Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

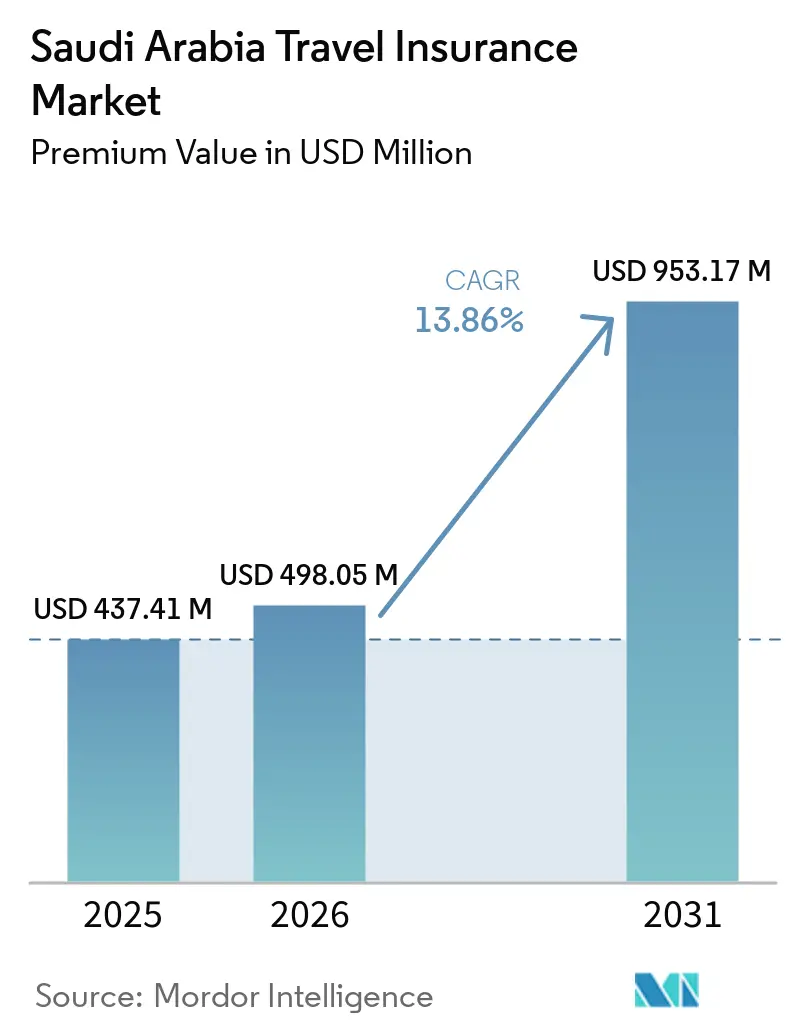

| Base Year Market Size (2025) | USD 437.41 Million |

| Market Size (2026) | USD 498.05 Million |

| Market Size (2031) | USD 953.17 Million |

| Growth Rate (2026 - 2031) | 13.86% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Saudi Arabia Travel Insurance Market Analysis by Mordor Intelligence

The Saudi Arabia Travel Insurance Market size in terms of premium value is projected to expand from USD 437.41 million in 2025 and USD 498.05 million in 2026 to USD 953.17 million by 2031, registering a CAGR of 13.86% between 2026 to 2031.

Robust growth reflects the push under Vision 2030 to scale tourism and expand international arrivals, which elevates travel protection from a discretionary add-on to a required element of trip planning. Mandatory medical coverage embedded in the tourist eVisa and stopover programs integrates insurance purchase into the visa journey, which raises compliance and simplifies issuance for inbound travelers. A separate 90-day scheme for Umrah and Hajj pilgrims standardizes cover and locks in continuity of service across approved providers. Aggregators and insurer digital channels shorten purchase and fulfillment times, which improves conversion among price-sensitive travelers who expect quick comparison and instant policy activation. Large domestic carriers and Sharia-compliant takaful brands remain central to product supply, while embedded experiences across airline, visa, and health ecosystems reinforce the Saudi Arabia Travel Insurance market’s structural tailwinds.

Key Report Takeaways

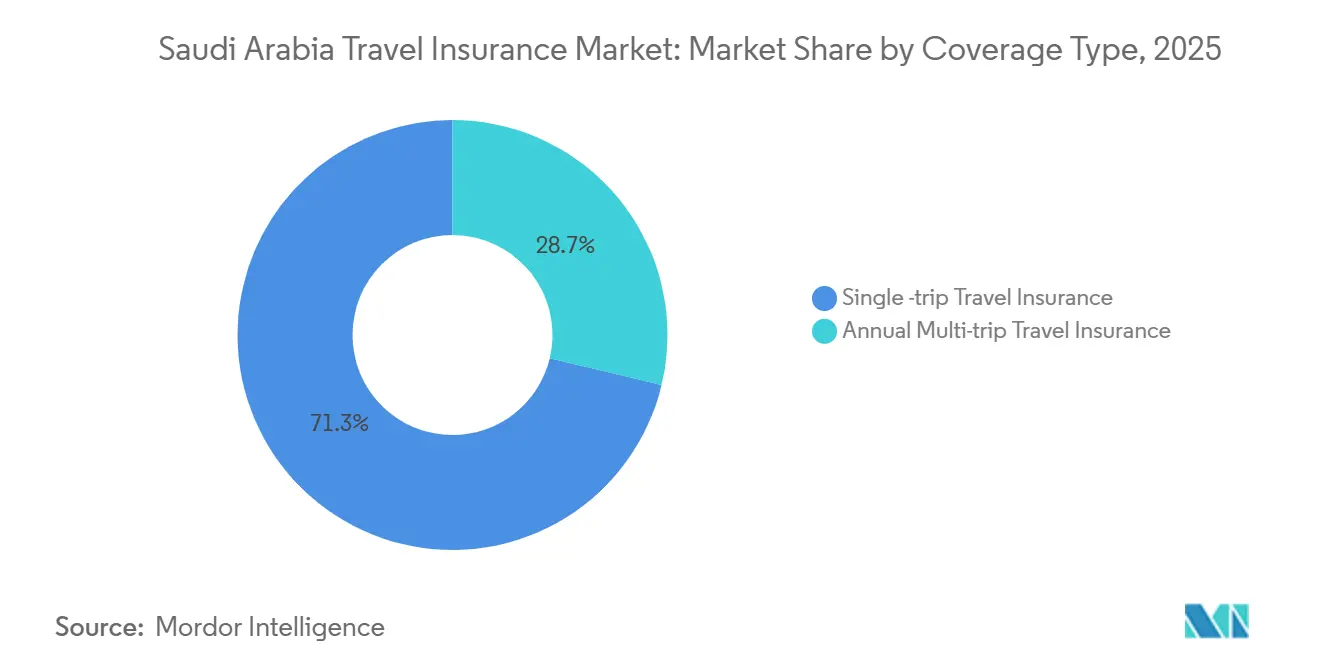

- By coverage type, single-trip policies accounted for 71.27% revenue share of the Saudi Arabia travel insurance market in 2025; annual multi-trip offerings are projected to expand at a 10.34% CAGR to 2031.

- By end user, business travelers held 37.81% of the Saudi Arabia travel insurance market size in 2025, while family travelers posted the quickest pace at 10.93% CAGR through 2031.

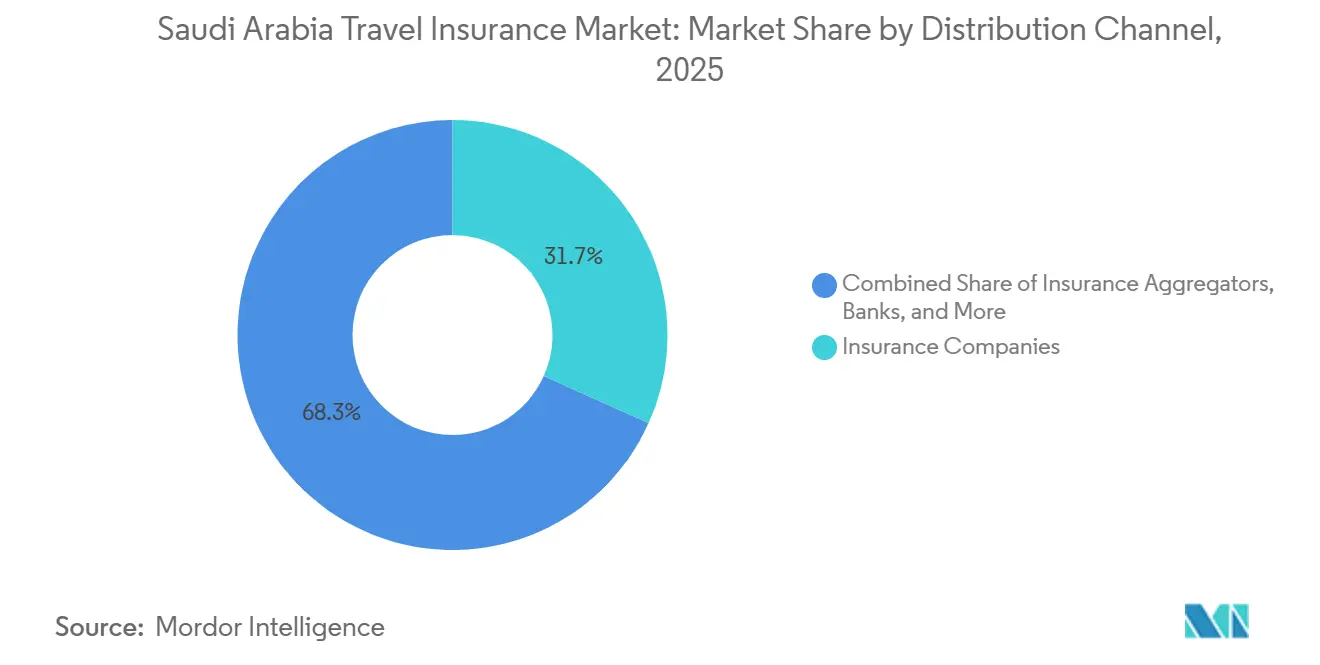

- By distribution channel, direct-to-consumer sales via insurance companies retained a 31.72% share of the Saudi Arabia travel insurance market in 2025; insurance aggregators record the highest forecast growth at 9.51% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Saudi Arabia Travel Insurance Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Vision 2030 tourism-influx push | +3.2% | National, with early gains in Riyadh, Jeddah, AlUla, NEOM, and Red Sea tourism zones | Medium term (2-4 years) |

| Mandatory Umrah/Hajj medical cover | +2.8% | National, concentrated in the Makkah and Madinah pilgrimage corridors | Short term (≤ 2 years) |

| Growing outbound middle-class spend | +2.1% | National, with a higher propensity in Riyadh, Eastern Province, and urban centers | Medium term (2-4 years) |

| Digital issuance via the eVisa platform | +1.9% | National, with spill-over to GCC cross-border travel | Short term (≤ 2 years) |

| Rise of Sharia-compliant takaful plans | +1.5% | National, with the strongest adoption in conservative regions | Long term (≥ 4 years) |

| Data-driven pricing by InsurTechs | +1.3% | National, led by Riyadh tech ecosystem, expanding to Jeddah, Dammam | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Vision 2030 Tourism-Influx Push Unlocks Structural Demand

Saudi Arabia’s Vision 2030 program positions tourism as a major pillar of diversification, with a multi-year plan to scale international arrivals and widen the mix of trip purposes beyond religious travel[1]Saudi Arabia, “Saudi Vision 2030,” Vision 2030, vision2030.gov.sa. The strategy’s focus on giga-projects such as NEOM, the Red Sea, and Qiddiya creates continuous visitor inflows tied to leisure, culture, sports, and business events that require tailored protection and medical benefits. Mandatory medical insurance for the tourist eVisa further normalizes purchase behavior among inbound travelers, which shifts travel insurance from a passive option to a standard trip requirement. Embedded coverage in visa pathways also reduces operational friction for carriers and platforms that process high volumes of short-stay visitors. The Saudi Arabia Travel Insurance market benefits as traveler volume objectives translate into policy issuance at scale, while product features adapt to activities linked to new destinations. Together, these levers build a predictable demand base that is aligned with the national tourism agenda.

Mandatory Umrah/Hajj Medical Cover Locks in Recurring Revenue

Pilgrimage travel is governed by rules that require medical insurance as a condition of entry, which creates a stable flow of policies across the year with concentrated peaks around the Umrah and Hajj seasons. The Council of Health Insurance defines benefits and provider networks for pilgrims, and official guidance details a 90-day validity framework that standardizes how coverage is delivered and used across approved facilities. The Ministry of Hajj and Umrah’s digital tools and official documents support issuance, verification, and claims, which lowers leakage and enhances compliance by linking insurance to every step of the pilgrimage journey[2]Ministry of Hajj and Umrah, “Document of the Rights of the Umrah Performer,” Ministry of Hajj and Umrah, haj.gov.sa. The Makkah Route Initiative completes many entry formalities in the country of origin, which enables earlier policy activation and smoother arrival processes that reinforce timely coverage. These measures keep protection near-universal in the pilgrimage corridor and anchor recurring revenue that reduces seasonal volatility for underwriters. This dynamic provides a structural foothold for the Saudi Arabia Travel Insurance market in years of fluctuating discretionary tourism.

Growing Outbound Middle-Class Spend Fuels Annual Multi-Trip Demand

A rise in outbound leisure, education, and caregiver travel among Saudi households is strengthening demand for policies that cover multiple trips in a year. Annual Multi-Trip formats reduce purchase frequency and provide predictable pricing, which suits families and professionals who cross borders several times for short stays. Sharia-compliant takaful carriers and leading insurers offer digital buying paths and wellness-linked services that improve perceived value while maintaining ease of use. Broader access to app-based enrollment and support also moves the point of purchase closer to everyday planning tools that travelers already use. Aggregators add transparency with side-by-side quotes and quick issuance, which helps non-expert buyers compare coverage terms with less friction. These behaviors lift the addressable base for repeat-use products and add momentum to the Saudi Arabia Travel Insurance market as travel patterns diversify.

Digital Issuance via eVisa Platform Accelerates Take-up

An insurance purchase embedded in visa steps shortens the path to coverage and standardizes the user experience for applicants across countries. The tourist visa and stopover programs require proof of medical insurance, which ensures that coverage is in force before travelers enter Saudi Arabia. Airline and visa platforms direct users through clear instructions on required fees and eligibility, which reduces ambiguity and support load during peak seasons. The approach aligns issuance with traveler identity verification and document checks, which raises policy accuracy and compliance. As a result, insurers and partners process large volumes with consistent enrollment flows while travelers benefit from a single, integrated journey. This operational model sustains the Saudi Arabia Travel Insurance market’s adoption curve without placing new burdens on travelers or agencies.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Low consumer awareness/price sensitivity | -1.8% | National, most acute in secondary cities and rural areas | Medium term (2-4 years) |

| Higher solvency‐capital requirements | -1.4% | National, disproportionately affecting smaller insurers | Short term (≤ 2 years) |

| Sparse post-COVID actuarial data | -0.9% | National, with a sector-wide impact on pricing accuracy | Medium term (2-4 years) |

| Bancassurance exclusivity limits aggregators | -0.7% | National, particularly in corporate distribution channels | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Low Consumer Awareness and Price Sensitivity Constrain Voluntary Uptake

Outside of visa-linked or pilgrimage-required purchase paths, many consumers still treat travel insurance as optional, which lowers penetration for outbound short-haul trips. Buyers who do not compare coverage features often focus on the lowest premium, which limits demand for comprehensive benefits that improve claims outcomes. Aggregator platforms have raised transparency by presenting multiple quotes and standardized information, but comparison shopping can also intensify price competition that compresses margins for full-featured products. Families with more predictable travel calendars are gradually adopting multi-trip options, yet awareness gaps remain among occasional travelers who underweight potential medical and cancellation risks. Wider digital access and clearer disclosures continue to narrow this gap, though behavior change outside mandatory channels requires consistent education over time. These factors create a drag on voluntary adoption even as the Saudi Arabia Travel Insurance market expands through embedded and regulated routes.

Higher Solvency-Capital Requirements Trigger Market Consolidation

Stronger prudential standards and governance expectations are raising the minimum scale needed to compete, which encourages combinations that pool capital and operating capabilities. Larger carriers can absorb compliance and technology investments more readily, which improves their ability to support integrated health and travel offerings at volume. Capital actions by reinsurers and insurers signal preparation for a more demanding regulatory environment that prioritizes resilience and risk management. Companies that expand internationally or bolster their capital base can diversify earnings and support product development that benefits frequent travelers and corporates. As prudential rules tighten, specialists and smaller players rely more on partnerships, digital distribution, and niche propositions to stay relevant. This tilt toward scale supports a more stable core for the Saudi Arabia Travel Insurance market while preserving innovation at the ecosystem edge.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Coverage Type: Single Trip Dominates, but Annual Multi-Trip Gains Momentum from Affluent Outbound Cohorts

Single Trip Travel Insurance accounted for 71.27% of the Saudi Arabia Travel Insurance market size in 2025, reflecting strong demand from inbound religious travelers and first-time visitors. Mandatory medical insurance for Umrah and Hajj creates a consistent base of one-time policies that align with the 90-day eligibility window defined in official guidance[3]Ministry of Hajj and Umrah, “Document of the Rights of the Umrah Performer,” Ministry of Hajj and Umrah, haj.gov.sa. Digital verification and standardized documents issued by the Ministry of Hajj and Umrah streamline proof of cover from application to departure, which encourages timely purchases. The stopover visa option requires medical insurance and allows quick enrollment through airline and visa interfaces, which routes more single-trip policies through embedded flows. Aggregators that present instant quotes across several carriers make one-time purchase decisions simple for casual or first-time travelers. As leisure beyond the holy cities extends to culture, entertainment, and coastal experiences, single-trip formats remain the default entry point for travelers who want straightforward cover for defined dates.

The Saudi Arabia Travel Insurance market size for Annual Multi-Trip is projected to expand at 10.34% CAGR between 2026 and 2031 as buyers weigh fewer transactions against wider coverage continuity. Takaful and cooperative carriers embed travel in digital health ecosystems and wellness programs, which improve day-to-day utility between trips. International plans from leading insurers bundle global access and high medical limits, which complement annual travel policies for expatriates and high-frequency travelers. App-based policy management and accessible telehealth increase perceived value for families who want prompt advice during emergencies abroad. As travelers plan for education, medical, and leisure itineraries across several countries, annual formats help control total spend while reducing purchase friction throughout the year.

By End User: Business Travelers Lead, but Family Leisure Surge Reflects Vision 2030 Consumer Shift

Business Travelers led in 2025 with a 37.81% share, supported by corporate travel tied to large-scale programs and international commerce. The Saudi Arabia Travel Insurance market benefits from established B2B relationships where insurance is embedded into corporate travel policies and procurement routines. Direct insurer channels serve these accounts through account managers and integrated claims support, which reinforces renewal stability. Digital issuance and endorsements enable small and mid-sized enterprises to add travel protection without complex onboarding, which broadens penetration in the business segment. Demand also comes from project-based movements and conferences that attract regional and overseas participants who require medical and trip interruption benefits. Internationally oriented plans appeal to executives who need higher medical limits and global provider access. These features help maintain the business segment’s weight in the Saudi Arabia Travel Insurance market even as leisure accelerates.

Family Travelers are forecast to grow at 10.93% CAGR through 2031 as tourism options expand and household travel budgets rise. The Saudi Arabia Travel Insurance industry is increasingly shaped by multi-generation trips that combine pilgrimage with culture, sports, and coastal stays, which increases the need for broader benefits and longer coverage windows. Official visa guidance that clarifies medical insurance requirements reduces uncertainty for first-time leisure visitors who travel with dependents. Takaful-led product suites include complementary lines such as domestic helper and home protection, which position travel as a logical add-on during family planning[4]Al Rajhi Takaful, “Shariah Compliance and Platforms,” Al Rajhi Takaful, alrajhitakaful.com. Aggregators help families match network coverage and benefit caps to personal health needs and destinations, which improves value realization at the point of purchase. As repeat outbound travel grows, households shift toward annual policies that provide continuous protection and reduce the need to re-enter medical information before every trip.

By Distribution Channel: Direct Sales Hold, but Digital Aggregators Disrupt with Speed and Transparency

Insurance Companies Direct held a 31.72% share in 2025 as large carriers leveraged brand strength, captive sales, and enterprise relationships to retain corporate and high-value individual accounts. Direct channels support complex benefit designs and provide claims coordination that many business travelers expect. Integrated propositions that bundle travel with health and assistance services strengthen retention where decision-makers value end-to-end service over marginal price differences. Digital self-service through insurer apps and portals complements in-person advisory for specialized travel patterns. As enterprise travel resumes and programmatic events multiply, the direct model remains resilient in accounts that prize continuity, negotiated service levels, and coordinated support.

Insurance Aggregators are projected to scale at a 9.51% CAGR through 2031, with instant comparisons and rapid policy issuance attracting price-sensitive and first-time buyers. The Saudi Arabia Travel Insurance market size for aggregators is projected to expand at 9.51% CAGR as platforms integrate more carriers and automate identity verification and documentation. Leading comparison portals display multiple travel and health options, issue certificates within minutes, and deliver policy documents for visa processing without manual handoffs. As households become more comfortable with app-based purchases, aggregators capture incremental demand that might otherwise defer or forgo coverage. Platform ratings and negotiated discounts reinforce customer trust and conversion. The Saudi Arabia Travel Insurance market, therefore, features a balanced channel mix in which aggregators drive acquisition at scale while direct carriers deepen enterprise and high-value relationships.

Geography Analysis

The Saudi Arabia Travel Insurance market shows natural concentration in corridors linked to international airports and pilgrimage routes, with Riyadh, Jeddah, Makkah, and Madinah serving the highest throughput. Policy issuance in the Makkah and Madinah corridor is closely tied to the mandated coverage for Umrah and Hajj, which ensures that inbound pilgrims are protected under standardized benefits. Government platforms and ministry documents coordinate the digital steps for pilgrims, which support timely enrollment and consistent claims settlement in designated networks. Riyadh hosts many corporate headquarters and insurers, which anchor product design and account servicing for business travel. Digital issuance tied to visa processes also spreads activation to points of origin, which distributes purchase flows across international markets while concentrating claims and assistance near Saudi destinations.

Tourism-led development is shifting more itineraries to the northwest and west coasts as giga-projects reach operational milestones. NEOM and the Red Sea destinations expand the mix of activities, which broadens coverage needs to include adventure benefits and higher medical assistance availability. Cultural hubs like AlUla add heritage and nature experiences to typical pilgrim journeys, which lengthen stays and increase the use of policies that combine multiple stops. Entertainment and sports venues near Riyadh extend domestic and inbound travel calendars into off-peak periods, which reduces seasonality in support volumes. Insurers respond with flexible add-ons that cover leisure activities at new sites, while assistance providers adjust networks to meet expected visitor flows across these zones. These patterns reinforce the geographic diversification of the Saudi Arabia Travel Insurance market as travelers add non-religious segments to their itineraries.

On the Red Sea coast, Jeddah’s role as a gateway for both pilgrims and leisure travelers continues to grow, and insurers market products that target expatriates and family visitors who split time between holy sites and coastal stays. Cross-border trips to and from neighboring Gulf states contribute a steady stream of short-duration policies that require straightforward medical coverage and roadside assistance links. Government clarity on visa-linked insurance helps keep inbound compliance high, which reduces disputes and improves the experience at ports of entry and departure. As the distribution footprint modernizes, aggregators reach secondary cities through digital onboarding and fulfillment. This unlocks white-space pockets of demand outside historical centers and supports inclusive growth in the Saudi Arabia Travel Insurance market.

Competitive Landscape

The Saudi Arabia Travel Insurance market features a mix of scale incumbents and specialist players that compete through product breadth, digital experience, and Sharia-compliant models. Large cooperative and takaful carriers distribute through direct and partner channels while investing in apps and portals that shorten issuance and claims timelines. International health plans that include global provider access strengthen value for frequent travelers and expatriates who require cross-border medical support. Aggregators attract new buyers with easy comparisons and promised price parity or better, which drives share gains in mass-market segments. At the same time, selected carriers emphasize Sharia governance and product certification to meet the preferences of customers who want takaful-based protection.

Capital moves and geographic expansion by reinsurance and primary players reinforce balance sheet strength and market reach. Saudi Re’s expansion into India aims to deepen access to Asian risk pools and diversify business lines, which supports capacity for cross-border travel products. The firm’s role as an exclusive reinsurer for national programs underscores a focus on structured, long-term arrangements that can stabilize underwriting cycles. Ownership changes among insurers, including the exit of a major global group from a local joint venture, have reshaped competitive strategies and brand positioning in selected lines. New entrants from the wider Gulf market have also established local operations to serve expatriates and residents who recognize their brands, which increases choice for consumers seeking motor, health, and travel bundles.

Product innovation centers on embedding travel protection within visa pathways, airline interactions, and health platforms. Direct carriers highlight end-to-end assistance and robust provider networks, which appeal to business accounts and families with specific medical needs. Aggregators bring reach and speed that cater to budget-focused segments and first-time buyers who want clarity more than bespoke advice. Targeted promotions through insurer apps stimulate trials in off-peak months and encourage add-on purchases for visitors and residents planning short domestic breaks and regional trips. As regulatory frameworks emphasize prudence and technology-driven oversight, scale carriers and reinsurers are well positioned to extend digital, Sharia-compliant, and multi-trip solutions that match evolving travel patterns across and beyond the Kingdom.

Saudi Arabia Travel Insurance Industry Leaders

Tawuniya

Bupa Arabia

Allianz Saudi Fransi

Gulf Insurance Group – Saudi

MedGulf

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Saudi Reinsurance Company (Saudi Re) launched a new branch in GIFT City, India, to enhance its presence in the Asian reinsurance market. This strategic expansion follows revenue and profitability gains in 2025 and positions the company to support cross-border travel insurance risk flows.

- November 2025: Orient Insurance KSA officially opened operations in Saudi Arabia on November 24, 2025, marking the entry of a well-established UAE insurer with over 40 years of experience into the Kingdom.

- December 2025: Medgulf obtained Sharia compliance certification from Shariyah Review Bureau on December 31, 2025, enabling the company to market Takaful-compliant products to Sharia-conscious consumers.

- February 2026: Amana Cooperative Insurance re-qualified its health insurance branch with the Insurance Authority on February 23, 2026, maintaining its operational license for one year.

Saudi Arabia Travel Insurance Market Report Scope

The travel insurance market refers to the industry that provides insurance policies covering financial risks associated with travel, such as trip cancellations, medical emergencies, lost baggage, and travel delays. The report focuses on the complete background of the Saudi Arabia Travel Insurance Market, which comprises an assessment of the developing market trends by segments, important changes in the market dynamics, and a market overview. Saudi Arabia Travel Insurance Market is Segmented By Insurance Coverage (Single-Trip Travel Insurance, Annual Multi-trip Travel Insurance, and Others), By Distribution channels (Direct Sales, Online Travel Agents, Airports And Hotels, Brokers, and Other Insurance Intermediaries), and By End-User (Senior Citizens, Business Travelers, Family Travelers, and Others (Education Travelers, etc)). The report offers market size and forecast values for the Saudi Arabia Travel Insurance Market in USD million for the above segments.

By Coverage Type

| Single Trip Travel Insurance |

| Annual Multi-Trip Travel Insurance |

By End User

| Senior Citizens |

| Education Travelers |

| Business Travelers |

| Family Travelers |

| Other End-Users |

By Distribution Channel

| Insurance Intermediaries |

| Insurance Companies (Direct) |

| Banks |

| Insurance Brokers |

| Insurance Aggregators |

| By Coverage Type | Single Trip Travel Insurance |

| Annual Multi-Trip Travel Insurance | |

| By End User | Senior Citizens |

| Education Travelers | |

| Business Travelers | |

| Family Travelers | |

| Other End-Users | |

| By Distribution Channel | Insurance Intermediaries |

| Insurance Companies (Direct) | |

| Banks | |

| Insurance Brokers | |

| Insurance Aggregators |

Key Questions Answered in the Report

What is the size and growth outlook for the Saudi Arabia Travel Insurance market to 2031?

The Saudi Arabia Travel Insurance market size was USD 437.41 million in 2025 and is projected to reach USD 953.17 million by 2031 at a 13.86% CAGR from 2026 to 2031.

Which coverage type leads and which is growing the fastest in Saudi Arabia?

Single Trip led with 71.27% share in 2025, while Annual Multi-Trip is forecast to grow at a 10.34% CAGR through 2031.

Which end-user segments are most important in Saudi Arabia travel protection?

Business Travelers held 37.81% in 2025, and Family Travelers are the fastest growing at a 10.93% CAGR through 2031 as leisure broadens under Vision 2030.

How do regulations shape demand for travel insurance in Saudi Arabia?

Medical insurance is required for tourist visas and stopover entries, and coverage for Umrah and Hajj is mandatory with a 90-day framework for eligible services.

What role do aggregators play in Saudi Arabia’s travel insurance distribution?

Aggregators present instant comparisons across multiple carriers, enable quick issuance for visa processing, and are projected to grow faster than direct channels.

Which offerings resonate with frequent and expatriate travelers in Saudi Arabia?

Annual multi-trip policies and international health plans with global networks appeal to repeat travelers and expatriates who seek continuous coverage and higher medical limits.

Page last updated on: