Global Medical Device Testing And Certification Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

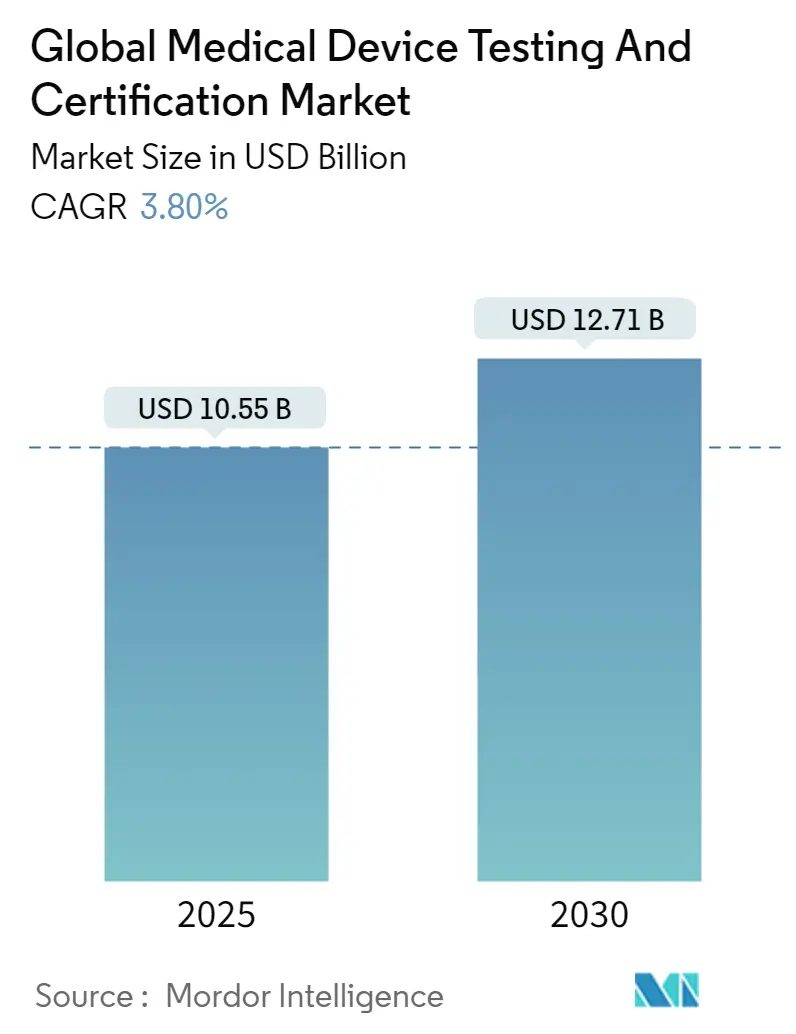

| Market Size (2025) | USD 10.55 Billion |

| Market Size (2030) | USD 12.71 Billion |

| Growth Rate (2025 - 2030) | 3.80% CAGR |

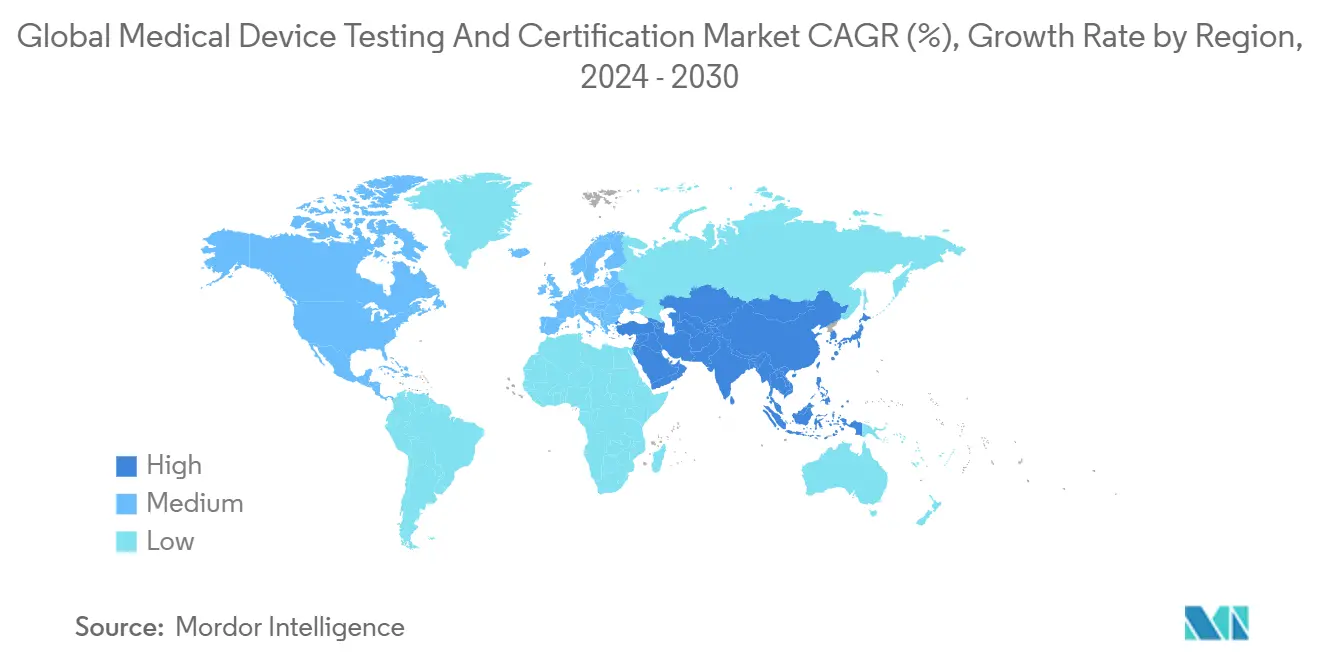

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

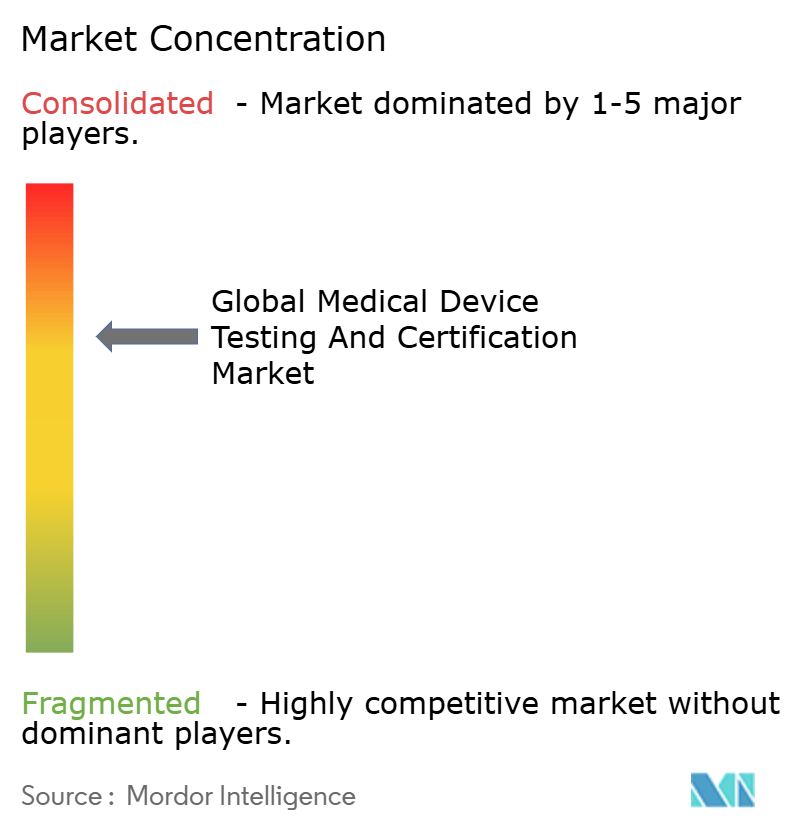

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Global Medical Device Testing And Certification Market Analysis by Mordor Intelligence

The medical device testing & certification services market reached a value of USD 10.55 billion in 2025 and is forecast to attain USD 12.71 billion by 2030, advancing at a 3.8% CAGR over the period. Demand is shaped by the simultaneous enforcement of the EU Medical Device Regulation (MDR) and the United States Food and Drug Administration (FDA) cybersecurity mandate, both of which expand validation scope and documentation depth. Mid-risk Class II devices dominate compliance volumes, while proliferating AI/ML algorithms and connected home diagnostics introduce novel test protocols that spur premium service demand. North America remains the revenue leader, although Asia-Pacific is registering the fastest laboratory expansion because China and India tightened national device laws in 2024, prompting foreign and domestic producers to outsource complex assays. Market participants with multi-jurisdictional accreditations benefit from persistent capacity constraints at EU notified bodies, which have doubled lead times since 2023. Sustainability audits, driven by European public procurement rules, and end-to-end cybersecurity assessments are emerging as differentiators that allow laboratories to charge higher margins for integrated engagements.

Key Report Takeaways

- By service type – Testing services captured 56.56% of medical device testing & certification services market share in 2024; software and cybersecurity testing is projected to expand at a 5.2% CAGR through 2030.

- By device class – Class II devices accounted for 43.34% of the medical device testing & certification services market size in 2024; the subsegment led revenue and is expected to register a 5.7% CAGR between 2025-2030.

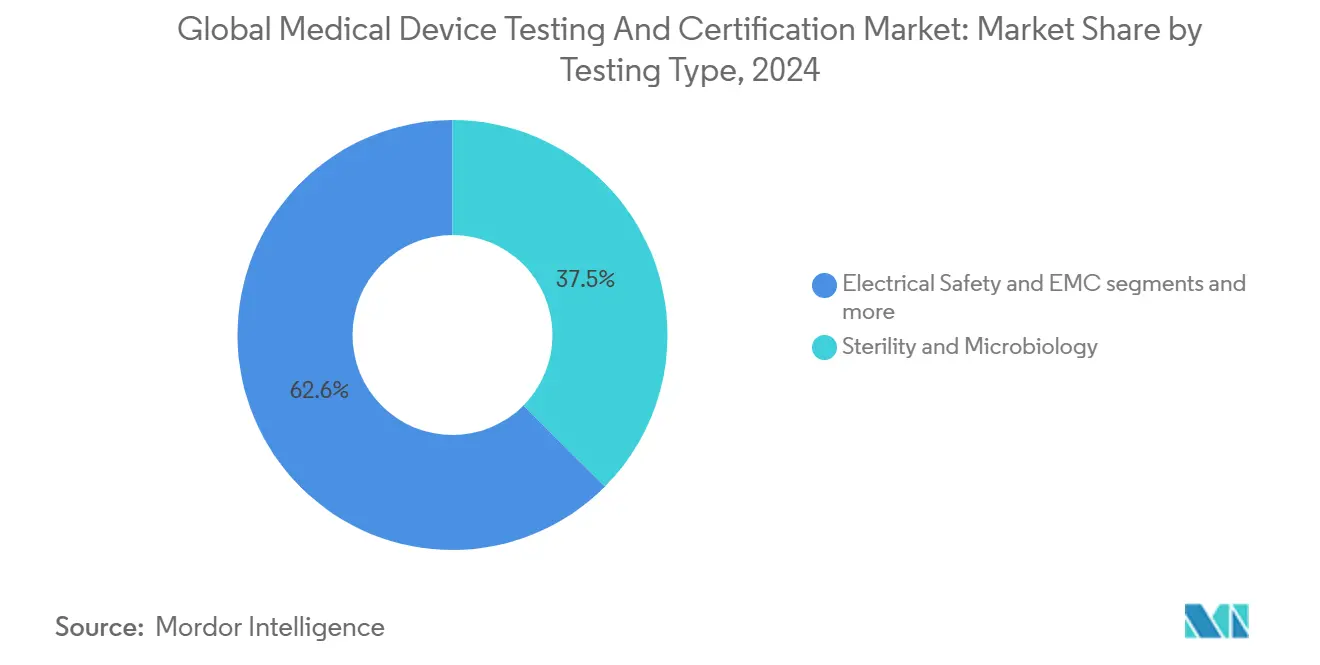

- By testing type – Sterility & microbiology commanded 37.45% share of the medical device testing & certification services market size in 2024; cybersecurity testing is the fastest-growing subsegment at 6.1% CAGR.

- By geography – North America held 38.95% revenue share in 2024, while Asia-Pacific is forecast to post the highest 6.7% CAGR through 2030.

Global Medical Device Testing And Certification Market Trends and Insights

Driver Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EU MDR and updated FDA Safer Devices Act requirements | +1.2% | EU & North America | Medium term (2-4 years) |

| Rapid uptake of AI/ML-enabled medical devices | +0.8% | North America & EU, expanding to Asia-Pacific | Long term (≥ 4 years) |

| Surge in home-use and wearable diagnostics | +0.6% | Global; strongest in North America & Asia-Pacific | Short term (≤ 2 years) |

| Mandatory pre-market cybersecurity submissions | +0.5% | North America, spill-over to EU | Short term (≤ 2 years) |

| Sustainability-linked procurement criteria | +0.3% | EU first, global roll-out | Long term (≥ 4 years) |

| Workforce upskilling certifications | +0.2% | Developed markets | Medium term (2-4 years) |

Source: Mordor Intelligence

Regulatory tightening under EU MDR and FDA Safer Devices Act

The 2024-2028 MDR transition window obliges every legacy device to re-seek CE marking under 23 General Safety and Performance Requirements, tripling technical-file depth for many manufacturers ec.europa.eu. Concurrently, Section 524B of the Safer Devices Act mandates U.S. pre-market submissions that include Software Bills of Materials and vulnerability management plans, expanding documentation for every connected product. The combined effect triggered a 40% surge in notified-body applications and elongated average review times beyond 24 months, prompting firms to outsource larger validation packages to accredited laboratories.

Rise in AI/ML-enabled devices driving specialized validation needs

The FDA’s public database recorded 882 cleared AI/ML medical devices by May 2024, up 45% year-on-year. Each algorithm demands bias detection, dataset shift analysis, and real-world performance monitoring, tests that exceed classical verification. The EU AI Act, classifying medical AI as “high risk”, further requires lifecycle risk management. Laboratories offering algorithm audit services therefore command premium pricing, and this service line is forecast to become a core revenue pillar of the medical device testing & certification services market over the coming decade.

Growth of home & wearable diagnostics expanding test volumes

Pandemic-era consumer familiarity with rapid antigen kits accelerated adoption of connected glucometers, ECG patches, and multi-analyte wearables. Regulators now insist on usability and human-factor evidence collected outside clinical settings, pushing up test unit counts by nearly 30% annually for high-volume consumer devices. Laboratories capable of running distributed user studies and environmental stress simulations attract continuous business from brands seeking fast global roll-outs, bolstering the medical device testing & certification services market.

Mandatory cybersecurity pre-market submissions

Since October 2023 the FDA refuses 510(k) filings lacking secure-by-design documentation, and connected devices launched without a vulnerability disclosure policy risk import detention. UL 2900 certification pathways have become the de facto benchmark ul.com. Testing houses that invested early in penetration-testing benches report project pipelines filled out to mid-2026, affirming cybersecurity as the fastest-growing revenue niche within the medical device testing & certification services market.

Restraint Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited capacity & long lead times at Notified Bodies | -0.9% | EU primarily, with global spill-over effects | Short term (≤ 2 years) |

| High testing costs for SMEs & start-ups | -0.6% | Global, with emerging markets most affected | Medium term (2-4 years) |

| Scarcity of standardized datasets for AI algorithm validation | -0.4% | Global, with North America & EU leading AI adoption | Long term (≥ 4 years) |

| Fragmented sustainability compliance requirements | -0.3% | Global, with EU and North America prioritized | Medium term (2-4 years) |

Source: Mordor Intelligence

Limited capacity & long lead times at notified bodies

Only 43 notified bodies serve the entire EU under MDR, and application-to-certification ratios exceed 4:1. Average review times rose from 14 months in 2022 to more than 26 months by late-2024. Manufacturers have consequently withdrawn certain low-margin products from the EU, shrinking potential testing volumes and tempering growth in the medical device testing & certification services market.

High testing costs for SMEs & start-ups

Comprehensive biocompatibility, sterility, EMC, and cybersecurity packages push even basic Class II validation bills above USD 500,000, a level that strains venture-backed start-ups. Though the FDA offers reduced 510(k) fees to small businesses, those savings cover only submission costs, not laboratory work. Many SMEs defer launches or pivot to markets with lighter regulations, reducing immediate service demand.

Segment Analysis

By Service Type: Testing services remain foundational while cybersecurity accelerates

Testing services held 56.56% of medical device testing & certification services market share in 2024, reflecting their status as the unavoidable regulatory entry ticket for all device classes. Certification services track behind because only EU and UK routes legally require third-party auditing, whereas the U.S. relies more on manufacturer self-attestation. However, as regulators intensify post-market surveillance, inspection & auditing revenues are gaining momentum. Cybersecurity and software validation—still statistically nested within testing services—represent the fastest revenue stream, posting 5.2% CAGR on account of the FDA and Health Canada mandates. Laboratories that integrate biological, mechanical, and digital-security benches in one location cut total turn-around time by up to 30%, enabling premium billing and reinforcing competitive moat. Consequently, the medical device testing & certification services market is shifting toward bundled, subscription-like quality-assurance contracts that lock in multi-year revenue visibility.

Continued investments in automated sample preparation and high-throughput analytics have trimmed direct labor per report by nearly 10% since 2022, raising operating margins. Certification services, hampered by notified-body scarcity, are forecast to grow at a slower 2.5% but remain indispensable for EU market access, sustaining a defensive revenue floor.

By Device Class: Complexity sweet-spot keeps Class II dominant

Class II devices accounted for 43.34% of the medical device testing & certification services market size in 2024 because they balance high unit volumes with stringent evidence requirements. Examples include infusion pumps, powered wheelchairs, and many AI-enabled imaging devices. Under the FDA Predetermined Change Control Plan, developers can revise algorithms without submitting a new 510(k) provided they validate performance boundaries, effectively locking in recurring test spend every time a model updates. Class III devices, though smaller in number, deliver premium fees due to mandatory clinical evidence and sterility assurance levels of 10^−6. Class I volumes continue to migrate toward in-house self-testing, yet the cybersecurity clause is pulling some connected devices into third-party labs. In Vitro Diagnostics (IVDs) remain a distinct growth pocket after the EU IVDR extended transitional deadlines to 2028, sustaining elevated certification backlogs.

Overall, rising software content in mid-risk products keeps the medical device testing & certification services market firmly anchored in the Class II space.

By Testing Type: Sterility maintains scale; cybersecurity drives momentum

Sterility & microbiology testing maintained 37.45% revenue share in 2024, supported by universal applicability across implants, disposables, and combination products. ISO 11737 updates on rapid microbial methods encourage labs to invest in PCR-based platforms that cut time-to-certificate by 2-3 days. Parallelly, cybersecurity testing recorded the most robust growth at 6.1% CAGR, reflecting the legislated pivot toward digitally connected devices. Electrical safety and electromagnetic compatibility (EMC) preserve relevance because 100% of new devices integrate wireless components. Packaging & shelf-life assays enjoy tailwinds from eco-friendly materials that require fresh stability datasets.

Conversely, sterility testing rises at a slower 3.1% but still adds nearly USD 0.6 billion in absolute terms over the forecast span. As laboratories cross-sell digital and microbiological services, average project value increases, improving order book resilience.

Note: Segment shares of all individual segments available upon report purchase

Geography Analysis

North America captured 38.95% of the medical device testing & certification services market in 2024, anchored by the FDA’s streamlined 510(k) and Breakthrough Device pathways that catalyze continuous product launches. Domestic laboratories benefit from deep payer systems that fund innovation and from a regulatory environment that explicitly recognizes several voluntary consensus standards, shortening validation cycles. From 2025-2030, the region is set to expand at 3.2% CAGR, slower than the global mean due to maturity.

Asia-Pacific is the clear volume engine, forecast to grow 6.7% annually. China’s updated Medical Device Regulation, effective July 2024, compels local producers to secure third-party biocompatibility and packaging data, driving steady sample inflows to regional labs. India’s Medical Device Rules amendment of 2024 extended third-party audit requirements to additional product categories, adding incremental demand. Foreign players are rapidly opening satellite laboratories in Suzhou, Bangalore, and Kuala Lumpur to capture the rising tide.

Europe suffered near-term drag from notified-body scarcity; however, once capacity normalizes, deferred applications will convert to billable tests, helping the region regain momentum beyond 2027. Latin America and the Middle East & Africa remain nascent but benefit from harmonization initiatives, which require proof of compliance with reference-market standards—typically executed by global lab networks.

Competitive Landscape

The competitive landscape exhibits moderate concentration, with the key providers—SGS SA, Intertek Group plc, Eurofins Scientific SE, TÜV SÜD, and UL Solutions. These firms leverage broad accreditation portfolios spanning ISO/IEC 17025, ISO 13485, and multiple regulatory authority recognitions to win multi-territory contracts. SGS expanded U.S. bioanalytical testing in January 2025 by partnering with Agilex Biolabs, strengthening its end-to-end pre-clinical through post-market proposition[1]Source: SGS, "Outstanding US FDA Inspection Solidifies Position as a Leader in Pharmaceutical Testing in China," SGS, sgs.com.

Intertek, TÜV SÜD, and UL Solutions are deploying automated laboratory management systems that cut data-entry errors and accelerate report generation, securing repeat business with multinational device makers seeking digital traceability. Eurofins deepened its medical portfolio via the December 2024 acquisition of Infinity Laboratories, adding eight U.S. facilities specialized in microbiology and package testing[2]Source: Eurofins Scientific, “Infinity Laboratories Acquisition,” eurofins.com . A wave of mid-tier consolidations—Applus+ buying Keystone Compliance and Apave acquiring Baltic Control—signal continued drive for scale to balance rising compliance overheads and to widen geographic coverage.

Niche specialists such as Nelson Labs, BSI Group, and Element Materials Technology maintain stronghold positions in biocompatibility, certification, and EMC respectively. They defend share through deep technical expertise, faster time-to-schedule, and proximity to innovation hubs. However, lab automation and AI-enhanced analytics are narrowing capability gaps, permitting larger rivals to encroach on specialty territories. Price competition remains muted because regulatory complexity and capacity bottlenecks support premium billing, yet customers increasingly favor multi-year framework agreements that bundle tests across product lifecycles to lock in discounts.

Global Medical Device Testing And Certification Industry Leaders

-

Eurofins Scientific

-

SGS SA

-

TÜV SÜD

-

British Standards Institution

-

Intertek Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: NAMSA and Terumo formed a global outsourcing partnership to accelerate regulatory approval of Terumo’s cardiovascular and endovascular devices, covering clinical, testing, and consulting services.

- January 2025: SGS launched specialized bioanalytical services in North America via collaboration with Agilex Biolabs, enhancing discovery through phase 3 support for device-drug combination products.

- December 2024: Eurofins Scientific acquired Infinity Laboratories, adding eight U.S. labs focused on microbiology, chemistry, and packaging tests for medical devices

Global Medical Device Testing And Certification Market Report Scope

As per the scope of the report, medical device testing, certification, and auditing are necessary to ensure the safety of the devices. These testing and certification can be provided by the third party under the recognized auditing organization. The global medical device testing and certification market are segmented by service type (testing services, inspection services, and certification services), sourcing type (in-house and outsourced), device class (class I, class II, and class III), technology (active implant medical device, active medical device, non-active medical device, in vitro diagnostic medical device, ophthalmic medical device, orthopedic and dental medical device, and other technologies), and geography (North America, Europe, Asia Pacific, Middle East and Africa, and South America). The report also offers the market size and forecasts for 19 countries across the regions. The report offers the value (in USD million) for the above segments.

| By Service Type (Value) | Testing Services | ||

| Certification Services | |||

| Inspection & Auditing Services | |||

| Others | |||

| By Device Class (Value) | Class I | ||

| Class II | |||

| Class III | |||

| In Vitro Diagnostic Devices | |||

| By Testing Type (Value) | Biocompatibility Testing | ||

| Sterility & Microbiology Testing | |||

| Electrical Safety & EMC | |||

| Software & Cybersecurity Testing | |||

| Mechanical & Physical Testing | |||

| Packaging & Shelf-life Testing | |||

| By Geography (Value) | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Middle East and Africa | GCC | ||

| South Africa | |||

| Rest of Middle East and Africa | |||

| Testing Services |

| Certification Services |

| Inspection & Auditing Services |

| Others |

| Class I |

| Class II |

| Class III |

| In Vitro Diagnostic Devices |

| Biocompatibility Testing |

| Sterility & Microbiology Testing |

| Electrical Safety & EMC |

| Software & Cybersecurity Testing |

| Mechanical & Physical Testing |

| Packaging & Shelf-life Testing |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa |

Key Questions Answered in the Report

What is the current size of the medical device testing & certification services market?

The medical device testing & certification services market size reached USD 10.55 billion in 2025 and is projected to grow to USD 12.71 billion by 2030.

Which service segment holds the largest share?

Testing services, including biocompatibility, sterility, and cybersecurity assays, captured 56.56% of medical device testing & certification services market share in 2024.

Why are Class II devices the primary revenue driver?

Class II devices combine high production volumes with moderate-to-high regulatory evidence requirements, making them the core demand source for outsourced testing throughout the forecast period.

How will cybersecurity regulations influence market growth?

The FDA mandate for pre-market cybersecurity submissions and the widespread adoption of UL 2900 standards are fuelling a 6.1% CAGR for cybersecurity testing services through 2030, faster than any other test category.

Which region is expected to grow the fastest?

Asia-Pacific is set to record a 6.7% CAGR thanks to tighter regulatory frameworks in China and India that compel manufacturers to increase third-party test volumes.