Separation Systems For Commercial Biotechnology Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

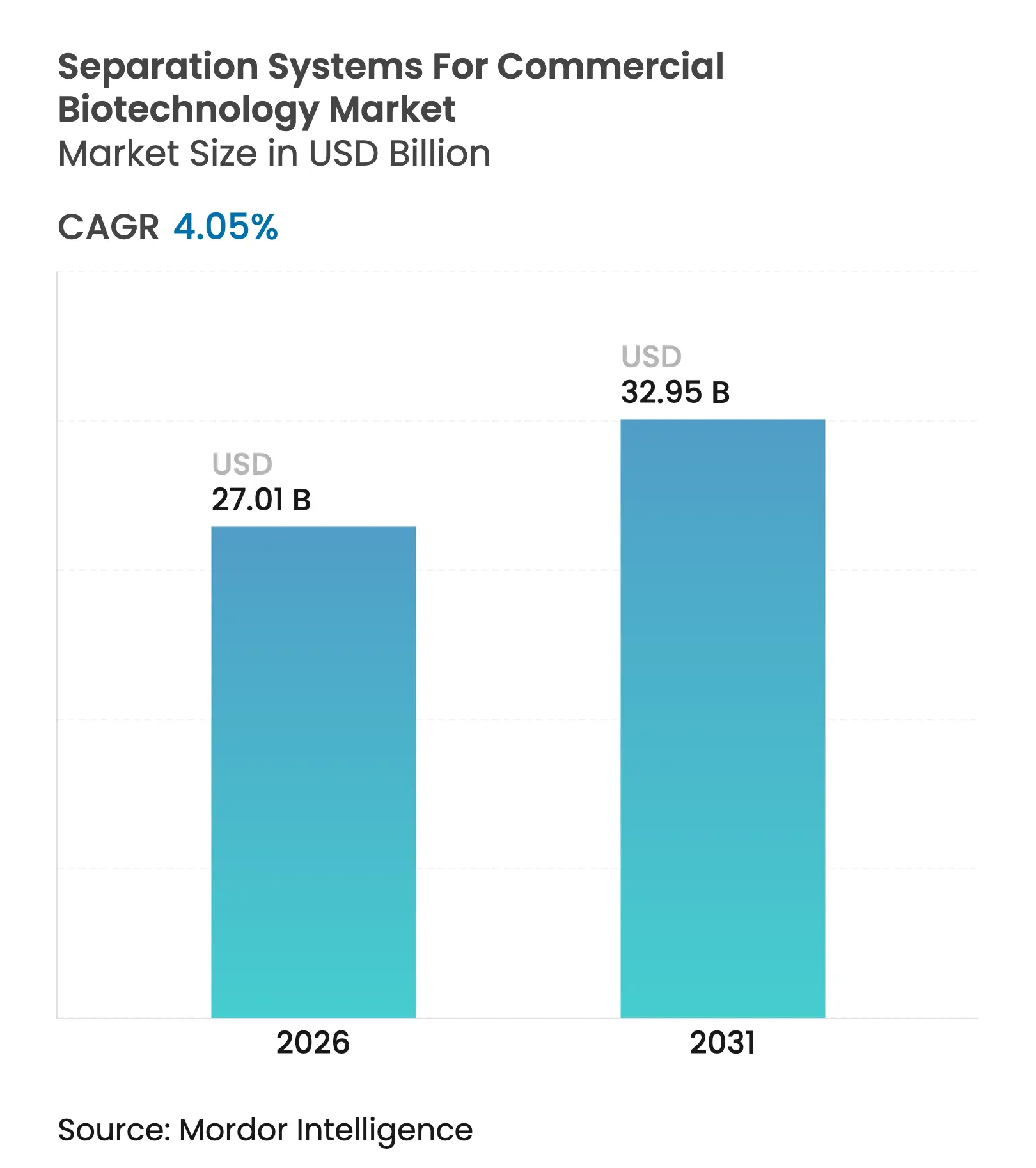

| Market Size (2026) | USD 27.01 Billion |

| Market Size (2031) | USD 32.95 Billion |

| Growth Rate (2026 - 2031) | 4.05 % CAGR |

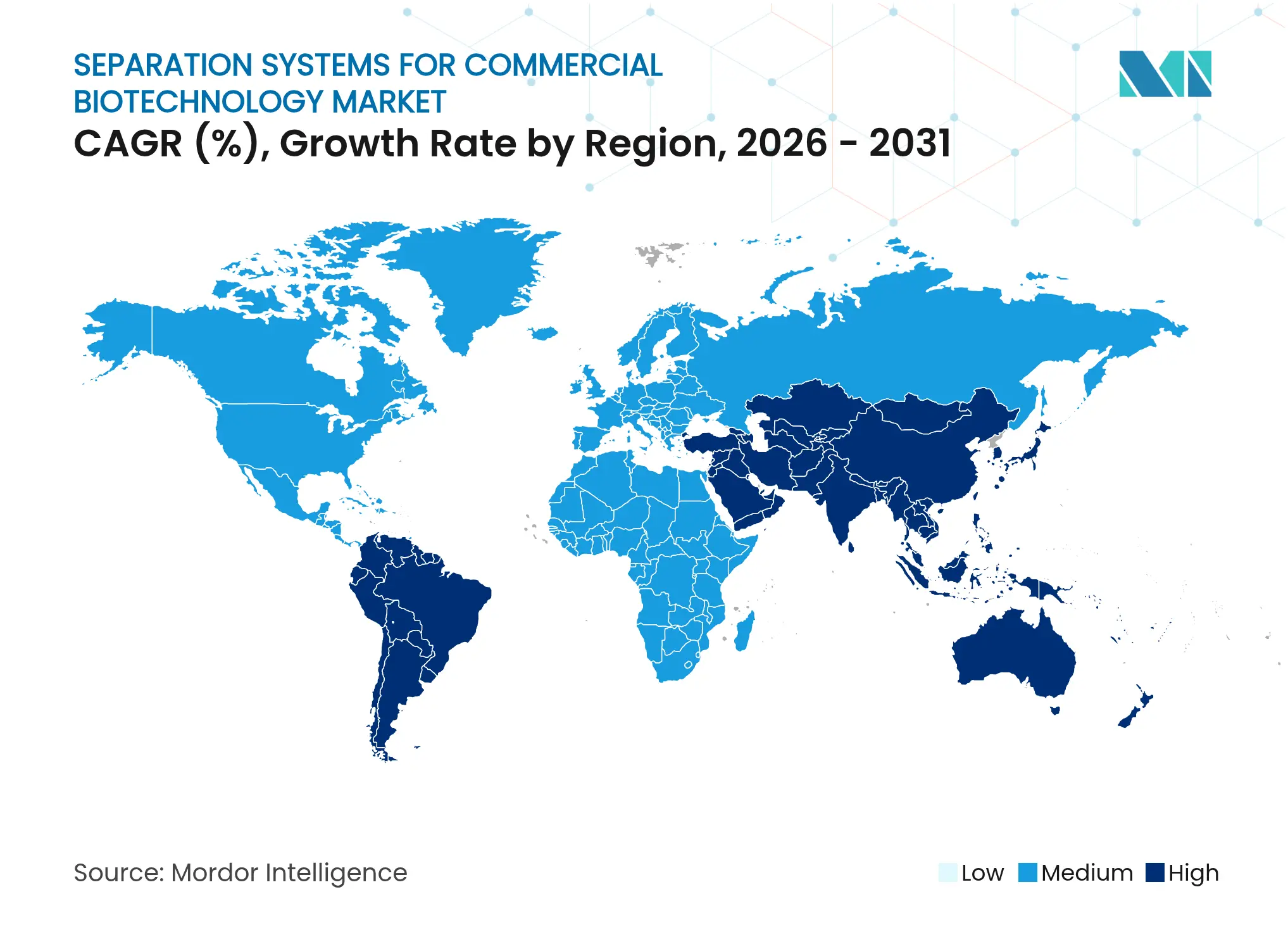

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

Separation Systems For Commercial Biotechnology Market Analysis by Mordor Intelligence

The separation systems for commercial biotechnology market size was valued at USD 25.96 billion in 2025 and estimated to grow from USD 27.01 billion in 2026 to reach USD 32.95 billion by 2031, at a CAGR of 4.05% during the forecast period (2026-2031). The growth trajectory reflects steady capacity expansions in biopharmaceutical manufacturing, even as laboratories adopt miniature, high-throughput devices that compress development cycles. Demand for flexible single-use equipment, rising volumes of viral-vector and mRNA products, and strong public-private funding for new biotech hubs are reshaping capital-allocation priorities. Competition is shifting from stand-alone chromatography columns toward integrated platforms that merge filtration, acoustic, and microfluidic modules, thereby lowering change-over times[1]Chinese Academy of Sciences, “Surprising ion transport behavior in nanofiltration membranes could reshape lithium recovery,” phys.org and enabling continuous downstream processing. Intensifying supplier consolidation, led by large multinationals purchasing niche technology firms, is widening the gap between full-line vendors and specialists focusing on discrete steps within the separation workflow.

Key Report Takeaways

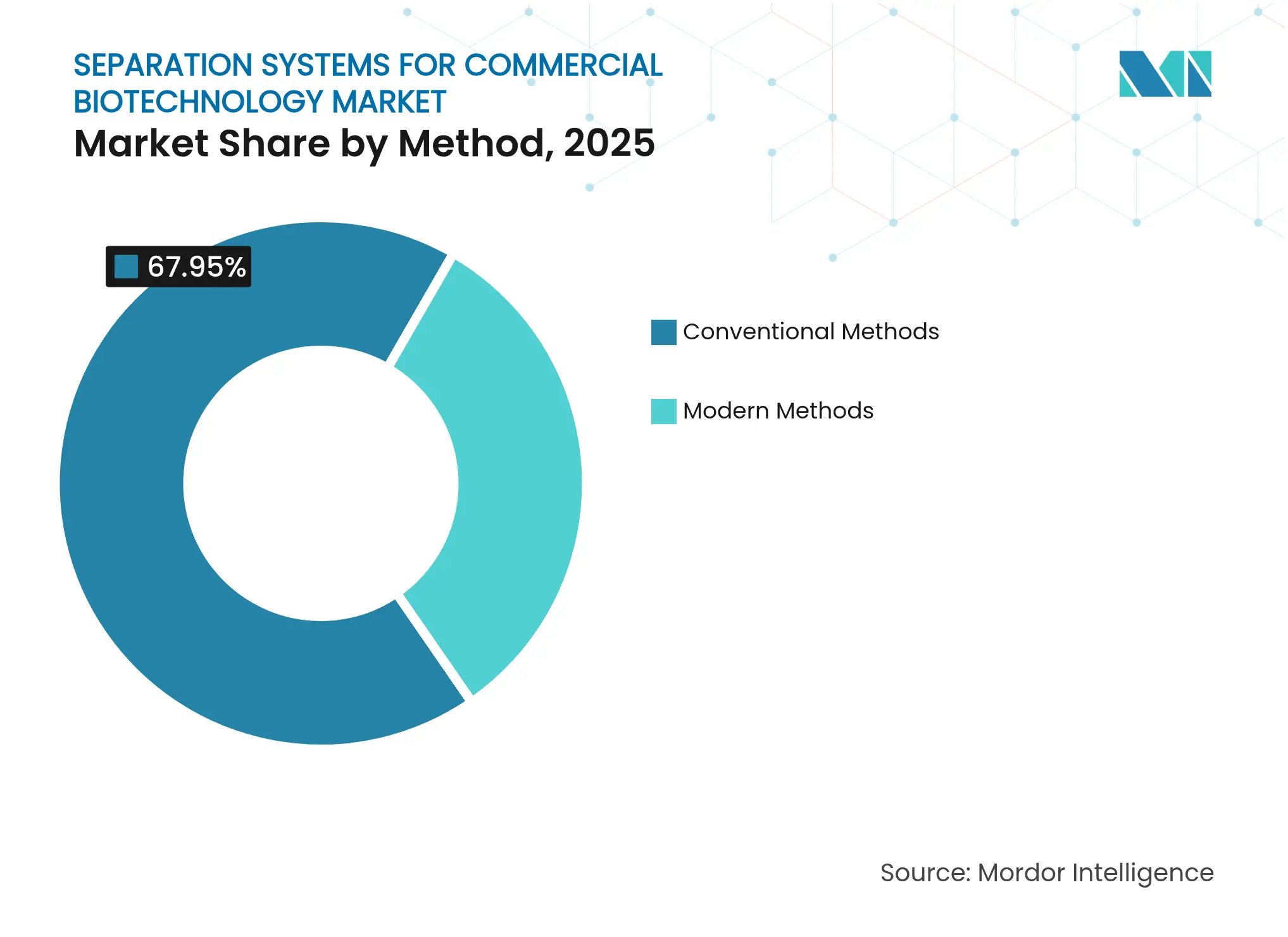

- By method, conventional technologies controlled 67.95% of the separation systems for commercial biotechnology market share in 2025, while modern alternatives are on track for a 7.02% CAGR to 2031.

- By scale, commercial-scale systems held 60.95% of the separation systems for commercial biotechnology market share in 2025; laboratory-scale equipment posts the fastest 6.05% CAGR through 2031.

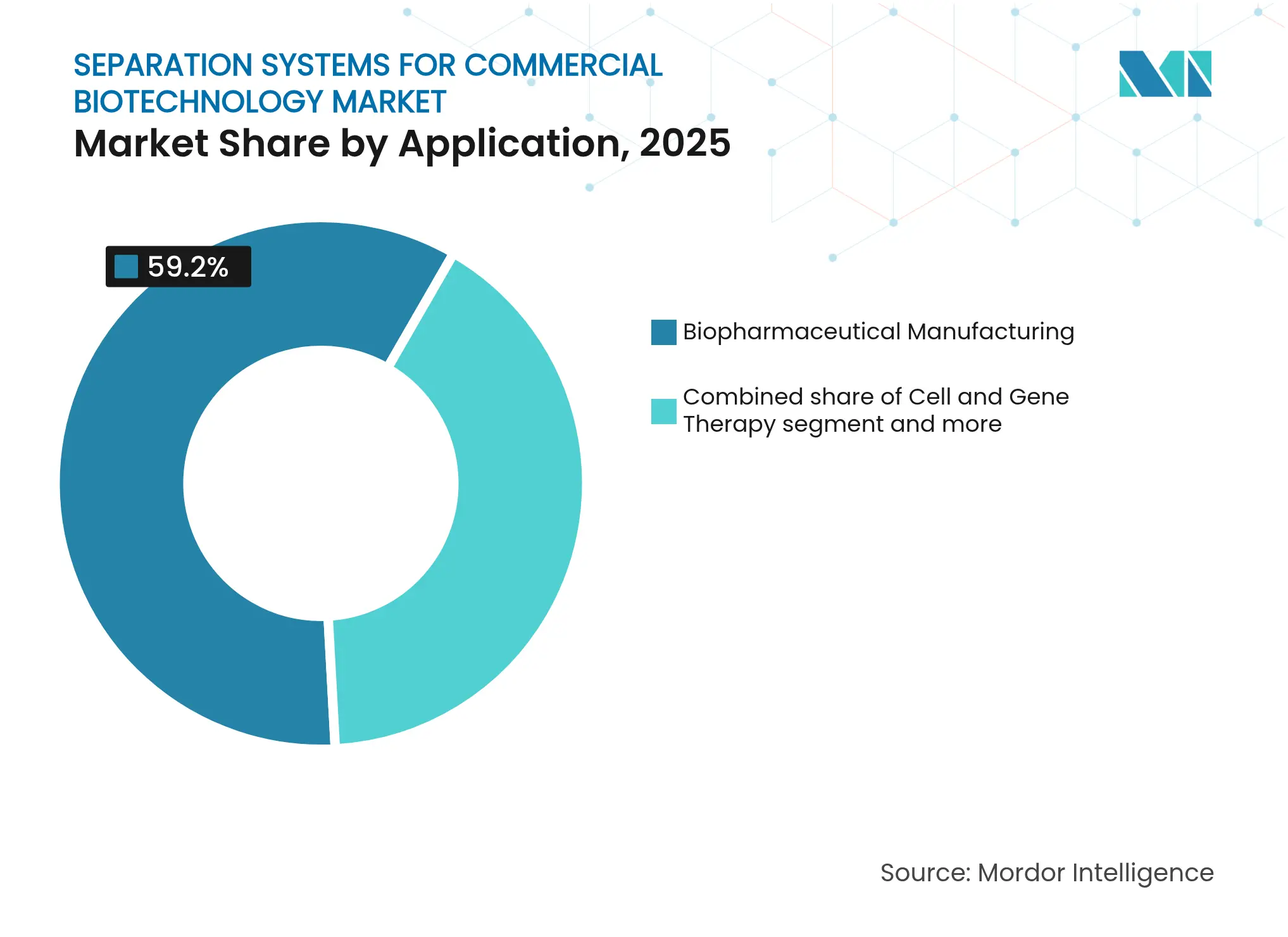

- By application, biopharmaceutical manufacturing accounted for 59.20% of the separation systems for commercial biotechnology market size in 2025, whereas cell and gene therapy is advancing at a 5.93% CAGR to 2031.

- By geography, North America maintained a 39.75% share in 2025; Asia-Pacific leads growth with a 5.48% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Separation Systems For Commercial Biotechnology Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Advances in High-Throughput Microfluidic Cell Sorting

Advances in High-Throughput Microfluidic Cell Sorting

| +1.2% | Global, early uptake in North America and EU | Medium term (2-4 years) |

(~) % Impact on CAGR Forecast

:

+1.2%

|

Geographic Relevance

:

Global, early uptake in North America and EU

|

Impact Timeline

:

Medium term (2-4 years)

|

Surging Demand for Viral-Vector & mRNA Therapies

Surging Demand for Viral-Vector & mRNA Therapies

| +1.1% | Global, focused on developed markets | Long term (≥ 4 years) | |||

AI-Driven Optimization of Chromatographic Workflows

AI-Driven Optimization of Chromatographic Workflows

| +0.9% | North America and EU core, expanding to Asia-Pacific | Medium term (2-4 years) | |||

Shift Toward Closed, Single-Use Downstream Platforms

Shift Toward Closed, Single-Use Downstream Platforms

| +0.8% | Global, strongest in regulated markets | Short term (≤ 2 years) | |||

Public–Private Funding Spikes for Biomanufacturing Hubs

Public–Private Funding Spikes for Biomanufacturing Hubs

| +0.7% | APAC core, spill-over to MEA | Long term (≥ 4 years) | |||

Growing Adoption of Membrane Adsorbers in Continuous

Processing

Growing Adoption of Membrane Adsorbers in Continuous

Processing

| +0.6% | Global, led by commercial-scale operations | Medium term (2-4 years) | |||

| Source: Mordor Intelligence | ||||||

Advances in High-Throughput Microfluidic Cell Sorting

Academic and corporate teams are miniaturizing flow paths so that acoustic or dielectrophoretic forces can sort individual cells without physical contact, eliminating shear damage that compromises viability. A University of Bristol group[2]University of Bristol, “Touchlessly moving cells: Biotech automation and an acoustically levitating diamond,” ScienceDaily, sciencedaily.com achieved automated manipulation of hundreds of cells per minute on a benchtop device, trimming drug-discovery timelines from months to weeks. Complementary Chinese work[3]Chinese Academy of Sciences, “Single-cell sorting platform accelerates discovery of high-value microbes from months to days,” phys.org demonstrated FlowRACS 3.0, which screened 250,000 microbial colonies in days rather than months. These breakthroughs reduce reagent consumption, accelerate clone selection, and ease scale translation, thereby improving return on investment for early-stage biologics programs. As platform vendors integrate such chips into modular skids, the separation systems for the commercial biotechnology market broaden beyond traditional column hardware.

Surging Demand for Viral-Vector & mRNA Therapies

Dozens of gene-replacement and RNA vaccines that reached commercial or late-stage pipelines in 2025 require separation steps capable of preserving delicate capsids and strands. Manufacturers are turning to low-pressure membrane chromatography and acoustic focusing to maintain infectivity while achieving the 99.9% impurity clearance thresholds regulators now expect. Purpose-built filters, such as Planova FG1, prevent fouling that hampers conventional depth filters, providing shorter processing times and higher batch yields. Each new therapeutic approval adds bespoke downstream designs, creating durable pull for suppliers able to tailor media or membranes to specific particle sizes and charge profiles. The separation systems for commercial biotechnology market therefore enjoys a structural demand uplift linked to the expanding licensed indications for advanced modalities.

AI-Driven Optimization of Chromatographic Workflows

Machine-learning engines ingest historical purification runs to predict optimal buffer gradients, temperature settings, and load densities. A Chinese research consortium validated an algorithm[4]Chinese Academy of Sciences, “Machine learning modeling assists intelligent process analysis for high-performance virus filtration,” phys.org trained on more than 900 virus-filtration datasets that improved yield consistency while cutting experimental iterations in half. Vendors now bundle inline spectroscopy probes with predictive software, turning batch purification into a closed-loop operation that adjusts in real time. This data-centric approach reduces resin use, curtails labor, and lowers failure risk, making it especially attractive to contract development and manufacturing organizations running numerous product changeovers. Widespread AI adoption is set to recalibrate performance baselines across the separation systems for commercial biotechnology market.

Shift Toward Closed, Single-Use Downstream Platforms

Disposables minimize cross-contamination risk and shorten validation cycles, aligning with regulators’ heightened scrutiny of multiproduct facilities. Polymeric membranes embedded in pre-sterilized cassettes now deliver binding capacities once exclusive to packed-bed resins, while remote sensor arrays verify integrity during operation. Launches such as the Purexa OdT mRNA affinity membrane show how suppliers combine specialty chemistries with plug-and-play housing suited to disposable flow paths. Momentum for single-use formats is strongest in small-volume, high-value products, yet pilot facilities are also swapping stainless steel for film-lined tanks to avoid costly cleaning downtime. As users recalibrate process economics, spending shifts away from fixed assets toward a recurring consumables model, reshaping revenue streams across the separation systems for commercial biotechnology market.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Capital-Intensive GMP Infrastructure Requirements

Capital-Intensive GMP Infrastructure Requirements

| -1.0% | Global, most severe in emerging markets | Long term (≥ 4 years) |

(~) % Impact on CAGR Forecast

:

-1.0%

|

Geographic Relevance

:

Global, most severe in emerging markets

|

Impact Timeline

:

Long term (≥ 4 years)

|

Regulatory Uncertainty for Novel Separation Consumables

Regulatory Uncertainty for Novel Separation Consumables

| -0.8% | Global, concentrated in highly regulated markets | Medium term (2-4 years) | |||

Skilled-Labor Shortages in Bioprocess Engineering

Skilled-Labor Shortages in Bioprocess Engineering

| -0.5% | Global, acute in North America and EU | Medium term (2-4 years) | |||

Supply-Chain Volatility for Specialty Resin Raw Materials

Supply-Chain Volatility for Specialty Resin Raw Materials

| -0.5% | Global, high impact on chromatography lines | Short term (≤ 2 years) | |||

| Source: Mordor Intelligence | ||||||

Capital-Intensive GMP Infrastructure Requirements

Good Manufacturing Practice updates introduced in 2024 oblige firms to retrofit HVAC, data-logging, and clean-room areas before they can deploy unfamiliar separation formats. Multimillion-dollar validation packages can erode the margin advantage promised by next-generation devices, forcing many smaller sponsors to outsource instead of bringing capabilities in-house. The resulting procurement hesitation slows technology circulation in cost-sensitive regions and tempers volume gains otherwise expected for the separation systems for commercial biotechnology market.

Regulatory Uncertainty for Novel Separation Consumables

Guidelines still revolve around silica resins and depth filters, leaving biomimetic membranes and adaptive algorithms in a grey zone. Sponsors, therefore, maintain duplicate workflows that pair new media with legacy columns until authorities publish clear comparability criteria. The duplicated expenditure dilutes immediate savings and postpones complete conversion to higher-performance materials, tempering near-term revenue gains for emerging suppliers.

Segment Analysis

By Method: Conventional Dominance Faces Modern Disruption

Conventional column chromatography, centrifugation, and membrane filtration retained 67.95% command of the separation systems for the commercial biotechnology market size in 2025, thanks to entrenched validation files and global supply availability. This foundation supports dependable product release cycles and underpins most commercial-scale antibody and vaccine plants. Yet the modern cohort—including acoustic, magnetic, and microarray techniques—logs a 7.02% CAGR to 2031 as innovators prioritize contact-free manipulation and multiplex control. Early adopters have documented productivity lifts when acoustic devices handle fragile stem-cell batches where shear sensitivity is critical. Growing familiarity and falling chip costs should extend adoption beyond niche R&D toward mid-volume production. The convergence of old and new methods encourages hybrid skids that deploy microfluidics upstream of ion-exchange columns, reflecting pragmatic risk management while still capturing efficiency upside across the separation systems for the commercial biotechnology market.

The qualitative leap in control precision is matched by new analytics that track individual molecule trajectories. Users report sharper eluate peaks, trimming polishing steps, and freeing buffer capacity. Suppliers that provide universal automation layers across both conventional and emergent modules stand to win service contracts and software licenses. As the regulatory path clears, modern methods are expected to chip away at the conventional base, yet co-existence will remain the norm for the next decade.

Note: Segment shares of all individual segments available upon report purchase

By Scale: Commercial Operations Drive Volume, Laboratory Innovation Accelerates

Commercial facilities consumed 60.95% of the separation systems for commercial biotechnology market share in 2025, reflecting bulk demand for monoclonal antibodies and recombinant proteins. Their purchasing criteria include uptime, global part availability, and audit traceability, steering them toward established OEMs and field-proven column hardware. Pilot-scale suites bridge discovery and production, optimizing parameters without full-scale financial risk, while benchtop units facilitate design-of-experiment campaigns. Laboratory-scale platforms post the swiftest 6.05% CAGR because universities and start-ups favor microfluidic and acoustic units that can process small volumes at high speed.

A vibrant feedback loop exists: proof-of-concept wins in academia often drive pilot-scale retrofits, which, once de-risked, migrate into whole plants. FlowRACS 3.0 illustrates this arc, evolving from a screening aid into a feeder step for fed-batch fermentation lines. Consequently, laboratory innovations shape the technology road map for the entire separation systems for commercial biotechnology market.

By Application: Biopharmaceuticals Lead, Cell Therapy Surges

The biopharmaceutical block commanded 59.20% of the separation systems for commercial biotechnology market size in 2025, anchored by large-volume antibody and vaccine campaigns that hinge on robust, regulation-ready separation stacks. Food, beverage, and cosmetic biotech add steady but modest volumes. Agricultural and environmental uses are rising on the back of sustainability commitments that treat waste streams as sources of valuable proteins or enzymes. Cell and gene therapy, however, records the fastest 5.93% CAGR as approvals accelerate for CAR-T, AAV, and lipid-nanoparticle formulations.

Ultragentle handling is mandatory in these modalities. Manufacturers are substituting membrane adsorbers and low-shear acoustic settlers for centrifuges to retain vector potency, stretching column lifetimes and cutting post-polish filtration. Diagnostics and research consumables bring extra demand volatility yet also open opportunities for rapid-change systems, further broadening revenue sources for the separation systems for commercial biotechnology market.

Note: Segment shares of all individual segments available upon report purchase

Geography Analysis

North America preserved a 39.75% of the separation systems for commercial biotechnology market share in 2025, fueled by grant funding for advanced therapeutics and M&A activity that bundles separation hardware with informatics services. Skilled workforces and established quality systems help the region absorb disruptive devices quickly. However, rising wage costs and labor shortages induce plants to automate buffer preparation and resin packing, which sustains spending on digital control layers.

Europe remains sizable yet mature. Stringent environmental targets motivate energy-efficient membrane operations and waste-reduction projects. Regional manufacturers value conformity and long-term service contracts, both offered by incumbents skilled at navigating diverse regulatory processes. Sustainability credentials are becoming tender differentiators, favoring suppliers able to document carbon-footprint reductions.

Asia-Pacific expands at a 5.48% CAGR through 2031, buoyed by multibillion-dollar life-science parks in China and India and realignment of supply chains following pandemic-era disruptions. Governments subsidize pilot plants and shared analytical facilities that help domestic firms reach global quality benchmarks. Japan and South Korea focus on regenerative medicine and high-purity intermediates, while Southeast Asia positions itself for contract vaccine fill-finish. The pace and diversity of projects in the region guarantee that the separation systems for the commercial biotechnology market find their most dynamic demand center east of the Suez Canal.

Competitive Landscape

Market Concentration

Industry structure remains moderately fragmented. Full-line providers, including Thermo Fisher Scientific, Danaher, and Sartorius, leverage end-to-end offerings that cover buffers, skids, and analytics. Their balance sheets let them swallow niche innovators, as seen in Thermo Fisher’s USD 4.1 billion acquisition of a purification business, which broadens its installed base in continuous chromatography. Yet specialist players flourish by targeting high-growth corners such as acoustic focusing or membrane adsorbers. Patents for low-pressure virus removal membranes and tunable acoustic chambers tripled between 2023 and 2025, revealing an innovation race stretching across continents.

Strategic partnerships between hardware makers and software firms multiply as AI-oriented control systems move from pilot to production. Vendors now pitch combined sensor-analytics packages that guarantee real-time release, cutting batch hold times. Hybrid offerings raise switching costs for clients and can lock in multiyear consumable contracts. Pricing tension persists in commodity filtration where local assemblers undercut global brands, but premium margins remain defendable for consumables certified for gene-therapy use.

Sustainability considerations add a new competitive vector. Suppliers trial bio-based membrane materials and recyclable chromatography housings compatible with waste-sorting streams. Equipment scope-3 emissions disclosures are becoming more detailed, and buyers weigh them during capital planning. Responding early grants a reputational advantage, while laggards risk exclusion from major tender lists. Consequently, environmental metrics now sit alongside yield and cost when customers compare bids within the separation systems for the commercial biotechnology market.

Separation Systems For Commercial Biotechnology Industry Leaders

*Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Researchers at the University of Hong Kong unveiled silk-based nanofiltration membranes that purify water 10 times faster than existing products using less than 1 bar pressure, pointing to low-energy routes for biotech separations.

- June 2025: Chinese Academy of Sciences scientists published a machine-learning framework that optimizes virus-filtration parameters by mining over 900 datasets, replacing trial-and-error screening.

- April 2025: A University of Bristol spin-out presented an acoustic wave platform that automates cell manipulation, shrinking equipment footprints while speeding drug-discovery cycles.

- January 2025: Bio-Rad Laboratories introduced Nuvia wPrime 2A resin targeting biomolecule purification workflows that demand higher selectivity and throughput.

Table of Contents for Separation Systems For Commercial Biotechnology Industry Report

1. Introduction

- 1.1Study Assumptions & Market Definition

- 1.2Scope of the Study

2. Research Methodology

3. Executive Summary

4. Market Landscape

- 4.1Market Overview

- 4.2Market Drivers

- 4.2.1Advances in High-Throughput Microfluidic Cell Sorting

- 4.2.2Surging Demand for Viral-Vector & mRNA Therapies

- 4.2.3AI-Driven Optimization of Chromatographic Workflows

- 4.2.4Shift Toward Closed, Single-Use Downstream Platforms

- 4.2.5Public-Private Funding Spikes for Biomanufacturing Hubs

- 4.2.6Growing Adoption of Membrane Adsorbers in Continuous Processing

- 4.3Market Restraints

- 4.3.1Capital-Intensive GMP Infrastructure Requirements

- 4.3.2Regulatory Uncertainty for Novel Separation Consumables

- 4.3.3Skilled-Labor Shortages in Bioprocess Engineering

- 4.3.4Supply-Chain Volatility for Specialty Resin Raw Materials

- 4.4Supply Chain Analysis

- 4.5Technological Outlook

- 4.6Porter's Five Forces Analysis

- 4.6.1Threat of New Entrants

- 4.6.2Bargaining Power of Buyers

- 4.6.3Bargaining Power of Suppliers

- 4.6.4Threat of Substitutes

- 4.6.5Intensity of Competitive Rivalry

5. Market Size & Growth Forecasts (Value)

- 5.1By Method

- 5.1.1Modern Methods

- 5.1.1.1Microarray

- 5.1.1.2Lab-on-a-chip

- 5.1.1.3Magnetic Separation

- 5.1.1.4Acoustic & Dielectrophoretic Separation

- 5.1.1.5Other Modern Methods

- 5.1.2Conventional Methods

- 5.1.2.1Chromatography

- 5.1.2.2Flow Cytometry

- 5.1.2.3Membrane Filtration

- 5.1.2.4Centrifugation

- 5.1.2.5Other Conventional Methods

- 5.2By Scale

- 5.2.1Laboratory-scale

- 5.2.2Pilot-scale

- 5.2.3Commercial-scale

- 5.3By Application

- 5.3.1Biopharmaceutical Manufacturing

- 5.3.2Cell & Gene Therapy

- 5.3.3Food, Beverage & Cosmetics Biotechnology

- 5.3.4Agriculture & Environmental Biotechnology

- 5.3.5Diagnostics & Research

- 5.4By Geography

- 5.4.1North America

- 5.4.1.1United States

- 5.4.1.2Canada

- 5.4.1.3Mexico

- 5.4.2Europe

- 5.4.2.1Germany

- 5.4.2.2United Kingdom

- 5.4.2.3France

- 5.4.2.4Italy

- 5.4.2.5Spain

- 5.4.2.6Rest of Europe

- 5.4.3Asia-Pacific

- 5.4.3.1China

- 5.4.3.2India

- 5.4.3.3Japan

- 5.4.3.4Australia

- 5.4.3.5South Korea

- 5.4.3.6Rest of Asia-Pacific

- 5.4.4Middle East and Africa

- 5.4.4.1GCC

- 5.4.4.2South Africa

- 5.4.4.3Rest of Middle East and Africa

- 5.4.5South America

- 5.4.5.1Brazil

- 5.4.5.2Argentina

- 5.4.5.3Rest of South America

6. Competitive Landscape

- 6.1Market Concentration

- 6.2Competitive Benchmarking

- 6.3Market Share Analysis

- 6.4Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1Agilent Technologies, Inc.

- 6.4.2Alfa Laval AB

- 6.4.3Asahi Kasei Medical Co., Ltd.

- 6.4.4Astrea Bioseparations Limited

- 6.4.5Becton, Dickinson and Company

- 6.4.6bioMérieux SA

- 6.4.7Bio-Rad Laboratories, Inc.

- 6.4.8Corning Incorporated

- 6.4.9Danaher Corporation

- 6.4.10GE HealthCare Technologies Inc.

- 6.4.11Merck KGaA

- 6.4.12Miltenyi Biotec, Inc.

- 6.4.13Novasep Holding SAS

- 6.4.14Repligen Corporation

- 6.4.15Revvity Inc.

- 6.4.16Sartorius AG

- 6.4.17Shimadzu Corporation

- 6.4.18Terumo Corporation

- 6.4.19Thermo Fisher Scientific Inc.

- 6.4.20W. R. Grace & Co.

7. Market Opportunities & Future Outlook

- 7.1White-space & Unmet-Need Assessment

Global Separation Systems For Commercial Biotechnology Market Report Scope

Separation systems purify biological products such as biopharmaceuticals, biochemicals, and diagnostic reagents depending on the electrostatic charge, density, diffusivity, shape, polarity, solubility, and volatility characteristics. The equipment that separates biological material from complex mixtures or solutions includes chromatography, membranes or filters, and centrifuges.

The separation systems for the commercial biotechnology market are segmented by method, application, and geography. By method, the market is segmented into modern methods and conventional methods. By application, the market is segmented as biopharmaceutical, food and cosmetics, agriculture, and other applications. By geography, the market is segmented as North America, Europe, Asia-Pacific, Middle East and Africa, and South America. The report also covers the estimated market sizes and trends for 17 countries across the major regions globally.

The report offers the value (USD) for all the above segments.