Membrane Contactor Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

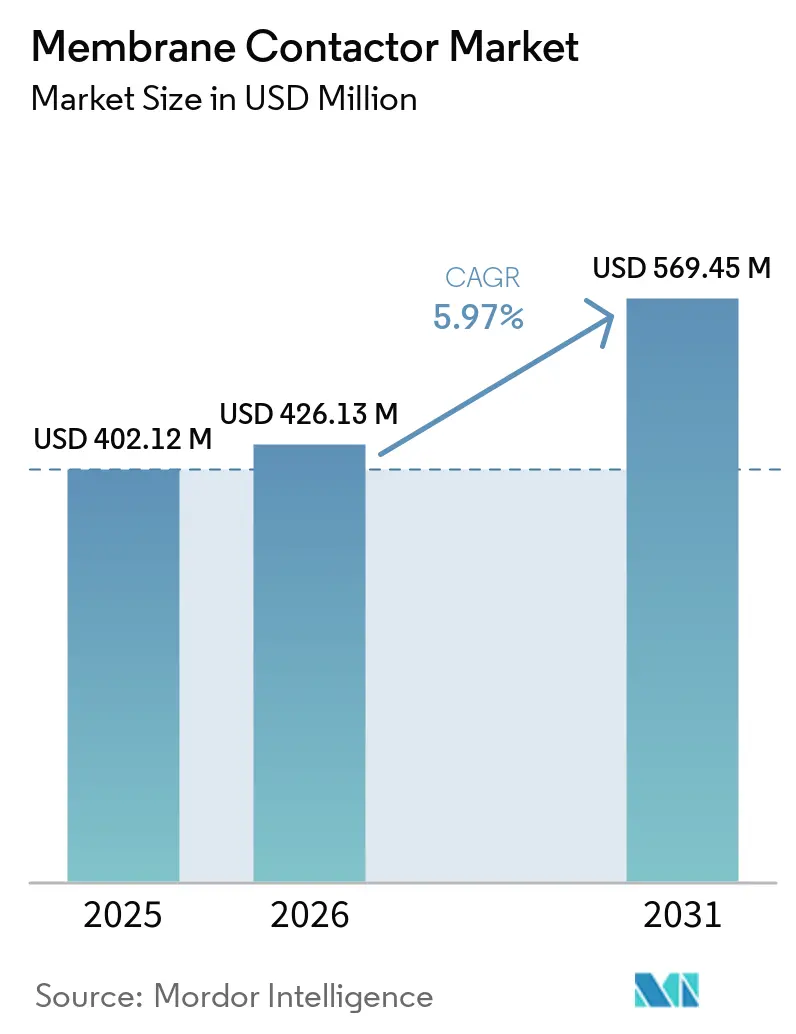

| Market Size (2026) | USD 426.13 Million |

| Market Size (2031) | USD 569.45 Million |

| Growth Rate (2026 - 2031) | 5.97% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Membrane Contactor Market Analysis by Mordor Intelligence

The Membrane Contactor Market size is expected to increase from USD 402.12 million in 2025 to USD 426.13 million in 2026 and reach USD 569.45 million by 2031, growing at a CAGR of 5.97% over 2026-2031. Compact membrane units are now preferred over traditional vacuum deaerators and packed columns. These units effectively maintain low dissolved-oxygen levels and achieve high carbon-dioxide removal without any thermal drawbacks. Investments are pouring into beverage bottling, ultrapure-water systems for semiconductors, and modular carbon-capture skids. These investments align with corporate decarbonization objectives, emphasizing the need for energy-efficient gas-transfer solutions. Innovations in hollow-fiber and spiral-wound modules have significantly reduced skid footprints and power demand compared to older systems. In North America and Europe, pharmaceutical and biotechnology projects are facing accelerated order backlogs. This surge is largely due to membrane contactors being integrated as the polishing stage in non-distillation water-for-injection trains, a move endorsed by the European Pharmacopeia. In the Asia-Pacific region, mandates for zero-liquid discharge and an expanding biogas-upgrading pipeline are bolstering the demand for polypropylene and polyvinylidene fluoride membranes. These membranes are favored for their ability to withstand aggressive chemicals and elevated temperatures.

Key Report Takeaways

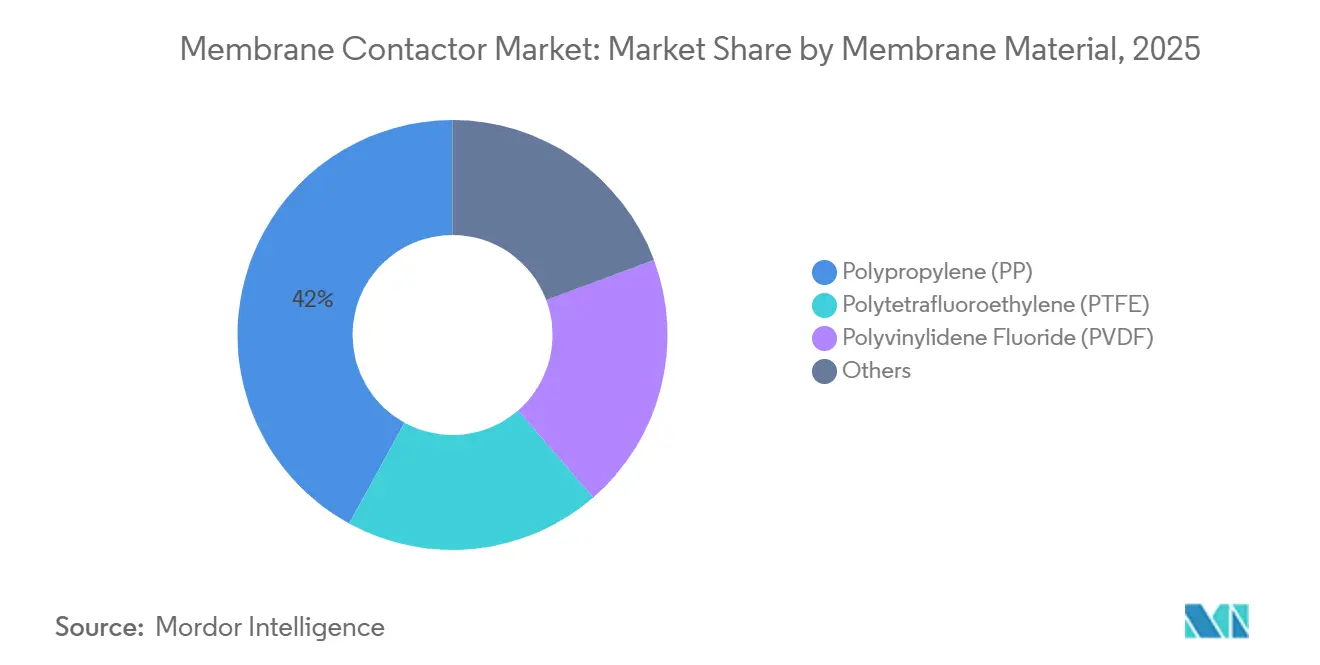

- By membrane material, polypropylene held 42.03% of the global membrane contactor market share in 2025; PVDF is projected to expand at a 6.26% CAGR over 2026-2031.

- By module configuration, hollow-fiber designs led with 56.33% revenue share in 2025, whereas spiral-wound modules are expected to advance at a 6.38% CAGR over 2026-2031.

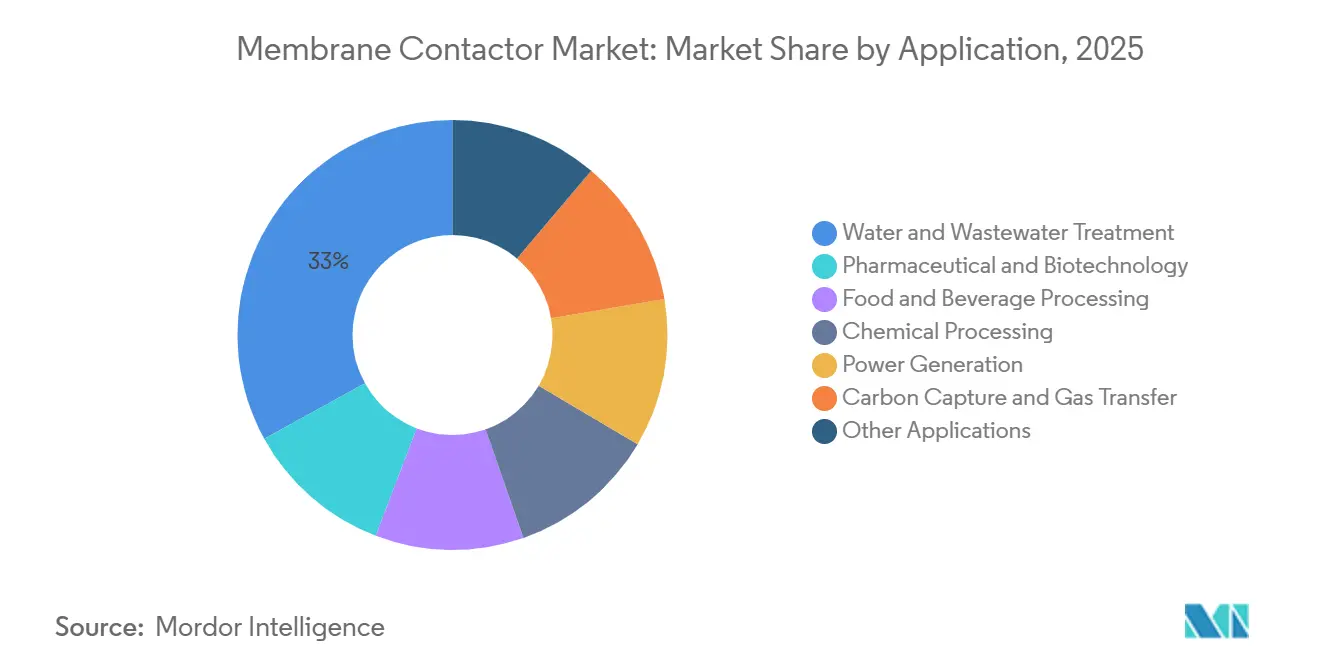

- By application, water and wastewater treatment accounted for 33.02% of 2025 revenue, while carbon capture and gas transfer is forecast to record a 6.42% CAGR over 2026-2031.

- By end user, industrial plants commanded 45.22% of 2025 sales; healthcare facilities are poised for the fastest 6.33% CAGR over 2026-2031.

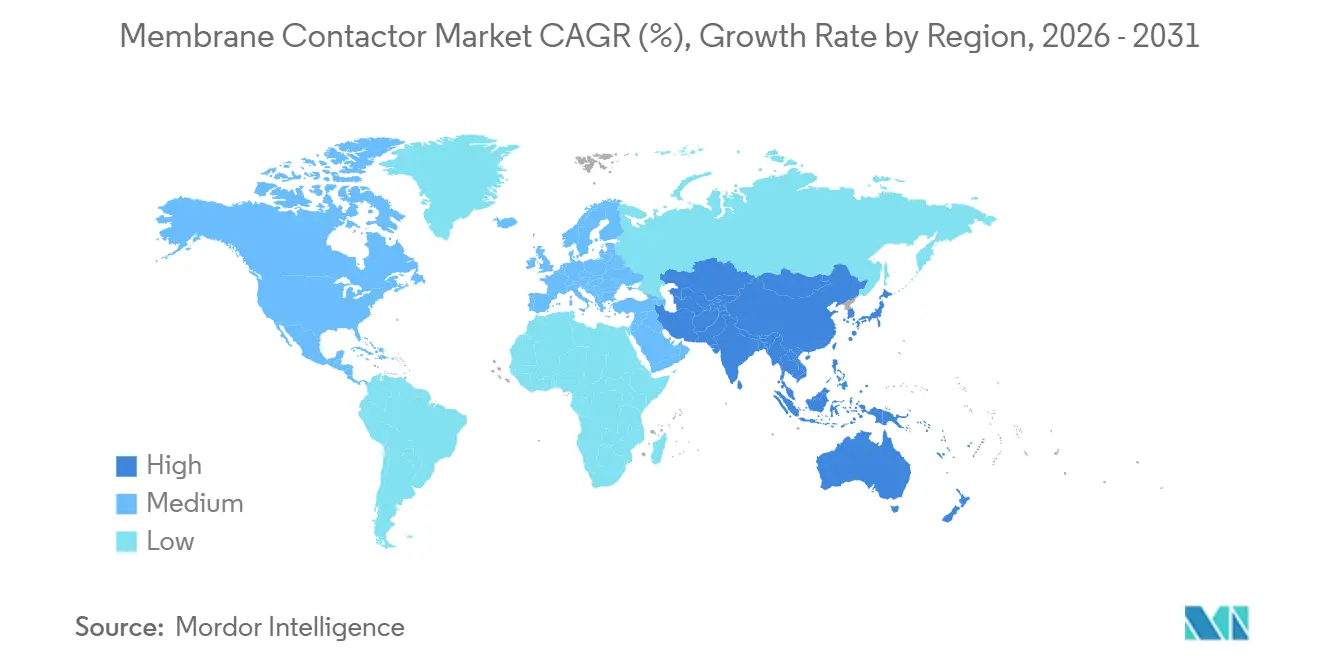

- By geography, Asia-Pacific contributed 40.28% to the 2025 turnover and is set to grow at a 6.56% CAGR over 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Membrane Contactor Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Efficient degassing demand in water and beverage processing | +1.20% | Global, with concentration in North America, Europe, and the Asia-Pacific beverage hubs | Medium term (2-4 years) |

| Adoption in pharma and biotech ultrapure utilities | +1.50% | North America and Europe (primary), Asia-Pacific emerging | Long term (≥ 4 years) |

| Compact modular gas-transfer systems for industrial retrofit | +0.90% | Global, with early adoption in North America and Europe | Short term (≤ 2 years) |

| Stricter nitrogen-discharge rules spurring ammonia stripping | +1.10% | Europe (EU UWWTD), North America (EPA NPDES), Asia-Pacific select markets | Medium term (2-4 years) |

| Scale-up for cryogenic biomethane liquefaction pre-treatment | +0.80% | Europe (biogas upgrading), North America (renewable natural gas), Asia-Pacific pilot projects | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Efficient Degassing Demand in Water and Beverage Processing

Compact membrane skids are now a staple in soft-drink, brewing, and packaged-water lines, effectively reducing dissolved oxygen levels to minimal levels without compromising volatile flavor compounds. In a notable shift, a major North American bottler transitioned from traditional vacuum deaerators to a Liqui-Cel unit, achieving significant cost savings through enhanced yield gains and a substantial reduction in energy consumption[1]3M, “Beverage Degassing Case Study,” 3m.com. Breweries are now retrofitting modules that occupy minimal space, sidestepping civil works and ensuring continuous process uptime. In Europe, beverage plants are enhancing their processes by integrating high-temperature water sterilization with adaptable clean-in-place cycles. This not only extends the membrane life significantly but also boosts product shelf life by curbing oxidative staling in beer and preventing vitamin degradation in soft drinks.

Adoption in Pharma and Biotech Ultrapure Utilities

Following the European Pharmacopeia's endorsement of non-distillation water for injection, membrane-based water for injection has captured a significant share of the installed capacity. At INCOG BioPharma’s Indiana fill-finish site, designed for large-scale production, membrane contactors ensure residual carbon dioxide and oxygen are polished, maintaining conductivity within stringent limits. Both Genentech’s facility in Holly Springs and Novo Nordisk’s site in North Carolina aim for extremely low oxygen levels in their biologic formulations. This precision is achieved using polyvinylidene fluoride hollow fibers, which can endure repeated oxidant cleaning. Notably, these methods offer substantial energy savings compared to multi-effect distillation, aligning seamlessly with net-zero roadmaps.

Compact Modular Gas-Transfer Systems for Industrial Retrofit

Manufacturers are increasingly opting for skid-mounted membrane packages, which can be installed in brownfield sites within a short timeframe. QILEE offers ammonia-stripping containers in various capacities, requiring only utility connections. Pentair's Helix spiral geometry enhances flux and reduces specific energy consumption in leachate treatment trials. Envirogen supplied an ultrapure-water skid, featuring capacitive de-ionization polishing, to Kemira, demonstrating quick paybacks even in space-limited chemical plants.

Stricter Nitrogen-Discharge Rules Spurring Ammonia Stripping

Under the European Commission’s Directive C(2026)662, recovered ammonium sulfate can now exceed the nitrogen application limits in nitrate-vulnerable zones. This regulatory change enhances the economic viability of membrane stripping. By utilizing hollow-fiber contactors alongside acid absorption, operators achieve high levels of ammonia capture, producing fertilizer with significant market value. In the United States, updates to the National Pollutant Discharge Elimination System have imposed stricter nitrate limits in water. This has driven the adoption of hydrophobic polypropylene contactors, which efficiently strip ammonia without creating sludge contaminated with per- and polyfluoroalkyl substances.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capital and operations and maintenance costs | -0.70% | Global, with acute sensitivity in price-competitive municipal tenders and emerging markets | Short term (≤ 2 years) |

| Membrane wetting/fouling in high-organic streams | -0.60% | Industrial wastewater (tannery, food processing, oily streams), chemical processing | Medium term (2-4 years) |

| Helium scarcity is inflating specialty module costs | -0.30% | Global supply chain, affecting high-performance PTFE and specialty composite membranes | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Capital and Operations and Maintenance Costs

Membrane contactors involve significantly higher capital expenditures compared to vacuum towers for similar flow rates. The cost of modules for membrane contactors is substantially greater than that of vacuum towers. Furthermore, membrane contactors require periodic replacement and regular chemical cleanings, leading to additional operational expenses over time[2]Applied Membranes, “Operating Cost Guidelines,” appliedmembranes.com. Economics improve where operators monetize energy or footprint savings, yet budget-constrained municipalities in South Asia often defer upgrades in favor of low-tech systems.

Membrane Wetting/Fouling in High-Organic Streams

Effluents from tanneries and food processing, rich in fats and proteins, wet hydrophobic pores. This process disrupts the gas-liquid interface, significantly reducing flux over time. While aggressive oxidant cleaning methods can reduce the lifespan of polypropylene, polyvinylidene fluoride, produced through thermally induced phase separation, offers better resistance to chemical attacks but is more expensive. Additionally, pretreatment steps such as coagulation and activated carbon treatments increase annual operations and maintenance costs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Membrane Material: PVDF Gains on Chemical Durability

The Global membrane contactor market size for membrane materials showed polypropylene at 42.03% in 2025, while PVDF’s superior resistance under pH 1-10 and 175 °C drives a 6.26% CAGR over 2026-2031. Pharmaceutical ammonia-stripping and biogas installations, which require frequent oxidant sanitization, rely on polyvinylidene fluoride modules. While polytetrafluoroethylene finds limited application in semiconductor ultrapurification, it is primarily due to the premium quality control associated with helium. Asahi Kasei's innovative double-skin polyvinylidene fluoride fibers not only reduce leakage risks but also incorporate cross-flow solids retention, streamlining both purification and concentration in a single pass.

While commercial initiatives are exploring membranes made from biological sources, they remain in the pilot phase. This is largely because alternatives have yet to match polyvinylidene fluoride’s renowned hydrophobicity and tensile strength. However, as regulatory bodies intensify scrutiny on fluorinated polymers, there is a noticeable increase in collaborative research and development. This partnership between membrane manufacturers and chemical recyclers aims to pioneer solvent-free production methods and establish closed-loop take-back systems.

By Module Configuration: Spiral-Wound Accelerates in Retrofits

The 2025 Global membrane contactor market share for hollow-fiber modules reached 56.33%, reflecting high surface area (>1,000 m²/m³) and backwash capability. Spiral-wound units are forecast for a 6.38% CAGR over 2026-2031. Thanks to slimmer housings designed for rack-mount retrofits, spiral-wound pervaporation membranes have been shown, in techno-economic studies on solvent dehydration, to significantly enhance mass transfer and reduce energy consumption compared to hollow fibers. Additionally, Pentair's Helix turbulence promoters contribute to notable increases in flux, making spiral systems ideal for leachate and industrial wastewater retrofits. Meanwhile, flat-sheet cassettes continue to be favored in laboratory screenings and specialized blood-oxygenation devices, where the speed of membrane changeouts takes precedence over packing density.

By Application: Carbon Capture Accelerates Fastest

Water and wastewater treatment represented 33.02% of market demand in 2025, spanning municipal potable-water degassing, industrial boiler feedwater deaeration, and zero-liquid-discharge ammonia stripping. Carbon capture and gas transfer is the fastest-growing application at 6.42% CAGR through 2026 to 2031. The European Union aims to expand operational carbon capture and storage facilities by 2025, while the UK invests in HyNet and East Coast Track-1 clusters. Projects like Northern Lights and STRATOS target direct-air capture. Hollow-fiber membrane contactors, offering high interfacial area and flood resistance, outperform packed columns in offshore and modular carbon capture. These are integral to EU Horizon projects like MEMCARB (CO2 and methane separation), MemCat (CO2 to ethylene conversion), and DAM4CO2 (photocatalytic membranes). In pharmaceuticals, they ensure ultrapure-water degassing and solvent dehydration, meeting US and European Pharmacopeia standards. In food and beverages, they enhance shelf life by combating oxygen-induced flavor degradation. Chemical processing benefits from solvent degassing and ammonia recovery, turning waste into ammonium sulfate. Power generation uses them for boiler feedwater treatment, preventing corrosion. Emerging applications in aquaculture, medical devices, and hydrogen purification are gaining research and development focus due to advancements in membrane materials and designs.

By End-User Industry: Healthcare Fastest on Biopharma Expansion

The industrial end-user segment held 45.22% market share in 2025, encompassing chemical manufacturing, oil and gas, metals and mining, and pulp and paper, where membrane contactors serve in wastewater ammonia stripping, process-water degassing, and solvent recovery. Healthcare is the fastest-growing end-user at 6.33% CAGR through 2026 to 2031. North America's pharmaceutical and biotechnology facilities have expanded capacities, supported by rising drug approvals. Investments target expansions in Indiana, new facilities in Holly Springs, and developments in North Carolina. These facilities use membrane contactors for ultrapure water injections and clean utilities. The European Pharmacopeia's approval of membrane-based water injections has driven global adoption, reducing energy use and boiler maintenance. In the food and beverage sector, breweries, soft-drink bottlers, and dairy processors use membrane contactors to control dissolved gases, preventing oxidation and spoilage. Additionally, industries like power, electronics, textiles, and aquaculture increasingly adopt membrane technologies for efficiency and cost savings.

Geography Analysis

Asia-Pacific generated 40.28% of 2025 revenue and is projected to grow at 6.56% CAGR over 2026-2031 as China's push for zero-liquid-discharge and its semiconductor expansion are driving up demand. DuPont's acquisition of Sinochem RO Memtech showcases localized module manufacturing, cutting down on import duties and logistics emissions. In Japan, major membrane producers are supplying polyvinylidene fluoride fibers to local pharmaceutical and display-panel manufacturing facilities, bolstered by robust quality-system certifications.

In North America, the expansion of biopharmaceuticals, advanced batteries, and semiconductor manufacturing facilities is spurring a surge in high-purity water demand. Projects from Genentech and Novo Nordisk are significantly increasing water for injection capacity, utilizing multiple contactor banks. Veolia's substantial deal with a chip manufacturing facility in the Midwest underscores the trend of water-intensive reshoring. Meanwhile, revisions by the United States Environmental Protection Agency on nitrates are tightening effluent standards, leading to a rise in ammonia-recovery systems.

Europe continues to lead in carbon capture and biomethane initiatives. The number of operational carbon capture and storage sites has grown significantly from 2024 to 2025. In the United Kingdom, the HyNet and East Coast clusters are paving the way for long-term markets for membrane carbon dioxide transfer skids. In Spain, Royal Decree 1085/2024 has spurred PURON membrane bioreactor retrofits, combining biological treatment with membrane degassing to meet irrigation-reuse standards.

South America, along with the Middle East and Africa, is emerging as a new frontier. Petrobras's floating production storage and offloading projects and Saudi Arabia's industrial wastewater reuse initiatives are turning to membrane modules for managing sulfate and ammonia. However, challenges like price sensitivity and a lack of service infrastructure are moderating rapid expansion.

Competitive Landscape

The Membrane Contactor Market is moderately concentrated. These multinationals leverage proprietary hollow-fiber and spiral-wound patents, bolstered by extensive global after-sales networks. In a strategic move, Parker Hannifin acquired Filtration Group in a deal that significantly enhances its filtration sales and strengthens its aftermarket presence by integrating with Filtration Group’s established service network. Veolia, with its acquisition of Water Technologies, aims to achieve substantial cost synergies, solidifying its role in delivering projects for semiconductor and biomethane facilities.

Membrane Contactor Industry Leaders

3M

DuPont

Alfa Laval

Asahi Kasei Corporation

Veolia Water Technologies, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: The European Commission has adopted Directive C(2026)662, amending the Nitrates Directive. This update permits RENURE fertilizers, including ammonium sulfate from membrane ammonia stripping, to exceed 170 kg nitrogen per hectare annually under strict traceability and quality standards. The directive is accelerating the adoption of ammonia recovery technologies, boosting fertilizer production, and driving growth in the membrane contactor market, particularly in livestock and wastewater treatment applications.

- November 2025: Parker Hannifin agreed to acquire Filtration Group for USD 9.25 billion. This acquisition expanded Parker's industrial filtration portfolio, adding USD 2 billion in sales, a 23.5% EBITDA margin, and 85% aftermarket revenue. Parker expects to achieve USD 220 million in synergies by the third year. This move strengthens Parker’s position in the membrane contactor market, enabling it to capitalize on global retrofit and service opportunities.

Global Membrane Contactor Market Report Scope

A membrane contactor is a separation device that uses a microporous or nonporous membrane to bring two phases, typically liquid and gas, into close contact without mixing. It enables selective mass transfer, such as removing dissolved gases or recovering volatile compounds, while preventing bulk flow. This technology is widely applied in water treatment, biogas upgrading, and ammonia recovery, offering compact design, high efficiency, and scalability.

The Membrane Contactor Market is segmented by membrane material, module configuration, application, end user industry, and geography. By Membrane Material, the market is segmented into polypropylene (PP), polytetrafluoroethylene (PTFE), polyvinylidene fluoride (PVDF), and others. By Module Configuration, the market is segmented into hollow fiber, flat sheet, and spiral wound. By Application, the market is segmented into water and wastewater treatment, pharmaceutical and biotechnology, food and beverage processing, chemical processing, power generation, carbon capture and gas transfer, and other applications. By end-user industry, the market is segmented into industrial, healthcare, food and beverage, power and energy, and other industries. The report also covers the market size and forecasts for the Global Membrane Contactor Market in 19 countries across major regions. The market sizes and forecasts are provided in terms of value (USD).

| Polypropylene (PP) |

| Polytetrafluoroethylene (PTFE) |

| Polyvinylidene Fluoride (PVDF) |

| Others |

| Hollow-Fiber |

| Flat-Sheet |

| Spiral-Wound |

| Water and Wastewater Treatment |

| Pharmaceutical and Biotechnology |

| Food and Beverage Processing |

| Chemical Processing |

| Power Generation |

| Carbon Capture and Gas Transfer |

| Other Applications |

| Industrial |

| Healthcare |

| Food and Beverage |

| Power and Energy |

| Other Industries |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Nordic Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Membrane Material | Polypropylene (PP) | |

| Polytetrafluoroethylene (PTFE) | ||

| Polyvinylidene Fluoride (PVDF) | ||

| Others | ||

| By Module Configuration | Hollow-Fiber | |

| Flat-Sheet | ||

| Spiral-Wound | ||

| By Application | Water and Wastewater Treatment | |

| Pharmaceutical and Biotechnology | ||

| Food and Beverage Processing | ||

| Chemical Processing | ||

| Power Generation | ||

| Carbon Capture and Gas Transfer | ||

| Other Applications | ||

| By End-user Industry | Industrial | |

| Healthcare | ||

| Food and Beverage | ||

| Power and Energy | ||

| Other Industries | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Nordic Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the size of the membrane contactor market?

The membrane contactor market stands at USD 426.13 million19.33 and is forecast to reach USD 569.45 million by 2031 at a 5.97% CAGR from 2026 to 2031.

Which membrane material is growing fastest?

PVDF is projected to record a 6.26% CAGR through 2031 because it resists acids, bases, and high-temperature cleanings.

Why are spiral-wound modules gaining share?

Their compact geometry slips into existing pipe racks, delivering 22% higher mass-transfer rates and 78% energy savings in retrofit studies.

What is the key driver in beverage processing?

Sub-20 ppb dissolved-oxygen targets achieved without flavor loss or large towers, which improves yield and lowers energy costs.

How will ammonia-recovery rules affect demand?

EU Directive C(2026)662 monetizes recovered ammonium sulfate, accelerating membrane stripping adoption across livestock and industrial wastewater streams.

Page last updated on: