Medical Transcription Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

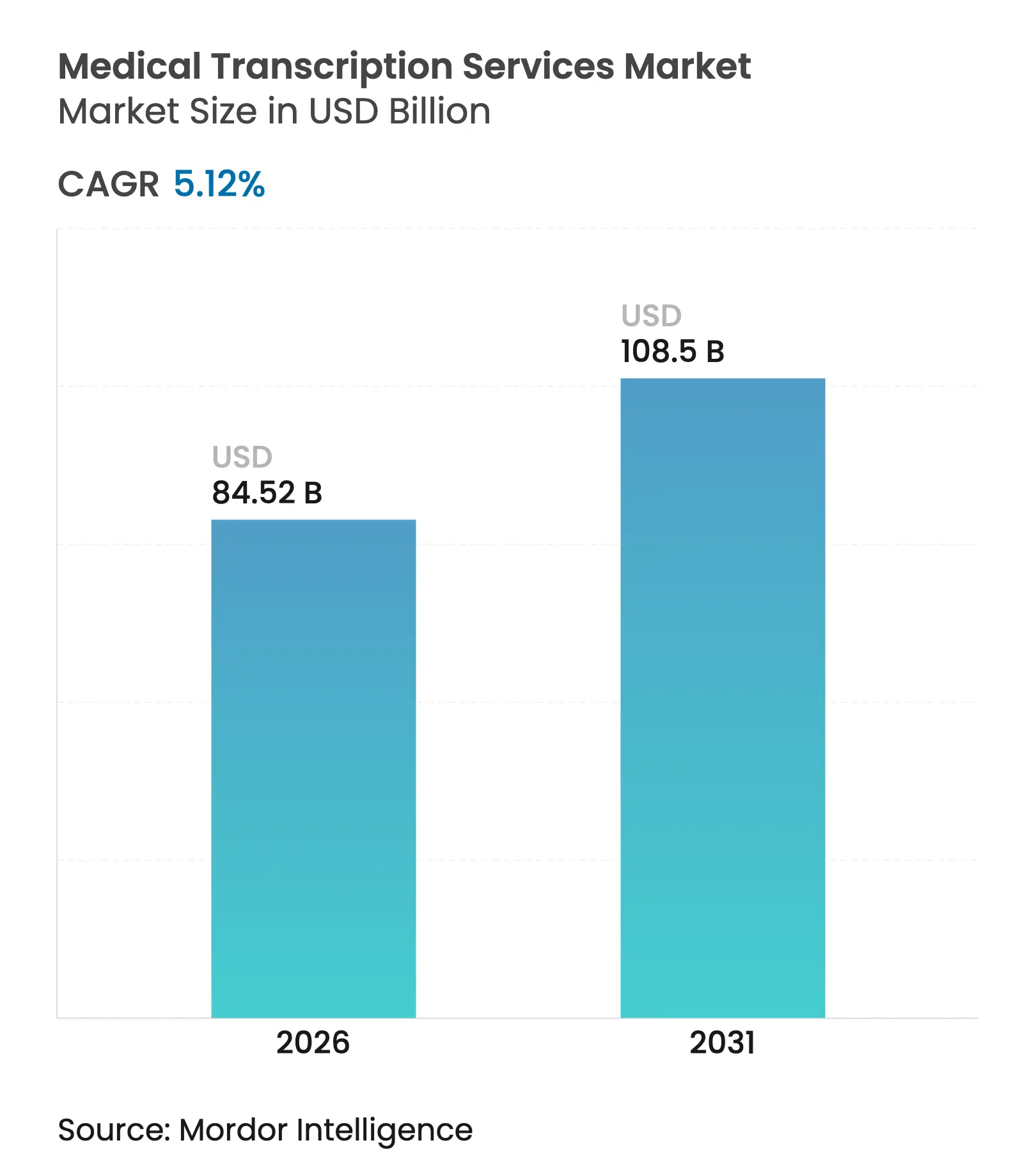

| Market Size (2026) | USD 84.52 Billion |

| Market Size (2031) | USD 108.5 Billion |

| Growth Rate (2026 - 2031) | 5.12 % CAGR |

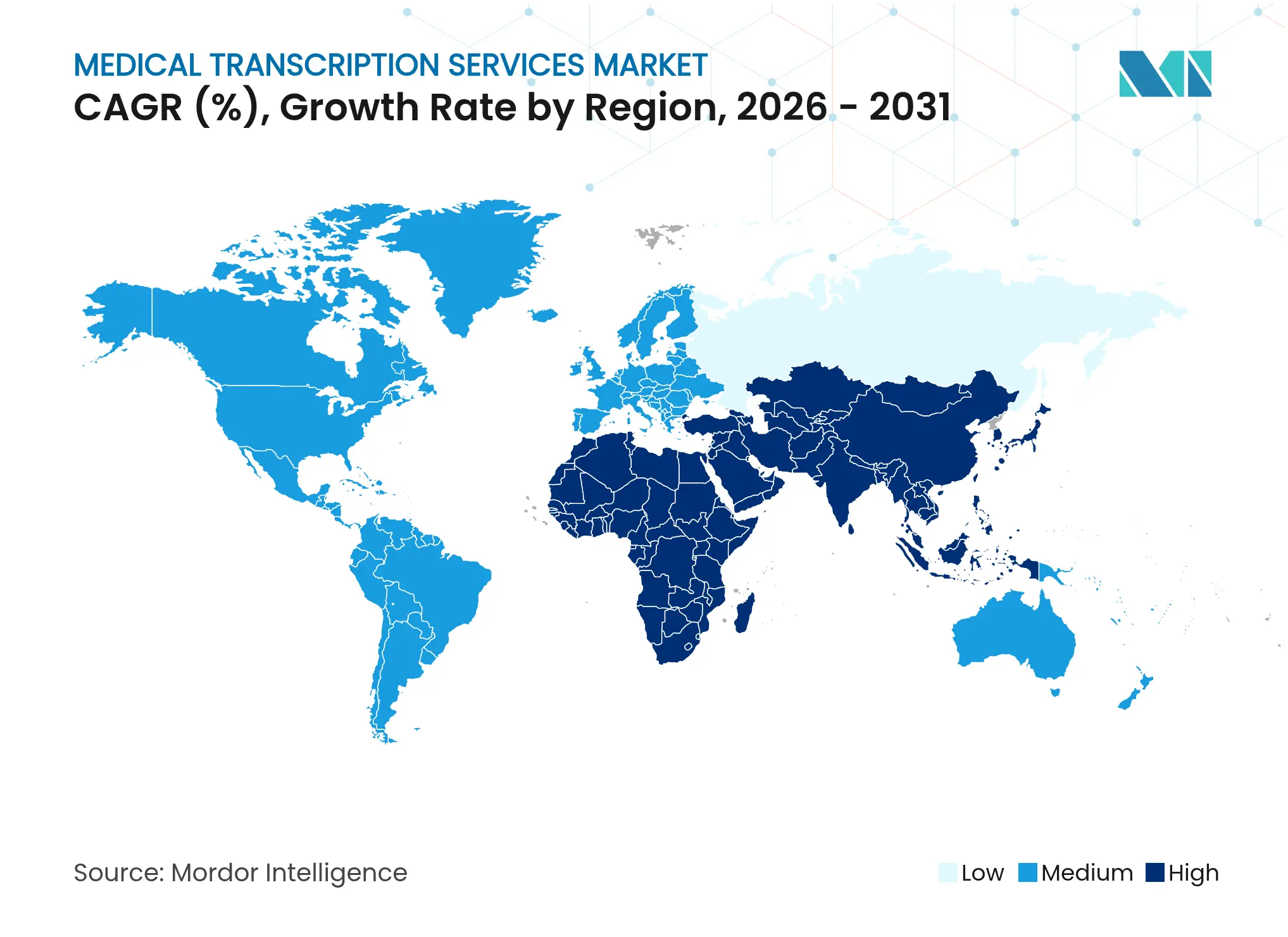

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

Medical Transcription Services Market Analysis by Mordor Intelligence

The medical transcription services market size is expected to grow from USD 80.41 billion in 2025 to USD 84.52 billion in 2026 and is forecast to reach USD 108.5 billion by 2031 at 5.12% CAGR over 2026-2031. Growth is propelled by mandatory electronic health record (EHR) interoperability, rapid uptake of ambient clinical intelligence (ACI) platforms, and heightened pressure to standardize documentation across telehealth and multi-state practices. Hospitals and physician groups are scaling AI-enabled tools that trim documentation time, while outsourcing and hybrid procurement provide cost relief amid staffing shortages. Asia Pacific is rising quickly on the strength of healthcare digitization programs and favorable labor economics, even as North America retains a commanding lead on technology adoption and regulatory momentum. Data-privacy incidents continue to expose vulnerabilities, driving demand for secure, HIPAA-compliant transcription workflows.

Key Report Takeaways

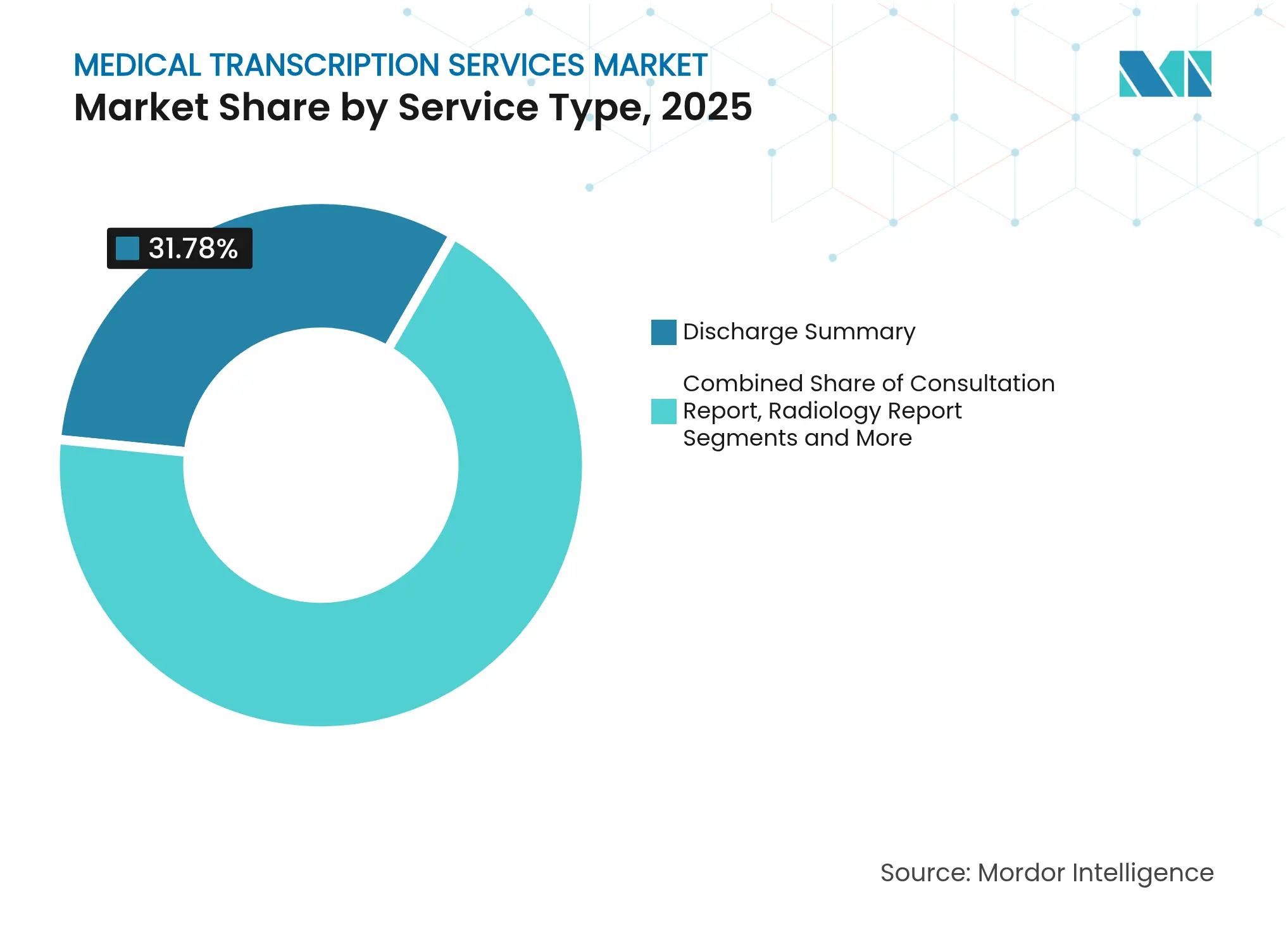

- By service type, discharge summaries led with 31.78% of the medical transcription services market share in 2025; radiology reports are forecast to expand at a 8.62% CAGR to 2031.

- By technology, EMR/EHR systems held 44.02% revenue share in 2025, while ACI platforms are advancing at an 8.1% CAGR through 2031.

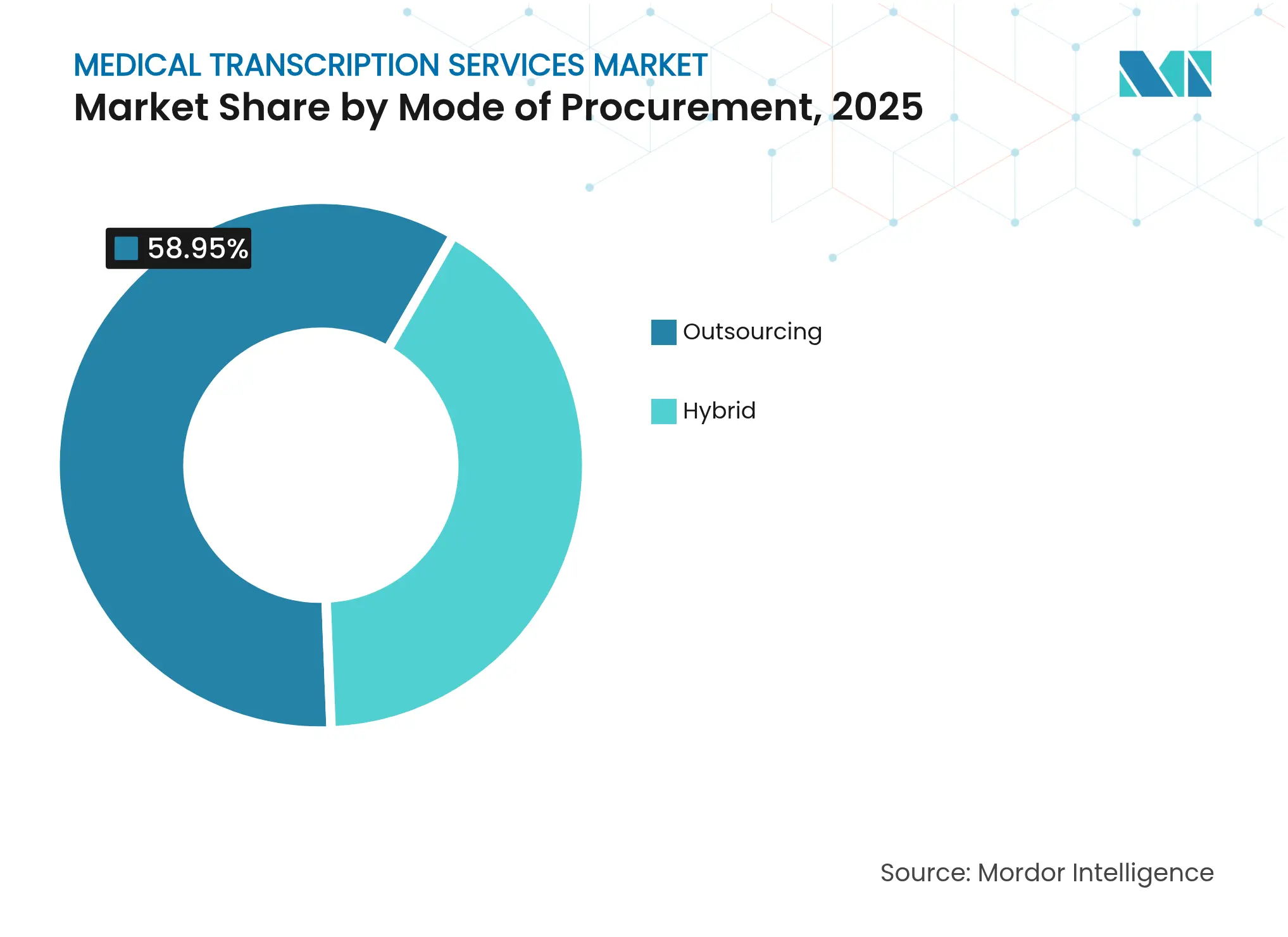

- By mode of procurement, outsourcing accounted for 58.95% of the medical transcription services market size in 2025; hybrid models are projected to grow at 9.05% CAGR between 2026-2031.

- By end-user, hospitals captured 45.78% of the medical transcription services market share in 2025, whereas physician groups register the fastest CAGR at 7.78% through 2031.

- By geography, North America commanded 41.05% share of the medical transcription services market in 2025 and Asia Pacific is progressing at 6.95% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Medical Transcription Services Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

EHR & interoperability mandates

accelerating digital documentation

EHR & interoperability mandates

accelerating digital documentation

| +1.2% | Global, early gains in North America and EU | Medium term (2-4 years) | (~) % Impact on CAGR Forecast:

+1.2%

|

Geographic Relevance

:

Global, early gains in North America

and EU

|

Impact Timeline

:

Medium term (2-4 years)

|

Cost-containment pressures driving

outsourcing to low-cost vendors

Cost-containment pressures driving

outsourcing to low-cost vendors

| +0.8% | Global, spill-over to core APAC markets | Short term (≤ 2 years) | |||

Reimbursement incentives for

accurate clinical documentation

Reimbursement incentives for

accurate clinical documentation

| +0.9% | North America & EU | Medium term (2-4 years) | |||

Ambient clinical intelligence

platforms shortening TAT

Ambient clinical intelligence

platforms shortening TAT

| +1.5% | Global, concentration in North America | Short term (≤ 2 years) | |||

Telehealth expansion creating

multi-state documentation demand

Telehealth expansion creating

multi-state documentation demand

| +0.7% | North America, expanding to Europe | Medium term (2-4 years) | |||

Specialty-specific template

libraries boosting accuracy & compliance

Specialty-specific template

libraries boosting accuracy & compliance

| +0.6% | Global | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

EHR & Interoperability Mandates Accelerating Digital Documentation

The December 2023 HTI-1 Final Rule obliges U.S. providers to adopt USCDI v3 by January 2026, forcing transcription vendors to align with new data-element standards while enabling certified API publish requirements by December 2024 healthit.gov. European systems face analogous pressure under the European Health Data Space, where tighter governance reduced research data permits by 46.9% in 2023 biomedcentral.com. Demand for interoperable, standards-ready documentation is lifting the medical transcription services market as providers rush to update systems without disrupting clinical throughput.

Cost-Containment Pressures Driving Outsourcing to Low-Cost Vendors

Sixty-three percent of U.S. hospitals now outsource transcription amid annual documentation opportunity costs estimated at USD 90-140 billion, spurring adoption of offshore models that lower unit costs while retaining onshore oversight fortherecordmag.com. Rapid shifts toward hybrid outsourcing are reshaping vendor selection criteria, rewarding firms that demonstrate HIPAA compliance and robust quality assurance.

Reimbursement Incentives for Accurate Clinical Documentation

The 2025 Medicare Physician Fee Schedule introduces new caregiver-training codes and telehealth allowances that hinge on granular documentation, reinforcing demand for error-free transcripts cms.gov. Although average payment rates decline 2.93%, providers can recoup revenue by meeting quality metrics, intensifying reliance on precise specialty templates across the medical transcription services market.

Ambient Clinical Intelligence Platforms Shortening TAT

Nuance’s DAX Copilot became generally available in January 2024, embedding GPT-4 within Epic workflows and halving documentation time while cutting clinician burnout 70% nuance.com. Early deployments across 3,442 physicians saved an hour per day per user, illustrating how ACI accelerates turnaround times and unlocks capacity across the medical transcription services market.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Data-privacy & cybersecurity

liabilities (HIPAA, GDPR)

Data-privacy & cybersecurity

liabilities (HIPAA, GDPR)

| -0.9% | Global, concentration in North America & EU | Short term (≤ 2 years) | (~) % Impact on CAGR Forecast:

-0.9%

|

Geographic Relevance

:

Global, concentration in North

America & EU

|

Impact Timeline

:

Short term (≤ 2 years)

|

Rapid uptake of

speech-recognition/NLP curbing manual volumes

Rapid uptake of

speech-recognition/NLP curbing manual volumes

| -1.2% | Global | Medium term (2-4 years) | |||

Shrinking pool of certified medical

language specialists

Shrinking pool of certified medical

language specialists

| -0.7% | Global, acute in North America | Long term (≥ 4 years) | |||

Point-of-care mobile apps shifting

workload to clinicians

Point-of-care mobile apps shifting

workload to clinicians

| -0.5% | Global | Medium term (2-4 years) | |||

| Source: Mordor Intelligence | ||||||

Data-Privacy & Cybersecurity Liabilities (HIPAA, GDPR)

The February 2024 Change Healthcare cyberattack disrupted USD 1.5 trillion in annual transactions and exposed 85 million patient records, heightening scrutiny of transcription providers’ security posture healthaffairs.org. The EU AI Act adds parallel compliance layers, inflating implementation costs and slowing procurement cycles across the medical transcription services market.

Rapid Uptake of Speech-Recognition/NLP Curbing Manual Volumes

AI systems now flag 82.7% of radiology-report errors in 3.5 seconds at USD 0.03 per file, steadily displacing traditional manual transcription workloads rsna.org. Vendors must pivot toward hybrid human-in-the-loop offerings to remain relevant.

Segment Analysis

By Service Type: Discharge Summaries Anchor, Radiology Reports Accelerate

Discharge summaries generated the largest revenue slice, claiming 31.78% of the medical transcription services market in 2025, underpinned by stringent medication-reconciliation and follow-up documentation rules. The segment benefits from mandated hand-off protocols that favor comprehensive narrative records. Radiology reports, while smaller, register the quickest climb at 8.62% CAGR as AI error-detection drives image-report creation efficiency. GPT-4-enabled auditing reduces turnaround to seconds, signaling deeper integration of automated note generation into imaging workflows.

Continued demand for history-and-physical and operative notes underscores persistent reliance on expert medical language. Consultation reports grow with tele-consults that involve multi-specialty care plans. AI-generated ambient summaries are emerging, yet still require expert verification, sustaining service-provider relevance across the medical transcription services market.

Note: Segment shares of all individual segments available upon report purchase

By Technology: EMR/EHR Dominance, ACI Platforms Surge

EMR/EHR systems absorbed 44.02% revenue in 2025, reflecting their role as centralized documentation hubs. HTI-1 compliance timelines compel vendors to align transcript workflows with new interoperability standards, cementing EHR anchorage within the medical transcription services market size narrative. ACI platforms advance fastest at 8.1% CAGR, compressing clinician workload and fostering a shift from retrospective dictation to live note capture.

PACS and RIS platforms enable streamlined radiology pathways, while speech-recognition advancements elevate baseline accuracy for routine narratives. Blockchain-based encryption tools surface in the “Others” category, catering to rising cybersecurity expectations. Each technology cohort collectively broadens choice for providers balancing cost, speed, and compliance across the global medical transcription services market.

By Mode of Procurement: Outsourcing Prevails, Hybrid Gains Momentum

Outsourcing retained 58.95% share of the medical transcription services market size in 2025 as health systems outsourced labor-intensive workflows to offshore hubs with favorable wage structures. Quality concerns have eased with ISO-aligned audits and secure VPN integrations.

Hybrid models, growing 9.05% CAGR, blend offshore production with domestic QA teams that reassure clinicians on contextual accuracy and regulatory adherence. The arrangement leverages cost efficiencies while hedging geopolitical and compliance risk—an attractive proposition for mid-sized hospitals navigating budget ceilings within the medical transcription services market.

Note: Segment shares of all individual segments available upon report purchase

By End-User: Hospitals Lead, Physician Groups Accelerate

Hospitals controlled 45.78% share in 2025, owing to multi-department note volumes and continuous inpatient care cycles. Their reliance on comprehensive discharge and operative reports sustains high transcription throughput. Physician groups expand rapidly at 7.78% CAGR, spurred by swift adoption of ACI tools that integrate seamlessly with ambulatory EHR installs.

Clinics sustain moderate growth, benefiting from expanding primary-care rolls and telehealth visits that still require structured documentation. Diagnostic imaging centers enjoy an uplift as AI-verified radiology narratives win acceptance. Academic medical centers and emerging ambulatory surgery hubs populate the diverse tail end, enriching service-mix depth in the medical transcription services market.

Geography Analysis

North America retained 41.05% of global revenue in 2025, buoyed by structured regulatory pathways and ready capital for health-IT upgrades. HTI-1 deadlines accelerate EHR migration roadmaps, compelling vendors to embed USCDI v3 data elements directly within transcript outputs. High-profile pilots such as The Permanente Medical Group’s ACI roll-out validate ROI claims and spark broader adoption. Canada and Mexico contribute incremental growth via cross-border telehealth and modernization grants that prioritize secure documentation exchanges.

Asia Pacific is the swiftest riser with 6.95% CAGR projected through 2031. Health-system digitization in India and China, paired with robust English-speaking transcription talent, cements the region as both service exporter and domestic consumer. Government e-health schemes funnel investments toward cloud EHRs, anchoring sustained demand within the broader medical transcription services market.

Europe records stable progress under GDPR and imminent EU AI Act obligations that elongate vendor vetting cycles. Germany, the United Kingdom, and France drive most volume, embracing hybrid procurement that keeps sensitive data onshore while leveraging offshore cost advantages. Middle East & Africa and South America show nascent potential, with private-sector hospital networks piloting ACI and speech-to-text tools to leapfrog legacy dictation workflows.

Competitive Landscape

Market Concentration

Market concentration sits at a moderate level as incumbent technology firms and specialized service bureaus reshape portfolios around AI augmentation. Nuance, backed by Microsoft, leverages GPT-4 to automate note creation and underpins more than 550,000 physician users globally. Solventum, spun off from 3M in 2024 with USD 8.2 billion in sales, reallocates R&D toward integrated voice-enabled health-record modules. RadNet’s USD 54 million acquisition spree signals mounting convergence between imaging operations and tech-driven reporting platforms.

Strategic partnerships dominate: cloud hyperscalers furnish GPU-intensive language models, while niche vendors supply domain-taxonomy enrichment and QA services. Geographic expansion remains key; service providers open satellite QA centers in Ireland, the Philippines, and Colombia to diversify risk and enhance uptime. Investment flows into cybersecurity hardening, with blockchain-backed audit trails emerging as differentiators amid rising ransom-ware threats across the medical transcription services market.

New entrants harness ambient AI to court small practices that previously deemed formal transcription unaffordable. Meanwhile, established outsourcers retrofit workforces with ML-assisted editing consoles that cut post-dictation turnaround by double-digit percentages. Competitive intensity thus revolves around how quickly firms align human expertise with scalable automation without compromising accuracy or compliance.

Medical Transcription Services Industry Leaders

*Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Deepgram launched Nova-3 Medical, an AI speech-to-text model tailored to clinical audio, enabling developers to build secure voice applications.

- February 2025: IKS Health introduced Scribble Now, completing its real-time AI clinical documentation suite at ViVE 2025.

- February 2025: Augnito Omni reported surging NHS and private-provider uptake of its AI ambient scribe, citing customizable outputs and cost savings.

Table of Contents for Medical Transcription Services Industry Report

1. Introduction

- 1.1Study Assumptions and Market Definition

- 1.2Scope of the Study

2. Research Methodology

3. Executive Summary

4. Market Landscape

- 4.1Market Overview

- 4.2Market Drivers

- 4.2.1EHR & Interoperability Mandates Accelerating Digital Documentation

- 4.2.2Cost-Containment Pressures Driving Outsourcing To Low-Cost Vendors

- 4.2.3Reimbursement Incentives For Accurate Clinical Documentation

- 4.2.4Ambient Clinical Intelligence (ACI) Platforms Shortening TAT

- 4.2.5Telehealth Expansion Creating Multi-State Documentation Demand

- 4.2.6Specialty-Specific Template Libraries Boosting Accuracy & Compliance

- 4.3Market Restraints

- 4.3.1Data-Privacy & Cybersecurity Liabilities (HIPAA, GDPR)

- 4.3.2Rapid Uptake Of Speech-Recognition/NLP Curbing Manual Volumes

- 4.3.3Shrinking Pool Of Certified Medical Language Specialists

- 4.3.4Point-Of-Care Mobile Apps Shifting Workload To Clinicians

- 4.4Value / Supply-Chain Analysis

- 4.5Regulatory Landscape

- 4.6Technology Outlook

- 4.7Porter’s Five Forces Analysis

- 4.7.1Bargaining Power of Suppliers

- 4.7.2Bargaining Power of Buyers

- 4.7.3Threat of New Entrants

- 4.7.4Threat of Substitutes

- 4.7.5Intensity of Competitive Rivalry

5. Market Size and Growth Forecasts (Value-USD)

- 5.1By Service Type

- 5.1.1History & Physical Report

- 5.1.2Discharge Summary

- 5.1.3Operative Note / Report

- 5.1.4Consultation Report

- 5.1.5Radiology Report

- 5.1.6Others

- 5.2By Technology

- 5.2.1EMR / EHR

- 5.2.2Picture Archiving & Communication System (PACS)

- 5.2.3Radiology Information System (RIS)

- 5.2.4Speech-Recognition Technology

- 5.2.5Ambient Clinical Intelligence Platforms

- 5.2.6Others

- 5.3By Mode of Procurement

- 5.3.1Outsourcing

- 5.3.2Hybrid (On-shore + Off-shore)

- 5.4By End-User

- 5.4.1Hospitals

- 5.4.2Clinics

- 5.4.3Physician Groups

- 5.4.4Diagnostic & Imaging Centers

- 5.4.5Academic Medical Centers

- 5.4.6Others

- 5.5By Geography

- 5.5.1North America

- 5.5.1.1United States

- 5.5.1.2Canada

- 5.5.1.3Mexico

- 5.5.2Europe

- 5.5.2.1Germany

- 5.5.2.2United Kingdom

- 5.5.2.3France

- 5.5.2.4Italy

- 5.5.2.5Spain

- 5.5.2.6Rest of Europe

- 5.5.3Asia-Pacific

- 5.5.3.1China

- 5.5.3.2Japan

- 5.5.3.3India

- 5.5.3.4Australia

- 5.5.3.5South Korea

- 5.5.3.6Rest of Asia-Pacific

- 5.5.4Middle East and Africa

- 5.5.4.1GCC

- 5.5.4.2South Africa

- 5.5.4.3Rest of Middle East and Africa

- 5.5.5South America

- 5.5.5.1Brazil

- 5.5.5.2Argentina

- 5.5.5.3Rest of South America

6. Competitive Landscape

- 6.1Market Concentration

- 6.2Market Share Analysis

- 6.3Company profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.3.1Nuance Communications

- 6.3.2Solventum

- 6.3.3iMedX

- 6.3.4nThrive

- 6.3.5Athreon

- 6.3.6IKS Health

- 6.3.7Acusis

- 6.3.8Dolbey Systems

- 6.3.9Saince

- 6.3.10SpectraMedi

- 6.3.11EHR Transcriptions

- 6.3.12Transcend Services

- 6.3.13World Wide Dictation

- 6.3.14Medi-Script

- 6.3.15Med-scribe

- 6.3.16Epic Systems Corporation

- 6.3.17Global Healthcare Resource

- 6.3.18BayScribe

- 6.3.19Voicebrook

- 6.3.20Celerity Solutions

7. Market Opportunities & Future Outlook

- 7.1White-space & Unmet-Need Assessment

Global Medical Transcription Services Market Report Scope

As per the scope of the report, medical transcription services are an allied health profession dealing with transcribing voice-recorded medical reports dictated by physicians, nurses, and other healthcare practitioners.

The medical transcription services market is segmented by service type, technology, mode of procurement, end user, and geography. The service type segment is further divided into history & physical report, discharge summary, operative note or report, consultation report, and others. The technology type segment is further divided into electronic medical records/electronic health records, picture archiving and communication systems, radiology information systems, speech recognition technology, and others. The mode of procurement segment is further divided into outsourcing, offshoring, and both. By end user, the market is segmented into hospitals, clinics, clinical laboratories, academic medical centers, and others. The geography segment is further divided into North America, Europe, Asia-Pacific, Middle East and Africa, and South America.