Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

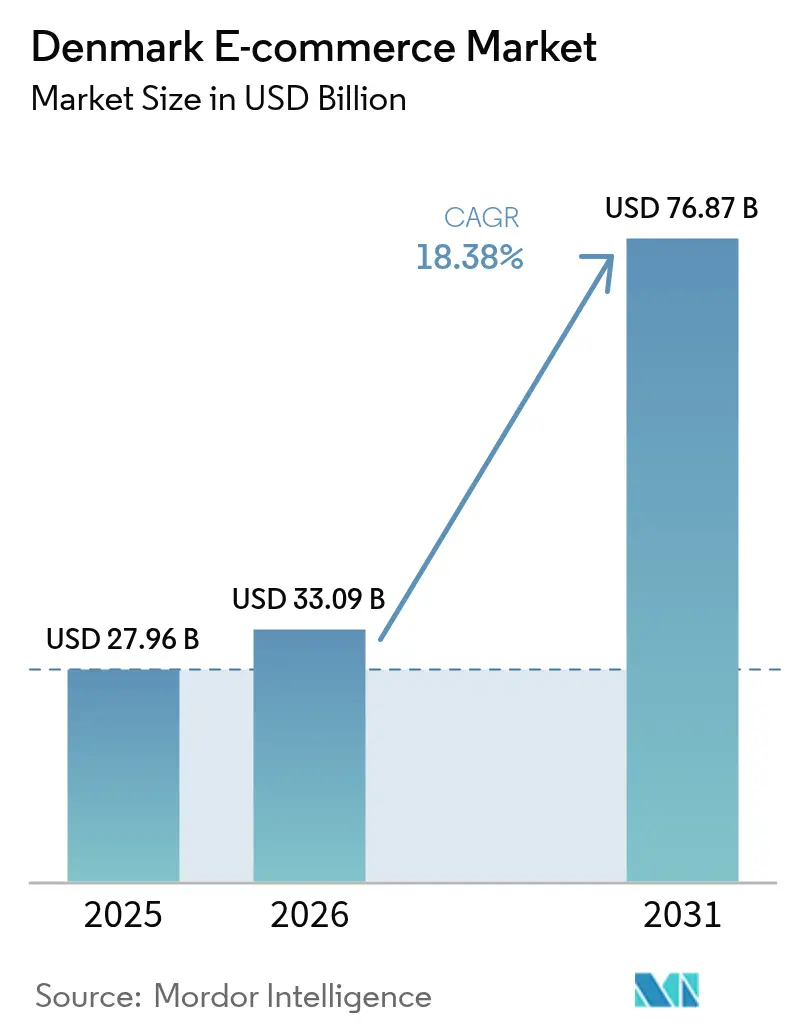

| Base Year Market Size (2025) | USD 27.96 Billion |

| Market Size (2026) | USD 33.09 Billion |

| Market Size (2031) | USD 76.87 Billion |

| Growth Rate (2026 - 2031) | 18.38% CAGR |

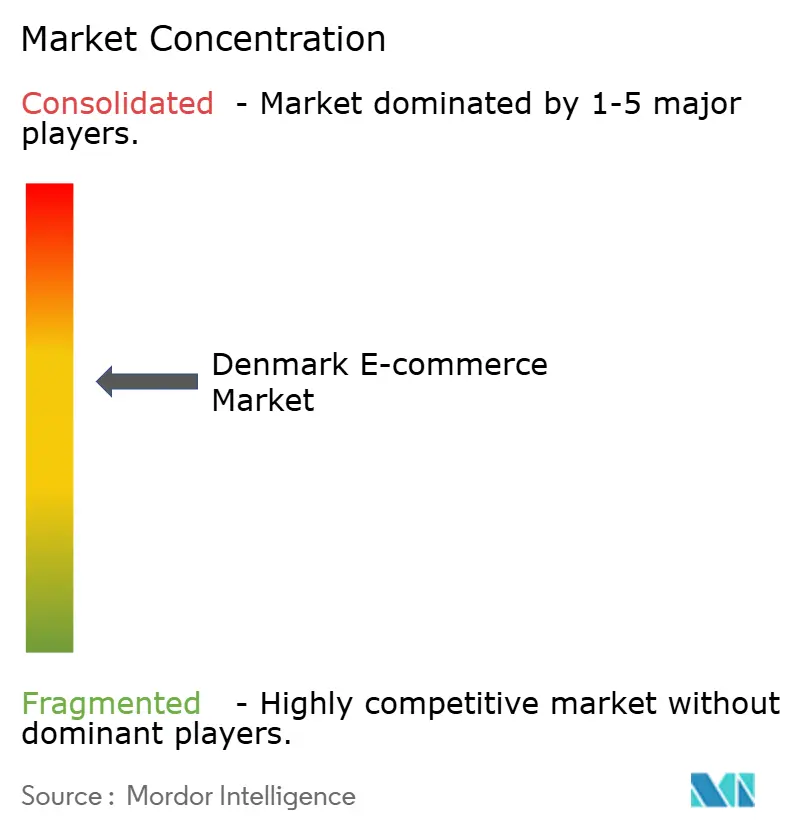

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Denmark E-commerce Market Analysis by Mordor Intelligence

The Denmark e-commerce market size is expected to grow from USD 27.96 billion in 2025 to USD 33.09 billion in 2026 and is forecast to reach USD 76.87 billion by 2031 at 18.38% CAGR over 2026-2031. Accelerators include a 90% digital-payment penetration rate, 4.5 million MobilePay users, and the government’s USD 138 million Digital Growth Strategy that subsidises SME web-shop adoption.[1]Danmarks Nationalbank, “Payment Habits in Denmark,” nationalbanken.dk Foreign entrants such as Temu are intensifying price competition, yet domestic retailers respond with omnichannel investments that leverage Denmark’s dense parcel-locker network to promise nationwide same-day delivery. Regulatory tailwinds-most notably the Corporate Sustainability Reporting Directive (CSRD)—raise the strategic value of traceable online supply chains and favour digitally native operators. Stable macro-conditions, including 3.6% GDP growth and 2.0% inflation in 2025, further underpin consumer spending resilience.

Key Report Takeaways

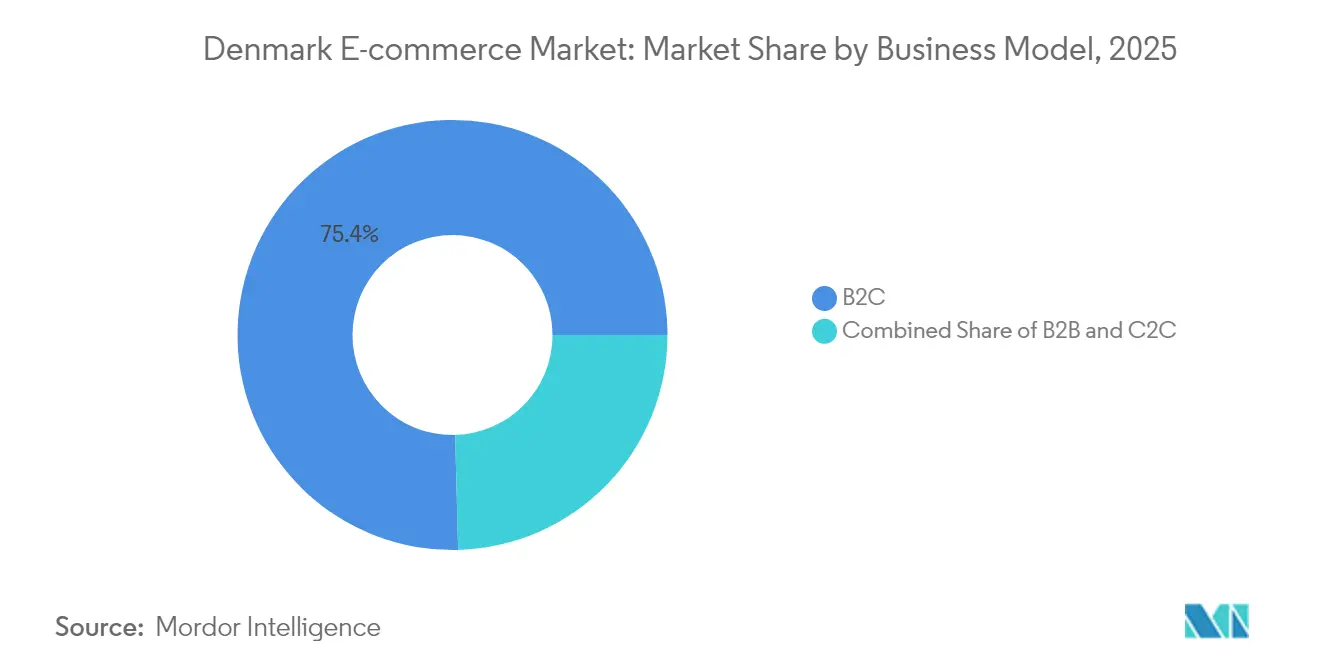

- By business model, B2C held 75.42% of the Denmark e-commerce market share in 2025; B2B is forecast to expand at a 21.20% CAGR through 2031.

- By device type, mobile commanded 59.02% of the Denmark e-commerce market size in 2025 and is set to grow at 22.07% CAGR to 2031.

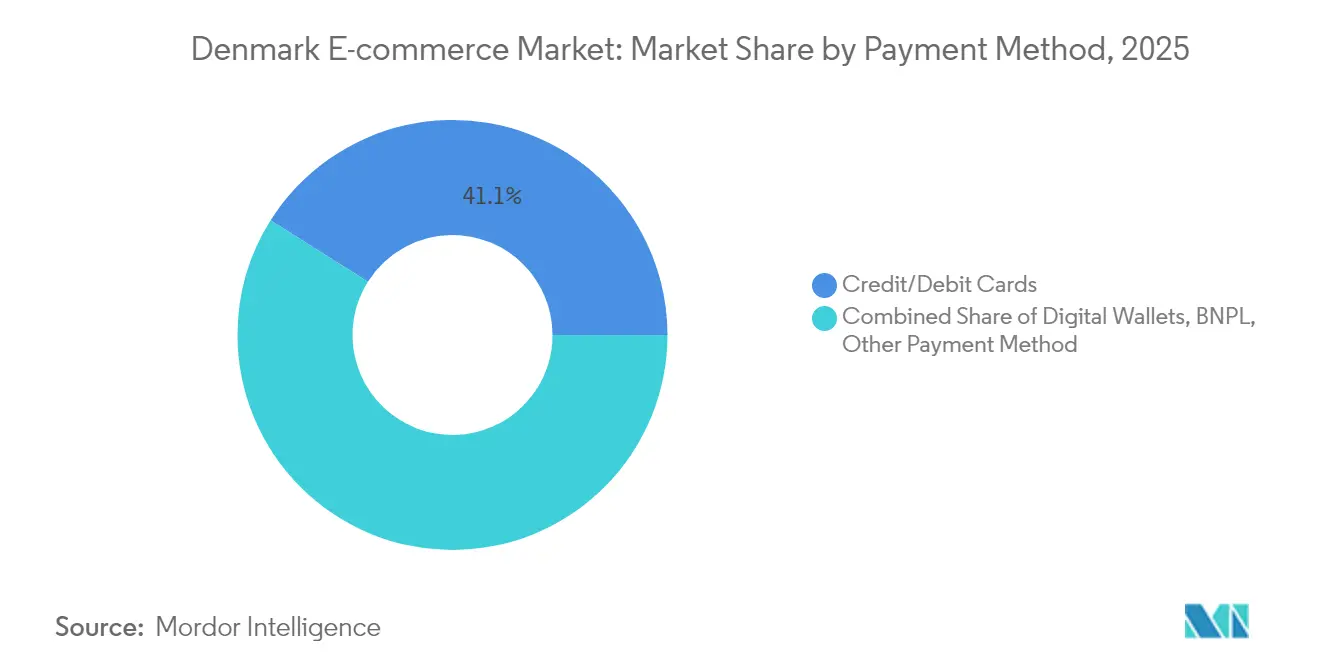

- By payment method, credit and debit cards retained a 41.05% share, while digital wallets are registering the fastest 23.46% CAGR.

- By B2C product category, fashion and apparel led with a 22.10% revenue share in 2025; food and beverages is projected to rise at a 24.12% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Denmark E-commerce Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| MobilePay-Led Digital-Wallet Ubiquity Accelerating Checkout Conversion Rates | +4.2% | National, with strongest penetration in urban centers | Short term (≤ 2 years) |

| Government 'Digital Growth Strategy 2023' Subsidising SME Web-shop Adoption | +3.8% | National, with priority focus on rural SMEs | Medium term (2-4 years) |

| Dense Parcel-Locker & Same-Day Logistics Network Enabling Less than 24 hr Delivery Promise | +3.1% | National, concentrated in Copenhagen, Aarhus, Odense metropolitan areas | Medium term (2-4 years) |

| CSRD Sustainability Mandate Driving Shift to Traceable Online Supply Chains | +2.7% | EU-wide, with Denmark as early adopter market | Long term (≥ 4 years) |

| Omnichannel Investments by Salling, Matas Converting Store Inventory to Online Fulfilment | +2.4% | National, with spillover effects to Nordic markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

MobilePay-led digital-wallet ubiquity accelerating checkout conversion rates

MobilePay covers 77% of Denmark’s population, delivers instant settlement, and lowers abandonment by 15-25% versus card-only checkouts. Retailers gain higher conversion without absorbing interchange fees, and B2B platforms benefit from the same API stack that automates invoice payments. The entrenched network effect raises consumer switching costs and presents an entry barrier for foreign marketplaces that lack domestic wallet parity. As wallet usage spreads to subscription and pay-by-link services, Danish merchants unlock recurring-revenue models and deeper customer data. Conversion gains translate into incremental GMV, pushing the Denmark e-commerce market toward scale advantages.

Government ‘Digital Growth Strategy 2023’ subsidising SME web-shop adoption

The state has earmarked USD 138 million through 2027 to train SMEs, co-fund platform builds, and embed cybersecurity tools.[2]U.S. Department of Commerce, “Denmark – Digital Economy,” trade.gov Six regional business houses give hands-on guidance, shortening the learning curve for rural firms previously deterred by compliance complexity. Subsidies offset onboarding costs to leading SaaS carts, broadening merchant diversity and category breadth. As rural merchants digitise, parcel volumes spread beyond major cities, raising utilisation of the locker network and supporting logistics price deflation. The programme also emphasises data analytics upskilling, enabling SMEs to refine assortment and pricing in real time.

Dense parcel-locker and same-day logistics network enabling < 24 h delivery promise

Parcel-locker penetration reaches 41%, the highest in the Nordics, and integrates with public-transport nodes for frictionless collection.[3]International Post Corporation, “Delivery Choice – Parcel Lockers,” ipc.be PostNord and retailers such as Salling Group optimise last-mile routes, cutting delivery costs and carbon footprints. Locker density allows national same-day SLAs at a fraction of courier-to-door economics. Fashion and consumer-electronics segments see uplift as immediacy influences basket conversion. Higher service levels form a defensible moat against cross-border entrants that cannot replicate infrastructure without heavy capex.

CSRD sustainability mandate driving shift to traceable online supply chains

From 2026, Danish companies must disclose cradle-to-gate impact metrics, compelling investment in digital ledgers and verifiable ESG tags. Platforms that automate emissions tracking gain a pricing premium and lower merchant churn. Sustainability-oriented consumers—59% of millennials are ready to pay more—reward compliant merchants, expanding green product GMV. CSRD also accelerates B2B adoption as corporates need auditable procurement trails, reinforcing the Denmark e-commerce market’s pivot to enterprise grade platforms.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Foreign Platforms (Temu, Amazon) Intensifying Price-Based Competition | -3.4% | National, with spillover effects across Nordic markets | Medium term (2-4 years) |

| High Delivery-Cost Sensitivity Hinders the Market | -2.8% | National, with strongest impact in rural and suburban areas | Short term (≤ 2 years) |

| GDPR & Local-Data Residency Rules Inflating Compliance Costs for SME E-tailers | -2.1% | EU-wide, with Denmark facing stricter enforcement | Long term (≥ 4 years) |

| Ageing Cohort Lagging Digital Adoption Despite Overall 99% Internet Access | -1.7% | National, with higher concentration in rural areas | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High delivery-cost sensitivity hinders the market

More than 40% of Nordic consumers drop baskets when delivery charges exceed personal thresholds, a behaviour amplified outside metro areas. Although parcel-locker density alleviates costs, grocery and low-ticket items still struggle to absorb fees without eroding retailer margins. Inflation-driven budget vigilance persists despite headline price easing, pushing merchants toward free-shipping thresholds and membership models that compress gross margin. The Denmark e-commerce market faces a balancing act between service differentiation and price elasticity.

Foreign platforms (Temu, Amazon) intensifying price-based competition

Temu became Denmark’s third-largest webshop in 2024 by deploying aggressive discounting. Amazon’s Nordic logistics hub further tightens pricing benchmarks. While choice expands for consumers, domestic players confront margin compression. Danish incumbents emphasise speed, sustainability, and local customer care to defend share, but these differentiators require continuous investment. EU product-safety probes into Temu introduce regulatory uncertainty, yet price wars are expected to persist through the medium term.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Business Model: Digital procurement momentum reshapes corporate buying

B2C controlled 75.42% of 2025 GMV, yet B2B’s 21.20% CAGR indicates a structural pivot as Danish SMEs migrate indirect spend online. The Denmark e-commerce market size for B2B orders is projected to double between 2026 and 2031 as firms seek catalogue consolidation and CSRD-ready reporting. Domestic platforms leverage MobilePay Business to automate reconciliation, while Zalando’s ZEOS and Salling Group’s wholesale APIs unlock cross-border reach. Higher average order values and lower return rates lift unit economics. Local preference for Danish language interfaces and ESG compliance tilts advantage toward home-grown platforms, limiting the appeal of generic international marketplaces.

Sustainability legislation accelerates vendor audits, and B2B portals integrating emissions calculators become default procurement engines. Meanwhile, B2C leaders experiment with marketplace models to monetise excess traffic and open new revenue streams. C2C remains niche but synergises with circular-economy initiatives endorsed by regulators, adding to overall market diversification.

By Device Type: Mobile-first commerce drives engagement across age cohorts

With 59.02% 2025 share, smartphones are the primary storefront and are forecast to reach 69.5% by 2031 at a 22.07% CAGR. The Denmark e-commerce market share advantage stems from ubiquitous 5G coverage and user familiarity with MobilePay’s one-tap flow. Retailers invest in PWA architecture to accelerate page loads and lower bounce rates. Location-based flash sales boost in-store traffic for omnichannel chains and blur lines between online and offline experiences.

Desktop remains relevant for complex, high-ticket items such as furniture or B2B requisitions where large screen and multitab research aid decision making. Emerging devices-smart TVs, in-car infotainment, voice assistants-collectively stay below 5% share yet represent experimentation ground for frictionless reordering and shoppable media formats, extending the Denmark e-commerce market’s touchpoints.

By Payment Method: Wallet adoption challenges card incumbency

Credit and debit cards still command 41.05% transaction share, but digital wallets post a 23.46% CAGR that could swing majority status by 2031. Wallet superiority lies in instant settlement, built-in authentication, and loyalty integration. BNPL grows among Gen Z, though the Financial Supervisory Authority’s consultations temper unregulated expansion. For merchants, wallet fees are competitive with acquiring costs while delivering data advantages that fuel personalisation.

Card networks remain indispensable for cross-border sales and high-ticket B2B invoices; therefore hybrid checkout stacks stay the norm in the Denmark e-commerce industry. Banks respond with tokenised card-on-file solutions to match wallet UX, ensuring frictionless multi-currency capability for foreign shoppers and sustaining inbound tourism spend.

By B2C Product Category: Fashion leadership meets grocery disruption

Fashion and apparel delivered a 22.10% share of 2025 GMV, benefiting from liberal return policies and AI-powered size recommendation models. Zalando’s planned ABOUT YOU acquisition signals further consolidation and data synergy. At the same time, food and beverages is the breakout category with a 24.12% CAGR as locker-to-fridge solutions and insulated click-and-collect expand reach. The Denmark e-commerce market size for online groceries is projected to outpace overall retail growth, supported by household time-saving priorities.

Consumer electronics sustain mid-teens growth, leveraging showrooming and trade-in programs to refresh upgrade cycles. Beauty and personal care gains as omnichannel chains like Matas merge digital tutorials with in-store diagnostics. Furniture and home goods confront bulky-item logistics but ride on Denmark’s design heritage and conscious-consumer trends. Smaller niches-from DIY to toys-capture equilibrium growth anchored by seasonal campaigns and influencer collaborations.

Geography Analysis

Urban concentration remains pronounced, with the Greater Copenhagen area accounting for an estimated 44.62% of national GMV in 2025. Same-day promise reliability tops 98% in the capital region, creating a benchmark that spreads to Aarhus and Odense as locker density climbs. Rural adoption, however, records faster percentage growth, spurred by state-funded broadband and SME digitisation grants. The Denmark e-commerce market enjoys a compact landmass that keeps average delivery distances under 300 km, sustaining cost efficiency.

Cross-border flows are seamless thanks to EU consumer-rights alignment; German and Swedish shoppers frequently utilise Danish domains for design goods, making Denmark a Nordic fulfilment hub. Currency conversion from Danish Krone to EUR introduces minor friction that multicurrency wallets increasingly absorb. National internet penetration stands at 99% and underpins uniform consumer reach.

Trade-fragmentation risk remains the chief geographic headwind, as shipping disruptions raise input costs. Yet diversified sourcing across EU, UK, and Asian suppliers mitigates single-region dependency. Denmark’s early CSRD compliance positions its merchants to attract sustainability-minded consumers in neighbouring markets where disclosure rules lag, converting regulation into competitive advantage.

Competitive Landscape

Denmark’s e-commerce arena is moderately fragmented. The top five players control roughly 45% of GMV, leaving room for specialised disruptors. Zalando dominates fashion, leveraging algorithmic personalisation and an expanding fulfilment-as-a-service product. Salling Group blends loyalty across bricks and clicks, pushing unified inventory visibility that delivers a 99.94% click-and-collect completion rate. Nemlig.com and Coop.dk defend grocery share through private-label pricing and cold-chain optimisation.

Temu and Amazon escalate price tension. Their pan-EU logistics give broad catalogue depth, but local service gaps persist-returns handling and Danish-language support remain weak points. Domestic players counter with sustainability credentials, leveraging shorter supply chains and CSRD-compliant reporting dashboards. Logistics tech start-ups integrate AI route-planning and autonomous locker restocking, signalling a tech-led competitive phase.

Partnership ecosystems flourish: Coop Danmark’s extended pact with Tata Consultancy Services migrates core ERP to SAP S/4HANA, unlocking real-time stock views that improve customer promises. Zalando’s ABOUT YOU acquisition expects EUR 100 million (USD 108 million) EBIT synergies via marketing pooling and shared last-mile assets. PostNord partners with locker manufacturers to double urban capacity by 2027, ensuring infrastructure keeps pace with rising parcel volumes.

Denmark E-commerce Industry Leaders

Apple Inc.

Harald Nyborg

Zalando SE

Elgiganten A/S

Bilka .dk (Salling Group)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Salling Group acquired Rimi Baltic and 33 Coop Denmark stores to widen geographic reach and boost scale economies; the deal aligns with its ASPIRE ’28 plan to secure upstream sourcing power and omnichannel leverage.

- March 2025: Zalando agreed to purchase ABOUT YOU, creating a dual-brand ecosystem aimed at demographic segmentation and EBIT synergies through joint marketing and shared fulfilment nodes.

- March 2025: Coop Danmark renewed its partnership with Tata Consultancy Services for a large-scale SAP S/4HANA migration, signalling a technology-first agenda to unify data and automate replenishment.

- February 2025: The Danish government allocated DKK 50 million (USD 7.1 million) to revitalise 16 town centres, indicating policy support for hybrid retail that blends physical experience with online convenience.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the Denmark e-commerce market as the gross merchandise value generated when Danish residents purchase physical goods or services via internet-enabled devices from domestic or foreign storefronts that settle the transaction in Danish kroner or an international equivalent.

Scope exclusion: Digital-only subscriptions, online classified listings, and business-to-government procurement portals are outside our frame.

Segmentation Overview

- By Business Model

- B2C

- B2B

- C2C

- By Device Type

- Smartphone / Mobile

- Desktop and Laptop

- Other Device Types

- By Payment Method

- Credit / Debit Cards

- Digital Wallets

- BNPL

- Other Payment Method

- By B2C Product Category

- Beauty and Personal Care

- Consumer Electronics

- Fashion and Apparel

- Food and Beverages

- Furniture and Home

- Toys, DIY and Media

- Other Product Categories

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed logistics operators, payment-gateway managers, brand web-store heads, and SME marketplace sellers across Copenhagen, Aarhus, and Odense. These exchanges clarified average basket values, return ratios, and the share of mobile checkouts, enabling us to validate assumptions surfaced during desk work.

Desk Research

We began with official statistics from bodies such as Statistics Denmark, the Danish Tax Agency's VAT filings, and Eurostat's Retail Trade Index to anchor retail baselines. Complementary insights on shopper behavior and device trends came from the EU Digital Economy and Society Index, PostNord's annual Nordic e-commerce survey, and Danish Central Bank card-payment bulletins. To assess cross-border flows, we screened customs shipment records available through Volza and short-haul parcel data shared by the Nordic Transport Association. Subscription-only resources, notably D&B Hoovers for retailer financials and Dow Jones Factiva for timely news, furnished firm-level signals. The sources listed illustrate, yet do not exhaust, the reference pool our analysts consulted.

Market-Sizing & Forecasting

A top-down build starts with national retail turnover, then applies online penetration rates by product cluster and cross-border uplift. Selective bottom-up checks, such as leading merchant revenue roll-ups and sampled average selling price multiplied by parcel counts, fine-tune totals. Key variables include internet user base growth, MobilePay adoption, parcel-locker density, average delivery fee, and DKK-USD exchange glide path. Five-year projections employ multivariate regression with scenario analysis, where coefficients are reviewed with interviewed experts before lock-in. Gaps in merchant disclosure are bridged by imputing sector-median margins adjusted for Denmark's higher logistics cost index.

Data Validation & Update Cycle

Outputs pass anomaly screens, variance checks against external macro signals, and peer review. Reports refresh annually, with mid-cycle updates triggered by material events, and a final analyst sweep precedes delivery.

Why Mordor's Denmark E-commerce Baseline Earns Trust

Published estimates often diverge because firms mix revenue with payment volume, bundle digital content, or freeze exchange rates at different points.

Key gap drivers include scope breadth, inclusion of B2B service marketplaces, and refresh cadence differences that skew comparisons, which are then compounded by varying assumptions on average selling prices and cross-border leakage.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 27.96 B (2025) | Mordor Intelligence | - |

| USD 24 B (2024) | Regional Consultancy A | Counts domestic online retail only, omits travel, food delivery, and services |

| USD 115.4 B (2024) | Industry Databank B | Aggregates card payment volume across B2C, C2C, and peer-to-peer transfers without deflation for refunds. |

The comparison shows that when scope alignment and variable rigor are inconsistent, figures swing widely. Mordor's disciplined segmentation, blended build-up, and annual refresh cycle provide decision-makers with a balanced, transparent baseline anchored to verifiable Danish data assets.

Key Questions Answered in the Report

What is the current value of the Denmark e-commerce market?

The market is valued at USD 33.09 billion in 2026, with a forecast CAGR of 18.38% through 2031.

Which business model is growing fastest in Danish e-commerce?

B2B transactions are advancing at a 21.20% CAGR, outpacing B2C albeit from a smaller base.

How important is MobilePay to online retail in Denmark?

MobilePay covers 77% of residents and cuts checkout abandonment 15-25%, making it a critical conversion driver.

What product category leads online sales?

Fashion and apparel holds a 22.10% revenue share, driven by rich return policies and AI size tools.

How is sustainability regulation affecting Danish e-commerce?

CSRD requires full supply-chain impact reporting by 2026, favouring platforms that offer integrated ESG tracking.

Are foreign marketplaces threatening local players?

Temu and Amazon intensify price competition, but domestic retailers leverage faster delivery and sustainability credentials to defend share.

Page last updated on: