Metagenomics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

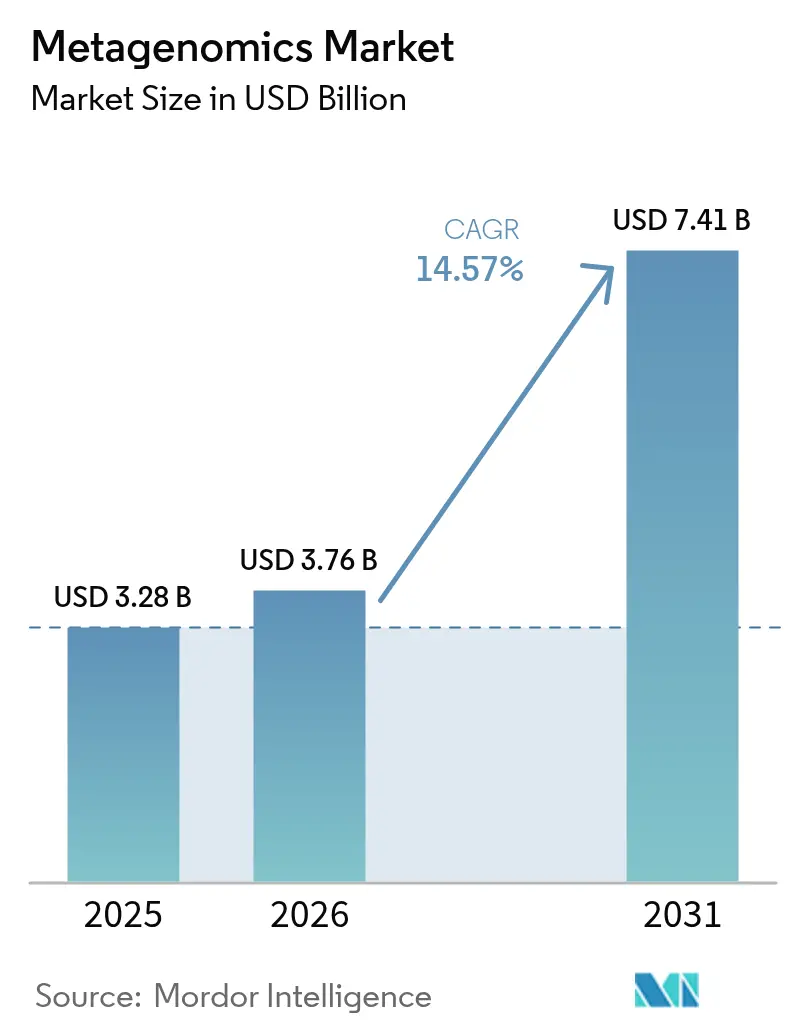

| Market Size (2026) | USD 3.76 Billion |

| Market Size (2031) | USD 7.41 Billion |

| Growth Rate (2026 - 2031) | 14.57% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Metagenomics Market Analysis by Mordor Intelligence

Metagenomics market size in 2026 is estimated at USD 3.76 billion, growing from 2025 value of USD 3.28 billion with 2031 projections showing USD 7.41 billion, growing at 14.57% CAGR over 2026-2031. Rising integration of artificial intelligence (AI) with sequencing platforms shortens pathogen identification time from days to hours, transforming the metagenomics market from research‐focused to clinically indispensable. Rapid cost compression—whole-genome sequencing prices fell from USD 100 million in 2001 to about USD 500 in 2023, which was the result of routine clinical and environmental use cases. North America maintains leadership, yet Asia Pacific records the quickest uptake as governments underwrite national microbiome programs and harmonize regulations. Product dynamics also evolve: kits & reagents retain the most significant slice of spending while outsourcing-driven services expand faster, mirroring the shortage of in-house bioinformatics talent. Competitive pressure is intensifying because AI-native entrants and USD 100-per-genome technology threaten incumbent pricing power.

Key Report Takeaways

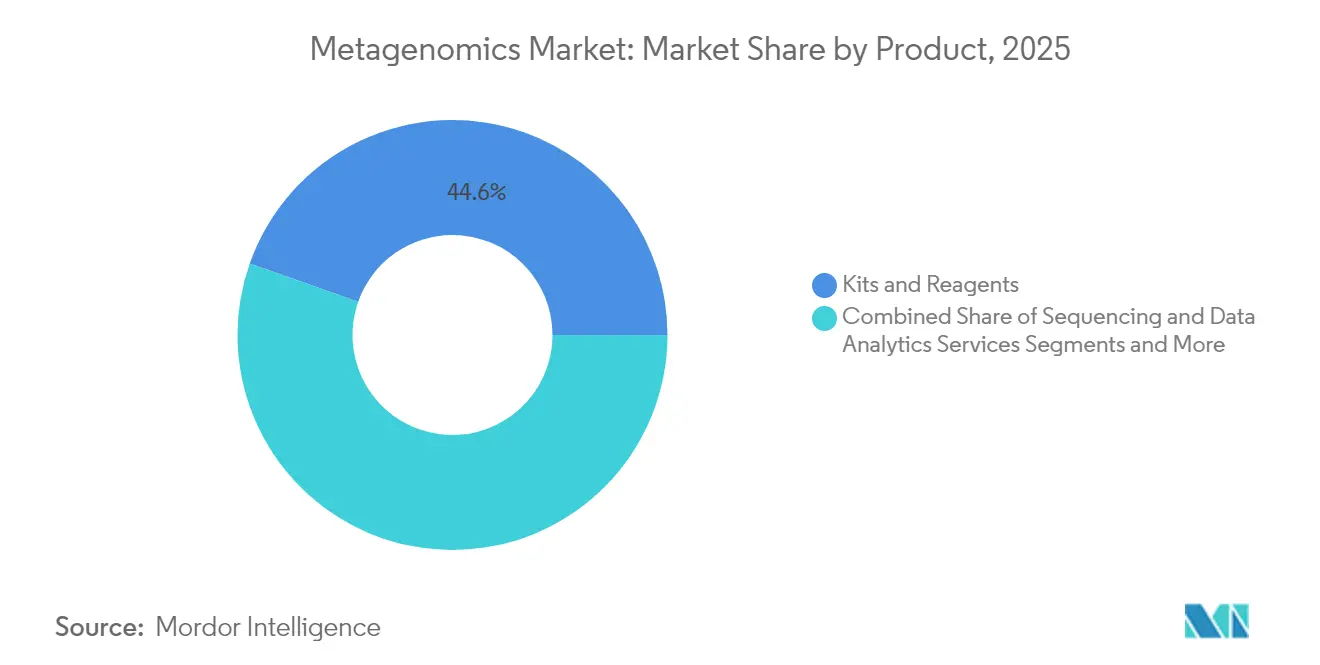

- By product category, kits & reagents held 44.60% of the metagenomics market share in 2025, whereas sequencing & data analytics services are forecast to advance at an 17.85% CAGR through 2031.

- By technology class, sequencing-driven workflows captured a 62.10% share of the metagenomics market in 2025, while third-generation long-read sequencing is projected to rise at an 20.90% CAGR.

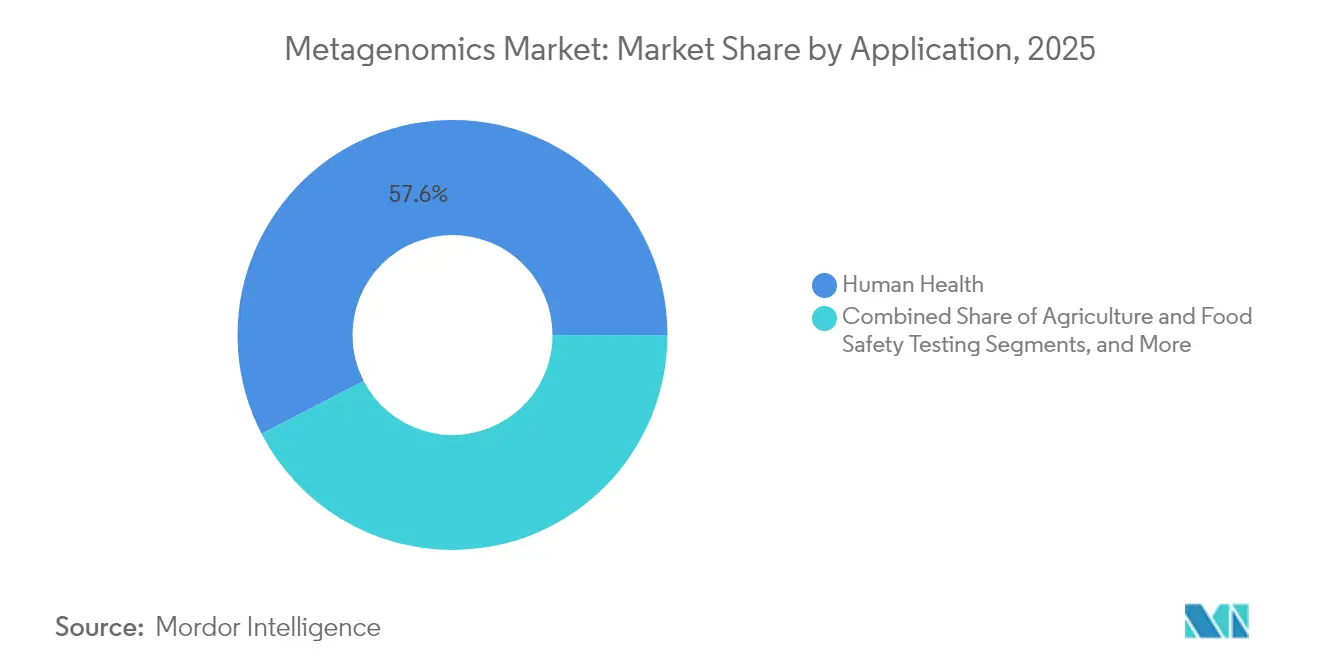

- By application, human health commanded 57.60% of the metagenomics market share in 2025; environmental monitoring and bioremediation are predicted to grow at a 23.20% CAGR to 2031.

- By end user, academic and research institutes accounted for 40.90% of the metagenomics market size in 2025, but clinical diagnostic laboratories showed the fastest 16.60% CAGR.

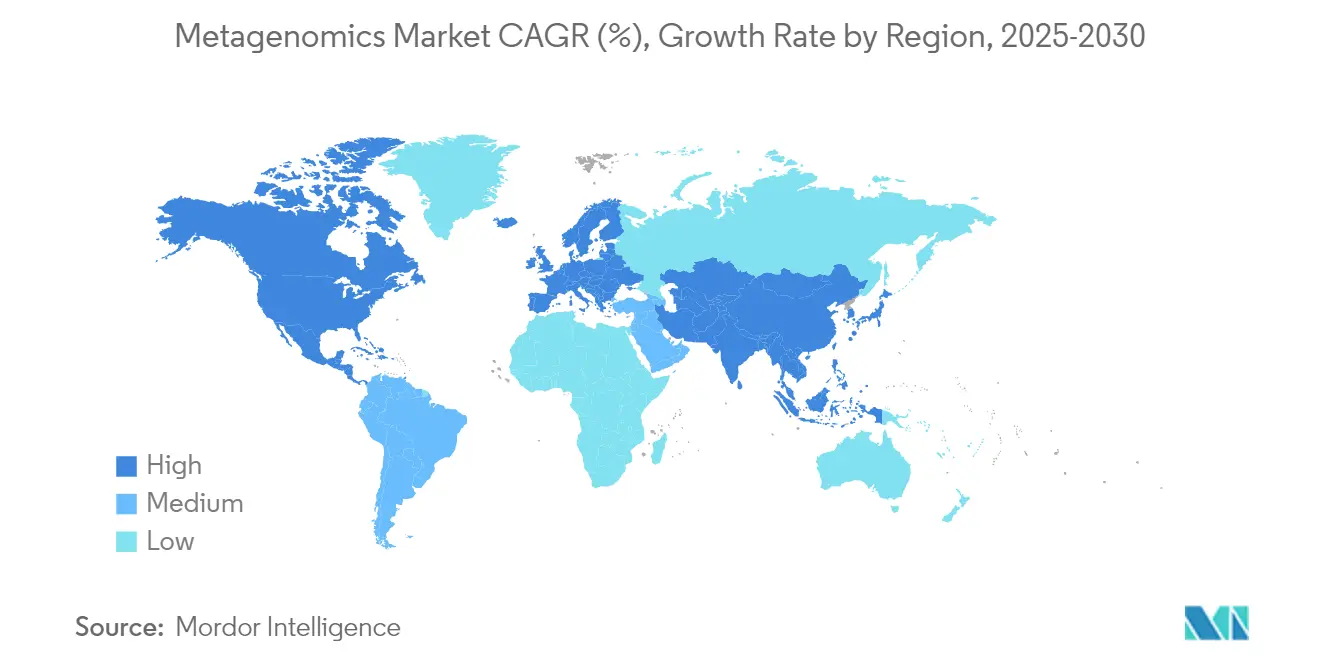

- Geographically, North America represented 46.20% of 2025 revenue, while Asia Pacific is on track for a 16.20% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Metagenomics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing R&D expenditure in metagenomics | +3.20% | Global; strongest in North America & EU | Medium term (2-4 years) |

| Declining cost of high-throughput sequencing | +4.10% | Global, accelerated adoption in APAC | Short term (≤ 2 years) |

| Continuous improvements in library-prep & bioinformatics pipelines | +2.80% | North America & EU leading; APAC following | Medium term (2-4 years) |

| Emergence of ultra-long-read sequencing enabling strain-level insights | +2.30% | Global research hubs, clinical labs in developed markets | Long term (≥ 4 years) |

| AI-powered point-of-care infectious-disease metagenomics platforms | +1.90% | North America & EU, expanding to APAC | Medium term (2-4 years) |

| National microbiome data-commons initiatives | +1.40% | United States, EU, China | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Increasing R&D Expenditure in Metagenomics

Pharmaceutical and biotechnology enterprises amplify metagenomics investments because microbial targets increasingly underpin novel drug discovery programs. Thermo Fisher Scientific earmarked USD 40-50 billion for acquisitions that strengthen metagenomics-adjacent capabilities, signaling boardroom conviction that next-generation therapeutics demand microbiome-centric data. The NIH’s Human Virome Program directs roughly USD 2.5 million toward 2026 tool development, fostering academic-industry alliances that accelerate clinical translation.[1]National Institutes of Health, “Human Virome Program Funding Opportunity,” nih.govGovernment grants such as the NSF Ecology and Evolution of Infectious Diseases initiative, with a USD 32 million budget for FY 2025, encourage multidisciplinary research linking metagenomics with computational modeling.[2]National Science Foundation, “Ecology and Evolution of Infectious Diseases,” nsf.gov

Declining Cost of High-Throughput Sequencing

Whole-genome sequencing prices plunged to USD 600 in 2024, unlocking widespread clinical deployment. Ultima Genomics further disrupted norms by achieving a USD 100 genome at Q60 accuracy, forcing incumbents to compress margins and accelerate product cycles.[3]Edward Dutka, “Q60 Accuracy at USD 100 per Genome,” science.org Additional price cuts, such as the University of Minnesota’s Element AVITI platform, now position next-generation sequencing below Illumina’s flagship NovaSeq for comparable throughput. Budgetary shifts away from capital equipment toward bioinformatics expertise reshape laboratory cost structures.

Continuous Improvements in Library-Prep & Bioinformatics Pipelines

Pipeline automation reduces hands-on time and contamination risk, enabling routine diagnostics in non-specialist settings. QIAGEN’s Digital Insights unit integrates AI-driven analytics that compress turnaround from days to hours. Illumina’s DRAGEN metagenomics workflow leverages NVIDIA GPUs for real-time computation. Machine-learning models achieve 93.6% sensitivity and 93.8% specificity in respiratory-virus detection, outperforming RT-PCR.

Emergence of Ultra-Long-Read Sequencing Enabling Strain-Level Insights

Oxford Nanopore Technologies and Pacific Biosciences deliver reads long enough to assemble complete microbial genomes, revealing structural variants and resistance genes that short-read methods overlook. Strain-level resolution enhances outbreak investigation, antimicrobial stewardship, and pollution source tracking.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Overall Cost Of Comprehensive Metagenomic Workflows | -2.80% | Global, particularly impacting emerging markets | Short term (≤ 2 years) |

| Shortage Of Skilled Bioinformaticians For Data Interpretation | -1.90% | Global, acute in APAC and emerging markets | Medium term (2-4 years) |

| Data-Privacy & Ethical Concerns Over Incidental Human Genomic Findings | -1.50% | EU & North America primarily, expanding globally | Medium term (2-4 years) |

| Export-Control Risks Disrupting Enzyme & Reagent Supply Chains | -1.20% | Global supply chains, acute impact on China-US trade | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Overall Cost of Comprehensive Metagenomic Workflows

Although sequencing itself is cheaper, total ownership costs remain high once computational infrastructure, storage, and accreditation are included. A Pentagon pilot concluded that daily metagenomic biosurveillance remains 10-100 times too costly for routine use unless sample pooling and virtualization mature further. Low- and middle-income regions pay up to USD 4,500 per genome because logistics and customs fees inflate consumable prices.

Shortage of Skilled Bioinformaticians for Data Interpretation

Global demand for specialists who can translate petabyte-scale data into clinical guidance outstrips supply. Most university programs still focus on wet-lab microbiology or general computer science, leaving a training gap in applied metagenomics. Smaller clinics struggle to recruit talent, driving demand for managed-service providers and cloud analysis portals, yet quality-control steps still require human oversight.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Services Surge Despite Reagents Dominance

Kits & reagents retained 44.60% of 2025 revenue because every sequencing run consumes standardized consumables that ensure reproducible results. However, sequencing & data analytics services are scaling at an 17.85% CAGR, reflecting laboratories’ preference to outsource compute-intensive steps to specialized providers. The metagenomics market size for services is projected to increase more than threefold by 2031. Instruments & consumables maintain steady replacement demand, whereas cloud-delivered software pipelines lower barriers for resource-constrained facilities.

Outsourcing momentum intensifies as regulators demand auditable pipelines that small laboratories rarely build in-house. QIAGEN’s Digital Insights partnership with major cloud vendors illustrates how service ecosystems capture recurring fees, while Novogene’s high-throughput model offers competitive pricing tiers for academic consortia. This combination of compliance burden and bioinformatics talent shortage should sustain double-digit growth for managed services over the forecast horizon.

By Technology: Third Generation Disrupts Short-Read Dominance

Sequencing-driven workflows represented 62.10% of the metagenomics market share in 2025, yet third-generation long-read platforms are expanding at 20.90% CAGR. Long reads assemble complete microbial genomes, reveal plasmid-borne resistance genes, and quantify epigenetic modifications in real time. Function-driven protocols remain niche but essential for bioprocess optimization, while amplicon-based approaches persist in cost-sensitive surveillance. The metagenomics market size for long-read applications should surpass USD 2.28 billion by 2031, catalyzed by hospital infection-control programs and large-scale environmental projects.

Real-time nanopore sequencing enables field-deployable diagnostics at border checkpoints and remote farms. Researchers combining long-read DNA and RNA sequencing now correlate active gene expression with genomic context, a capability expected to unlock new anti-infective targets. Meanwhile, platform vendors seek standards harmonization so that hybrid assemblies merge the depth of short reads with the context of long ones.

By Application: Environmental Monitoring Accelerates Beyond Healthcare

Human health remains the largest application, accounting for 57.60% of 2025 revenue, as clinical diagnostics and pharmaceutical discovery rely on high-resolution microbiome data. Yet environmental monitoring and bioremediation are growing fastest at 23.20% CAGR, underpinned by climate adaptation mandates and corporate net-zero commitments. From oil spill cleanup to wastewater surveillance, governments and multinationals increasingly pay for microbial community profiling instead of chemical assays. The metagenomics market size for environmental deployments is forecast to quadruple by 2031.

Rapid microbiome assays also benefit crop-yield optimization and food authenticity testing, reducing recall risk and improving traceability. In clinical settings, metagenomic antimicrobial-resistance surveillance guides stewardship policies, reducing broad-spectrum antibiotic use in tertiary hospitals by measured margins.

By End User: Clinical Labs Transition from Research Tools

Academic and research institutions accounted for 40.90% of 2025 spending, showcasing metagenomics’ academic roots. Clinical diagnostic laboratories, however, are growing at 16.60% CAGR as the FDA clarifies laboratory-developed test requirements and payers introduce reimbursement codes. If reimbursement uptake remains on track, the metagenomics market size for clinical labs will likely overtake academic demand before 2031. Pharmaceutical and biotechnology firms continue to integrate microbiome data into target-discovery pipelines, ensuring sustained demand for high-throughput sequencing.

Contract research organizations (CROs) benefit from smaller biotech clients that outsource end-to-end projects, including wet-lab work, bioinformatics, and regulatory documentation. Environmental and food-testing labs expand metagenomic capacity to comply with stricter pathogen-monitoring rules in North America and the European Union.

Geography Analysis

North America controlled 46.20% of global revenue in 2025 due to established sequencing infrastructure, dense biotech clusters, and favorable reimbursement. Federal projects such as the NIH All of Us Research Program continue to channel funding into microbiome-heavy protocols, sustaining domestic demand. Canada’s Precision Health Initiative further bolsters regional sequencing volumes.

Europe maintains a robust position, benefiting from the Horizon Europe funding stream and the European Medicines Agency’s supportive stance on real-world microbiome data. Cross-border clinical trials increasingly incorporate metagenomic endpoints, encouraging standardized data pipelines across European reference labs. The region also houses several leading bioinformatics software vendors that export platforms globally.

Asia Pacific represents the fastest-growing geography at 16.20% CAGR through 2031. China’s National GeneBank expansion and India’s Genome India initiative exemplify government-funded programs that aim to leapfrog legacy infrastructure. Domestic players such as BGI leverage cost-efficient platforms like DNBSEQ-T7 to drive local adoption while exporting solutions to Africa and Latin America. Singapore and South Korea invest heavily in AI-enabled precision medicine pilots, positioning the broader region as a testbed for end-to-end metagenomics ecosystems. The Middle East and Africa show nascent but rising interest as public-health agencies embrace wastewater surveillance for early outbreak alerts—South America partners with European labs to transfer protocols and build local talent pipelines.

Competitive Landscape

The metagenomics market shows moderate concentration as Illumina holds roughly 80% of DNA-sequencing revenue, yet that dominance faces erosion from AI-native newcomers and ultra-low-cost chemistry. Incumbents pursue vertical integration, with Thermo Fisher Scientific spending more than USD 4 billion annually on acquisitions that connect sample prep, analytics software, and cloud delivery. QIAGEN doubles down on Digital Insights subscriptions to shift its revenue mix toward recurring data services.

Disruptors such as Ultima Genomics slash per-genome prices, compelling incumbents to re-align innovation roadmaps. Oxford Nanopore’s portable sequencers and Pacific Biosciences’ HiFi reads offer accuracy that now rivals short-read benchmarks, broadening clinical acceptance. AI is rapidly turning into the key differentiator, as illustrated by Karius, whose FDA-designated breakthrough test outperforms standard respiratory panels by scanning for thousands of pathogens simultaneously.

Partnership ecosystems are expanding. Illumina teamed with NVIDIA to accelerate multiomic AI pipelines, while bioMérieux collaborates with Illumina for bacterial outbreak surveillance in public-health labs. QIAGEN’s alliance with McGill University focuses on protocols for low-biomass samples, underscoring how suppliers depend on academic centers for validation studies. Service providers like Novogene and Element Biosciences undercut equipment-based models by selling sequencing-as-a-service with transparent pricing, appealing to smaller entities that cannot justify capital purchases.

Metagenomics Industry Leaders

Illumina, Inc

PerkinElmer Inc.

QIAGEN N.V.

F. Hoffmann-La Roche Ltd

Novogene Co., Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Illumina unveils constellation-mapped read technology and a 5-base solution that simultaneously profiles genetic and methylation signals, targeting commercialization in 2026 to streamline multiomic workflows.

- February 2025: Thermo Fisher Scientific announces a USD 4.1 billion acquisition of Solventum’s Purification & Filtration unit to bolster biologics production, projecting USD 125 million synergy by year five.

- January 2025: Illumina and NVIDIA partner to fuse DRAGEN algorithms with NVIDIA GPUs for AI-powered multiomic analytics aimed at drug-discovery acceleration.

- December 2024: QIAGEN releases AI-enabled Ingenuity Pathway Analysis extension that automates biological insight generation from complex datasets.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

According to Mordor Intelligence, we size the metagenomics market as all revenues generated from reagents, consumables, instruments, sequencing, and data-analytics services that enable untargeted genomic profiling of mixed microbial communities in clinical, environmental, industrial, and agricultural samples. Our study tracks only new product and service sales that are invoiced in the open market during the calendar year.

Scope exclusion: custom on-premise bioinformatics software that is developed under non-commercial academic grants is not counted.

Segmentation Overview

- By Product

- Sequencing & Data Analytics Services

- Kits & Reagents

- Instruments & Consumables

- Software & Pipeline Tools

- Others

- By Technology

- Sequencing-Driven Metagenomics

- Function-Driven Metagenomics

- Third-Generation Long-Read Sequencing

- Amplicon-Based Targeted Sequencing

- Metatranscriptomics

- By Application

- Human Health

- Environmental Monitoring & Bioremediation

- Agriculture & Food Safety Testing

- Others

- By End-User

- Academic & Research Institutes

- Pharmaceutical & Biotechnology Companies

- Clinical Diagnostic Laboratories

- Environmental & Food Testing Labs

- CROs & Service Providers

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

We conducted semi-structured calls and questionnaires with lab directors, hospital microbiologists, CRO managers, bioinformatics tool vendors, and regional distributors across North America, Europe, Asia-Pacific, and Latin America. These discussions validated kit price curves, average read depths purchased per project, and emerging clinical adoption triggers, which then refined our model assumptions.

Desk Research

We began by mining freely available tier-1 datasets such as NIH GenBank release statistics, NCBI's Sequence Read Archive upload volumes, EU-OS's antimicrobial resistance dashboard, WHO Global Pathogen Surveillance updates, and USDA agricultural microbiome trials; these helped us benchmark sequencing throughput, sample volumes, and funding patterns. Our analysts also screened peer-reviewed articles in Nature Microbiology and Environmental Microbiology, company 10-Ks, SEC filings, and trade-association notes, followed by selective pulls from D&B Hoovers and Questel patent analytics for supplier revenue splits and IP velocity.

Additional desk work covered customs shipment codes for DNA extraction kits, procurement notices scraped via Tenders Info, and news flows on pricing moves captured through Dow Jones Factiva. This list is illustrative; many other open and paid sources were tapped for corroboration and gap filling.

Market-Sizing & Forecasting

A top-down reconstruction that links global NGS output (Gb) to average reads required per metagenomic workflow, multiplied by blended ASPs, delivers the base year value. Select bottom-up checks, supplier revenue roll-ups, and sampled laboratory procurement tallies calibrate the totals. Key variables include flow-cell cost per gigabase, mean library prep throughput, count of metagenomics-focused clinical trials, government R&D outlays in genomics, and public cloud storage pricing. Ten-year forecasts apply multivariate regression with scenario analysis around sequencing cost decline and healthcare R&D intensity. Gaps in granular supplier data are bridged using region-weighted ASP imputation validated through distributor interviews.

Data Validation & Update Cycle

Outputs pass a two-step analyst peer review, variance checks against independent industry ratios, and anomaly resolution before sign-off. We refresh the model annually and trigger interim reviews when material events, such as major price cuts, large funding rounds, or regulatory shifts, occur.

Why Mordor's Metagenomics Baseline Commands Decision-maker Trust

Published estimates often differ; scopes, pricing baskets, update cadence, and validation depth rarely align. Our disciplined variable selection and yearly refresh make our figure the dependable reference point for planners.

Key gap drivers include whether services revenue is counted, the treatment of legacy Sanger workflows, and the aggressiveness of long-term sequencing cost assumptions.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 3.28 B (2025) | Mordor Intelligence | - |

| USD 2.25 B (2024) | Global Consultancy A | excludes data-analytics services and uses static ASPs |

| USD 2.00 B (2023) | Industry Association B | older base year, no primary validation of kit volumes |

| USD 1.81 B (2023) | Trade Journal C | omits environmental testing segment and applies conservative clinical uptake |

Taken together, the comparison shows that when scope breadth, fresh primary inputs, and cross-checks converge, Mordor Intelligence delivers a balanced baseline that clients can trace, replicate, and confidently build upon.

Key Questions Answered in the Report

What is the current size of the metagenomics market?

The metagenomics market stands at USD 3.76 billion in 2026 and is forecast to reach USD 7.41 billion by 2031.

Which region is growing fastest in the metagenomics market?

Asia Pacific is expanding at a 16.20% CAGR as national genomics programs stimulate infrastructure and regulatory alignment.

Why are sequencing & data-analytics services growing so rapidly?

Laboratories increasingly outsource bioinformatics because talent shortages and compliance requirements make in-house pipelines costly; the services segment is advancing at an 17.85% CAGR.

How does long-read sequencing differ from traditional short-read methods?

Long-read platforms assemble complete microbial genomes and detect structural variants in real time, driving a 20.90% CAGR for third-generation sequencing applications.

What are the main restraints facing the metagenomics industry?

High total workflow costs and a global shortage of bioinformaticians are the top barriers, together suppressing CAGR growth by about 4.7 percentage points.

Which company currently dominates DNA-sequencing revenue?

Illumina controls around 80% of global DNA-sequencing revenue but faces emerging competition from cost-disruptive and AI-native newcomers.

Page last updated on: