Online Doctor Consultation Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

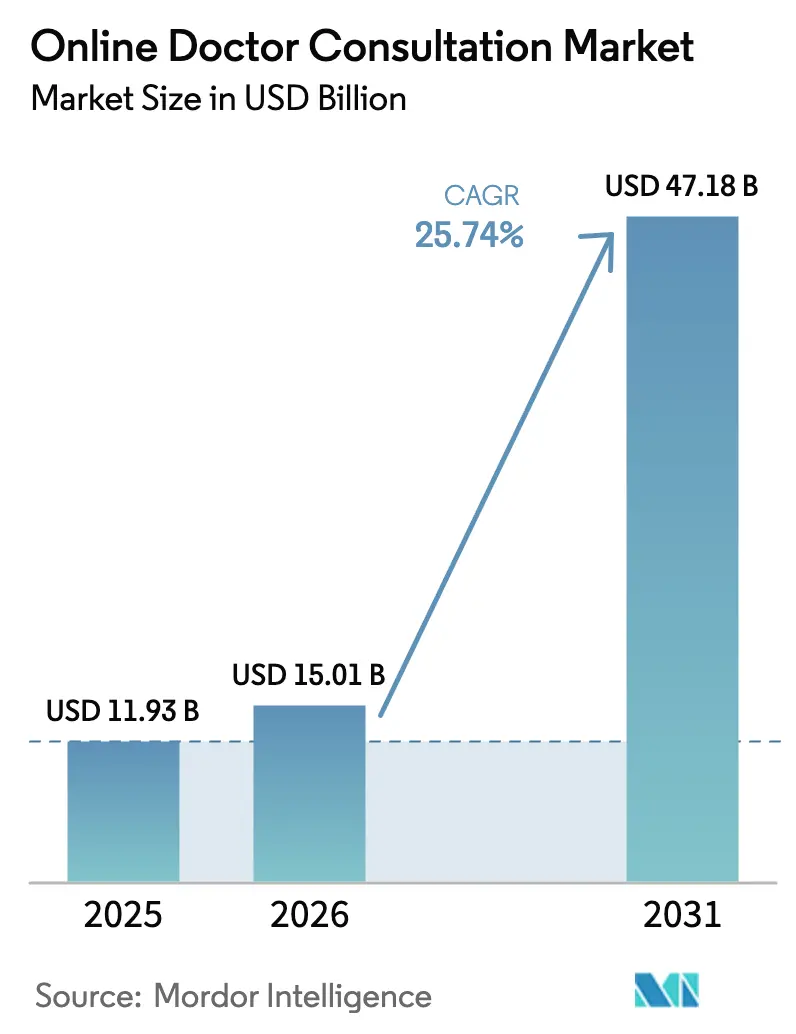

| Market Size (2026) | USD 15.01 Billion |

| Market Size (2031) | USD 47.18 Billion |

| Growth Rate (2026 - 2031) | 25.74% CAGR |

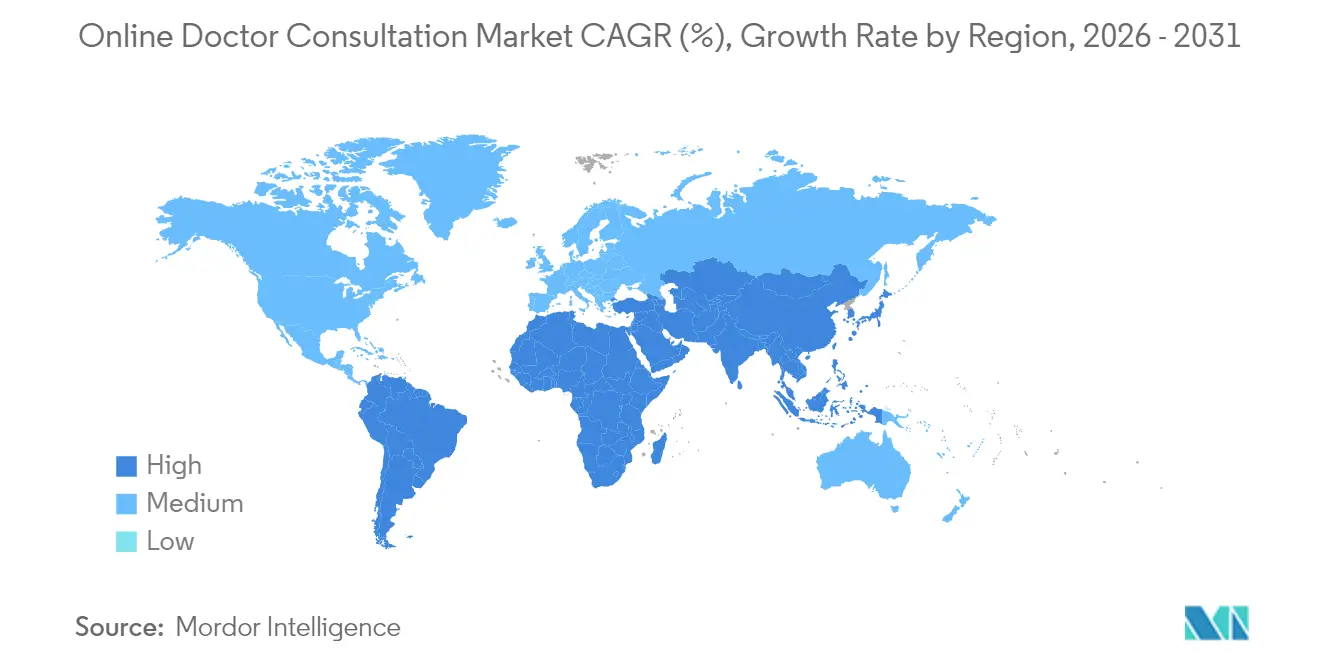

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Online Doctor Consultation Market Analysis by Mordor Intelligence

Online doctor consultation market size in 2026 is estimated at USD 15.01 billion, growing from 2025 value of USD 11.93 billion with 2031 projections showing USD 47.18 billion, growing at 25.74% CAGR over 2026-2031. This sustained growth reflects the transition from pandemic-driven telehealth surges to routine, integrated virtual care. 5G roll-outs facilitate real-time high-definition video visits, governments in Europe and Asia now reimburse a wider range of e-health services, and corporate “virtual-first” health plans in North America shift millions of covered lives to online entry points. North America led with a 38% revenue share in 2024, yet Asia-Pacific recorded the quickest regional expansion at 12.3% CAGR as public platforms such as India’s eSanjeevani scale to hundreds of millions of consultations. Mobile apps commanded 70% of all visit volume in 2024, while video consultations accounted for 60% of encounters, underscoring patient and clinician preferences for visually rich interactions. Competitive intensity remains moderate: global incumbents add mental-health, chronic-care, and remote screening capabilities through acquisitions, whereas regional specialists differentiate on language support, local regulatory compliance, and pharmacy fulfillment.

Key Report Takeaways

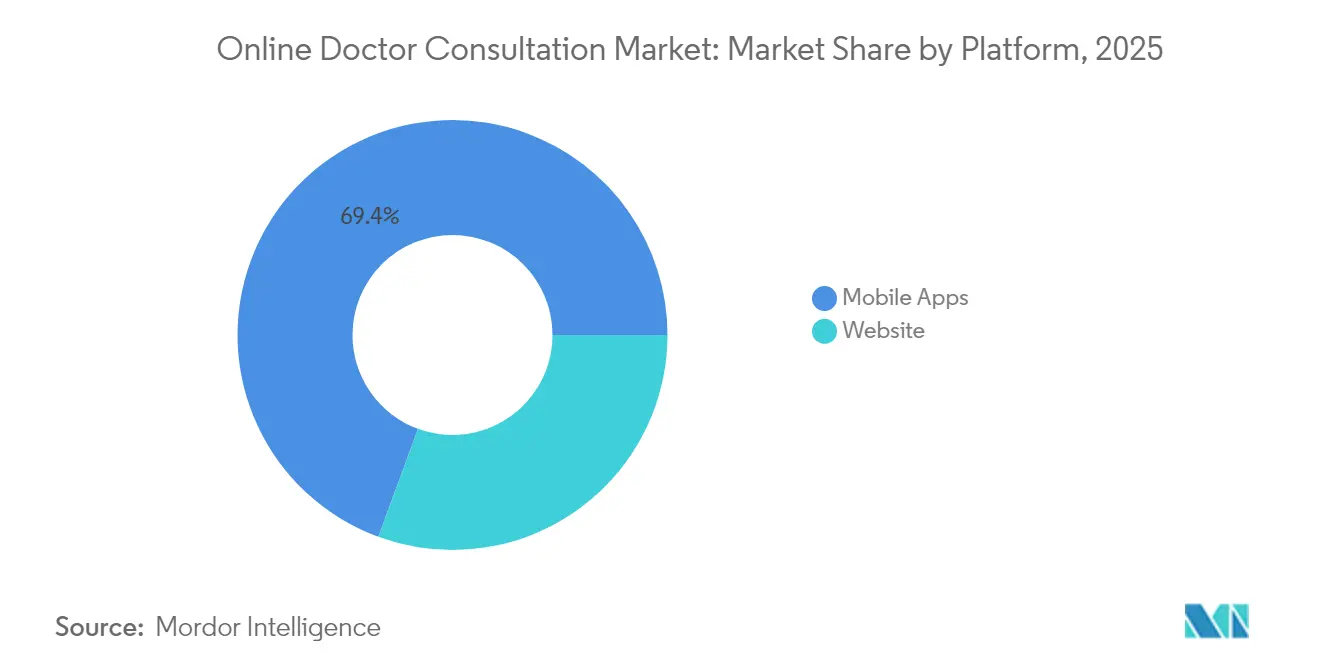

- By platform, mobile apps held 69.40% of the Online doctor consultation market share in 2025.

- By consultation type, video chat accounted for 59.20% share of the Online doctor consultation market size in 2025 and is forecast to register an 24.3% CAGR to 2031.

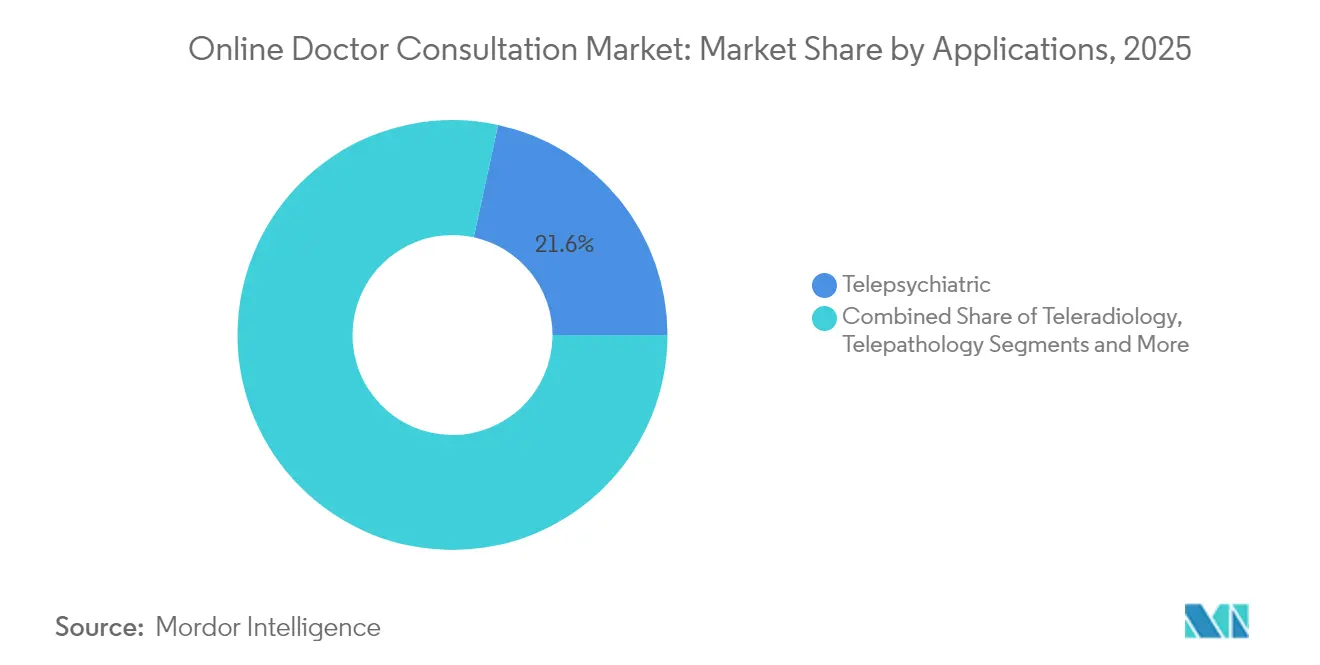

- By application, telepsychiatric services led with a 21.60% revenue share in 2025; the segment is advancing at a 28.6% CAGR through 2031.

- By end user, independent consultants captured 13.25% of the Online doctor consultation market size growth trajectory between 2026-2031, outpacing hospitals.

- By geography, North America led with a 37.60% share in 2025, while Asia-Pacific is the fastest-growing region at a 28.40% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Online Doctor Consultation Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Proliferation of 5G & Low-Latency Networks Enabling Real-time Video Visits | +1.8% | Global, with early gains in North America, Europe, and urban Asia-Pacific | Medium term (2-4 years) |

| Expansion of National e-Health Reimbursement Codes in Europe & Asia | +1.5% | Europe & Asia-Pacific core, spill-over to emerging markets | Long term (≥ 4 years) |

| Employer Adoption of Virtual-First Health Plans in North America | +1.2% | North America, with expansion to multinational corporations globally | Short term (≤ 2 years) |

| Inclusion of Mental-Health Teleconsults in Public Insurance in Japan and Australia | +0.9% | Asia-Pacific, with policy replication potential in developed markets | Medium term (2-4 years) |

| AI-Triage Chatbots Driving First-Contact Consult Volumes | +1.1% | Global, with faster adoption in tech-forward markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Proliferation of 5G and Low-Latency Networks

Ultra-high-bandwidth coverage eliminates video lags and supports streaming of continuous biometric data during online consultations, enabling telestroke triage and remote ICU monitoring in real time. [1]Dina M. El-Sherif, “Telehealth and Artificial Intelligence Insights,” md-journal.com Rural facilities now access metropolitan specialists across multiple disciplines, reducing medical travel and bolstering local outcomes. 5G also underpins emerging virtual-reality therapies and augmented-reality surgical guidance, broadening the clinical scope of the Online doctor consultation market. Network operators and hospital systems co-invest in edge-computing hubs that process sensitive clinical data locally, maintaining privacy while meeting latency requirements.

Expansion of National e-Health Reimbursement Codes

Germany removed the ceiling on reimbursable video visits in 2024, and Singapore, Korea, and Japan activated dedicated telepsychiatry billing codes, creating a stable revenue model for providers. [2]Gleiss Lutz, “Telemedicine Update: Legal Framework,” gleisslutz.com Standardized coding aligns payment parity with in-person services, encouraging hospitals to integrate telehealth as a front-door service rather than an ancillary offering. Reimbursement harmonization also enables cross-border second opinions within regional economic blocs, amplifying addressable patient pools for platform operators.

Employer Adoption of Virtual-First Health Plans

Large employers now embed virtual visits as the first touchpoint, cutting emergency room spending by up to 30% and shortening time-to-appointment from weeks to hours. Plans route employees to Teladoc-powered primary care or chronic-disease programs before physical referrals, driving predictable volumes to platform partners. Insurers replicate the model, bundling unlimited virtual consultations with high-deductible policies to enhance perceived value while containing claims costs.

AI-Powered Triage Chatbots

Health systems deploying conversational AI document 35% shorter call-center queues and 30% more completed virtual visits as chatbots automate symptom capture and scheduling. [3]Fabric Health, “Chat & Conversational AI,” fabrichealth.com Pre-visit histories delivered to clinicians streamline workflows, lifting per-hour consult capacity. Early-phase pilots at Mayo Clinic validate 94% diagnostic concordance, reinforcing clinician confidence.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented E-Prescription Integration Across Cross-Border Consults | -1.3% | Global, with acute challenges in EU cross-border scenarios | Long term (≥ 4 years) |

| Physician Licensing Restrictions in South-East Asia & Middle East | -0.8% | South-East Asia & Middle East, limiting regional expansion | Medium term (2-4 years) |

| Low Digital Literacy in 65+ Segment Slowing Adoption | -0.7% | Global, with higher impact in rural and developing regions | Long term (≥ 4 years) |

| High Platform Churn Due to Freemium Pricing Wars | -0.5% | Global, with concentration in competitive urban markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Fragmented E-Prescription Integration

Divergent national drug formularies and incompatible electronic prescription standards create compliance costs that erode platform margins and slow international expansion. Telehealth providers must maintain multiple pharmacy integrations and perform country-specific validation steps, stretching IT resources and prolonging onboarding times for new markets. Progress toward a single EU eRx data set is under discussion but full convergence remains distant.

Physician Licensing Restrictions

Only 23 of 51 Asian countries have binding telemedicine rules; several require in-country licensure for every online consultation, splitting the addressable clinician pool and limiting scale economies. Platforms therefore establish separate legal entities and provider panels in each jurisdiction, raising overhead and delaying break-even timelines. Regulatory harmonization initiatives led by ASEAN health ministers could mitigate the barrier but agreement on malpractice coverage and data sovereignty remains challenging.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Platform: Mobile Apps Accelerate Patient Engagement

Mobile applications represented USD 8.27 billion of revenue and 69.40% market share in 2025 within the Online doctor consultation market. Usage is projected to climb at an 26.4% CAGR as smartphones become the default health gateway. Push notifications drive appointment adherence, while integration with wearable sensors enables continuous glucose, blood-pressure, or sleep-quality feeds during consults. Patient-portal research shows 51% of US adults accessed health data via apps in 2024, up from 38% in 2020. Websites retain relevance for complex chart reviews and large-screen imaging but edge toward niche use among older or low-vision populations. The Online doctor consultation market size for website-based services is forecast to grow modestly at 18.2% CAGR, sustained by enterprise workflows such as multi-disciplinary tumor boards.

The competitive dynamic favors app-centric entrants that iterate consumer features quickly, including bilingual symptom checkers and one-click prescription refills. Yet mobile platforms must maintain rigorous security to retain clinician trust: two-factor authentication, end-to-end encryption, and device biometrics are now baseline expectations. App marketplaces also impose commission fees that website operators avoid, prompting some providers to promote progressive-web apps as cost-saving hybrids.

By Consultation Type: Video Dominance Meets Asynchronous Disruption

Video visits generated 59.20% of service volume in 2025, equal to USD 7.06 billion, and will expand at 24.3% CAGR as broadband and 5G coverage deepen. Synchronous video allows physicians to observe non-verbal cues and perform limited physical assessments, preserving the bedside dynamic. Audio-only calls serve follow-ups or counseling in low-bandwidth regions, while asynchronous modalities—secure text, images, and AI-guided Q&A—grow fastest at 28.1% CAGR. The Online doctor consultation market size for text-first encounters is small today but attracts cost-conscious younger demographics who value immediacy over face-to-face interaction.

AI-driven triage funnels many routine cases through chatbots that resolve queries or escalate to physicians only when clinical judgment is required. Hybrid workflows lower physician burden and monetize AI licenses, creating new revenue streams. Platform strategists therefore bundle unlimited messaging with monthly subscriptions, cross-selling premium video slots for complex issues.

By Applications: Mental-Health Leadership

Telepsychiatry captured a 21.60% revenue share in 2025—USD 2.58 billion—within the Online doctor consultation market and is growing 28.6% annually as pandemic-related stress and workforce shortages converge. Public insurers in Japan and Australia now reimburse virtual counseling on parity with in-person sessions, unlocking latent demand. Teleradiology and telepathology contribute consistent enterprise revenue streams, while teledermatology benefits from high-resolution smartphone cameras. Telecardiology gains momentum through remote patient-monitoring bundles for hypertension and heart-failure care.

Competitive differentiation hinges on specialty depth: mental-health platforms add AI sentiment analysis and 24/7 crisis interventions, whereas imaging-focused services integrate PACS connectivity and DICOM viewers. The Online doctor consultation market share of niche fields such as teleophthalmology remains below 3% due to equipment requirements, but innovations in phone-based visual acuity testing could spark future expansion.

By End User: Independent Consultants Gain Momentum

Hospitals owned 34.50% of revenue in 2025 yet face margin pressure as independent consultants grow at 26.8% CAGR, riding physician dissatisfaction with facility employment models. The Online doctor consultation market size attributable to independents is projected to surpass USD 12.34 billion by 2031 as direct-pay telehealth and concierge models proliferate. Hospitals, however, retain complex care pathways and insurer networks that independents cannot easily replicate. Rehabilitation centers and retail clinics build hybrid models, blending brick-and-mortar therapy with virtual check-ins to maintain continuity.

Platform vendors now tailor practice-management suites with scheduling, payment, and malpractice coverage features that lower administrative barriers for physicians launching solo telehealth practices. Cloud-based EHR integration ensures continuity as patients transition between independent and hospital-based providers, reinforcing ecosystem stickiness.

Geography Analysis

North America generated 37.60% of global revenue in 2025, underpinned by Medicare’s expanded telehealth codes (now extended through 2025) and employer-sponsored virtual-first plans that cover tens of millions of workers. US consumer surveys reveal 64% of adults prefer online visits for routine issues, citing convenience and time savings. Canada integrates telehealth to bridge remote-community physician gaps, while Mexico’s Seguro Popular successor program tests mobile e-health pilots. Despite mature infrastructure, broadband deserts and low digital literacy among seniors still cap universal uptake, requiring targeted subsidy and education programs.

Europe’s progress is steady but heterogeneous. Germany abolished online-visit volume caps, and the European Health Data Space aims to standardize cross-border record exchange. Nordic countries approach full reimbursement parity, whereas Eastern Europe faces budget and infrastructure headwinds. The Online doctor consultation market benefits from pan-EU migration, with expatriates seeking specialists in their language across borders. GDPR compliance imposes rigorous data-security obligations that favor well-capitalized incumbents.

Asia-Pacific advances fastest, at 28.40% CAGR, propelled by population scale and government initiatives. India’s eSanjeevani has logged more than 275 million visits, demonstrating low-cost telehealth scalability. China’s “Internet + Healthcare” ecosystem blends AI triage, electronic prescriptions, and couriered medicines. Australia’s Medicare subsidizes virtual mental-health sessions, addressing rural shortages. Regulatory fragmentation persists—only 23 of 51 Asian nations have binding telehealth laws—but ASEAN working groups are drafting mutual-recognition frameworks. The Middle East liberalizes slowly, yet the Gulf Cooperation Council funds national telehealth platforms to manage chronic-disease burdens amid expatriate populations.

Competitive Landscape

Global leadership is contested by Teladoc Health, Amwell, Ping An Good Doctor, Practo, Doctor Anywhere, and several regional specialists. Consolidation accelerates capability expansion: Teladoc purchased UpLift Health (USD 30 million) for mental-health depth and Catapult Health (USD 65 million) for at-home screenings in 2025. Amwell divested its psychiatric unit to Avel eCare, reallocating capital to core platform R&D and enterprise integrations. Asian players focus on consumer market-share grabs through multilingual chatbots and embedded pharmacy delivery.

Competitive vectors increasingly revolve around:

1. Clinical-outcome evidence—platforms publish peer-reviewed reductions in HbA1c or depression scores;

2. AI differentiation—first-contact triage, auto-documentation, and risk prediction;

3. Omnichannel fulfillment—integrating diagnostics, labs, and same-day prescription shipping.

Partnership ecosystems matter: Teladoc’s alignment with Amazon Health provides seamless enrollment of chronic-care programs to Prime members. Australian insurer Medibank selected Amwell for preventative initiatives, demonstrating B2B2C reach. Start-ups attack white spaces, such as language-specific marketplaces serving migrant workers or AI-only asynchronous consults for dermatology.

Pricing competition remains measured; most platforms pivot from freemium to subscription bundles for unlimited primary-care access. That shift lowers churn and improves lifetime value. Hardware integration—sphygmomanometers, glucometers, wearables—creates additional lock-in and data moat advantages.

Online Doctor Consultation Industry Leaders

Babylon Health

Practo Technologies Pvt. Ltd

Alibaba Health Information Technology Limited

Doctor Anywhere

Amwell Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Teladoc Health acquired UpLift Health Technologies for USD 30 million to embed insurance-covered mental-health services into its BetterHelp offering, strengthening the platform’s behavioral-care vertical.

- February 2025: Teladoc Health bought Catapult Health for USD 65 million, gaining VirtualCheckup screening technology that enables at-home labs and follow-on virtual consultations, positioning Teladoc to capture preventive-care budgets.

- January 2025: Amwell sold its Psychiatric Care unit to Avel eCare for USD 21 million and redirected resources toward API-first platform enhancements and AI scribe functionality.

- January 2025: Teladoc partnered with Amazon Health Benefits, allowing millions of U.S. members to enroll in chronic-condition programs through their Amazon account, cementing a high-traffic acquisition funnel.

Global Online Doctor Consultation Market Report Scope

Online doctor consultations make up one of the biggest markets for telemedicine. The market only covers remote consultations between patients and doctors that happen online via websites or mobile apps. Both public and private medical institutions can schedule these consultations.

The Online Doctor Consultation Market is segmented by Platform (Websites and Mobile Apps) and Geography (North America, Europe, Asia Pacific, Latin America, and the Middle East and Africa). The market sizes and forecasts are provided in terms of value (USD million) for all the above segments.

| Website |

| Mobile Apps |

| Video Chat |

| Audio Chat |

| Other Consultation Types |

| Telepyschiatric |

| Teleradiology |

| Telepathology |

| Teledermatology |

| Telecardiology |

| Other Applications |

| Hospitals |

| Independent Consultants |

| Rehabilitation Centers |

| Other End-users |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Nordics | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East | United Arab Emirates |

| Saudi Arabia | |

| Kuwait | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Rest of Africa |

| By Platform | Website | |

| Mobile Apps | ||

| By Consultation Type | Video Chat | |

| Audio Chat | ||

| Other Consultation Types | ||

| By Applications | Telepyschiatric | |

| Teleradiology | ||

| Telepathology | ||

| Teledermatology | ||

| Telecardiology | ||

| Other Applications | ||

| By End User | Hospitals | |

| Independent Consultants | ||

| Rehabilitation Centers | ||

| Other End-users | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Nordics | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East | United Arab Emirates | |

| Saudi Arabia | ||

| Kuwait | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current size of the Online doctor consultation market?

The market stands at USD 15.01 billion in 2026 and is on track to reach USD 47.18 billion by 2031, reflecting a 25.74% CAGR.

Which region is growing fastest?

Asia-Pacific posts the highest growth at a 28.40% CAGR, driven by large-scale public platforms and supportive reimbursement in Japan, India, and Australia.

What platform type dominates usage?

Mobile applications led with 69.40% of global visit volume in 2025 thanks to smartphone penetration and integrated wearable-sensor data.

How are employers influencing adoption?

North American corporations implement virtual-first benefit plans that route employees to online primary care, cutting ER spending by up to 30% and boosting predictable telehealth volumes.

Which specialty segment shows the strongest growth?

Telepsychiatry leads with a 21.60% revenue share and a 28.6% CAGR as mental-health demand surges and parity reimbursement expands.

What are the main regulatory hurdles?

Cross-border e-prescription incompatibility and fragmented physician licensing in parts of Asia and the Middle East limit international scaling, shaving as much as 1.3 percentage points off forecast CAGR.

Page last updated on: