Menstrual Health Apps Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

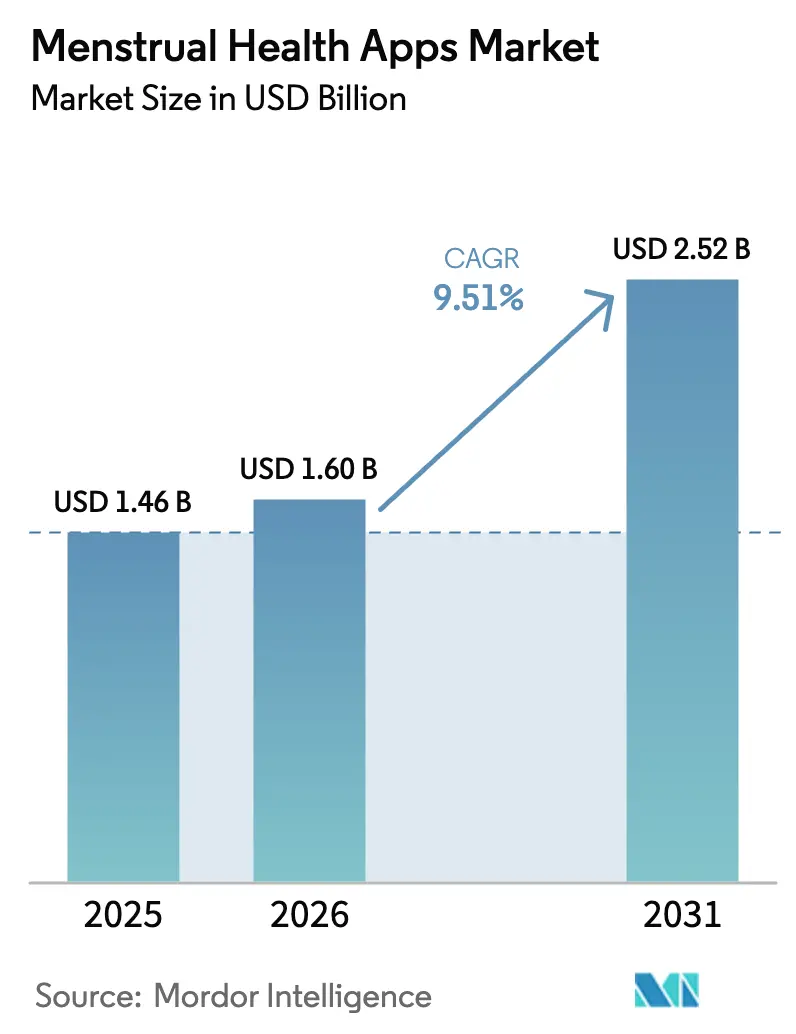

| Market Size (2026) | USD 1.60 Billion |

| Market Size (2031) | USD 2.52 Billion |

| Growth Rate (2026 - 2031) | 9.51% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Menstrual Health Apps Market Analysis by Mordor Intelligence

The menstrual health apps market size is expected to grow from USD 1.46 billion in 2025 to USD 1.60 billion in 2026 and is forecast to reach USD 2.52 billion by 2031 at 9.51% CAGR over 2026-2031. Intensifying smartphone adoption, regulatory acceptance of algorithm-based fertility tracking, and employer-sponsored reproductive-health benefits are combining to shift personal cycle data from clinic files to consumer-controlled apps, expanding the menstrual health apps market far beyond its early-adopter base. Venture funding signals durable confidence: Flo Health’s July 2024 Series C valued the company above USD 1 billion, while Maven Clinic closed a USD 125 million Series F at a USD 1.7 billion valuation in October 2024. Hardware integration is another structural tailwind, with Apple Watch wrist-temperature sensors feeding retrospective ovulation estimates straight into Cycle Tracking, lowering input friction and pulling high-income users deeper into the menstrual health apps market. Meanwhile, Karnataka’s 2025 law granting 12 annual paid menstrual-leave days without medical certification is encouraging Indian employers to provide app subscriptions so that HR teams can audit leave utilization, a policy model likely to disperse through Asia Pacific and stimulate further market penetration.

Key Report Takeaways

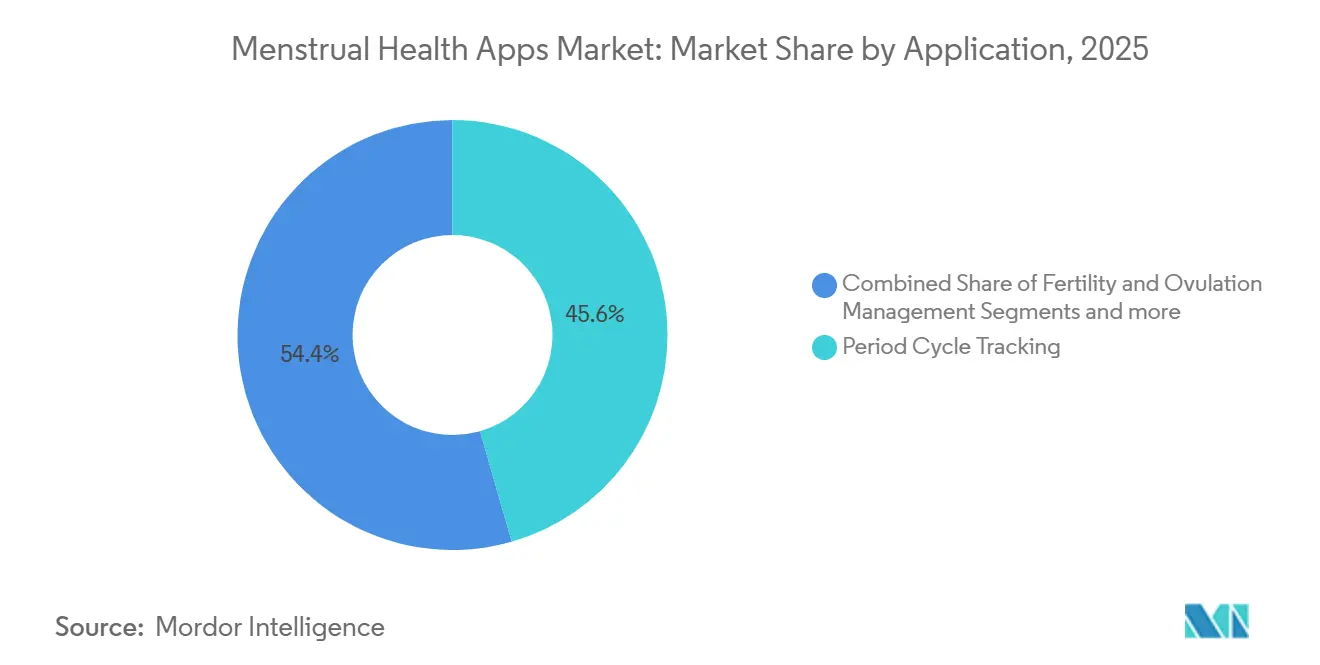

- By application, Period Cycle Tracking led with 45.56% of the menstrual health apps market share in 2025.

- By platform, Android commanded 57.61% of the menstrual health apps market size in 2025.

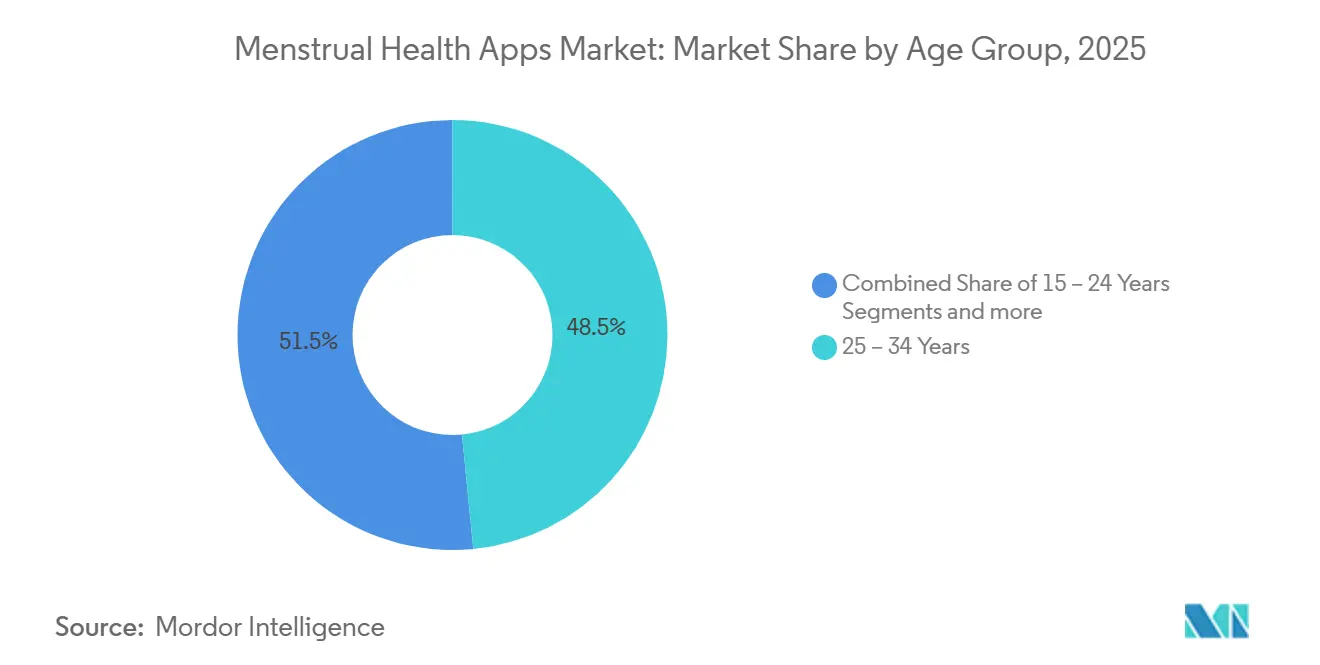

- By age group, the 25–34 segment accounted for 48.47% of users in 2025, while the 15–24 cohort is advancing at a 10.49% CAGR through 2031.

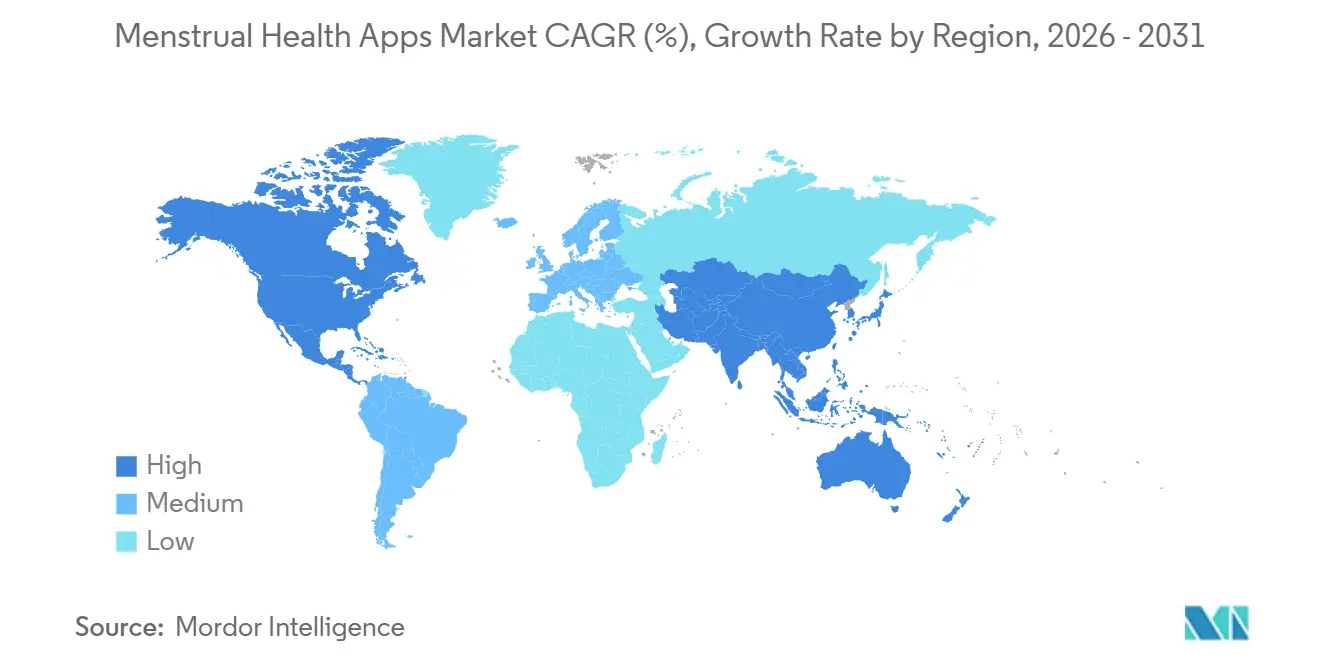

- By geography, North America held 42.12% of the menstrual health apps market size in 2025; Asia-Pacific is growing fastest at a 10.59% CAGR toward 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Menstrual Health Apps Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increased awareness of menstrual & reproductive health | +1.8% | Global, with concentrated campaigns in India, Sub-Saharan Africa | Medium term (2-4 years) |

| Rising smartphone & mobile-internet penetration | +2.1% | APAC core, spill-over to MEA and Latin America | Short term (≤ 2 years) |

| Integration with smart-wearables & health-OS ecosystems | +1.5% | North America, Western Europe, urban APAC | Medium term (2-4 years) |

| Freemium & subscription models accelerating ARPU | +1.3% | Global, premium tiers in North America and EU | Short term (≤ 2 years) |

| Menstrual-leave legislation catalysing employer uptake | +0.9% | Spain, Japan, India (Karnataka), South Korea, Taiwan | Long term (≥ 4 years) |

| Decentralised health-data wallets enabling trust-based onboarding | +0.6% | EU (GDPR-compliant jurisdictions), pilot programs in US | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Increased Awareness of Menstrual and Reproductive Health

Public-health campaigns reframing menstruation as a rights issue rather than a hygiene concern are widening the menstrual health apps market in low-income regions. UNFPA’s 2024 initiative integrated cycle literacy into secondary curricula across 12 nations, while Unicharm India’s school program reached 760,000 adolescents by mid-2025, normalizing app use among first-time trackers.[1]United Nations Population Fund, “Menstrual Health and Rights,” unfpa.org Maven Clinic’s employer agreements with Amazon, AT&T, and Microsoft convert awareness into enterprise revenue, sidestepping direct-to-consumer acquisition costs. Japan’s health ministry logged a 23% annual rise in menstrual-leave claims in fiscal 2024, and downloads of Unicharm’s Sofy app crossed 3.37 million by June 2025, illustrating how policy normalization can accelerate digital adoption. Cultural destigmatization is also visible on social media, where Gen Z users share symptom-tracking screenshots, reinforcing peer-to-peer diffusion and deepening the menstrual health apps market footprint. The net result is a broader funnel of novice users who often transition from free tracking to premium analytics within six months.

Rising Smartphone and Mobile-Internet Penetration

GSMA tallied 1.8 billion mobile subscribers and 1.4 billion mobile-internet users across Asia Pacific in 2024, with India’s smartphone penetration hitting 54% and Indonesia’s at 68%, pushing the menstrual health apps market into millions of new hands. Adjust’s 2025 trends report scored Asia Pacific 45, the highest global growth index for health and fitness apps, while India’s average cost-per-install sat at USD 0.03, enabling scale acquisition under tight budgets. Android’s 57.61% market share in 2025 mirrors this dynamic, yet iOS is expanding faster at a 10.41% CAGR because Apple’s multi-device lock-in lifts switching costs. The diverging economics compel dual strategies: Android apps chase volume through ad-supported freemium tiers, whereas iOS apps monetize via annual subscriptions enhanced by wearables. Accelerating 4G rollouts in Africa and Latin America are expected to echo Asia’s pattern, setting up the menstrual health apps market for sustained double-digit regional growth.[2]Apple, “Using Cycle Tracking,” apple.com

Integration with Smart Wearables and Health OS Ecosystems

Maven Clinic’s June 2025 accord with Oura Ring pipes continuous skin-temperature and heart-rate variability into fertility predictions, reducing manual data entry and enhancing cycle-phase accuracy. Apple Watch Series 8 wrist-temperature sensors, live in the market since 2022, remove the need for bedside thermometers and auto-populate Cycle Tracking across iPhone, Watch, and iPad, tightening Apple’s hold on the premium end of the menstrual health apps market. Bellabeat’s May 2025 IVY+ tracker offers continuous monitoring with a seven-day battery, appealing to users who prefer a dedicated device over a smartwatch experience. Hardware pipelines create a data moat; platforms lacking wearable APIs risk relegation to basic calendars, a feature now bundled free in operating systems. Consequently, investors are steering capital toward companies that can secure firmware integrations, elevating the importance of hardware alliances in the menstrual health apps market.

Freemium and Subscription Models Accelerating ARPU

RevenueCat’s 2025 benchmarks report median Day-60 revenue per install at USD 1.98 for health apps and Year-1 lifetime value per payer at USD 86.35, underscoring that disciplined monetization is already baked into top performers. Trial-to-paid conversion averages 39.9% but jumps to 68.3% among the top-decile, proving that carefully crafted onboarding flows lift cash-flow velocity. Flo Health disclosed 5 million paid subscribers and USD 200 million gross bookings in 2024, equating to an ARPU around USD 40, aligned with the median annual subscription price of USD 39.99. Premium tiers now bundle AI symptom analytics, telehealth consultations, and life-stage content, turning the menstrual health apps market into a recurring-revenue engine rather than a one-time download. As more jurisdictions pass app-store tax transparency laws, platform operators are renegotiating payment splits, which could further improve publisher margins over the forecast horizon.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing data-privacy & cyber-security concerns | -1.2% | Global, acute in US post-Dobbs, EU under GDPR | Short term (≤ 2 years) |

| Algorithmic accuracy & regulatory scrutiny of health claims | -0.8% | North America (FDA), EU (CE marking), emerging in APAC | Medium term (2-4 years) |

| Post-Roe legal discovery risks for U.S. user data | -0.7% | United States, spillover to multinational platforms | Short term (≤ 2 years) |

| Stricter app-store policies on sensitive health data | -0.5% | Global (Apple App Store, Google Play) | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Data-Privacy and Cyber-Security Concerns

The Federal Trade Commission’s 2021 settlement with Flo Health mandates independent privacy audits through 2041, making the case a perpetual reminder of liability in the menstrual health apps market.[3]Federal Trade Commission, “Flo Health Settlement,” ftc.gov Mozilla’s 2022 review showed 72% of period apps lacked transparent deletion policies, while 40% skipped encryption in transit. California’s Delete Act, effective 2026, requires one-click erasure across all brokers, while Connecticut’s SB 3 bans geofencing around reproductive-health clinics, raising compliance complexity. Apple’s HealthKit integration rules introduced in 2025 now require third-party security assessments, a cost shock for early-stage developers. Together, these frameworks amplify user skepticism and inflate legal budgets, slightly dampening the menstrual health apps market growth rate.

Algorithmic Accuracy and Regulatory Scrutiny of Health Claims

Natural Cycles secured FDA 510(k) clearance in 2018 with a 0.98 perfect-use Pearl Index, yet updated guidance on AI-enhanced fertility algorithms is still absent, pressing other vendors into regulatory limbo. A 2024 JMIR study covering 326 users recorded a 14% unplanned-pregnancy rate among those relying on apps for contraception, spotlighting real-world efficacy gaps. The European Union AI Act classifies predictive health algorithms as high risk from 2025 onward, demanding conformity assessments and post-market surveillance that inflate compliance expenditure. App-store review teams now request clinical documentation before approving marketing claims, creating a bottleneck for quick iteration. Collectively these factors inject caution into commercial rollouts, slowing feature velocity in the menstrual health apps market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Symptom Analytics Moving From Wellness to Clinical

Menstrual Health Management and Symptom Analytics is projected to expand at a 10.34% CAGR to 2031, outrunning the broader menstrual health apps market thanks to demand for predictive insights that go beyond ovulation timing. Period Cycle Tracking maintained 45.56% of 2025 revenue, but commoditization looms as Apple and Google continue bundling basic calendars for free. The menstrual health apps market size for symptom analytics is forecast to add nearly USD 420 million in new value over the outlook period, while anomaly alerts for endometriosis and polycystic ovary syndrome help users seek care earlier, tightening links with clinicians.

Flo’s November 2025 study of 19 million users confirmed statistically robust correlations between luteal-phase progesterone and symptoms like mood fluctuations, prompting the platform to surface personalized clinical prompts. Natural Cycles rolled out NC° Perimenopause in October 2025, signaling that life-stage verticals can extend customer lifetime value. Fertility & Ovulation Management remains a middle-ground monetizer, but Ava’s FDA-cleared bracelet automates data capture via overnight wrist sensors, raising the competitive bar for manual-entry apps. As symptom analytics secure scientific validation, payer acceptance inside employer and insurer benefits is expected to rise, adding an enterprise layer to the menstrual health apps market.

By Platform: iOS Premium Posture Versus Android Scale

Android held 57.61% share in 2025 due to its dominance in Asia Pacific and Latin America where price-sensitive consumers flood the menstrual health apps market. Yet iOS is growing quicker at a 10.41% CAGR to 2031, buoyed by Apple Watch sensors and cross-device synchronization that increases stickiness. The menstrual health apps market size derived from iOS users already accounts for a disproportionate 60% of paid subscribers at Flo even though iOS commands just 40% of total installs.

RevenueCat notes median Year-1 lifetime value on iOS at USD 92.50 against USD 78.20 on Android, validating higher customer-acquisition spend on Apple’s ecosystem. Google’s Health Connect API aims to mirror HealthKit’s interoperability, but uptake is modest, and many leading platforms route wearable data through Apple’s frameworks. Compliance hurdles further skew the landscape: Apple’s 2025 demand for third-party security audits raises costs that many Android-first developers cannot absorb. Consequently, the menstrual health apps market is bifurcating: Android apps rely on freemium ad revenue, while iOS apps bundle subscription tiers with wearable analytics, producing higher per-user economics.

By Age Group: Gen Z Growth and Perimenopause Opportunities

Users aged 15–24 are expanding at a 10.49% CAGR, stimulated by school-based menstrual education programs such as Unicharm India’s initiative that has normalized digital tracking among first-time users. The 25–34 cohort still makes up 48.47% of the 2025 installed base, aligning with peak fertility years and premium-feature uptake, including basal-temperature charting and ovulation kits.

Mature demographics are rising too. NC° Perimenopause and Flo’s menopause module serve the 45+ group, which Oova data shows comprises 46% of hormone-strip users. Amissa’s Apple Watch integration delivers clinician-readable symptom severity scoring, creating a bridge to hormone-replacement consultations. As a result, the menstrual health apps market is becoming a lifelong companion rather than a fertility-only tool, with platforms vying to retain users across reproductive milestones.

Geography Analysis

North America represented 42.12% of 2025 revenue in the menstrual health apps market, lifted by employer benefits, FDA-cleared contraceptive apps, and high smartphone penetration. RevenueCat’s 2025 dashboard places median Year-1 value per payer at USD 95.40 in the region, reflecting willingness to pay for premium analytics. Post-Dobbs privacy anxieties spurred California, Connecticut, and Washington to pass consent laws for geolocation and browsing-history linkage, raising compliance overhead for smaller providers.

Europe mirrors North America’s regulatory intensity under GDPR and the incoming AI Act, yet Spain’s menstrual-leave law and German employer uptake are turning policy into revenue funnels. Asia Pacific is the fastest-growing cluster at 10.59% CAGR, fueled by affordable smartphones and favorable policy, such as Karnataka’s 2025 menstrual-leave mandate. GSMA reports 1.8 billion subscribers in the region, underpinning a giant addressable base.

Middle East and Africa and South America are nascent but promising. Brazil’s Pix instant-payment network reached 150 million users in 2024, lowering friction for subscription conversions. South African insurers like Discovery Health are piloting cycle-tracking rewards, and Gulf Cooperation Council countries combine near-universal smartphone ownership with cultural guardedness, requiring physician referrals over mainstream marketing.

Competitive Landscape

The menstrual health apps market is moderately fragmented. A March 2024 Reproductive BioMedicine Online survey put Clue at 31.6% and Flo at 24.2% of user share, with no player able to impose premium pricing beyond USD 39.99 median annual fees. Venture capital is concentrating behind platforms capable of telehealth, wearable data, and employer channels, as illustrated by Flo’s unicorn round and Maven’s USD 1.7 billion valuation. Apple’s free Cycle Tracking threatens to commoditize basic prediction, compelling rivals to differentiate through AI symptom analytics, regulatory approvals, or hardware tie-ins, such as Natural Cycles’ FDA clearance.

White-space innovation is concentrating on perimenopause, as shown by NC° Perimenopause and Flo’s menopause library, and on employer benefits where Maven’s 2,000+ corporate clients validate B2B appetite. Most startups lack the resources for decentralized health-data wallets, leaving trust gaps in U.S. jurisdictions sensitive to legal discovery. The top five players control slightly below 60% of active users, keeping competitive intensity high and margins moderate.

Menstrual Health Apps Industry Leaders

Flo Health

Glow Inc

Biowink GmbH

Ovia Health

Eve

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Maven Clinic began piloting Medicaid value-based contracts in three U.S. states, layering cycle tracking into broader maternal-health bundles.

- November 2025: Karnataka introduced 12 paid menstrual-leave days without medical certification, boosting employer demand for cycle-tracking audit trails.

- November 2025: Flo Health published peer-reviewed findings on 19 million user cycles, linking symptom clusters to luteal-phase hormone shifts.

- October 2025: Natural Cycles launched NC° Perimenopause, supporting users aged 45 plus with irregular cycles.

Global Menstrual Health Apps Market Report Scope

As per the scope of the report, the menstrual health application allows women to track their menstrual cycles and receive a prediction for their period dates. Most apps also provide predictions of ovulation day and the fertile window. The menstrual health apps market is segmented by application type (period cycle tracking, fertility and ovulation management, and menstrual health management), platform type (android, iOS, and other platforms), and geography (North America, Europe, Asia-Pacific, the Middle East, Africa, and South America). The report offers the value (in USD million) for the above segments.

| Period Cycle Tracking |

| Fertility & Ovulation Management |

| Menstrual Health Management & Symptom Analytics |

| Android |

| iOS |

| Others |

| 15 – 24 Years |

| 25 – 34 Years |

| 35 – 44 Years |

| 45 + Years (Peri- & Post-menopause) |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Application | Period Cycle Tracking | |

| Fertility & Ovulation Management | ||

| Menstrual Health Management & Symptom Analytics | ||

| By Platform | Android | |

| iOS | ||

| Others | ||

| By Age Group | 15 – 24 Years | |

| 25 – 34 Years | ||

| 35 – 44 Years | ||

| 45 + Years (Peri- & Post-menopause) | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current revenue size of the menstrual health apps market?

The menstrual health apps market size stood at USD 1.60 billion in 2026.

How fast is the market expected to grow?

The sector is forecast to post a 9.51% CAGR and reach USD 2.52 billion by 2031.

Which platform contributes most users?

Android devices held 57.61% of 2025 market share, driven by high penetration in Asia Pacific and Latin America.

Which application segment is expanding fastest?

Menstrual Health Management and Symptom Analytics is pacing ahead with a 10.34% CAGR through 2031.

Which region will see the highest growth?

Asia Pacific is projected to expand at a 10.59% CAGR through 2031 on the back of affordable smartphones and supportive legislation.

What drives employer adoption of cycle-tracking apps?

Policies like Karnataka’s 12-day menstrual-leave mandate and corporate benefit packages are pushing companies to fund app subscriptions that verify leave and support retention.

Page last updated on: