Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

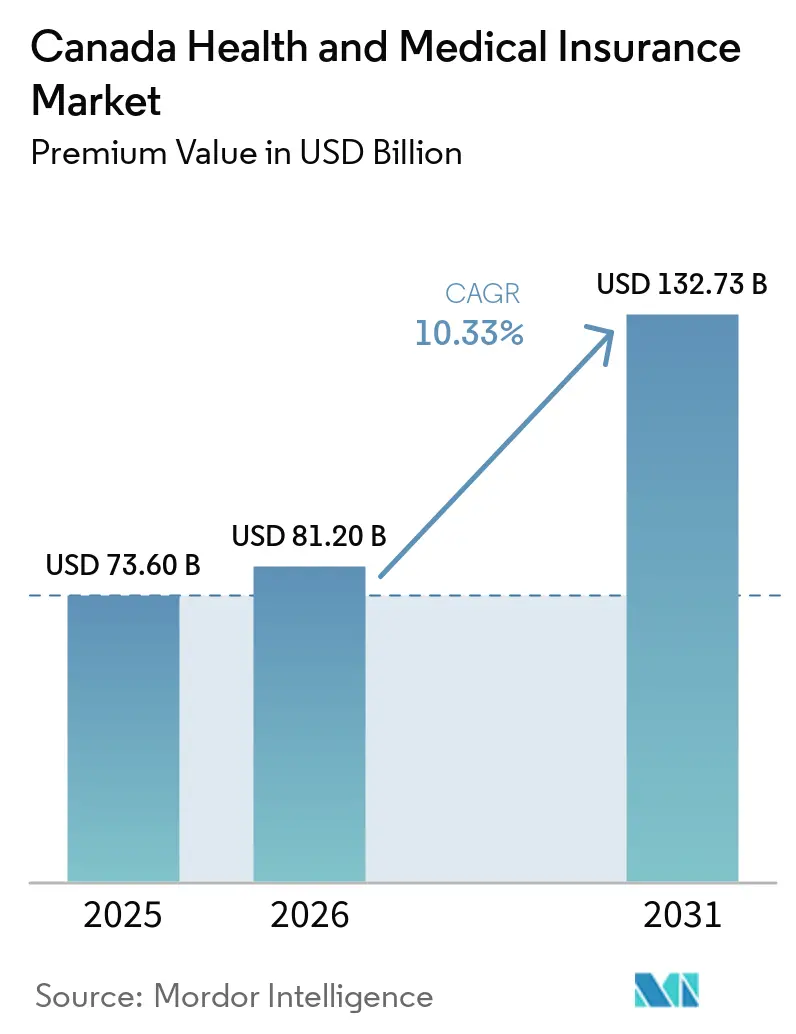

| Base Year Market Size (2025) | USD 73.60 Billion |

| Market Size (2026) | USD 81.20 Billion |

| Market Size (2031) | USD 132.73 Billion |

| Growth Rate (2026 - 2031) | 10.33% CAGR |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Canada Health and Medical Insurance Market Analysis by Mordor Intelligence

The Canada Health And Medical Insurance Market size in terms of premium value is expected to grow from USD 73.60 billion in 2025 to USD 81.20 billion in 2026 and is forecast to reach USD 132.73 billion by 2031 at 10.33% CAGR over 2026-2031.

Public funding momentum frames demand patterns as the Government of Canada advances a decade-long USD 200 billion plan focused on access, modernization, and primary care renewal that is reshaping the boundary between universal programs and private supplemental benefits. The Pharmacare Act, which received Royal Assent in October 2024, is being implemented through bilateral agreements for coverage of contraception and diabetes medications, while Quebec and Alberta chose to preserve distinct provincial frameworks. Employer-sponsored plans continue to anchor access to extended health, dental, and wellness benefits, supported by stable payroll funding and plan governance that maintain continuity through cycles in employment and inflation. Provinces are amplifying biosimilar mandates and savings reinvestments, with British Columbia and Ontario codifying automatic transitions that private payers are mirroring to maintain consistent experiences and reduce adjudication friction across the Canadian health and medical insurance market.

Key Report Takeaways

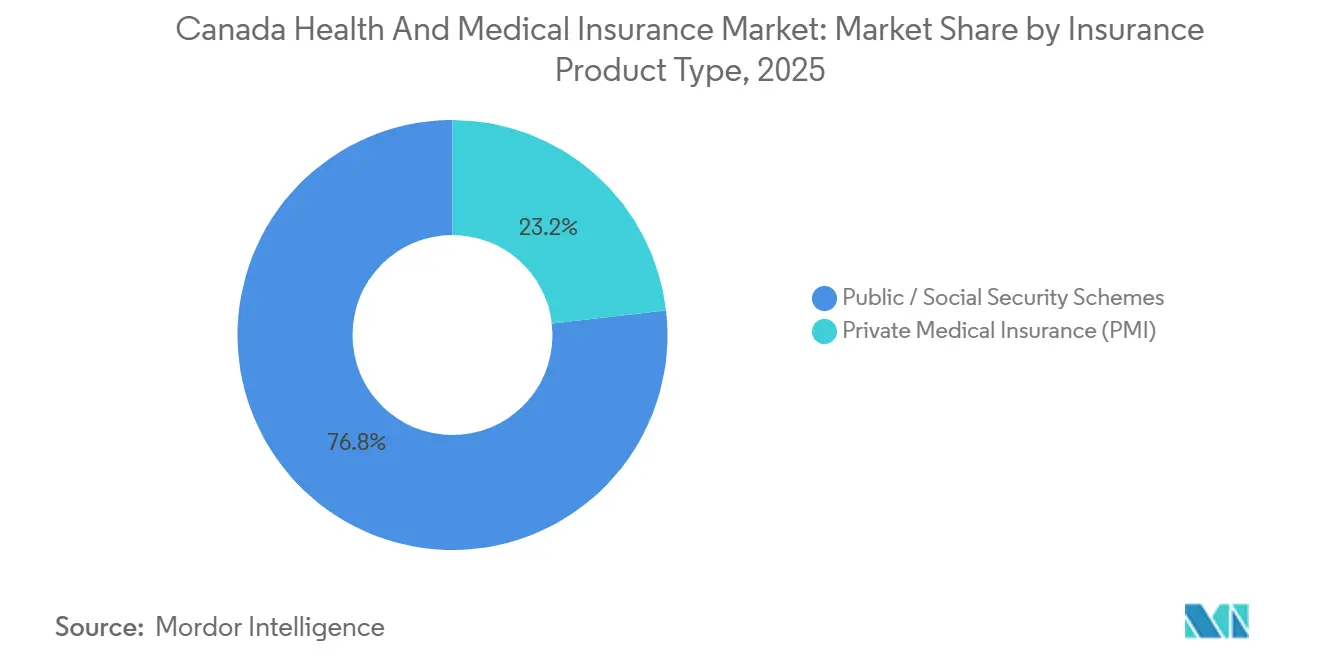

- By insurance product type, public and social security schemes led with 76.82% of the Canada health and medical insurance market share in 2025 and are projected to expand at an 8.24% CAGR through 2031.

- By term of coverage, long-term plans held 94.63% of the Canadian health and medical insurance market share in 2025 and are expected to advance at a 3.08% CAGR through 2031.

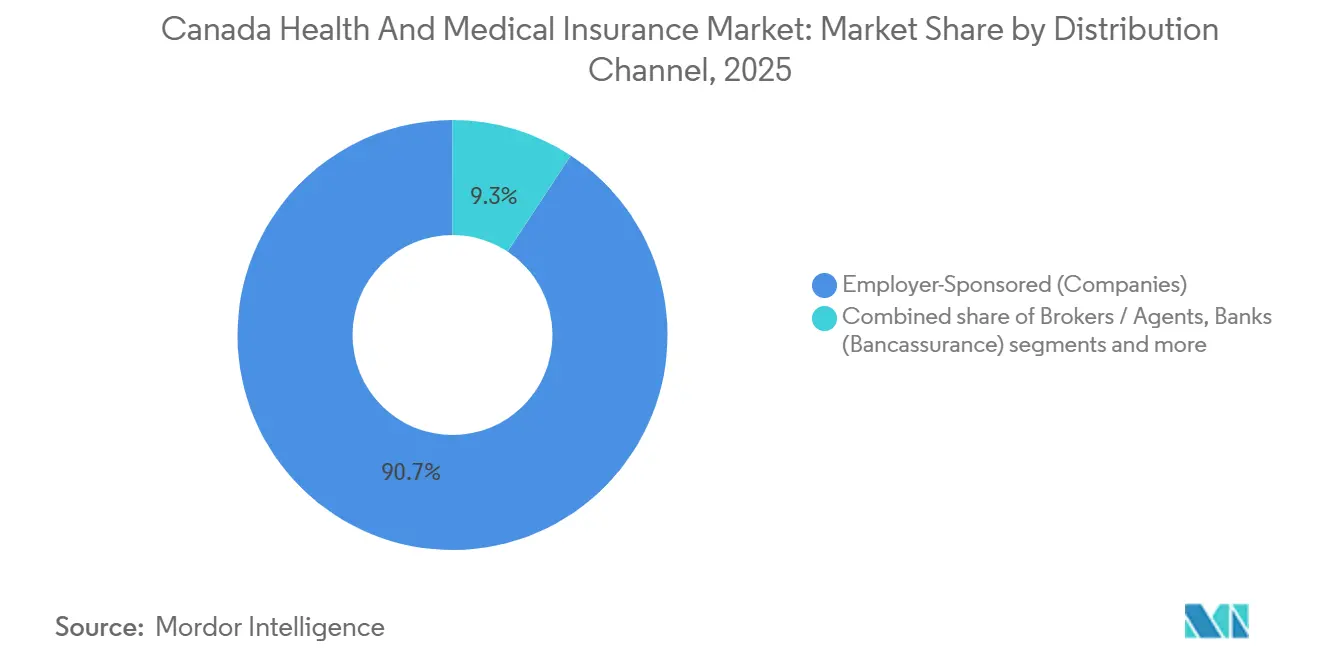

- By distribution channel, employer-sponsored plans commanded 90.74% of the Canadian health and medical insurance market share in 2025, while direct-to-consumer is projected to post the fastest 11.12% CAGR through 2031.

- By end-user segment, large corporates accounted for 69.28% of the Canadian health and medical insurance market share in 2025, while SMEs are projected to record the highest 5.57% CAGR through 2031.

- By geography, Ontario held 50.63% of the Canada health and medical insurance market share in 2025, while Alberta is expected to be the fastest-growing province at a 4.52% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Canada Health and Medical Insurance Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Employer-sponsored group benefits dominance | +2.3% | National, concentrated in Ontario at 50.63% share, Quebec with RAMQ private-plan mandate, and Alberta growth corridor | Short term (≤ 2 years) |

| Virtual care integration embedded in group plans | +1.8% | National, with higher uptake in British Columbia and Newfoundland and Labrador, and growing rural access | Medium term (2-4 years) |

| Public program expansions catalyze PMI plan redesign | +1.4% | National, early gains in Manitoba, Prince Edward Island, British Columbia, and Yukon, with complex coordination in Ontario and Alberta | Medium term (2-4 years) |

| Biosimilar switching momentum shaping private formularies | +0.9% | National, led by British Columbia, Saskatchewan, and Ontario, mandates and reinforced in Manitoba, Prince Edward Island, Newfoundland and Labrador, and Yukon | Long term (≥ 4 years) |

| PBM and digital adjudication scale enabling new product designs | +1.2% | National, TELUS Health, and Express Scripts Canada at scale with slower integration in Northern territories | Short term (≤ 2 years) |

| Quebec RAMQ private-plan mandate sustaining coverage penetration | +0.7% | Quebec-specific, with precedent value monitored in Atlantic provinces | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Employer-Sponsored Group Benefits Dominance

Employer-sponsored benefits anchor access to non-hospital services and top-up coverage, which supports steady enrollment and renewals across the Canadian health and medical insurance market. Ontario’s 2025 to 2026 plan sustains system capacity with multi-billion allocations to hospitals, physician services, and home and community care, reinforcing the complementary role of private plans for prescription drugs outside hospitals, dental, vision, and paramedical services [1]Ontario Ministry of Health, “Published Plans and Annual Reports 2025-2026,” Government of Ontario, ontario.ca. Large distribution partners are using analytics to tailor plan designs and engagement for multigenerational workforces, which improves alignment with chronic disease risks and disability management goals. Carriers that blend digital channels with in-person support are deepening member relationships and reducing administrative friction through connected care and modern claims engines. These conditions help maintain employer coverage as the dominant channel in 2025 and preserve its strategic role in product innovation within the Canadian health and medical insurance market.

Virtual Care Integration Embedded in Group Plans

Virtual care is a permanent feature of group plans, with platforms providing fast access, clinical navigation, and pharmacy services that reduce unnecessary in-person visits and support continuity of care. Capabilities now include e-claims, expanded chronic care pathways, and programs that connect primary and specialty teams along a single member journey, which improves satisfaction and adherence. Pharmacy innovations and digital prescription tools enable synchronized refills and automated workflows, lowering administrative delays and supporting timely therapy starts. These tools shape expectations for omnichannel access across chat, video, and in-person consultations, which influences plan communications and benefit usage across the Canadian health and medical insurance market. Insurers are adopting AI-enabled triage and claims automation that shorten cycle times and standardize experiences across digital service layers.

Biosimilar Switching Momentum Shaping Private Formularies

Mandatory biosimilar transitions are expanding across provinces, and private payers are aligning to reduce confusion and support consistent pharmacy adjudication. British Columbia’s program has delivered significant savings and reinvestments into glucose monitoring and other therapies, demonstrating how pharmacare policies can extend access while bending drug trends. Ontario’s 2025 directive mandates transitions for Eylea, Actemra, and Xolair by May 2026, which sets a clear schedule for both public and private plan alignment. Saskatchewan’s 2026 policy expands interprovincial harmonization over a 12-month implementation period, strengthening PBM contracting leverage and formulary consistency. Federal analysis estimates further savings potential if uptake reaches European benchmarks, which sustains policy momentum across the Canadian health and medical insurance market.

Quebec RAMQ Private Plan Mandate Sustaining Coverage Penetration

Quebec’s Act Respecting Prescription Drug Insurance requires universal drug coverage through RAMQ or qualifying private plans, which sets a structural floor for private enrollment and coverage continuity among working-age residents and retirees. Private plans must meet or exceed public maximum member contribution and co-insurance caps, which standardize access and stabilize out-of-pocket exposure across plan types. Pharmacists’ associations flagged that Quebec’s hybrid model already achieves pharmacare objectives, and the province opted out of Bill C-64 to maintain provincial administration and coordination. This framework preserves private insurer penetration in a large provincial market and reduces crowd-out risks linked to federal expansion in neighboring provinces. As federal initiatives evolve, Quebec’s model continues to inform hybrid solutions in Atlantic and Prairie regions within the Canada health and medical insurance market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Specialty drug inflation is raising loss ratios in private plans | -1.4% | National with pressure in major urban centers and small-plan pooling exposure | Long term (≥ 4 years) |

| Pharmacare (C-64) and CDCP crowd-out risk for selecting private benefits | -1.8% | Prince Edward Island, Manitoba, British Columbia, and Yukon initial agreements, and Quebec and Alberta opt-outs | Medium term (2-4 years) |

| Distribution channel licensing (MGA) is raising compliance costs | -0.6% | Ontario rulemaking leads with Saskatchewan precedent | Medium term (2-4 years) |

| Preferred pharmacy network scrutiny, limiting cost levers | -0.8% | Ontario has potential policy spillovers and a national debate | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Specialty Drug Inflation Raising Loss Ratios in Private Plans

Specialty drug costs are the largest single driver of private plan trend, with biologic disease modifiers across inflammatory and ophthalmology conditions absorbing a rising share of spend through 2024 and 2025. Weight-management therapies accelerated in 2024 after new launches, which increased exposure for sponsors that operate open formularies and broad coverage criteria. Biosimilar-first strategies and step therapy are gaining ground as plan sponsors seek to offset inflationary pressure while maintaining access, and public biosimilar policies provide reference points for private alignment. Prior authorization measures for select therapies are being refined to ensure clinical appropriateness and adherence to label, which moderates off-label use and non-essential demand. This environment is shaping benefit design changes across the Canadian health and medical insurance market to protect loss ratios and coverage sustainability for employers and individuals.

Distribution Channel Licensing (MGA) Raising Compliance Costs

Ontario’s financial services regulator paused its proposed Managing General Agent licensing rule in February 2026 to refine scope and proportionality after industry feedback, but directionally tighter oversight appears likely over time [2]Financial Services Regulatory Authority of Ontario, “FSRA Pauses MGA Rule,” fsrao.ca. The proposed framework adds licensing, minimum E&O coverage, and trust accounting requirements, which can compress margins for smaller MGAs without scale or centralized compliance resources. Saskatchewan’s MGA licensing regime provides an operating precedent that shows how fees and insurance thresholds can accumulate for wholesalers and intermediaries. Larger broker platforms can amortize compliance costs across broader premium bases and legal teams, which accelerates consolidation in distribution layers. Over the medium term, these rules will influence distribution strategy and carrier partnerships throughout the Canadian health and medical insurance market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Insurance Product Type: Public Schemes Anchor Universal Access as Private Tops Up

Public and social security schemes commanded 76.82% share in 2025, and this segment of the Canada health and medical insurance market size is projected to expand at an 8.24% CAGR through 2031 as provinces reinforce core access under the medicare framework. The Canada Health Act sets requirements for publicly insured hospital and physician services, and provinces extend these programs with targeted benefits for drugs and dental care that vary by income and eligibility rules [3]Health Canada, “How Publicly Funded Health Care Coverage Works,” Government of Canada, canada.ca. Provincial per-capita health spending differs by geography and age profile, with higher costs in territories and Atlantic regions that reflect service delivery challenges and older populations. Quebec’s hybrid model mandates universal drug coverage through RAMQ or qualifying private plans, which ensures both continuity and comparability of protection across residents. British Columbia and Ontario are adding operating budgets and pharmacare investments, which improve baseline capacity and reduce out-of-pocket exposure for covered categories.

Private medical insurance accounts for the remaining share and fills coverage gaps for prescriptions outside hospitals, dental, vision, paramedical services, enhanced hospital accommodations, and medical transportation above provincial schedules. Group coverage dominates private distribution and remains attractive through employer cost-sharing and negotiated service models, while individual coverage supports retirees, the self-employed, and those not eligible for workplace plans. Public drug policies, especially biosimilar switching, influence private formulary decisions as carriers seek to keep alignment with provincial plans and reduce adjudication friction. As pharmacare pilots mature, private plans are emphasizing navigation, mental health, and specialty pharmacy management to maintain clear value propositions in the Canada health and medical insurance industry.

By Term of Coverage: Long-Term Plans Dominate Through Employer Lock-In

Long-term coverage at 12 months or more held 94.63% of the premium share in 2025, and this segment of the Canadian health and medical insurance market is expected to advance at a 3.08% CAGR through 2031 due to annual renewals and stable employer participation. Employers calibrate eligibility, waiting periods, and cost-sharing to meet workforce needs, which sustains membership over time and aligns with annual review cycles. Group pooling and multi-year procurement reduce volatility from catastrophic claims compared with standalone individual underwriting, which supports predictable renewal outcomes. Analytics and modern communications are improving plan navigation and benefits literacy among employees, which raises perceived value and utilization. These features keep long-term structures as the default for employer coverage across the Canadian health and medical insurance market.

Short-term coverage under 12 months captures a small residual share and addresses episodic needs such as travel health or temporary medical coverage for visitors and students, while most Canadians rely on long-term plans for ongoing protection. Carriers are modernizing underwriting and onboarding with AI to speed decisions for eligible applications, which strengthens the case for durable contracts and lowers acquisition costs. Multi-year community health partnerships, such as diabetes prevention clinics, connect insurance with prevention and remission programs that enhance long-term member retention. As provinces invest in primary and acute care, the short-term segment will remain focused on travel and specialized events rather than replacing long-term structures in the Canadian health and medical insurance industry.

By Distribution Channel: Employer Platforms Overshadow Direct-to-Consumer Growth

Employer-sponsored channels commanded 90.74% of distribution in 2025, and direct-to-consumer recorded the fastest 11.12% CAGR projection through 2031 within the Canada health and medical insurance market size as digital-first journeys expand access. Employers are refining plan communications and analytics to close knowledge gaps and raise uptake of virtual care, mental health programs, and wellness services among members. Carriers are combining walk-in service centers with robust digital channels to improve omnichannel service and reduce friction in claims and coordination. Standardized small business plans with immediate quotes and quick onboarding are addressing HR capacity constraints at smaller employers. These distribution dynamics keep employer-led models at scale while opening room for targeted direct-to-consumer growth across the Canadian health and medical insurance market.

Banks retain a modest role in cross-selling alongside wealth offerings, while brokers and agents remain primary intermediaries for plan design and renewals in group benefits. Regulatory initiatives around MGA licensing are reshaping compliance requirements, which gives scale players advantages in technology and legal support. PBM platforms such as Express Scripts and TELUS Health are standardizing adjudication and data flows that make select direct-to-consumer path designs more feasible for lower-complexity benefits. Over the medium term, these shifts will influence product mixes and channel economics across the Canadian health and medical insurance industry.

By End-User Segment: Large Corporates Fund Pooling; SMEs Drive Innovation

Large corporates accounted for 69.28% of the Canadian health and medical insurance market share in 2025, supported by economies of scale, risk pooling, and data-driven plan optimization that lowers per-employee costs. Large employers deploy analytics to manage disability risks and enhance chronic disease outcomes, which reduces volatility at renewal and supports long-term workforce health. Quebec’s pooling framework stabilizes catastrophic claim exposure for small groups and preserves sustainability across employer sizes under the province’s universal drug coverage mandate. Prevention partnerships and clinical programs with academic and hospital partners add a long-horizon component to corporate benefits strategies. As biosimilar policies spread, large multijurisdictional employers can implement step therapy and formulary alignment rapidly across national footprints.

SMEs held 30.72% share and are the fastest-growing end-user group with a 5.57% CAGR outlook to 2031, helped by accessible digital administration, pooled rate structures, and modular accounts for wellness and mental health. Pooled SME programs enable micro and small employers to access comprehensive benefits with stable renewal trends compared with standalone underwriting. Tiered SME plans with quick implementation timelines and predictable pricing are expanding access to coverage in sectors with limited HR resources. Administration services, only models, and stop-loss pricing create options for healthier SME groups to lower the total cost of risk while maintaining member experience. These features suggest consistent growth for SMEs as they converge toward large corporate capabilities in the Canadian health and medical insurance market.

Geography Analysis

Ontario led with 50.63% of the Canada health and medical insurance market share in 2025, while Alberta is projected to post the fastest 4.52% CAGR to 2031 based on economic momentum, health system restructuring, and interprovincial migration. Ontario’s 2025 to 2026 plan funds hospitals, physician services, and home and community care at scale, which maintains public access while preserving supplemental roles for private benefits in areas such as dentistry, vision, paramedical services, and out-of-hospital prescription drugs. Quebec maintains a hybrid prescription drug framework with universal coverage either through RAMQ or private plans, which sustains private penetration and streamlines coordination for employers. British Columbia continues to invest in primary care teams and pharmacare, which aligns public and private formularies and reduces out-of-pocket exposure for covered therapies and devices. Alberta’s health service transformation introduces regional corridors and specialized agencies to improve throughput and access, which complements private coverage oriented toward speed and choice for diagnostics and specialist access.

Quebec’s influence is anchored in its universal drug coverage mandate and pooling rules that moderate volatility for small employers and provide a stable market structure for carriers. British Columbia’s biosimilar program and growing operating budgets have enabled reinvestments into glucose monitors and other therapies, which inform private plan coordination decisions and reinforce formulary alignment. Ontario’s biosimilar mandate running to May 2026 provides a clear roadmap for synchronized transitions across payers, reducing confusion and administrative load for pharmacies and patients. Variations in public per-capita spending by province reflect demographic and geographic realities, which shape supplemental coverage needs and plan design mixes by region. These provincial policies define the operating context for private plan strategy within the Canadian health and medical insurance market.

Alberta’s surgery volumes and virtual pilots illustrate how targeted innovations can ease bottlenecks in capacity-constrained zones and support outcomes that are relevant to employer plans that value timely access. The Rest of Canada exhibits higher per-capita public outlays in several Atlantic provinces due to older population structures and geographic delivery costs, which shape the mix of private top-ups and service add-ons. Saskatchewan’s 2026 biosimilar alignment with Alberta and other provinces highlights Prairie and Atlantic coordination that private plans track closely to keep consistent pharmacy and formulary practices. These currents combine to support Alberta’s faster growth outlook while keeping Ontario the largest provincial share of the Canada health and medical insurance market.

Competitive Landscape

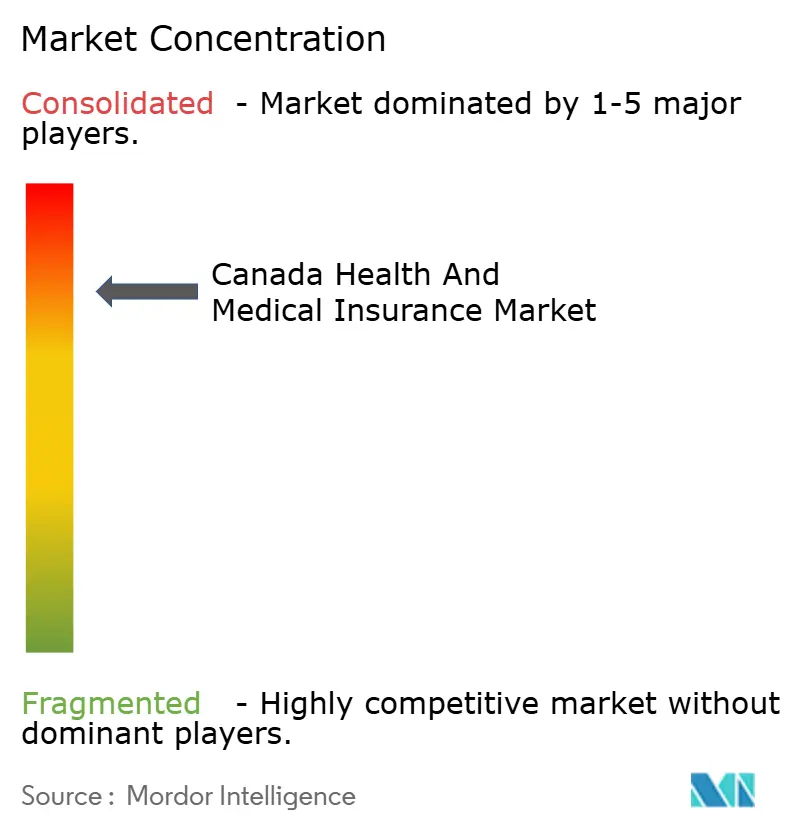

The Canadian health and medical insurance market is moderately to highly concentrated, with five incumbents accounting for a large share of private health and dental premiums while facing competition from digital platforms and PBM-converged models. Sun Life reinforced institutional capabilities through pension risk transfers, which strengthen cross-client relationships and support integrated benefits strategies over long horizons. Manulife scaled AI across operations and accelerated underwriting decisions in Canada, lowering acquisition costs and improving digital onboarding for members. Desjardins expanded into national wealth management with a pending acquisition that broadens cross-sell opportunities for protection and health benefits. These moves sustain scale advantages in distribution, capital, and data that shape competitive conduct and product roadmaps.

Regulatory and competition oversight are also influencing market structure. FSRA paused its MGA licensing rule to refine scope and proportionality, which has implications for intermediary oversight and viability for smaller entrants. The Competition Bureau’s review of PBM practices could alter preferred network economics and pharmacy steering, which would affect plan costs and member journeys across distribution channels. Industry collaboration on AI-driven fraud detection is advancing under technology partnerships that improve detection speed and accuracy in life and health lines. Combined with biosimilar mandates, these levers are bending the trend and aligning formularies across public and private payers in the Canadian health and medical insurance market.

Carriers are extending partnerships with clinical institutions and technology vendors to deliver prevention programs and new member tools. Sun Life renewed funding for a diabetes prevention and remission clinic, indicating a commitment to measurable health outcomes and employer value. Manulife launched a Global Longevity Institute with academic partners to address aging and healthcare affordability, which informs product innovation and underwriting. Medavie Blue Cross operationalized an AI program and expanded its connected care suite that integrates virtual triage and booking, showing how insurers are shifting from transactional claims to continuous care enablement. These initiatives strengthen differentiation and member engagement while complementing provincial health goals within the Canadian health and medical insurance market.

Canada Health and Medical Insurance Industry Leaders

Manulife

Sun Life

Canada Life

Desjardins

GreenShield

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: iA Financial Group acquired First Growth Multi Family Office, managing over USD 1.5 billion in assets under administration, marking its seventh acquisition since launching a USD 500 million acquisition fund in 2024 and extending its reach into ultra-high-net-worth segments for cross-sell of protection and savings solutions. The transaction broadens distribution among sophisticated clients that use insurance-linked estate and tax solutions. Integration is expected to deepen advice-led channels for holistic planning.

- January 2026: Manulife Canada announced that its AI-driven underwriting engine, MAUDE, achieved 58% instant approval rates for eligible life insurance applications by December 2025, enabling automatic policy issuance in as little as two minutes for term life coverage up to USD 2 million and permanent products up to USD 500,000. The rollout accelerates onboarding and reduces customer acquisition costs, supporting faster cycle times for intermediated and direct channels. The initiative aligns with broader AI deployments and positions Manulife to scale predictive decisioning in adjacent benefits workflows.

- November 2025: Sun Life renewed a USD 600,000 partnership with the Montreal Heart Institute Foundation to support the Sun Life Diabetes Prevention and Remission Clinic through 2028, expanding access to intensive lifestyle intervention programs with strong remission outcomes in early cohorts. The program links prevention and plan value by addressing a high-prevalence condition. The collaboration strengthens clinical data for benefits strategies focused on metabolic health.

- October 2025: iA Financial Corporation completed its acquisition of RF Capital Group, significantly expanding its wealth and insurance operations in Canada. This move had strengthened iA's position as an independent non-bank financial services provider by integrating its insurance expertise with RF Capital's wealth management capabilities.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the Canada health and medical insurance market as all premiums written for plans that fund medically necessary and supplemental services for residents and temporary workers under private policies and provincial public schemes. Benefits captured include hospital, physician, prescription drug, dental, and vision coverage where an insurance contract, not direct tax transfer, is the payment vehicle.

Scope Exclusions: travel health, critical illness lump-sum products, and stand-alone accident covers are left outside the sizing so that only mainstream reimbursement business is modeled.

Segmentation Overview

- By Insurance Product Type

- Private Medical Insurance (PMI)

- Individual Policy Coverage

- Group Policy Coverage

- Public / Social Security Schemes

- Private Medical Insurance (PMI)

- By Term of Coverage

- Short-term (Less Than 12 months)

- Long-term (Greater Than Equal to 12 months)

- By Distribution Channel

- Brokers / Agents

- Banks (Bancassurance)

- Direct-to-Consumer (Online / Phone)

- Employer-Sponsored (Companies)

- Other Channels (Affinity, Associations)

- By End-user Segment

- Individuals

- SMEs

- Large Corporates

- By Geography

- Ontario

- Quebec

- British Columbia

- Alberta

- Rest of Canada

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed underwriting managers at national insurers, group benefit brokers in Ontario and Alberta, and actuaries advising mid-sized employers. We also surveyed human resources heads in manufacturing and technology firms to understand plan design shifts and likely uptake of voluntary benefits, thereby validating secondary findings and filling data gaps.

Desk Research

We began with publicly available data from Statistics Canada, the Canadian Institute for Health Information, the Canadian Life & Health Insurance Association fact book, federal budget papers on the Canada Health Transfer, and Organisation for Economic Co-operation and Development health expenditure tables. Company annual reports and OSFI solvency filings supplied carrier performance indicators, while D&B Hoovers and Dow Jones Factiva offered premium splits and strategic developments. Numerous other open datasets and periodicals were cross-checked to round out the evidence base.

Market Sizing and Forecasting

A top-down build starts with provincial health spending and private supplemental premium pools, followed by penetration rate adjustments for individual, SME, and large corporate cohorts. Select bottom-up checks, such as sampled average premium times covered lives and broker channel audits, are layered to refine totals. Key variables feeding the model include employer-sponsored coverage penetration, average premium inflation, demographic aging ratios, drug cost inflation, and provincial plan copay policy changes. Multivariate regression with scenario analysis projects these drivers through 2030; assumptions are stress tested with expert consensus and historic elasticities. Any residual data voids are bridged through weighted interpolation grounded in observed carrier disclosures.

Data Validation and Update Cycle

Outputs pass a three-stage review: variance scans versus historical series, peer cross-checks, and senior analyst sign-off. We refresh figures once a year, with rapid updates triggered by policy or currency swings, ensuring clients always receive our latest vetted view.

Why Mordor's Canada Health and Medical Insurance Baseline Stands Up to Scrutiny

Published figures diverge because firms pick different policy baskets, price bases, and update cadences.

Mordor's disciplined scope matching only reimbursable medical cover and its annual refresh yields a clear, decision-ready baseline.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 73.60 B (2025) | Mordor Intelligence | - |

| USD 201.66 B (2024) | Regional Consultancy A | Bundles life and accident lines; uses gross written, not earned, premiums |

| USD 101.50 B (2023) | Global Consultancy B | Includes travel and creditor policies; narrower employer sample |

| USD 91.09 B (2020) | Trade Journal C | Historic base year held constant; no currency normalization for trend |

The comparison shows that larger or smaller values usually arise from scope creep into life or accident products, differing premium definitions, or outdated baselines. By anchoring forecasts to transparent variables and timely public data, Mordor Intelligence delivers a balanced, reproducible benchmark that decision makers can rely on.

Key Questions Answered in the Report

What is the projected size and growth of the Canadian health and medical insurance market?

The Canadian health and medical insurance market size is expected to grow from USD 73.60 billion in 2025 to USD 132.73 billion by 2031 at a 10.33% CAGR from 2026 to 2031.

Which distribution channel leads in Canada's health and medical insurance, and what is its outlook?

Employer-sponsored plans led with 90.74% of distribution in 2025, while direct-to-consumer is projected to record the fastest 11.12% CAGR through 2031 as digital journeys expand.

How are public policies affecting the Canadian health and medical insurance market?

The Pharmacare Act and federal funding for primary care and modernization are driving coordination for select drug categories, while biosimilar mandates in provinces like Ontario and British Columbia are shaping private formularies and generating savings that influence plan design.

Which provinces are most important for the Canadian health and medical insurance market?

Ontario held 50.63% share in 2025 and remains the largest, while Alberta is the fastest growing through 2031, with Quebec's hybrid RAMQ model maintaining strong private-plan participation.

What segments drive growth in the Canadian health and medical insurance market?

Public and social security schemes led with 76.82% share in 2025 and are projected to grow at 8.24% CAGR, while SMEs lead growth on the end-user side with a 5.57% CAGR, and direct-to-consumer expands fastest among channels at 11.12%.

How are carriers using technology to improve the Canadian health and medical insurance market?

Carriers and PBMs are leveraging real-time adjudication, AI-powered underwriting, and virtual care platforms to reduce cycle times, improve access, and enhance fraud detection, which supports better outcomes and member experiences.

Page last updated on: