Membrane Bioreactor Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

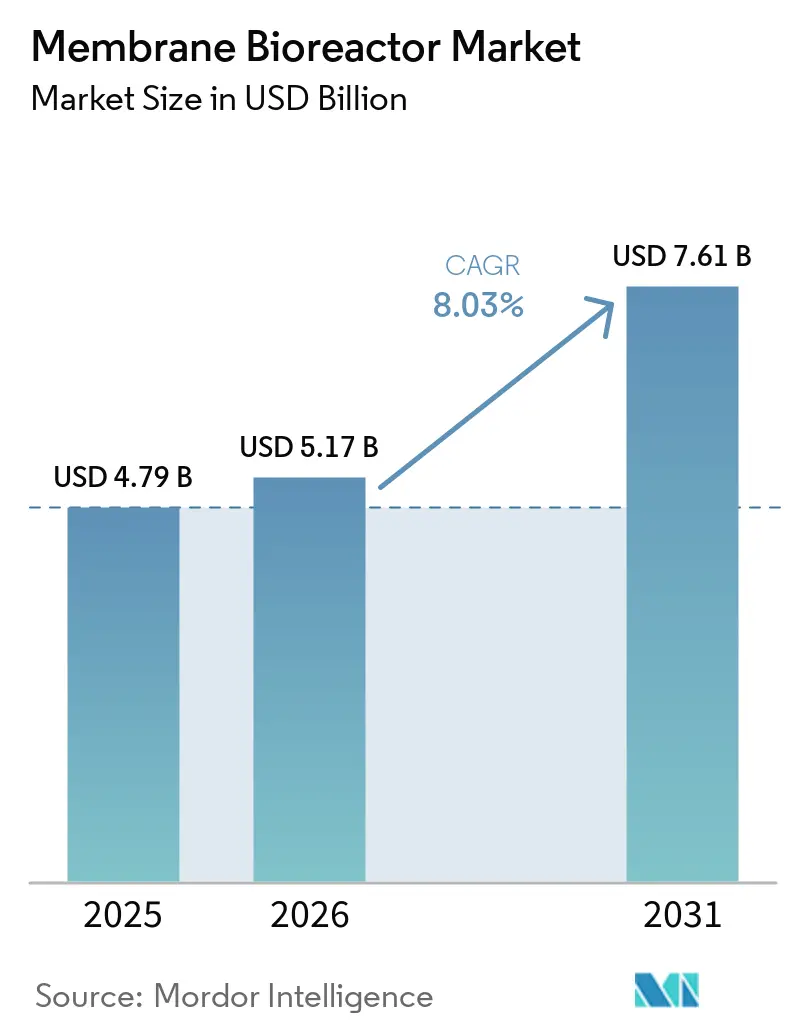

| Market Size (2026) | USD 5.17 Billion |

| Market Size (2031) | USD 7.61 Billion |

| Growth Rate (2026 - 2031) | 8.03% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Membrane Bioreactor Market Analysis by Mordor Intelligence

The Membrane Bioreactor Market size is expected to grow from USD 4.79 billion in 2025 to USD 5.17 billion in 2026 and is forecast to reach USD 7.61 billion by 2031 at 8.03% CAGR over 2026-2031. Tightening discharge regulations in the European Union and China, rapid urbanization across the Asia-Pacific, and artificial-intelligence-driven maintenance protocols that extend membrane life by 18 days are accelerating adoption. Quaternary treatment mandates, PFAS limits, and energy-neutrality targets are pushing municipalities toward high-flux units that fit inside existing tankage, while containerized systems win remote industrial sites that need plug-and-play deployment within six weeks. Module suppliers have answered with ceramic tubular geometries that tolerate high turbidity, hydrophilic coatings that lower bio-fouling, and digital twins that anticipate cleaning cycles, together trimming chemical costs by up to 75%. Competitive intensity is rising as incumbents bundle equipment, software, and financing, while regional specialists market pay-as-you-treat offerings that defer capital outlays for small utilities.

Key Report Takeaways

- By membrane type, hollow-fiber configurations led with 56.22% of the membrane bioreactor market share in 2025. Multi-tubular modules are forecast to expand at an 8.28% CAGR between 2026 and 2031, the fastest growth rate among product categories.

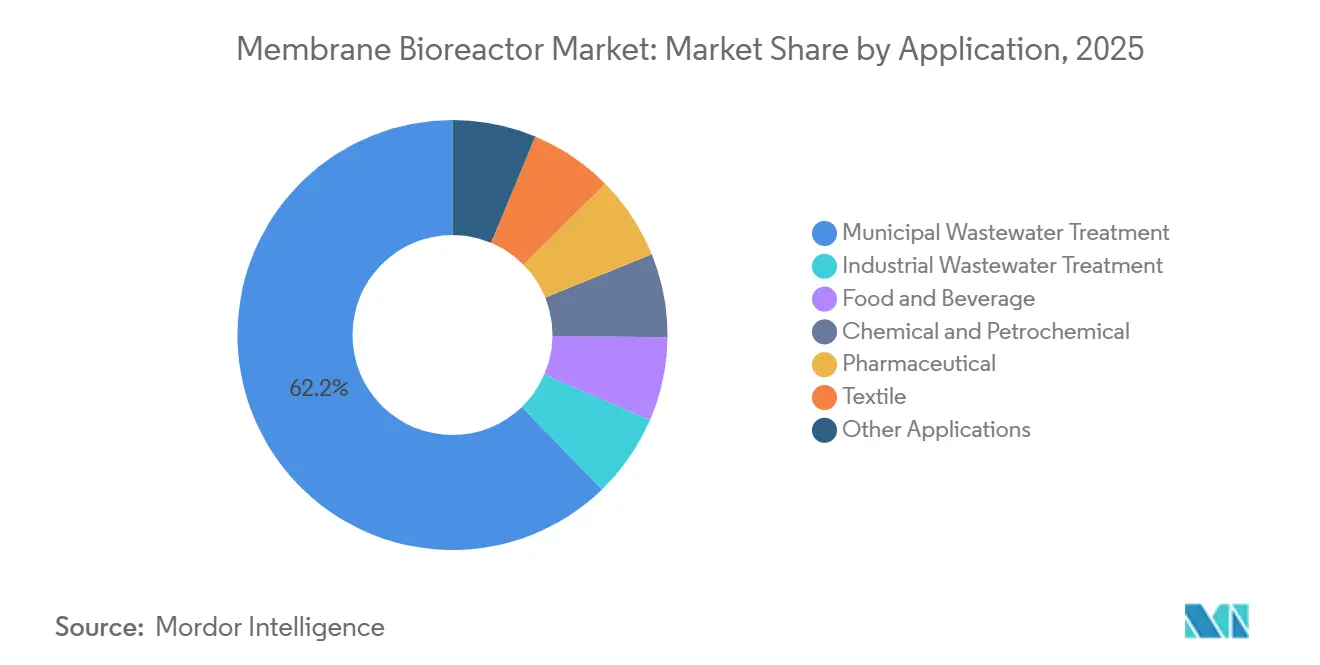

- By application, municipal wastewater treatment commanded 62.23% share of the membrane bioreactor market in 2025. Industrial installations are projected to grow at an 8.53% CAGR between 2026 and 2031, outpacing municipal expansion.

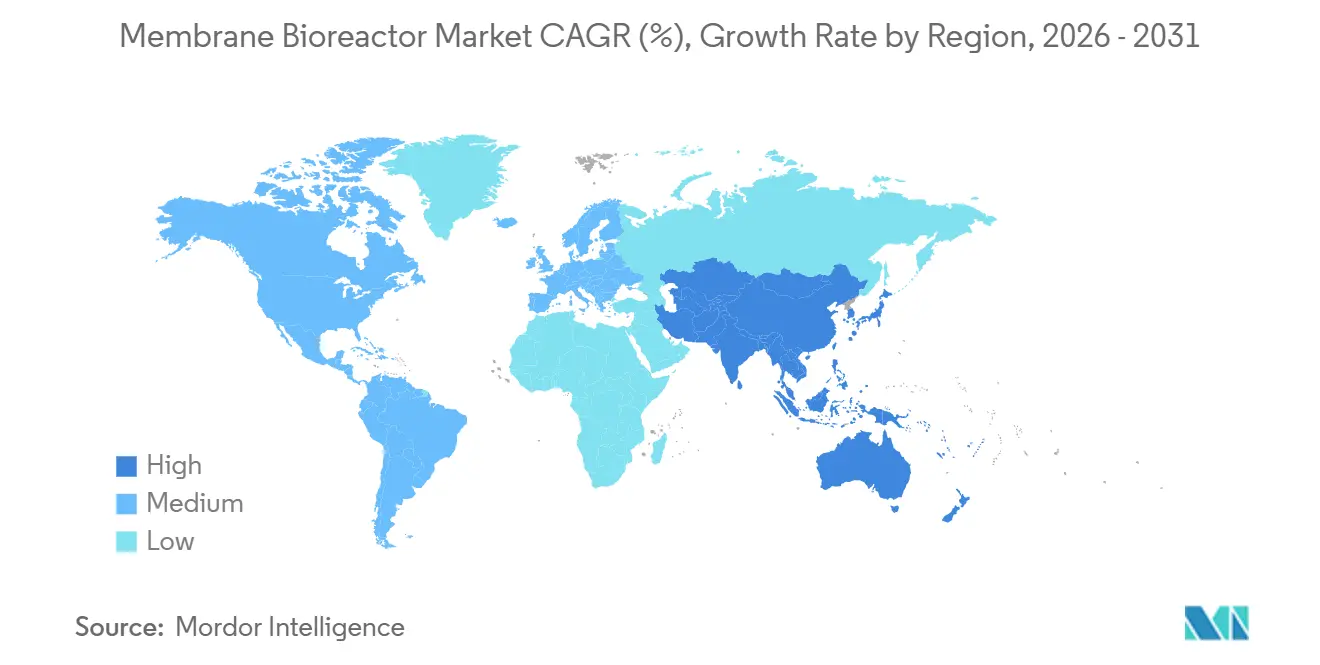

- Asia-Pacific captured 45.12% share in 2025 and is advancing at an 8.36% CAGR between 2026 and 2031, the highest regional pace.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Membrane Bioreactor Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Demand for Water Reuse and Recycling | +2.10% | Global, with concentration in water-stressed regions | Medium term (2-4 years) |

| Stringent Wastewater-Discharge Regulations | +1.80% | North America and EU, expanding to APAC | Short term (≤ 2 years) |

| Urbanization and Industrialization in Emerging Economies | +1.50% | APAC core, spill-over to MEA and Latin America | Long term (≥ 4 years) |

| Advances in Membrane Materials and Module Designs | +1.20% | Global, led by Japan and Germany innovation hubs | Medium term (2-4 years) |

| MBR-Anaerobic Digestion Hybrids for Energy-Positive Plants | +1.10% | Europe and North America, pilot deployments in APAC | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stringent Wastewater-Discharge Regulations

Under the revamped European Union Urban Wastewater Treatment Directive, wastewater treatment plants serving significant population equivalents must incorporate quaternary treatment and achieve energy neutrality within the specified timeline. This requirement is driving utilities to adopt membrane bioreactors, which combine biological processing and ultrafiltration in a single tank. In July 2025, China's Sichuan province established a global benchmark by introducing a provincial limit on per- and polyfluoroalkyl substances effluents. The regulation restricts the levels of these substances for industrial discharges, a standard considered unattainable without the use of membrane polishing[1]Sichuan Provincial Government, “PFAS Discharge Limits DB51/3202-2024,” sc.gov.cn. Since 2024, India’s National Green Tribunal has shut down numerous textile and pharmaceutical units for non-compliance, sparking a surge in retrofit demand in Tamil Nadu and Gujarat. The United States Environmental Protection Agency set stringent limits for perfluorooctanoic acid and perfluorooctane sulfonate in drinking water, but in 2025, it retracted similar rules for wastewater, creating a regulatory void that promotes pre-treatment within industrial boundaries. In Southeast Asia, the certification under the International Organization for Standardization for non-sewered sanitation has fast-tracked the deployment of decentralized membrane bioreactor units, achieving both pathogen removal and nutrient recovery standards.

Rapid Urbanization and Industrialization in Asia-Pacific

India generates a significant amount of sewage daily, but treats only a small portion of it, leaving a substantial gap that can be addressed by using dense-packing Membrane Bioreactors without requiring additional land. In China, several facilities have received certification from the Alliance for Water Stewardship, with more than half achieving the highest recognition by combining Membrane Bioreactors with reverse osmosis. This approach has significantly reduced treatment costs and ensured a quick return on investment. Singapore's Tuas Water Reclamation Plant, which began operations in 2026, uses advanced ceramic membranes to achieve a high recovery rate while effectively reducing brine disposal[2]Public Utilities Board Singapore, “Tuas Water Reclamation Plant,” pub.gov.sg . Under the Pasig River program, Metro Manila aims for extensive sewerage coverage by the end of the decade, opting for modular membrane bioreactors that can be installed in phases, sidestepping the typical lengthy civil works schedule. By the end of the decade, the urban population in the ASEAN region is expected to grow significantly, intensifying reuse mandates in cities like Jakarta, Bangkok, and Ho Chi Minh City.

Advances in Membrane Materials and Module Designs

Launched in April 2026, Toray's biopharma module achieves significantly enhanced filtration efficiency while requiring a much smaller footprint. This innovation allows drug plants to retrofit skids without the need for reinforcing frames. In municipal pilots, PVDF modified with tannic acid and graphene oxide demonstrated improved flux and extended cleaning intervals, hinting at a potential for longer membrane life. Jiuwu Hi-Tech's ceramic tubular units can handle high turbidity levels and operate under varying pressure conditions, all while effectively retaining solids in titanium-dioxide wash streams. DuPont's hydrophilic-coated MemPulse modules enabled Florida's Bee Ridge plant to expand its capacity significantly. This was achieved without additional aeration, resulting in a substantial deferral of civil work costs. Photocatalytic self-cleaning composites showcased their prowess by removing a high percentage of color in live textile effluent. This advancement hints at the future potential of membranes capable of simultaneous disinfection and decolorization.

Rise of Containerized and Decentralized MBRs for Remote Sites

Plug-and-play units, with capacities ranging from small to large volumes, reduce footprints significantly and can be commissioned in a short timeframe. This rapid deployment makes them highly appealing to mining camps and oil-sands pads, especially those racing to comply with stringent zero-discharge regulations. In Western Australia, new mines are mandated to recycle a substantial percentage of their water by the end of the decade. This regulation has spurred the installation of numerous containerized units in recent years. In Oman, the Al Ansab plant expanded its capacity significantly using a cartridge-add strategy, successfully avoiding considerable civil work expenses. In Sub-Saharan Africa, solar-powered units operate off-grid for a majority of their runtime, effectively bypassing the need for diesel logistics. In recent years, the United States Department of Defense deployed several units at forward bases, achieving significant annual savings on tanker costs.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Membrane fouling and cleaning downtime | -1.20% | Global, acute in high-salinity industrial streams | Short term (≤ 2 years) |

| Skilled operator gap in smaller utilities | -0.80% | North America, Europe, and emerging Asia-Pacific markets | Medium term (2-4 years) |

| Uncertain PFAS standards raising retrofit risk | -0.50% | North America, divergent state policies | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Membrane Fouling and Cleaning Downtime

In brine-rich feeds, transmembrane pressure can increase significantly over a short period. This rise necessitates recovery cleans that lead to a notable reduction in daily operational capacity. At Stockholm’s Henriksdal plant, transitioning to demand-driven cleans and reducing hypochlorite usage has resulted in substantial annual cost savings and a significant decrease in global warming potential. Cake layers, with particles much smaller than those in pristine film, are considerably less permeable, making air-scour removal more difficult. While sequential alkali-acid cleans can restore a high percentage of flux, they require extended downtime. However, enhanced coagulation has the potential to extend the interval between cleans, thereby increasing the lifespan of membranes.

Skilled-Operator Gap in Smaller Municipalities

A significant portion of the wastewater workforce in the United States is expected to retire within the next decade. However, only a limited number of states are utilizing State Revolving Fund set-asides for operator training. Many rural utilities are experiencing high vacancy rates, and a considerable number lack succession plans, increasing the risk of compliance issues. In India, a large percentage of operators in smaller cities are unlicensed, which is associated with a notable rate of non-compliance in effluent testing. Remote monitoring platforms have the potential to enable a single technician to manage multiple decentralized plants, but adoption remains low among municipalities with smaller budgets in the United States. The industry is increasingly promoting containerized packages as “operate by exception,” featuring artificial intelligence dashboards that notify local staff only when necessary.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Membrane Type: Hollow Fiber Dominance Faces Tubular Challenge

Hollow-fiber units held 56.22% of the membrane bioreactor market in 2025. The high packing density significantly reduces the required tank volume. However, the membrane bioreactor market for multi-tubular designs is projected to grow at an 8.28% CAGR between 2026 and 2031, as in high-turbidity streams, industrial operators prioritize robustness over footprint. Flat-sheet cartridges strike a balance, effectively handling high concentrations of mixed liquor suspended solids. These cartridges also permit in-situ chemical cleans, significantly reducing downtime. Singapore's Tuas plant, with a significant treatment capacity, opted for ceramic tubular modules to process petrochemical waste. This decision not only bypassed expensive pre-treatment processes but also significantly reduced costs associated with chemical oxygen demand removal. Due to the vulnerability of hollow-fiber membranes to breakage under high pressure, DuPont and Toray introduced reinforced variants with enhanced burst strength, catering to industrial retrofits. In Oman, KUBOTA's cartridge-add model expanded in phases, demonstrating the advantages of modular scaling over traditional green-field concrete approaches.

By Application: Industrial Segments Outpace Municipal Growth

Municipal treatment controlled 62.23% of 2025 revenue, yet the membrane bioreactor market across industrial wastewater treatment applications is forecast to grow 8.53% CAGR between 2026 and 2031. Pharmaceuticals, food, and chemical industries are increasingly adopting zero-liquid discharge practices. Pharmaceutical facilities, with active ingredient levels exceeding a certain threshold, are now combining Membrane Bioreactors with nanofiltration. This combination achieves high removal rates, aligning with discharge standards set by Germany and Switzerland.

Food and beverage manufacturers are turning to containerized units. These units can be installed quickly and adeptly handle significant seasonal load fluctuations, all while adhering to effluent targets. Chemical and petrochemical industries are retrofitting their systems. At Ecolab’s Taicang site, they have integrated Membrane Bioreactor-Reverse Osmosis systems that successfully eliminate phenolics, achieving the coveted zero-liquid discharge. However, textile dyeing facilities are treading carefully. While Membrane Bioreactor technology can remove a substantial percentage of color, they find it is necessary to pair it with Reverse Osmosis polishing for water reuse in polyester-cotton processes, especially in Bangladesh and Vietnam. In North America, states like Florida, California, and Texas are emerging as growth hubs. Here, stringent nutrient limits and coastal considerations are driving retrofitting efforts, exemplified by Bee Ridge’s capacity enhancement within its original basin.

Geography Analysis

Asia-Pacific secured 45.12% of 2025 sales and is projected to sustain an 8.36% CAGR between 2026 and 2031. China's Platinum AWS plants achieve significant savings on treatment costs by utilizing advanced hybrid technologies. Meanwhile, India faces a substantial treatment gap, prompting retrofits tailored to existing sites. In Tokyo, Japan, the urgency of upgrading aging sewers is underscored by high land prices. South Korea is taking proactive measures, mandating a considerable percentage of wastewater reuse for new industrial parks by the end of the decade.

North America accounted for a significant portion of the 2025 revenue. Highlighting the trend, Florida's Bee Ridge project increased its throughput with the help of thousands of modules. This move underscores how tourism-centric regions are steering clear of seeking permits for new green-field plots. In a nod to sustainability, Canada's mining sector has integrated multiple containerized units since 2024, aligning with British Columbia's stringent zero-discharge code. Further south, México is investing heavily in border-city initiatives in 2025, aiming to tackle transboundary pollution challenges.

Europe commanded a notable share in 2025. Driving this momentum is Germany's ambitious Wolfsburg-Stahlberg plant, poised to be the nation's largest facility by 2027, thanks to the revamped Urban Wastewater Directive. While the Middle-East and Africa currently hold a modest share, they are on a rapid ascent. A testament to this growth is Oman's Al Ansab, which boasts a significant capacity and reclaims a large portion of its effluent for irrigation. South America, with a smaller share, proudly hosts Latin America's crown jewel: the Riachuelo plant in Buenos Aires, which became operational in 2025.

Competitive Landscape

The Membrane Bioreactor Market is moderately consolidated. Specialists like Newterra and Fluence, operating in containerized setups, are making inroads at remote sites. They promise significant reductions in footprint and swift lead times, directly challenging municipal incumbents accustomed to longer build cycles. A patent race is heating up around photocatalytic self-cleaning films, projected to substantially reduce lifecycle costs by the end of the decade and potentially undermine chemical supplier revenues.

Membrane Bioreactor Industry Leaders

TORAY INDUSTRIES, INC.

Mitsubishi Chemical Group Corporation.

KUBOTA Corporation

Xylem Inc.

Veolia

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: Membion began constructing Germany’s largest MBR plant in Wolfsburg-Stahlberg (EUR 14 million). Commissioning is scheduled for mid 2027, underscoring MBR’s expanding role in sustainable wastewater treatment markets.

- July 2025: Veolia had unveiled its Vitória WRS in Brazil, successfully reclaiming 85% of wastewater using advanced membrane bioreactors and reverse osmosis. This initiative not only catered to industrial needs but also safeguarded freshwater access for 200,000 residents. The move amplified demand, spurred innovation, and accelerated adoption in the global Membrane Bioreactor Market.

Global Membrane Bioreactor Market Report Scope

A Membrane Bioreactor (MBR) is a wastewater treatment technology combining activated sludge biological processes with membrane filtration (microfiltration or ultrafiltration). Instead of gravity settling, membranes retain biomass and solids while allowing clean water to pass. This integration delivers superior effluent quality, removes bacteria and viruses, enables higher mixed liquor suspended solids operation, and supports compact, energy-efficient designs widely adopted in municipal and industrial water reuse.

The Membrane Bioreactor Market is segmented by membrane type, application, and geography. By membrane type, the market is segmented into hollow fiber, flat sheet, and multi‑tubular. By application, the market is segmented into municipal wastewater treatment, industrial wastewater treatment, food and beverage, chemical and petrochemical, pharmaceutical, textile, and other applications. The report also covers the market size and forecasts for the Membrane Bioreactor Market in 17 countries across major regions. For each segment, the market sizing and forecasts have been done on the basis of value (USD).

| Hollow Fiber |

| Flat Sheet |

| Multi-tubular |

| Municipal Wastewater Treatment |

| Industrial Wastewater Treatment |

| Food and Beverage |

| Chemical and Petrochemical |

| Pharmaceutical |

| Textile |

| Other Applications |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| NORDIC Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Membrane Type | Hollow Fiber | |

| Flat Sheet | ||

| Multi-tubular | ||

| By Application | Municipal Wastewater Treatment | |

| Industrial Wastewater Treatment | ||

| Food and Beverage | ||

| Chemical and Petrochemical | ||

| Pharmaceutical | ||

| Textile | ||

| Other Applications | ||

| By Geography | Asia-Pacific | China |

| Japan | ||

| India | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| NORDIC Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the size of the Membrane Bioreactor Market?

The Membrane Bioreactor Market stands at USD 5.17 billion in 2026 and is forecast to reach USD 7.61 billion by 2031 at a 8.03% CAGR from 2026 to 2031.

Which region will add the most new capacity between 2026 and 2031?

Asia-Pacific is projected to expand at an 8.36% CAGR, supported by large projects in China, India, and Singapore.

Why are multi-tubular membranes gaining share in heavy industry?

They tolerate more than 5,000 NTU turbidity and high salinity, reducing downtime in petrochemical and mining effluent service.

What role does artificial intelligence play in plant operations?

AI models predict fouling up to one week in advance and can cut chemical spending by about 3.5% and energy by 0.5%.

How do containerized MBRs benefit remote sites?

Factory-built units deploy in four to six weeks, are 50% smaller than traditional plants, and can run off-grid with solar power.

What is the biggest technical barrier to wider adoption?

Membrane fouling remains the key constraint, raising cleaning costs and requiring skilled operators that many small utilities lack.

Page last updated on: