Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

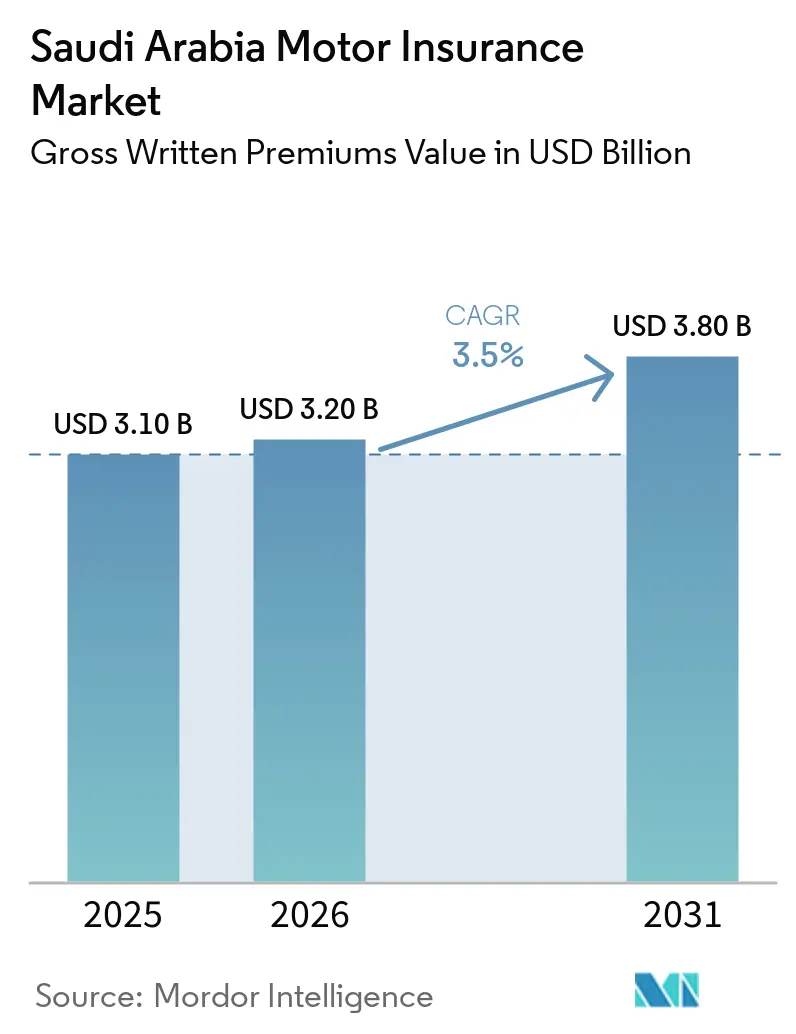

| Base Year Market Size (2025) | USD 3.10 Billion |

| Market Size (2026) | USD 3.20 Billion |

| Market Size (2031) | USD 3.80 Billion |

| Growth Rate (2026 - 2031) | 3.50% CAGR |

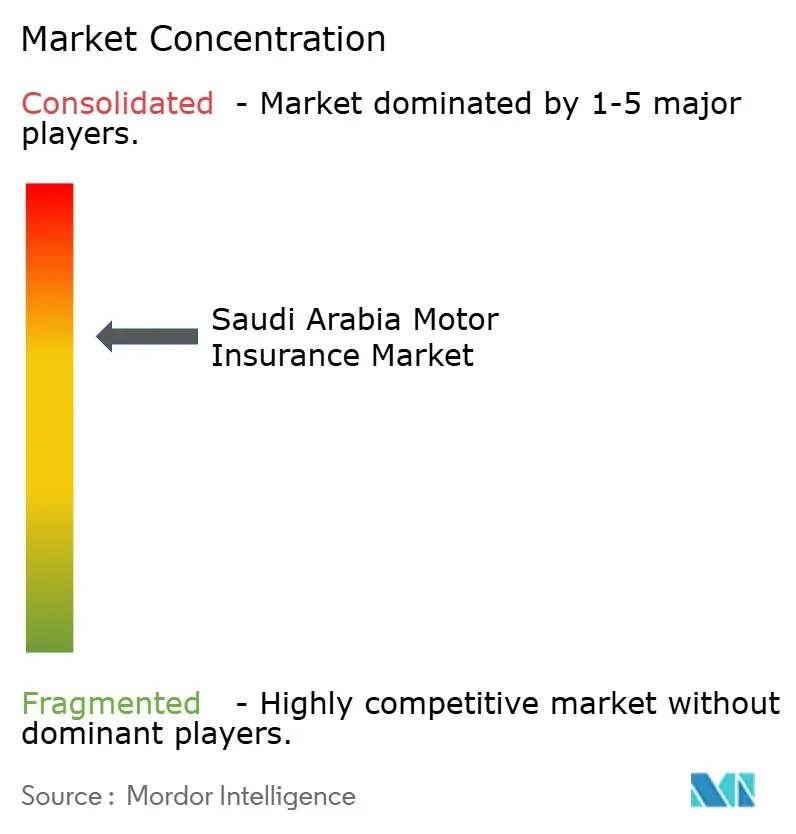

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Saudi Arabia Motor Insurance Market Analysis by Mordor Intelligence

The Saudi Arabia Motor Insurance Market size in terms of gross written premiums value is projected to be USD 3.10 billion in 2025, USD 3.20 billion in 2026, and reach USD 3.80 billion by 2031, growing at a CAGR of 3.5% from 2026 to 2031.

The growth trajectory is anchored by stricter electronic enforcement of compulsory cover, amended comprehensive-policy rules that broaden covered drivers, an ongoing shift to aggregator-led distribution, and faster digital claims processing that improves retention and reduces leakage. Regulatory changes have introduced a mandatory 30% local reinsurance cession and tighter supervisory oversight, which lifts capital resilience and underwriting discipline but also increases operating costs for mid-tier carriers. Digital-first issuance on licensed aggregators is expanding, which compresses acquisition costs for scale players while creating pricing transparency that reins in unprofitable competition in third-party liability lines. Claims digitization led by Najm and integrated with standardized damage valuation has shortened cycle times and cut loss-adjustment expenses, which supports the pivot away from highly commoditized TPL into comprehensive and telematics-enriched products[1]Najm Corporate Communications, “Najm Services and Digital Claims Journey,” Najm for Insurance Services, najm.sa. Consolidation and operating model upgrades signal a market preparing for risk-based capital rules in 2027 and aligning product design with regulatory intent and consumer expectations.

Key Report Takeaways

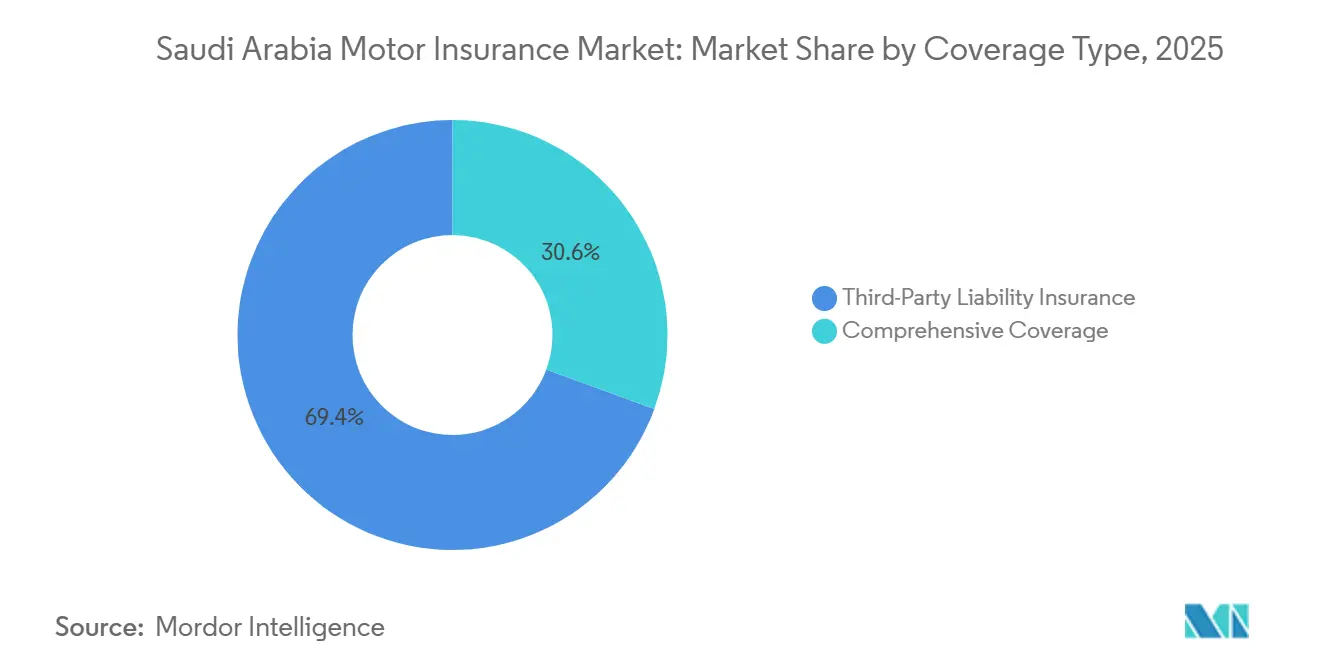

- By coverage type, Third-Party Liability held 69.4% of the Saudi Arabia motor insurance market share in 2025, while comprehensive coverage is forecast to expand at a 9.7% CAGR through 2031.

- By distribution channel, aggregators and comparison portals captured 74.4% of retail motor flows in 2025, and embedded, or platform partnerships are projected to grow at a 13.9% CAGR to 2031.

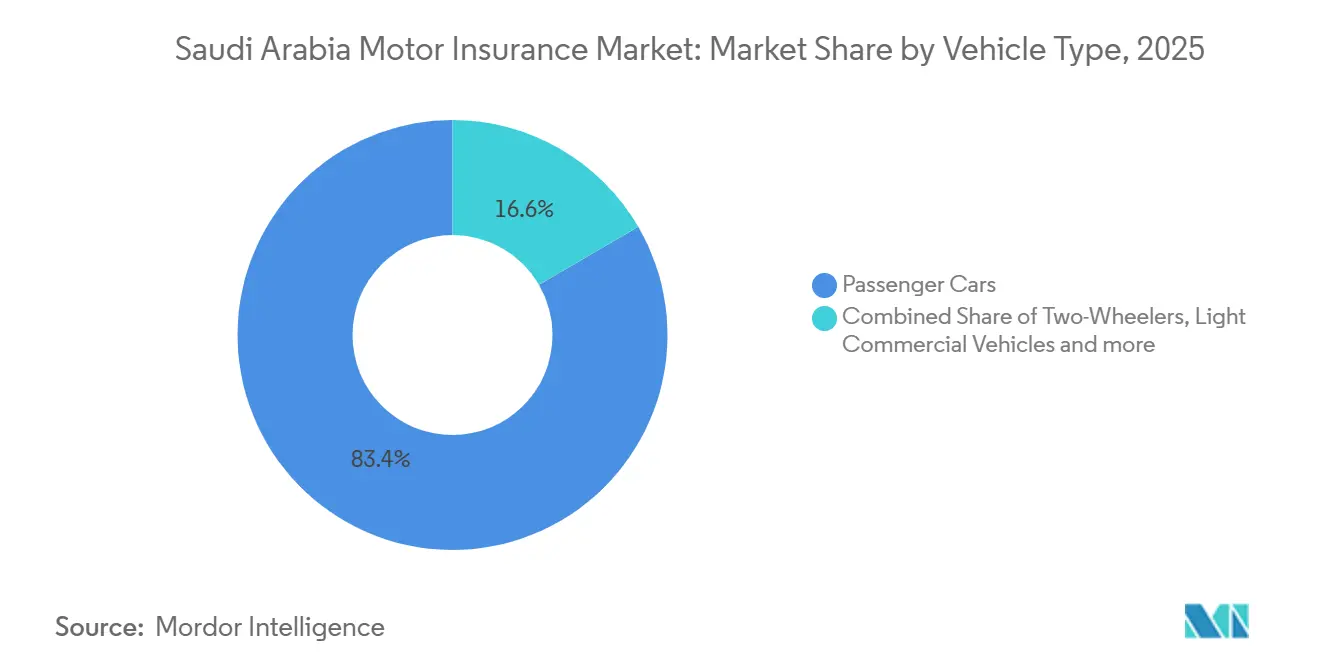

- By vehicle type, passenger cars accounted for an 83.38% share in 2025 and are advancing at a 7.4% CAGR through 2031.

- By vehicle age, used vehicles held a 57.4% share in 2025, while new vehicles are projected at an 8.2% CAGR through 2031.

- By geography, Central region together accounted for a 34.35% share in 2025, and the Western Region is projected at a 7.16% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Saudi Arabia Motor Insurance Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Electronic monitoring of uninsured vehicles lifts compliance | +0.8% | National, with early gains in Riyadh, Jeddah, and Dammam metropolitan clusters | Short term (≤ 2 years) |

| Broadened comprehensive policy rules spur upgrades from TPL | +1.1% | National, led by Central and Western Regions (Riyadh, Jeddah corridors) | Medium term (2-4 years) |

| Robust vehicle sales expand the insurable car parc | +0.7% | National, strongest in urban hubs | Medium term (2-4 years) |

| Aggregator-led distribution and embedded partnerships scale issuance | +0.5% | National, amplified in digitally mature cities | Short term (≤ 2 years) |

| Digitized claims stack shortens cycle times and reduces friction | +0.4% | National, with highest throughput in Central and Eastern Regions | Long term (≥ 4 years) |

| Saudization of sales roles improves compliance and upsell | +0.2% | National, with pilot programs concentrated in major metropolitan areas | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Electronic Monitoring Of Uninsured Vehicles Lifts Compliance And Policy Volumes From 2026

Saudi Arabia’s electronic monitoring program flags uninsured vehicles through periodic plate scans and issues automated notices, which has expanded the insured pool and stabilized policy renewals as coverage compliance rises in large cities. The integration of monitoring outputs with digital government services further reduces administrative lag for policy updates and renewals. The combination of enforcement and automated verification has curbed lapse rates and bolstered on-time renewals in metropolitan corridors where adoption of digital services is high. Insurers report that volume gains first flowed into TPL portfolios, prompting a later pivot to comprehensive upselling as pricing in TPL began to normalize with better capacity discipline. The resulting mix shift supports the Saudi Arabia motor insurance market as more customers move from compliance-only protection to broader own-damage cover. Execution differences remain by region based on digital penetration and enforcement intensity, which preserves pockets of opportunity for targeted outreach through aggregator channels.

Broadened Comprehensive Policy Rules Spur Upgrades From TPL From 2026

Comprehensive rules amended in November 2023 expanded coverage to include close relatives and sponsored drivers under individual policies, which improves the value proposition for multi-driver households and catalyzes upgrades from TPL. The rule change also preserved customization flexibility for corporate buyers, which keeps fleet procurement aligned with tailored needs while raising baseline protections for individual clients. The February 2025 leasing clarification reinforced competitive procurement by requiring multiple quotes, which encourages adoption of embedded insurance flows at the point of sale and reduces binding friction for lessees[2]Saudi Press Agency Staff, “Amended Comprehensive Motor Insurance Rules Take Effect,” Saudi Press Agency, spa.gov.sa. Insurers are responding with tiered products that bridge the gap between TPL and full comprehensive, which softens price sensitivity while expanding own-damage protections. The combined regulatory push and product innovation underpin a measured rise in comprehensive uptake in higher-income corridors where vehicle values and financing penetration are higher. This conversion dynamic supports the Saudi Arabia motor insurance market as large city buyers shift toward broader cover and family-inclusive policies.

Aggregator-Led Distribution And Embedded Partnerships Scale Retail Issuance

Licensed aggregators and comparison portals have become the dominant retail distribution route, aggregating quotes from multiple insurers and enabling real-time binding with automated data submission. The leading platforms integrate directly with insurer systems and digital government services to confirm policy updates, which helps reduce issuance time to minutes and lowers acquisition costs for scale players. App-based features such as policy comparisons, installment options, and automated renewal prompts improve conversion and keep customers within digital ecosystems favored by insurers and regulators. Embedded models at dealerships, lenders, and consumer-finance apps extend this reach by placing motor coverage at the point of vehicle financing or checkout, which aligns product selection with customer intent and lender requirements. Incumbents are also building captive digital agencies to internalize aggregator economics and protect pricing power on renewal cohorts. The acceleration of platform-based distribution reinforces transparency and standardization in policy issuance, which supports sustainable growth in the Saudi Arabia motor insurance market as digitally mature customers adopt aggregator journeys.

Digitized Claims Stack Shortens Cycle Times And Reduces Friction

The claims digitization stack, led by Najm for accident reporting and integrated with standardized damage valuation platforms, compresses processing times and reduces manual handoffs for minor incidents. On-site response in major cities and electronic issuance of accident reports enable faster filing, while standardized estimates streamline interactions between workshops and insurers. These linkages cut loss-adjustment expenses and improve customer experience, which lifts renewal propensity on comprehensive lines where service quality drives retention. Partnerships to enhance data exchange and technology capabilities have strengthened the sector’s digital infrastructure, which supports secure data processing, better KYC, and scalable claims workflows[3]Editorial Team, “ZainTECH and Najm Partner to Drive Digital Transformation,” ZainTECH, zaintech.com. The digitization push also sets the groundwork for telematics-driven products that reward safe driving, which can further differentiate comprehensive offerings and reduce frequency and severity over time. As these improvements propagate beyond major cities, they will widen the impact on the Saudi Arabia motor insurance market through higher satisfaction and lower leakage.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| TPL rate softening and pricing cyclicality pressure margins | -0.6% | National, most acute in high-volume retail TPL segments in Central and Western Regions | Medium term (2-4 years) |

| Loss-cost inflation in parts, labor, and repair networks | -0.4% | National, amplified in Eastern Region and import-heavy Western corridors | Short term (≤ 2 years) |

| Low comprehensive uptake among price-sensitive cohorts | -0.3% | National, with lower-income Southern and Northern Regions most exposed | Medium term (2-4 years) |

| Data privacy and compliance burdens for aggregators and embedded channels | -0.1% | National, with enforcement intensity highest in Riyadh | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

TPL Rate Softening And Pricing Cyclicality Pressure Underwriting Margins

Price competition intensified through 2024 and early 2025 as aggregators’ transparency and capacity additions drove TPL premiums lower in key urban markets, which pressured underwriting results and pushed combined ratios above sustainable levels for several players. Rate stabilization began later in 2025 as carriers curtailed loss-making capacity and shifted focus to comprehensive upselling, but residual cyclicality in TPL remains a structural challenge for margin durability. Public updates from leading insurers noted the return of measured rate increases in Q3 2025, reflecting healthier pricing discipline when volume-led growth reached its limit. The distribution shift toward aggregators amplifies this pattern since lowest-price ranking mechanics can pull rates down unless carriers enforce minimums and value-adds. The local cession requirement improves capital buffers but does not remove the cyclicality risk in TPL, which remains standardized on cover and thus highly sensitive to price movements. The persistence of this restraint continues to weigh on the Saudi Arabia motor insurance market until mix shifts and product differentiation mitigate pure price competition.

Loss-Cost Inflation In Parts, Labor, And Repair Networks

Repair-cost inflation from parts and labor has raised average claim severities and put pressure on comprehensive pricing and deductibles. Workshop capacity in import-heavy regions faces longer lead times and higher markups on non-GCC brands, which lifts cost per repair and extends settlement timelines if not tightly managed with preferred networks. Standardized valuation platforms help align estimates, yet disputes over actual repair invoices can still occur and add to administrative load. Scale players are investing in preferred repair networks and negotiating parts supply to cap cost escalation and protect settlement speed for comprehensive claims. Insurers with tighter workshop integration tend to show better settlement metrics and lower leakage, which supports retention but requires operational scale to replicate across regions. The short-term impact of cost inflation remains a drag on the Saudi Arabia motor insurance market until supply chains and workshop throughput normalize.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Coverage Type: TPL anchors volume, comprehensive upgrades pivot strategy

Third-party liability accounted for 69.4% of Saudi Arabia's motor insurance market share in 2025, while comprehensive rose on the back of regulatory support and product innovation that strengthened the upgrade path from TPL. The comprehensive segment is projected to expand at a 9.7% CAGR through 2031 as aggregators and embedded flows at the point of leasing lift attach rates for own-damage cover in higher-value vehicles. Insurers are deploying tiered offers that add value without full comprehensive pricing, which helps bridge customer expectations to broader protection. The November 2023 rule changes that expanded coverage to close relatives and sponsored drivers improved perceived value for multi-driver households, supporting balanced growth in comprehensive policies. As more customers experience improved claims service through digitized processes, willingness to trade up from compliance-only cover is improving in urban corridors. This mix evolution positions the Saudi Arabia motor insurance market to gradually rebalance away from hyper-commoditized TPL.

Comprehensive’s momentum is reinforced by platform-enabled comparison that makes total cost and features visible at decision time, which reduces friction for buyers already engaged in vehicle financing. Leading insurers are prioritizing product clarity and modular add-ons such as roadside assistance and geographical extensions, which support higher average premiums with transparent value. Regions with higher vehicle values and stronger financing penetration see faster conversion to comprehensive, which raises per-policy revenue and stabilizes retention on multi-year financing cohorts. TPL remains essential for volume and compliance, but growth in TPL aligns with vehicle-parc expansion rather than pricing, which keeps margins thin when competition accelerates. As rate cycles in TPL stabilize, carriers are expected to maintain focus on comprehensive differentiation and service quality, which supports long-term sustainability in the Saudi Arabia motor insurance market.

By Distribution Channel: Aggregators dominate retail, embedded partnerships surge fastest

Aggregators and comparison portals captured 74.4% of retail flows in 2025, reflecting consumer preference for unified digital journeys and rapid quote-to-bind execution. The leading platforms connect to more than 20 insurers, confirm policy updates in near real time, and provide installment options that reduce upfront friction for price-sensitive buyers[4]Product Team, “Tameeni Insurance | Compare Over 20+ Insurance Companies,” Rasan Tameeni, tameeni.com. Digitally mature cities show the highest aggregator adoption, which accelerates the tilt from agent-led channels to app-based issuance. Embedded and platform partnerships are projected to grow at a 13.9% CAGR through 2031 as OEM dealers, lenders, and fintech checkouts place insurance directly into transaction flows. This model aligns underwriting with lender risk appetite and compresses acquisition cost, which improves unit economics for larger carriers. The direct channel continues to serve retention plays, while corporate fleets remain relationship-led through brokers and agents for tailored programs.

Insurers are also building captive digital agencies that internalize aggregator economics, keep renewal pools within their ecosystems, and offer benefits such as installment payments and expedited claims. Platform economics introduce new compliance obligations on data privacy, cybersecurity, and disclosure, which leading aggregators address through app updates and transparency features aligned with regulatory guidance. The model’s efficiency and standardization support balanced growth and better service quality in the Saudi Arabia motor insurance market, though carriers must calibrate commissions and pricing floors to avoid reintroducing unsustainable cycles. As embedded flows mature, more comprehensive upgrades at point of sale should reinforce the premium mix improvement already visible in higher-income urban corridors. Over time, scale advantages in technology and partnerships are likely to deepen, favoring carriers with modernized cores and robust API connectivity.

By Vehicle Type: Passenger cars dominate, commercial uptake constrained by retention gaps

Passenger cars accounted for 83.38% of Saudi Arabia's motor insurance market share in 2025 and are projected at a 7.4% CAGR through 2031, leading both in share and growth due to private-vehicle prevalence and strong urban demand. The passenger-car mix benefits from financing penetration and better feature sets that encourage comprehensive adoption, which improves per-unit revenue and retention on multi-year loan tenures. Light commercial vehicles contribute meaningfully in logistics-heavy corridors but carry lower comprehensive attachment due to SME cost sensitivity. Medium and heavy commercial vehicles command high per-policy premiums yet often rely on reinsurance for risk dispersion, which limits direct revenue capture by primary insurers. Telematics-ready offerings are beginning to differentiate comprehensive propositions in passenger cars and could later extend to fleets as data governance standards mature. As more customers experience smoother claims via standardized workflows, retention on comprehensive lines should strengthen passenger-car momentum.

Commercial segments face distinct constraints related to underwriting depth, spare-part availability for imported vehicles, and workshop capacity, which raise the bar for profitable retention. Scale carriers are building fleet-underwriting capabilities and negotiating workshop terms to improve control over cost and turnaround times, while smaller players pursue selective participation. Two-wheelers remain a marginal segment under current usage and safety norms, which limits their contribution to volume and revenue. The near-term path of growth in the Saudi Arabia motor insurance market remains anchored in passenger vehicles, supported by platform sales, financing mandates during loan tenure, and product modularity that eases transition from TPL to broader cover. As embedded offers expand in dealer and lender ecosystems, passenger cars will continue to set the pace for mix improvement and balanced growth.

By Vehicle Age: Used vehicles lead share, new-car growth outpaces on financing mandates

Used vehicles held a 57.4% share in 2025, while new vehicles, supported by bank-financing requirements for comprehensive cover, show faster growth with an 8.2% projected CAGR. Aggregators and embedded flows at dealerships simplify binding at purchase, which raises comprehensive attach rates and helps newer cohorts stay insured through the financing period. Older vehicles skew toward TPL due to price sensitivity and parts depreciation, which depresses comprehensive uptake and narrows margins when competition intensifies. Insurers are introducing hybrid offerings that provide limited own-damage protection for used vehicles at lower premiums, which appeals to owners seeking partial coverage without the full cost of comprehensive. Claims frequency and severity dynamics differ by age, and carriers calibrate deductibles and benefit limits accordingly to protect margins. Over the forecast, the new-vehicle cohort acts as a stabilizer for premium quality and retention.

Geographically, used-vehicle concentration is higher in regions with lower average incomes and sparser dealer networks, which rely more on aggregator outreach and awareness campaigns to improve conversion. New-vehicle buyers in large cities display higher comprehensive attachment due to financing and dealership integration, which strengthens the revenue base and provides multi-year retention from loan-linked policies. Digital claims convenience and rapid updates post-incident help limit churn across both cohorts, but the uplift is more pronounced on comprehensive lines where service quality is a bigger driver of loyalty. As financing and embedded issuance expand, the balance within the Saudi Arabia motor insurance market should continue to tilt toward newer vehicles with broader protection. This mix is supportive of sustainable growth and resilient profitability through the cycle.

Geography Analysis

Central Region accounted for 34.35% of premiums in 2025, led by Riyadh’s dense vehicle base, large corporate presence, and early adoption of digital issuance and claims services. Compliance-led TPL flows exited the trough as enforcement took hold in metropolitan clusters, while product differentiation and telematics pilots have nudged a measured rise in comprehensive penetration in higher-income segments. As the compliance dividend matures, the Central Region’s growth moderates while maintaining leadership in absolute premium volume. Efficient claims handling through Najm and integrated damage valuation systems helps preserve retention in Central corridors, which sets a benchmark for service standards nationally. The concentration of leading insurers and digital-first distribution supports continued process optimization and mix improvement in this region.

Growth shifts toward the Western Region with a 7.16% projected CAGR through 2031, supported by economic expansion across Jeddah and the religious tourism corridor that drives seasonal vehicle activity and rental demand. Aggregators and embedded flows are strengthening reach along dealer networks, and standardized claims processes improve service quality in urban districts, which lifts renewal rates and encourages upgrades from TPL to broader cover. Logistics and port activity sustain light-commercial demand, while consumer finance and dealership integrations help maintain comprehensive attachment in new-vehicle sales. As digital infrastructure and workshop capacity deepen, Western Region performance is expected to contribute a growing share of premium gains for the Saudi Arabia motor insurance market. The combination of large population centers and channel modernization is central to this trajectory.

Eastern Region contributes a sizable premium base given corporate fleets and imported high-value vehicles, which raises average insured sums and comprehensive mix where employer mandates apply. Preferred workshop networks and negotiated parts supply are more important in this region due to import intensity, which can mitigate the friction from longer parts lead times and higher markups. Southern and Northern Regions present catch-up potential as Najm’s footprint expands and aggregator adoption rises, helping close service gaps and reduce accident-to-settlement timelines. As digital issuance expands and localized hiring supports community engagement, these regions can contribute incremental volume over the long term. Balanced progress on enforcement, workshop capacity, and channel reach should help the Saudi Arabia motor insurance market extend coverage and improve retention beyond the largest cities.

Competitive Landscape

Market concentration sits at moderate-to-high levels, with the top five players together holding a significant share of industry premiums in 2025. Tawuniya led the national market with a 27.49% revenue share as of Q3 2024, supported by multi-channel distribution, a strong digital app, and captive aggregator economics through a proprietary digital agency. Al Rajhi Takaful maintained a large-scale presence with a Sharia-compliant model and a strong mobile interface, while MedGulf gained retail and SME reach after merging with Buruj in late 2025. Walaa focused on property and casualty insurance lines with efforts to optimize workshop partnerships for loss control, although broader TPL rate cycles weighed on results in 2025. The concentration profile supports investments in digitization and telematics pilots, which smaller carriers find harder to replicate at scale.

Consolidation accelerated as capital and operating requirements tightened and as local cession rules took effect in 2025, which increased the value of scale and prudent risk transfer. The MedGulf and Buruj merger created the fourth-largest player by combining capital bases and distribution footprints, positioning the company to push deeper into retail lines where comprehensive attachment trails corporate segments. Arabian Shield finalized its merger with Alinma Tokio Marine in late 2023, and other mid-tier mergers remained under evaluation, a trend aligned with the adoption of risk-based capital expected in 2027. The local cession mandate improved domestic reinsurance capacity and encouraged primary insurers to refine treaty placements, which became a differentiator in protecting margins on comprehensive while cushioning volatility in TPL. The M&A wave and treaty optimization reflect how the Saudi Arabia motor insurance market is reorganizing around sustainability and capital efficiency.

Strategic differentiation increasingly centers on digital distribution and claims, Sharia-compliant propositions, and workshop-network control. Captive digital agencies and app-first servicing help carriers internalize economics otherwise paid to aggregators, while embedded issuance at dealers and lenders places cover within customer purchase journeys. Najm’s telematics collaboration with technology partners has enabled pilots that reward safer driving with premium discounts, laying a path for risk-based pricing that can reduce frequency and severity over time. Preferred workshop arrangements and negotiated parts procurement aim to reduce claim severity and settlement delays, which strengthens retention and aligns with customer expectations for comprehensive coverage. As digitization and data sharing standards advance, players with modernized cores, API connectivity, and strong ecosystem partnerships are likely to consolidate their share in the Saudi Arabia motor insurance market. The result is a competitive field where scale, technology, and product design drive an advantage that compounds over time.

Saudi Arabia Motor Insurance Industry Leaders

Tawuniya

Al Rajhi Takaful

MedGulf

GIG

Walaa

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: The Insurance Authority suspended United Cooperative Assurance (UCA) from issuing or renewing all motor insurance policies, including comprehensive motor insurance, effective February 19, 2026, after the company failed to correct operational deficiencies negatively impacting policyholders and beneficiaries; UCA remains obligated to honor existing policies and claims, with the suspension remaining until compliance with regulatory standards is achieved, reflecting the Authority's intensified oversight to stabilize the sector and protect stakeholder rights.

- January 2026: Saudi Reinsurance Company (Saudi Re) launched a new branch in Gujarat International Finance Tec-City (GIFT City), India, aligning with the company's expansion strategy and geographic risk diversification; the Asian market accounts for 22% of Saudi Re's business portfolio, and India is among the company's largest international markets and one of the world's top ten insurance markets with total premiums exceeding USD 130 billion, with this move fully aligned with the National Insurance Strategy's objective to enable Saudi reinsurance companies to expand globally.

- November 2025: – Mediterranean and Gulf Cooperative Insurance and Reinsurance Company (MEDGULF) and Buruj Cooperative Insurance Company completed their merger, with Buruj merging into MEDGULF to form the fourth-largest insurer in Saudi Arabia; under the all-share agreement, MEDGULF issued 33.2 million new ordinary shares (SAR 10 nominal value each) to Buruj shareholders at a 1.11:1 exchange ratio, increasing MEDGULF's share capital by 31.58% from SAR 1.1 billion to SAR 1.4 billion, with former Buruj shareholders holding a 24% stake in the combined entity and trading in Buruj shares suspended for permanent delisting from Tadawul.

- September 2025: Najm for Insurance Services and Elm Company signed a cooperation agreement during the Money20/20 Middle East conference to enhance data exchange and technological services within the Saudi insurance sector, establishing a legal framework for data processing, sharing, transfer, and exchange between both organizations while cooperating on the development and protection of digital systems; this agreement aims to build an advanced and secure digital infrastructure for the insurance sector, supporting Saudi Vision 2030 objectives.

Saudi Arabia Motor Insurance Market Report Scope

The motor insurance market is defined as the segment of the insurance industry that offers financial protection and coverage for motor vehicles against risks such as accidents, theft, fire, and third-party liabilities.

The Saudi Arabia motor insurance market is segmented by insurance type and distribution channel. By insurance type, the market is segmented into third-party liability and comprehensive. By distribution channel, the market is segmented into agents, brokers, banks, online, and other distribution channels. The report offers market size and forecasts in terms of value (USD) for all the above segments.

By Coverage Type

| Third-Party Liability Insurance |

| Comprehensive Coverage |

By Distribution Channel

| Insurance Agents / Brokers |

| Direct Sales |

| Bancassurance |

| Embedded / Platform Partnerships |

| Aggregators & Comparison Portals |

By Vehicle Type

| Passenger Cars |

| Two-Wheelers |

| Light Commercial Vehicles |

| Medium & Heavy Commercial Vehicles |

By Vehicle Age

| New Vehicles |

| Used Vehicles |

By Geography (Saudi Regions)

| Central Region |

| Western Region |

| Eastern Region |

| Southern Region |

| Northern Region |

| By Coverage Type | Third-Party Liability Insurance |

| Comprehensive Coverage | |

| By Distribution Channel | Insurance Agents / Brokers |

| Direct Sales | |

| Bancassurance | |

| Embedded / Platform Partnerships | |

| Aggregators & Comparison Portals | |

| By Vehicle Type | Passenger Cars |

| Two-Wheelers | |

| Light Commercial Vehicles | |

| Medium & Heavy Commercial Vehicles | |

| By Vehicle Age | New Vehicles |

| Used Vehicles | |

| By Geography (Saudi Regions) | Central Region |

| Western Region | |

| Eastern Region | |

| Southern Region | |

| Northern Region |

Key Questions Answered in the Report

What is the current Saudi Arabia motor insurance market size and growth outlook to 2031

The Saudi Arabia motor insurance market size was USD 3.1 billion in 2025 and is projected to reach USD 3.8 billion by 2031 at a 3.5% CAGR, supported by regulatory modernization, digital distribution, and claims digitization.

Which coverage type leads and which is growing fastest in Saudi Arabia

Third-party liability led with 69.4% share in 2025, while comprehensive is the fastest growing with a projected 9.72% CAGR, reflecting upgrades as rules broaden covered drivers and embedded issuance expands.

How are aggregators changing buying behavior in Saudi Arabia motor insurance

Licensed aggregators and embedded platforms now dominate retail issuance by simplifying comparisons, accelerating binding, and enabling installments, which improves conversion and nudges upgrades to comprehensive cover.

Which regions contribute most to premiums in Saudi Arabia

Central Region led with 34.35% of 2025 premiums, while Western Region is projected to grow fastest through 2031, supported by urban demand, logistics activity, and strong aggregator penetration.

What are the main risks to profitability in the Saudi Arabia motor insurance market

TPL pricing cyclicality and loss-cost inflation in parts and labor pressure margins, which carriers counter with product mix shifts to comprehensive, workshop partnerships, and digitized claims workflows.

How will local reinsurance cession rules affect primary insurers in Saudi Arabia

The 30% local cession improves capital resilience and encourages more selective growth, while making treaty optimization a key lever for protecting margins on comprehensive and stabilizing TPL exposure.

Page last updated on: