Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

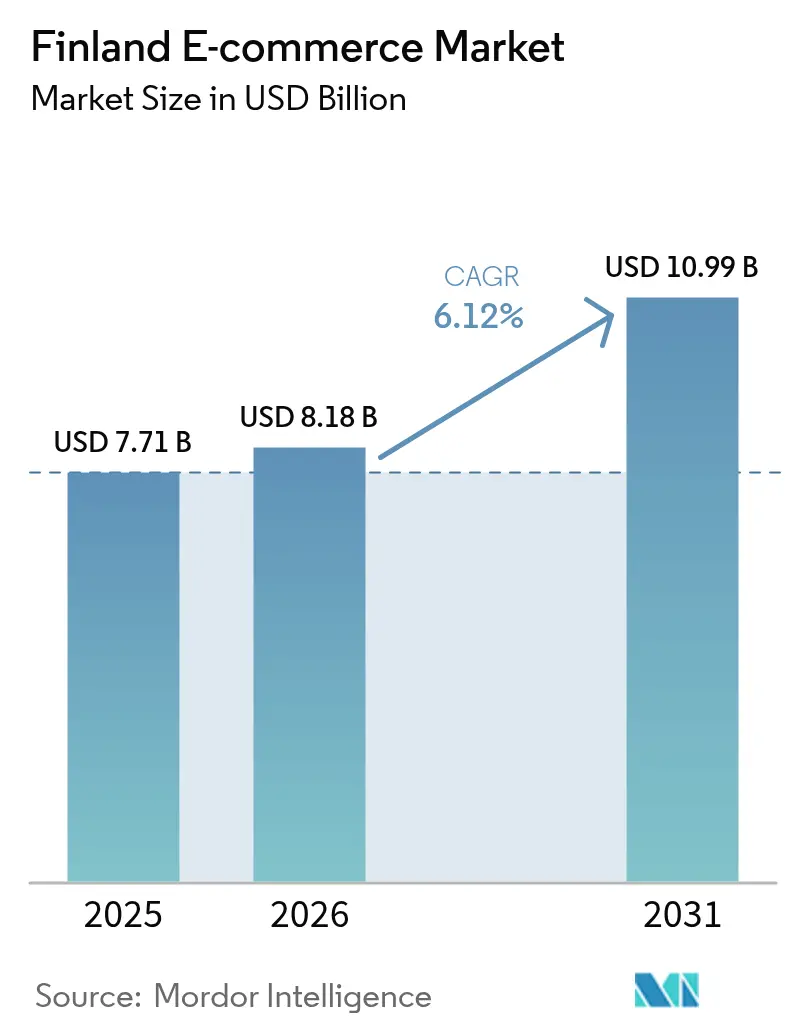

| Base Year Market Size (2025) | USD 7.71 Billion |

| Market Size (2026) | USD 8.18 Billion |

| Market Size (2031) | USD 10.99 Billion |

| Growth Rate (2026 - 2031) | 6.12% CAGR |

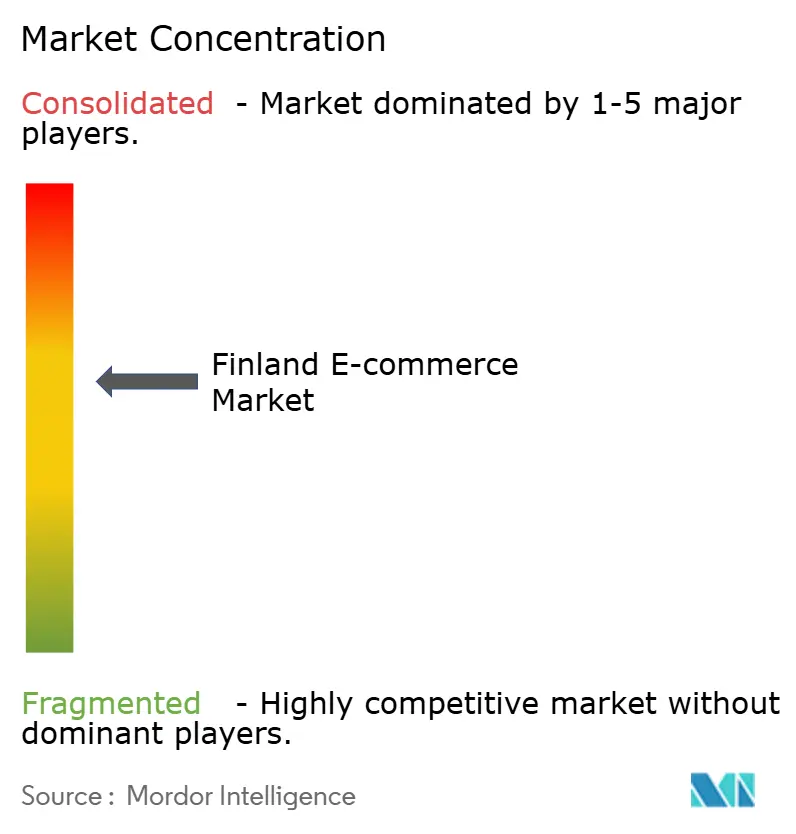

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Finland E-commerce Market Analysis by Mordor Intelligence

Finland e-commerce market size in 2026 is estimated at USD 8.18 billion, growing from 2025 value of USD 7.71 billion with 2031 projections showing USD 10.99 billion, growing at 6.12% CAGR over 2026-2031. Strong digital infrastructure, high card penetration, and a EUR 10 million (USD 10.9 million) public-sector AI program are reinforcing consumer confidence in online transactions.[1]Government of Finland, “AI Integration Budget Announcement,” govinsider.asia MobilePay and similar apps are normalizing instant payments, while automated parcel lockers remove logistics friction in sparsely populated regions. Cross-border shopping remains influential as 47% of Finns buy from foreign sites to access lower prices and wider assortments.[2]Paytrail, “E-commerce in Finland 2024,” paytrail.com Competitive intensity grows as Zalando acquires ABOUT YOU, while local leader Verkkokauppa.com prioritizes margins over volumes amid subdued consumer sentiment.

Key Report Takeaways

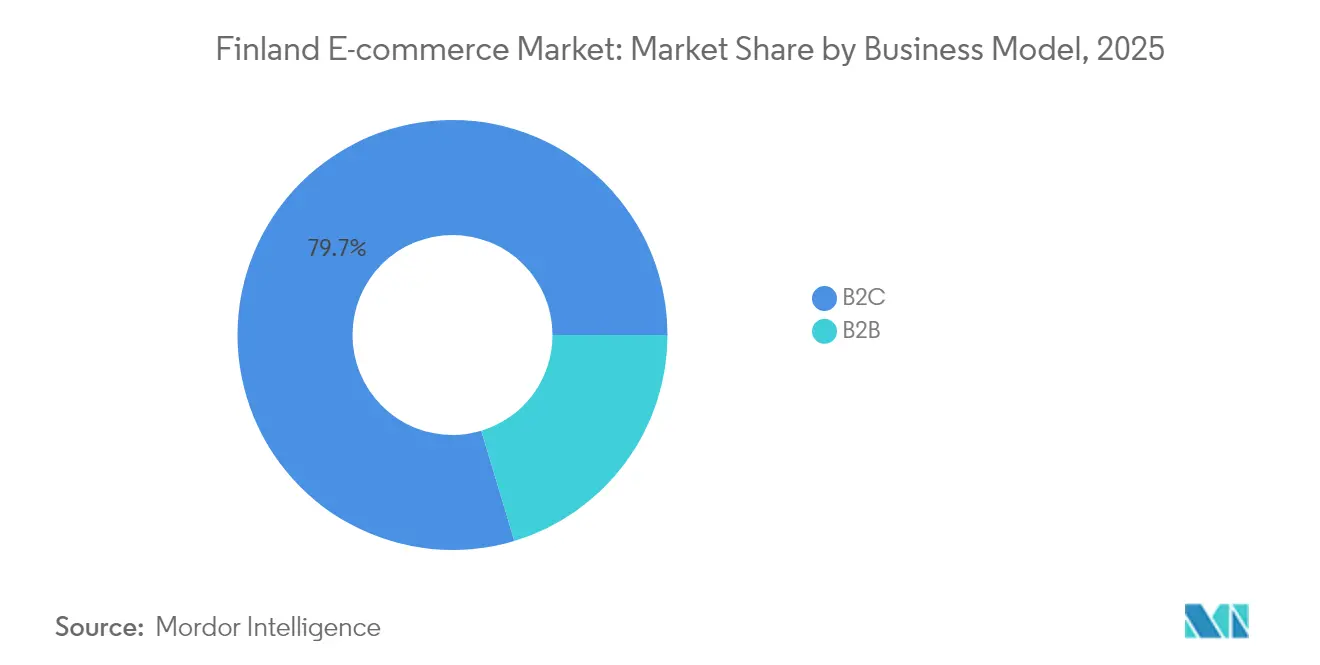

- By business model, B2C transactions led with 79.65% revenue share in 2025; B2B is projected to expand at an 8.12% CAGR through 2031.

- By device type, smartphones captured 68.10% of the Finland e-commerce market share in 2025, while smartphones are advancing at a 7.10% CAGR through 2031.

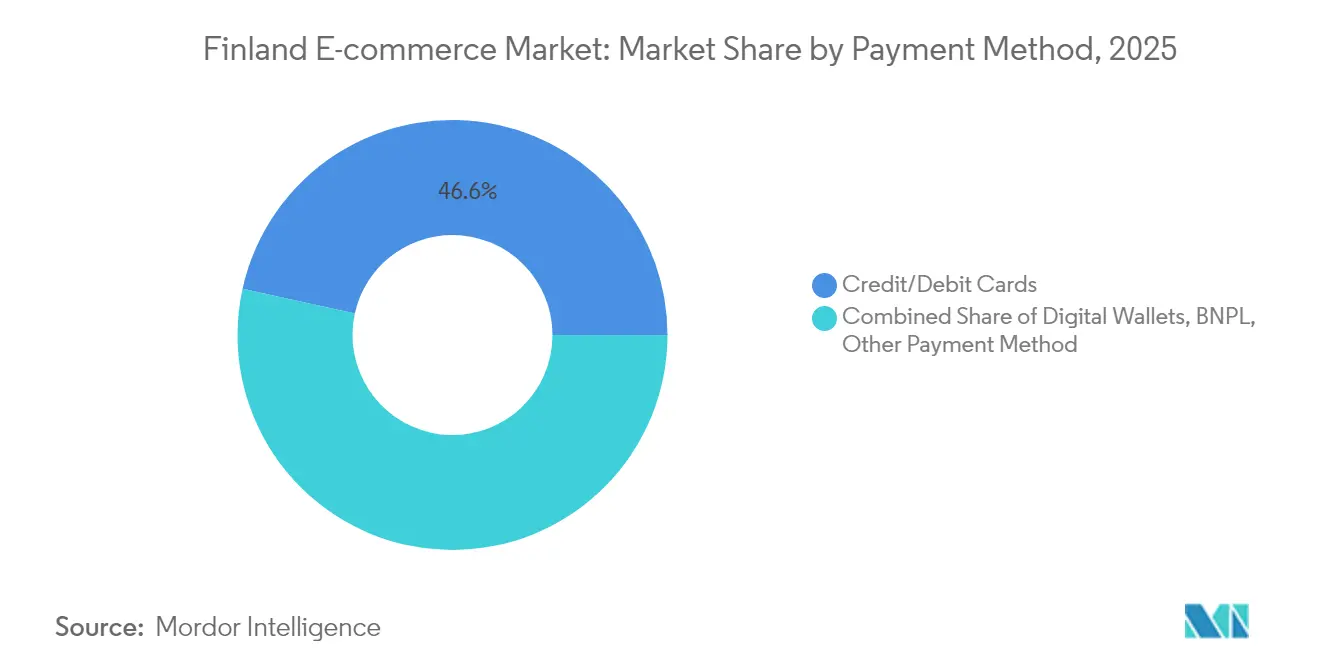

- By payment method, credit and debit cards commanded 46.55% share of the Finland e-commerce market size in 2025; BNPL solutions are growing at a 9.66% CAGR to 2031.

- By B2C product category, fashion & apparel held 24.72% revenue share in 2025; food & beverages is forecast to rise at an 11.25% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Finland E-commerce Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Widespread Adoption of MobilePay & Other Instant Payment Apps Boosting Conversion Rates | +1.2% | National, with higher penetration in urban areas | Short term (≤ 2 years) |

| Rapid Expansion of Automated Parcel Locker Networks in Sub-Arctic & Rural Regions | +0.8% | National, with focus on rural and sub-Arctic regions | Medium term (2-4 years) |

| Government-Led Digital Public Services Normalising Online Transactions | +0.9% | National | Medium term (2-4 years) |

| Nordic Consumer Preference for Sustainable "Re-commerce" Platforms | +0.7% | National, with spillover to Nordic region | Long term (≥ 4 years) |

| German & Swedish Cross-Border Pure-Plays Increasing SKU Variety | +0.6% | National, with cross-border implications | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Widespread Adoption of MobilePay & Other Instant Payment Apps Boosting Conversion Rates

Instant payments now underpin friction-free checkouts, helping merchants cut abandonment and processing fees as online banking still accounts for 55% of preferences but skews older.[3]Stripe, “2024 Nordic Payments Report,” stripe.com The EUR 100 million (USD 109 million) digitalization fund upgrades payment rails and encourages merchant acceptance. This momentum accelerates the Finland e-commerce market beyond card-centric constraints, lifting overall conversion rates and enlarging merchant addressable volumes.

Rapid Expansion of Automated Parcel Locker Networks in Sub-Arctic & Rural Regions

Posti operates nearly 2,000 lockers, ensuring secure, weather-proof pickup even at −20 °C. Unified Nordic locker protocols rolling out in 2025 simplify cross-border fulfilment and cut rural delivery costs. With 90% notification response rates, lockers broaden regional access and unlock incremental demand that previously lacked last-mile reliability.

Government-Led Digital Public Services Normalising Online Transactions

Nation-wide e-ID, bank ID and mobile ID logins make official tasks digital-first, transferring trust to retail platforms and lifting online engagement among seniors and late adopters. Inclusive help desks secure adoption, while a EUR 10 million (USD 10.9 million) AI budget raises user-experience benchmarks that spill into private commerce.

Nordic Consumer Preference for Sustainable “Re-commerce” Platforms

Fifty-seven percent of Finnish shoppers weigh environmental impact, spurring circular services like Emmy-Inrego’s clothing-for-electronics exchange. Verkkokauppa.com’s “Vaihtokauppa” trade-in plus K-Group’s refurbishment pilots embed reuse models, differentiating offerings while capturing value from returned goods.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Return Rates in Fashion Category Driving Reverse-Logistics Costs | -0.6% | National, with higher impact in urban areas | Short term (≤ 2 years) |

| Stringent EU VAT One-Stop-Shop (OSS) Compliance Burden for SMEs | -0.4% | National, with cross-border implications | Medium term (2-4 years) |

| Relatively Small Domestic Addressable Market Limiting Economies of Scale | -0.3% | National | Long term (≥ 4 years) |

| Same-Day Delivery Expectations Escalating Fulfilment Cost Base | -0.5% | Urban areas, with spillover to suburban regions | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Return Rates in Fashion Category Driving Reverse-Logistics Costs

Returns near 40% hurt margins by elevating inspection, repackaging, and disposal expenses. Retailers deploy AI-based sizing tools, customer-profiling engines, and consolidated pickup programs to curb repeated returns while preserving customer goodwill.

Stringent EU VAT One-Stop-Shop (OSS) Compliance Burden for SMEs

From January 2025, Finnish sellers surpassing EUR 100,000 (USD 109,000) in EU-wide turnover must file detailed cross-border VAT, prompting extra accounting spend and deterring nascent exporters. Software upgrades and tax advisory fees compress SME working capital, slowing their international scaling within the Finland e-commerce market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Business Model: B2B Digitization Accelerates Despite B2C Dominance

In 2025, B2C held 79.65% of revenue, underscoring its anchor role in the Finland e-commerce market. However, an 8.12% CAGR positions B2B as the lead growth engine as Finnish enterprises automate procurement via mandatory European e-invoicing standards. Kesko illustrates this pivot: 55% of group sales now stem from direct B2B channels that use AI demand-planning tools to fully align inventory and retailer forecasts.

B2C momentum stabilizes through frictionless payments and dense parcel networks, yet discretionary fashion spend faced softness in 2024 amid inflation worries. B2B adoption accelerates when wholesalers deploy machine-learning models that shrink stock-outs and exposure to price volatility—features that resonate with industrial buyers seeking cost control and resilience.

By Device Type: Mobile Commerce Dominance Reinforces Urban-Rural Digital Divide

Smartphones accounted for 68.10% of transactions in 2025, underpinning the Finland e-commerce market, and continue to grow at a 7.10% CAGR as 5G becomes universal. Desktop use remains prevalent in corporate buying and high-ticket items requiring deeper specification comparisons, while tablets and smart TVs serve niche entertainment transactions.

Verkkokauppa.com saw online sales hit 66% of turnover and a 33% surge in express delivery orders-signals that mobile shoppers expect near-instant fulfilment. Remote regions ride mobile networks to bypass limited fixed broadband; nonetheless, sparse delivery points necessitate locker rollouts and community pickup hubs.

By Payment Method: BNPL Disruption Challenges Traditional Card Dominance

Cards still hold 46.55% share, yet BNPL grows 9.66% CAGR, reflecting consumers’ search for budget flexibility in a high-inflation setting. Digital wallets benefit from biometric authentication and privacy controls prized by Finnish users.

Helsinki-based Starcart, freshly licensed as a payment institution, blends AI price discovery with BNPL options across 200+ stores, signaling how fintech entrants can diversify the Finland e-commerce industry’s payment stack. Card issuers respond with installment add-ons and loyalty accelerators to retain share.

By B2C Product Category: Food & Beverages Growth Outpaces Fashion Leadership

Fashion remains top at 24.72% share but combats high returns and eco scrutiny. Meanwhile, food & beverages is set to scale 11.25% CAGR as urban professionals embrace 15-minute “quick commerce” for groceries and meals. Electronics shrink from 16% to 7% of total retail spend as consumers delay upgrades.

Wolt’s new gifting module widens its basket mix beyond meals, a play at lifestyle positioning that lifts average order values. S-Group’s rollout of electronic shelf labels automates price elasticity tests, balancing margin and demand in both fresh and ambient assortments.

Geography Analysis

Southern urban centers-Helsinki, Espoo, and Vantaa-generate a disproportionate share of the Finland e-commerce market thanks to dense locker networks and ubiquitous same-day delivery. Parcel volumes per capita in Greater Helsinki outstrip national averages as commuters rely on click-and-collect convenience.

Northern and sub-Arctic regions display higher mobile-only engagement since physical retail density is lower. Posti’s 2,000 automated lockers tighten service coverage, mitigating weather-linked disruptions and reducing average rural delivery time by 1.4 days. Locker deployment elevates customer satisfaction scores in Lapland and Kainuu provinces where home delivery can be cost-prohibitive.

Cross-border influences remain strong: 47% of Finnish shoppers transact abroad, mainly with Swedish and German e-tailers offering broader assortments and price advantages. PostNord’s service harmonization cuts cross-Nordic transit times by up to 18 hours and provides a consistent parcel-tracking interface. Adoption of the EU Import One-Stop-Shop grew VAT declarations to EUR 26.3 billion (USD 30.8 billion) in 2023, highlighting Finland’s integration into the wider European e-commerce space.

Competitive Landscape

The Finland e-commerce market shows moderate concentration, with Verkkokauppa.com edging peers despite a 7% revenue dip to EUR 467.8 million (USD 510 million) in 2024 because of a rigorous cost-optimization playbook that lifted operating margin. Meanwhile, Zalando’s EUR 6.50 (USD 7.10) per-share bid for ABOUT YOU seeks EUR 100 million (USD 109 million) in synergies, promising faster Nordic deliveries and deeper assortment breadth.

Technology uptake distinguishes winners. Kesko’s predictive analytics shrink food waste, preserving margins, whereas S-Group’s electronic shelf labels automate real-time price changes across 100+ stores. Fintech-powered platforms such as Starcart use AI to curate the cheapest combined basket across multiple retailers, raising customer stickiness and challenging traditional marketplaces.

M&A appetite remains high as domestic players weigh regional scale benefits against the cost of last-mile expansion. Beyond fashion consolidation, niche acquisitions target logistics tech, returns management, and sustainability solutions-areas critical to sustained profitability in the Finland e-commerce market.

Finland E-commerce Industry Leaders

Verkkokauppa.com

Motonet Oy

Zalando SE

Gigantti Oy (Elkjøp)

K-Ruoka (Kesko Oyj)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Aibidia raised USD 28 million Series B to extend its AI-driven transfer-pricing suite to the US, signaling confidence in exportable Finnish tax-tech and diversifying local fintech talent toward B2B SaaS growth strategies.

- May 2025: Wolt introduced a gifting function so users can send curated items from local stores, expanding beyond food into lifestyle retail and boosting average order values.

- January 2025: PostNord unified its parcel-locker and service-point standards across the Nordics to streamline cross-border fulfilment and improve delivery predictability.

- November 2024: Klevu secured USD 12 million to deepen AI search and merchandising tools, underlining the premium on conversion-rate optimization technologies in the Finland e-commerce market.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the Finnish e-commerce market as every monetary transaction in which residents purchase physical goods or digitally delivered services over the internet on any device, whether the order is fulfilled locally or cross-border. Value is stated in current U.S. dollars. Mordor Intelligence values the market at USD 7.71 billion for 2025.

Scope Exclusion: pure online banking, in-game micro-payments, and business-to-government procurement are outside this valuation.

Segmentation Overview

- By Business Model

- B2C

- B2B

- By Device Type

- Smartphone / Mobile

- Desktop and Laptop

- Other Device Types

- By Payment Method

- Credit / Debit Cards

- Digital Wallets

- BNPL

- Other Payment Method

- By B2C Product Category

- Beauty and Personal Care

- Consumer Electronics

- Fashion and Apparel

- Food and Beverages

- Furniture and Home

- Toys, DIY and Media

- Other Product Categories

Detailed Research Methodology and Data Validation

Primary Research

Interviews with online retail managers, parcel locker operators, fintech engineers, and consumer rights officials across Helsinki, Tampere, and Oulu helped us confirm cross-border purchase share, mobile checkout conversion, and return ratios. Two short online polls captured shopper frequency, basket size, and payment preferences across urban and rural cohorts.

Desk Research

Mordor analysts began with official dashboards from the Bank of Finland, Statistics Finland, and the Finnish Commerce Federation, which outline payment flows, buyer counts, and parcel volumes. Trend color on last mile behavior came from Posti's parcel locker index, while Eurostat and the U.S. Trade.gov country guide provided wider consumer spending context. To tighten commercial layers, we tapped D&B Hoovers for retailer financials and Dow Jones Factiva for transaction news; ECDB's open sample clarified order values and device splits. The sources listed are illustrative, and many other public datasets and regulatory bulletins supported evidence gathering.

Market Sizing and Forecasting

The 2024-2025 baseline was rebuilt top down by reconciling national card and credit transfer outflows with customs adjusted parcel statistics, then cross checked through sampled retailer revenue roll ups and order counts. Key variables like internet penetration, smartphone share of checkouts, parcel locker pickup share, average order value, cross-border purchase ratio, and digital wallet adoption anchor the base year. Forecasts to 2030 employ multivariate regression tied to GDP per capita and inflation; any bottom up gaps are bridged using average selling prices agreed during primary calls.

Data Validation and Update Cycle

Outputs move through variance filters and senior review; anomalies trigger re-contact with source experts before sign off. We refresh the model each year and publish interim revisions when material regulatory or macro shocks arise.

Why Mordor's Finland E-commerce Baseline Inspires Confidence

Published estimates often diverge because firms choose different scopes, currencies, and refresh cadences, which can leave decision makers unsure of the true opportunity.

Key gap drivers include whether services such as travel are counted, the year chosen for the base figure, reliance on single secondary feeds, and the extent of primary validation. By anchoring on verifiable payment data and continuously vetting assumptions, Mordor Intelligence delivers a balanced midpoint that planners can trust.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 7.71 B (2025) | Mordor Intelligence | - |

| USD 7.07 B (2025) | Regional Consultancy A | Counts travel bookings and relies on a single secondary dataset |

| USD 6.74 B (2024) | Industry Data Platform B | Goods only scope with limited primary validation |

These comparisons show that careful scope selection, primary cross checks, and annual refreshes let Mordor present the most dependable baseline for Finnish e-commerce planning.

Key Questions Answered in the Report

What is the current Finland e-commerce market size and projected growth?

The market is valued at USD 8.18 billion in 2026 and is forecast to grow at a 6.12% CAGR to USD 10.99 billion by 2031.

Which segment is expanding fastest within the Finland e-commerce market?

B2B e-commerce is advancing at an 8.12% CAGR as enterprises accelerate digital procurement.

How dominant is mobile commerce in Finland?

Smartphones account for 68.10% of online transactions and continue to grow at 7.10% CAGR, reflecting a mobile-first consumer base.

Why are Buy Now Pay Later services gaining traction?

BNPL options are expanding at 9.66% CAGR as consumers seek flexible budgeting tools amid inflation pressures.

What regulatory change poses challenges for Finnish SMEs selling abroad?

From January 2025, SMEs exceeding EUR 100,000 (USD 117212.68) EU sales must comply with the VAT One-Stop-Shop regime, adding cross-border tax complexity.

How are logistics innovations impacting rural Finnish shoppers?

Nearly 2,000 automated parcel lockers cut delivery times and costs, increasing satisfaction and access in rural and sub-Arctic regions.

Page last updated on: