Spiral Membrane Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 8.3 Billion |

| Market Size (2031) | USD 14.28 Billion |

| Growth Rate (2026 - 2031) | 11.48% CAGR |

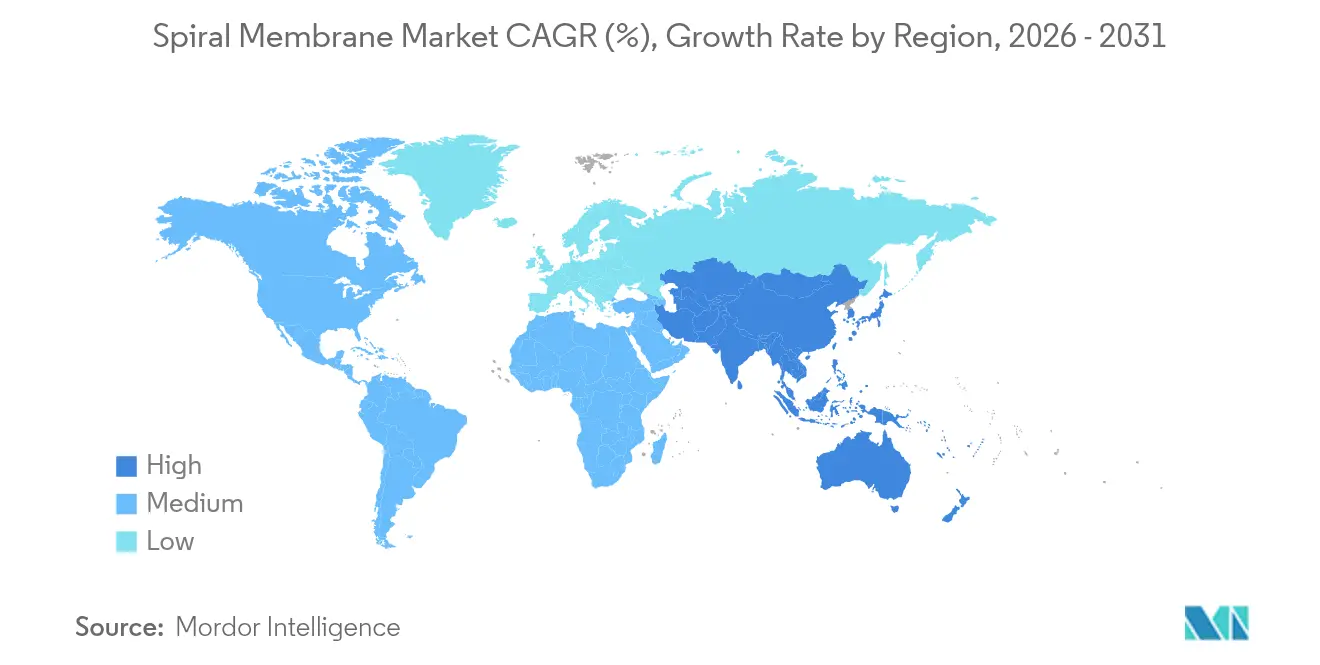

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Spiral Membrane Market Analysis by Mordor Intelligence

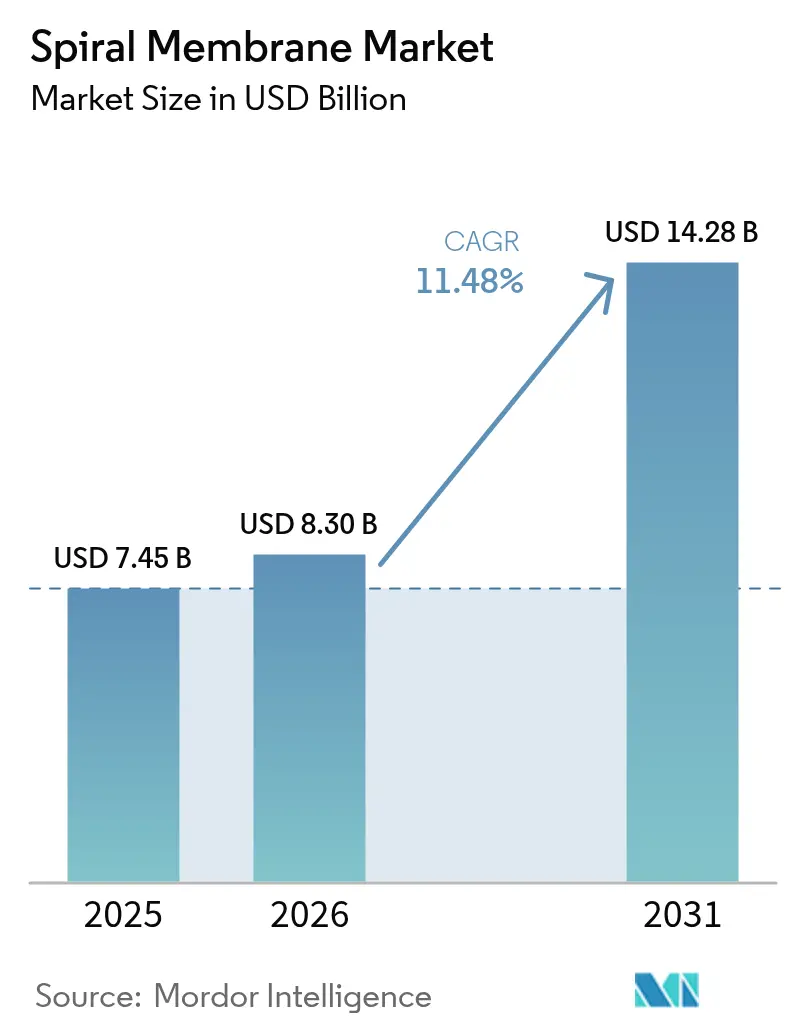

The Spiral Membrane Market size was valued at USD 7.45 billion in 2025 and estimated to grow from USD 8.3 billion in 2026 to reach USD 14.28 billion by 2031, at a CAGR of 11.48% during the forecast period (2026-2031). Strong growth rests on the technology’s ability to increase water-treatment capacity while satisfying tightening discharge standards. Buyers in industrial and municipal sectors gravitate toward spiral membranes because their high packing density lowers equipment footprints and capital costs. Polyamide thin-film composite (TFC) elements remain the mainstream choice for large-scale desalination, yet fluoropolymer designs are winning share in harsh-chemistry streams. Reverse osmosis (RO) installations drive the bulk of current demand, though ultrafiltration (UF) modules are scaling quickly as food and beverage processors intensify protein-recovery projects. Regionally, Asia Pacific dominates both usage and momentum: local regulations now compel factories, utilities, and lithium-brine operators to adopt advanced treatment for compliance. North America and Europe provide steady upgrade demand as operators replace aging equipment and pursue per- and polyfluoroalkyl substances (PFAS) abatement. Competitive dynamics remain moderately fragmented; multinational suppliers reinforce their positions through material science advances and targeted acquisitions that broaden service portfolios.

Key Report Takeaways

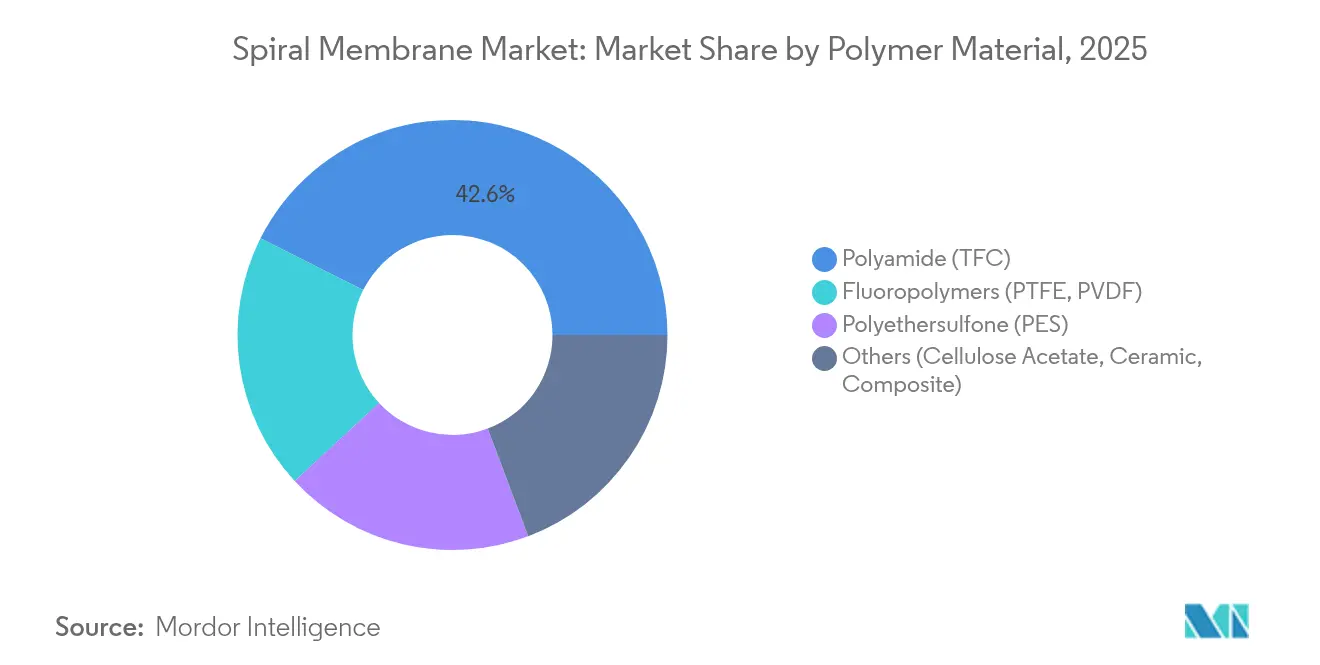

- By polymer material, polyamide TFC products captured 42.58% of the spiral membrane market share in 2025, while fluoropolymers are projected to post a 12.34% CAGR through 2031.

- By separation technique, reverse osmosis accounted for 46.88% of revenue in 2025; ultrafiltration is set to record the fastest 12.52% CAGR to 2031.

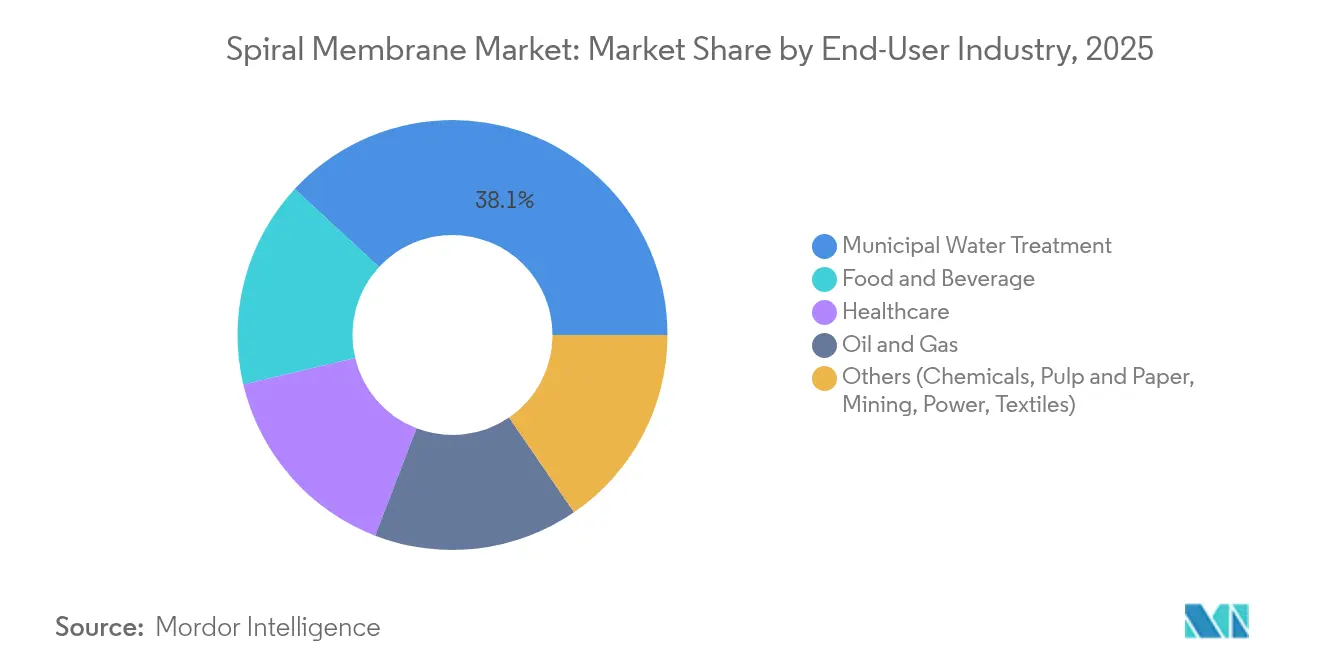

- By end-user industry, municipal water treatment held 38.12% of revenue in 2025; the food and beverage segment is forecast to advance at a 12.76% CAGR over the period.

- By geography, Asia Pacific commanded 33.74% of 2025 revenue and is projected to expand at a 12.63% CAGR, topping all other regions.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Spiral Membrane Market Trends and Insights

Driver Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expanding food and beverage protein-fractionation needs | +2.8% | Global, with concentration in North America & EU dairy regions | Medium term (2-4 years) |

| Stricter industrial and municipal wastewater discharge norms | +3.2% | Global, led by APAC regulatory tightening | Short term (≤ 2 years) |

| Shift from hollow-fiber to high-flux spiral-wound modules | +1.9% | North America & EU industrial sectors | Medium term (2-4 years) |

| Adoption of hot-sanitizable spiral membranes in bioprocessing | +1.4% | North America & EU pharmaceutical hubs | Long term (≥ 4 years) |

| Lithium-brine concentration via spiral nanofiltration in battery supply chain | +2.4% | APAC core, spill-over to South America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Expanding Food and Beverage Protein-Fractionation Needs

Dairy processors and juice bottlers are migrating from thermal concentration to membrane fractionation so they can produce value-added protein isolates that sell at 40-60% price premiums. Modern spiral-wound microfiltration lines separate whey proteins with 99% efficiency while preserving functional properties, allowing manufacturers to serve sports-nutrition, medical-nutrition, and infant-formula channels. Recent spacer redesigns lift cross-flow velocity, which suppresses fouling and stretches run times between cleanings. Plant managers also appreciate the smaller footprint; spiral modules pack two to three times more surface area than equivalent hollow-fiber units, lowering civil‐work costs.

Shift from Hollow-Fiber to High-Flux Spiral-Wound Modules

Industrial water operators notice that spiral-wound designs deliver up to three-fold higher packing density than hollow-fiber counterparts, enabling smaller skids and lower replacement costs. Cleaning protocols also improve: new feed-spacer geometries enhance turbulence, reducing chemical use. These benefits are decisive in viscous streams such as dairy, sugar, and gelatin, where hollow-fiber membranes foul rapidly.

Adoption of Hot-Sanitizable Spiral Membranes in Bioprocessing

Biopharmaceutical plants now specify hot-sanitizable spiral elements that tolerate 121 °C steam, eliminating harsh chemicals, simplifying validation, and cutting downtime. Growth in monoclonal-antibody and cell-therapy output accelerates uptake. Single-use system designers value the compact layout and the ability to maintain sterility throughout continuous manufacturing.

Stricter Industrial and Municipal Wastewater Discharge Norms

Policy changes such as the revised EU Urban Wastewater Treatment Directive and Asia Pacific zero-liquid-discharge mandates force utilities and factories to add advanced treatment lines capable of removing micropollutants, pharmaceuticals, and PFAS[1]European Commission, “Urban Wastewater Treatment Directive Revision,” wateronline.com . Municipalities retrofit conventional activated-sludge plants with membrane bioreactors that integrate spiral modules, cutting biosolid output by 90%. Textiles, chemicals, and pharmaceuticals now install multi-stage RO and nanofiltration trains to keep effluent within allowable limits, creating non-discretionary demand that shields the spiral membrane market from short-cycle economic swings.

Restraint Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Membrane fouling and cleaning-chemical costs | -2.1% | Global, particularly in high-fouling applications | Short term (≤ 2 years) |

| High energy/pressure demand for RO operations | -1.8% | Global, concentrated in energy-intensive regions | Medium term (2-4 years) |

| Volatile pricing of ultra-pure polyamide casting films | -1.3% | Global, with supply chain concentration in Asia Pacific | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Membrane Fouling and Cleaning-Chemical Costs

Across Dutch desalination plants, cleaning accounts for 24% of RO operating expenses. Biofouling shortens membrane life, especially in polyamide elements that cannot tolerate free chlorine. Developers are coating surfaces with zwitterionic polymers and leveraging pulsed-flow cleaning to cut chemical use in half. Until these tools mature, elevated cleaning and downtime costs will temper adoption in heavily bio-active streams.

High Energy/Pressure Demand for RO Operations

Producing 1 m³ of permeate from seawater still consumes 3-4 kWh of electricity on average. Energy can reach 50% of a plant’s operating bill, a barrier in regions with costly power. Although isobaric recovery devices reclaim up to 98% of hydraulic energy and ultra-high-permeability membranes raise flux by 25-30%, widespread deployment takes time. Capital outlays for 120-bar pumps and corrosion-resistant piping remain substantial.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Polymer Material: Polyamide Dominance Faces Fluoropolymer Challenge

Polyamide thin-film composites retained a 42.58% spiral membrane market share in 2025, propelled by decades of performance optimization in desalination where 99.5% salt rejection is routine. PES holds niche utility in bioprocessing because it withstands repeated steam cycles. Fluoropolymers such as PVDF and PTFE, though only a small slice today, are on track to grow 12.34% annually, capturing opportunities in lithium brine, semiconductor, and aggressive-solvent streams. These chemistries tolerate pH 0–14 and temperatures to 120 °C, features that justify premium pricing. Surface-activation techniques—plasma etching, UV grafting—now overcome their intrinsic hydrophobicity, pushing water flux toward polyamide territory.

The polyamide segment draws strength from mature supply chains and competitive pricing, but its chlorine sensitivity restricts reuse after fouling events, nudging operators toward fluoropolymer retrofits. Ceramic and composite designs populate extreme environments such as produced-water clean-up, where uptime outweighs capital intensity. They represent a small yet strategic fragment of the spiral membrane market size for specialty chemicals and mining services.

By Separation Technique: RO Leadership Challenged by UF Innovation

Reverse osmosis sustained 46.88% revenue in 2025 on the back of global desalination and ultrapure-water applications. Plants achieve permeate with fewer than 10 ppm total dissolved solids, a spec unattainable by thermal distillation at comparable cost. UF lines, however, are accelerating at a 12.52% CAGR. Food, dairy, and biotech processors adopt UF for high-value protein concentration, cutting chemical steps out of flowsheets. Nanofiltration occupies the middle ground, excelling at selective divalent-ion removal for water softening or solvent-recycling tasks. Microfiltration still serves as RO pretreatment and beverage clarification, but its share grows slowly.

Advances in UF membrane chemistry upgrade fouling resistance and heightened flux, enabling single-pass recoveries above 90% for whey proteins. The spiral membrane market size for lithium extraction also leans on NF’s selective permeability, where sodium passes but magnesium and calcium remain, boosting lithium yield.

By End-User Industry: Municipal Leadership Meets F&B Innovation

Municipal utilities represented 38.12% of 2025 revenue as governments funded infrastructure to meet tightening nutrient and micropollutant limits. Membrane bioreactor adoption in cities such as Beijing and Chennai expands 14.5% annually. Meanwhile, food and beverage processors form the fastest-growth cohort at 12.76% CAGR; spiral-wound modules concentrate proteins, sugars, and juices while meeting clean-label expectations. Healthcare manufacturers also increase spending, driven by single-use biologics production. Oil and gas operators embrace ceramic-lined spiral elements to recycle produced water and cut freshwater withdrawals by 98%.

Municipal segments concentrate on total cost of ownership, valuing elements that resist biofouling and reduce chemicals. Food and beverage buyers prioritize product purity and temperature control, favoring hot-sanitizable PES and fluoropolymer designs. The spiral membrane market size for mining and textiles remains smaller but grows steadily as zero-liquid-discharge rules spread.

Geography Analysis

Asia Pacific commands the largest slice of spiral membrane market share at 33.74% in 2025, and its 12.63% CAGR through 2031 outpaces all other regions. Environmental enforcement now compels Chinese factories to install advanced membranes, while India funnels public funds into municipal upgrades under schemes such as the Jal Jeevan Mission. Semiconductor fabs in Taiwan, Japan, and South Korea require ultra-pure water below 5 ppt total organic carbon, pushing demand for high-selectivity RO and UF stacks. Australia leans on spiral-wound RO to secure potable water for cities facing protracted drought.

North America is the second-largest consumer as the Infrastructure Investment and Jobs Act channels USD 55 billion into water-system modernization. Aging RO trains from the early-2000s are being swapped for high-permeability designs that cut energy 20-25%. Market activity centers on upgrading PFAS removal and industrial reuse. Mexico’s automotive corridor invests in zero-liquid-discharge, boosting local spiral membrane imports.

Europe maintains strict effluent norms under the Water Framework Directive, spurring retrofits across food, beverage, and pharmaceutical plants. Scandinavian utilities pilot PFAS-targeted nanofiltration, while southern states deploy seawater desalination to offset prolonged drought. Suppliers see healthy aftermarket sales as operators adhere to energy-efficiency and circular-economy targets.

Latin American demand concentrates in mining hubs. Chile and Argentina fit spiral nanofiltration for lithium salars, extracting battery-grade feedstock while recycling brine. Brazil’s pulp-and-paper mills adopt RO for closed-loop bleaching circuits, trimming chemical oxygen demand discharges by 85%. The Middle East and North Africa emphasize megascale RO plants where state utilities explore energy-recovery devices to offset power constraints. Sub-Saharan Africa’s uptake remains low but climbs as multilateral lenders finance sewage-reuse projects in water-scarce cities.

Competitive Landscape

The spiral membrane market remains highly consolidated. DuPont retained its Water Solutions division in 2025, signaling long-term confidence after weighing a divestiture. Toray Industries expands integrated offerings by fusing RO, NF, and MBR modules under one digital monitoring platform. SUEZ consolidates aftermarket service networks after Veolia’s acquisition of Water Technologies and Solutions closed in 2025, pushing synergies in global procurement.

Thermo Fisher’s USD 4.1 billion purchase of Solventum’s purification unit strengthens vertically integrated bioprocessing systems aimed at hot-sanitizable spiral membranes. Niche players—NX Filtration, Aquaporin, and Keppel—commercialize biomimetic and 2D-material layers that promise double-digit flux gains. Start-ups concentrate on surface-anchored zwitterionic coatings that curb fouling without chlorine. Competitive intensity is highest in commodity water treatment where lifecycle costs dictate supplier selection; in contrast, pharmaceutical and lithium-extraction clients favor high-performance membranes, accepting premiums for specialized functionality.

Spiral Membrane Industry Leaders

SUEZ

DuPont

LG Chem

Hydranautics (Nitto)

Toray Industries Inc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: ZwitterCo unveiled a new line of sanitary superfiltration (SF) spiral membrane elements, harnessing its advanced second-generation SF technology. These FDA-compliant membranes are tailored for whey processing, facilitating the production of whey protein concentrate (WPC) and whey protein isolate (WPI).

- July 2024: Kovalus Separation Solutions, previously known as Koch Separation Solutions, is pouring over USD 20 million into a cutting-edge, 140,000 square-foot facility in Mexico dedicated to spiral membrane element assembly.

Global Spiral Membrane Market Report Scope

The Spiral Membrane market report includes:

| Polyamide (TFC) |

| Polyethersulfone (PES) |

| Fluoropolymers (PTFE, PVDF) |

| Others (Cellulose Acetate, Ceramic, Composite) |

| Microfiltration (MF) |

| Ultrafiltration (UF) |

| Nanofiltration (NF) |

| Reverse Osmosis (RO) |

| Municipal Water Treatment |

| Food and Beverage |

| Healthcare |

| Oil and Gas |

| Others (Chemicals, Pulp and Paper, Mining, Power, Textiles) |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN | |

| Australia and New Zealand | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| South Africa | |

| Rest of Middle East and Africa |

| By Polymer Material | Polyamide (TFC) | |

| Polyethersulfone (PES) | ||

| Fluoropolymers (PTFE, PVDF) | ||

| Others (Cellulose Acetate, Ceramic, Composite) | ||

| By Separation Technique | Microfiltration (MF) | |

| Ultrafiltration (UF) | ||

| Nanofiltration (NF) | ||

| Reverse Osmosis (RO) | ||

| By End-user Industry | Municipal Water Treatment | |

| Food and Beverage | ||

| Healthcare | ||

| Oil and Gas | ||

| Others (Chemicals, Pulp and Paper, Mining, Power, Textiles) | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current Spiral Membrane Market size?

The spiral membrane market size reached USD 8.3 billion in 2026 and is forecast to hit USD 14.28 billion by 2031, reflecting an 11.48% CAGR.

Which polymer material holds the largest spiral membrane market share?

Polyamide thin-film composite membranes led with 42.58% market share in 2025 thanks to proven performance in desalination and industrial reuse.

Why is Asia Pacific growing fastest in the spiral membrane market?

Rapid industrialization, stricter effluent rules, and heavy investments in municipal water infrastructure drive Asia Pacific’s 12.63% CAGR.

How are spiral membranes applied in food and beverage processing?

Dairy and juice producers use spiral-wound microfiltration and ultrafiltration to recover proteins and clarify liquids while preserving flavor and nutrition, supporting a 12.76% CAGR in this segment.

Page last updated on: