Artificial Pancreas Device System Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

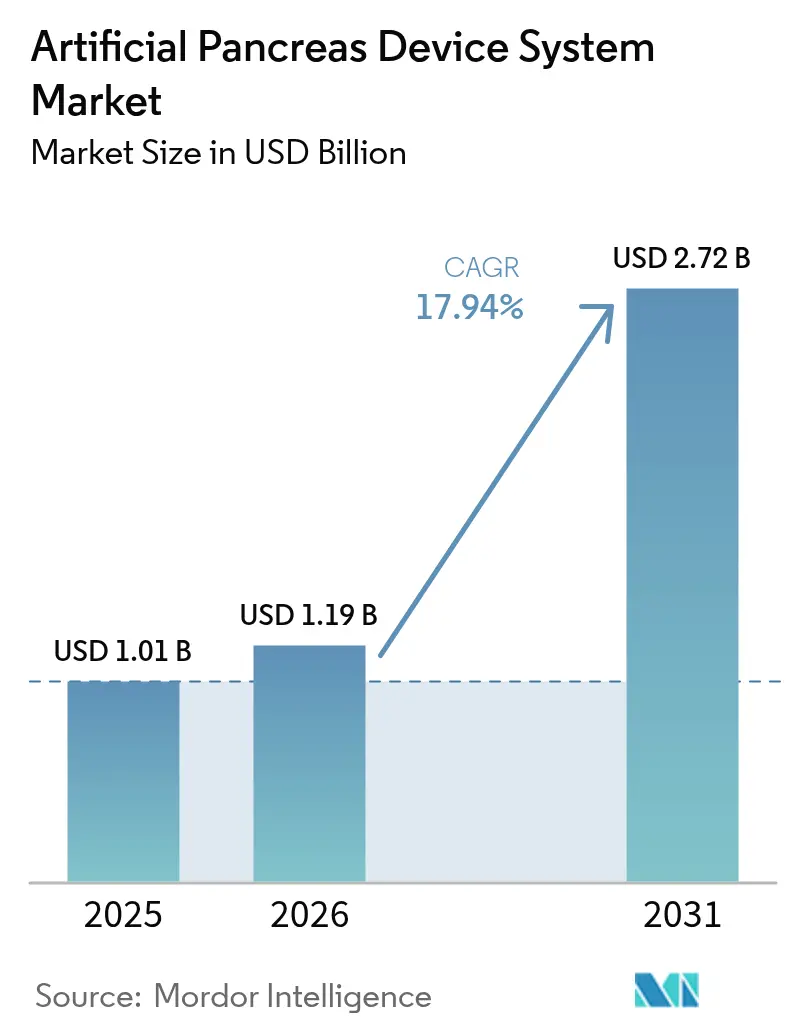

| Market Size (2026) | USD 1.19 Billion |

| Market Size (2031) | USD 2.72 Billion |

| Growth Rate (2026 - 2031) | 17.94% CAGR |

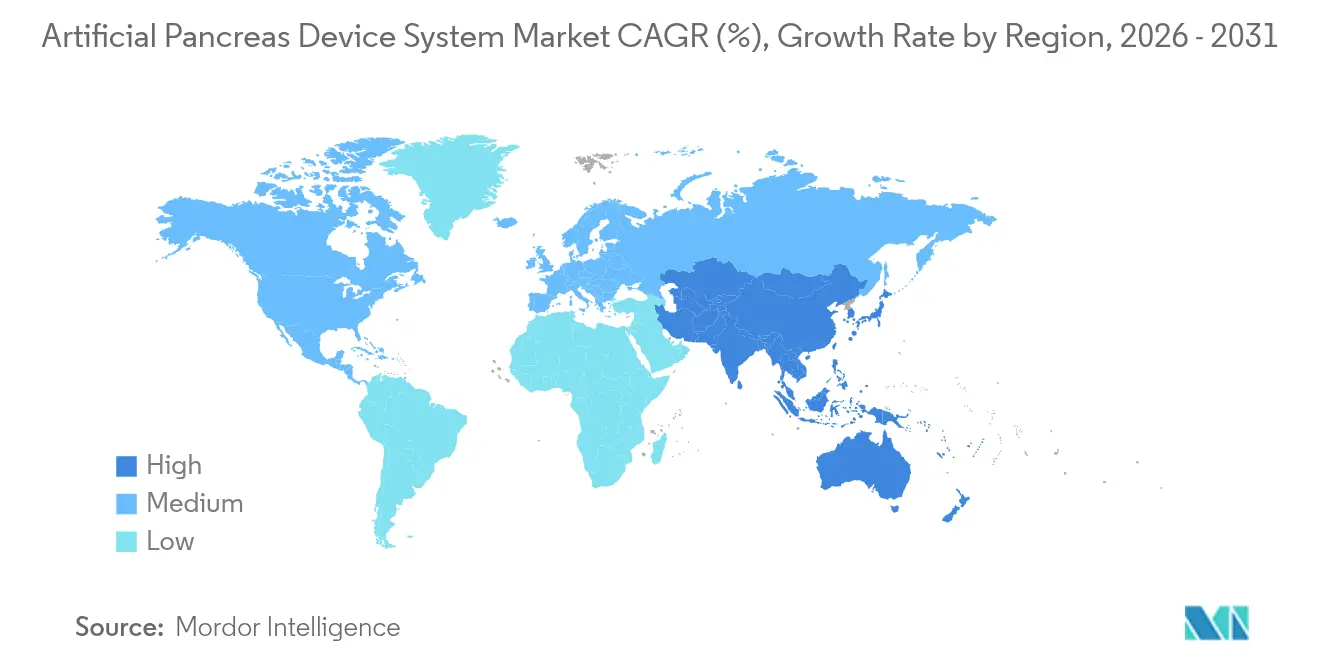

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Artificial Pancreas Device System Market Analysis by Mordor Intelligence

The artificial pancreas device system market size is expected to grow from USD 1.01 billion in 2025 to USD 1.19 billion in 2026 and is forecast to reach USD 2.72 billion by 2031 at 17.94% CAGR over 2026-2031. Demand is propelled by rising insulin-dependent diabetes prevalence, rapid gains in continuous glucose monitoring (CGM) accuracy, and the shift toward home-based connected chronic-care models that ease the burden of manual insulin dosing. Integrated automated insulin delivery (AID) platforms now combine CGM, insulin pumps, and AI-driven control algorithms, improving time-in-range outcomes while reducing hypoglycemia risk. Venture-capital inflows and strategic alliances between device makers and sensor specialists are accelerating product pipelines and expanding geographic reach. However, high total cost of ownership, uneven insurance coverage outside high-income countries, and cybersecurity concerns around cloud-connected devices temper adoption, especially in emerging economies.

Key Report Takeaways

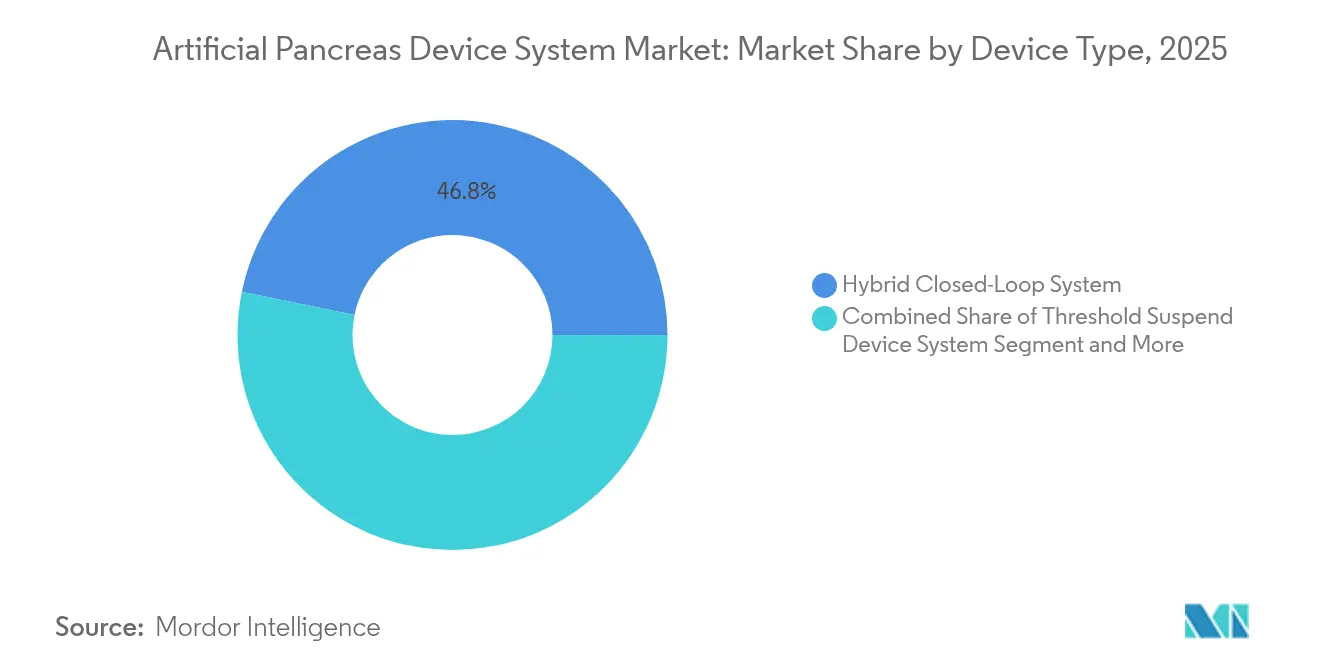

- By device type, Control-to-Target/Hybrid Closed-Loop platforms led with 46.78% revenue in 2025; Fully Automated Closed-Loop/Bionic Pancreas systems are projected to expand at a 23.85% CAGR through 2031.

- By component, insulin pumps held 49.92% of the artificial pancreas device system market share in 2025, while control algorithm/software is advancing at a 25.14% CAGR between 2026-2031.

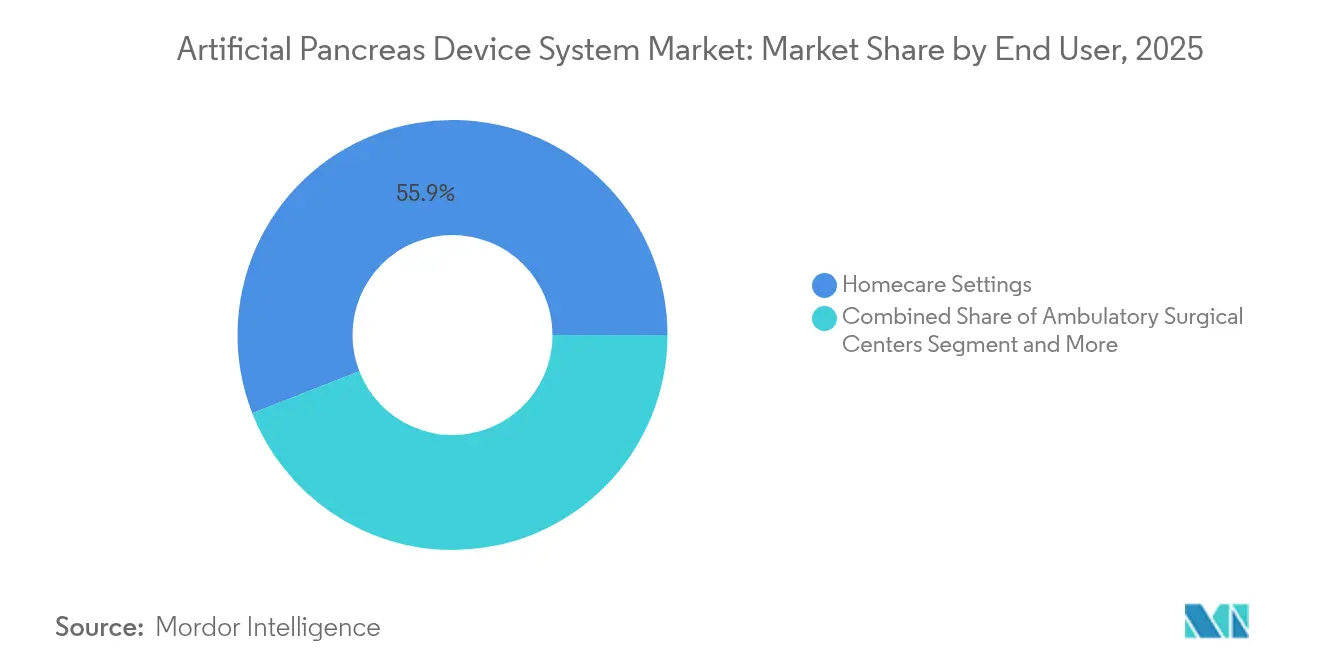

- By end user, homecare settings captured 55.92% of the artificial pancreas device system market size in 2025; ambulatory surgical centers are forecast to grow at 18.74% CAGR to 2031.

- By patient age, adults accounted for 70.10% share of the artificial pancreas device system market size in 2025 and the pediatric cohort is expanding at a 20.98% CAGR through 2031.

- By geography, North America dominated with 42.98% revenue in 2025; Asia-Pacific records the fastest regional CAGR at 18.88% during 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Artificial Pancreas Device System Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating Global Incidence of Insulin-Dependent Diabetes Requiring Automated Glycemic Control | +5.2% | Global, with higher impact in North America and Europe | Long term (≥ 4 years) |

| Accuracy & Wearability Advances in Continuous Glucose Monitoring Sensors | +4.8% | Global, with early adoption in North America and Europe | Medium term (2-4 years) |

| Shift Toward Home-Based, Connected Chronic Care Driving Adoption of Wearable AID Devices | +3.7% | North America, Europe, and urban centers in Asia-Pacific | Medium term (2-4 years) |

| Med-tech–Digital Health Convergence Enabling Integrated Artificial Pancreas Ecosystems | +3.1% | North America, Europe, and advanced healthcare markets in Asia-Pacific | Medium term (2-4 years) |

| Robust VC & Strategic Funding Fueling R&D and Commercial Scale-Up | +2.4% | Global, with concentration in North America | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Escalating Global Incidence of Insulin-Dependent Diabetes Requiring Automated Glycemic Control

Diabetes affects 422 million people worldwide and could reach 629 million by 2045, heightening demand for technology that eases daily insulin management. Healthcare systems seek cost-effective methods to curb complications, and artificial pancreas platforms improve time in target glucose range by 12.59% versus conventional pumps, lowering hospitalization risk. Insurers increasingly classify these systems as long-term cost savers despite high upfront prices, facilitating uptake across high-income markets and gradually in price-sensitive regions.

Accuracy & Wearability Advances in Continuous Glucose Monitoring Sensors

Smaller, more precise CGM sensors such as Dexcom G7 and Abbott’s dual-analyte devices extend wear duration and reduce calibration needs, strengthening the value proposition of artificial pancreas solutions. FDA approval of over-the-counter CGM in 2024 broadened access, while longer-wear sensors like Eversense 365 support a full-year implant cycle[1]Senseonics Holdings, “Eversense 365 Sensor Update,” senseonics.com. Improved comfort and reliability drive higher patient adherence, directly boosting automated insulin delivery performance.

Shift Toward Home-Based, Connected Chronic Care Driving Adoption of Wearable AID Devices

Homecare captures 56.5% of 2024 revenues as patients embrace self-management supported by telehealth monitoring. COVID-19 accelerated remote-care workflows, making cloud-linked artificial pancreas platforms mainstream in chronic disease programs. Pediatric users benefit from remote caregiver oversight, which reduces family stress and enhances adherence, encouraging faster adoption among children.

Med-Tech–Digital Health Convergence Enabling Integrated Artificial Pancreas Ecosystems

Partnerships that link CGM sensors, insulin pumps, and AI software create holistic ecosystems addressing exercise, sleep, and meal variability. Digital twin simulations developed at the University of Virginia personalize algorithm parameters, improving glycemic stability without extensive in-clinic testing. Converged platforms enhance user experience and data visibility for clinicians, driving competitive differentiation.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Total Cost of Ownership and Patchy Insurance Coverage in Emerging Economies | -3.6% | Global, with higher impact in emerging markets and developing economies | Medium term (2-4 years) |

| Cyber-Security, Data Privacy & Interoperability Risks in Connected AID Platforms | -2.1% | Global, with higher impact in regions with stringent data protection regulations | Medium term (2-4 years) |

| Limited Long-Term Real-World Evidence Across Diverse Patient Cohorts | -1.5% | Global, with higher impact in regions with conservative regulatory approaches | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Total Cost of Ownership and Patchy Insurance Coverage in Emerging Economies

Acquisition costs can exceed USD 7,000, with annual consumables adding thousands more, challenging affordability where reimbursement is limited[2]Centers for Medicare & Medicaid Services, “Glucose Monitor Policy,” cms.gov. Payer decisions vary by clinical evidence and budget impact, resulting in unequal access between insured and uninsured groups. In middle-income countries, public insurance rarely covers advanced diabetes tech, slowing artificial pancreas adoption despite large patient pools.

Cyber-Security, Data Privacy & Interoperability Risks in Connected AID Platforms

Smartphone-linked pumps and cloud analytics expand attack surfaces, raising concerns over unauthorized dose adjustments. Regulators now demand secure-by-design architectures, elongating approval timelines. GDPR requirements in Europe compel data-minimization features, while device-to-device incompatibilities can constrain user choice and integration into electronic health records, dampening perceived benefits.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Device Type: Hybrid Systems Dominate, Bionic Pancreas Accelerates

Hybrid closed-loop platforms generated 46.78% of 2025 revenue, serving as a transitional step toward full automation while preserving manual bolus discretion. They command much of today’s artificial pancreas device system market owing to clinician familiarity and incremental cost over legacy pumps. Fully automated/bionic solutions are projected to grow at 23.85% CAGR, fueled by AI-driven dual-hormone algorithms that deliver an 80% average time-in-range and markedly reduce hypoglycemia. Threshold-suspend and control-to-range models retain niche roles for users prioritizing simplicity or cost, but their share will decline as algorithmic sophistication becomes mainstream.

Second-generation bionic pancreases leverage neural-network-based pattern recognition to auto-adjust basal and bolus doses based on sensed metabolic trends, removing the need for carb counting in many scenarios. Manufacturers pair these systems with interoperable CGM to attract do-it-yourself (DIY) communities transitioning toward regulated products. Regulatory bodies now provide modular clearances for pumps and sensors, encouraging competitive mix-and-match ecosystems that expand patient choice within the artificial pancreas device system market.

By Component: Pumps Lead, Algorithms Surge

Insulin pumps represented 49.92% of 2025 component revenue and remain foundational to every deployment. Miniaturized tubeless formats such as Tandem Mobi enhance discretion, while smartphone-controlled models like Medtronic’s MiniMed 8-Series streamline daily routines. Algorithms/software exhibit the fastest 25.14% CAGR because deep-reinforcement learning enables highly personalized insulin titration, boosting median time-in-range to 87.45%. This growth underpins expanding demand for upgradable firmware licenses, a recurring-revenue layer inside the artificial pancreas device system market.

CGM sensors form the second-largest value pool, and upgrades to one-year implants reduce service burden. Disposable sets and sensor consumables provide steady annuity streams for manufacturers. Component-level interoperability designations from the FDA accelerate multi-vendor pairing, positioning software innovators to capture value without owning hardware.

By End User: Homecare Dominates, Ambulatory Centers Accelerate

Home settings held 55.92% revenue in 2025, reflecting consumer desire for autonomy and supportive reimbursement for remote monitoring. Telehealth integration lets clinicians titrate settings off-site, enhancing glycemic outcomes while cutting clinic visits. Ambulatory surgical centers will expand usage at 18.74% CAGR as perioperative protocols embed automated insulin delivery to stabilize glucose and avoid complications.

Hospitals remain vital for training and managing complex cases, and AI-assisted inpatient titration systems now rival senior endocrinologist performance, keeping mean glucose in range 76.4% of the time. Seamless transitions between care sites reduce glycemic variability during discharge, underscoring ecosystem value.

By Patient Age Group: Adults Predominate, Pediatrics Accelerate

Adults accounted for 70.10% of 2025 uptake because of higher disease prevalence and disposable income. Clinical trials confirm glycated hemoglobin improvements from 7.9% to 7.3% with bionic pancreas use, reinforcing clinician confidence. Pediatric demand, rising at 20.98% CAGR, benefits from caregiver desire for overnight safety and reduced regimen complexity; children aged 2-6 gained 2.8 extra hours in-range daily in University of Virginia studies.

Manufacturers design age-specific user interfaces and remote-monitoring dashboards, balancing independence for adolescents with parental oversight. As early adoption demonstrates lifelong complication reduction, payers are beginning to reimburse pediatric systems, widening artificial pancreas device system market penetration.

Geography Analysis

North America captured 42.98% revenue in 2025, leveraging high type 1 diabetes prevalence, broad private insurance coverage for AID, and an active VC ecosystem. FDA approval of over-the-counter CGM broadened candidate pools and lowered entry hurdles. Beta Bionics’ USD 206 million IPO in 2025 exemplified investor conviction and funded U.S. commercial scale-up.

Europe ranks second by revenue, backed by robust universal healthcare and supportive clinical guidelines. The U.K.’s National Health Service began national rollout of artificial pancreases in 2024, setting a cost-effectiveness precedent for other public payers. Data-privacy regulation spurs manufacturers to implement advanced cybersecurity, potentially offering European patients higher trust in connected ecosystems.

Asia-Pacific is the fastest-growing region at 18.88% CAGR through 2031. Urbanizing lifestyles have lifted regional diabetes incidence, and rising household income supports uptake of premium devices. China and India house large patient pools; tiered pricing and local manufacturing alliances help mitigate affordability constraints. Japan’s aging demographics and favorable reimbursement drive high per-capita device density. Regional digital-health infrastructure allows smartphone-centric artificial pancreas deployments to integrate seamlessly with national telemedicine platforms, propelling further expansion.

Competitive Landscape

Market concentration is moderate with established device companies leveraging installed pump and CGM bases. Medtronic, Tandem Diabetes Care, Insulet, and Dexcom lead portfolio breadth and geographic reach. Strategic alliances such as Abbott-Medtronic integrate top-tier sensors with next-generation pumps, shortening innovation cycles.

Beta Bionics disrupts with the iLet platform that requires only body-weight input, simplifying onboarding and appealing to first-time users. Firms emphasize interoperability to win DIY users seeking flexible components. Open-source AID communities, estimated at 10,000 users, push commercial vendors to accelerate software updates and transparency.

Regulatory clearance speed and payer evidence dossiers are crucial competitive levers. Leaders invest heavily in large-scale real-world evidence to secure coverage expansion, while start-ups rely on breakthrough-device designations to fast-track approvals. Continuous software-as-a-medical-device updates create recurring revenue and lock-in users, intensifying rivalry within the artificial pancreas device system market.

Artificial Pancreas Device System Industry Leaders

Medtronic plc

Tandem Diabetes Care, Inc

Insulet Corporation

Defymed

DexCom Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: University of Virginia unveiled digital-twin modeling that personalizes insulin algorithms for forthcoming artificial pancreas releases.

- April 2025: Medtronic filed 510(k) for MiniMed 780G pump interoperable with Abbott CGM, aiming for U.S. clearance in 2026.

Global Artificial Pancreas Device System Market Report Scope

As per the scope of the report, an artificial pancreas device system is a medical device that links a glucose monitor to an insulin infusion pump where the pump automatically takes action (using a control algorithm) based on the glucose monitor reading. The Artificial Pancreas Device System (APDS) market is segmented by Device type (Threshold Suspended Device System, Control to Range (CTR) System, and Control to Target(CTT) System), End User (Hospitals and Clinics and Others), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The market report also covers the estimated market sizes and trends for 17 different countries across major regions, globally. The report offers the value (in USD million) for the above segments.

| Threshold Suspend Device System |

| Control-to-Range (CTR) System |

| Control-to-Target / Hybrid Closed-Loop System |

| Fully Automated Closed-Loop / Bionic Pancreas |

| Insulin Pump |

| Continuous Glucose Monitor |

| Control Algorithm / Software |

| Disposable Infusion Sets & Sensors |

| Hospitals & Clinics |

| Homecare Settings |

| Ambulatory Surgical Centers |

| Pediatric (Less Than 18 Years) |

| Adult (Greater Than 18 Years) |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Device Type | Threshold Suspend Device System | |

| Control-to-Range (CTR) System | ||

| Control-to-Target / Hybrid Closed-Loop System | ||

| Fully Automated Closed-Loop / Bionic Pancreas | ||

| By Component | Insulin Pump | |

| Continuous Glucose Monitor | ||

| Control Algorithm / Software | ||

| Disposable Infusion Sets & Sensors | ||

| By End User | Hospitals & Clinics | |

| Homecare Settings | ||

| Ambulatory Surgical Centers | ||

| By Patient Age Group | Pediatric (Less Than 18 Years) | |

| Adult (Greater Than 18 Years) | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large is the artificial pancreas device system market in 2026?

The artificial pancreas device system market size is USD 1.19 billion in 2026.

What is the expected growth rate for artificial pancreas solutions through 2031?

Global revenue is projected to rise at an 17.94% CAGR between 2026 and 2031.

Which region is growing fastest for automated insulin delivery platforms?

Asia-Pacific records the highest forecast CAGR at 18.88% during 2026-2031.

Which device type is gaining share most quickly?

Fully automated closed-loop/bionic pancreas systems are advancing at 23.85% CAGR.

What main obstacle limits uptake in emerging markets?

High total cost of ownership and inconsistent insurance coverage remain primary barriers.

Page last updated on: