Medical Radiation Shielding Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 1.69 Billion |

| Market Size (2031) | USD 2.32 Billion |

| Growth Rate (2026 - 2031) | 6.54% CAGR |

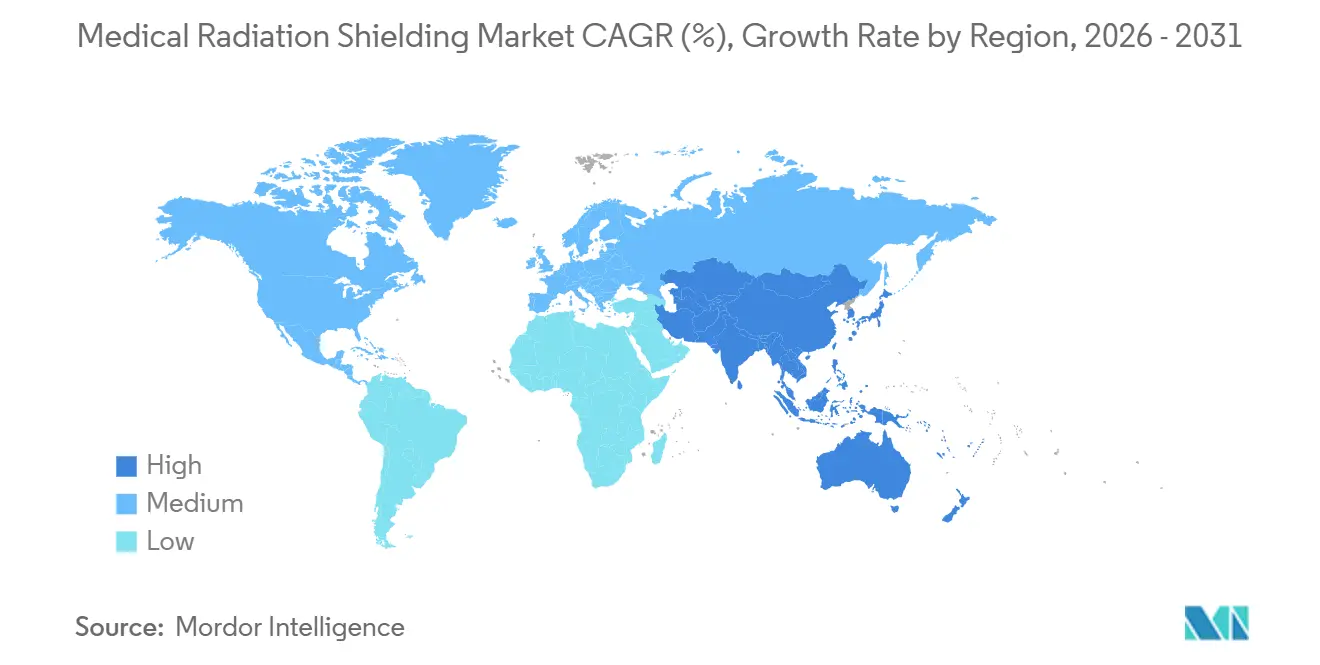

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

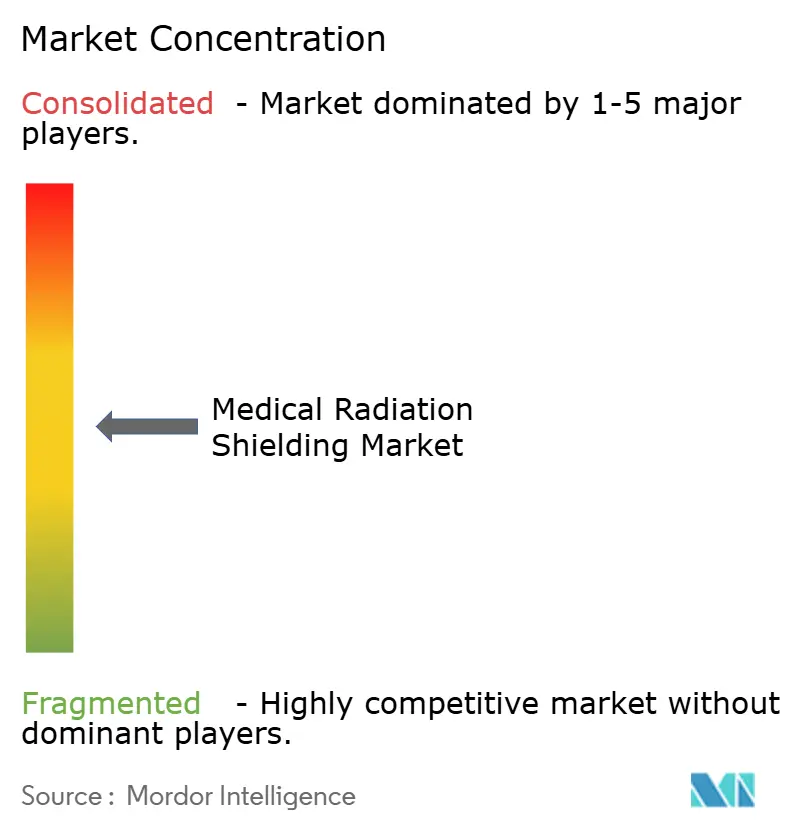

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Medical Radiation Shielding Market Analysis by Mordor Intelligence

The Medical Radiation Shielding Market size is projected to be USD 1.59 billion in 2025, USD 1.69 billion in 2026, and reach USD 2.32 billion by 2031, growing at a CAGR of 6.54% from 2026 to 2031.

Demand tracks the rising global cancer burden, faster adoption of proton and heavy ion therapy, and the build-out of radiopharmaceutical plants in the Asia-Pacific. Non-lead composites are gaining traction because they cut weight, lower disposal risk, and enable quick retrofits of legacy vaults. Vertically integrated suppliers that recycle lead and smelt tungsten in-house are softening margin pressure from volatile metals prices. Turnkey contracts that bundle shielding, civil works, and regulatory filings are now the preferred procurement route for new particle therapy centers, especially in China and India.

Key Report Takeaways

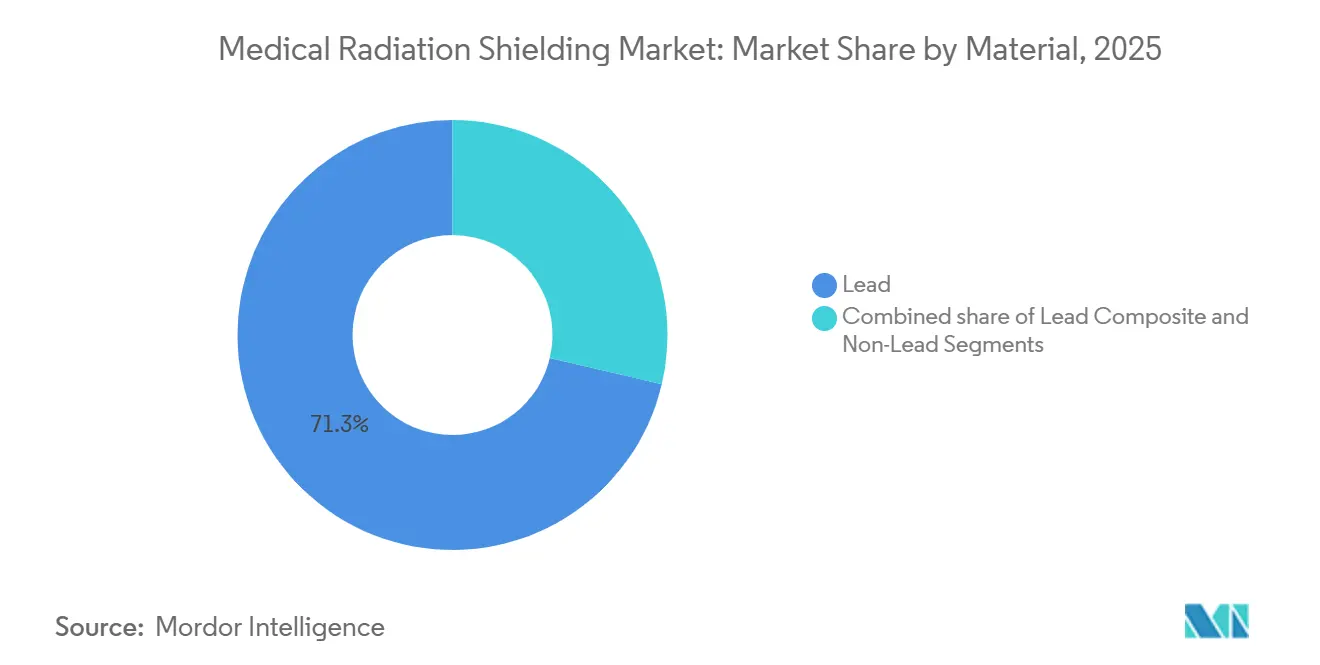

- By material, lead retained 71.32% of the medical radiation shielding market share in 2025, while non-lead composites are forecast to expand at an 8.35% CAGR to 2031.

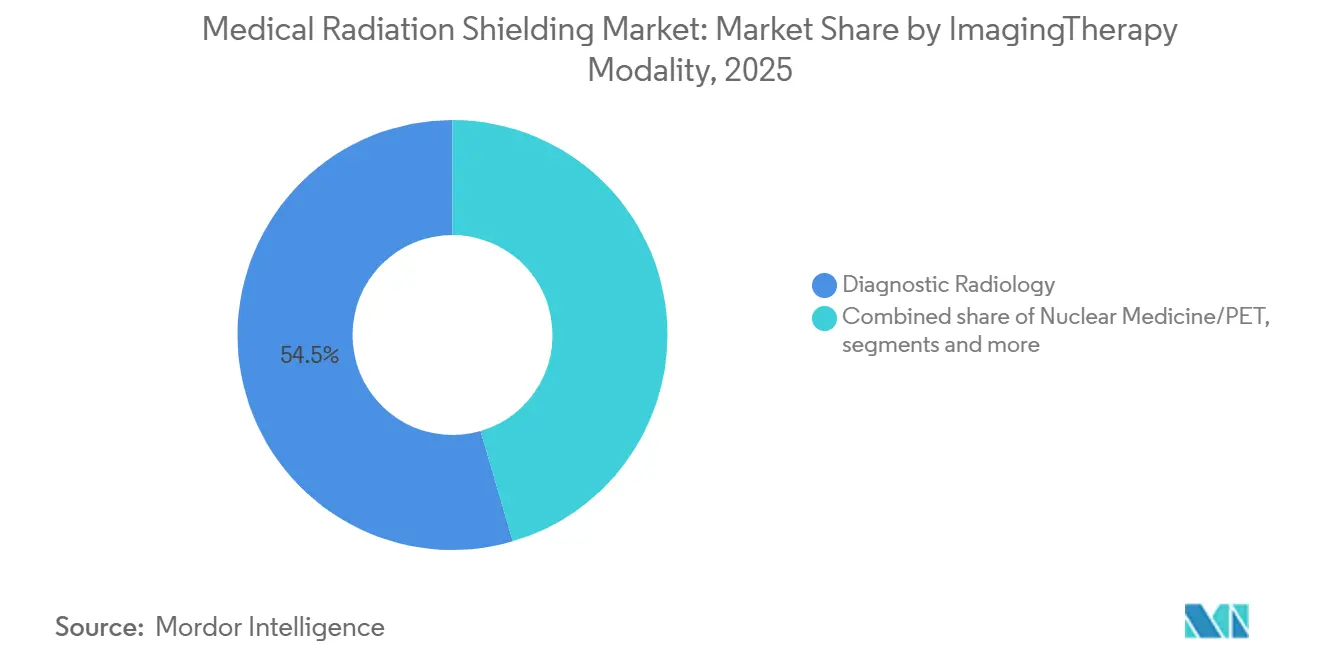

- By imaging and therapy modality, diagnostic radiology led with a 54.53% revenue share in 2025; proton and heavy ion therapy are projected to post the fastest growth rate of 9.51% through 2031.

- By end user, hospitals accounted for 61.56% of the medical radiation shielding market size in 2025, and ambulatory surgery centers are projected to grow at a 9.84% CAGR from 2026 to 2031.

- By geography, North America captured 35.65% of the 2025 revenue, while the Asia-Pacific region is projected to advance at a 7.23% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Medical Radiation Shielding Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Global Cancer Incidence | +1.2% | Global, acute in Asia-Pacific and Sub-Saharan Africa | Medium term (2-4 years) |

| Adoption of Advanced Radiation Modalities | +0.8% | North America, Europe, Japan, South Korea, Singapore | Long term (≥ 4 years) |

| Expansion of Nuclear Medicine Capacity | +1.1% | North America, Europe, China, India | Medium term (2-4 years) |

| Government-Funded Oncology Programs | +0.9% | Asia-Pacific, Middle East & Africa, Latin America | Long term (≥ 4 years) |

| Uptake of Intraoperative Radiation Therapy | +0.7% | North America, Western Europe, urban Asia-Pacific | Short term (≤ 2 years) |

| 3D-Printed Polymer–Tungsten Retrofits | +0.6% | Global, early in Eastern Europe and Southeast Asia | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Global Cancer Incidence Elevating Radiotherapy and Imaging Installations

Cancer remains the second-leading cause of death worldwide, and 50-60% of patients need radiotherapy during treatment[1]International Atomic Energy Agency, “Rays of Hope initiative,” iaea.org. Twenty-three Sub-Saharan countries still lack radiotherapy devices, so the IAEA's Rays of Hope program is deploying linear accelerators and cobalt-60 units in these regions. Each new vault requires 2-4 mm of lead-equivalent shielding for walls, ceilings, and floors, which necessitates several metric tons of material. The growing adoption of CT and fluoroscopy in emerging markets further accelerates shielding demand for technician protection. Continued screening initiatives and universal coverage pledges are maintaining a robust global pipeline of shielding projects, which is expected to crest in the next four years.

Adoption of Advanced Radiation Modalities Necessitating Enhanced Shielding

The number of global proton therapy centers rose to 114 by 2025, with an additional 40 centers slated for completion by 2030. These facilities require 3 m neutron-attenuating concrete walls complemented by borated polyethylene layers. Image-guided and intensity-modulated linear accelerators also require tighter control over scatter radiation, driving the need for retrofits of existing bunkers. Vendors such as Hitachi bundle vault design with equipment supply, compressing schedules but pushing project costs over USD 100 million for a two-gantry proton suite[2]MD Anderson Cancer Center, “Proton therapy program updates,” mdanderson.org. Integrated suppliers that manage civil works, shielding physics, and approvals are positioned to win these long-cycle contracts.

Expansion of Nuclear Medicine and Radiopharmaceutical Manufacturing

Targeted radionuclide therapies for neuroendocrine and prostate cancers are moving to mainstream protocols. Novartis added hot cells with tungsten-lined glove boxes to its Indianapolis plant, incurring a USD 120 million investment in 2025. Orano Med has earmarked EUR 250 million for thorium and lead isotope production, requiring modular, shielded labs. The EU also approved EUR 2 billion for the Pallas reactor, which will need extensive containment shielding. Facilities must incorporate lead-glass windows, HEPA-filtered HVAC systems, and dosimetry sensors, thereby opening the scope for turnkey shielding packages.

Government-Funded Oncology Infrastructure in Emerging Markets

India budgeted USD 1.5 billion through 2026 to build 20 tertiary cancer centers. China subsidizes up to 60% of radiotherapy equipment and construction, lifting installed machines above 3,000 by 2024. These programs favor prefabricated shielding panels that can be installed in weeks rather than months, enabling rapid capacity expansion. Local fabricators that partner with global experts to meet IAEA codes are gaining share, while foreign suppliers compete on engineering certification and fast installation.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capital expenditure for shielded facilities and bunker construction | -1.3% | Global, with acute impact in Sub-Saharan Africa, South Asia, and Latin America | Short term (≤ 2 years) |

| Volatile prices of lead, tungsten, and non-lead alloys | -0.9% | Global, pronounced in Asia-Pacific and Europe | Medium term (2-4 years) |

| Environmental liability from lead-contaminated waste streams | -0.7% | North America and Europe under strict disposal regulations; emerging relevance Asia-Pacific | Medium term (2-4 years) |

| Limited availability of certified radiation shielding engineers in developing regions | -0.6% | Sub-Saharan Africa, South Asia, and parts of Latin America | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Capital Expenditure for Shielded Facilities and Bunker Construction

External-beam vaults cost USD 1.5–3 million each, while proton centers exceed USD 100 million, with shielding accounting for up to 30% of the expenditure. Many public hospitals in low-income regions rely on annual appropriations, stretching procurement cycles beyond 18 months. The U.S. EPA classifies waste as hazardous, adding USD 200–400 per metric ton in disposal fees and deterring retrofits[3]U.S. Environmental Protection Agency, “RCRA hazardous waste guidelines,” epa.gov. Prefabricated barriers and 3D-printed composites offer relief but still need code validation, prolonging decision timelines in cash-constrained markets.

Volatile Prices of Lead, Tungsten, and Non-Lead Alloys

Lead averaged USD 2,100–2,200 per metric ton in 2025, while tungsten hovered between USD 270 and USD 330 per metric ton. Export quotas from China and Vietnam amplified price swings, squeezing suppliers locked into fixed-price contracts. Bismuth traded around USD 6 per pound, reflecting tight refining capacity. Fabricators with recycling loops or their own smelters are partially insulated, but smaller regional players often absorb cost spikes, hampering R&D for non-lead solutions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material: Non-Lead Composites Gain Ground on Retrofit and Environmental Advantages

Lead remained dominant in 2025, accounting for 71.32% of revenues; however, the medical radiation shielding market size for non-lead composites is forecast to grow at an 8.35% CAGR through 2031. California Proposition 65 audits and the EU Restriction of Hazardous Substances directive intensified the shift. Tungsten-polymer panels produced through 3D printing cut weight by 30-40% and speed up installation. Borated polyethylene demand is rising alongside particle therapy projects, because it attenuates fast neutrons. Suppliers that deliver hybrid portfolios lead for high-attenuation walls and non-lead for weight-sensitive retrofits capture cross-segment opportunities.

The portability of polymer-tungsten tiles appeals to imaging chains upgrading multiple sites. Hospitals in seismic zones welcome lighter walls that reduce the need for structural steel. Recycling programs that reclaim lead from decommissioned vaults provide input for cast-lead bricks used in new builds, easing disposal concerns. These trends collectively erode lead’s share while opening space for specialty fabricators fluent in both metal casting and additive manufacturing.

By Imaging/Therapy Modality: Proton Therapy Drives Premium Shielding Demand

Diagnostic radiology accounted for 54.53% of 2025 revenue, but proton and heavy ion therapy are expected to expand at a 9.51% CAGR, outpacing every other modality. Each proton gantry requires 3 m of thick concrete, plus borated polyethylene, pushing project budgets well above those of traditional linac rooms. The medical radiation shielding market size for particle therapy suites is therefore set to swell, even though the absolute number of centers remains modest.

Nuclear medicine plants need glove boxes, hot cells, and lead-glass windows, creating steady demand as targeted radionuclide therapies are commercialized. External-beam linacs still account for the most extensive installed base, particularly in emerging regions upgrading from cobalt-60 units. Intraoperative radiation therapy systems are driving growth in modular barriers, benefiting firms that can fabricate custom panels in days rather than weeks.

By End User: Ambulatory Surgery Centers Embrace Compact IORT Solutions

Hospitals accounted for 61.56% of 2025 revenue, yet ambulatory surgery centers are forecasted to grow at a rate of 9.84% yearly, the highest among end users. Lightweight 1-2 mm panels let outpatient facilities add radiation capability without significant structural changes, shortening build times. The medical radiation shielding market share for ambulatory centers is expected to rise steadily through 2031.

Diagnostic imaging chains deploy mobile CT trailers that need removable lead curtains, driving a niche for snap-fit shielding. Veterinary hospitals and research labs form a smaller but consistent customer base, as regulators enforce occupational exposure limits. Vendors supplying pre-engineered kits sized to standard operating rooms are improving margins through volume production. Hospitals still anchor absolute demand, but growth momentum is clearly shifting to the outpatient space.

Geography Analysis

North America generated 35.65% of 2025 revenue, buoyed by high healthcare spending and stringent FDA oversight that mandates certified shielding materials. Replacement cycles for aging vaults sustain projects in urban markets, while proton therapy expansions in Connecticut and Tampa require premium neutron protection. EPA waste rules are accelerating the adoption of non-lead alternatives, encouraging closed-loop recycling.

The Asia-Pacific region is the growth engine, with a projected 7.23% CAGR through 2031, driven by public-sector build-outs in China and India. China surpassed 3,000 radiotherapy machines in 2024, thanks to provincial subsidies that cover up to 60% of the costs. India’s USD 1.5 billion cancer-center program prefers modular panels to compress timelines. Private chains, such as Apollo Hospitals, are adding proton centers in Chennai and Kolkata, thereby amplifying demand for neutron-grade concrete.

Europe emphasizes lead-free solutions under the Restriction of Hazardous Substances (RoHS) directive, spurring research and development in bismuth and tungsten composites. The Middle East funds centers of excellence in the United Arab Emirates and Saudi Arabia to stem the flow of outbound medical tourism. Sub-Saharan Africa remains underserved, but the IAEA Rays of Hope initiative is opening a multi-year pipeline of external-beam vaults. South America’s first proton therapy unit commenced operations in Buenos Aires in 2025, signaling a rising demand for premium shielding.

Competitive Landscape

The top five vendors control roughly 40% of global revenue, indicating moderate concentration. Mirion Technologies leveraged its USD 800 million 2024 revenue base to cross-sell shielding with radiation detectors. Strategic alliances between barrier suppliers and linac or cyclotron OEMs are now essential for securing turnkey contracts, especially in regions building first-generation particle centers. Engineering certification, rapid installation, and compliance with IEC codes are the primary buying criteria as regulators tighten lead-waste rules under the U.S. Resource Conservation and Recovery Act.

3D-printed polymer–tungsten panels present white-space growth. Regional specialists in Eastern Europe and Southeast Asia undercut Western pricing by 20-30%, though they still face capacity and standards hurdles. Vendors incorporating cloud-based workflow tools that auto-populate licensing forms and stream dosimetry data to inspectors finish projects weeks faster than rivals, giving them an execution edge. Market momentum is clearly shifting from pure material supply to integrated project delivery, favoring players that combine materials engineering with regulatory expertise.

Medical Radiation Shielding Industry Leaders

Nelco Inc

Marshield

Radiation Protection Products Inc

Gaven Industries Inc

Esco Technologies Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Carl Zeiss Meditec received FDA 510(k) clearance for an upgraded Intrabeam IORT system needing just 1-2 mm lead-equivalent wall protection.

- April 2025: Rampart IC, a Birmingham-based developer of radiation shielding for interventional suites, announced the acquisition of ClearShield. ClearShield specializes in manufacturing lead-free, radiation-attenuating acrylic. The deal aims to enhance radiation protection solutions offered by both companies.

- April 2025: NanoRay, a pioneer in Taiwan’s X-ray technology, has made significant advancements in its field. As of 2024, the company’s transmission X-ray tube technology offers 80% radiation reduction, 90% lower power consumption, and a 60° wider beam angle. These innovations significantly enhance image quality and efficiency in medical and industrial applications.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the medical radiation shielding market as the sale of fixed or mobile structural products, walls, doors, barriers, booths, glass, curtains, panels, bricks, and advanced non-lead composites, installed to attenuate ionizing radiation produced by diagnostic imaging systems, nuclear medicine rooms, and external-beam radiotherapy bunkers. Measured value includes new equipment, retrofits, and replacement shielding supplied to healthcare end users across hospitals, imaging centers, ambulatory surgery centers, and research institutes.

Scope Exclusions: Consumable personal protective garments, non-medical industrial shielding, and purely detection or dosimetry devices fall outside this valuation.

Segmentation Overview

- By Material

- Lead

- Lead Composite

- Non-Lead (Bismuth, Tungsten, Antimony, Borated PE)

- By Imaging / Therapy Modality

- Diagnostic Radiology (X-ray, CT, Fluoroscopy)

- Nuclear Medicine / PET

- External Beam Radiation Therapy (LINAC, IMRT, IGRT)

- Proton & Heavy Ion Therapy

- By End User

- Hospitals

- Diagnostic Imaging Centers

- Ambulatory Surgery Centers

- Other End Users

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest Of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest Of Asia-Pacific

- Middle-East And Africa

- GCC

- South Africa

- Rest Of Middle East And Africa

- South America

- Brazil

- Argentina

- Rest Of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed radiation oncologists, medical physicists, hospital facility managers, and shielding contractors across North America, Europe, and Asia-Pacific. The conversations validated typical shielded room footprints, material mix shifts toward lead-free composites, installation lead times, and average selling prices, which strengthened our desk findings and aligned regional variance assumptions.

Desk Research

We began with public datasets that frame the demand pool, including cancer incidence and imaging procedure volumes from the World Health Organization, International Agency for Research on Cancer, and OECD Health Statistics. Construction codes and shielding standards were reviewed from the International Atomic Energy Agency, National Council on Radiation Protection & Measurements, and U.S. Nuclear Regulatory Commission. Trade shipment records and producer price trends were drawn from sources such as UN Comtrade, Volza, and Asia Metal. Financial filings and investor decks of listed shielding suppliers complemented the outlook, while paid platforms like D&B Hoovers and Dow Jones Factiva provided revenue splits that anchor supplier roll-ups. The sources listed are illustrative; many additional references informed data checks and clarifications.

Market-Sizing & Forecasting

A top-down construct estimates total shielded room demand by linking counts of active CT, MRI, LINAC, and proton units to recommended barrier specifications, then multiplying by region-specific average shield cost. Results are cross-checked through selective bottom-up supplier revenue roll-ups and channel ASP × volume samples before final calibration. Key variables in the model include annual imaging equipment installations, number of new cancer radiotherapy centers, average wall thickness standards, lead price indices, and hospital capital-expenditure budgets. Multivariate regression projects each driver, while scenario analysis captures regulatory tightening or rapid composite adoption, so forecasts remain responsive. Data gaps in bottom-up inputs are filled through conservative interpolation from nearest known supplier benchmarks.

Data Validation & Update Cycle

Our outputs pass two rounds of anomaly screening, peer review, and senior analyst sign-off. Figures are compared with independent procedure growth rates and raw-material consumption signals. The report refreshes every twelve months, and interim updates are triggered when regulatory changes, raw-material shocks, or mergers materially alter our baseline.

Why Our Medical Radiation Shielding Baseline Inspires Confidence

Published estimates naturally diverge because firms choose different inclusion rules, base years, and refresh cadences. According to Mordor Intelligence, the disciplined link between imaging capacity, engineering codes, and material pricing keeps our view grounded, while others may apply flat revenue growth factors or exclude retrofit activity.

Key gap drivers include narrower product baskets that omit composite panels, use of constant ASPs without commodity price escalation, or models tied to diagnostic procedure counts only. Another variance arises when some studies freeze currency at historical rates, whereas we update with average annual exchange rates.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 1.58 B (2025) | Mordor Intelligence | - |

| USD 1.51 B (2025) | Global Consultancy A | Excludes retrofit projects and uses static ASPs |

| USD 1.40 B (2024) | Trade Journal B | Omits lead-free composites and applies 2022 exchange rates |

These comparisons show that Mordor's blended top-down and bottom-up approach, refreshed annually and anchored to clearly traceable drivers, delivers a balanced baseline that decision-makers can rely on when planning capacity expansions or supply strategies.

Key Questions Answered in the Report

What is the forecast value of the medical radiation shielding market in 2031?

The market is expected to reach USD 2.32 billion by 2031, growing at a 6.54% CAGR.

Which material segment is growing the fastest?

Non-lead composites, especially polymer-tungsten and borated polyethylene blends, are projected to rise at an 8.35% CAGR through 2031.

Why is Asia-Pacific the fastest growing region?

Government-funded oncology programs in China and India, along with private proton therapy investments, are driving a projected 7.23% CAGR in the region.

How are 3D-printed shields impacting demand?

Additive manufacturing lowers weight and installation labor, reducing retrofit costs by up to 25% and accelerating adoption in cost-sensitive markets.

What is the main restraint for new shielding projects?

High capital expenditure, with vaults costing USD 1.5-3 million and proton centers exceeding USD 100 million, remains the primary barrier.

Which end-user segment is expanding the quickest?

Ambulatory surgery centers, fueled by compact intraoperative radiation therapy systems, are advancing at a 9.84% CAGR through 2031.

Page last updated on: