Ceramic Membranes Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 9.62 Billion |

| Market Size (2031) | USD 14.68 Billion |

| Growth Rate (2026 - 2031) | 8.82% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

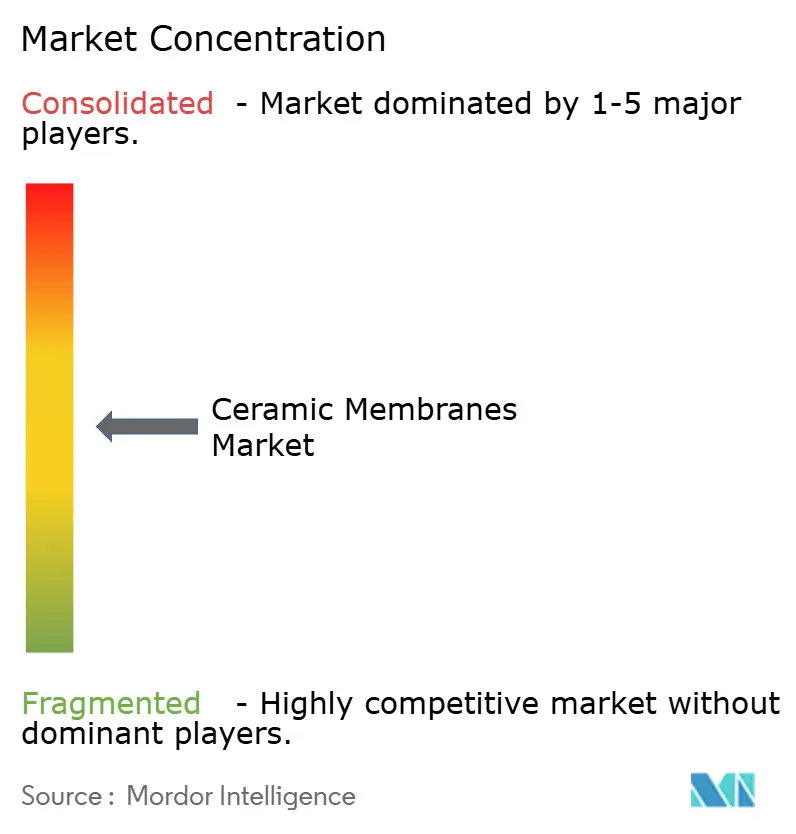

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Ceramic Membranes Market Analysis by Mordor Intelligence

The Ceramic Membranes Market size is expected to increase from USD 8.84 billion in 2025 to USD 9.62 billion in 2026 and reach USD 14.68 billion by 2031, growing at a CAGR of 8.82% over 2026-2031. Accelerating adoption follows three converging streams: utilities are replacing aging polymeric systems to comply with tighter nutrient-discharge limits, dairy processors are switching to alumina and titania tubes to cut energy use in protein concentration, and Asian semiconductor fabs are installing silicon-carbide modules to recycle ultrapure water from chemical-mechanical planarization. In parallel, regional content rules inside China and India are spurring domestic production, while Europe’s impending PVDF restrictions tilt specifications toward all-inorganic membranes. Saudi Arabia has begun large-scale retrofits of desalination pretreatment, confirming the technology’s value in harsh, high-salinity streams. Taken together, these shifts give the ceramic membrane market a resilient double-digit demand runway, even as polymeric competitors defend low-TDS niches.

Key Report Takeaways

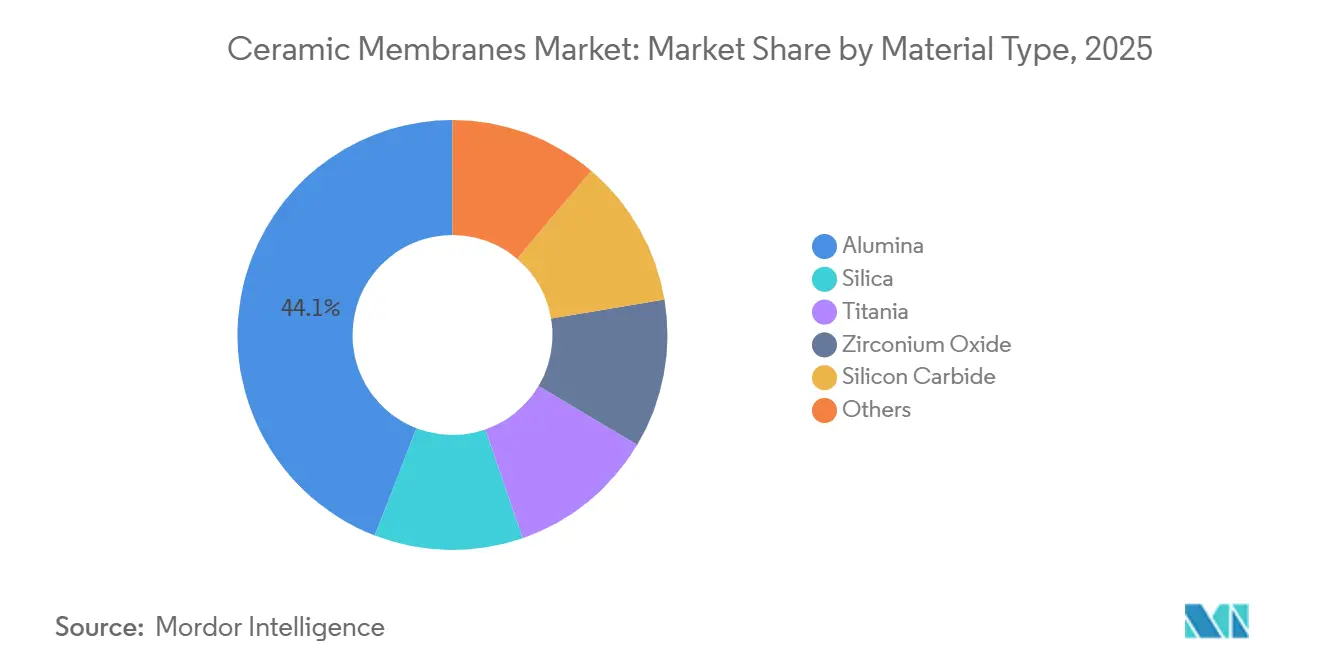

- By material type, alumina captured 44.12% of the ceramic membranes market share in 2025, whereas titania variants are forecast to grow at a 9.80% CAGR to 2031.

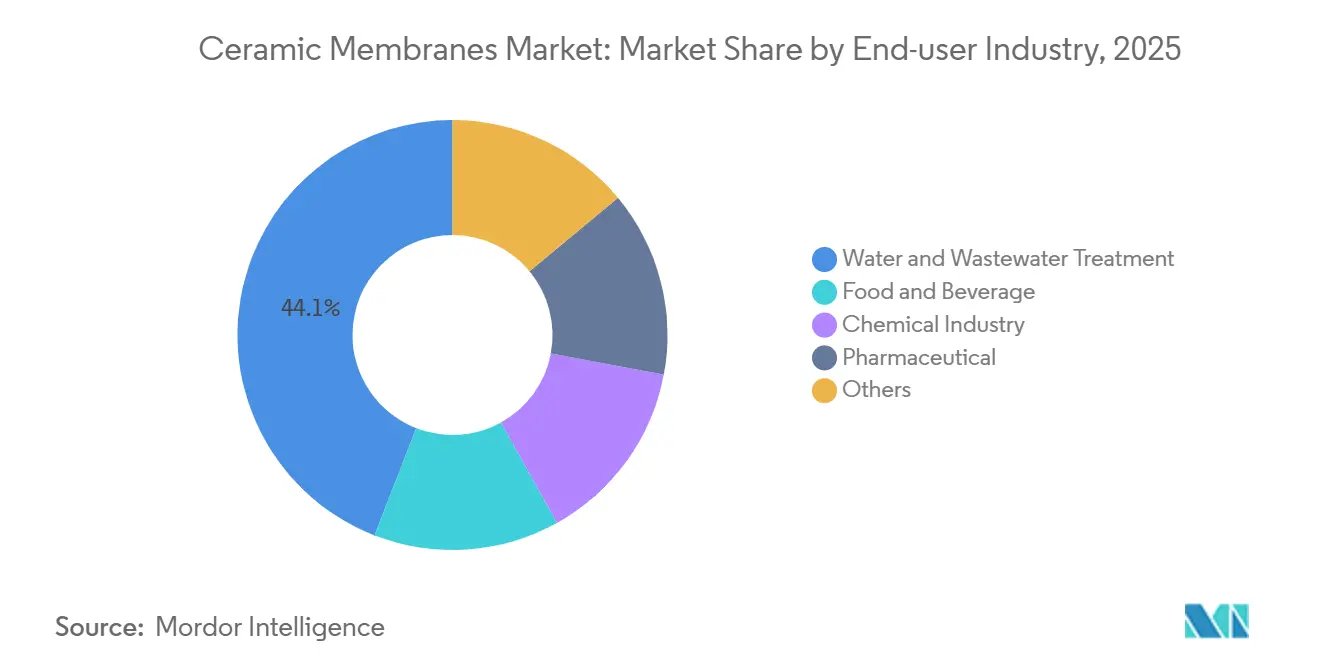

- By end-user industry, water and wastewater treatment led with 44.10% revenue share in 2025, while food and beverage processing is projected to expand at a 9.65% CAGR through 2031.

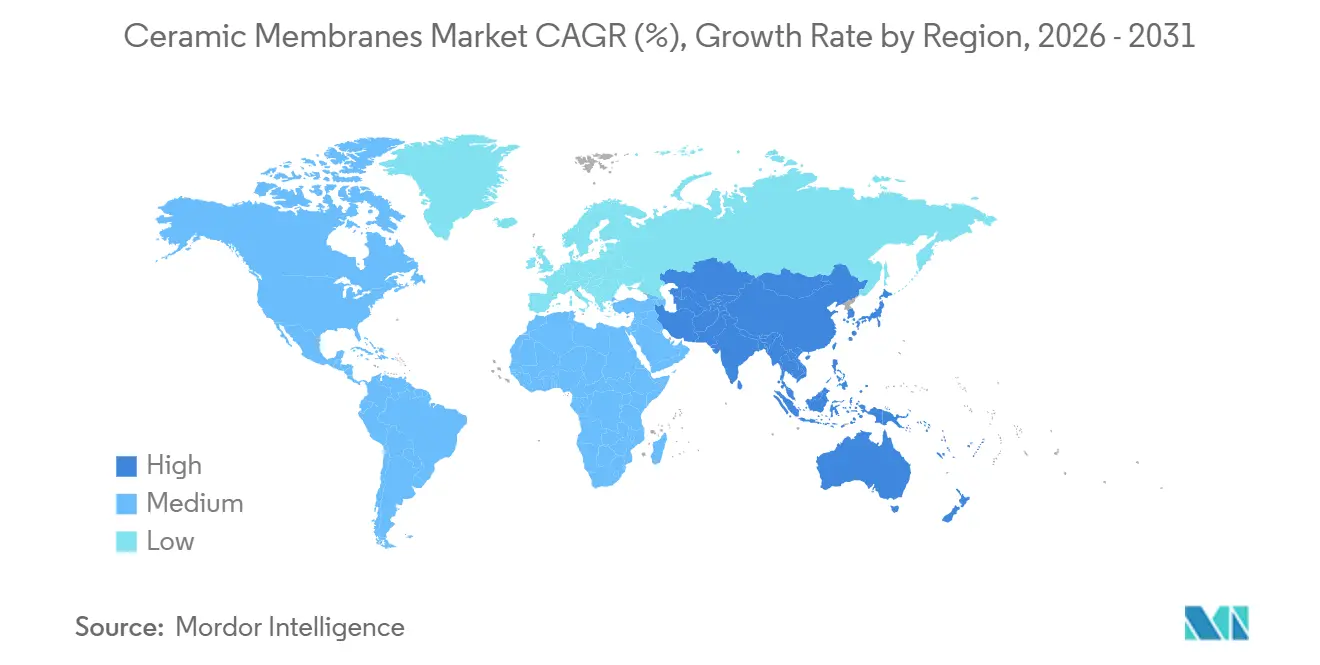

- By geography, Asia-Pacific accounted for 52.98% of the ceramic membranes market size in 2025 and is advancing at a 10.02% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Ceramic Membranes Market Trends and Insights

Driver Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Demand for Water & Wastewater Treatment Infrastructure | +2.8% | Global, focused in APAC and Middle East | Long term (≥ 4 years) |

| Stringent Industrial Effluent Regulations Worldwide | +2.1% | North America, EU, China | Medium term (2–4 years) |

| Longer Service-Life & Lower Lifecycle Cost vs. Polymeric Membranes | +1.6% | Global, early adoption in EU and North America | Medium term (2–4 years) |

| Expansion of Dairy & Beverage Protein-Concentration Processes | +1.4% | North America, EU, APAC | Short term (≤ 2 years) |

| Pending PVDF-Based Membrane Restrictions Driving Ceramic Adoption | +0.9% | EU core, spillover to North America | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Water & Wastewater Treatment Infrastructure

Emerging-economy governments are funding decentralized systems that operate with minimal operator input. India’s Jal Jeevan Mission allocated USD 50 billion to rural water supply and specified ceramic microfiltration for 60% of new installations because backwash intervals stretch to 72 hours versus 24 hours for polymeric cartridges[1]Ministry of Jal Shakti, “Jal Jeevan Mission Progress,” dea.gov.in. China’s zero-liquid-discharge mandate for coal-chemical parks drove 1.8 million m² of ceramic area installations across 340 plants in 2024–2025. Middle-Eastern plants, such as ACWA Power’s Taweelah facility, now front-load RO with 120,000 m² of alumina tubes, cutting chemical dosing by 35%. U.S. nutrient-removal retrofits in Maryland and Virginia adopted ceramic membranes to meet 3 mg/L total nitrogen limits without footprint expansion. Collectively, these programs lift public-sector spending, anchoring longer-term demand for the ceramic membrane market.

Stringent Industrial Effluent Regulations Worldwide

Across regions, regulators are tightening discharge limits that polymeric systems struggle to meet. The US EPA’s 2024 Organic-Chemicals ELGs limit BOD to 10 mg/L and turbidity to 0.5 NTU; ceramic membranes comply without flocculation, avoiding sludge-haul costs that exceed USD 80 per dry ton. Europe’s revised Industrial Emissions Directive now favors cleaning-in-place cycles under 30 minutes, a benchmark ceramics reach with 2% caustic at 80°C[2]U.S. Environmental Protection Agency, “Organic Chemicals ELGs,” epa.gov. China’s pharmaceutical standard GB 31962-2015 caps COD at 50 mg/L, prompting 22 API plants in Zhejiang to switch to ceramic units in 2025 to avoid CNY 500,000 penalties per incident. These simultaneous policy moves add a durable 2.1-point lift to the forecast CAGR for the ceramic membrane market.

Longer Service-Life & Lower Lifecycle Cost vs. Polymeric Membranes

Lifecycle assessments increasingly tilt toward ceramics when downtime and replacement cycles enter the equation. A 2025 Water Research Foundation study comparing 1,000 m³/day municipal plants found ceramic systems needed USD 320,000 in membrane replacements over 10 years, compared with USD 890,000 for polymeric hollow-fibers. Lower hydraulic resistance lets ceramic membranes run at 0.15-0.25 kWh/m³, roughly half the polymeric range. Durability also translates into cheaper insurance; Munich Re’s 2025 guidelines assign lower business-interruption risk, trimming premiums 15–20 basis points. These cost vectors collectively reinforce the total-cost leadership that underpins the ceramic membrane market.

Expansion of Dairy & Beverage Protein-Concentration Processes

Food processors are shifting from thermal to membrane separations to decarbonize operations. Arla Foods cut steam use by 60% when it installed a four-stage ceramic ultrafiltration line in early 2025. Oat-drink makers rely on titania ceramics that maintain flux for 30-day campaigns where polymers foul in hours. Orders for ceramic membrane skids in food applications climbed 28% year-on-year in GEA Group’s 2025 results. FDA allergen-control guidance recommending validated 10 ppm residual-protein cleaning favors ceramic elements that tolerate high-temperature caustic. These processes and regulatory tailwinds feed a short-term boost in the ceramic membrane market.

Restraint Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Prevalence of Low-Pressure Polymeric Alternatives in Low-TDS Uses | -1.20% | Global, concentrated in North America and EU for municipal applications | Medium term (2-4 years) |

| Limited Operator Expertise at Municipal Utilities | -0.80% | Emerging markets (India, Southeast Asia, Africa), spillover to smaller North American utilities | Long term (≥ 4 years) |

| Scarcity of Large-Scale Ceramic Tube Suppliers Outside Asia | -0.70% | North America, Europe, South America, Middle East-Africa; minimal impact in APAC | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Prevalence of Low-Pressure Polymeric Alternatives in Low-TDS Uses

In low-turbidity surface water, polymeric hollow-fiber capital still undercuts ceramics. A 2025 American Water Works Association survey put polymeric microfiltration at USD 420 per m³/day versus USD 680 for ceramics. New PES modules tolerate 500 ppm sodium hypochlorite, narrowing the chemical-resistance gap. Sixty-two percent of North American utilities in a 2025 Water Environment Federation poll ranked the lowest 10-year NPV above the longest life. Retrofitting older low-pressure plants can add USD 150,000–300,000 in ancillary upgrades per train, muting the ceramic membrane market’s near-term upside in these settings.

Limited Operator Expertise at Municipal Utilities

Backwash and chemical-clean cycles for ceramics differ markedly from polymers, yet training lags deployment. The International Water Association reported flux losses exceeding 40% within two years at 18 plants in India and Indonesia, where operators used room-temperature caustic. Workforce shortfalls loom: the US Bureau of Labor Statistics forecasts a 6% decline in water-plant operators by 2032. Vendor-supplied remote-monitoring platforms exist, but only 30% of utilities fund the needed IT backbone. Procurement inertia compounds the issue; 40% of Southeast-Asian tenders still write in polymeric membranes by default, even when lifecycle analytics point the other way. The resulting knowledge gap shaves 0.8 points off the ceramic membrane market’s CAGR.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: Alumina Dominance Meets Titania’s Niche Surge

Alumina captured 44.12% of 2025 revenue, making it the anchor of the ceramic membrane market share. Silicon-carbide follows in abrasive service, but titania variants are set to grow fastest at 9.80% CAGR on semiconductor and pharma demand for 50 nm cut-offs. The ceramic membrane market size for alumina-based elements is projected to reach USD 6.5 billion by 2031 as domestic Chinese capacity pushes unit prices below USD 200/m². Cost differentials persist, titania commands USD 320–400/m² due to phase-control firing, yet its photocatalytic self-cleaning provides a premium in high-purity operations. Emerging glass-ceramic composites promise mid-range cost and broad pH tolerance, hinting at future share redistribution.

Price and durability advantages keep alumina firmly ahead through 2031, but the application mix is diversifying. Silicon-carbide’s Mohs 9.5 hardness makes it indispensable for mining tailings and shale-gas produced water. Zirconia serves solvent-rich organic nanofiltration, though its yttria stabilization cost caps volume under 6%. ISO 19749 test updates covering photocatalytic activity will help titania suppliers differentiate on fouling resistance, maintaining a high single-digit growth trajectory inside the ceramic membrane market.

By End-User Industry: Water Treatment Anchors, Food Processing Accelerates

Water and wastewater treatment held 44.10% revenue in 2025 as utilities raced to meet nutrient and metal effluent rules. The ceramic membrane market size for municipal service is expected to hit USD 7.2 billion by 2031, with Asia-Pacific upgrades driving half that total. Desalination pretreatment remains pivotal; removing colloidal silica before RO extends element life from five to eight years and halves chemical cleans, an ROI that utilities in the Gulf now quantify at USD 0.07 per m³ saved.

Food and beverage lines are growing quicker, clocking a 9.65% CAGR through 2031. Craft breweries that swapped diatomaceous-earth filters for ceramic crossflow cut batch filtration from six hours to 90 minutes and eliminated hazardous filter-aid waste, confirming payback under three years. Whey-protein and plant-protein isolators leverage ceramics’ 95°C wash resilience to ensure allergen-clean surfaces. On balance, nutrient extraction and beverage clarification will push the ceramic membrane market past USD 3 billion in F&B revenue alone by 2031, closing the gap with municipal demand.

Geography Analysis

Asia-Pacific held 52.98% of 2025 revenue and will grow at 10.02% CAGR through 2031 on synchronized infrastructure build-outs, stricter discharge limits, and localized manufacturing. China’s 14th Five-Year Plan earmarked CNY 180 billion for industrial wastewater upgrades, and domestic suppliers such as JIUWU now quote 30% below imports. India’s Jal Jeevan Mission specs ceramics for 60% of village plants, raising the ceramic membrane market’s addressable volume across South Asia. Japan, South Korea, and Taiwan fund high-reuse industrial parks, further cementing regional dominance.

North America’s 2025 market share was lifted by Clean Water Act compliance, Indigenous water-system funding, and shale-gas produced-water recycling. Milwaukee, Newark, and Flint pilot ceramic plants to remove particulate lead, potentially opening a USD 900 million municipal retrofit pool by 2028. Canada’s CAD 1.9 billion remote-community program likewise favors ceramics thanks to freeze-thaw durability. Mexico’s Bajío industrial corridor added 14 ceramic wastewater plants in 2025, cementing a continental manufacturing-hub trend.

Europe’s 2025 market value was impacted by regulatory momentum trumping budget headwinds. Germany subsidizes Baltic runoff nutrient removal, the UK funds AMP8 phosphorus cuts, and the Netherlands fast-tracks PVDF swap-outs. Southern Europe lags on capex, but high-salinity niches still pull in ceramic bids. Latin America and Middle East-Africa together form a 7% sliver, yet billion-dollar desalination retrofits in Saudi Arabia and UAE telegraph high-growth pockets inside the global ceramic membrane market.

Competitive Landscape

The ceramic membranes market is moderately concentrated. Strategic activity centers on vertical integration and advanced coatings. GEA bought 30% of Atech Innovations in 2024 to secure glass-ceramic formulations that cut costs by 20%. Patent filings climbed to 47 in 2025 at the European Patent Office, half focusing on anti-fouling surface layers. Start-ups such as Mantle pilot 3D-printed gradient-porosity membranes that boost flux 40%, although costs remain double conventional sintering. Procurement now insists on ISO 19749 and ASTM D6908 compliance, favoring incumbents with in-house test rigs and shortening the addressable window for unverified newcomers.

Ceramic Membranes Industry Leaders

JIUWU HI-TECH

LiqTech Holding A/S

Pall Corporation

Saint-Gobain

Veolia

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: LiqTech announced a joint venture with Jiangsu JiTRI Marine Equipment Co., Ltd. to develop silicon-carbide membrane water-treatment systems for Chinese maritime applications.

- February 2025: LiqTech International received supplier approval for its silicon-carbide membrane water-treatment system for WinGD dual-fuel engines, enabling 80–95% water reuse rates in emission-control systems.

Global Ceramic Membranes Market Report Scope

Ceramic membranes, as inorganic filters, excel in liquid filtration. Their robust nature renders them highly efficient, especially in scenarios requiring resistance to harsh chemicals like acids and potent solvents.

The ceramic membranes market is segmented by material type, end-user industry, and geography. By material type, the market is segmented into alumina, silica, titania, zirconium oxide, silicon carbide, and others (glassy materials, magnesia, carbon, and glass-ceramic composites). By end-user industry, the market is segmented into water and wastewater treatment, food and beverage, chemical industry, pharmaceutical, and other end-user industries (biotechnology, textile, and petrochemical). The report also covers the market size and forecasts for the ceramic membrane market for 27 major countries. For each segment, the market sizing and forecasts are done in terms of value (USD).

| Alumina |

| Silica |

| Titania |

| Zirconium Oxide |

| Silicon Carbide |

| Others (Glassy Materials, Magnesia, carbon, Glass-Ceramic composites, etc.) |

| Water and Wastewater Treatment |

| Food and Beverage |

| Chemical Industry |

| Pharmaceutical |

| Others (Biotechnology, Textile, Petrochemical, etc.) |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Malaysia | |

| Thailand | |

| Indonesia | |

| Vietnam | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| NORDIC Countries | |

| Turkey | |

| Russia | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| Qatar | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| South Africa | |

| Rest of Middle-East and Africa |

| By Material Type | Alumina | |

| Silica | ||

| Titania | ||

| Zirconium Oxide | ||

| Silicon Carbide | ||

| Others (Glassy Materials, Magnesia, carbon, Glass-Ceramic composites, etc.) | ||

| By End-user Industry | Water and Wastewater Treatment | |

| Food and Beverage | ||

| Chemical Industry | ||

| Pharmaceutical | ||

| Others (Biotechnology, Textile, Petrochemical, etc.) | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| Malaysia | ||

| Thailand | ||

| Indonesia | ||

| Vietnam | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| NORDIC Countries | ||

| Turkey | ||

| Russia | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| Qatar | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

How fast is the ceramic membranes market expected to grow between 2026 and 2031?

The market is projected to rise from USD 9.62 billion in 2026 to USD 14.68 billion in 2031, reflecting an 8.78% CAGR driven by regulatory mandates and infrastructure upgrades.

Which region contributes the largest revenue to ceramic filtration solutions?

Asia-Pacific held 52.98% of 2025 revenue and is on track for the fastest 10.02% CAGR, supported by industrial growth and extensive municipal water investments.

What material currently leads commercial adoption in filtration modules?

Alumina-based elements maintain 44.12% share thanks to mature manufacturing economics and versatile performance across municipal and industrial duties.

Why are food and beverage processors accelerating ceramic membrane purchases?

Ceramic microfiltration withstands hot cleaning and sustains high protein-rejection rates, enabling efficient whey processing and cold-pasteurization without compromising product safety.

Which companies are making notable strategic moves in this space?

Saint-Gobain pushes silicon-carbide technology for oil-produced water, LiqTech targets marine and industrial reuse with flat-sheet designs, and NGK partners with MHI for bioethanol dehydration systems.

Page last updated on: