Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

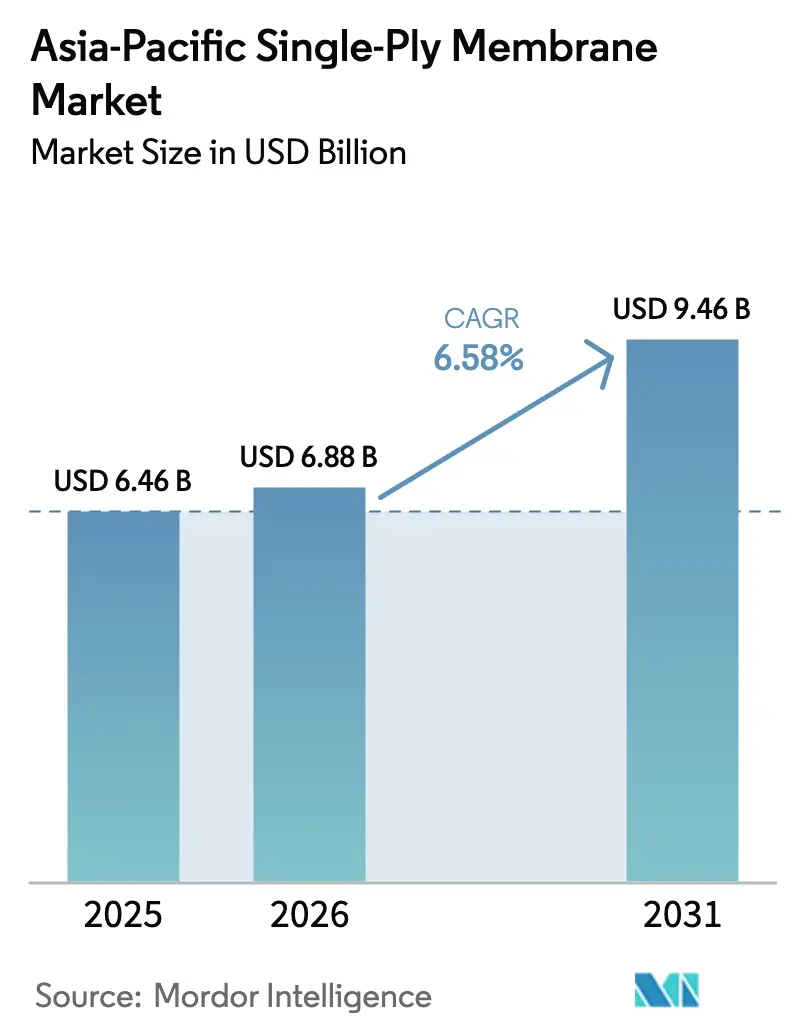

| Base Year Market Size (2025) | USD 6.46 Billion |

| Market Size (2026) | USD 6.88 Billion |

| Market Size (2031) | USD 9.46 Billion |

| Growth Rate (2026 - 2031) | 6.58% CAGR |

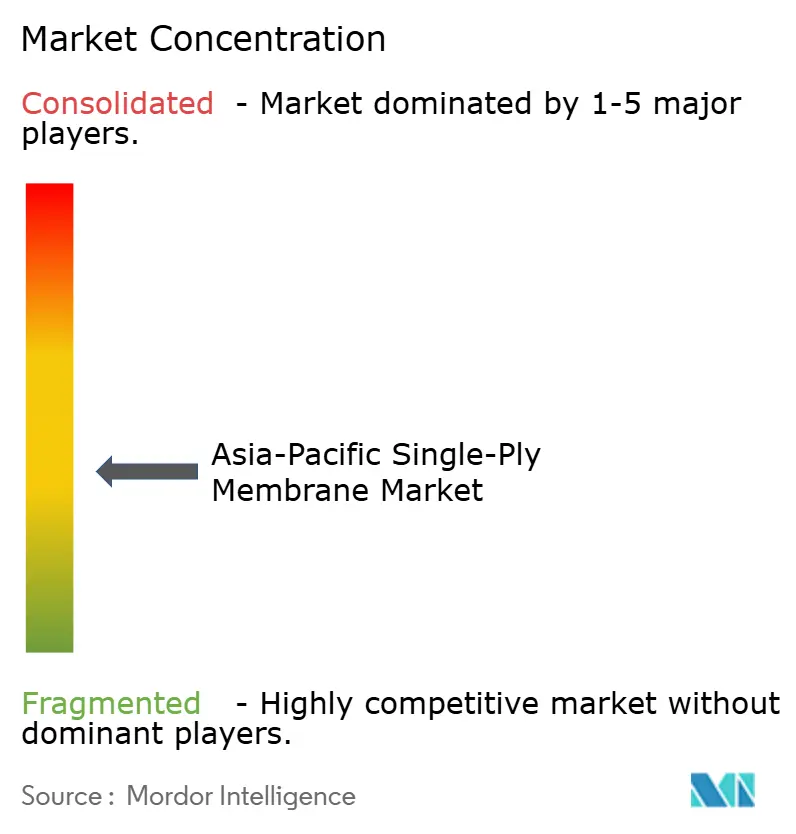

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Asia-Pacific Single-Ply Membrane Market Analysis by Mordor Intelligence

The Asia-Pacific Single-Ply Membrane Market size is projected to expand from USD 6.46 billion in 2025 and USD 6.88 billion in 2026 to USD 9.46 billion by 2031, registering a CAGR of 6.58% between 2026 to 2031. Infrastructure investments in China, Vietnam, and Indonesia continue to drive demand for bridges, tunnels, and landfills. Meanwhile, net-zero building codes in India and Japan are accelerating the adoption of cool roofs, directing spending toward white thermoplastic polyolefin (TPO) and ethylene-propylene-diene monomer (EPDM) roofing materials. Data center operators in Singapore, Mumbai, and Jakarta are increasingly specifying membrane systems with four-hour cure windows to minimize cooling downtime. TPO’s heat-welded seams meet these requirements more effectively than torch-applied modified bitumen sheets. The shift toward factory-welded products is gaining momentum as modular construction standards expand. For example, Hong Kong’s public housing Modular Integrated Construction (MiC) program and China’s 30% prefabrication mandate have reduced on-site labor by 30% and lowered defect rates to below 2%. However, a volatile polyolefin feedstock cycle, projected to increase by 22% between January 2024 and December 2025, is putting pressure on gross margins. Despite this, vertical integration strategies by companies such as Sika, Oriental Yuhong, and Dow are helping these market leaders mitigate cost pressures and maintain a competitive edge over smaller extruders.

Key Report Takeaways

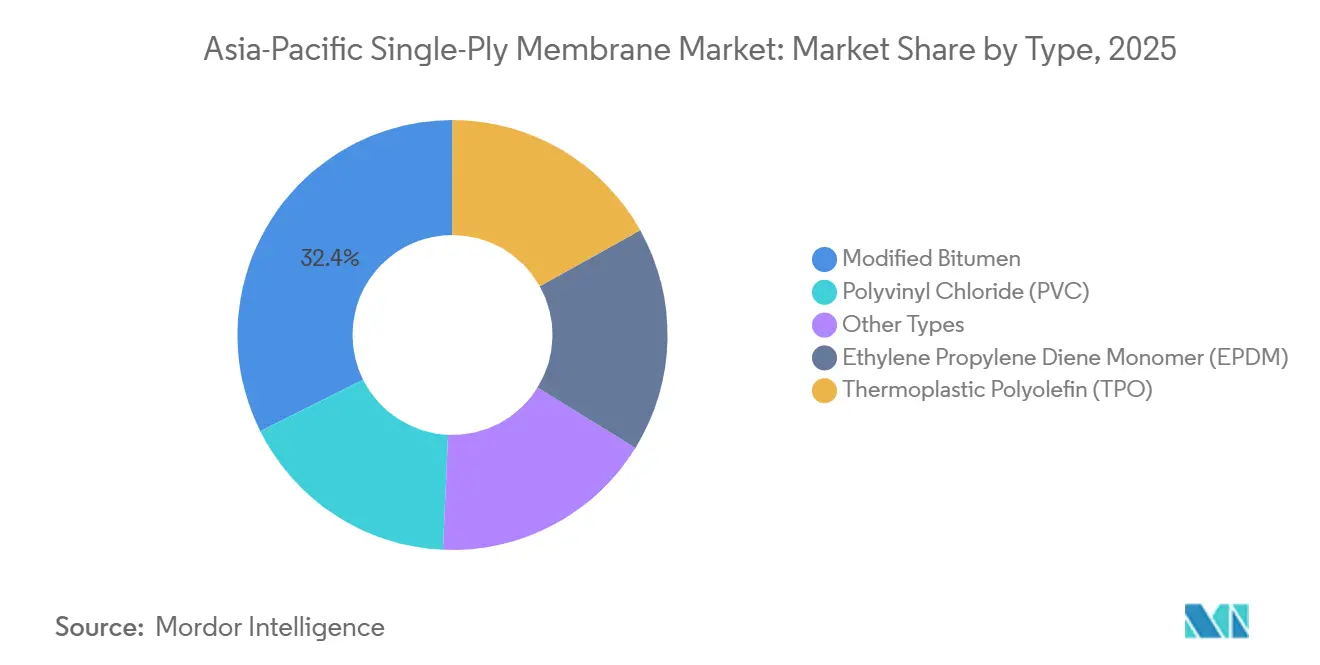

- By type, modified bitumen commanded 32.38% of the Asia-Pacific single-ply membrane market share in 2025, while thermoplastic polyolefin (TPO) is advancing at an 8.41% CAGR through 2031.

- By application, infrastructure (bridges, tunnels, landfills) accounted for 50.72% of the Asia-Pacific single-ply membrane market share in 2025 and is projected to expand at a 6.72% CAGR through 2031.

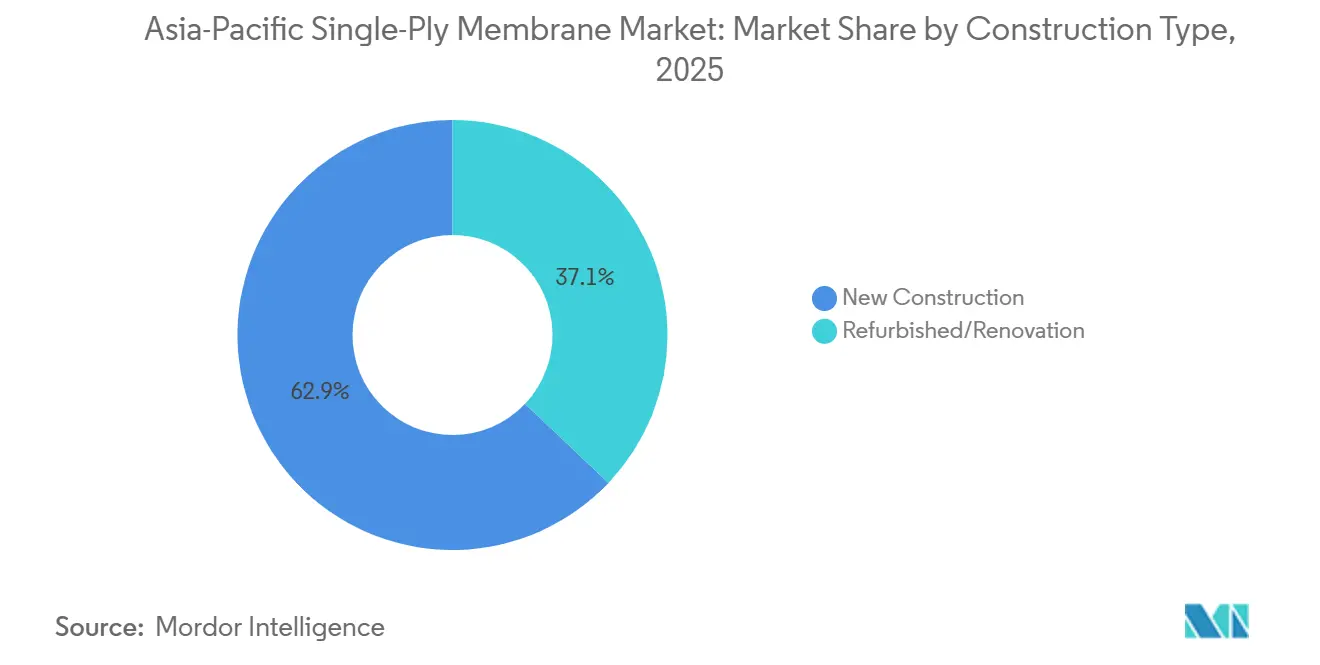

- By construction type, new construction represented 62.92% of the Asia-Pacific single-ply membrane market share in 2025 and is expected to grow at a 6.77% CAGR through 2031.

- By geography, China absorbed 69.96% of the Asia-Pacific single-ply membrane market share in 2025 and is forecast to register a 7.31% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Asia-Pacific Single-Ply Membrane Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Tightening building-energy codes driving cool-roof adoption | +1.8% | India, Japan, China, with spillover to Singapore and South Korea | Medium term (2-4 years) |

| Accelerating re-roofing cycle in commercial real-estate | +1.5% | India, Japan, South Korea, with early gains in Mumbai, Tokyo, Seoul | Short term (≤ 2 years) |

| Government net-zero mandates boosting reflective membranes | +1.3% | APAC core (China, India, Japan), extending to ASEAN-6 | Long term (≥ 4 years) |

| Modular construction boosting demand for factory-welded rolls | +1.0% | China, India, Vietnam, with pilot projects in Malaysia and Thailand | Medium term (2-4 years) |

| Data-centre capacity boom requiring low-downtime roof systems | +0.9% | Singapore, India, Indonesia, Japan, with concentrated demand in Jurong, Mumbai, Jakarta | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Tightening Building-Energy Codes Driving Cool-Roof Adoption

Mandatory cool-roof thresholds are turning energy-efficiency objectives into enforceable procurement criteria, favoring high-albedo TPO and PVC membranes. India’s Energy Conservation Building Code 2024 specifies an SRI ≥ 78 for low-slope roofs across nine climate zones, effectively excluding dark modified bitumen from new projects in cities such as Chennai, Hyderabad, and Kolkata[1]Bureau of Energy Efficiency India, “Energy Conservation Building Code 2024,” beeindia.gov.in. Japan’s revised Building Energy Efficiency Act, effective April 2025, mandates non-residential buildings larger than 300 m² to meet passive-cooling standards, driving EPDM upgrades in office buildings across Tokyo and Osaka. In China, the GB 50189 update links green-building tax incentives to reflective roofs, accelerating TPO adoption in cities like Shenzhen and Guangzhou. Singapore’s Green Mark 2024 provides bonus points for roofs with an aged SRI ≥ 63, aligning its standards with California Title 24 benchmarks. Collectively, these regulations are projected to reduce the market share of non-reflective membranes by an estimated 18-22% in major Asia-Pacific metropolitan areas by 2028.

Accelerating Re-Roofing Cycle in Commercial Real Estate

Aging building inventories in Japan, South Korea, and India are shortening re-roofing cycles from 25-30 years to 18-22 years, as property owners prioritize energy savings over lifecycle extensions. India’s commercial renovation market reached INR 45,000 crore (USD 5.3 billion) in 2025, with 45% of leases involving refurbished properties. Japanese developers have expedited retrofits to comply with the April 2025 efficiency law, despite a 7.1% decline in new construction starts as of October 2024. In South Korea, property owners in Seoul and Busan accessed KRW 2.5 trillion (USD 1.9 billion) in low-interest loans for housing upgrades, focusing on reflective roofs. In Singapore, landlords are proactively re-roofing Grade-A properties, such as the Marina Bay Financial Centre, up to eight years ahead of schedule to maintain Green Mark Platinum certifications. Re-roofing is transitioning from a reactive measure to a proactive environmental, social, and governance (ESG) investment, yielding rental increases of 12-15% in sustainability-focused markets.

Government Net-Zero Mandates Boosting Reflective Membranes

Net-zero commitments are incorporating cool-roof requirements into public procurement policies, establishing a baseline demand for reflective membranes. China’s 2060 net-zero roadmap mandates that all new public buildings be net-zero-ready by 2030, requiring reflective roofs in 14 provincial capitals. India’s National Green Building Programme offers 10% faster permit approvals for projects with SRI-compliant roofs, reducing developers’ revenue cycles by six to eight weeks. Japan has allocated JPY 2 trillion (USD 13.3 billion) through 2030 for building decarbonization, with 18% of the funds directed toward passive-cooling technologies, including reflective membranes. South Korea’s 2050 Carbon Neutral Scenario targets 70% of new commercial roofs to achieve an albedo ≥ 0.65 by 2035. Non-compliance penalties, ranging from 5-12% of project value, are positioning reflective membranes as a necessary risk-mitigation measure rather than an optional upgrade.

Modular Construction Boosting Demand for Factory-Welded Rolls

The rise of prefabrication is shifting membrane welding from on-site labor to controlled factory environments, reducing defects and accelerating construction timelines. Hong Kong’s MiC program delivered 5,000 public-housing units in 2025 using factory-bonded TPO layers, eliminating the need for torch work. In China, a mandate for 30% prefabricated content in new urban housing by 2025 has led companies like Oriental Yuhong to commercialize self-adhesive TPO rolls designed for modular roof panels. Vietnam’s six-road expressway project, valued at VND 32,200 billion (USD 1.3 billion), employs factory-welded EPDM on precast bridge decks to meet tight monsoon construction schedules. Factory welding has reduced seam-failure rates from 8-12% to below 2%, a critical improvement for modular contractors offering decade-long warranties. This structural shift in construction logistics is driving growth in the Asia-Pacific single-ply membrane market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile polyolefin and plasticizer prices | -1.2% | Global, with acute pressure in China, India, Southeast Asia | Short term (≤ 2 years) |

| PVC and phthalate regulatory scrutiny | -0.8% | China, Japan, South Korea, with spillover to ASEAN-6 | Medium term (2-4 years) |

| Skilled-installer shortage in Tier-2 Asia-Pacific cities | -0.6% | India (Visakhapatnam, Coimbatore), Vietnam (Da Nang), Indonesia (Surabaya), Thailand (Chiang Mai) | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Volatile Polyolefin and Plasticizer Prices

Crude oil-driven polypropylene price swings of 22% between January 2024 and December 2025 reduced the gross margins of non-integrated TPO extruders by 3-5 percentage points. Plasticizer costs for PVC membrane production increased by 18% in Q2 2025 following China's addition of four phthalates to its RoHS restricted list[2]Ministry of Industry and Information Technology China, “RoHS 2026 Amendment,” miit.gov.cn. Dow’s silicone expansion in Zhangjiagang aims to address non-phthalate alternatives; however, the 18-24 months required for field validation delays broader commercial adoption. Smaller producers in Vietnam and Indonesia, lacking hedging mechanisms, implemented downstream price increases of 12-15%, leading to project delays in cost-sensitive infrastructure tenders. These market dynamics have accelerated vertical integration strategies, such as Sika’s resin acquisition and Oriental Yuhong’s entry into bitumen refining. These approaches help mitigate input cost volatility and strengthen market positions in the Asia-Pacific single-ply membrane segment.

PVC and Phthalate Regulatory Scrutiny

Stricter chemical safety regulations are narrowing formulation options for PVC sheets. China’s January 2026 RoHS amendment bans DEHP, DBP, BBP, and DIBP in electrical installations, including building-integrated photovoltaic membranes. In 2024, Japan classified three phthalates as Specified Chemical Substances, limiting their permissible presence to 0.1% by weight. South Korea’s K-REACH now requires lifecycle documentation for construction-grade plasticizers, adding compliance costs of KRW 80-120 million (USD 60,000-90,000) per product line. Non-harmonized regulatory thresholds compel manufacturers to maintain region-specific SKUs, undermining scale economies. While the existing PVC roof base, comprising approximately 25-30% of the regional stock, offers retrofit opportunities for EPDM or TPO membranes, new PVC product introductions face increasing regulatory constraints, exerting a moderate negative impact on the Asia-Pacific single-ply membrane market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: TPO Outpaces Legacy Bitumen

Modified bitumen accounted for 32.38% of the Asia-Pacific single-ply membrane market share in 2025, while TPO is projected to grow at a CAGR of 8.41% through 2031. Infrastructure buyers continue to prefer torch-applied bitumen for freeze-thaw bridges under China’s Belt and Road procurement standards. On the other hand, data-center clients increasingly adopt heat-welded TPO, which meets ≤ 0.5% seam-failure targets and four-hour cure windows, driving its adoption in Singapore, Jakarta, and Mumbai campuses. EPDM holds a mid-teens market share, favored by Tokyo renovators for its closed-cell resilience against typhoon-driven rain. PVC's growth is hindered by China’s phthalate ban, although high-rise condo developers in Singapore value its weldability in areas where torch flames are prohibited.

Modified bitumen’s dominance in bridges and tunnels is expected to decline gradually, with a 4-6 percentage point reduction by 2029 as India’s SRI threshold is fully implemented. EPDM’s market presence is strengthening due to Japan’s stimulus for retrofit energy savings, while PVC suppliers are racing to qualify non-phthalate plasticizers ahead of China’s January 2026 deadline.

By Application: Infrastructure Anchors Revenue Growth

Infrastructure accounted for 50.72% of the Asia-Pacific single-ply membrane market share in 2025 and is expected to grow at a CAGR of 6.72% through 2031. Vietnam’s USD 4.1 billion Vung Tau-Can Gio bridge utilizes modified bitumen for saltwater decks, while Thailand and Laos completed a 1,350-meter span in December 2025, sealed with EPDM on expansion joints. Indonesia’s Trans-Sumatra Toll Road requires membranes for 180 bridges and 14 tunnels, with Oriental Yuhong aiming to supply these projects through its Southeast Asia plants.

Commercial real estate holds a mid-20s market share, supported by India’s INR 45,000 crore renovation wave, which is replacing dark bitumen with reflective TPO to reduce HVAC loads by up to 20%. Residential growth remains limited due to the dominance of pitched-roof tiles in detached homes, though high-rise condos in Hong Kong and Singapore are adopting TPO terraces to meet Green Mark standards. Industrial buyers, such as pharmaceutical plants, continue to specify PVC for its chemical-resistant properties. The Asia-Pacific single-ply membrane market thus reflects a dual trend: infrastructure projects sustain bitumen demand, while energy-conscious commercial segments drive TPO adoption.

By Construction Type: New-Build Dominates Despite Retrofit Tailwinds

New construction captured 62.92% of the Asia-Pacific single-ply membrane market share in 2025 and is projected to grow at a CAGR of 6.77% through 2031. Indonesia’s Nusantara capital mandates net-zero-ready construction, favoring factory-welded TPO over torch-applied bitumen. China’s 30% prefabrication rule ensures high-capacity utilization of roll-stock plants. Renovation, while smaller in scale, is accelerating at a CAGR of 6.3% due to tightening energy codes in Tokyo, Seoul, and Sydney, prompting early roof replacements.

Refurbished properties face longer sales cycles as tenants remain in place during phased installations. However, premium offices in Singapore’s Marina Bay underwent re-roofing eight years early to maintain Green Mark Platinum certifications. South Korea’s KRW 2.5 trillion loan program supports reflective roofing for apartment blocks to reduce summer cooling loads. Suppliers are adapting their portfolios accordingly: Sika’s 35 Chinese facilities focus on high-volume TPO sheets for new builds, while its Singapore hub develops low-odor liquids for retrofits in occupied buildings, ensuring a balanced contribution to the Asia-Pacific single-ply membrane market.

Geography Analysis

China held 69.96% of the Asia-Pacific single-ply membrane market share in 2025 and is expected to grow at a CAGR of 7.31% through 2031. This growth is driven by Belt and Road infrastructure projects and domestic leaders like Oriental Yuhong, which reported RMB 40.1 billion (USD 5.5 billion) in revenue in 2024 across 50 facilities. Reflective-roof incentives under GB 50189 are boosting demand in Shenzhen and Guangzhou office parks, although overall construction activity declined mid-single digits according to Sika’s 9-month 2025 update. China’s January 2026 phthalate ban challenges PVC suppliers unless they adopt non-phthalate plasticizers. Prefabrication mandates further support for factory-welded membrane production, maintaining China’s dominant market position.

India’s demand is fueled by an 8-10 GW data-center roadmap and an INR 45,000 crore re-roofing backlog. The Energy Conservation Building Code 2024 enforces SRI ≥ 78 across nine zones, effectively phasing out dark bitumen roofs in cities like Mumbai, Chennai, and Hyderabad. Holcim’s partnership with Tata Steel integrates membrane supply into warehouse frames, capitalizing on India’s logistics growth. Meanwhile, a skill shortage in Visakhapatnam is driving demand for self-adhered TPO sheets that reduce reliance on skilled installers.

Japan and South Korea are experiencing robust retrofit activity. Japan’s April 2025 energy code has spurred EPDM and TPO adoption in Tokyo towers, despite a 7.1% decline in new construction starts as of October 2024. South Korea’s KRW 2.5 trillion renovation stimulus supports reflective roofs meeting albedo 0.65 targets. Coastal regions prone to typhoons favor EPDM for its superior water resistance.

Vietnam’s VND 32,200 billion expressway project and the USD 4.1 billion Vung Tau-Can Gio bridge are driving demand for bitumen and EPDM. Indonesia’s Trans-Sumatra Toll Road and Nusantara capital city projects include cool-roof requirements, benefiting TPO suppliers. Malaysia’s MRT3 and Pan Borneo projects are increasing demand for liquid-applied membranes in complex geometries. Australia, New Zealand, and the Philippines contribute smaller market shares, with Australia’s labor shortages accelerating the adoption of self-adhered systems.

Competitive Landscape

The Asia-Pacific single-ply membrane market is moderately fragmented, with the top five companies holding a combined 52% market share in 2025. Brookfield’s USD 5.8 billion acquisition of Johns Manville in December 2024 highlights private equity interest in roofing cash flows and brings North American R&D expertise to Asia for localized formulations. Sika expanded to 35 facilities in the Asia-Pacific region in January 2025, reducing TPO lead times to three to five days for Southeast Asian contractors and achieving 12% volume growth in 2025. Holcim’s collaboration with Tata Steel bypasses distributors, capturing an additional 8-10% margin on warehouse projects.

Oriental Yuhong’s 50-plant network provides raw-material hedging, mitigating the impact of 22% polypropylene price fluctuations in 2025. GAF’s SeamShield induction-welding technology reduces seam failures to below 2%, a critical factor for hyperscale data centers where downtime costs exceed USD 10,000 per hour. Dow’s Zhangjiagang silicone facility produces non-phthalate plasticizers essential for PVC compliance with China’s January 2026 regulations. Smaller firms like Joaboa Technology and Jiangsu Canlon focus on green-roof and photovoltaic membranes but lack regional distribution networks, limiting their market influence. Compliance with ISO 9001 and ASTM D6878 standards is now a baseline requirement, with differentiation increasingly based on installation speed, reflectivity retention, and feedstock resilience.

Asia-Pacific Single-Ply Membrane Industry Leaders

Sika AG

Carlisle Companies Inc.

Oriental Yuhong

Soprema Group

Jiangsu Canlon Building Materials Co.,Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Sika AG acquired Elmich Pte Ltd, a Singapore-based provider of sustainable urban greening and green roof solutions. This acquisition strengthened Sika's single-ply membrane portfolio in the Asia-Pacific region and increased its capabilities for commercial and residential buildings.

- January 2025: Sika AG opened two plants in Singapore and Xi’an. These facilities increased regional capacity and reduced TPO single-ply membrane lead times to three to five days.

Asia-Pacific Single-Ply Membrane Market Report Scope

Single-ply membranes are flexible and lightweight sheets made from synthetic polymers, such as PVC and TPO, or rubber, such as EPDM. These materials are primarily used for waterproofing flat or low-slope roofs. They offer durability, UV resistance, and can be installed using mechanical fastening, full adhesion, or ballasting methods.

The Asia-Pacific Single-Ply Membrane Market is segmented by type, application, construction type, and geography. By type, the market is segmented into modified bitumen, ethylene propylene diene monomer (EPDM), thermoplastic polyolefin (TPO), polyvinyl chloride (PVC), and other types. By application, the market is segmented into infrastructure (bridges, tunnels, landfills), residential, commercial, and industrial and institutional. By construction type, the market is segmented into new construction and refurbished/renovation. The report also covers the market size and forecasts for single-ply membrane in 8 countries across the region. For each segment, the market sizing and forecasts have been done on the basis of value (USD).

By Type

| Modified Bitumen |

| Ethylene Propylene Diene Monomer (EPDM) |

| Thermoplastic Polyolefin (TPO) |

| Polyvinyl Chloride (PVC) |

| Other Types |

By Application

| Infrastructure (Bridges, Tunnels, Landfills) |

| Residential |

| Commercial |

| Industrial and Institutional |

By Construction Type

| New Construction |

| Refurbished/Renovation |

By Geography

| China |

| India |

| Japan |

| South Korea |

| Indonesia |

| Vietnam |

| Thailand |

| Malaysia |

| Rest of Asia-Pacific |

| By Type | Modified Bitumen |

| Ethylene Propylene Diene Monomer (EPDM) | |

| Thermoplastic Polyolefin (TPO) | |

| Polyvinyl Chloride (PVC) | |

| Other Types | |

| By Application | Infrastructure (Bridges, Tunnels, Landfills) |

| Residential | |

| Commercial | |

| Industrial and Institutional | |

| By Construction Type | New Construction |

| Refurbished/Renovation | |

| By Geography | China |

| India | |

| Japan | |

| South Korea | |

| Indonesia | |

| Vietnam | |

| Thailand | |

| Malaysia | |

| Rest of Asia-Pacific |

Key Questions Answered in the Report

What is the size of the Asia-Pacific single-ply membrane market?

The Asia-Pacific single-ply membrane market stands at USD 6.88 billion in 2026 and is on track to reach USD 9.46 billion by 2031.

Which type is growing the fastest through 2031?

Thermoplastic Polyolefin (TPO) is the fastest expanding type at 8.41% CAGR through 2031, driven by cool-roof codes and low-downtime installation.

Why are reflective roofs important in Asia-Pacific?

Tightening energy codes in India, Japan, China, and others mandate high SRI values, making reflective membranes essential for compliance and for lowering cooling loads.

Which application segment leads demand in 2025?

Infrastructure applications such as bridges and tunnels account for 50.72% of revenue in 2025.

Page last updated on: