Trocars Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 0.87 Billion |

| Market Size (2031) | USD 1.12 Billion |

| Growth Rate (2026 - 2031) | 5.10% CAGR |

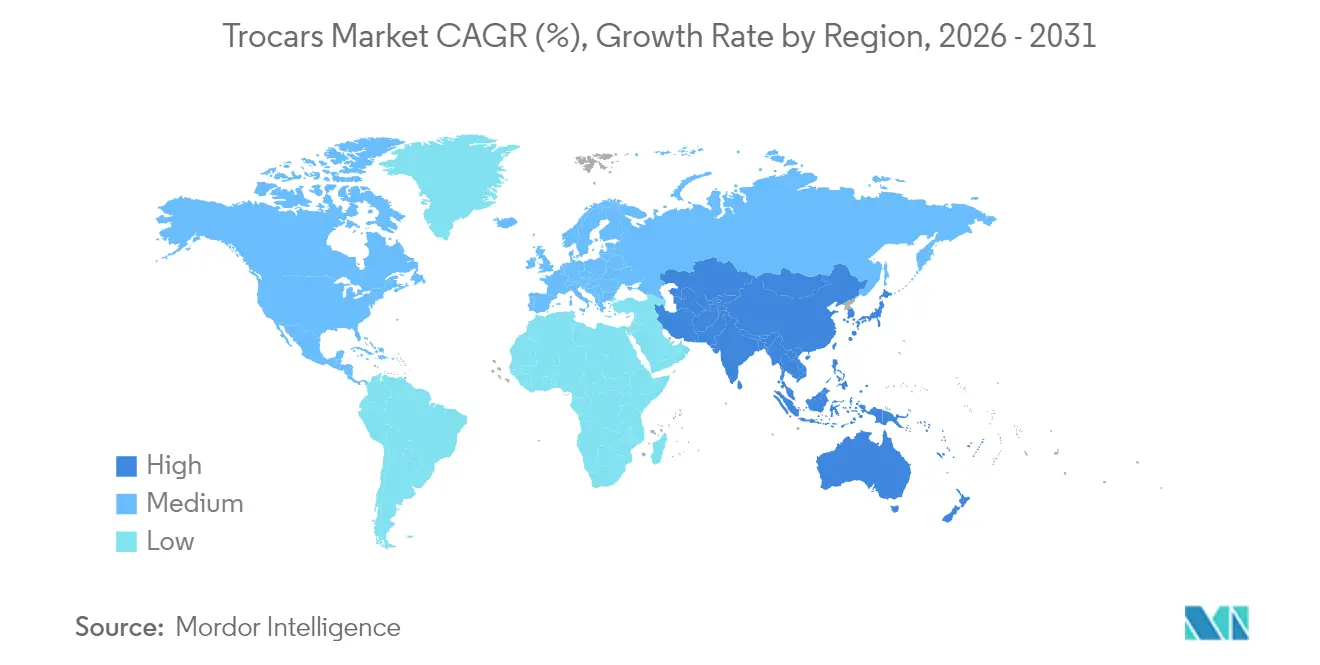

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

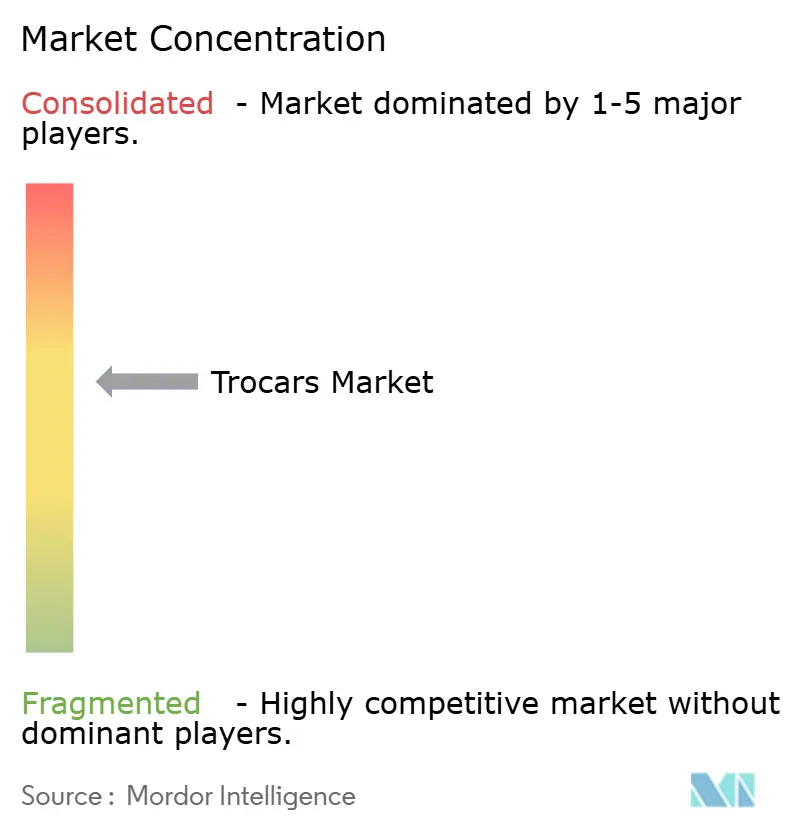

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Trocars Market Analysis by Mordor Intelligence

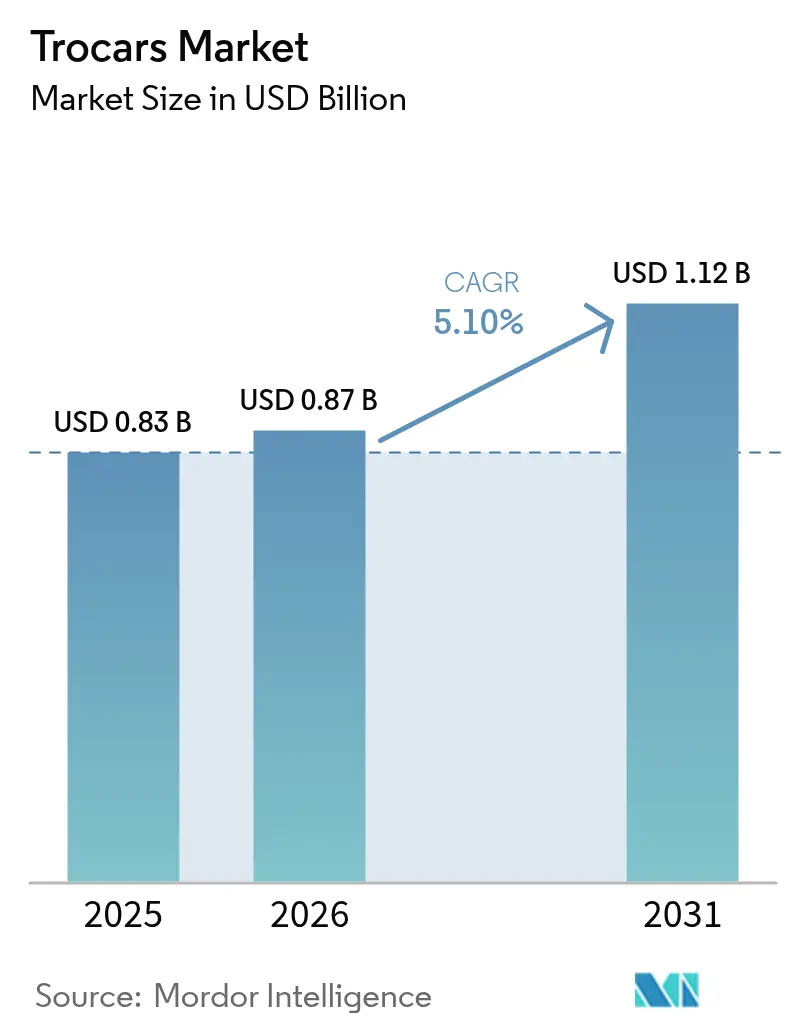

The Trocars Market size was valued at USD 0.83 billion in 2025 and estimated to grow from USD 0.87 billion in 2026 to reach USD 1.12 billion by 2031, at a CAGR of 5.10% during the forecast period (2026-2031).

Growth is tied to the continued shift from open surgery toward minimally invasive techniques, the rapid penetration of optical entry systems, and expanding procedure volumes in ambulatory settings. Asia-Pacific is projected to post the strongest 6.87% CAGR as governments underwrite laparoscopic skills programs that broaden access to sophisticated care. In North America, bulk-purchase agreements between device makers and ambulatory surgery centers (ASCs) are driving higher unit volumes while tightening price points. Meanwhile, sustainability-driven regulations on sharps disposal are amplifying interest in reposable hybrids that balance infection control with lower waste profiles. Competitive intensity is moderate: two diversified med-tech leaders dominate global channels, but niche companies are winning specialty contracts by offering bariatric-specific shafts and low-force optical tips.

Key Report Takeaways

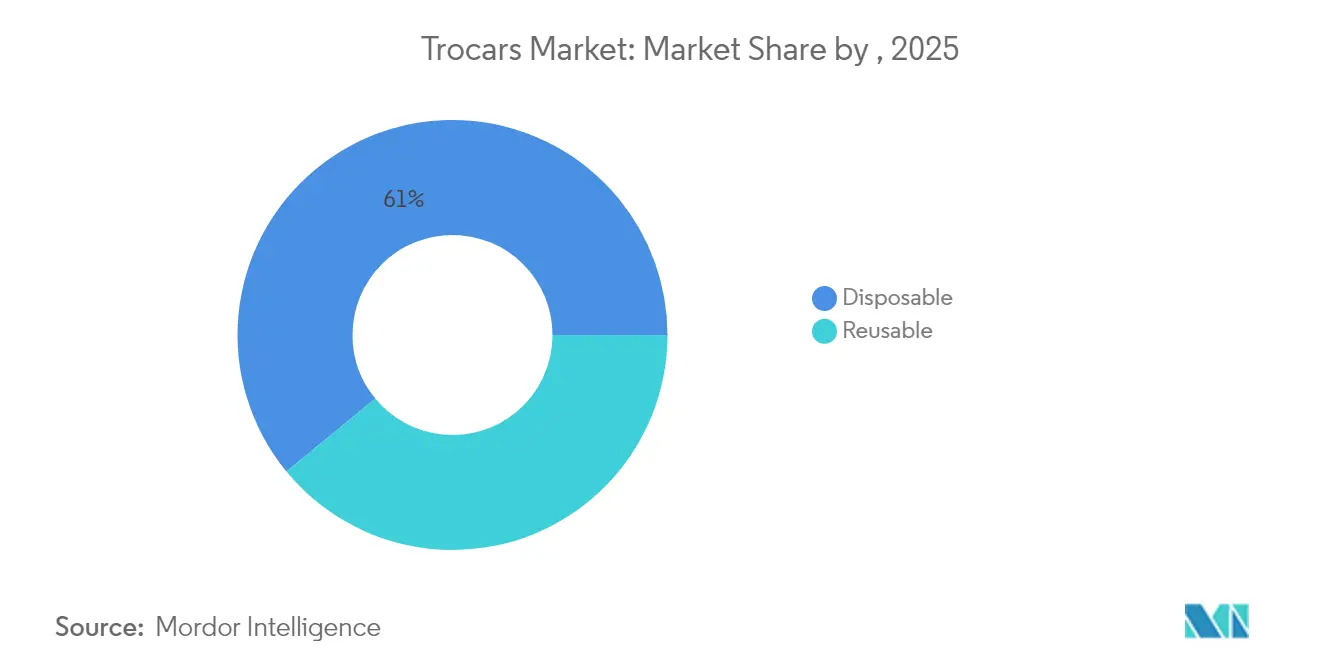

- By product type, disposable trocars held 60.95% of trocars market share in 2025, whereas reposable/hybrid designs are set to expand at a 5.96% CAGR through 2031.

- By tip design, bladeless units led with 46.10% revenue share in 2025; optical/direct-vision models are the fastest-growing at a 7.33% CAGR to 2031.

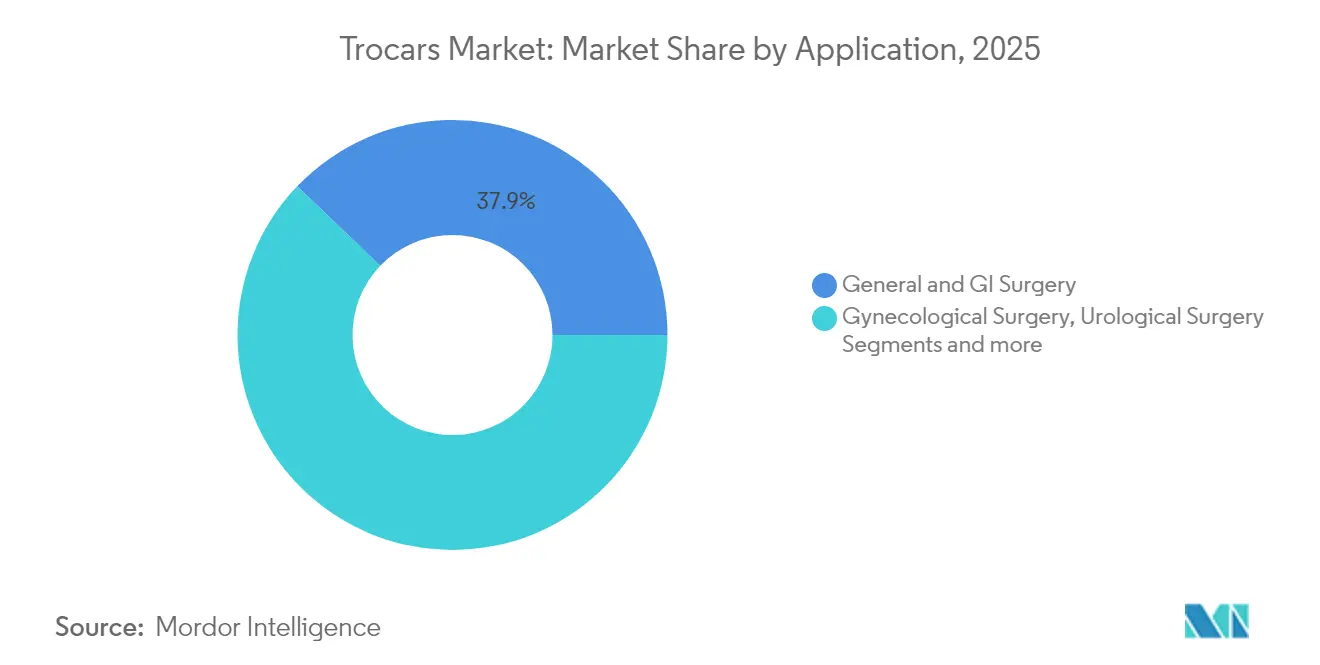

- By application, general and gastrointestinal surgery accounted for 37.85% of the trocars market size in 2025, while bariatric procedures are advancing at a 6.78% CAGR through 2031.

- By end-user, hospitals commanded 61.90% of trocars market share in 2025; ASCs record the highest growth at a 6.42% CAGR between 2026 and 2031.

- By geography, Asia-Pacific is forecast to register a 6.69% CAGR, outpacing all other geographies

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Trocars Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shift to minimally invasive surgery | +1.80% | Global, strongest in Asia-Pacific | Medium term (2-4 years) |

| Rising bariatric procedure volumes | +1.20% | North America, Europe, Asia-Pacific | Medium term (2-4 years) |

| Faster replacement of disposable trocars | +0.80% | North America, Europe | Short term (≤2 years) |

| Government-funded laparoscopic training | +0.70% | Asia-Pacific, MEA, Latin America | Medium term (2-4 years) |

| Migration toward optical entry systems | +1.40% | Global, led by North America | Medium term (2-4 years) |

| OEM–ASC volume contracting | +0.60% | North America | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Rapid Shift from Open to Minimally Invasive Procedures

Surgeons now favor laparoscopy over laparotomy because it cuts mortality odds by 90% and major complications by 62% in trauma diagnostics. Shorter inpatient stays translate to leaner hospital budgets and faster bed turnover, intensifying institutional preference for trocar-dependent approaches. Device makers answer with procedure-specific kits that package access ports, insufflation filters, and smoke evacuation valves, a shift that fuels premium pricing. The surge in evidence-backed clinical benefits propels the trocars market, especially in systems that integrate optical guidance for safer first entry. Hospitals are therefore rewriting capital expenditure plans to prioritize laparoscopic towers and complementary trocar disposables, anchoring recurring revenue streams for vendors.

Rising Bariatric Surgery Volumes

Obesity prevalence keeps bariatric interventions on a 6.96% CAGR upswing, spurring demand for long-shaft, low-drag trocars able to traverse thicker abdominal walls [1]Anne-Sophie Studer et al., "Fully Ambulatory Robotic Single Anastomosis Duodeno-Ileal Bypass (SADI): 40 Consecutive Patients in a Single Tertiary Bariatric Center," BMC Surgery, bmcsurg.biomedcentral.com. Robotic single-anastomosis duodeno-ileal bypass (SADI) techniques that enable same-day discharge further accelerate adoption, as payers reward outpatient metabolic surgery. Engineering teams now model trocar tips to cut insertion torque while safeguarding pneumoperitoneum, an advance valued by high-BMI patient cohorts. Vendors that secure bariatric center-of-excellence endorsements capture sticky channel partnerships because surgeons tend to standardize on a single platform for workflow familiarity. This bariatric momentum compounds overall trocars market growth through dependable case volumes and procedure-specific up-sells such as extended-length optical obturators.

Industry Migration toward Optical Entry Systems

Clinical data show optical trocars achieve 100% first-pass visualization with just 0.3% injury incidence among 1,187 patients. Visual confirmation mitigates blind puncture risks, especially in repeat-laparotomy cases with adhesions. Hospitals quantify this safety premium when negotiating malpractice insurance, allowing device vendors to defend higher unit prices. Optical systems also integrate seamlessly with 4K scopes, expanding compatibility across wider OR fleets. Resultant demand lifts the trocars market for premium access devices that deliver lower complication-related costs and faster patient ambulation.

OEM–ASC Bulk-Purchase Contracts

ASCs treated 3.3 million Medicare beneficiaries, with USD 6.1 billion in payments, underlining their bargaining clout [2]Medicare Payment Advisory Commission, "Report to the Congress: Medicare Payment Policy," Medicare Payment Advisory Commission, medpac.gov. To secure this channel, manufacturers negotiate tiered rebates contingent on case volumes, bundling trocars with insufflators or robotic arms. ASCs value predictable, sterile disposables that forgo reprocessing overhead, and their lean supply models favor single-vendor continuity. The resulting locked-in contracts amplify annualized unit shipments, sustaining trocars market expansion despite ASP compression.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Sharps-waste disposal scrutiny | −0.7% | Europe, North America | Medium term (2-4 years) |

| Trocar-related complications | −0.3% | Global | Long term (≥4 years) |

| Regulatory challenges for device approvals | −0.4% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Trocar-related Complications

Trocar-site hernia, although infrequent, incurs added surgeries and drives insurer pushback on certain port diameters. A 2024 case report details an incarcerated ventral hernia following robotic hysterectomy that necessitated emergent repair. Litigation fears compel some facilities to mandate fascial-closure devices for ports larger than 10 mm, increasing procedure time and cost. While bladeless and radially expandable tips reduce fascial defects, residual complication risks sustain clinical reservations, modestly damping trocars market growth in high-risk cohorts such as morbidly obese or elderly patients.

Increasing Regulatory Scrutiny on Sharps Waste Disposal

European regulators now require granular reporting of single-use instrument waste, highlighting that disposables can emit up to 18 times more CO₂ equivalents than reusable alternatives. Hospitals must absorb rising disposal fees and may face procurement audits that disfavor all-plastic trocars lacking recycling pathways. Vendors are countering with hybrid handles paired to peel-pack sterile cannulas, trimming landfill weight by 60%. Yet, until robust take-back schemes scale, environmental compliance costs temper trocars market momentum across sustainability-focused regions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Reposable Hybrids Disrupt Traditional Categories

Disposable units commanded 60.95% of trocars market share in 2025 due to ready-to-use sterility and zero reprocessing labor. Hospitals running high laparoscopy volumes accept the recurrent spend because SSI avoidance outweighs unit cost. Yet sustainability mandates and capital-budget pressures are redirecting attention to hybrid models whose reusable handle pairs with a sterile cannula. This hybridization captured 22.00% of the trocars market size and is projected to outpace the overall industry at a 5.96% CAGR. Life-cycle assessments show hybrid designs cut greenhouse emissions by 50% compared with fully disposable sets. Providers that invest in validated washer-disinfector workflows realize decade-scale savings as handle amortization lowers effective cost per case. Consequently, purchasing committees in Europe and Canada now embed carbon-reduction scoring into tenders, strengthening hybrid demand.

Reusables maintain a foothold in teaching hospitals where sterile-processing staffing is ample and capital amortization spreads over thousands of cases. Some U.S. integrated delivery networks (IDNs) record six-year payback periods on reusable ports, inclusive of maintenance contracts. Even so, surgeon preference for lightweight polymer housings keeps fully reusable stainless-steel sets niche. Over the forecast horizon, competitive positioning will revolve around modular designs that allow single-handed obturator release, integrated insufflation valves, and RFID tags for usage tracking. Vendors optimizing those features without inflating upfront price are poised to win incremental trocars market share across value-conscious health systems.

By Tip Design: Optical Visualization Transforms Insertion Safety

Bladeless devices delivered 46.10% of 2025 revenue, favored for their tissue-separating cones that lower peritoneal puncture force. However, optical/direct-vision models are expanding 7.33% annually as outcomes data vindicate real-time entry visualization. One multi-center trial reported zero major vascular injuries when an optical obturator was employed in 1,187 cases. The superior safety profile aligns with payer quality metrics and malpractice risk reduction, allowing hospitals to justify premium pricing

Bladed trocars, historically the mainstay for high-resistance tissue, still populate trauma and bariatric sets where rapid access is paramount. Innovations such as atraumatic shields that retract only upon reaching peritoneum mitigate cut-through risk, preserving their relevance. Direct trocar insertion techniques are gaining endorsement after a 2024 comparative study showed a 3.3% complication rate versus 15.7% with Veress needle entry. Future competitive edge lies in multi-modal ports that toggle between optical and bladeless modes, extending utility across diverse patient anatomies and thereby deepening vendor penetration into the trocars market.

By Application: Bariatric Procedures Drive Specialized Innovation

General and gastrointestinal surgery maintained 37.85% revenue share in 2025 as laparoscopy became default for cholecystectomy, appendectomy, and colorectal resections. Bariatric interventions, however, exhibit the sharpest 6.78% CAGR thanks to rising obesity and revisions for failed sleeve gastrectomies. Extended-length ports, anti-slip fixation balloons, and wider insufflation channels differentiate bariatric trocars, generating ASPs 15-20% above standard sets. The segment’s growth lifts the trocars market size as insurers increasingly reimburse metabolic surgery to offset chronic disease costs.

Gynecology accounts for a stable 17.00% share, with robotic hysterectomies sustaining demand for 8 mm robotic-arm-compatible ports. Urology and “other” emerging laparoscopic procedures-thoracic, pediatric, and fertility preservation-together form a 20.00% slice and are projected to rise moderately on the back of technology diffusion. As surgeons push minimally invasive boundaries, manufacturers engage key opinion leaders to co-design procedure-specific cannulas, ensuring that every new specialty spurt translates into incremental trocars market expansion rather than generic commoditization.

By End-User: Ambulatory Centers Reshape Purchasing Dynamics

Hospitals generated 61.90% of 2025 revenue, but their growth is tempered by budget caps and sterilization backlogs. ASCs, by contrast, are clocking 6.42% annual growth and represent the most vibrant sales avenue. They prefer disposable kits that enable efficient room turnover and align with one-time bundled drilldowns in CPT-based reimbursements. To secure the channel, manufacturers align catalog pricing with group purchasing organization (GPO) tiers and include staff in-service training, deepening brand loyalty.

Specialty clinics-fertility, colorectal, endometriosis-constitute the remaining 9.00% of trocars market size and value differentiated features such as ultra-low-profile heads to fit within cramped single-incision setups. Despite lower absolute volume, their procedure specialization yields predictable re-order cycles. Vendors cultivating these micro-segments through tailored sampling programs secure recurring margins that cushion price erosion in mass hospital contracts.

Geography Analysis

North America occupied 41.95% of the trocars market in 2025, anchored by 4 million laparoscopic cases and aggressive ASC growth. Canada’s universal payment system reimburses optical upgrades for rural trauma centers, while Mexico benefits from cross-border medical tourism that channels U.S. retirees into private hospitals. Regulatory predictability and established sterilization standards sustain premium ASPs, reinforcing North America’s contribution to overall trocars market size.

Asia-Pacific posts the highest 6.69% CAGR. China funds laparoscopic skill labs in county hospitals, spurring double-digit trocar volume gains and shortening the capability gap with coastal tertiary centers. India’s middle class increasingly opts for private bariatric packages, translating into robust reorder activity for extended-length optical ports. Japan favors early adoption of optical entry systems due to its aging surgeon workforce seeking safer insertions. South Korea and Australia champion top-of-the-line disposable kits integrated with smoke evacuation. Together these dynamics underpin the region’s growing slice of trocars market share and justify localized manufacturing to curb import tariffs.

Europe represents around 27.80% revenue, with Germany, France, and the United Kingdom leading procedure counts. The EU’s Green Deal forces hospitals to file annual environmental impact disclosures, pressuring them to shift from all-plastic disposables to hybrid handles. Scandinavian tenders now award up to 20% weightage to lifecycle carbon metrics, accelerating reposable adoption. Central and Eastern Europe trail in spending power but attract donor-funded laparoscopic programs that stimulate baseline trocar demand. Beyond the EU, the Middle East’s GCC states are outfitting new mega-hospitals with robotic suites and high-spec optical ports, while Africa’s uptake centers on South Africa’s academic hospitals and Nigeria’s private centers.

Latin America holds a mid-single-digit share yet offers upside as Brazil liberalizes import duties on critical medical devices. Argentina’s volatile currency restricts capital imports but creates gray-market demand for reusable stainless-steel sets. Pan-regional distributors filling these gaps build first-mover advantage ahead of regulatory harmonization. Collectively, geographic diversification insulates the global trocars market against localized reimbursement or supply chain shocks, sustaining a steady aggregate demand curve.

Regulatory Landscape

Trocar devices are regulated as medical devices in major markets, typically under the US FDA Class II framework (21 CFR 876.1500) where most products follow the 510(k) premarket notification pathway. In 2026, the US quality compliance baseline shifted as the FDA transitioned from the Quality System Regulation to the Quality Management System Regulation (QMSR), incorporating ISO 13485:2016 by reference (effective February 2, 2026), pushing manufacturers to align quality systems and documentation to the updated structure for continued US commercialization.

In Europe, the EU Medical Device Regulation (Regulation (EU) 2017/745, MDR) continues to govern conformity assessment and post-market obligations for surgical access devices, with standards alignment serving as a key practical lever for compliance. The European Commission published Implementing Decision (EU) 2026/1231 on June 17, 2026, updating the list of harmonised standards supporting MDR presumption of conformity, increasing the urgency for vendors to refresh technical files, testing packages, and supplier quality controls against the revised standards referenced in the Official Journal of the European Union.

Competitive Landscape

Medtronic global revenue, leveraging broad portfolios and captive distribution. Ethicon’s bladeless and optical trocars remain standard in North American teaching hospitals, while Medtronic’s extended-length VersaOne line dominates bariatric contracts. Stryker, through complementary insufflator and imaging platforms, secures bundled deals that raise switching costs for hospitals already invested in its endoscopy towers.

Strategic M&A sharpens competitive positioning. Medtronic’s acquisition of Fortimedix infused it with micro-laparoscopic intellectual property that translates into slimmer 2.9 mm ports aimed at scar-averse cosmetic surgery . Johnson & Johnson’s OTTAVA robotic system, now in IDE trials, will lock buyers into proprietary trocar geometries, extending its razor-razorblade revenue model. Smaller innovators such as Applied Medical and GENICON carve space via value-priced hybrid handles and country-specific regulatory agility, enabling them to win tenders that penalize high carbon footprints.

Digital ecosystems form the next battleground. Johnson & Johnson’s Polyphonic platform stitches trocar usage data to intra-operative video so surgeons can benchmark port placement against peer datasets. Medtronic counters with AI-guided placement prompts on its robotic console, reducing insertion retries. Patent filings concentrate on trocar tip profiles that lower insertion torque and shield internal viscera, signaling continual functional innovation rather than price-led competition. Collectively these maneuvers elevate switching barriers and lock in annuity-like consumable sales, shaping the future structure of the trocars market.

Trocars Industry Leaders

-

CONMED Corporation

-

B. Braun Melsungen AG

-

Medtronic plc

-

Ethicon Inc. (Johnson & Johnson)

-

Teleflex Incorporated

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Market opportunities for trocar devices arise from shifts in how hospitals and ambulatory surgery centers evaluate access devices, balancing safety, workflow, and environmental impact. Optical and direct-vision entry continues to expand its clinical and purchasing footprint, with real-world outcomes data signaling favorable safety and efficiency signals in contemporary practice, creating whitespace for differentiated optical platforms that deliver lower insertion force and better compatibility with existing imaging stacks. The 2026 US regulatory activity, including Karl Storz's 510(k) clearance for trocars with valve seals (K254228) and Taiwan Surgical Corporation’s Inno-Port disposable bladed trocar (K252532), reinforces ongoing product iteration and wider adoption in US hospital and ASC settings.

A second opportunity area is sustainability-aligned product architecture and procurement readiness, as tenders increasingly weigh lifecycle impact. Hybrid and reposable configurations, such as reusable handles paired with sterile cannulas, address this procurement shift while preserving sterility and turnaround speed valued by ASCs. Vendors that couple these designs with traceability and take-back packaging gain leverage in contracts where environmental reporting and sharps-disposal costs influence purchasing decisions, supported by EU MDR standard updates and continued emphasis on environmental criteria in hospital procurement.

Recent Industry Developments

- May 2026: Karl Storz SE & Co. KG received US FDA 510(k) clearance (K254228) for trocars with valve seals. The clearance supports commercialization of updated sealing performance, which is central to maintaining pneumoperitoneum and reducing leakage-related workflow interruptions. It also signals continued product iteration within the established Class II 510(k) pathway for trocar access devices.

- March 2025: Johnson & Johnson MedTech obtained US FDA 510(k) clearance for Monarch Quest, extending its robotic platform capabilities into pulmonology. While not a trocar-only event, it broadens the company’s minimally invasive ecosystem and can influence adjacent access-device standardization as hospitals and ASCs consolidate vendors around integrated procedure platforms.

- March 2024: Stryker showcased next-generation Mako SmartRobotics with expanded shoulder indications.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this report, the market is measured as revenues generated from trocars used to create access ports during minimally invasive procedures, where a cannula and obturator system enables instrument entry into the body cavity.

Scope exclusions: Veterinary trocars and stand-alone obturators sold without matching sleeves are excluded from this sizing.

Segmentation Overview

-

By Product Type

- Disposable

- Reusable

-

By Tip Design

- Bladed

- Bladeless

- Optical

-

By Application

- General & Gastrointestinal Surgery

- Gynecological Surgery

- Urological Surgery

- Bariatric Surgery

- Other Laparoscopic Procedures

-

By End-user

- Hospitals

- Ambulatory Surgery Centers (ASCs)

- Specialty Clinics

-

By Geography (Value)

-

North America

- United States

- Canada

- Mexico

-

Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

-

Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia- Pacific

-

Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

-

South America

- Brazil

- Argentina

- Rest of South America

-

North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research is used to ground the model in procedure volumes, adoption signals, and product safety and clearance context before any sizing math is applied. We mainly refer to public health statistics and surveillance sources such as the US CDC, OECD health data, and WHO indicators, alongside procedure and clinical practice signals from bodies such as the American College of Surgeons and peer reviewed journals that cover laparoscopic technique trends.

To translate demand drivers into a realistic device revenue pool, we also review regulator and trade information such as the US FDA databases, customs and import export statistics, and hospital procurement and tender disclosures where available. Company filings, investor presentations, and reputable press coverage are used to cross check product mix language and geographic exposure, supported by paid subscriptions for company financials and intelligence plus patent databases to confirm innovation and product cycle timing. These desk sources are illustrative, and many other public references were also used for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work is used to validate what the desk signals cannot fully answer, including how trocar usage per procedure varies by specialty and how ASPs move with material choices, safety features, and hospital purchasing patterns. We spoke with a mix of manufacturers, distributors, surgeons, sterile processing and OR procurement roles, and hospital supply chain teams across APAC, EMEA, and the Americas, so assumptions could be challenged against what is seen in real buying cycles.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 33% | CXOs: 13% | APAC: 43% |

| Mid tier: 51% | Functional/Unit leaders: 27% | EMEA: 37% |

| Smaller Players: 16% | Managers: 60% | Americas: 20% |

Market-Sizing & Forecasting

The sizing starts with a top-down build where procedure volumes and minimally invasive penetration are used to reconstruct the addressable trocar demand pool, and then it is converted into value using realistic usage rates and pricing. In practice, the model is anchored on indicators such as laparoscopic and robotic procedure counts, trocar units used per case (including multi-port patterns), the split between disposable, reusable, and reposable systems, and observed ASP ranges by tip and safety mechanism.

After the global total is formed, we corroborate it with selective bottom-up approximations using supplier and channel checks, along with sampled ASP times volume logic at the region level. If a sub-region has limited published procedure data, the gap is handled through proxy variables such as surgical infrastructure growth, hospital admission trends, and import patterns for laparoscopic consumables, and then adjusted after expert feedback.

For the forecast, scenario analysis is used so the model can reflect different pathways for elective surgery recovery, MIS adoption in emerging markets, and pricing pressure from group purchasing. Where inputs were debated, we used the consensus range from interviews and applied it back to the assumptions so the forecast stays explainable and repeatable.

Data Validation & Update Cycle

Outputs are validated through triangulation across independent signals, which include procedure trends, regional device spend direction, and the implied unit volumes that the final revenue numbers suggest. Outliers are reviewed for causes such as unusual ASP jumps, currency timing, or a region being over-modeled relative to its surgical capacity, and then the assumptions are rechecked before sign-off.

The report is refreshed annually, and interim updates are triggered when material events occur, such as major regulatory actions or sharp shifts in elective surgery volumes. Before delivery, we run a final pass to confirm the latest public indicators, and any interview-driven changes are reflected in the model tables and commentary.

Mordor Intelligence's Trocars Market Size Compared Against Other Published Estimates

Published market sizes for trocars can vary even when the same end use is being discussed, because the included product sets, pricing logic, and the years used for currency conversion are not always handled the same way. Differences also come from how each study treats disposable versus reusable systems, and whether procedure growth is assumed from broad surgery totals or from MIS specific signals.

Stand-alone obturators sold without matching sleeves sit outside Mordor Intelligence's scope, and this single exclusion can shift totals when other publications count accessory-only revenues as part of the trocar market. Gaps can also appear when ASPs are projected using straight-line growth without checking procurement behavior, or when regional totals are extended from a limited set of country inputs without a follow-up validation step.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 0.83 B (2025) | |

| Industry Research Publisher A | USD 0.86 B (2025) | Uses a different base-year setup and can include a broader accessory revenue pool, and the pricing bridge is typically presented with fewer checks against hospital purchasing cycles. |

| Industry Research Publisher B | USD 0.76 B (2024) | Anchors the series to an earlier base year and a longer forecast window, with limited clarity on how reusable versus disposable revenue is normalized across regions and converted into a single USD view. |

The table shows that most spreads are explainable once scope and year alignment are made explicit. By tying the model to procedure-linked demand indicators, a clear unit-per-case logic, and transparent inclusions and exclusions, the final number remains traceable to inputs that can be checked and updated over time.

Key Questions Answered in the Report

What is the current size of the trocars market?

The trocars market generates USD 0.87 billion in 2026 and is projected to reach USD 1.12 billion by 2031.

Which region is growing fastest in the trocars market?

Asia-Pacific leads growth with a 6.69% forecast CAGR as government-funded training programs expand laparoscopic capacity.

Why are optical entry trocars gaining popularity?

Optical trocars allow real-time visualization, cutting insertion injuries to just 0.3% in large patient cohorts and motivating hospitals to pay premium prices for safety.

How do sustainability regulations affect trocar purchasing?

Sharps-waste and carbon-footprint rules encourage hospitals to consider reposable or hybrid designs that cut landfill mass by up to 60%.

What role do ambulatory surgery centers play in the trocars market?

ASCs are the fastest-growing end-user segment at a 6.42% CAGR, favoring bulk-purchase contracts for disposable trocars that streamline turnover and reduce sterilization overhead.

Page last updated on: