Medical Transcription Software Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

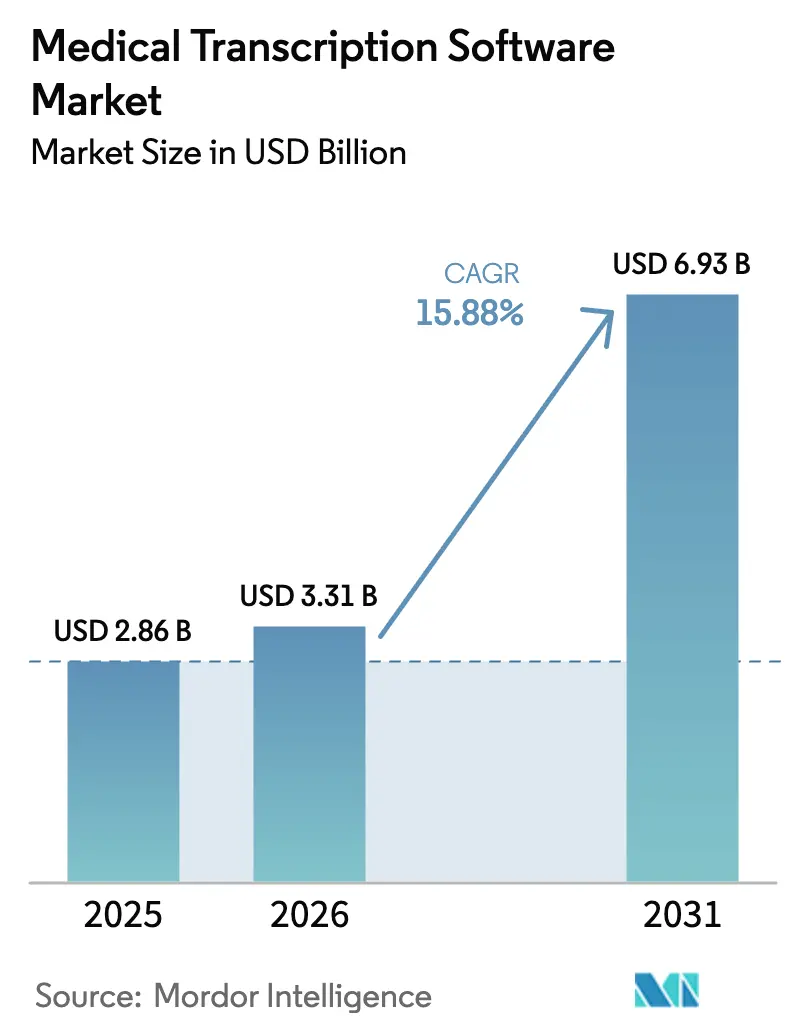

| Market Size (2026) | USD 3.31 Billion |

| Market Size (2031) | USD 6.93 Billion |

| Growth Rate (2026 - 2031) | 15.88% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Medical Transcription Software Market Analysis by Mordor Intelligence

The medical transcription software market size is expected to grow from USD 2.86 billion in 2025 to USD 3.31 billion in 2026 and is forecast to reach USD 6.93 billion by 2031 at 15.88% CAGR over 2026-2031. Broad adoption is tied to ambient clinical intelligence, electronic health record (EHR) integration mandates, and clinician-burnout mitigation initiatives. Hospitals are deploying AI-powered dictation that cuts documentation time by as much as 50%, while cloud deployment gains favor as a lower-overhead alternative to on-premise builds. Front-end speech recognition remains the primary interface during patient encounters, yet integrated voice solutions embedded in EHRs now record the fastest CAGR. Regionally, North America provides the deepest installed base, whereas Asia-Pacific drives incremental demand amid government-backed digitization programs.

Key Report Takeaways

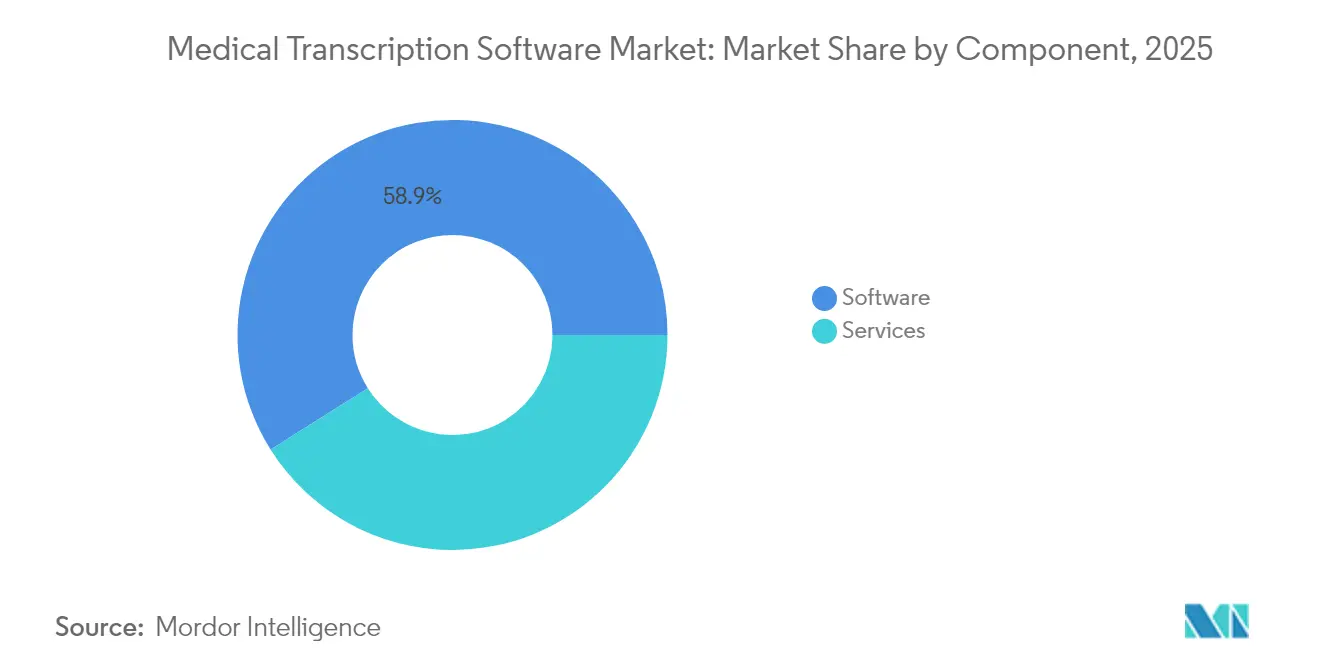

- By component, software held 58.94% of the medical transcription software market share in 2025, while services are forecast to expand at a 17.12% CAGR to 2031.

- By deployment mode, cloud-based models captured 56.62% revenue share in 2025; the segment leads growth at 17.25% CAGR.

- By end user, hospitals commanded 48.35% of the medical transcription software market size in 2025, whereas diagnostic laboratories advance at an 17.74% CAGR through 2031.

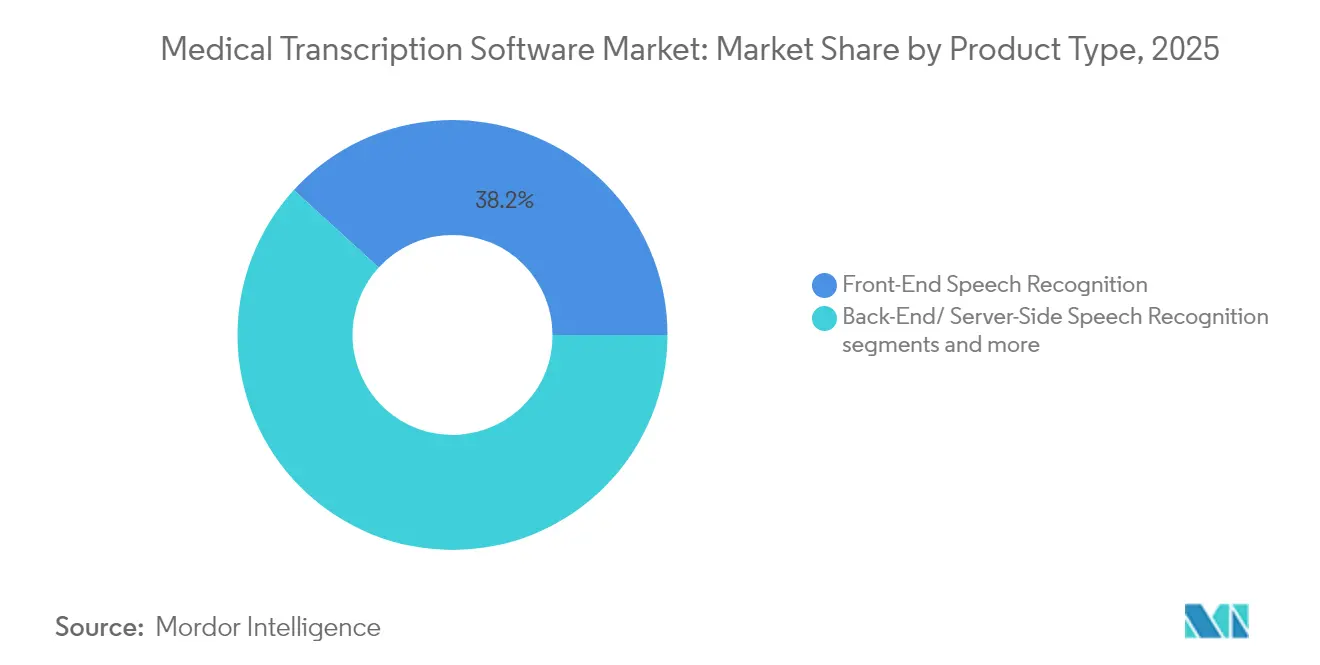

- By type, front-end speech recognition led with 38.21% market share in 2025; integrated EHR voice recognition is projected to climb at an 17.98% CAGR.

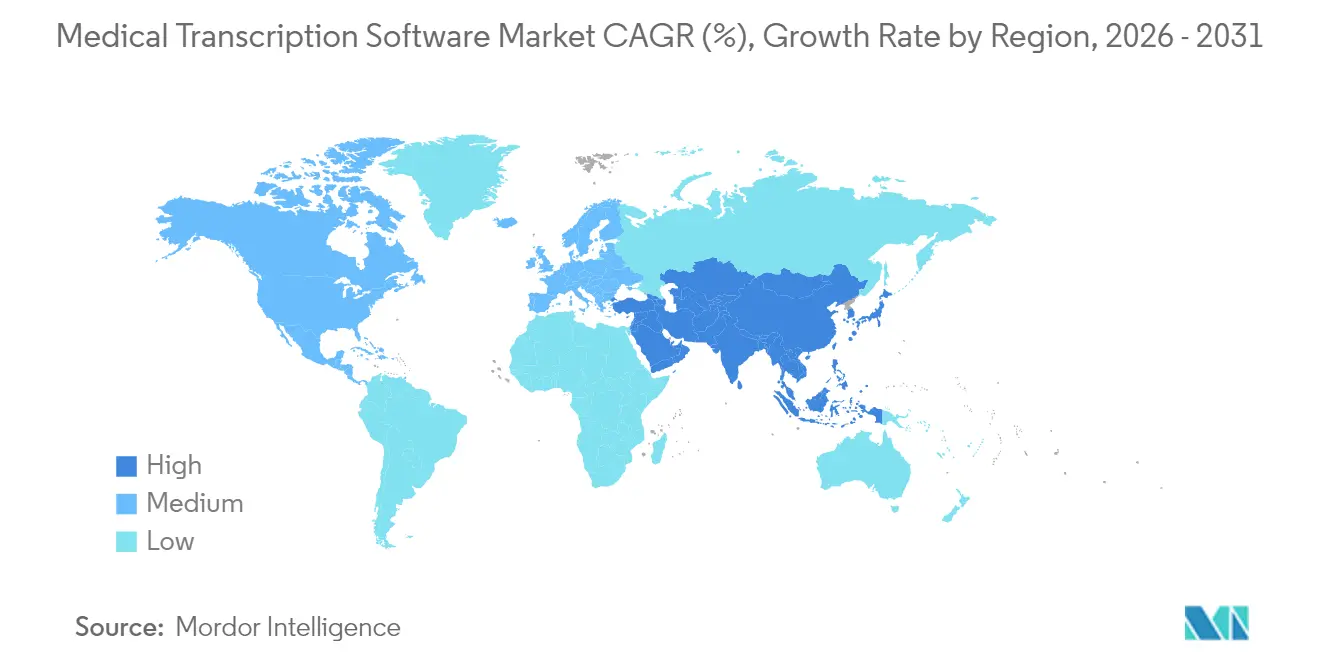

- Geographically, North America retained 40.76% share in 2025, while Asia-Pacific is set to post the swiftest growth at 18.22% CAGR

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Medical Transcription Software Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising adoption of EHR-integrated speech recognition solutions | +4.2% | Global, with North America & Europe leading | Medium term (2-4 years) |

| Need to reduce clinician documentation burden | +3.8% | Global, particularly acute in developed markets | Short term (≤ 2 years) |

| Growing outsourcing to cost-efficient AI transcription vendors | +2.9% | Global, with APAC emerging as key service hub | Medium term (2-4 years) |

| Ambient Clinical Intelligence (ACI) deployment in exam rooms | +3.1% | North America & EU, expanding to APAC | Long term (≥ 4 years) |

| Specialty-specific NLP for non-English medical vocabulary | +1.8% | APAC core, spill-over to MEA and Latin America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Adoption of EHR-Integrated Speech Recognition Solutions

EHR vendors now bundle voice tools directly into clinical workflows, with Nuance present in nearly 80% of purchasing shortlists due to its Epic alliance. Dragon Ambient eXperience (DAX) Copilot automatically drafts notes during visits and routes them into the chart in seconds. Tight linkage avoids documentation silos, accelerates reimbursement cycles, and raises switching costs—advantages that strengthen incumbents while posing entry barriers to new vendors.

Need to Reduce Clinician Documentation Burden

Physicians devote roughly two hours to documentation for every hour spent with patients, propelling adoption of AI transcription that lowers clerical load and lifts morale. Kaiser Permanente reports 65-70% uptake among physicians when voice AI is fully embedded. Patient satisfaction also rises—93% of respondents notice a more engaged encounter when doctors use conversational AI assistants. These outcomes shift transcription from optional utility to workforce-retention imperative

Growing Outsourcing to Cost-Efficient AI Transcription Vendors

Health systems increasingly contract specialized partners that combine speech recognition with medical editors, freeing internal teams for higher-value tasks. Outsourcing mitigates capital expense and accelerates deployment while delivering competitive accuracy levels. APAC service hubs supply multilingual capability, positioning the region as a preferred location for follow-the-sun transcription workflows.

Ambient Clinical Intelligence (ACI) Deployment in Exam Rooms

Ambient recorders capture natural conversation without interrupting eye contact, then use NLP to render structured notes. NextGen Ambient Assist claims 2 hours daily time savings per provider. Augmedix processes more than 3 million encounters annually, illustrating scalability. As hardware requirements shrink to a microphone and secure cloud connection, deployment friction falls and clinical adoption broadens.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data-privacy & HIPAA compliance concerns | -2.1% | Global, with stricter enforcement in EU & North America | Short term (≤ 2 years) |

| High upfront cost for small practices | -1.8% | Global, particularly acute in rural and developing markets | Medium term (2-4 years) |

| Clinician liability fears from AI "hallucinations" | -1.4% | Global, with heightened concerns in litigious markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Data-Privacy & HIPAA Compliance Concerns

Cross-border data transfer raises scrutiny under HIPAA and GDPR, stretching procurement cycles as providers demand rigorous security audits and business associate agreements. Vendor preference often tilts to on-premise or sovereign-cloud deployments despite higher costs, giving an edge to suppliers with certified environments and seasoned legal teams.

High Upfront Cost for Small Practices

Only 21% of critical-access hospitals possess robust EHR capability because of capital and staffing constraints[1]Source: Agency for Healthcare Research and Quality, “Health IT in Small and Rural Communities,” ahrq.gov . Total cost of ownership encompasses software, microphones, networking, and staff training—a burden that pushes many rural clinics to remain manual or seek shared-service cooperatives.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Segment Accelerates Despite Software Dominance

Software platforms form the backbone of the medical transcription software market, representing 58.94% revenue in 2025 and anchoring clinical documentation across 600,000 clinicians worldwide. Continuous upgrades in natural-language processing and ambient note generation keep software indispensable. Parallelly, the services segment is projected to grow 17.12% annually as health systems externalize non-core documentation to specialized providers offering round-the-clock editing support. These providers surf the same AI wave by layering human review atop speech recognition, delivering accuracy that matches regulatory thresholds.

Service contracts increasingly bundle performance guarantees and compliance clauses, making them attractive for institutions lacking in-house transcription oversight. Cost predictability, scalability, and quick onboarding reinforce momentum. In response, software-only vendors are embedding auto-quality-assurance functions to retain accounts that might otherwise migrate to managed services. The interplay ensures both components advance—and collectively expand the medical transcription software market

By Deployment Mode: Cloud Solutions Drive Market Transformation

Cloud architectures captured 56.62% of the medical transcription software market share in 2025, underpinned by subscription models that trade capital expenditure for operating cost. Elastic scaling accommodates fluctuating encounter volumes and simplifies feature rollout. On-premise deployments persist in institutions with strict data-sovereignty policies, yet growth lags at single-digit rates.

From a financial lens, pay-as-you-go billing aligns with value-based-care economics, spurring adoption among midsize hospitals. Cyber-resilience also improves: hyperscale clouds meet or exceed HITRUST and ISO 27001 standards, alleviating board-level security concerns. Nevertheless, EU providers sometimes insist on regional data centers to satisfy GDPR, sustaining a niche for private-cloud vendors. Overall, cloud’s agility and lower entry cost consolidate its leadership within the medical transcription software market.

By End User: Diagnostic Laboratories Emerge as Growth Leaders

Hospitals continue to account for 48.35% of the medical transcription software market size in 2025 thanks to high patient volumes and reimbursement-linked documentation requirements. Yet diagnostic laboratories are forecast to advance 17.74% annually as genetic and pathology testing trigger surging narrative data. Automated speech-to-text shortens turnaround, feeding structured results directly into laboratory information systems.

Physician offices and clinics, especially in rural regions, display growing appetite for subscription-based tools that sidestep heavy IT lifts. Academic centers leverage voice AI for trial documentation, further broadening penetration. Collectively, diverse end-user requirements propel ongoing enrichment of vocabularies and workflow integrations across the medical transcription software marke

By Type: Integrated EHR Solutions Gain Momentum

Front-end speech recognition delivered the largest slice—38.21%—of 2025 revenue, acting as the clinician’s main dictation workstation. Integrated voice recognition with EHRs, however, is slated for the highest 17.98% CAGR as health systems opt for seamless, click-free charting. Deep coupling with order sets, problem lists, and billing codes minimizes toggling and creates a single source of truth.

Back-end server transcription serves high-volume batch needs such as radiology. Service-based transcription retains relevance for organizations seeking turnkey accuracy with minimal internal oversight. The type segmentation underscores a migration from siloed dictation toward fully embedded conversational AI—an evolution that underpins future expansion of the medical transcription software market.

Geography Analysis

North America led with 40.76% share in 2025 amid mature EHR adoption, Meaningful Use incentives, and escalating clinician-wellness programs. Enterprise rollouts at Intermountain Health and Community Health Network illustrate scale benefits as DAX Copilot permeates multispecialty workflows. Canada follows similar patterns, although procurement lengthens due to provincial privacy reviews. Mexico’s public-hospital modernization is nascent, restraining near-term spending.

Asia-Pacific will record the fastest 18.22% CAGR through 2031 as China, India, and Japan inject funds into national digital-health blueprints. NEC’s generative-AI EHR pilot evidences Japan’s appetite for speech-enabled documentation. India accelerates via Ayushman Bharat Digital Mission incentives, while Southeast Asian providers adopt cloud transcription to leapfrog legacy IT. Skill shortages, however, spotlight the need for managed services and multilingual language models.

Europe sustains steady growth as GDPR renders security a frontline differentiator. Germany and France favor local hosting, prompting US suppliers to establish in-region data centers. The United Kingdom’s NHS continues voice-enrichment pilots tied to clinical-safety approvals. Southern European markets, burdened by fiscal austerity, trail in penetration but present upside as EU recovery funding targets digital-health upgrades.

South America and the Middle East & Africa account for smaller slices yet show rising demand in private hospital chains. Multinational insurers expanding value-based-care programs create incremental impetus. Infrastructure gaps and economic volatility temper near-term scale, but regulatory convergence with international standards gradually lowers market-entry hurdles, thereby enlarging the addressable base for the medical transcription software market.

Competitive Landscape

Microsoft’s acquisition of Nuance elevated the combined firm to market leadership, with Dragon Medical platforms reaching more than 600,000 clinicians. Moderate concentration prevails as legacy suppliers such as 3M and Dolbey compete against nimble disruptors Abridge, Suki, and DeepScribe that emphasize physician-centric design and subscription pricing. Ambient intelligence is the battleground: Microsoft’s Dragon Copilot integrates dictation and passive listening, claiming 70% burnout reduction.

Meanwhile, Commure and Athelas jointly acquired Augmedix in 2025, forming a portfolio that processes 3 million appointments annually[2]Source: Commure, “Commure and Athelas sign deal to acquire Augmedix,” commure.com . White-space opportunities lie in specialty vocabularies and regional languages, areas where local firms partner with academic linguists for proprietary datasets. Vendors also differentiate via HIPAA-grade encryption, synthetic-voice anonymization, and real-time quality alerts to mitigate AI hallucination risk. Pricing shifts toward encounter-based fees tightened to value-based metrics, reshaping revenue models across the medical transcription software market.

Medical Transcription Software Industry Leaders

Microsoft Corporation (Nuance Communications, Inc.)

3M Company

NextGen Healthcare

iMedX

Augmedix

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Microsoft launched Dragon Copilot, merging dictation with ambient listening; deployed across 600 health systems

- February 2025: Commure & Athelas agreed to acquire Augmedix, creating the largest AI documentation software provider

Global Medical Transcription Software Market Report Scope

As per the scope of the report, medical transcription software is tailored to convert voice-recorded medical reports into precise and formatted text documents, ensuring smooth documentation of patient information. The software offers numerous advantages, including enhanced efficiency, reduced manual errors, and the guarantee of timely and accurate medical record documentation. Medical transcription software transforms digital voice recordings into text for medical professionals. This software uses speech recognition and natural language processing (NLP) technologies to convert speech to text and store the recorded dictations.

The medical transcription software market is segmented by deployment mode, technology, end user, application, and geography. By deployment mode, the market is segmented into cloud-based and on-premises. By technology, the market is segmented into speech recognition and natural language processing (NLP). By end user, the market is segmented into hospitals/clinics, diagnostic centers, and other end users. By application, the market is segmented into clinical documentation, radiology reports, surgical reports, and pathology reports. By geography, the market is segmented into North America, Europe, Asia-Pacific, Middle East and Africa, and South America. The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The market provides the value (USD) for the above-mentioned segments.

| Software |

| Services |

| Cloud-based |

| On-Premise |

| Hospitals |

| Clinics & Physician Offices |

| Diagnostic Laboratories |

| Academic & Research Institutes |

| Others |

| Front-End Speech Recognition |

| Back-End / Server-Side Speech Recognition |

| Integrated Voice Recognition with EHR |

| Service-Based Medical Transcription |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa |

| By Component (Value) | Software | |

| Services | ||

| By Deployment Mode (Value) | Cloud-based | |

| On-Premise | ||

| By End User (Value) | Hospitals | |

| Clinics & Physician Offices | ||

| Diagnostic Laboratories | ||

| Academic & Research Institutes | ||

| Others | ||

| By Type (Value) | Front-End Speech Recognition | |

| Back-End / Server-Side Speech Recognition | ||

| Integrated Voice Recognition with EHR | ||

| Service-Based Medical Transcription | ||

| By Geography (Value) | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How big is the Medical Transcription Software Market?

The Medical Transcription Software Market size is expected to reach USD 3.31 billion in 2026 and grow at a CAGR of 15.88% to reach USD 6.93 billion by 2031.

Which component leads the Medical Transcription Software Market?

Software platforms hold the largest 58.94% share, although services are expanding faster at 17.12% CAGR.

Why are cloud deployments growing faster than on-premise models?

Cloud solutions reduce upfront capital outlays, scale elastically, and offer accredited security postures that simplify compliance.

Which region is expected to grow the quickest through 2031?

Asia-Pacific is projected to advance at an 18.22% CAGR thanks to government-backed digitization programs and multilingual AI demand.

Page last updated on: