Metrology Services Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

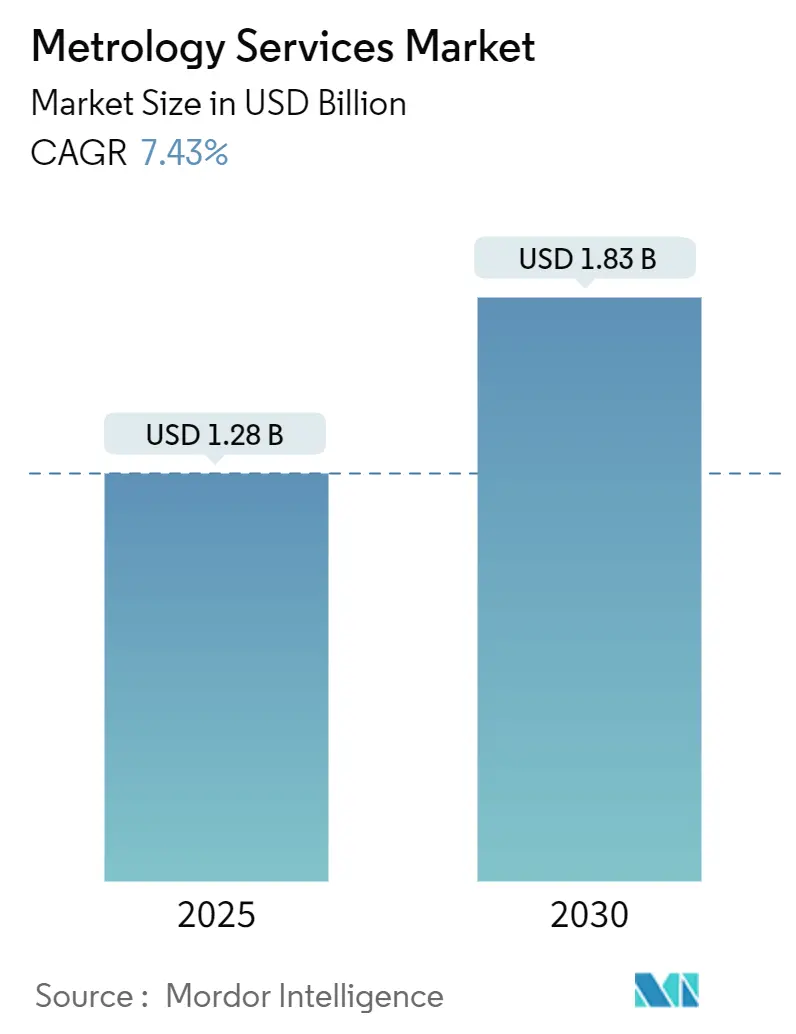

| Market Size (2025) | USD 1.28 Billion |

| Market Size (2030) | USD 1.83 Billion |

| Growth Rate (2025 - 2030) | 7.43% CAGR |

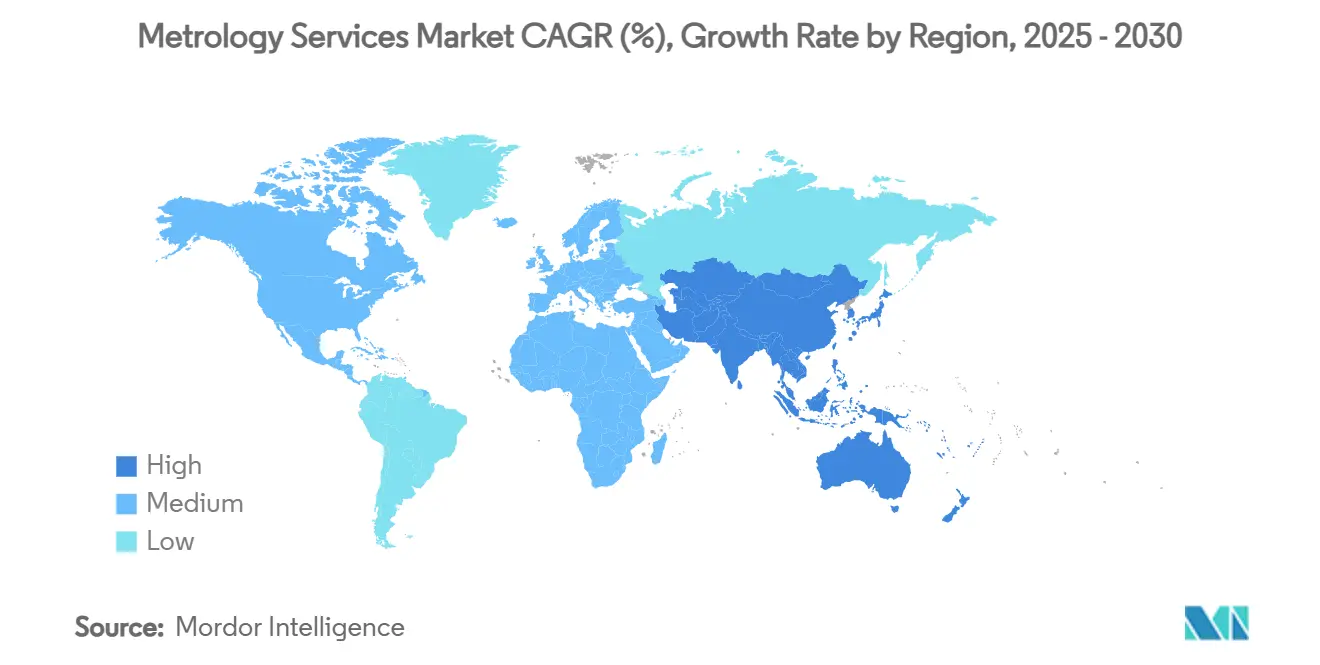

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

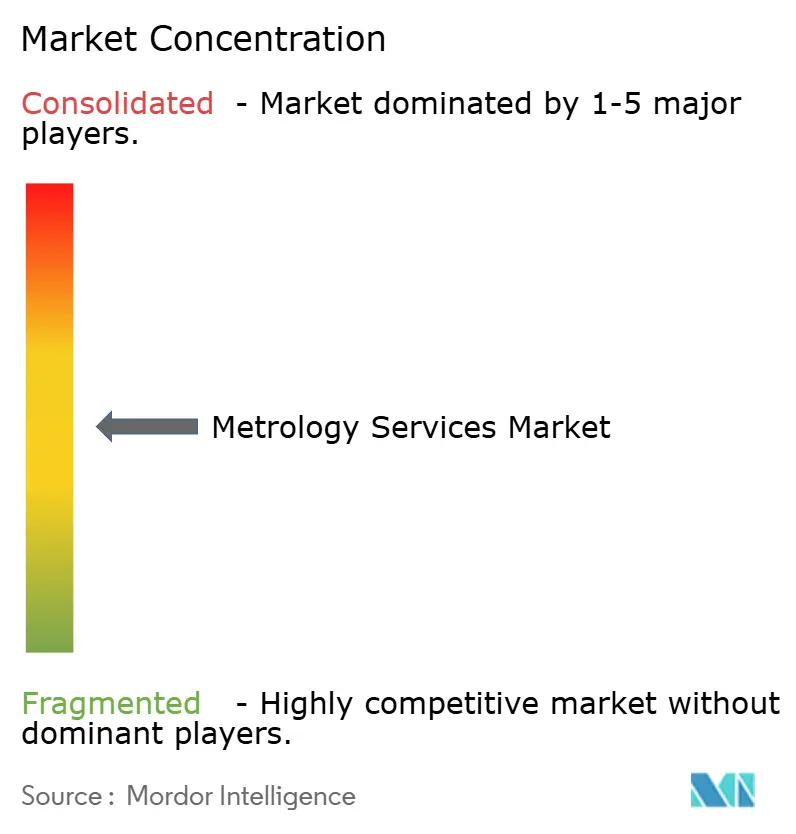

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Metrology Services Market Analysis by Mordor Intelligence

The metrology services market size stands at USD 1.28 billion in 2025 and is forecast to reach USD 1.83 billion by 2030, advancing at a 7.43% CAGR. The expansion reflects manufacturers’ shift from episodic calibration toward digitally integrated, real-time measurement that underpins Industry 4.0 production. Accelerated aerospace MRO recovery, tighter FDA medical-device rules, and growing reliance on digital twins pull metrology from a cost-center to a competitiveness lever.[1]Oliver Wyman, “Aviation MRO In Demand,” oliverwyman.com Manufacturers in Asia-Pacific add momentum as China and India scale precision factories, while portable scanning technologies promise faster returns on investment than legacy CMM installations. Competitive attention has moved from standalone hardware to cloud-connected software suites, driving consolidation such as Hexagon’s Geomagic purchase. Persistent risks include a shortage of certified dimensional-metrology professionals and rising cybersecurity exposure in connected shop-floor systems.[2]National Institute of Standards and Technology, “Enabling the Digital Thread,” nist.gov

Key Report Takeaways

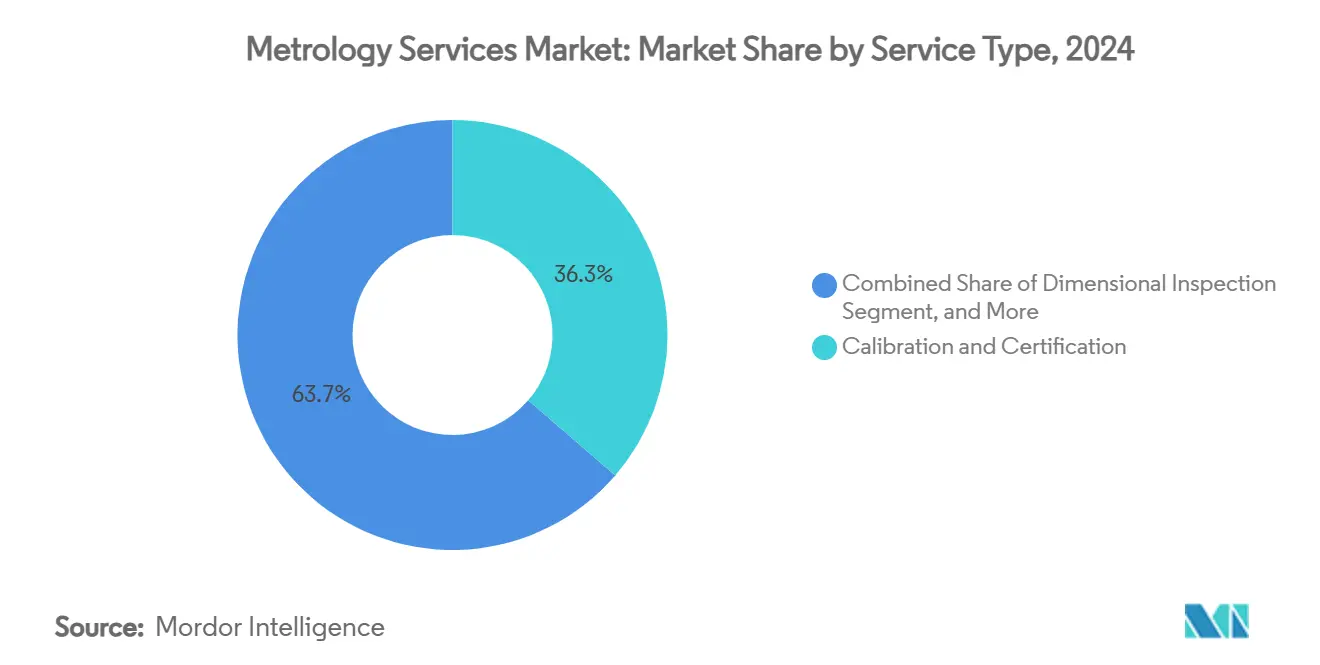

- By service type, Calibration and Certification led with 36.34% of the metrology services market share in 2024, while 3-D Scanning/Optical Digitizer services are projected to grow at an 8.34% CAGR to 2030.

- By equipment type, Coordinate Measuring Machines accounted for 41.89% of the metrology services market size in 2024, whereas Laser Trackers and Scanners are poised for a 9.12% CAGR through 2030.

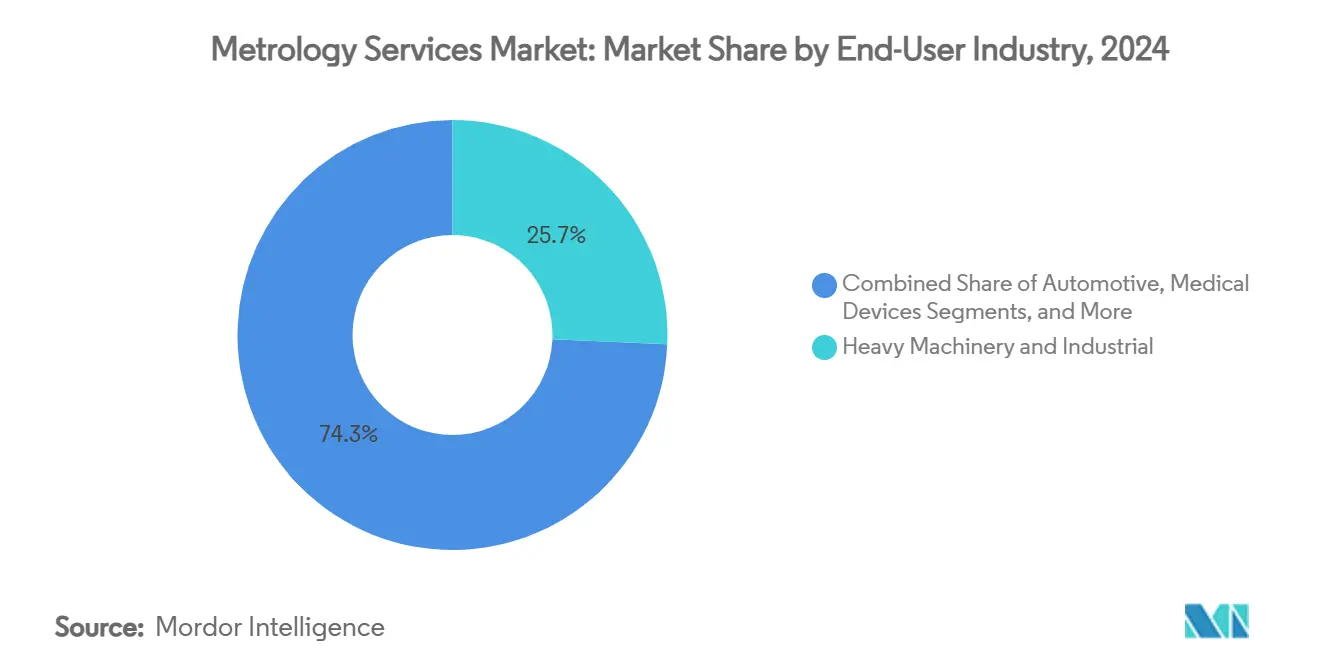

- By end-use industry, Heavy Machinery held 26.45% of the metrology services market size in 2024, but Medical Devices will advance at a 7.98% CAGR between 2025-2030

- By measurement location, Off-site Laboratory Services controlled 43.78% of the metrology services market share in 2024, yet On-site/In-process services are forecast to climb at an 8.67% CAGR to 2030.

- By geography, North America commanded 39% revenue share in 2024; APAC is projected to record the quickest expansion at an 8.39% CAGR through 2030.

Global Metrology Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing demand for 100% in-process quality control (Industry 4.0) | +1.6% | Global — APAC leads | Medium term (2–4 years) |

| Tightening international calibration and traceability regulations | +0.8% | North America and Europe | Short term (≤ 2 years) |

| Rapid uptake of 3-D scanning and portable CMM outsourcing | +1.2% | Global — especially APAC | Medium term (2–4 years) |

| Resurgence of aerospace MRO volumes post-2024 | +0.9% | North America, Europe, India | Short term (≤ 2 years) |

| Digital-twin-enabled predictive calibration contracts | +0.7% | U.S., Germany, Japan | Long term (≥ 4 years) |

| Subscription “Metrology-as-a-Service” for SMEs | +0.6% | Developed markets | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Growing demand for 100 % in-process quality control (Industry 4.0)

Real-time quality assurance integrates measurement directly into production, replacing batch inspection with continuous data capture. BENTELER’s Vigo plant inspects 5 million 3-D points per part without contact, shrinking cycle times while raising precision. AI-driven predictive maintenance now accompanies these systems, and 64 % of MROs state their AI investments meet expectations. ANSI-approved QIF (ISO 23952:2020) enables seamless data flow among engineering, manufacturing, and quality, reinforcing traceability. NIST’s Digital Thread work further codifies interoperable data structures. These advances create fresh revenue streams for providers able to bundle software, sensors, and analytics rather than one-off calibrations.

Tightening international calibration and traceability regulations

FDA rules under 21 CFR Parts 11 and 820 demand electronic calibration records and NIST traceability, pushing medical-device firms toward accredited metrology partners. Aerospace suppliers must meet AS9100 trace-chain mandates, with Tektronix noting that outsourcing eases audit burdens. Digital Calibration Certificates shift compliance toward machine-readable outputs, aligning with ISO 10012 measurement-management requirements. Australia’s CASA illustrates sector-specific enforcement by insisting on calibration evidence for aviation equipment. Together, these rules raise baseline service demand and favor vendors with multi-domain accreditation.

Rapid uptake of 3-D scanning and portable CMM outsourcing

Portable laser scanners cost roughly USD 100,000 versus USD 200,000 plus USD 55,000 in infrastructure for traditional CMMs, yielding faster ROI for SMEs. FARO’s Leap ST adds five scanning modes for diverse geometries. Annual maintenance costs are similar, but infrastructure savings tip the scales toward handheld devices. Hexagon’s battery-powered Leica AT500 operates wirelessly in harsh shops.[3]Hexagon, “Leica Absolute Tracker AT500,” hexagon.com Korea’s optical frequency-comb interferometry reaches 0.34 nm precision in 25 µs, signaling the next leap in portable accuracy.[4]National Research Council of Science and Technology, “Optical Frequency Comb Integration,” phys.org These innovations accelerate outsourcing to specialists who own such assets.

Resurgence of aerospace MRO volumes post-2024

Aviation MRO climbed back to USD 114 billion in 2024 and is set for 2.7% yearly growth to 2035. India’s MRO revenue is on track for 50 % growth by 2026 amid fleet expansion. Laser trackers cut inspection times up to 75 % on engines and landing gear. Near-line 3-D scanners feed instant repair data for safety compliance. Ongoing material shortages and a looming 19 % mechanic shortfall intensify demand for external metrology expertise that can offset labor gaps.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High total cost of precision instruments and accreditation | –0.9% | Global — SMEs hit hardest | Short term (≤ 2 years) |

| Shortage of certified dimensional-metrology professionals | –0.5% | North America and Europe, spreading to APAC | Medium term (2–4 years) |

| Cyber-security and IP-leak risks in connected shop-floor metrology | –0.3% | Advanced regions | Medium term (2–4 years) |

| Lack of universal data-interoperability standards | –0.2% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High total cost of precision instruments and accreditation

Capital outlays for high-end equipment plus ISO/IEC 17025 accreditation deter new entrants. NIST’s fee schedule shows sizable charges for advanced calibrations, while laboratories must fund environmental controls and skilled staff. Alliance Calibration notes the procedural intensity of international standards audits. Many SMEs struggle to absorb these costs, echoing World Bank findings on conformity barriers to global trade. NIST’s robotics measurement program helps smaller firms evaluate affordable systems. Nevertheless, financial hurdles remain a drag until hardware prices drop or subscription models scale.

Shortage of certified dimensional-metrology professionals

Modern systems pair mechanical sensors with complex software, yet training pipelines lag. Renishaw’s 5-axis REVO and MODUS platform demand programming and analytics skills beyond traditional gauge blocks. ZEISS has expanded remote courses to fill gaps for FDA validation services. NIST collaborates with academia on curricula for smart factories. Without an influx of multi-disciplinary talent, service capacity risks bottlenecks — a concern already visible in North America and Europe.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Digital Integration Drives Scanning Growth

The metrology services market size for Calibration and Certification stood at USD 463 million in 2024, translating to 36.34% of revenue. Real-time production goals, however, propel 3-D Scanning/Optical Digitizer services toward an 8.34% CAGR, as portable scanners overcome cost and infrastructure barriers. FARO’s Leap ST showcases high-throughput handheld functionality, while AI-assisted analytics unlock predictive insights beyond dimension checks. Dimensional Inspection remains essential for aerospace MRO as fleets age, whereas GD&T consulting grows on the back of stricter tolerance regimes.

Outsourcing gains ground as SMEs sidestep capex by paying only for usage. Reverse engineering and simulation demand expand alongside digital twin adoption. Providers embedding cloud dashboards and machine-learning fault detection cement stickier contracts, demonstrating how data stewardship outvalues mere measurement in the evolving metrology services market.

By Equipment Type: Portability Reshapes Market Dynamics

Coordinate Measuring Machines delivered 41.89% of 2024 revenue, yet volumetric growth now tilts toward Laser Trackers and Scanners at 9.12% CAGR. Hexagon’s wireless AT500 extends metrology to harsh, temperature-variant environments, shortening set-up time by eliminating cabling. Laser trackers are popular in aerospace overhaul bays where weight and reach matter. Optical and video systems serve semiconductor fabs, and form-surface technologies address high-precision gears.

Next-generation accuracy is emerging from optical frequency-comb interferometry, hitting sub-nanometer resolution — a capability expected to cascade into portable devices by 2030. Integration platforms such as ZEISS CONNECTED QUALITY orchestrate disparate sensors into unified data lakes, reinforcing the shift from hardware-centric to software-defined value capture in the metrology services market.

By End-Use Industry: Medical Devices Accelerate Despite Heavy-Machinery Dominance

Heavy Machinery and General Industry contributed 26.45% of revenue in 2024, anchored by construction-equipment OEMs scaling capacity in Asia-Pacific. Yet Medical Devices will post the fastest 7.98% CAGR, as FDA rules elevate calibration rigor and traceability. ZEISS’s validation service packages illustrate tailored offerings for clean-room environments demanding sub-micron assurance. Automotive adoption rises with EV drivetrain tolerances, while Aerospace remains linked to MRO cycles calling for high-precision laser tracker verification.

Semiconductor lines seek nanometer-scale metrology, spurring investment in optical and X-ray systems. Energy producers require turbine shaft alignment under thermal load, a niche filled by mobile laser tracker crews. The expanding medical-device footprint in India, forecast to reach USD 280 billion value by 2025, suggests durable demand for biomedical measurement expertise

By Measurement Location: On-site Services Transform Traditional Models

Off-site laboratories still represented 43.78% of 2024 turnover, buoyed by legacy accreditation and environmental control benefits. Nonetheless, on-site and in-process services will outgrow labs at 8.67% CAGR, because real-time feedback cuts scrap and logistics. ABB’s vision-system deployment inspects every part without halting production, spotlighting what customers now expect.

Hybrid mobile labs combine traceability with field convenience; battery-powered scanners help reach large forgings or turbine casings. Hexagon’s Digital Factory replicates plant layouts, allowing remote experts to validate measurements virtually. Long-term, NIST’s on-machine measurement research hints at universal sensor fusion directly on CNC spindles, signaling a future where measurement ceases to be a separate step.

Geography Analysis

North America controlled 39% of 2024 revenue, supported by aerospace MRO rebound, FDA oversight, and advanced manufacturing investments. Hexagon’s partnership with Elliott Matsuura doubled Canadian support coverage, reflecting sustained demand for integrated hardware-software packages. Supply-chain bottlenecks and a forecast 19% mechanic shortfall by 2028 could squeeze capacity, yet NIST’s cybersecurity and calibration programs offer regional competitive safeguards.

Asia-Pacific is the fastest-growing region, with the metrology services market expected to expand at 8.39% CAGR through 2030. India’s projected 45 billion-rupee MRO sector by 2026 and China’s high-precision machining clusters drive volume. Government incentives, reduced GST on aviation parts, and rapid infrastructure build-out favor local uptake of scanning and laser-tracker services. Trescal’s Thailand acquisition underscores regional consolidation opportunities.

Europe registers steady growth on the back of electric-vehicle programs and stringent ISO requirements. Germany advances integrated metrology within smart factories, while UK precision shops adopt 5-axis CMMs to remain globally competitive. South America and the Middle East are emerging plays; despite economic headwinds, industrial diversification and energy projects are unlocking pilot contracts for portable measurement crews.

Competitive Landscape

The metrology services market remains moderately fragmented. Hexagon’s USD 123 million Geomagic acquisition deepens its software stack and signals a pivot toward data-centric growth. Planned spin-off of its Asset Lifecycle Intelligence division will create a pure-play SaaS entity, freeing capital for sensor innovation. ZEISS posted 8% revenue growth to EUR 10.894 billion in 2024 while channeling 15% into R&D, validating an innovation-led race.

FARO Technologies topped Q1 2025 with USD 82.9 million sales and 57% gross margin on the back of the Leap ST handheld scanner, illustrating how nimble product cycles win profits. Service-oriented consolidator Trescal added EUR 12 million sales by buying labs in Brazil, Korea, Thailand, and the US, highlighting room for roll-up plays LABMATE-ONLINE.COM. Adoption of QIF and other interoperability standards favors companies able to harmonize multi-vendor data across cloud platforms, elevating software eco-systems as a new moat

Metrology Services Industry Leaders

Hexagon AB

Carl Zeiss AG

FARO Technologies Inc.

Renishaw plc

Nikon Metrology NV

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: SGS agreed to acquire Applied Technical Services for USD 1,325 million to boost North-American revenue above USD 1.5 billion and capture aerospace, power, and manufacturing cross-sell synergies.

- March 2025: Hexagon initiated plans to spin off its Asset Lifecycle Intelligence division, targeting completion in H1 2026 to sharpen strategic focus and unlock shareholder value.

- February 2025: Nova closed the purchase of Sentronics Metrology GmbH, expanding process-control depth for semiconductor fabs.

- January 2025: FARO launched the Leap ST handheld 3-D device and upgraded CAM2 software, adding five scanning modes for diverse manufacturing needs.

- December 2024: Hexagon bought 3D Systems’ Geomagic software suite for USD 123 million, strengthening scan-to-model automation.

Global Metrology Services Market Report Scope

| Calibration and Certification |

| Dimensional Inspection |

| 3-D Scanning / Optical Digitizer and Scanner |

| GDandT Consulting and Training |

| Reverse Engineering and Simulation |

| Coordinate Measuring Machines |

| Laser Trackers and Scanners |

| Optical and Video Measuring Machines |

| Form and Surface Metrology Systems |

| Automotive |

| Aerospace and Defense |

| Electronics and Semiconductor |

| Energy and Power Generation |

| Medical Devices |

| Heavy Machinery and Industrial |

| Other End-Use Industries |

| Off-site Laboratory Services |

| On-site / In-process (Inline/At-line) |

| Hybrid / Mobile Labs |

| North America |

| South America |

| Europe |

| Asia-Pacific |

| Middle East and Africa |

| By Service Type | Calibration and Certification |

| Dimensional Inspection | |

| 3-D Scanning / Optical Digitizer and Scanner | |

| GDandT Consulting and Training | |

| Reverse Engineering and Simulation | |

| By Equipment Type Serviced | Coordinate Measuring Machines |

| Laser Trackers and Scanners | |

| Optical and Video Measuring Machines | |

| Form and Surface Metrology Systems | |

| By End-Use Industry | Automotive |

| Aerospace and Defense | |

| Electronics and Semiconductor | |

| Energy and Power Generation | |

| Medical Devices | |

| Heavy Machinery and Industrial | |

| Other End-Use Industries | |

| By Measurement Location | Off-site Laboratory Services |

| On-site / In-process (Inline/At-line) | |

| Hybrid / Mobile Labs | |

| By Geography | North America |

| South America | |

| Europe | |

| Asia-Pacific | |

| Middle East and Africa |

Key Questions Answered in the Report

What is the current value of the metrology services market?

The metrology services market size is USD 1.28 billion in 2025 and is projected to reach USD 1.83 billion by 2030.

Which segment is growing fastest within metrology services?

3-D Scanning/Optical Digitizer services are expanding at an 8.34% CAGR because they meet real-time quality control needs.

Why is Asia-Pacific the most attractive growth region?

Manufacturing expansion in China and India, plus a projected 50 % jump in India’s MRO revenue by 2026, drive regional demand for precision measurement.

How are regulations influencing service demand?

FDA 21 CFR Parts 11 and 820 and AS9100 standards require documented, traceable calibrations, pushing manufacturers toward accredited service providers.

What technology trends will shape service offerings by 2030?

Portable laser trackers, AI-enabled analytics, digital calibration certificates, and on-machine measurement solutions will dominate future contract requirements.

Page last updated on: