Clot Management Devices Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

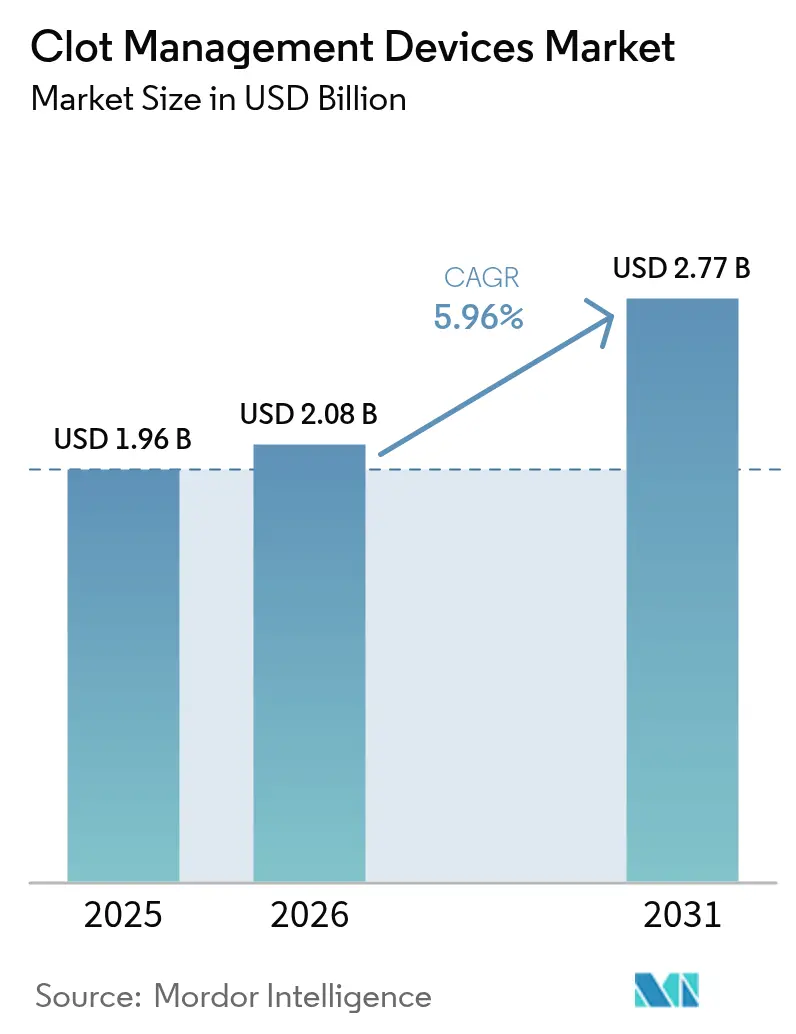

| Market Size (2026) | USD 2.08 Billion |

| Market Size (2031) | USD 2.77 Billion |

| Growth Rate (2026 - 2031) | 5.96% CAGR |

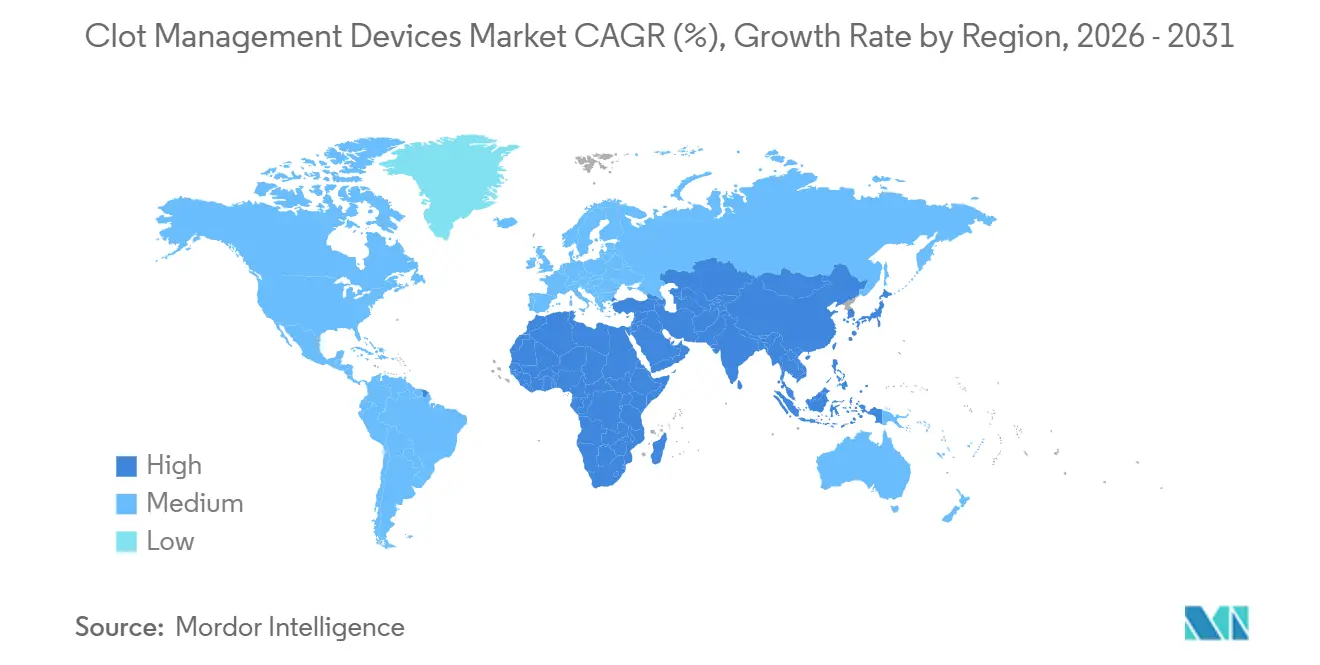

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Clot Management Devices Market Analysis by Mordor Intelligence

The Clot Management Devices Market size is projected to expand from USD 1.96 billion in 2025 and USD 2.08 billion in 2026 to USD 2.77 billion by 2031, registering a CAGR of 5.96% between 2026 to 2031.

Demand is being driven by three key factors: an aging global population is increasing ischemic stroke cases to 11.9 million annually. Landmark clinical trials, such as SELECT2 and ANGEL-ASPECT, have expanded the treatment window for mechanical thrombectomy to 24 hours post-symptom onset. Furthermore, the Asia-Pacific region is witnessing rapid growth in stroke centers, with China alone housing over 300 comprehensive facilities. While the venous-thromboembolism device segment faces slower growth due to direct oral anticoagulants eroding filter and thrombolysis revenues, neurovascular embolectomy platforms are outperforming the broader clot management devices market. These platforms are projected to grow at a 7.54% CAGR, driven by first-pass recanalization rates exceeding 40% in real-world registries. Competitive dynamics intensified in early 2026 when Boston Scientific acquired Penumbra for USD 14.5 billion, signaling a strategic shift toward a “buy-not-build” approach among established players. Meanwhile, ambulatory surgical centers (ASCs) are emerging as competitive service providers, supported by Medicare's 46% payment differential favoring ASCs over hospital outpatient departments, which is reshaping procedure economics.

Key Report Takeaways

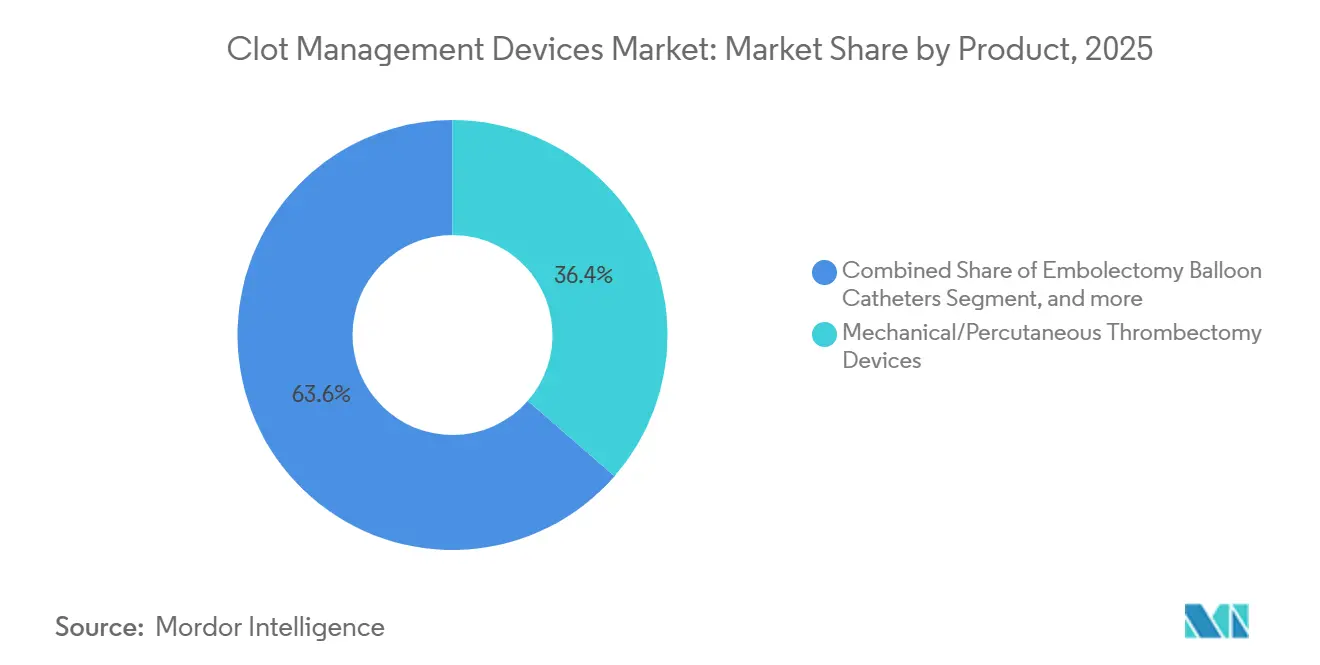

- By product category, neurovascular thrombectomy solutions captured 36.42% of 2025 revenue and are advancing at a 7.54% CAGR through 2031, while legacy inferior vena cava filters face contraction amid safety and retrieval-rate concerns.

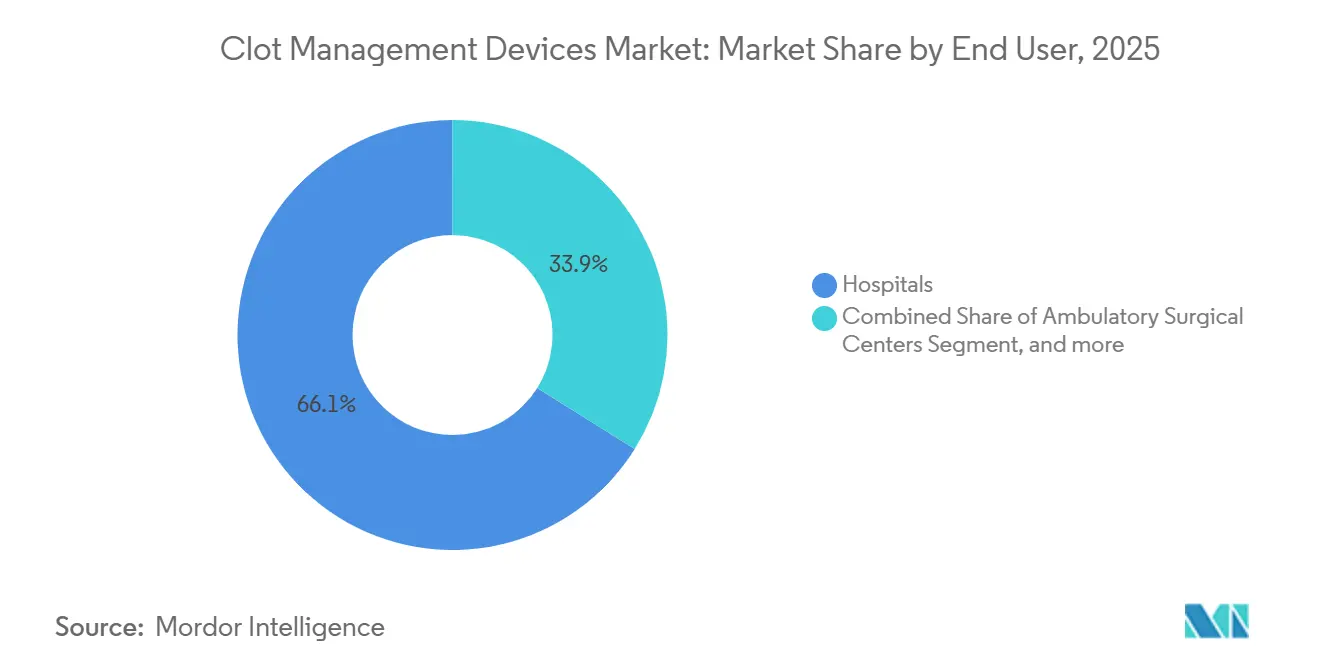

- By end user, hospitals accounted for 66.10% of 2025 spending, yet ASCs are the fastest-growing channel, with an 8.11% CAGR, as the number of cardiology-driven centers climbed from 55 in 2018 to 221 in 2023.

- By geography, North America accounted for 43.65% of 2025 revenue, while Asia-Pacific is on track for a 6.43% CAGR, reflecting aggressive network expansion in China, India, and Japan.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Clot Management Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating Global Burden Of Thromboembolic Disorders | +1.2% | Global, acute in aging OECD and urbanizing APAC markets | Long term (≥ 4 years) |

| Increasing Adoption Of Endovascular Therapies Over Open Surgery | +1.5% | North America and Europe lead; APAC catching up | Medium term (2-4 years) |

| Technological Advancements In Mechanical Thrombectomy Platforms | +1.0% | Global, R&D centered in U.S. and Western Europe | Short term (≤ 2 years) |

| Expanding Reimbursement And Funding For Stroke And VTE Interventions | +0.8% | North America, Europe, select APAC nations | Medium term (2-4 years) |

| Growth Of Ambulatory And Outpatient Vascular Care Settings | +0.6% | United States, Western Europe, early-stage uptake in APAC | Medium term (2-4 years) |

| Rising Healthcare Investment In Emerging Markets | +0.5% | Latin America, Southeast Asia, Middle East & North Africa | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Escalating Global Burden of Thromboembolic Disorders

Ischemic stroke and venous thromboembolism now produce more than 12 million acute events every year, and stroke incidence rose 70% between 1990 and 2019 as populations aged and metabolic risk factors multiplied. The United States logs 900,000 venous-thromboembolism cases annually, yet mechanical thrombectomy reached only 8% of eligible large-vessel occlusions in 2021, leaving a vast untreated cohort. Rural communities compound the care gap because one-third of Americans live more than a 60-minute drive from a thrombectomy-capable center, pushing demand for hub-and-spoke telestroke networks that will expand procedure volume. China’s 300-plus comprehensive stroke centers still deliver far fewer thrombectomies per capita than the United States, a lag that is expected to narrow as trained neurointerventionalists proliferate and reimbursement aligns. Given that non-communicable diseases are forecast to account for 73% of global deaths by 2030, the driver’s influence endures regardless of short-term economic swings.

Increasing Adoption of Endovascular Therapies Over Open Surgery

Mechanical thrombectomy penetration in U.S. stroke admissions climbed from 0.75% in 2010 to 8.4% in 2021, chiefly because endovascular treatment avoids the morbidity and rehabilitation costs linked to open neurosurgical decompression. Health-economic analyses demonstrate net savings of USD 15,000-25,000 per patient when thrombectomy achieves successful recanalization within six hours. The Zoom System, cleared by the FDA in 2025, reduced the groin-puncture-to-reperfusion time to a median of 19 minutes, addressing concerns about procedural complexity in smaller hospitals. Radial-access techniques championed by Terumo now allow same-day discharge for select cases, further tilting hospitals toward catheter-based care. As operator training spreads through regional centers, endovascular volumes are forecast to rise worldwide over the medium term.

Technological Advancements in Mechanical Thrombectomy Platforms

The first-pass effect has become the proxy for clinical excellence, and hybrid aspiration-plus-stent technologies now deliver 40-48% first-pass recanalization, compared with 30-35% for single-modality systems. Penumbra’s Lightning Flash 2.0 and Stryker’s AXS Vecta 46 both feature larger-bore catheters that can evacuate clots more efficiently, while Medtronic’s updated Solitaire boosts radial force to lower fragmentation risk. Trackability improvements mean next-generation catheters traverse tortuous arches and carotids once accessible only via surgical cut-down, enlarging the addressable pool by up to 20%. Because 510(k) clearances for incremental upgrades average only 6-9 months, commercial adoption of each engineering refresh is nearly immediate. These rapid innovation cycles should continue to add momentum to the clot management devices market through at least 2028.

Expanding Reimbursement and Funding for Stroke and VTE Interventions

Medicare continues to reimburse mechanical thrombectomy at USD 20,000-30,000 per case, anchoring U.S. profitability. More importantly, bundled-payment pilots now tie hospital bonuses and penalties to 90-day functional outcomes, nudging administrators to ensure every eligible patient receives thrombectomy when algorithms predict benefit. Germany pays EUR 8,000-12,000 (USD 8,700-13,000) under its DRG scheme, whereas the U.K. is only now funding additional regional centers outside London, producing access gaps within the National Health Service. Asia-Pacific policies vary: Japan reimburses the full procedure but caps device price, China added thrombectomy to its national catalog in 2021, yet leaves provinces to execute, and India still leans on private insurance, limiting uptake outside tier-one cities. Because capital build-outs and staff training follow policy by one-to-two years, reimbursement remains a medium-horizon tailwind for the clot management devices industry.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent Regulatory And Clinical Evidence Requirements | -0.5% | North America and Europe under FDA & EU MDR regimes | Short term (≤ 2 years) |

| High Procedural And Device Costs In Cost-Constrained Systems | -0.7% | Southern Europe, Latin America, Southeast Asia | Long term (≥ 4 years) |

| Therapeutic Competition From Pharmacologic Anticoagulation And Thrombolysis | -0.4% | Global, strongest in high-income countries | Medium term (2-4 years) |

| Safety And Liability Concerns Related To Implantable Filters And Devices | -0.3% | North America and Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Stringent Regulatory and Clinical Evidence Requirements

The FDA’s 2024 guidance now requests head-to-head non-inferiority data versus predicates for neurovascular thrombectomy devices, boosting pivotal-trial budgets to USD 10-20 million and stretching timelines by two years[1]U.S. Food and Drug Administration, “Non-Clinical and Clinical Guidance for Neurothrombectomy Devices,” fda.gov. Europe’s simultaneous transition to the Medical Device Regulation triggered a wave of recertification demands, and limited notified-body capacity has already generated review backlogs of 12-18 months. Such hurdles disproportionately hurt start-ups, encouraging consolidation as majors buy cleared portfolios rather than pursue greenfield R&D. Boston Scientific’s purchase of Penumbra and Stryker’s earlier move for Inari Medical typify that response. Although clearer evidence ultimately benefits patient safety, the near-term impact trims innovation velocity and temporarily drags on clot management devices market growth.

High Procedural and Device Costs in Cost-Constrained Systems

A U.S. mechanical thrombectomy can cost USD 20,000-30,000, including devices priced at USD 3,000-5,000 each, while many Southern European hospitals budget only EUR 50,000-100,000 (USD 54,000-108,000) per year for all neurovascular consumables[2]MedPAC, “March 2026 Report to Congress: Medicare Payment Policy,”. Biplane angiography suites cost USD 1.5-2.5 million, a capital outlay beyond the means of most regional hospitals in Latin America and Southeast Asia, which default to tissue plasminogen activator at a tenth of the cost. Although ASCs operate 46% cheaper than hospital outpatient departments, U.S. payers remain cautious about approving thrombectomy outside full-service hospitals owing to post-procedure monitoring risks. Cost, therefore, is likely to remain a structural barrier in lower-resource geographies for at least the next decade.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Neurovascular Platforms Outpace Legacy Venous Devices

Neurovascular thrombectomy systems dominated the mechanical clot management devices market share at 36.42% of 2025 revenue and are forecast to expand at a 7.54% CAGR through 2031. This momentum stems from robust evidence: SELECT2 showed that 20.3% of large-core patients achieved functional independence after thrombectomy, compared with 7% with medical care alone, validating expanded indications. Hybrid aspiration-plus-stent solutions such as Penumbra Lightning Flash 2.0 deliver 40-48% first-pass rates, a material jump in the performance metric most correlated with 90-day outcomes.

Conversely, inferior vena cava filters and catheter-directed thrombolysis devices face growth headwinds as direct oral anticoagulants address many prophylactic indications, and the FDA highlights low retrieval rates and late complications. New entrants like AngioDynamics’ AlphaVac PE have created a niche between pharmacologic and purely mechanical approaches, but overall growth remains modest. Mechanical embolectomy balloons remain in use for peripheral arterial disease but steadily yield to large-bore aspiration catheters that clear the clot more quickly while preserving the endothelium.

By End User: ASCs Disrupt Hospital Dominance

Hospitals billed 66.10% of 2025 device revenue, reflecting their 24/7 stroke-team staffing and installed angiography infrastructure. Still, ASCs are capturing outsized incremental volume, recording an 8.11% CAGR as cardiology-led centers multiplied fourfold between 2018 and 2023. Terumo’s radial-access campaign dovetails with the fast-turnover workflows typical of outpatient settings, cutting access-site complications and eliminating overnight stays.

The clot management devices market size associated with ASC procedures is projected to climb sharply once CMS finalizes codes that reimburse mechanical thrombectomy outside hospitals. Specialty clinics, while small today, could pivot into chronic-disease hubs that stock retrievable vena cava filters and peripheral thrombectomy kits for cancer and sickle-cell populations, but regulatory hurdles limit speed. Overall, end-user dynamics underscore a gradual but irreversible shift toward lower-cost care venues.

Geography Analysis

North America accounted for 43.65% of 2025 sales but will likely trail global averages in growth, as utilization has plateaued at roughly 8% of ischemic stroke admissions and further expansion depends on closing rural-access gaps. Canada reimburses thrombectomy nationwide yet suffers capacity bottlenecks that stretch elective vascular waits to a half-year in some provinces. Mexico’s market remains under-penetrated; only 2% of eligible strokes receive thrombectomy, largely due to out-of-pocket cost exposure exceeding USD 10,000 per episode.

Asia-Pacific delivers the fastest trajectory with a 6.43% forecast CAGR. China’s 300-center stroke network still serves far fewer cases per capita than the United States, signaling huge latent demand once operator training and provincial payers align. India’s private chains are racing to add suites; Apollo alone opened 15 neurovascular labs since 2022, even though 62% of Indian health-care spending remains out of pocket. Japan’s demographic tilt—28% of citizens over 65—makes thrombectomy a public-health imperative despite tight price caps.

Europe’s heterogeneous pay landscape drags on adoption. Germany’s DRG reimbursements keep volumes stable, but in Spain and Italy, tight budgets ration cases to younger, higher-NIHSS patients. The U.K. increased the number of thrombectomy-capable centers from 24 in 2015 to more than 50 by 2025, yet rural Wales and Scotland still face transfer times of several hours. Gulf Cooperation Council states mirror Western models with premium pricing, whereas most of sub-Saharan Africa lacks biplane angiography equipment, limiting uptake to urban private hospitals.

Competitive Landscape

Consolidation is reshaping the clot management devices industry. Boston Scientific’s USD 14.5 billion purchase of Penumbra in January 2026 combined the leading aspiration pipeline with Boston’s global channel, supporting device bundles spanning neuro, venous, and peripheral indications. Twelve months earlier, Stryker paid USD 4.9 billion for Inari Medical, bringing FlowTriever and ClotTriever technologies under the same roof as Stryker’s neurovascular franchise and broadening its hospital reach. Teleflex’s EUR 760 million agreement to absorb BIOTRONIK’s vascular line illustrates a similar revenue-buying agenda, especially given Europe’s MDR hurdles.

Medtronic, Johnson & Johnson’s Cerenovus unit, and Abbott remain formidable, yet margin pressure is intensifying as health systems negotiate volume-for-price deals. White-space innovation now clusters around medium-vessel devices, actively retrievable vena cava filters, and hybrid aspiration-pharmacologic catheters. Start-ups such as Imperative Care are carving niches by demonstrating record-low procedure times and hemorrhage rates, positioning themselves for future take-outs rather than independent scale.

Regulatory architecture favors those with deep pockets; the FDA’s product code NRY demands robust comparative data sets, and EU MDR recertification queues further strain smaller enterprises. Consequently, the top five suppliers already hold well over 70% of global revenue, a share that could exceed 80% once announced deals close.

Clot Management Devices Industry Leaders

Boston Scientific Corporation

Edward Lifesciences

AngioDynamics, Inc.

Medtronic

LeMaitre Vascular Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Boston Scientific announced the USD 14.5 billion acquisition of Penumbra, creating the sector’s first fully integrated neurovascular-to-peripheral thrombectomy portfolio.

- February 2025: Stryker completed its USD 4.9 billion purchase of Inari Medical, adding FlowTriever and ClotTriever devices to its catalogue.

- January 2025: Imperative Care secured FDA 510(k) clearance for its Zoom System, reporting a 19-minute median groin-puncture-to-reperfusion interval in the 211-patient IMPERATIVE trial.

- October 2024: Contego Medical obtained FDA PMA for the Neuroguard IEP 3-in-1 carotid stent system with integrated embolic protection.

Global Clot Management Devices Market Report Scope

As per the scope of the report, clot management devices are tools designed to remove or dissolve blood clots within vessels, restoring normal blood flow. They include thrombectomy devices, clot retrieval systems, and thrombolytic delivery tools. These devices are critical in treating conditions like stroke, deep vein thrombosis, and pulmonary embolism.

The Clot Management Devices Market is Segmented by Product (Embolectomy Balloon Catheters, Catheter-Directed Thrombolysis Devices, Mechanical/Percutaneous Thrombectomy Devices, Inferior Vena Cava Filters, and Neurovascular Embolectomy/Thrombectomy Devices), End User (Hospitals, Ambulatory Surgical Centers, and Specialty Clinics), and Geography (North America, Europe, Asia-Pacific, Middle East & Africa, and South America). The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the value (in USD million) for the above segments.

| Embolectomy Balloon Catheters |

| Catheter-Directed Thrombolysis Devices |

| Mechanical/Percutaneous Thrombectomy Devices |

| Inferior Vena Cava (IVC) Filters |

| Neurovascular Embolectomy/Thrombectomy Devices |

| Hospitals |

| Ambulatory Surgical Centers (ASCs) |

| Specialty Clinics |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product | Embolectomy Balloon Catheters | |

| Catheter-Directed Thrombolysis Devices | ||

| Mechanical/Percutaneous Thrombectomy Devices | ||

| Inferior Vena Cava (IVC) Filters | ||

| Neurovascular Embolectomy/Thrombectomy Devices | ||

| By End User | Hospitals | |

| Ambulatory Surgical Centers (ASCs) | ||

| Specialty Clinics | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large will global demand for clot-removal devices be by 2031?

The clot management devices market size is forecast to reach USD 2.77 billion by 2031, expanding from USD 2.08 billion in 2026 at a 5.96% CAGR.

Which product class is growing quickest?

Neurovascular thrombectomy platforms lead with a 7.54% CAGR, powered by clinical evidence that widened treatment windows to 24 hours and improved first-pass success.

Why are ambulatory surgical centers attracting attention?

ASCs enjoy Medicare payments that average 46% below hospital outpatient rates, and radial-access techniques now allow same-day discharge for stable thrombectomy patients, fueling an 8.11% CAGR.

What is the key regulatory headwind?

The FDA and EU MDR now require comparative-effectiveness trials and extensive clinical dossiers, adding up to USD 20 million in cost and up to two years in extra time to market.

Which region should drive the next growth wave?

Asia-Pacific posts the highest forecast CAGR at 6.43% as China, India, and Japan invest aggressively in comprehensive stroke centers and operator training.

How is industry competition evolving?

Recent mega-deals, including Boston Scientific-Penumbra and Stryker-Inari, signal a shift to growth via acquisition, leaving startups to pursue niche innovation or partner with majors for distribution.

Page last updated on: