billion in trade. Plants in Nuevo León, Coahuila, and Chihuahua funnel parts northward, and value-added warehouses in Monterrey supply just-in-time kits to Detroit in under 48 hours. Central Mexico, anchored by the Mexico City-Querétaro axis, acts as the nation’s consolidation hub, blending domestic distribution with export staging; the region’s multimodal linkages enable sub-24-hour truck relays between ports and maquiladoras, reinforcing the Mexico third-party logistics market.

Southern corridors receive fresh attention through the USD 850 million Interoceanic Corridor that links Salina Cruz to Coatzacoalcos, targeting 1.4 million TEUs annually by 2033. Ten planned industrial parks and dredging upgrades could shift Asia-U.S. East Coast containers off the Panama Canal, creating a new load center for third-party providers. Yet poor road quality and sparse secure parking still deter time-sensitive cargo, keeping growth modest until rail and port works finish in 2025.

Pacific coast hubs such as Manzanillo and Lázaro Cárdenas expand crane capacity to 10 million TEUs, strengthening links with Asian suppliers. Gulf terminals in Veracruz and Altamira support energy projects and agro-export cold chains, while rising industrial clusters in Guanajuato and Aguascalientes leverage Bajío tollways for balanced access to both oceans. The Mexico third-party logistics market, therefore, mirrors the country’s polycentric economic map, with each zone specializing in lanes that match its industrial DNA and infrastructure readiness.

Competitive Landscape

The competitive field is moderately fragmented: global integrators such as DHL, GEODIS, Kuehne+Nagel, and DSV coexist with domestic specialists Traxión and Solistica. Scale once conferred advantage, yet differentiation now hinges on technology, vertical expertise, and security protocols. Blue Yonder’s AI engines power predictive ETAs for automotive and pharma accounts, while Solistica’s real-time cargo-monitoring command centers reduce theft exposures along central highways.

Cross-border expertise remains a battleground. C.H. Robinson, Nuvocargo, and Trimble exploit the Complemento Carta Porte mandate to bundle compliance services with transportation bids. Meanwhile, asset-heavy fleets hedge risk by carving out separate asset-light subsidiaries to tap brokerage margins without swelling depreciation. Ongoing consolidation—typified by Nuvocargo’s 2025 acquisition of Merge Transportation—signals a gradual roll-up of midsize brokers aiming for network density and TMS scale.

Security spending skews market share toward cash-rich players able to finance telematics, escort services, and cargo insurance buffers. Providers that can demonstrate less than 1% claims ratios command premium rates among life-sciences and high-tech shippers. Over 2025–2030, the Mexico third-party logistics market is poised for deeper strategic alliances as digital platforms match vetted carriers with demand, compressing spot margins but lifting overall service quality.

Mexico 3PL Industry Leaders

DHL Supply Chain

Solistica

Traxión

CEVA Logistics

Kuehne + Nagel

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Walmart earmarked USD 6 billion for 1,500 new Mexican stores and two AI-driven distribution centers in Bajío and Tlaxcala.

- January 2025: Nuvocargo acquired Merge Transportation, widening its North American 3PL footprint and securing CTPAT certification for brokerage services.

- December 2024: CPKC finished a USD 100 million double-track expansion at the Laredo-Nuevo Laredo rail bridge, doubling cross-border train throughput.

- October 2024: Foxconn opened a Guadalajara plant for Nvidia GB200 chips and invested USD 241 million in Chihuahua for AI servers, reinforcing electronics near-shoring.

Mexico 3PL Market Report Scope

Third-party logistics companies provide a number of services that have to do with the logistics of the supply chain. This includes transportation, warehousing, picking and packing, inventory forecasting, order fulfillment, packaging, and freight forwarding.

A complete background analysis of the 3PL Mexico Industry market, which includes an assessment of the economy, market overview, market size estimation for key segments, emerging trends in the market, market dynamics, and key company profiles, are covered in the report. The impact of COVID-19 has also been incorporated and considered during the study.

The 3PL Mexico Market is Segmented by Services (Domestic Transportation Management, International Transportation Management, and Value-added Warehousing and Distribution) and End Users (Automotive, Consumer and Retail, Energy, Healthcare, Industrial and Aerospace, Technology, and Other End Users). The report offers market sizes and forecasts in value (USD) for all the above segments.

By Service

| Domestic Transportation Management (DTM) | Roadways |

| Railways | |

| Airways | |

| Waterways | |

| International Transportation Management (ITM) | Roadways |

| Railways | |

| Airways | |

| Waterways | |

| Value-Added Warehousing & Distribution (VAWD) |

By End User

| Automotive |

| Energy & Utilities |

| Manufacturing |

| Life Sciences & Healthcare |

| Technology & Electronics |

| E-commerce |

| Consumer Goods & FMCG |

| Food & Beverages |

| Others |

By Logistics Model

| Asset-Light (Management-Based) |

| Asset-Heavy (Own Fleet & Warehouses) |

| Hybrid |

| By Service | Domestic Transportation Management (DTM) | Roadways |

| Railways | ||

| Airways | ||

| Waterways | ||

| International Transportation Management (ITM) | Roadways | |

| Railways | ||

| Airways | ||

| Waterways | ||

| Value-Added Warehousing & Distribution (VAWD) | ||

| By End User | Automotive | |

| Energy & Utilities | ||

| Manufacturing | ||

| Life Sciences & Healthcare | ||

| Technology & Electronics | ||

| E-commerce | ||

| Consumer Goods & FMCG | ||

| Food & Beverages | ||

| Others | ||

| By Logistics Model | Asset-Light (Management-Based) | |

| Asset-Heavy (Own Fleet & Warehouses) | ||

| Hybrid | ||

Key Questions Answered in the Report

What is the forecast value of the Mexico third-party logistics market by 2031?

It is projected to reach USD 33.58 billion, reflecting a 5.66% CAGR.

Which service segment is growing fastest in Mexico’s 3PL space?

Value-added warehousing and distribution is advancing at a 7.05% CAGR due to robotics-enabled fulfillment demand.

How large is the automotive share in Mexico’s 3PL sector?

Automotive held 30.62% of Mexico third-party logistics market share in 2025, sustained by 3.8 million vehicle exports.

Why are asset-light models gaining traction?

They reduce capital exposure and distribute security risk while leveraging technology platforms for visibility and compliance.

What is the key geographic corridor for cross-border trade?

The Laredo-Nuevo Laredo crossing processes nearly 3 million trucks and USD 320 billion in annual bilateral trade.

How does cargo theft affect logistics costs?

Elevated theft rates increase insurance premiums and force route detours, trimming sector CAGR by an estimated 1.0%.

Page last updated on: