Men Grooming Appliances Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 7.71 Billion |

| Market Size (2031) | USD 9.44 Billion |

| Growth Rate (2026 - 2031) | 4.15% CAGR |

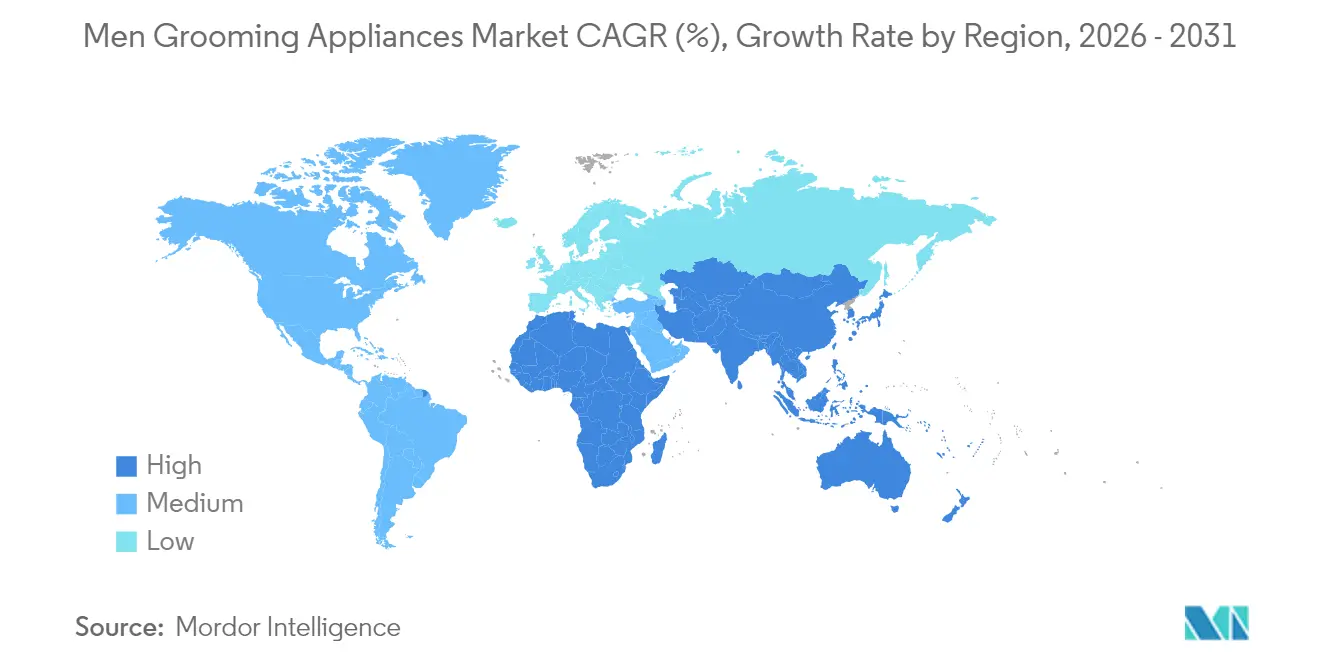

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Men Grooming Appliances Market Analysis by Mordor Intelligence

The men’s grooming appliances market size was valued at USD 7.40 billion in 2025 and estimated to grow from USD 7.71 billion in 2026 to reach USD 9.44 billion by 2031, at a CAGR of 4.15% during the forecast period (2026-2031). This growth is driven by increasing male interest in personal appearance, a shift toward multifunctional devices, and the rapid expansion of e-commerce. Grooming activities such as beard styling, body grooming, and hair maintenance are increasingly seen by men as integral to daily hygiene and self-expression rather than as acts of vanity. This change has fueled the adoption of shavers, trimmers, clippers, and body groomers. Social media platforms significantly aid product discovery, while AI-powered shavers and trimmers enhance personalization and boost perceived value. Hardware innovations now focus on cordless designs, lithium-ion batteries, and waterproof casings, enabling wet-dry versatility. While growth is evident across all regions, the Asia-Pacific region leads, with domestic brands offering competitive pricing and app-enabled features. The competitive landscape is becoming more challenging, particularly with the entry of Chinese brands whose aggressive pricing strategies are pressuring the margins of established players despite their brand heritage.

Key Report Takeaways

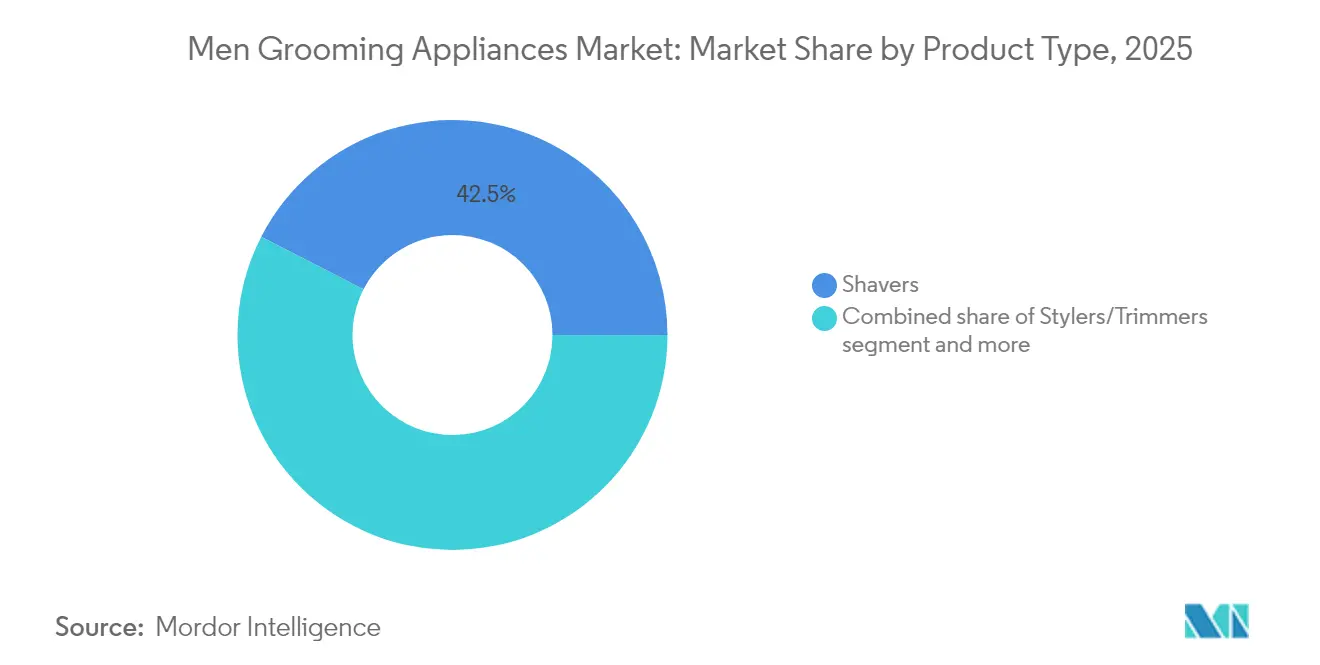

- By product type, shavers led with 42.45% revenue share in 2025, whereas stylers and trimmers are forecast to grow at a 4.72% CAGR to 2031.

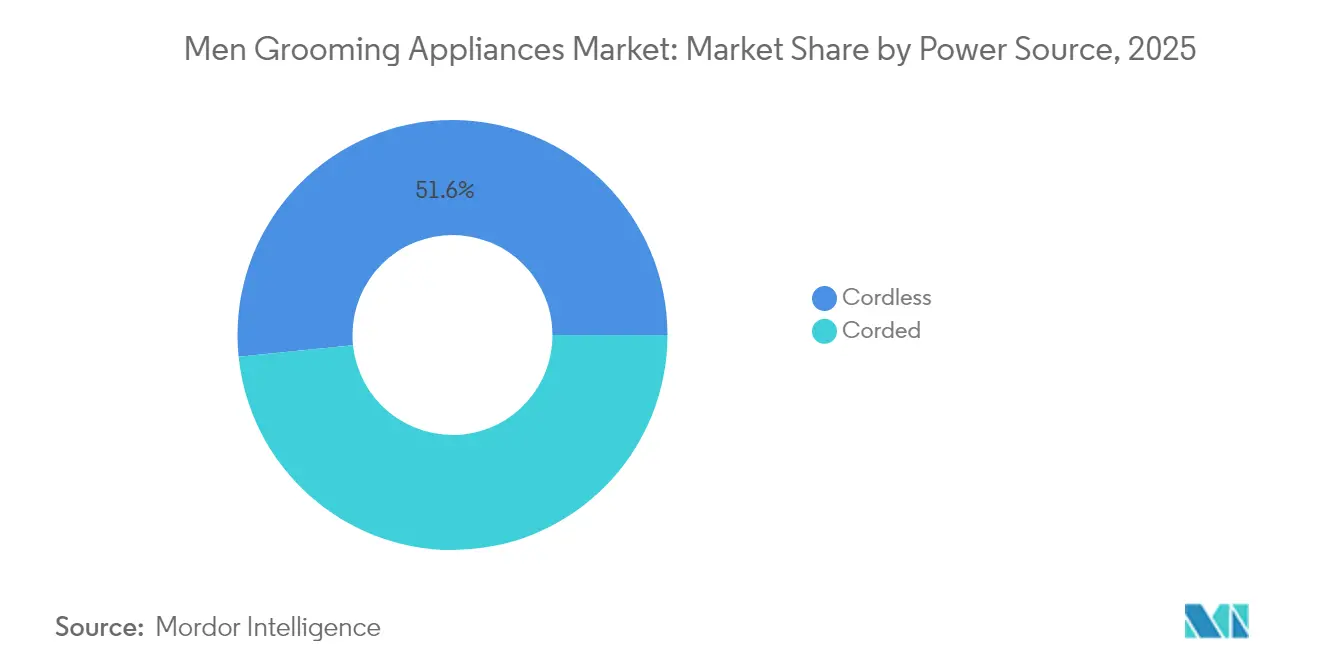

- By power source, cordless devices captured 51.62% of the men’s grooming appliances market share in 2025, while the same category is projected to expand at a 5.05% CAGR through 2031.

- By distribution channel, specialty stores retained 36.45% of the 2025 value, but online stores will record the fastest 5.55% CAGR to 2031.

- By region, North America held 38.25% of 2025 revenue, whereas the Asia-Pacific is poised for the highest 4.82% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Men Grooming Appliances Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising male-grooming consciousness and aspirational lifestyles | +1.2% | Urban Asia-Pacific and North America | Medium term (2-4 years) |

| The rising influence of social media and digital platforms is shaping the market | +0.9% | Gen Y and Gen Z globally | Short term (≤ 2 years) |

| Innovation in smart grooming appliances | +0.8% | North America and Europe first, Asia-Pacific for volume | Medium term (2-4 years) |

| Growing demand for multifunctional and compact grooming devices | +0.7% | Global, strongest in space-constrained urban markets | Long term (≥ 4 years) |

| Brand loyalty fostered by diversified product portfolios targeting different age groups | +0.5% | North America and Europe mature users, emerging in Asia-Pacific | Long term (≥ 4 years) |

| Introduction of waterproof and cordless grooming devices | +0.6% | Premium positioning in developed economies | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising male-grooming consciousness and aspirational lifestyles

Male grooming norms have transitioned from basic hygiene to a focus on refined aesthetics. The "looksmaxxing" trend, driven by Gen Z, prioritizes enhancing facial symmetry, skin texture, and grooming precision. This shift has fueled demand for devices that provide salon-quality results at home. Manufacturers are addressing this demand by marketing grooming appliances as tools for career progression and improved social confidence, rather than as products of vanity. This approach is particularly effective in the Asia-Pacific region, where Confucian values emphasizing professional appearance align with increasing disposable incomes. However, sustaining this growth poses a challenge as economic uncertainties impact discretionary spending, prompting consumers to assess the value of premium grooming devices more critically. In 2024, 51.71 million men were employed full-time in the U.S., according to the Bureau of Labor Statistics, reflecting a growing awareness of grooming among working men[1]Bureau of Labor Statistics, "Labor Force Statistics from the Current Population Survey", bls.gov. Employment reinforces appearance standards, increases social exposure, and raises the stakes for maintaining a well-groomed look. As more men take on formal and customer-facing roles, their adoption of regular grooming routines grows, driving demand for appliances like shavers, trimmers, and clippers.

The rising influence of social media and digital platforms is shaping the market

Instagram and YouTube have become significant platforms for product discovery. Among Indian male consumers, influencers' credibility and authenticity influence purchase intent more effectively than traditional advertising. Brands are leveraging this by partnering with micro-influencers to demonstrate practical product applications, such as shaving tutorials, beard-trimming techniques, and before-and-after transformations, which appeal to younger audiences. Wahl's Style Selector tool, which uses AI to simulate different beard styles on user-uploaded photos, highlights how digital engagement can lead to product trials. However, the effectiveness of this strategy varies by region: North American and European consumers prefer polished influencer content, while Asia-Pacific buyers focus on peer reviews and unboxing videos that emphasize value for money. The regulatory framework remains inconsistent, with no unified disclosure standards for sponsored grooming content, creating compliance challenges as jurisdictions enforce stricter influencer marketing rules. Furthermore, increasing internet usage among men is boosting social media connectivity. For example, in 2024, 70% of the global male population had access to the internet, according to the International Telecommunication Union (ITU)[2]International Telecommunication Union (ITU), "Facts and Figures 2024", itu.int.

Innovation in smart grooming appliances

Artificial intelligence is shifting from smartphones to personal care devices, turning grooming tools into responsive systems. Philips' i9000 series, priced between USD 180 to USD 420, boasts sensors that detect hair density 500 times a second. Using its SkinIQ algorithm, the series adjusts motor speed in real-time. Additionally, Bluetooth connectivity tracks shaving habits and, through a companion app, suggests maintenance schedules. Braun's Skin i-expert IPL device, unveiled in February 2024, employs AI to recognize skin tone and hair color across sessions, fine-tuning light intensity for comfort. While these advancements tackle a primary consumer issue, erratic results from manual tweaks, they also bring challenges: reliance on apps, the need for firmware updates, and concerns over data privacy. Navigating GDPR compliance in Europe and the shifting data-localization mandates in India and China complicates engineering efforts. Strategically, this suggests a market split: smart devices will carve out a premium connected segment and a more traditional offline value tier, leaving little room in between.

Growing demand for multifunctional and compact grooming devices

With urban spaces becoming smaller, the demand for multifunctional grooming devices is increasing. Panasonic's MULTISHAPE system features interchangeable heads for tasks such as shaving and body grooming, helping to minimize clutter and lower ownership costs. Similarly, Philips' 19-in-1 trimmer caters to consumers who prioritize versatility over specialized performance. This trend is particularly prominent in Asia-Pacific cities like Mumbai, Shanghai, and Tokyo, where storage space is limited, and in Latin America, where affordability drives the preference for multifunctional devices. However, a key challenge lies in ensuring that attachments designed for various body zones comply with differing safety and hygiene standards, complicating regulatory approvals. The IEC 60335-2-8 standard for electric shavers and hair clippers does not fully address these multi-use scenarios, prompting manufacturers to adopt cautious design approaches or pursue market-specific certifications.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cost of advanced grooming appliances | -0.6% | Asia-Pacific and Latin America price-sensitive buyers | Short term (≤ 2 years) |

| Concerns about device durability and maintenance requirements. | -0.4% | Mature markets with repeat-purchase fatigue | Medium term (2-4 years) |

| Potential skin irritation or allergies | -0.3% | Heightened awareness in Europe and North America | Long term (≥ 4 years) |

| Beard-styling trend lowers shave frequency | -0.5% | North America and Europe, emerging in urban Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High cost of advanced grooming appliances

Premium electric shavers, priced above USD 300, come with an additional cost: the high expense of replacement consumables. For example, Braun's Series 9 Pro+ heads cost USD 73, Philips' i9000 heads are priced at USD 63, and Panasonic's ES-LV97 heads retail for USD 65. Manufacturers generally recommend replacing these heads every 12 to 18 months. Australian consumer tests have shown similar findings, with mid-tier model replacement heads priced at approximately USD 33. These recurring costs can be a shock, particularly in price-sensitive markets where annual replacement expenses nearly equal the cost of a new budget shaver. To address this, brands have adopted a two-pronged strategy: Philips OneBlade appeals to cost-conscious consumers with replacement heads priced at USD 17, while premium lines justify their higher prices by offering AI features and app connectivity. However, this strategy poses a risk: if consumers perceive limited value in advanced features, premium sales could decline. Additionally, the lack of standardized durability testing under IEC 60335-2-8 enables manufacturers to set replacement intervals that prioritize consumable revenue over product longevity. This practice may eventually attract regulatory scrutiny.

Beard-styling trend lowers shave frequency

The prevalence of facial hair among men aged 18 to 38 has significantly increased, with more individuals opting for beards, stubble, or mustaches. This growing trend has led to a noticeable decline in the demand for daily shaving, compelling blade manufacturers to adapt their strategies. In response, electric shaver brands are shifting their focus toward stylers and trimmers—devices specifically designed to groom and maintain facial hair rather than remove it entirely. However, this strategic shift presents a challenge, as trimmers do not generate the recurring revenue associated with consumable products like replacement blades or shaver heads, thereby compressing profit margins. The increasing popularity of facial hair is not merely a passing fashion trend; it is deeply rooted in psychological factors such as the desire for affiliation, status enhancement, and mate attraction. These underlying motives suggest that the trend is likely to persist beyond typical fashion cycles. Consequently, shaver manufacturers are faced with a critical decision: either expand their product offerings to include beard-care solutions and related adjacencies or prepare for structurally lower growth rates in their core product categories.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Stylers Surge While Shavers Hold Scale

Shavers accounted for a significant 42.45% share of the market value in 2025, underscoring the impact of decades-long brand investments by leading players such as Philips, Braun, and Panasonic. This dominance reflects the sustained efforts of these companies in building brand equity and consumer trust. As beard grooming increasingly replaces the traditional practice of daily shaving, the stylers and trimmers segment is expected to grow at a compound annual growth rate (CAGR) of 4.72% through 2031, surpassing the overall market growth rate. While epilators cater to body grooming and hair clippers address DIY haircuts, both are witnessing modest growth as consumers increasingly turn to home grooming to cut down on salon visits. Highlighting a trend, Philips' 19-in-1 trimmer and Panasonic's MULTISHAPE platform showcase manufacturers' strategy of bundling products into modular systems, tapping into cross-category spending. While IEC 60335-2-8 regulatory compliance ensures electric shavers and clippers meet baseline safety standards, it falls short of fully addressing multi-use attachments. This oversight leaves manufacturers to navigate the gap, often opting for conservative designs or seeking market-specific certifications.

The rising popularity of stylers is altering the competitive landscape. Traditional shaver brands are feeling the pinch on margins, as trimmers don't offer the recurring revenue from replacement blades or foil cartridges, historically a subsidy for device pricing. Wahl and Andis, once synonymous with professional barber tools, are carving out retail space by spotlighting precision-trimming features that appeal to the modern beard enthusiast. Meanwhile, Chinese brands like Xiaomi and Flyco are shaking up the market with app-connected trimmers, priced 30% to 40% lower than their Western counterparts. This aggressive pricing strategy pressures established brands to defend their premium pricing through advanced AI features or by leaning on their brand legacy. Despite clinical evidence suggesting mechanical epilation only leads to temporary immune activation and reduced melanogenesis, epilators remain a niche category, hindered by lingering discomfort perceptions. Hair clippers enjoyed a surge during pandemic lockdowns as DIY haircuts became the norm, but demand has since stabilized with the reopening of salons.

By Power Source: Cordless Dominance Accelerates

Cordless devices accounted for 51.62% of the market value in 2025 and are expected to grow at a 5.05% CAGR through 2031. This growth is primarily driven by advancements in lithium-ion batteries, which now provide runtimes of 90 to 150 minutes, and the adoption of IPX7 waterproofing, enhancing their wet-dry functionality. Xiaomi's 2024 electric shaver illustrates this trend, offering 90 minutes of cordless operation, USB-C fast charging, and full submersion capability, all priced under USD 50. Similarly, Philips' i9000 series extends runtime to 150 minutes and features wireless charging, targeting premium consumers who prioritize convenience over cost. While corded devices remain essential in professional barber shops due to their need for uninterrupted power, their market share is declining as battery technology continues to close the performance gap.

Regulatory developments in various regions are increasingly supporting cordless designs. For example, Europe's Ecodesign Directive and WEEE regulations impose compliance costs on corded devices, requiring end-of-life disassembly and recycling. Although cordless models with lithium-ion batteries are subject to stricter disposal rules under the EU Battery Directive, manufacturers mitigate these challenges through take-back programs that also enhance customer retention. In China, the CCC certification process for corded appliances involves more stringent electromagnetic compatibility testing compared to battery-powered devices, creating a regulatory advantage for cordless designs. In India, the BIS IS 302-2-8 standard applies equally to both power sources, but cordless devices are better suited to tier-2 and tier-3 cities, where frequent power outages make them more practical. This indicates a strategic shift: cordless designs are set to dominate, while corded devices will be confined to professional niches and ultra-budget segments, where consumers prioritize affordability over convenience.

By Distribution Channel: Online Momentum Strengthens

Specialty stores represented 36.45% of the market value in 2025, highlighting their critical role in product demonstrations and fulfilling immediate consumer needs. These stores hold a significant share of the men’s grooming appliances market due to their emphasis on premium brands, expert guidance, and the appealing “try before you buy” experience. This approach enhances the shopping experience and drives their value share above their volume share. Online stores, supported by Amazon's Prime Day promotions and the growth of direct-to-consumer brands, are projected to grow at a 5.55% CAGR through 2031, steadily gaining ground over traditional retail. E-commerce platforms offer advantages such as unlimited shelf space and dynamic pricing. For example, a consumer can compare 50 electric shavers online in just 10 minutes, a task that is challenging in physical stores, limited to 8 to 12 SKUs. Amazon's beauty category, which includes grooming appliances, experienced growth through 2024, with men’s personal care emerging as a high-potential segment. While supermarkets, hypermarkets, and other channels like department stores and airport duty-free shops cater to convenience-focused purchases, they lack the assortment depth and price transparency that online platforms provide.

The shift to online platforms is transforming the economics of specialty retailers. The importance of in-store demonstrations, such as feeling a shaver's weight or testing its motor, has decreased as YouTube reviews and influencer unboxings offer virtual trials. In response, brands are increasingly treating specialty stores as showrooms. For example, Philips and Braun maintain flagship displays in high-traffic malls but redirect purchase intent to their e-commerce platforms using QR codes and exclusive online bundles. This strategy helps maintain retail relationships while capturing higher-margin direct sales. However, it also creates challenges: inventory fragmentation and return complexities arise when consumers research in-store, purchase online, and return items to physical locations. Additionally, regulatory compliance adds further complications. For instance, the EU's Digital Services Act holds platforms accountable for counterfeit grooming appliances, prompting companies like Amazon and Alibaba to strengthen their seller vetting processes.

Geography Analysis

North America accounted for 38.25% of the global market value in 2025, supported by high per-capita grooming expenditures and a well-developed retail infrastructure. However, growth is expected to slow. The increasing popularity of beard styling is reducing shaving frequency, while economic uncertainties are limiting discretionary spending. The U.S. remains the largest individual market, as evidenced by Procter and Gamble's USD 1.3 billion impairment charge on Gillette, highlighting the challenges faced by traditional shaving products. Canada and Mexico, though smaller contributors, are experiencing faster growth due to urbanization and a growing awareness of male grooming. The U.S. has a significant male population, which supports the grooming appliances market. According to the U.S. Census Bureau, the male resident population reached 168.34 million in 2024. Regulatory requirements in North America are relatively simple: the FDA classifies electric shavers as Class I medical devices, requiring registration and device listing but no premarket approval. Additionally, the UL 60335-2-8 certification ensures electrical safety, a standard most global manufacturers incorporate into their designs. A key challenge in the region is the shift toward budget-friendly options. Superdrug's 17% year-over-year increase in own-brand razor sales reflects declining brand loyalty as consumers prioritize cost.

Asia-Pacific is projected to achieve the fastest regional CAGR of 4.82% through 2031, driven by urbanization, increasing disposable incomes, and the availability of affordable devices from Chinese manufacturers. Domestic Chinese brands such as Xiaomi, Flyco, and Midea's Povos label are gaining market share by leveraging app connectivity and competitive pricing, particularly in tier-2 and tier-3 cities where grooming appliances are becoming essential rather than aspirational. In India, brands like Havells, Nova, and SSK are targeting the mass market with trimmers priced below USD 30, while Philips focuses on the premium segment with AI-powered shavers. Japan and South Korea, though mature and high-value markets, face growth limitations. Companies like Panasonic and Hitachi emphasize precision engineering and skincare integration, but aging populations and market saturation constrain expansion. Regulatory requirements vary across the region: in China, the CCC certification and GB standards can delay product launches by 6 to 9 months, while India's BIS IS 302-2-8 standard mandates local testing, favoring domestic manufacturers. Southeast Asia, including Thailand, Indonesia, and Singapore, is emerging as a competitive market, with Western and Chinese brands competing for first-time buyers in rapidly urbanizing areas.

Europe faces growth challenges due to sustainability mandates and economic stagnation, but it remains strategically important because of high average selling prices and strong brand loyalty. Compliance with the CE marking under the Low Voltage Directive 2014/35/EU, as well as REACH, RoHS, and the WEEE Directive, increases costs. This environment benefits established players like Philips, Braun, and Groupe SEB, which have developed reverse-logistics networks for recycling end-of-life products. While the UK, Germany, France, Italy, and Spain dominate European sales, Eastern Europe—particularly Poland and Russia—is growing faster due to changing grooming norms and improved retail infrastructure. South America and the Middle East and Africa, though smaller markets, are gaining attention as disposable incomes rise. However, Brazil's INMETRO certification and the UAE's ESMA conformity standards create entry barriers that slow market growth but also protect early entrants from low-cost competitors.

Competitive Landscape

The men’s grooming appliances market is moderately consolidated. Philips, Procter and Gamble (Braun, Gillette), and Panasonic lead the men's grooming appliances market, holding a substantial global share. However, Chinese entrants such as Xiaomi, Flyco, and Midea are gaining traction by offering competitive pricing and app-enabled features that appeal to younger consumers. In response, established players are expanding their product portfolios. For example, Panasonic's MULTISHAPE modular system and Philips' 19-in-1 trimmer integrate multiple grooming functions into a single device. This approach lowers the total cost of ownership for consumers while increasing switching costs. However, it also compresses profit margins, as multifunctional devices lack the recurring revenue streams generated by replacement blades or foil cartridges. Opportunities exist in skincare integration, such as devices that combine shaving with exfoliation or moisturizer application, and in subscription models that bundle consumables with device financing, though consumer adoption remains uncertain. Additionally, direct-to-consumer brands are disrupting the market by bypassing retail markups, while Chinese appliance manufacturers are supplying private-label products to retailers like Superdrug.

Major players in the market include Procter and Gamble Company, Koninklijke Philips N.V., Panasonic Corporation, Spectrum Brands Holdings, Inc., and Wahl Clipper Corporation. These companies are focusing on innovation through advanced technologies, such as cordless operation, extended battery life, and AI-enabled features, to differentiate their products. Strategic expansion via omnichannel distribution networks is also a priority, with firms partnering with online retailers and strengthening their direct-to-consumer channels. Many companies are demonstrating operational flexibility by localizing manufacturing in emerging markets while maintaining global quality standards. Additionally, market leaders are emphasizing sustainability and customer-centric approaches by offering personalized grooming solutions and improved after-sales services.

As hardware becomes increasingly commoditized, technology is emerging as the primary differentiator. Philips' i9000 series features sensors that measure hair density 500 times per second, adjusting motor speed using its SkinIQ algorithm. Similarly, Braun's Skin i-expert IPL employs AI to optimize light intensity based on skin tone over multiple sessions. Wahl's Style Selector tool leverages AI to simulate beard styles on user-uploaded photos, converting digital engagement into product trials. However, these innovations also introduce challenges, such as app dependency, firmware updates, and data privacy concerns. Regulatory frameworks like GDPR and China's Personal Information Protection Law are only beginning to address these issues. The strategic implication is that companies capable of balancing hardware performance, software intelligence, and regulatory compliance will gain a competitive advantage, while those relying solely on brand heritage or distribution scale risk losing market share to more agile competitors.

Men Grooming Appliances Industry Leaders

-

Koninklijke Philips N.V.

-

Panasonic Corporation

-

Wahl Clipper Corporation

-

Procter and Gamble Company

-

Spectrum Brands Holdings, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: MANSCAPED has unveiled the Weed Whacker 3.0 Pro, an electric trimmer tailored for nose, ear, and eyebrow hair. This latest iteration boasts enhanced features, ensuring precision grooming.

- July 2025: Panasonic Corporation unveiled The Barikan, its latest series of professional clippers, targeting hair and beauty practitioners as part of its push into the global market.

- July 2025: Panasonic unveiled LAMDASH linear shaver ES-L690U. The new shaver boasts a shaving sensor that adjusts power based on stubble thickness, seamlessly toggling between BOOST and SOFT modes for a gentle yet close shave. Additionally, it incorporates a Direct Magnetic Linear Motor Drive operating at 14,000 cpm.

- April 2025: Philips has unveiled its most advanced shaver to date: the i9000 Shaver Series, setting a new standard in premium, personalized male grooming.

Global Men Grooming Appliances Market Report Scope

| Shavers |

| Stylers/Trimmers |

| Epilators |

| Hair Clippers |

| Corded |

| Cordless |

| Supermarkets/Hypermarkets |

| Specialty Stores |

| Online Stores |

| Other Distribution Channels |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Sweden | |

| Belgium | |

| Poland | |

| Netherlands | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Thailand | |

| Singapore | |

| Indonesia | |

| South Korea | |

| Australia | |

| New Zealand | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| South Africa | |

| Saudi Arabia | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| Product Type | Shavers | |

| Stylers/Trimmers | ||

| Epilators | ||

| Hair Clippers | ||

| Power Source | Corded | |

| Cordless | ||

| Distribution Channel | Supermarkets/Hypermarkets | |

| Specialty Stores | ||

| Online Stores | ||

| Other Distribution Channels | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Sweden | ||

| Belgium | ||

| Poland | ||

| Netherlands | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Thailand | ||

| Singapore | ||

| Indonesia | ||

| South Korea | ||

| Australia | ||

| New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| South Africa | ||

| Saudi Arabia | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current global value of the men’s grooming appliances market?

The segment is valued at USD 7.71 billion in 2026 and is forecast to reach USD 9.44 billion by 2031.

Which product category is expanding the fastest?

Stylers and trimmers are projected to grow at a 4.72% CAGR, outpacing shavers and other segments.

Why are cordless grooming devices becoming more popular?

Longer lithium-ion runtimes, USB-C charging, and full waterproof ratings make cordless models more convenient than corded options.

Which geography is set to record the highest growth through 2031?

Asia Pacific is expected to post the fastest 4.82% CAGR through 2031, helped by rising disposable incomes and competitively priced domestic brands.

Page last updated on: