Methylene Diphenyl Di-isocyanate (MDI) Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

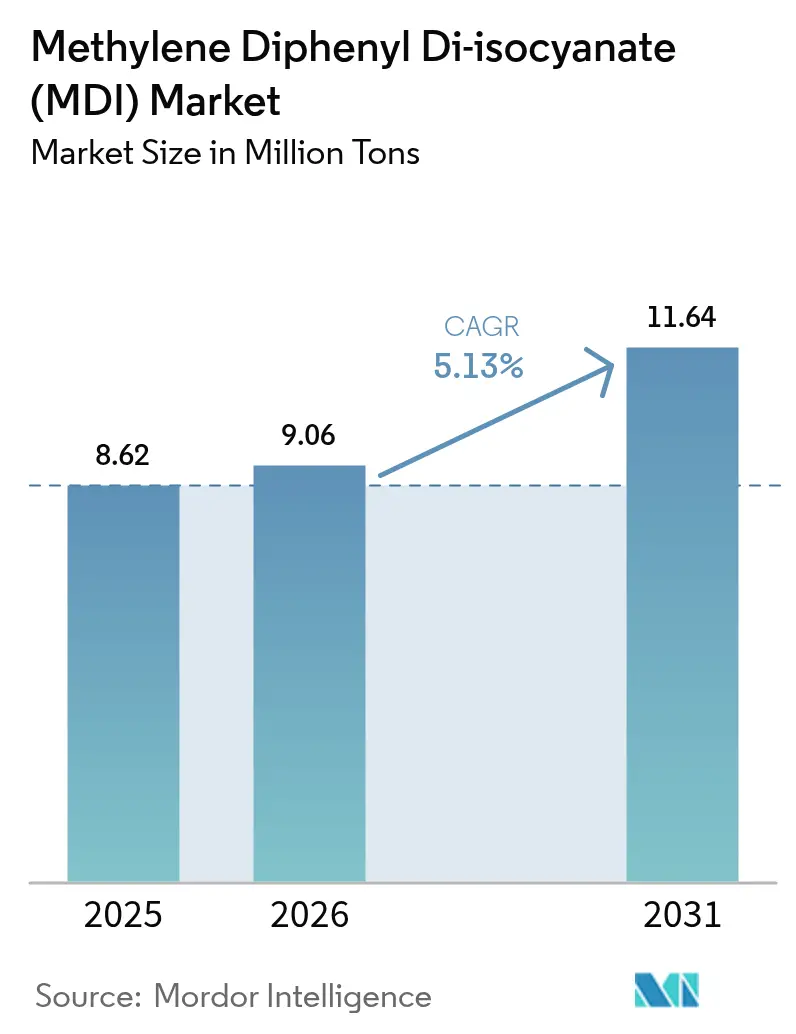

| Market Volume (2026) | 9.06 Million tons |

| Market Volume (2031) | 11.64 Million tons |

| Growth Rate (2026 - 2031) | 5.13% CAGR |

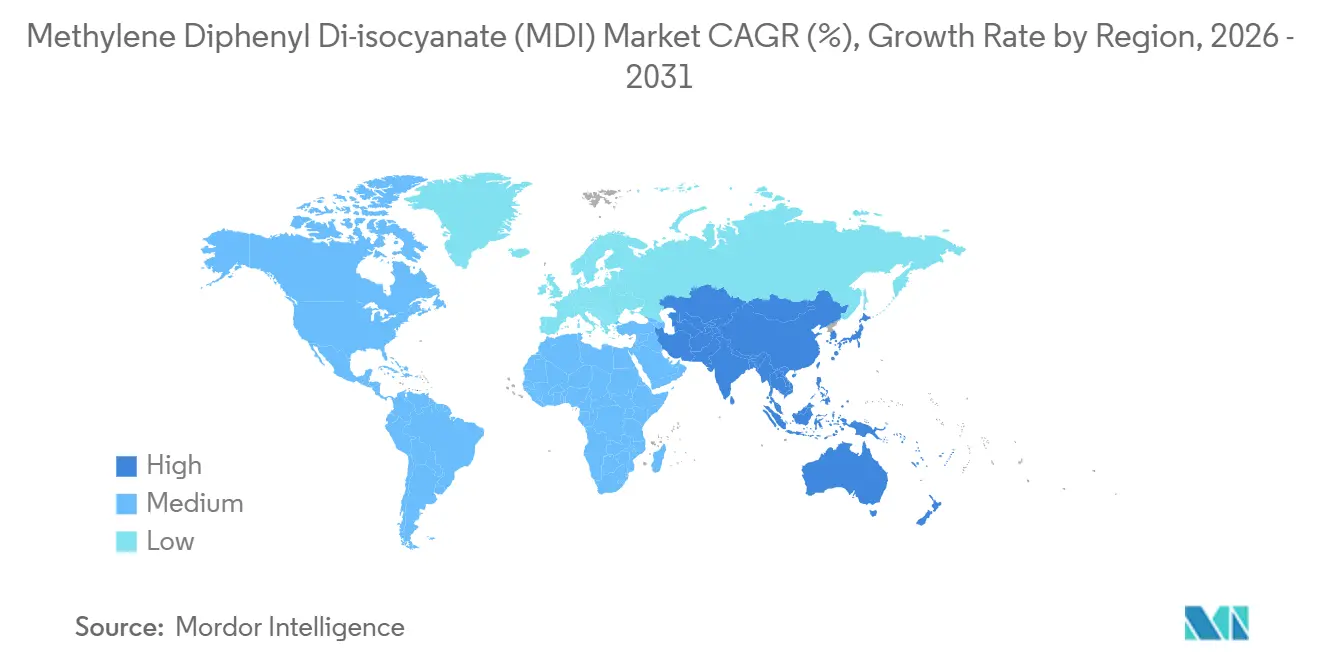

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Methylene Diphenyl Di-isocyanate (MDI) Market Analysis by Mordor Intelligence

The Methylene Diphenyl Di-isocyanate Market size is expected to grow from 8.62 million tons in 2025 to 9.06 million tons in 2026 and is forecast to reach 11.64 million tons by 2031 at a 5.13% CAGR over 2026-2031. Code-driven insulation upgrades, the build-out of pharmaceutical and food cold-chain logistics, and rising electric-vehicle (EV) battery safety requirements are creating a steady pull on demand. Continuous polyisocyanurate (polyiso) boards now dominate commercial roofing because they hit mandatory R-values without adding structural weight, while spray-foam retrofits seal air leaks that account for a significant portion of residential heating losses. Appliance makers have switched to low-GWP hydrocarbon blowing agents, a move that favors polymeric MDI systems able to preserve closed-cell integrity at thinner thicknesses. In parallel, automotive platforms are embedding flame-retardant MDI foams between lithium-ion cells to delay thermal runaway, creating an emerging yet fast-scaling niche. Tight labor markets and stricter worker-exposure limits are nudging fabricators toward low-free-monomer grades that simplify compliance and cut insurance premiums.

Key Report Takeaways

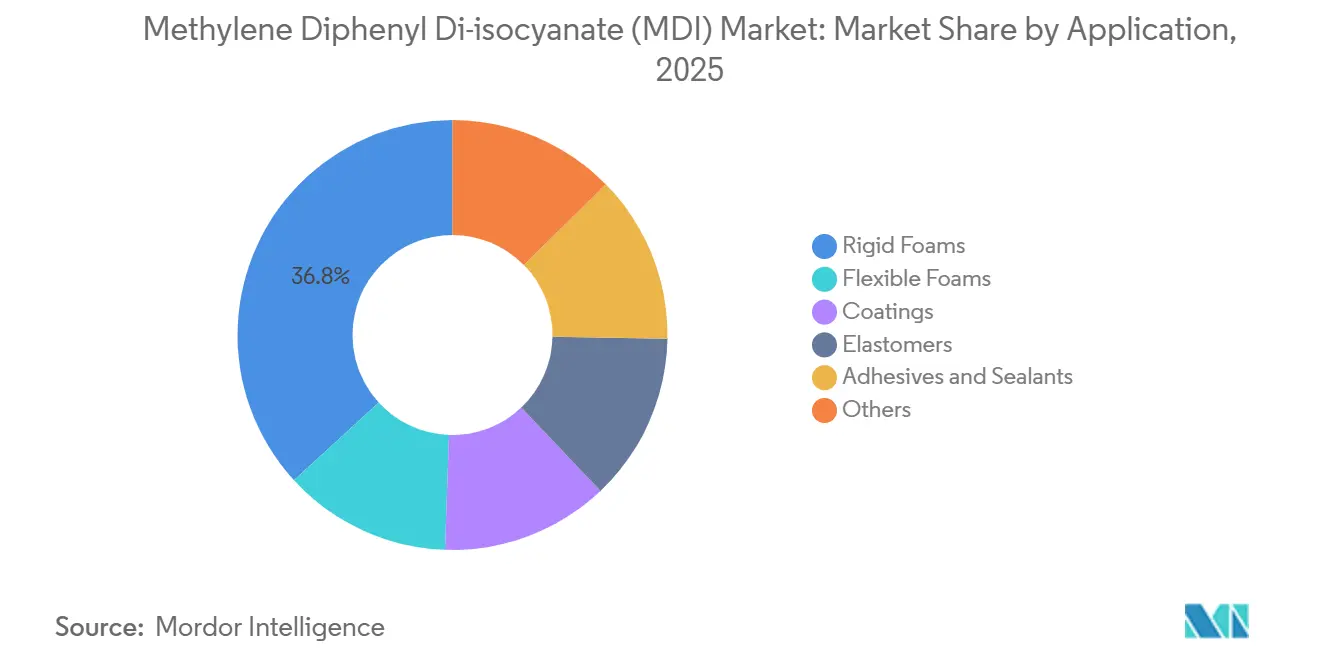

- By application, rigid foams held a 36.81% share of the MDI market in 2025 and are advancing at a 5.69% CAGR through 2031.

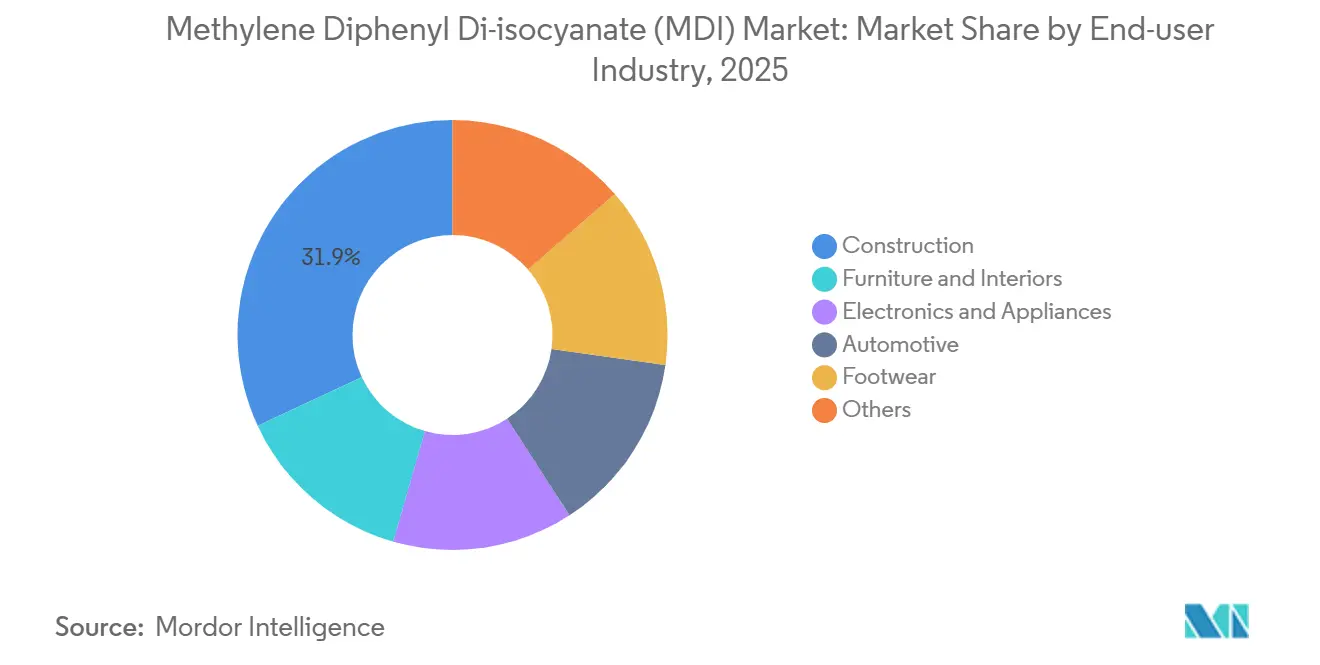

- By end-user, construction commanded 31.94% of the MDI market size in 2025, while the same segment is projected to expand at a 5.31% CAGR to 2031.

- By geography, Asia-Pacific captured 46.77% of the MDI market share in 2025 and is on track for the fastest 5.97% CAGR during 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Methylene Diphenyl Di-isocyanate (MDI) Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in polyurethane-insulation demand from net-zero buildings | +1.2% | Europe, North America, APAC urban clusters | Medium term (2-4 years) |

| Cold-chain capacity build-out for food and pharma | +0.9% | Global, with concentration in APAC and North America | Long term (≥ 4 years) |

| HVAC efficiency regulations boosting appliance foams | +0.7% | North America, EU, Japan, South Korea | Short term (≤ 2 years) |

| Rise of battery-thermal-management foams in EV packs | +0.6% | APAC (China, South Korea), Europe, North America | Medium term (2-4 years) |

| Mass-balanced / ISCC-Plus certified MDI gaining traction | +0.5% | Europe, North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surge in Polyurethane-Insulation Demand From Net-Zero Buildings

Across Europe, the U.S., and parts of Asia, energy codes mandate wall R-values between 20 and 30. This benchmark is achieved using polyiso boards, as opposed to opting for thicker mineral wool. The EU Energy Performance of Buildings Directive is set to drive upgrades in millions of homes. This initiative is projected to boost the consumption of rigid foam in the coming years. Starting January 2026, California’s Title 24 update will elevate roof R-values statewide, solidifying the demand for Class A fire-rated polyiso boards. Passive House certifications in Germany and Austria saw a significant increase, underscoring a homeowner trend towards continuous insulation, which curtails heating loads annually.

Cold-Chain Capacity Build-Out for Food and Pharma

Biologic drugs and mRNA vaccines mandate storage temperatures between 2 °C and 8 °C, frequently dipping below –70 °C during transit. Cencora pledged an investment to quintuple its refrigerated space in Alabama, employing spray-applied MDI foam to ensure temperature stability[1]Cencora, “Cold-Chain Network Expansion,” cencora.com . Global refrigerated-warehouse volume is projected to increase, with rigid MDI boards continuing as the preferred insulation choice.

HVAC Efficiency Regulations Boosting Appliance Foams

Starting in 2027, U.S. standards will limit refrigerator energy use to below a certain threshold annually. This pushes brands to either enhance cabinet insulation or switch to lower-lambda foams. Meanwhile, Europe's F-gas regulation is steering the industry towards cyclopentane blowing agents, which align seamlessly with the cell-stabilizing chemistry of polymeric MDI. Similarly, Japan's updated Top Runner benchmarks and South Korea's more stringent energy labels are both leaning towards advanced MDI foam cores in their premium models.

Rise of Battery-Thermal-Management Foams in EV Packs

In 2024, tests revealed that an MDI foam layer can delay thermal propagation between cells, providing occupants with crucial extra time to exit. A two-component system launched in 2025 achieves a glass-transition temperature, aligning with forthcoming Chinese regulations that mandate fire-retardant separators in packs exceeding a specific capacity. Additionally, automakers are integrating these foams into seat frames, resulting in a reduction in cabin noise.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stricter worker-exposure limits for di-isocyanates | -0.8% | Europe, North America, Japan | Short term (≤ 2 years) |

| Crude-oil volatility hitting aniline feedstock | -0.6% | Global | Short term (≤ 2 years) |

| Emerging non-isocyanate PU chemistries | -0.4% | Europe, North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stricter Worker-Exposure Limits for Di-Isocyanates

aREACH Annex XVII has introduced a mandate: users processing more than 0.1% di-isocyanate by weight must undergo certified training every five years. This requirement has led to an increase in site compliance costs and has also necessitated upgrades to ventilation systems[2]European Chemicals Agency, “Di-isocyanates Restriction,” echa.europa.eu. In 2024, the United Kingdom set similar airborne limits, and Japan is in the process of finalizing comparable regulations, targeting a 2027 implementation. While larger converters are able to absorb these added costs, smaller operations are feeling the pinch on their margins, leading to a trend of consolidation in the industry.

Crude-Oil Volatility Hitting Aniline Feedstock

Benzene, accounting for a significant portion of aniline's production costs, closely follows Brent crude prices. Specifically, an increase in oil prices results in a notable uptick in aniline prices within a three-month window. In 2025, spot aniline prices fluctuated, squeezing margins for producers lacking in-house aromatic resources. However, Wanhua's integration of coal-to-aniline provides a buffer against such cost pressures.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Rigid Foams Dominate Insulation Mandates

Rigid foams captured 36.81% of the methylene diphenyl di-isocyanate market share in 2025 and will rise at a 5.69% CAGR through 2031. Continuous-panel insulation achieves R-20 wall targets with a thinner profile compared to extruded polystyrene, steering architects towards polyiso boards. Spray-foam retrofits gained significant traction due to increased funding support. Additionally, as appliance foams transition to hydrocarbon blowing agents, there's an increased preference for polymeric MDI’s closed-cell density.

Among the rigid-foam options, spray-foam insulation emerged as the fastest-growing choice, with contractors prioritizing its air-sealing and vapor-barrier benefits. Rigid MDI boards are also the go-to for commercial baking ovens, refrigerated trailers, and walk-in coolers aiming to maintain sub-zero temperatures. While elastomers and coatings cater to niche markets, they remain steady, being utilized in high-abrasion rollers and chemically resistant floor finishes. Furthermore, adhesives derived from MDI prepolymers are bonding turbine blades and automotive composites, capitalizing on their high shear strength during thermal cycling.

By End-User Industry: Construction Fuels the Volume Upswing

Construction accounted for 31.94% of the methylene diphenyl di-isocyanate market size in 2025 and is on track for a 5.31% CAGR to 2031. Europe's push for zero-emission new builds by 2030, coupled with its goal for class-D retrofits, is fueling a surge in deep-energy renovations that emphasize the need for continuous insulation. In India, a mandate for insulation in high cooling-degree zones is set to boost the demand for rigid foam significantly by 2028.

As North American and European markets reach maturity, the furniture and interiors sector witnesses steady growth. In contrast, Southeast Asia is ramping up its capacity annually, primarily to cater to the export of sofas and mattresses. Electronics and appliance manufacturers are increasingly opting for thicker foams to comply with energy labels. Meanwhile, the automotive sector is broadening its horizons, venturing into battery-thermal foams. In the footwear industry, MDI-based thermoplastic polyurethane midsoles are becoming the go-to choice for endurance running shoes, with Adidas now incorporating bio-polyols in a portion of its production.

Geography Analysis

Asia-Pacific held 46.77% of the global methylene diphenyl di-isocyanate market volume in 2025 and is set for a 5.97% CAGR through 2031. China's ambitious addition of urban housing annually, paired with Wanhua's expansive complex, solidifies the region's supply foundation. In India, a push for insulation codes and enhanced cold-storage facilities is driving volume expansion. Meanwhile, Vietnam and Indonesia are becoming hubs for relocated furniture and footwear industries. Japan and South Korea are prioritizing appliance insulation upgrades, driven by initiatives like Top Runner and energy labeling.

North America, holding a significant share in demand, sees rising consumption buoyed by weatherization retrofits and a transition to cyclopentane-blown refrigerator foams, even with a mature housing stock. In Canada, revised codes are spurring a surge in spray-foam adoption, especially in provinces experiencing more than 5,000 heating degree-days.

Europe, accounting for a notable portion of the global volume, grapples with high energy costs impacting local producers. However, stringent building directives pave a clear retrofit pathway extending through 2033. The remaining market is split between South America and the Middle-East and Africa. Brazil is poised for a rebound with easing interest rates, while Saudi Arabia's Sadara is strategically exporting competitively priced cargoes from Jubail to Europe and Asia.

Competitive Landscape

The methylene diphenyl di-isocyanate (MDI) market is moderately consolidated. Wanhua’s coal-to-aniline chain underscores cost leadership; BASF and Covestro monetize process know-how through technology licensing in China and India. Huntsman and Dow focus on low-free-monomer prepolymers to meet airborne exposure caps. Venture-funded NIPU start-ups remain in the pilot phase but are closely watched by OEMs hedging regulatory risk.

Methylene Diphenyl Di-isocyanate (MDI) Industry Leaders

Wanhua

Covestro AG

BASF

Huntsman International LLC

Dow

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: The United States Department of Commerce issued preliminary antidumping duties of 376.12% to 511.75% on Chinese MDI imports.

- January 2025: BASF raised Lupranate MDI prices by USD 300 per ton across ASEAN and South Asia, citing sustainable business development, as well as continued increases in the cost of transportation, energy, and regulatory efforts as major factors.

Global Methylene Diphenyl Di-isocyanate (MDI) Market Report Scope

Methylene diphenyl diisocyanate (MDI) is a type of aromatic isocyanate with a wide application base in large-scale commercial and consumer sectors. For the production of MDI, aniline is condensed with formaldehyde to form methylenedianiline (MDA), which is reacted with phosgene to form MDI.

The methylene diphenyl diisocyanate (MDI) market is segmented by application, end-user industry, and geography. By application, the market is segmented into rigid foam, flexible foam, coatings, elastomers, adhesives and sealants, and other applications. By end-user industry, the market is segmented into construction, furniture and interiors, electronics and appliances, automotive, footwear, and other end-user industries. The report also covers the market sizes and forecasts in 16 countries. For each segment, the market sizing and forecasts were made based on volume (Tons).

| Rigid Foams |

| Flexible Foams |

| Coatings |

| Elastomers |

| Adhesives and Sealants |

| Others |

| Construction |

| Furniture and Interiors |

| Electronics and Appliances |

| Automotive |

| Footwear |

| Others |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Russia | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Application | Rigid Foams | |

| Flexible Foams | ||

| Coatings | ||

| Elastomers | ||

| Adhesives and Sealants | ||

| Others | ||

| By End-user Industry | Construction | |

| Furniture and Interiors | ||

| Electronics and Appliances | ||

| Automotive | ||

| Footwear | ||

| Others | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Russia | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

How fast will global demand for methylene diphenyl di-isocyanate grow through 2031?

Volume is forecast to climb from 9.06 million tons in 2026 to 11.64 million tons by 2031, a 5.13 % CAGR driven by insulation codes, cold-chain logistics, and EV battery safety needs.

Which application contributes the largest tonnage of MDI?

Rigid polyurethane foams, used in continuous boards and spray-foam insulation, led with 36.81 % of 2025 demand and will remain the growth engine.

Why are appliance manufacturers switching to polymeric MDI foams?

Hydrocarbon blowing agents mandated by F-gas rules pair best with polymeric MDI, allowing refrigerators to hit 2027 energy-efficiency targets without thicker walls.

What makes Asia-Pacific the fastest-growing region?

China’s huge insulation retrofit program and India’s cold-storage expansion push Asia-Pacific MDI consumption toward a 5.97 % CAGR through 2031.

Could non-isocyanate polyurethanes displace MDI by 2031?

Pilot trials show promise, but slower cure speeds and higher costs mean commercial substitution is improbable before 2030, keeping MDI dominant this decade.

Page last updated on: