Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

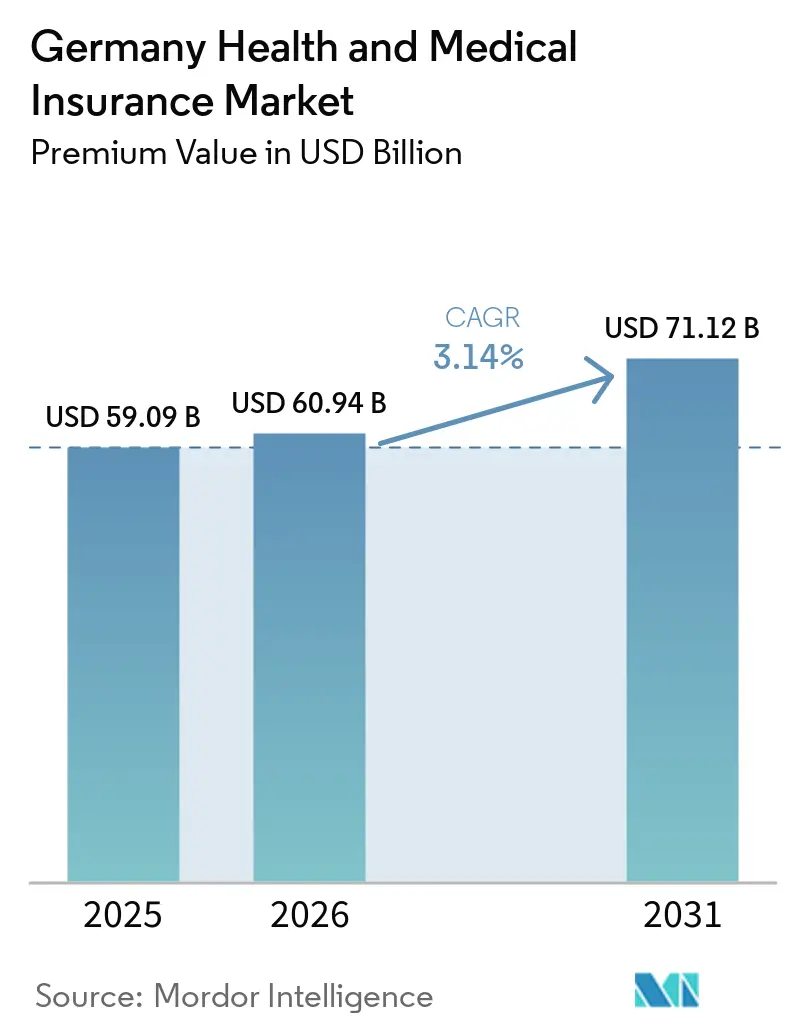

| Base Year Market Size (2025) | USD 59.09 Billion |

| Market Size (2026) | USD 60.94 Billion |

| Market Size (2031) | USD 71.12 Billion |

| Growth Rate (2026 - 2031) | 3.14% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Germany Health and Medical Insurance Market Analysis by Mordor Intelligence

The Germany Health And Medical Insurance Market size in terms of premium value is expected to grow from USD 59.09 billion in 2025 to USD 60.94 billion in 2026 and is forecast to reach USD 71.12 billion by 2031 at 3.14% CAGR over 2026-2031.

Rising life expectancy, a chronic disease burden that is among Europe’s heaviest, and a regulatory commitment to universal coverage give the market a resilient baseline even as statutory insurers wrestle with deficits. Contribution-rate hikes inside the statutory system are nudging many high-income workers toward supplemental private cover, while the nationwide electronic patient record (ePA) rollout is accelerating end-to-end digitalization that trims reimbursement lags and administrative waste. Corporate group plans remain the backbone of the Germany health and medical insurance market, underwriting 72% of total contracts, and direct digital channels, though still smaller than tied-agent sales, are compounding at an 8.97% CAGR as younger adults opt for app-based onboarding. Regional dynamics add another layer: Westdeutschland commands the largest premium pool, yet Ostdeutschland posts the highest growth rate, aided by telemedicine that bridges physician shortages. Private insurers leverage this digital momentum to bundle virtual consults and disease-management modules, while statutory funds emphasize preventive programs that can flatten future cost curves.

Key Report Takeaways

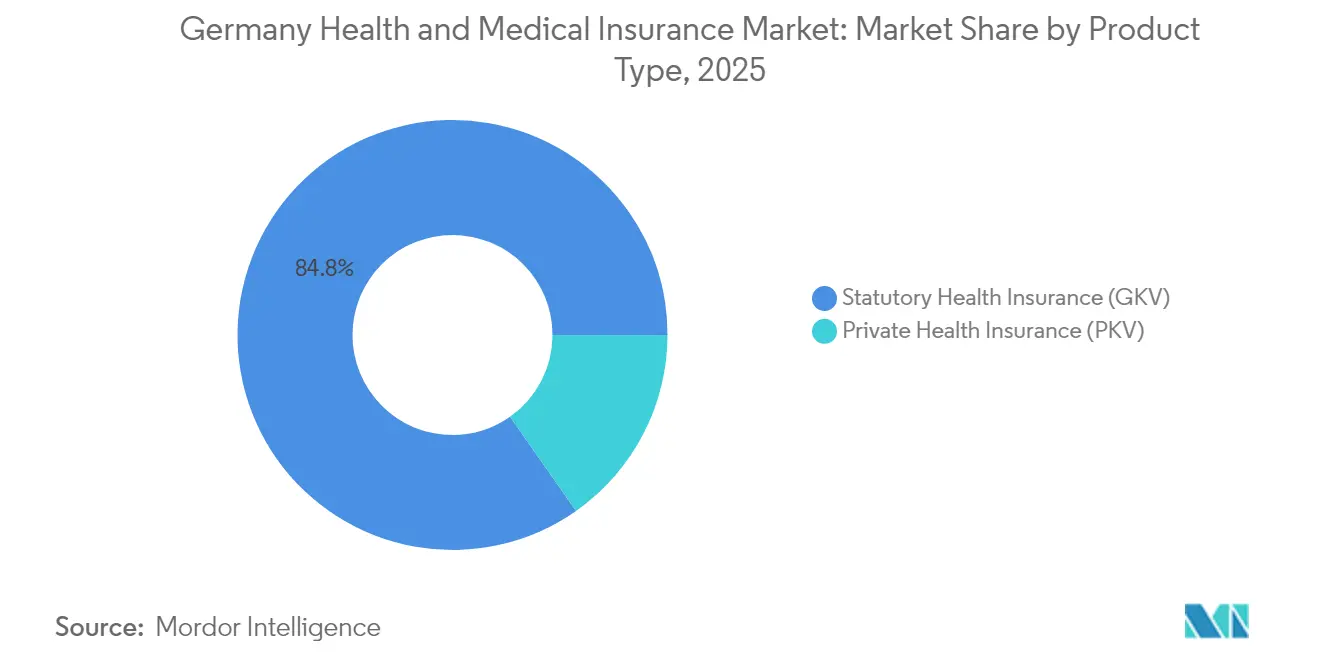

- By product type, statutory health insurance (GKV) led with 84.75% of Germany health and medical insurance market share in 2025, whereas private health insurance (PKV) is forecast to log the fastest 4.45% CAGR through 2031.

- By the terms of coverage, long-term contracts captured 89.65% of the Germany health and medical insurance market size in 2025, while short-term expat plans are projected to expand at a 6.1% CAGR by 2031.

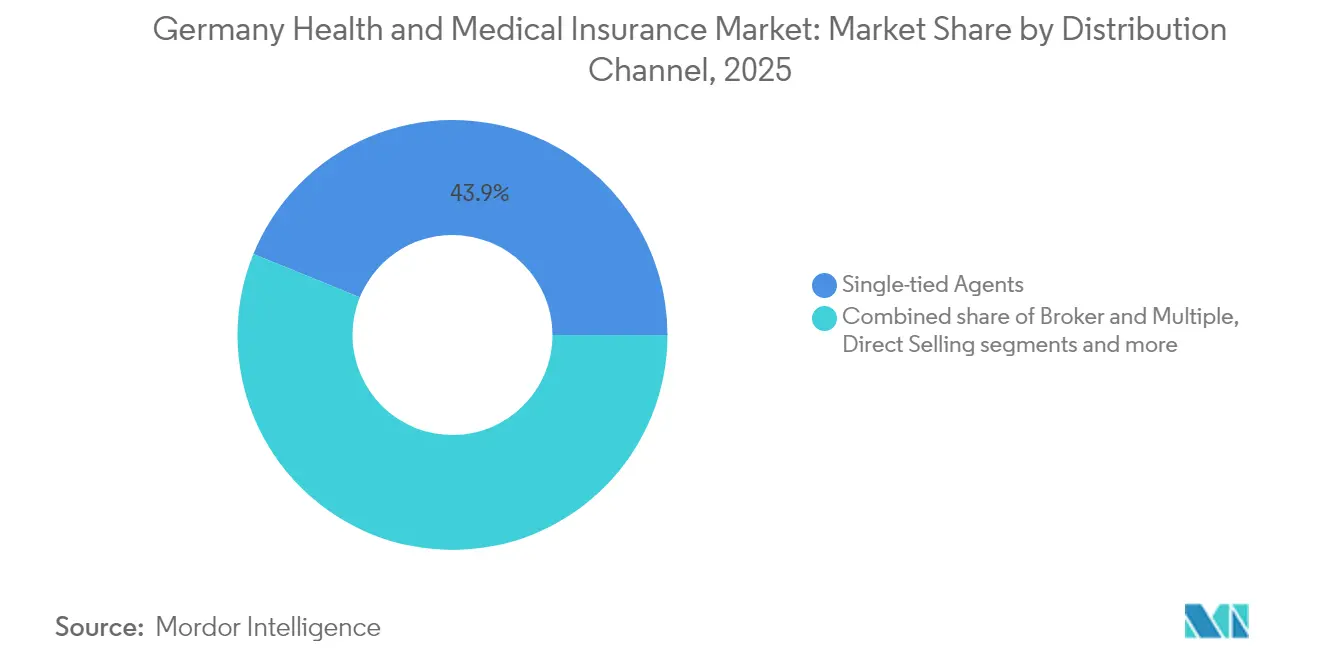

- By distribution channel, single-tied and insurance-group intermediaries held 43.85% revenue share in 2025; direct digital channels show the strongest 8.55% CAGR outlook toward 2031.

- By end-user, corporate and employer-sponsored group plans controlled 71.60% of the Germany health and medical insurance market size in 2025, whereas SME plans are set for a 4.18% CAGR through 2031.

- By region, Westdeutschland accounted for 42.95% of the premium in 2025, and Ostdeutschland is on pace for the quickest 3.62% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Germany Health and Medical Insurance Market Trends and Insights

Drivers Impact Analysis*

| Driver | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Ageing population & chronic-disease prevalence | +0.8% | National, rural concentration | Long term (≥ 4 years) |

| Escalating statutory contribution rates driving supplemental cover | +0.6% | National, high-income clusters | Medium term (2-4 years) |

| Digital-health & ePA rollout accelerating insurer innovation | +0.4% | Urban centers lead | Medium term (2-4 years) |

| Rising per-capita health-expenditure outlay | +0.5% | National with regional variance | Long term (≥ 4 years) |

| Expansion of employer-sponsored group PHI plans | +0.3% | Industrial regions | Medium term (2-4 years) |

| InsurTech MGA cost-disruption lowering admin expense | +0.2% | Digital-native demographics nationwide | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Aging Population & Chronic-Disease Prevalence

Germany’s over-65 cohort is projected to approach one-third of residents by 2050, a demographic shift that enlarges insurance risk pools and amplifies the demand for geriatric and chronic-care benefits[1]Statistisches Bundesamt, “Bevölkerungsvorausberechnung 2050,” destatis.de. Healthcare outlays already exceed USD 6,414 per person, the European Union’s peak level, and chronic illnesses such as diabetes and coronary disease dominate hospital days. Actuaries respond by refining age-band pricing, while carriers roll out prevention platforms that link wearable data to premium discounts. Digital nursing services, reimbursed under new telecare tariffs, help soften workforce shortages in eldercare facilities. Taken together, population aging remains the primary structural engine of the Germany health and medical insurance market.

Escalating Statutory Contribution Rates Driving Supplemental Cover

Statutory spending rose 6.8% in 2025 against only 3.7% revenue growth, lifting the average additional GKV contribution to 2.5%[2]GKV-Spitzenverband, “Finanzentwicklung der Krankenkassen 2025,” gkv-spitzenverband.de. High earners now face monthly deductions of USD 651.91 at a contribution ceiling of USD 71,442, prompting many to seek private dental, alternative treatment, or private ward upgrades. Carriers market modular riders that plug GKV gaps without forcing full departure from the statutory pool, an approach resonating with professionals who value continuity of coverage yet want premium amenities. This arbitrage mechanism accelerates premium inflows to the private side of the Germany health and medical insurance market.

Digital-Health & ePA Roll-Out Accelerating Insurer Innovation

The ePA initiative automatically set up electronic files for 73 million statutorily insured persons in January 2025, with full data interoperability scheduled for October[3]Gematik, “ePA-Rollout 2025 Zeitplan,” gematik.de. Techniker Krankenkasse has already enrolled 600,000 users. Insurers integrate these datasets with teleconsult platforms, enabling real-time drug interaction checks and paperless sick leave certification. Sixty-four digital therapeutics (DiGA) sit on the reimbursable list, covering conditions from chronic insomnia to irritable bowel syndrome, though only 31% of physicians prescribe them routinely. As use grows, carriers expect claim-cycle times to fall and fraud detection to improve, reinforcing the digital pivot anchoring the Germany health and medical insurance market.

Rising Per-Capita Health-Expenditure Outlay

Hospital stays, complex interventions, and high-cost specialty drugs propelled DAK-Gesundheit to raise its combined rate to 17.4% in 2025, a move designed to plug a financing gap of USD 15.12 billion. The International Monetary Fund singles out Germany’s consumption-heavy spending pattern as a cost escalator. In response, carriers embed price-comparison tools in member apps that steer patients to efficient hospitals and pharmacies. Bundled case rates for knee replacements and heart procedures are being piloted to curb runaway charges, fostering long-term margin stability across the Germany health and medical insurance market.

Restraints Impact Analysis*

| Restraint | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Structural GKV deficit & political price pressure | –0.4% | National, policy-driven | Medium term (2-4 years) |

| Premium inflation in PKV dampening new uptake | –0.3% | National, middle-income focus | Short term (≤ 2 years) |

| Prospect of “Bürgerversicherung” single-payer reform | –0.2% | National, private-segment uncertainty | Long term (≥ 4 years) |

| Intermediary talent shortage inflating acquisition cost | –0.1% | Rural regions most acute | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Structural GKV Deficit & Political Price Pressure

Germany's reserve buffers have dipped beneath the mandated threshold of USD 5.18 billion. It has ignited discussions around imposing an expenditure moratorium and seeking increased federal transfers to stabilize the system. While policymakers are hesitant to raise contributions further, fearing added strain on payroll costs and potential economic repercussions, insurers find their pricing flexibility significantly curtailed. Such constraints hinder the swift adoption of costly digital upgrades, which are essential for modernizing operations, improving efficiency, and dampening short-term profitability for insurers in Germany's health and medical sector. The ongoing structural GKV deficit and political price pressures are expected to continue influencing market dynamics in the near term.

Premium Inflation in PKV Dampening New Uptake

In 2024, average tariffs for private health insurance (PKV) surged by 7%. Concurrently, the threshold for mandatory insurance was raised to USD 79,704, limiting the number of individuals able to transition from statutory health insurance (GKV). This increase in the threshold has further narrowed the pool of eligible individuals, particularly affecting middle-income earners who may find private insurance less accessible. Many younger professionals are hesitant to commit to contracts that may see rising costs as they age, as this creates long-term financial uncertainty. In response, insurers are testing capped-increase guarantees to address these concerns, but these measures have yet to gain widespread acceptance. Consequently, this hesitance is stifling new business growth, leaving insurers to explore additional strategies to attract and retain customers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: GKV Dominance Faces Digital Disruption

Statutory health insurance maintained 84.75% control of the Germany health and medical insurance market in 2025, anchored by universal access and employer cost-sharing. The Germany health and medical insurance market size grows as GKV funds leverage scale to embed ePA services, but their deficits intensify. 82 of 93 funds raised contribution rates for 2025, signaling a pivot to non-price differentiation, such as wellness apps and rapid reimbursement.

Private carriers, post the quickest 4.45% CAGR to 2031 by targeting high-income consumers with concierge benefits and guaranteed specialist access. The consolidation strengthens that play: BaFin cleared the Gothaer-Barmenia merger valued at over USD 7.56 billion, creating the sixth-largest private insurer. The integrated entity can negotiate hospital tariffs more forcefully and spread IT costs over a larger base, reshaping competitive architectures within the Germany health and medical insurance market.

By Term of Coverage: Long-Term Preferences Drive Stability

In 2025, long-duration policies dominated the Germany health and medical insurance market, making up 89.65% of its size. This trend mirrors the country's tradition of lifetime statutory entitlements and a strong culture of stable employment. Insurers are now linking loyalty bonuses to wellness targets, providing premium rebates for gym visits, which are conveniently tracked through app QR codes. Its heightened engagement incentivizes healthier habits and also enriches underwriting data, leading to better forecasts for chronic diseases. Additionally, the integration of wellness programs into insurance offerings reflects a broader shift toward preventive healthcare, aiming to reduce long-term costs for both insurers and policyholders.

While short-term expat plans currently hold a smaller share, they are projected to grow at an annual rate of 6.1%. This surge is largely fueled by the influx of foreign students, gig workers, and employees on temporary postings. Digital brokers are streamlining services by integrating visa letters, tele-doctor consultations, and multilingual claims assistance into a single smartphone platform. These innovations enhance customer convenience and accessibility, making such plans more attractive to a diverse and mobile population. Such strategic maneuvers diversify revenue streams and provide a buffer for carriers, shielding them from demographic saturation in Germany's core health and medical insurance segments. Furthermore, the growing demand for short-term plans highlights the evolving needs of an increasingly globalized workforce, prompting insurers to adapt their offerings to remain competitive in this dynamic market.

By Distribution Channel: Digital Transformation Reshapes Access

In 2025, single-tied agents and bank assurance partners held onto a 43.85% market share, leveraging their deep-rooted community ties and expertise in statutory compliance. These traditional channels continue to play a significant role in the market, particularly in regions where personal relationships and trust remain critical factors in purchasing decisions. Meanwhile, the direct online channel surged ahead, boasting an 8.55% CAGR, as consumers increasingly gravitate towards robo-advice engines, which can swiftly compare tariffs and complete KYC processes in under two minutes. The convenience and speed offered by these digital solutions have made them particularly appealing to tech-savvy and time-conscious consumers.

In response, traditional intermediaries have begun incorporating video chat and e-signature features, slashing policy-issue times from days down to mere hours. These advancements aim to enhance customer experience and retain competitiveness in a rapidly digitizing market. Additionally, open-banking APIs streamline the process by pre-populating income data, thus reducing input errors and improving overall efficiency. However, a shortage of talent among intermediaries has resulted in lower physical brokerage penetration in rural areas, where access to skilled professionals remains limited. This gap has further accelerated digital adoption and intensified shifts in the channel mix, fundamentally altering the landscape of the Germany health and medical insurance market. As digital channels continue to gain traction, the market is expected to witness a more pronounced transformation in the coming years.

By End-User: Corporate Plans Drive Market Expansion

In 2025, employer group contracts accounted for 71.60% of premium revenue, bolstered by Germany's tradition of embedding health benefits in collective agreements through its works council. This approach ensures that health benefits remain a critical component of employee welfare. Large manufacturers are securing multi-year rate stability clauses linked to occupational safety metrics, providing predictability in costs while promoting workplace safety. Additionally, carriers are enhancing their competitive tenders by bundling services like mental health hotlines and fertility support, which cater to the evolving needs of employees and improve overall satisfaction.

Small and medium-sized enterprises (SMEs) are rapidly advancing, boasting a 4.18% CAGR projected through 2031. This growth is largely attributed to digital brokers who are streamlining processes by auto-uploading employee rosters directly from payroll software, significantly reducing administrative burdens. Furthermore, the increasing adoption of telerehabilitation services, now reimbursable, is adding substantial value for firms aiming to lower absenteeism and improve employee productivity. These developments are driving the adoption of health and medical insurance among SMEs. This expanding presence solidifies a robust premium pipeline for Germany health and medical insurance market, ensuring sustained growth and innovation in the forecast period.

Geography Analysis

Westdeutschland maintains national leadership thanks to high-value corporate clusters that finance comprehensive group benefits and well-equipped hospitals that accept smart-card check-in and e-prescriptions. ePA login rates surpass 40% in Hamburg, enabling predictive analytics that flag high-risk populations for proactive outreach. Premium yield per enrollee runs above the national average, reinforcing revenue dominance. These mature financial and protection ecosystems are also strongly aligned with the broader Germany life and non-life insurance market, where strong corporate penetration, bancassurance channels, and digital distribution models continue to support stable premium inflows across both life and non-life segments.

In Ostdeutschland, structural funds renovate district hospitals and install e-ICU beds, closing historical care gaps. Growing tech ecosystems in Dresden and Leipzig draw young professionals who gravitate to app-only private cover. Standardized statutory rates raise contributions, yet improved service access justifies higher deductions in many households.

Norddeutschland adapts group plans for international crews in shipyards and offshore wind farms, including evacuation clauses and 24/7 helplines in multiple languages. In Süddeutschland, automotive and precision-engineering exporters embed musculoskeletal wellness programs in insurance contracts to combat assembly-line injuries. Together, these regional narratives underscore how localized product tailoring supports cohesive expansion in the Germany health and medical insurance market.

Competitive Landscape

In the Germany health and medical insurance market, competition remains moderate. The top five players - Techniker Krankenkasse, Barmer, DAK-Gesundheit, AOK Bayern, and AOK Baden-Württemberg - collectively command nearly half of the premium market. Meanwhile, consolidation in the private health insurance (PKV) sector is gaining traction. A notable merger between Gothaer and Barmenia has already crossed the USD 7.56 billion revenue mark, with expectations of cost efficiencies from their unified core-policy platforms.

Digital capabilities have emerged as a defining competitive edge. Allianz Partners’ Lumi ecosystem, catering to over 1 million users, has achieved a remarkable 70% reduction in in-person doctor visits. It slashes claim costs and also saves members significant travel time. In response, statutory funds are leveraging AI for preventive measures. For instance, Techniker Krankenkasse’s alert system for diabetes foot care has successfully reduced amputations in its pilot groups.

Regulatory changes are presenting a dual-edged sword: they both constrain and stimulate innovation. The Gesundheitsversorgungsstärkungsgesetz, for instance, lifts budget caps on general practitioners (GPs). It mandates insurers to cover more consultations, but it also provides valuable data to refine chronic-care pathways. Insurers are adept at swiftly utilizing ePA records for personalized outreach not only to bolster customer loyalty but also to achieve lower hospital readmission rates, thereby enhancing their performance in the competitive landscape of the Germany health and medical insurance market.

Germany Health and Medical Insurance Industry Leaders

Techniker Krankenkasse (TK)

AOK – Die Gesundheitskasse

Barmer

DAK-Gesundheit

Debeka

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Allianz, BlackRock, and T&D Holdings agreed to acquire Viridium Group for USD 3.78 billion, adding 3.4 million life and health policies.

- March 2025: BaFin cleared the Gothaer-Barmenia merger, forming Germany’s sixth-largest PKV carrier with a USD 7.56 billion turnover.

- February 2025: BARMER, TK, and KNAPPSCHAFT launched digital sign-ups for under-34 skin cancer screening.

- January 2025: Allianz Partners struck a deal with Aetna International to migrate global health contracts and launch an SME-centric Summit plan.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the German health and medical insurance market as the yearly gross premium revenue booked inside Germany by statutory health insurance funds (Gesetzliche Krankenversicherung) and private medical insurers covering hospitalization, outpatient care, and prescribed drugs for residents, cross-border commuters, and expatriates. According to Mordor Intelligence, all group and individual contracts are valued at face premium and converted to constant 2024 US dollars.

Scope exclusion: Supplementary travel, accident-only, dental-only, and long-term care riders lie outside this scope.

Segmentation Overview

- By Product Type (Value)

- Statutory Health Insurance (GKV)

- Private Health Insurance (PKV)

- By Term of Coverage (Value)

- Short-term

- Long-term

- By Distribution Channel (Value)

- Single-tied / Insurance-group Intermediaries

- Broker & Multiple Agents

- Credit Institutions

- Direct Selling

- Other Channels

- By End-User/Customer Type

- Corporate/Employer (Group Plans)

- Individual/Families

- SME's (Small & Medium-sized Enterprises)

- Others

- By Region

- Norddeutschland

- Ostdeutschland

- Westdeutschland

- Süddeutschland

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts spoke with actuaries at sickness funds, brokers serving SMEs, hospital billing managers, and digital-health founders across all four macro-regions. These interviews confirmed penetration assumptions, channel migration, and average premium moves.

Desk Research

We gathered enrollment, contribution, and claims ratios from Destatis, the Federal Ministry of Health, and the Bundesversicherungsamt, then tied them to Eurostat and OECD series on income and aging. Quarterly ledgers from GKV-Spitzenverband and PKV-Verband sharpened the public-private split. A second pass used company filings, Bundesbank statistics, and leading national press to map tariff shifts. D&B Hoovers and Dow Jones Factiva, two paid databases we access, supplied insurer financials. The sources named illustrate our mix and are not exhaustive.

Market-Sizing & Forecasting

We start with a top-down premium pool reported by regulators, which is then reconciled with selective bottom-up checks (sampled average premium × covered lives) to fine-tune totals. Variables such as contribution ceilings, real GDP, unemployment, digital enrollment share, and chronic-disease prevalence feed a multivariate regression that projects growth through 2030. Three-year moving averages bridge any data gaps.

Data Validation & Update Cycle

Model outputs face variance tests against loss ratios and solvency margins before senior review. Reports refresh annually, with interim updates triggered by major tariff or policy shifts, and a final pass is completed before delivery.

Why Mordor's Germany Health and Medical Insurance Baseline Earns Trust

Published estimates often differ because firms adopt dissimilar premium concepts, exchange-rate locks, and refresh cadences. Our disciplined definition and yearly rebasing reduce these distortions. Key gap drivers include some publishers bundling nursing-care premiums, others applying aggressive inflation escalators, or projecting off pandemic anomalies.

Our disciplined definition and yearly rebasing reduce these distortions. Key gap drivers include some publishers bundling nursing-care premiums, others applying aggressive inflation escalators, or projecting off pandemic anomalies.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 59.09 B (2025) | Mordor Intelligence | - |

| USD 409.10 B (2025) | Global Consultancy A | Bundles nursing-care premiums; keeps nominal euros |

| USD 54.04 B (2024) | Research Boutique B | Older base year; expatriates excluded |

| USD 68.73 B (2025) | Publisher C | Adds travel and accident riders; fixed euro-USD rate |

These comparisons show that clients can trace every Mordor figure back to verifiable ledgers and transparent steps, giving boardrooms a dependable baseline for planning.

Key Questions Answered in the Report

What is the current value of the Germany health and medical insurance market and how fast will it grow?

The market stands at USD 60.94 billion in 2026 and is forecast to reach USD 71.12 billion by 2031, implying a 3.14% CAGR.

Why does statutory health insurance still dominate despite rising contribution rates?

GKV retains 84.75% of the market share because it guarantees universal access and employer cost-sharing, although higher earners increasingly add private supplemental cover to fill benefit gaps.

How will the electronic patient record (ePA) affect insurers and policyholders?

EPA provides real-time data that shortens claims cycles, improves care coordination, and supports telemedicine services, ultimately lowering administrative costs and enhancing the patient experience.

Which distribution channel is expanding fastest and why?

Direct digital channels are compounding at an 8.55% CAGR because app-based onboarding, robo-advice, and e-signatures appeal to younger, tech-savvy consumers.

What regional market shows the highest growth, and what drives it?

Ostdeutschland is growing fastest at a 3.62% CAGR, driven by telehealth that mitigates physician shortages, infrastructure upgrades, and standardized contribution rates.

How significant are employer-sponsored plans in the Germany health and medical insurance industry?

Corporate group contracts account for 71.60% of policies, reflecting Germany’s tradition of embedding health benefits in collective labor agreements and the competitive need to attract skilled talent.

Page last updated on: