Membrane Separation Technology Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

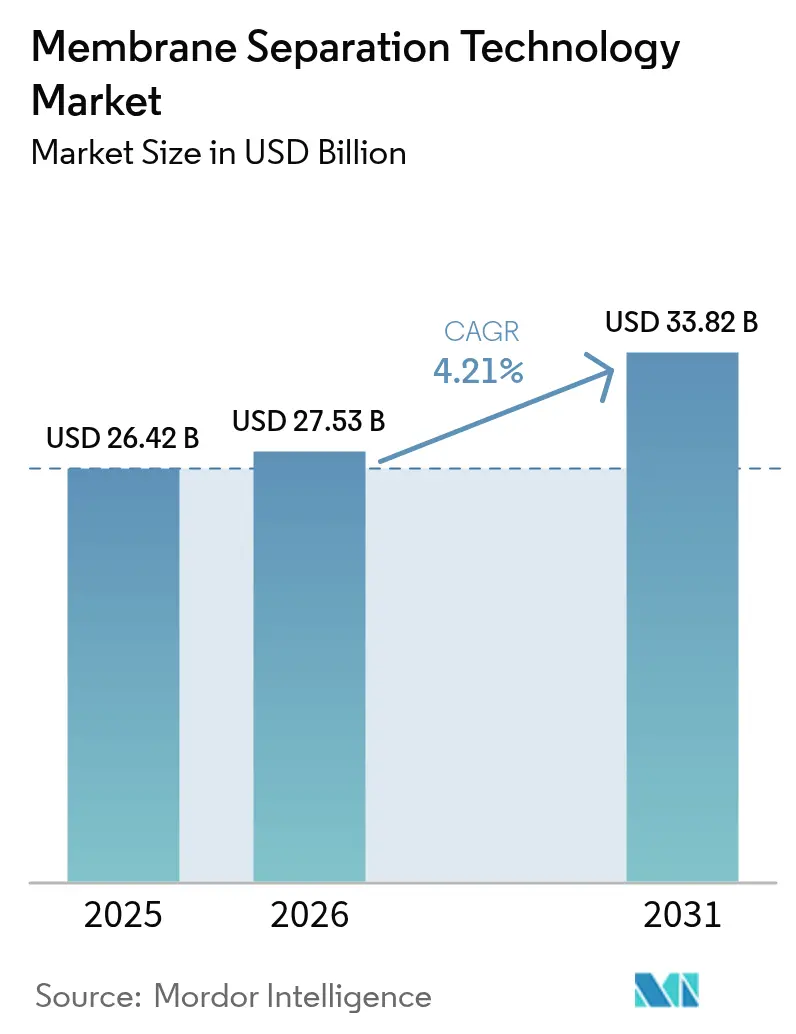

| Market Size (2026) | USD 27.53 Billion |

| Market Size (2031) | USD 33.82 Billion |

| Growth Rate (2026 - 2031) | 4.21% CAGR |

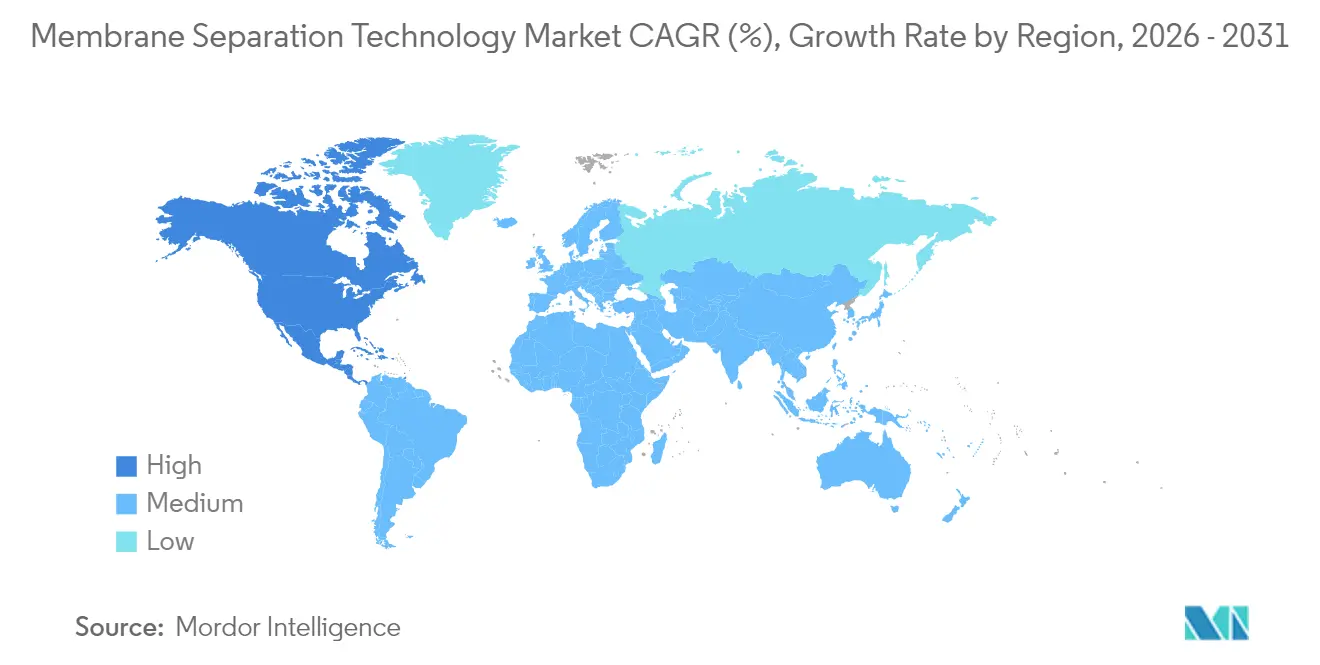

| Fastest Growing Market | North America |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Membrane Separation Technology Market Analysis by Mordor Intelligence

The Membrane Separation Technology Market size market is expected to grow from USD 26.42 billion in 2025 to USD 27.53 billion in 2026 and is forecast to reach USD 33.82 billion by 2031 at 4.21% CAGR over 2026-2031. Robust demand for high-quality water, tougher discharge rules, and rapid progress in membrane chemistry anchor this expansion. Reverse osmosis holds sway because large-scale desalination projects still prize its high salt rejection, yet forward-osmosis pilots and smarter hybrid systems are narrowing the efficiency gap. Polymeric membranes remain the workhorse thanks to cost advantages, but composite-hybrid designs loaded with graphene oxide or metal-organic frameworks are capturing attention for their higher selectivity and better fouling resistance. Hollow fiber modules dominate installations because their self-supporting geometry packs more surface area per vessel, trims installation weight, and cuts long-run maintenance needs. Regionally, Asia-Pacific’s industrial surge keeps it in the lead, while North America’s fresh PFAS rules lift demand for nanofiltration and next-generation reverse-osmosis lines.

Key Report Takeaways

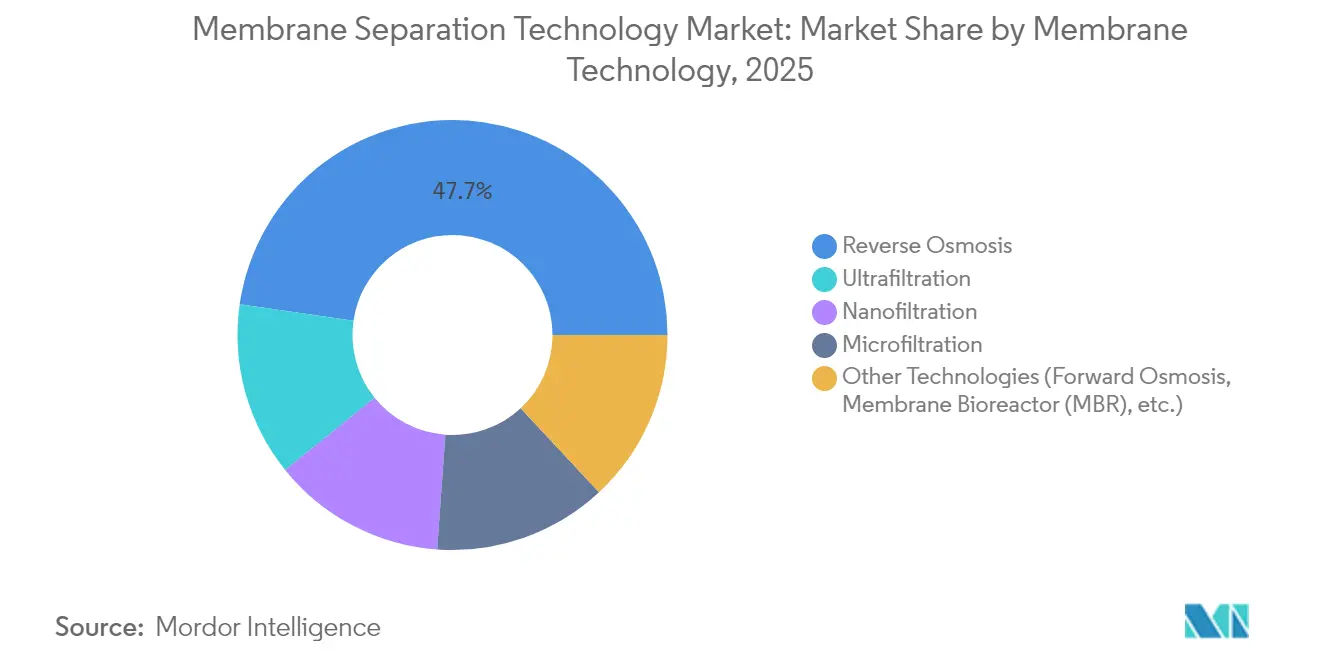

- By membrane technology, reverse osmosis commanded 47.73% of membrane separation technology market share in 2025, whereas forward-osmosis and membrane bioreactor systems are projected to log the quickest 4.92% CAGR through 2031.

- By membrane material, polymeric grades captured 64.52% of the membrane separation technology market size in 2025; composite-hybrid variants are on track for a 5.11% CAGR over the forecast window.

- By module configuration, hollow fiber accounted for 52.66% of the membrane separation technology market size and is forecast to expand at a 4.96% CAGR between 2026-2031.

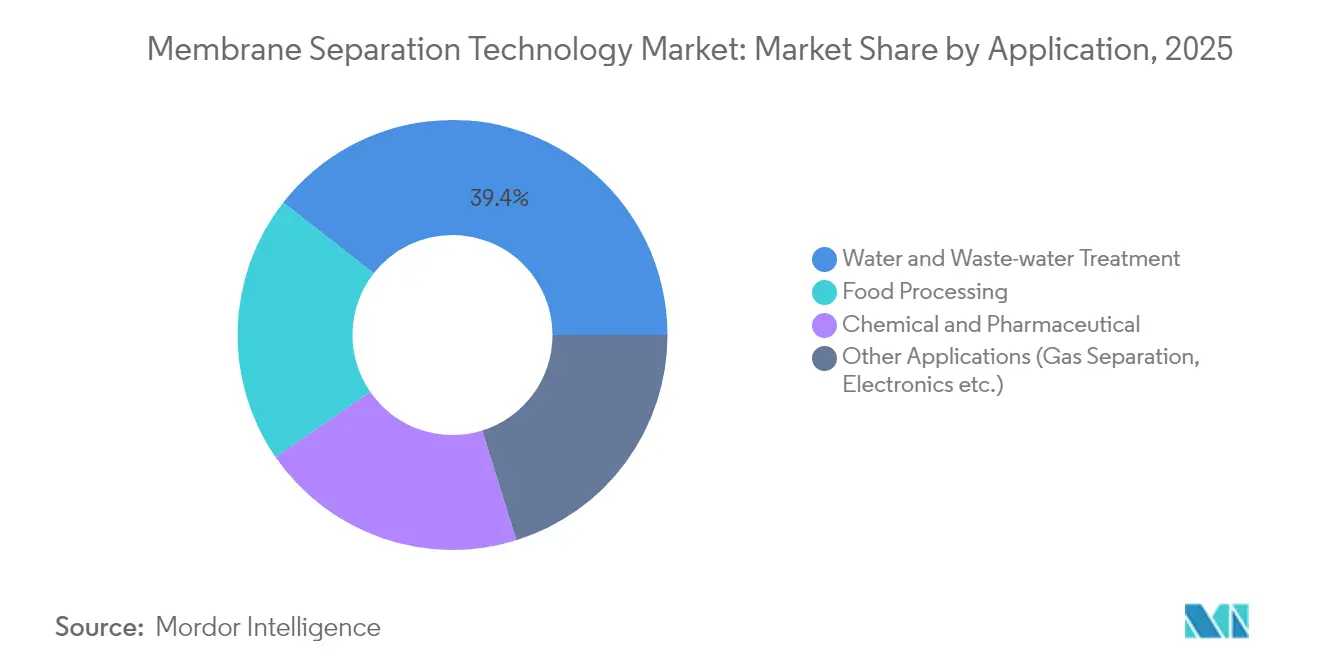

- By application, water and wastewater treatment led with 39.42% of revenue in 2025, while chemical and pharmaceutical processing is set to grow at a 5.09% CAGR to 2031.

- By geography, Asia-Pacific held 40.83% of revenue in 2025, while North America is the fastest-growing region at a 4.86% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Membrane Separation Technology Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Demand for Water and Waste-Water Treatment | +1.2% | Global, with highest impact in Asia-Pacific and Middle East | Long term (≥ 4 years) |

| Growth in Food, Beverage and Pharma Processing | +0.8% | North America and EU, expanding to Asia-Pacific | Medium term (2-4 years) |

| Stricter Industrial Effluent Regulations | +0.7% | Global, led by EU and North America | Short term (≤ 2 years) |

| Adoption of Forward-Osmosis and Electrically Responsive Membranes | +0.5% | North America and EU, pilot deployments in Asia-Pacific | Long term (≥ 4 years) |

| Low-Alcohol Beverage Processing Demand | +0.3% | Global, concentrated in developed markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Water and Waste-Water Treatment

Water scarcity affects 2 billion people globally, creating unprecedented demand for membrane-based purification technologies that can process contaminated water sources previously deemed unusable. Municipal water treatment facilities are increasingly adopting membrane bioreactor systems, with China alone implementing over 300 MBR plants achieving nearly 100% annual growth compared to the global rate of 10.9%. The technology's ability to produce high-quality effluent suitable for direct reuse is driving adoption in water-stressed regions, where traditional treatment methods prove inadequate for meeting stringent discharge standards. Advanced membrane configurations are enabling utilities to extract potable water from sources with high salinity and organic contamination levels. The shift toward decentralized water treatment systems is creating new market segments, particularly in industrial zones where on-site treatment reduces transportation costs and regulatory compliance risks.

Growth In Food, Beverage and Pharma Processing

Dairy groups now rely on cross-flow microfiltration to concentrate whey proteins without heat damage, extending product lines into high-margin nutritional isolates DAIRYNETWORK.COM. Pharmaceutical plants are shifting from distillation to ultrafiltration for water-for-injection; Asahi Kasei’s latest skid removes 99.999% endotoxins while trimming energy draw by 30%[1]Asahi Kasei Corporation, “UF-UF Systems for Pharmaceutical Water,” asahikasei.com . The surge in low-alcohol beverages further strengthens demand because hollow fiber nanofiltration strips ethanol while preserving delicate aroma compounds better than vacuum evaporation. Membrane steps also isolate bioactive ingredients for functional foods at ambient temperatures, protecting heat-sensitive nutraceuticals and lowering operating costs.

Stricter Industrial Effluent Regulations

The EU Industrial Emissions Directive compels chemical plants to adopt Best Available Techniques, propelling uptake of ceramic nanofiltration lines that withstand high temperatures and harsh solvents EUR-LEX.EUROPA.EU. North American refineries mirror this trend as the US Environmental Protection Agency tightens heavy-metal limits in discharge permits. Modular membrane skids allow staged expansions when rules get tougher, sidestepping costly civil works. Coupled with real-time conductivity monitoring, membranes help factories recycle 40%-60% of process water, tempering fresh-water withdrawals and complying with ESG mandates.

Adoption of Forward-Osmosis and Electrically Responsive Membranes

Forward-osmosis plants now exploit recyclable draw solutions, slicing specific energy use by 30% relative to classic reverse osmosis in high-brine streams. Laboratory prototypes of electrically gated nanochannels shift permeability with a one-volt cue, replicating 15 bar of hydraulic pressure and enabling on-the-fly tuning. AI-coupled membrane bioreactors forecast fouling and schedule clean-in-place cycles automatically, extending membrane life by 25% and cutting chemical use. These breakthroughs open fresh opportunities in difficult niches such as produced-water treatment and selective resource recovery.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Capital and Operating Costs | -0.9% | Global, most pronounced in developing markets | Medium term (2-4 years) |

| Membrane Fouling and Maintenance Complexity | -0.6% | Global, particularly in industrial applications | Short term (≤ 2 years) |

| Impending PFAS Restrictions on Membrane Components | -0.4% | EU and North America, expanding globally | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Capital and Operating Costs

Ceramic membranes outlast polymeric rivals but require pricier alumina or zirconia substrates, elevating installed costs by up to 50% in low-income regions. Where power rates exceed USD 0.12 /kWh, energy line items can raise life-cycle ownership by 20-30% over conventional clarification. Investors demand clear visibility on payback, lengthening procurement cycles for public utilities that already face budget constraints. Financing hurdles spur innovative leasing models and outcome-based contracts that shift capital risk to suppliers, yet adoption remains slow in markets with limited credit access.

Membrane Fouling and Maintenance Complexity

Biofouling slashes flux in food and beverage applications rich in proteins and polysaccharides. Graphene-oxide surface coatings delay colonization but add manufacturing steps and cost premiums of 10-12%. Industrial users often lack trained technicians to diagnose early fouling, leading to daily cleans that boost chemical use and downtime. Predictive analytics platforms tied to trans-membrane pressure sensors are starting to fill this gap, but widespread deployment hinges on stronger digital skills at plant level.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Membrane Technology: Reverse Osmosis Holds a Comfortable Lead but Alternatives Accelerate

Reverse osmosis contributed 47.73% to the membrane separation technology market in 2025 on the back of seawater desalination megaprojects and industrial reuse schemes. Utilities pick RO for its near-universal chemistry barrier and mature supply base that cushions capital costs. Forward-osmosis together with membrane bioreactors is now the fastest-expanding cluster at a 4.92% CAGR, showing that operators want lower energy profiles for high-TDS feeds. Ultrafiltration and nanofiltration continue to carve space by handling specific solute ranges and acting as robust pretreatment steps that safeguard downstream RO arrays.

Hybrid trains that weld microfiltration, nanofiltration, and advanced oxidation in one compact skid are entering pilot stages across Europe. This modular architecture shortens commissioning by 25% and achieves target effluent quality without bespoke civil works. The membrane separation technology industry therefore sees integrators compete on smart process controls and interoperable element designs rather than on polymer recipes alone.

By Membrane Material: Polymeric Grades Remain Mainstay but Composite-Hybrid Builds Momentum

Polymeric membranes accounted for 64.52% of the membrane separation technology market size in 2025 owing to scalable extrusion lines and well-studied chemistries. Polyethersulfone and polyvinylidene fluoride dominate potable-water deployments where mechanical resilience and chlorine tolerance are prized. However, looming PFAS phase-outs are nudging suppliers to tweak formulations and test fluorine-free alternatives.

Composite-hybrid membranes will clock a 5.11% CAGR through 2031 by embedding graphene oxide, zeolites, or metal-organic frameworks inside polymer backbones that raise selectivity without hurting permeability. Pilot ceramic-supported composites already outperform legacy polymers in hot acid streams, granting them footholds in petrochemical and mining sectors. The resultant material diversification lowers reliance on any single chemical feedstock and mitigates regulatory risks that could otherwise slow the membrane separation technology market.

By Module Configuration: Hollow Fiber Clinches Both Volume and Velocity

Hollow fiber retained 52.66% of shipments in 2025 and is forecast to rise at a 4.96% CAGR to 2031, making it the unrivaled champion in surface-area efficiency. Plants favor the geometry because it self-supports, dispenses with spacers, and delivers higher packing densities that trim footprint by up to 20%. Gas-tight hollow fiber bundles now target hydrogen recovery and CO₂ removal, broadening revenue prospects.

Spiral-wound elements keep their hold in reverse-osmosis trains due to standardized dimensions and well-priced housings. Plate-and-frame stacks address niche hygienic duties where full-face clean-in-place access is mandatory. Tubular modules, though niche, endure in pulp and paper mills that endure heavy solids loading. Advances in automated potting and fiber integrity-testing assure plant managers of trouble-free runs, reinforcing hollow fiber’s broadening acceptance.

By Application: Water Treatment Still Dominates While Pharma Races Ahead

Water and wastewater treatment represented 39.42% of 2025 revenue and remains central to the membrane separation technology market. Municipal plants champion hollow fiber ultrafiltration as a polishing step before disinfection, enabling potable reuse programs that offset groundwater stress. Industrial clusters add closed-loop rinse water circuits equipped with nanofiltration to slash intake fees and meet zero-liquid-discharge mandates.

Chemical and pharmaceutical lines, though smaller, will post a 5.09% CAGR to 2031—the steepest among end uses. Biologics firms install single-use tangential-flow filters to speed batch changeovers while keeping sterility risk low. Beverage groups broaden the reach of dealcoholized beer and wine, a segment that pivotally leans on spiral-wound nanofiltration cassettes to preserve volatile aromas. These trends cement membranes as essential enablers of product innovation and green manufacturing agendas.

Geography Analysis

Asia-Pacific generated 40.83% of global sales in 2025, underpinned by double-digit industrial growth across China, India, and Vietnam. China rolled out more than 300 membrane bioreactor projects last year, showcasing readiness to leapfrog directly to advanced treatment technologies without legacy aeration lagoons CHINA-WATER.ORG. Regional electronics clusters add wafer-grade ultrapure water capacity every quarter, giving polymeric ultrafiltration and reverse-osmosis skid suppliers a dependable sales funnel. Government subsidies for rural potabilization further widen the addressable base.

North America is on track for the swiftest 4.86% CAGR to 2031 because tightened PFAS caps in drinking water spur urgent retrofit orders. Several US municipalities have issued design-build contracts for nanofiltration lines guaranteed to strip 99% of long-chain PFAS, lifting demand for low-pressure high-selectivity membranes EPA.GOV. Canada’s mining friends are next: revised effluent limits for selenium and nitrate mean membrane concentrators are replacing multi-step chemical treatments.

Europe constitutes a mature yet innovative arena where strict industrial emission ceilings nourish continuous upgrades. Germany and the Netherlands refine ceramic nanofiltration for hard-to-treat leachate and refinery waste, adding use cases that slowly migrate to neighboring markets. Meanwhile, the Middle East accelerates large-scale seawater desalination, typically pairing energy-recovery devices with advanced thin-film composite membranes. African utilities trail but receive concessional finance for containerized treatment units that bypass piped infrastructure deficits, planting seeds for long-run growth.

Competitive Landscape

Global supply is moderately consolidated. DuPont, 3M, Toray, and Veolia collectively held a combined 52% share in 2024, leveraging vast patent estates, broad element catalogues, and service networks. DuPont canceled a proposed water-business spin-off in March 2025, signaling confidence that drinking-water and lithium-extraction membranes warrant internal investment DUPONT.COM. The company continues to bundle ion-exchange and membrane products for holistic treatment packages, raising switching costs for clients.

Strategic moves intensify: Thermo Fisher paid USD 4.1 billion for Solventum’s purification unit to bolster bioproduction offerings and cross-sell into single-use assemblies[2]Thermo Fisher Scientific, “Thermo Fisher to Acquire Solventum’s Purification & Filtration Unit,” thermofisher.com. Toray scales graphene-oxide coating on hollow fibers to cut fouling in MBRs, while Veolia pilots electrically responsive membranes, aiming to commercialize them by 2028. Smaller innovators such as NX Filtration and Aquaporin pursue IPO funds or licensing deals, betting that biomimetic channels and thin nano-porous layers will capture premium niches.

White-space opportunities sprout in lithium brine purification where nanofiltration selectively rejects divalent ions yet passes lithium at high flux. Multiple Australian start-ups trial these membranes in Chile and Argentina to sidestep reagent-heavy precipitation routes. AI-enabled predictive maintenance also turns into a battleground; service contracts now promise uptime benchmarks with penalties that incentivize vendors to deploy cloud analytics and edge sensors across installed fleets.

Membrane Separation Technology Industry Leaders

DuPont

TORAY ENGINEERING Co.,Ltd.

Veolia Water Technologies & Solutions

Nitto Denko Corporation

3M

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Thermo Fisher Scientific acquired Solventum's Purification and Filtration business for USD 4.1 billion, expanding its bioproduction capabilities and membrane separation technology portfolio in biologics manufacturing.

- July 2023: DuPont introduced FilmTec™ LiNE-XD, a nanofiltration membrane separation technology designed for lithium-brine purification in Direct Lithium Extraction (DLE) operations. The technology uses membrane chemistry to separate lithium from other ions in brine solutions.

Global Membrane Separation Technology Market Report Scope

The Membrane Separation Technology Market report include:

| Reverse Osmosis |

| Ultrafiltration |

| Nanofiltration |

| Microfiltration |

| Other Technologies (Forward Osmosis, Membrane Bioreactor (MBR), etc.) |

| Polymeric |

| Ceramic |

| Composite / Hybrid (Graphene, MOF, Zeolite) |

| Spiral Wound |

| Hollow Fiber |

| Plate and Frame |

| Tubular |

| Water and Waste-water Treatment |

| Food Processing |

| Chemical and Pharmaceutical |

| Other Applications (Gas Separation, Electronics etc.) |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| NORDIC Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Membrane Technology | Reverse Osmosis | |

| Ultrafiltration | ||

| Nanofiltration | ||

| Microfiltration | ||

| Other Technologies (Forward Osmosis, Membrane Bioreactor (MBR), etc.) | ||

| By Membrane Material | Polymeric | |

| Ceramic | ||

| Composite / Hybrid (Graphene, MOF, Zeolite) | ||

| By Module Configuration | Spiral Wound | |

| Hollow Fiber | ||

| Plate and Frame | ||

| Tubular | ||

| By Application | Water and Waste-water Treatment | |

| Food Processing | ||

| Chemical and Pharmaceutical | ||

| Other Applications (Gas Separation, Electronics etc.) | ||

| By Geography | Asia-Pacific | China |

| Japan | ||

| India | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| NORDIC Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the current size of the membrane separation technology market?

The market is valued at USD 27.53 billion in 2026 and is forecast to reach USD 33.82 billion by 2031.

Which membrane technology holds the largest share today?

Reverse osmosis leads with 47.73% of global revenue thanks to its established role in desalination and high-purity water production.

Which application segment is growing fastest through 2031?

Chemical and pharmaceutical processing is projected to post a 5.09% CAGR owing to stricter purity needs in biologics and sterile formulations.

Why is North America the fastest-growing regional market?

New PFAS drinking-water limits have triggered accelerated investments in nanofiltration and low-pressure reverse-osmosis replacements.

What is the biggest restraint on wider adoption of membrane technologies?

High capital outlays and operating costs, especially for ceramic systems, continue to delay purchases in developing regions.

Page last updated on: