Liquid Applied Membrane Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

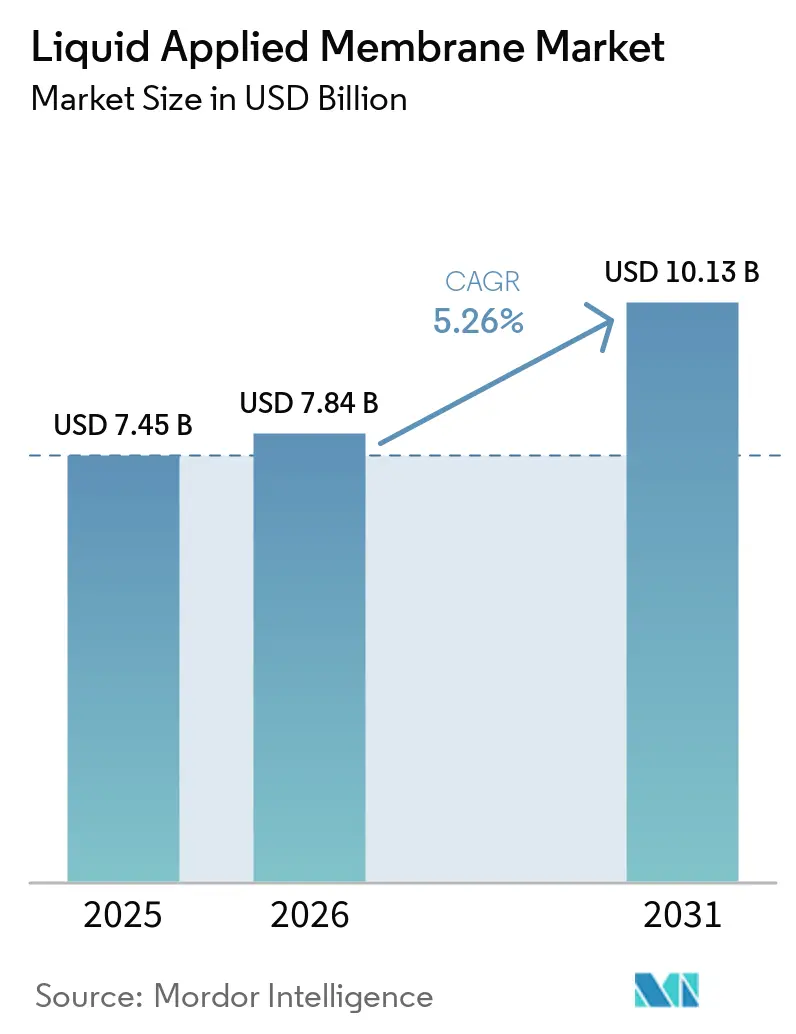

| Market Size (2026) | USD 7.84 Billion |

| Market Size (2031) | USD 10.13 Billion |

| Growth Rate (2026 - 2031) | 5.26% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Liquid Applied Membrane Market Analysis by Mordor Intelligence

The Liquid Applied Membrane Market size is projected to expand from USD 7.45 billion in 2025 and USD 7.84 billion in 2026 to USD 10.13 billion by 2031, registering a CAGR of 5.26% between 2026 to 2031. Seamless spray technologies are displacing prefabricated sheets because they eliminate lapped joints, accommodate complex details, and speed installation. Asia-Pacific dominates current demand and exhibits the fastest expansion as governments fund rail, road, and housing megaprojects worth USD 1.7 trillion per year. Polyurethane systems gain traction on job sites that value rapid cure and high elongation, while acrylic dispersions grow in regions tightening volatile organic compound limits. Roofing renovations in North America and Europe, photovoltaic-ready designs in Germany and Japan, and balcony codes in dense Asian cities all lift recurring re-coating cycles and sustain steady volume growth.

Key Report Takeaways

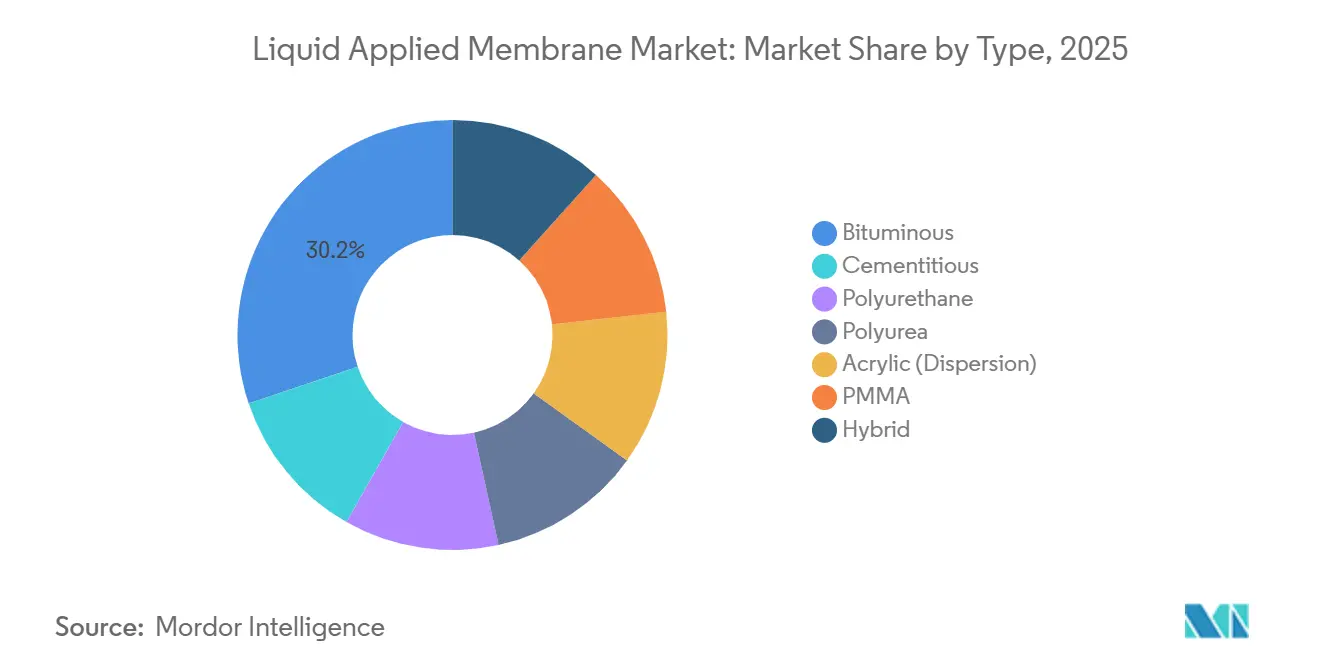

- By type, bituminous membranes retained 30.16% of the Liquid Applied Membrane market share in 2025; polyurethane systems are advancing at a 6.31% CAGR through 2031.

- By application, roofing captured 36.12% of the Liquid Applied Membrane market size in 2025 and is projected to post a 6.84% CAGR through 2031.

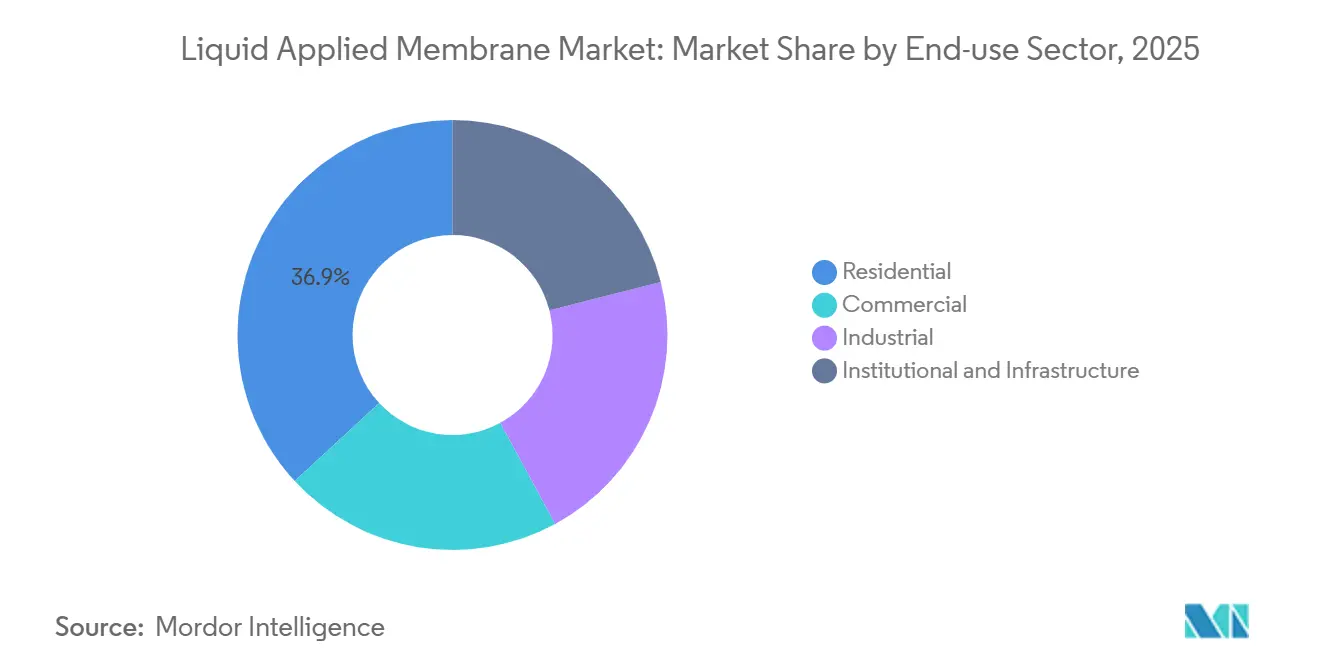

- By end-use sector, residential construction held 36.89% revenue share in 2025 and is growing at 6.25% CAGR to 2031.

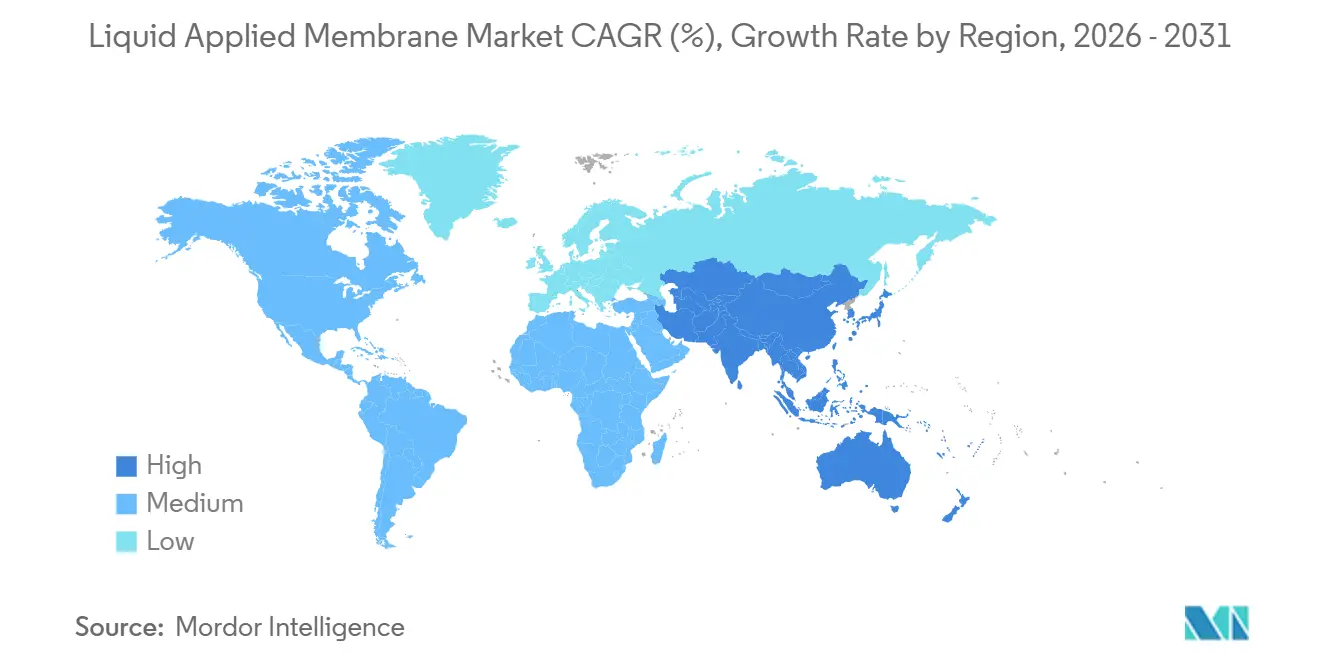

- By geography, Asia-Pacific commanded 53.22% of 2025 global revenue and is expected to expand at a 6.92% CAGR during the forecast period (2026-2031), the fastest regional growth rate.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Liquid Applied Membrane Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Infrastructure boom in Asia-Pacific and Africa | +1.80% | Asia-Pacific core, spill-over to Middle East and Africa | Long term (≥ 4 years) |

| Cost-effective retro-fitting for ageing roofs in mature economies | +0.90% | North America and Europe, selective uptake in Japan and Australia | Medium term (2-4 years) |

| Regulations mandating VOC-free solutions | +1.20% | North America and Europe immediate, expanding to ASEAN and Latin America | Medium term (2-4 years) |

| Rapid adoption of PV-ready liquid roof skins | +1.00% | Global, with early gains in Germany, California, Japan, and South Korea | Medium term (2-4 years) |

| Emergence of self-healing micro-capsule chemistries | +0.60% | North America and Europe pilot projects, Asia-Pacific scale-up post-2028 | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Infrastructure Boom in Asia-Pacific and Africa

Asia-Pacific governments collectively channel about USD 1.7 trillion each year into rail hubs, elevated expressways, and mixed-use podiums, all of which mandate robust waterproofing[1]Asian Development Bank, “Meeting Asia’s Infrastructure Needs,” adb.org. China alone recorded 6.8% construction output growth in 2025, fueling basement and parking-deck demand where sheets cannot negotiate penetrations. India added 7.2% residential growth in 2025 under affordable-housing schemes that prefer spray cementitious membranes priced 30% below imported polyurethane. African nations face a USD 100 billion annual infrastructure gap, so bituminous emulsions that tolerate high temperatures and require minimal surface prep remain attractive. Supply tightness surfaced in late 2025 when Southeast Asian lead times for polyurethane stretched to 12 weeks, forcing contractors to switch to acrylics with lower elongation.

Regulations Mandating VOC-Free Solutions

The 2024 United States Architectural and Industrial Maintenance (AIM) Rule capped volatile organic content in architectural coatings at 50 g/l, effectively eliminating solvent-borne mastics. Europe already restricts limits to 30 g/l and enforces job-site inspections that fine non-compliance up to EUR 50,000. California’s 2025 amendments tightened roof-coating thresholds to 25 g/l, accelerating the adoption of moisture-cure polyurethane. Reformulation expenses are significant; one major supplier spent USD 18 million to convert its roofing line, yet recouped costs by pricing water-based systems 15% higher. Thailand’s draft rule mirrors the European Union (EU) limits, signaling a converging global baseline.

Rapid Adoption of PV-Ready Liquid Roof Skins

Building-integrated solar capacity doubled between 2023 and 2025 to 45 GW as designers favored membranes that avoid fastener penetrations[2]International Energy Agency, “PVPS Annual Report 2025,” iea.org. Germany now mandates solar-ready roofs on new commercial structures over 1,000 m², specifying peel adhesion above 2 N/mm⁻¹. A leading supplier launched a polyurethane membrane in 2025 that secured 12 million m² of European logistics roofs within nine months. Japan updated waterproofing standards to require UV reflectance above 0.80, steering projects toward white acrylic elastomers that lower module temperatures by up to 10°C. Comparative cost analysis shows spray polyurethane and coating at USD 22 m² versus USD 31 m² for adhered TPO (Thermoplastic Polyolefin), with faster solar installation readiness.

Emergence of Self-Healing Micro-Capsule Chemistries

A 2025 peer-reviewed study showed polyurethane membranes loaded with 5 wt% isocyanate-filled capsules sealed 200 µm (micrometer) cracks within 48 hours and regained 92% tensile strength. A multinational chemical company filed three patents covering encapsulation that prevents premature polymerization, using melamine-formaldehyde shells. Field trials on 50,000 m² of Dutch roofs extended service life by five years and cut lifecycle cost by 28% at a 5% discount rate. Capsule additives add USD 3-5/kg, lifting installed prices up to 25%, so early adoption concentrates in data centers and pharma plants where downtime penalties outweigh premiums. Only two global capsule suppliers hold meaningful capacity, creating a bottleneck until Asian producers scale after 2027.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Availability of sheet and prefabricated membranes | -0.70% | Global, most acute in North America where TPO and EPDM systems dominate commercial roofing | Short term (≤ 2 years) |

| Volatile petro-chemical feedstock prices | -0.90% | Global, acute in Asia-Pacific and Middle East due to supply-chain dependencies | Short term (≤ 2 years) |

| Incoming micro-plastic restrictions on polymer additives | -0.50% | Europe immediate, North America and ASEAN by 2027-2028, rest of world post-2029 | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatile Petro-Chemical Feedstock Prices

Brent crude fluctuated between USD 65 and USD 95/bbl (barrel) in 2025, swinging MDI (Methylene Diphenyl Diisocyanate) and polyol spot prices 25-30% quarterly and compressing polyurethane gross margins from 28% to 19%. European bitumen hit EUR 520/t when Russian vacuum-residue exports tightened, a 35% premium to Middle Eastern supply. Acrylic monomer costs spiked 18% after a Texas cracker outage, prompting formulation changes that sacrificed 10% elongation but preserved price competitiveness. Contractors now lock six-month forward contracts, transferring risk to distributors that absorbed USD 40 million losses in 2025. Large multinationals hedge with annual agreements capped at 8% escalation, whereas small fabricators remain exposed.

Incoming Micro-Plastic Restrictions on Polymer Additives

The REACH Annex XVII rule phases out particles less than 5 mm in coatings by 2027, banning many slip-resistance beads. Mineral substitutes increase viscosity 15-20% and add up to EUR 1.20/kg in cost. One leading supplier spent EUR 12 million and 18 months to reformulate 40 SKUs but gained first-mover advantage by securing German occupational approval nine months ahead of peers. California added polymer microbeads to its candidate list in 2025, and ASEAN proposed a harmonized threshold, signaling 30% of global construction will bar non-compliant products by 2028. Mineral-filled membranes show 8-12% lower elongation, so seismic regions now demand ASTM C836 testing before approval.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Polyurethane Outpaces Legacy Bitumen

Bituminous systems captured 30.16% of the Liquid Applied Membrane market share in 2025 due to low installed costs of USD 8-12 m². Polyurethane leads growth at 6.31% CAGR during the forecast period (2026-2031), driven by a two-hour cure that halves project schedules and by same-day return-to-service requirements in retail reroofs. Polyurea serves tunnels where 10-second gel times resist 15-bar water pressure, though brittleness at low temperatures restricts use in cold climates. Acrylic dispersions gain acceptance where regulators cap VOCs (Volatile Organic Compounds); exposed roofs in sun-belt states specify white acrylic for superior UV stability.

Cementitious coatings are favored in Middle East housing because they cost USD 4-6 m² and tolerate rough substrates. PMMA (Poly(methyl methacrylate)) is concentrated in Europe, where chemistries provide 400% elongation and 25-year warranties at premium prices. Hybrid blends combine polyurethane with polyurea or modified bitumen to balance cost and performance, exemplified by a leading hybrid that delivers 300% elongation at half the pure-polyurea cost. Overall, polyurethane’s momentum positions it to edge bitumen down to some share by 2031 as regulations and labor economics favor fast-cure, one-coat systems.

By Application: Roofing Dominates, Underground Gains Traction

Roofing represented 36.12% of the Liquid Applied Membrane market size in 2025 and is projected to advance at a 6.84% CAGR during the forecast period (2026-2031), fastest among uses, as 42% of the United States' commercial roofs date before 1980 and require periodic re-coating. Spray polyurethane foam adds R-value and waterproofs in a single layer, cutting energy bills and avoiding tear-offs. Underground and tunnel linings' share will grow due to projects such as China opened 680 km of subways in 2025, each lined with polyurea membranes rated for 15 bar pressure.

Wall and façade applications' market share is driven by below-grade foundations in flood-prone regions and wind-driven rain protection on coastal envelopes. Other niches, such as balconies, podiums, potable tanks, and planters, collectively are rising steadily as building codes tighten water ingress limits. Roofing may slip marginally by 2031 as underground projects increase, yet it remains the premier battleground where suppliers bundle membranes with solar-mount warranties.

By End-Use Sector: Residential Leads, Institutional Accelerates

Residential building consumed 36.89% of global volume in 2025 and will progress at a 6.25% CAGR during the forecast period (2026-2031) because the Asia-Pacific region added 58 million urban residents during the year. Affordable-housing programs in India specify low-cost cementitious or acrylic membranes, whereas luxury towers in China and Singapore pay premiums for polyurethane that supports rooftop amenities.

Commercial facilities with logistics roofs prefer, and retail centers select liquid systems when numerous penetrations raise sheet-membrane labor by 40-60%. Institutional and infrastructure end-uses are expected to register fast growth as governments refurbish bridges and parking decks; fast-cure polyurethane allows lane reopening within four hours, saving USD 50,000 per lane-km per day in congested corridors. Industrial plants prefer low-odor water-based membranes to avoid production shutdowns.

Geography Analysis

Asia-Pacific commanded 53.22% of 2025 revenue and will grow at a 6.92% CAGR. China posted CNY 31.8 trillion (USD 4.4 trillion) construction output and consumed 42 million m² of balcony and terrace membranes. India’s 7.2% residential expansion and Japan’s seismic-resilient waterproofing code changes both accelerate polyurethane uptake. South Korea’s Green Remodeling retrofit program applied spray-foam and elastomeric coatings to 180,000 homes, reflecting regional enthusiasm for energy-efficient envelopes. ASEAN markets grew 8.1% in 2025 under rail and expressway investment, pushing polyurea tunnel demand.

In North America, the United States' reroofing cycles and federal infrastructure funds consumed a significant volume of membranes in 2025. Canada’s provincial flood-mitigation codes lifted polyurethane by 11% year-on-year. Mexico’s near-shoring boom drove 22% growth in logistics roofing along the border. Regional CAGR moderates as prefab systems with factory-applied waterproofing rise.

Europe's market share will expand on the Renovation Wave that targets 35 million building upgrades by 2030. Germany’s solar-ready roof mandate generated 28% membrane growth in 2025, while the United Kingdom Building Safety Act requires third-party waterproofing certification, favoring suppliers with long-standing British Board of Agrément (BBA) approvals. Southern Europe grows above average as hospitality and balcony retrofits specify acrylic and cementitious coatings.

In South America, Brazil led the regional volume where residential activity rose 5.8%. Argentina contracted slightly, yet luxury projects still import PMMA for differentiation. Regional CAGR is substantial as World Bank loans support infrastructure. Middle East and Africa's 2025 market share was lifted by Saudi and the United Arab Emirates (UAE) megaprojects that together used a significant volume of membranes. African affordable-housing programs prefer cementitious emulsions priced under USD 10 m².

Competitive Landscape

The Liquid Applied Membrane market is highly fragmented. Technology leadership differentiates players. Compliance with ISO 9001 and regional approvals lets global brands charge 30-40% premiums in institutional tenders. Furthermore, competitive pressure will intensify as European firms absorb microplastic reformulation costs and Asian resin makers scale up. Mergers and acquisitions (M&A) activity is likely between 2027-2029 as incumbents seek feedstock security and geographic reach.

Liquid Applied Membrane Industry Leaders

Sika AG

Carlisle Companies Incorporated

GAF Materials LLC

SOPREMA Group

BASF

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: Siplast, Inc. introduced TeraPROOF, a portfolio of high-performance below-grade waterproofing solutions aimed at protecting commercial structures from water intrusion. The product line included pre-applied membranes, post-applied systems, and liquid membranes, strengthening the company’s position as a comprehensive building enclosure provider.

- May 2025: GCP Applied Technologies’ Integritank liquid-applied membrane system was selected for the 1 km Coatzacoalcos immersed-tube tunnel in Mexico.

Global Liquid Applied Membrane Market Report Scope

Liquid-applied membrane (LAM) is a monolithic, fully bonded, liquid-based coating suitable for many waterproofing and roofing applications. Liquid membranes combine the properties of adhesive sheet membranes while adding significant technological advancements by creating an instant-setting coating. They combine the elastic properties of new-generation polymers with the waterproof characteristics of highly emulsified asphalt.

The Liquid Applied Membrane market is segmented by type, application, end-use sector, and geography. The market is segmented by type into cementitious, bituminous, polyurethane, polyurea, acrylic (dispersion), PMMA, and hybrid (polyurethane/polyurea (PU/PUA), modified polyurethane-bituminous, and more). The market is segmented by application into roofing, walls, underground and tunnels, and other applications (floors, balconies, walkways, podiums, tanks, potable water tanks, planter boxes, and more). By end-use sector, the market is segmented into residential, commercial, industrial, and institutional and infrastructure. The report also covers the market size and forecasts for the Liquid Applied Membrane market in 16 countries across major regions. Each segment's market sizing and forecasts are based on revenue (USD).

| Cementitious |

| Bituminous |

| Polyurethane |

| Polyurea |

| Acrylic (Dispersion) |

| PMMA |

| Hybrid (polyurethane/polyurea (PU/PUA), modified polyurethane-bituminous, etc.) |

| Roofing |

| Walls |

| Underground and Tunnels |

| Other Applications (Floors, Balconies, Walkways, Podiums, Tanks, Potable Water Tanks, Planter Boxes, etc.) |

| Residential |

| Commercial |

| Industrial |

| Institutional and Infrastructure |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Russia | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Type | Cementitious | |

| Bituminous | ||

| Polyurethane | ||

| Polyurea | ||

| Acrylic (Dispersion) | ||

| PMMA | ||

| Hybrid (polyurethane/polyurea (PU/PUA), modified polyurethane-bituminous, etc.) | ||

| By Application | Roofing | |

| Walls | ||

| Underground and Tunnels | ||

| Other Applications (Floors, Balconies, Walkways, Podiums, Tanks, Potable Water Tanks, Planter Boxes, etc.) | ||

| By End-use Sector | Residential | |

| Commercial | ||

| Industrial | ||

| Institutional and Infrastructure | ||

| Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Russia | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the projected global value of the liquid applied membrane market in 2031?

The liquid applied membrane market is forecast to reach USD 10.13 billion by 2031.

Which chemistry is expected to grow fastest through 2031?

Polyurethane systems are projected to post a 6.31% CAGR, the highest among all chemistries.

Why are liquid membranes preferred for photovoltaic-ready roofs?

They create seamless substrates that avoid fastener penetrations, speeding solar installation and preserving warranties.

Which region holds the largest market share today?

Asia-Pacific accounted for 53.22% of global revenue in 2025 and will keep leading through 2031.

How will microplastic regulations affect product formulations?

Suppliers must replace polymer beads with mineral fillers, increasing viscosity and costing up to EUR 1.20/kg while slightly reducing elongation performance.

Page last updated on: