Market Overview

| Study Period | 2019 - 2030 |

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

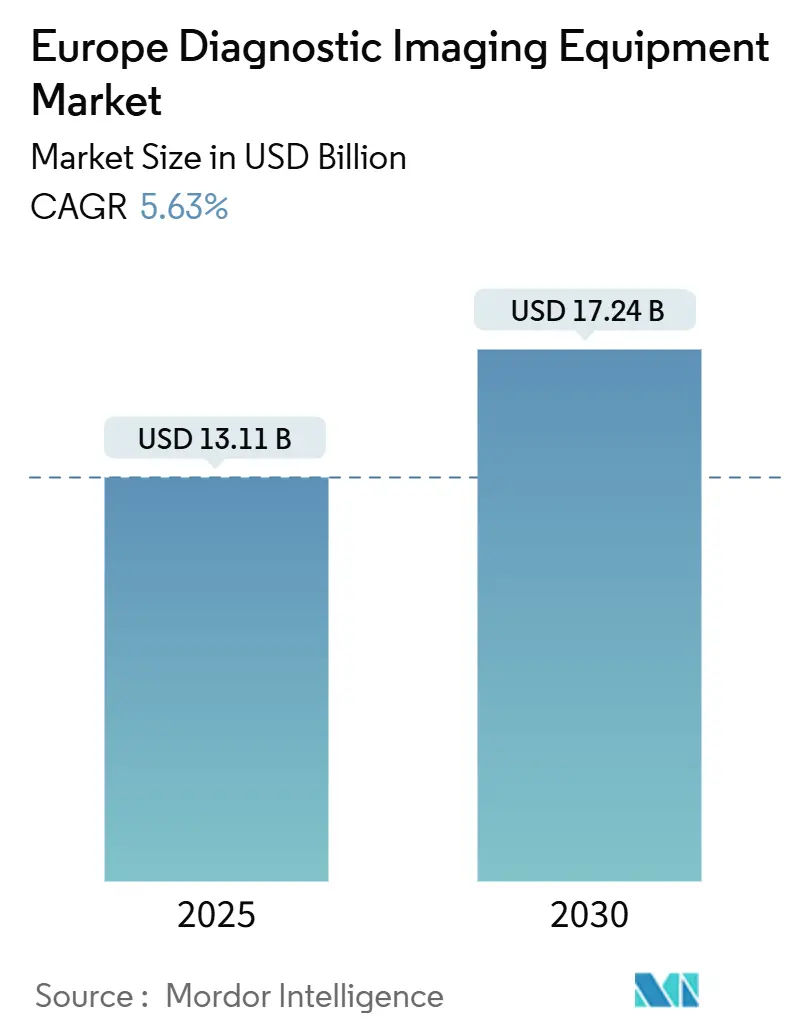

| Market Size (2025) | USD 13.11 Billion |

| Market Size (2030) | USD 17.24 Billion |

| Growth Rate (2025 - 2030) | 5.63% CAGR |

| Market Concentration | High |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Europe Diagnostic Imaging Equipment Market Analysis by Mordor Intelligence

The Europe diagnostic imaging equipment Market size is estimated at USD 13.11 billion in 2025, and is expected to reach USD 17.24 billion by 2030, at a CAGR of 5.63% during the forecast period (2025-2030). Accelerated equipment renewal cycles, a rapidly greying population, and hospital digitization mandates underpin the growth curve. Photon-counting CT, helium-free MRI, and AI-enabled workflow software improve image quality, slash scan times, and offset workforce shortages, creating strong replacement demand. Governments funnel fresh capital into modern imaging suites through schemes such as Germany’s Hospital Future Act and France’s Health Innovation Plan, widening the revenue base for vendors. Meanwhile, private equity groups consolidate outpatient radiology chains, boosting purchasing power for large fleet upgrades. Intensifying competition among Siemens Healthineers, Philips, and GE HealthCare drives aggressive product launches that emphasize sustainability, automation, and total-cost-of-ownership reduction

Key Report Takeaways

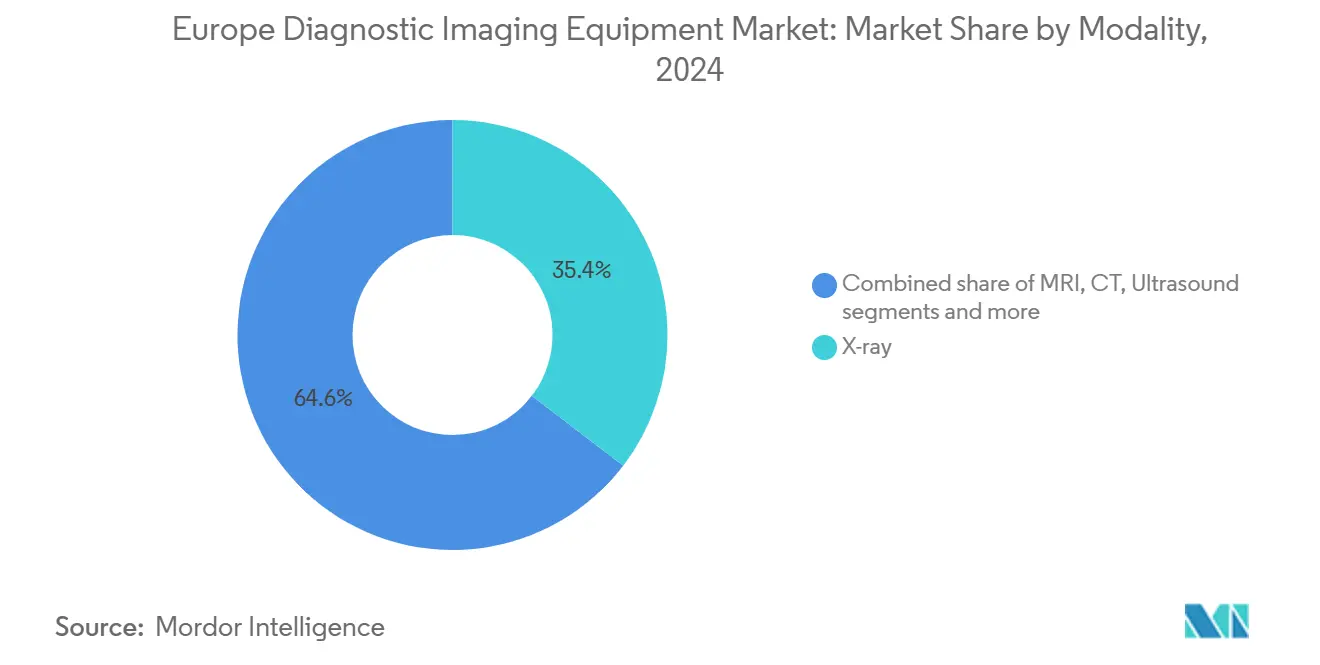

- By modality, X-ray systems led with 35.41% revenue share in 2024; MRI is projected to expand at a 7.46% CAGR to 2030.

- By portability, fixed systems held 79.21% of the Europe diagnostic imaging equipment market share in 2024, while mobile and handheld systems recorded the highest projected CAGR at 7.12% through 2030.

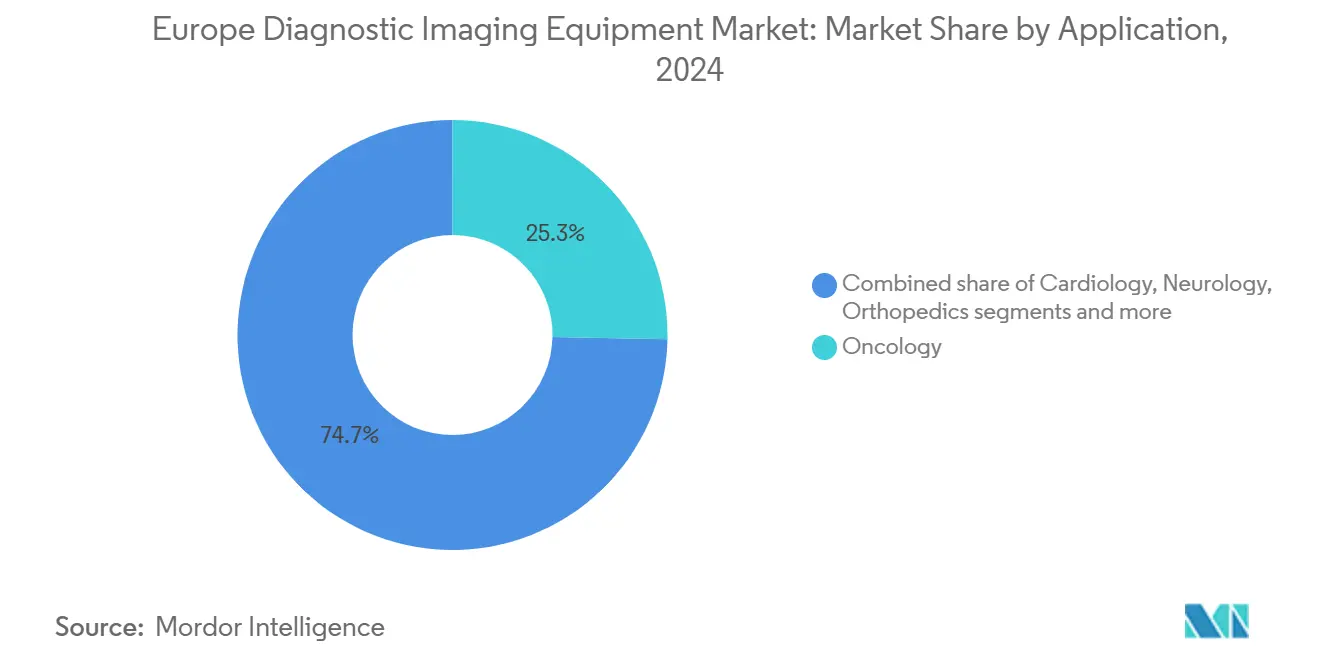

- By application, oncology accounted for a 25.31% share of the Europe diagnostic imaging equipment market size in 2024 and cardiology is advancing at a 6.82% CAGR through 2030.

- By end user, hospitals captured 71.18% of revenue in 2024; diagnostic imaging centers post the quickest growth at a 7.95% CAGR to 2030.

- By country, Germany held a market share of 26.69% in 2024 and France acquired the fastest growth in the Europe diagnostic imaging industry with a CAGR of 5.86% from 2025 to 2030.

Europe Diagnostic Imaging Equipment Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Aging population and chronic disease burden | +1.8% | Germany, Italy, Eastern Europe | Long term (≥ 4 years) |

| Continuous imaging technology innovation | +1.2% | Core EU markets | Medium term (2-4 years) |

| Hospital modernization and digital investment | +0.9% | Germany, France, Netherlands | Medium term (2-4 years) |

| Uptake of minimally invasive image-guided procedures | +0.7% | Western Europe | Short term (≤ 2 years) |

| Expansion of outpatient and mobile imaging service models for greater access | +0.5% | UK, Netherlands, Scandinavia | Short term (≤ 2 years) |

| Government initiatives promoting early diagnosis and digital health integration | +0.4% | France, Germany, Netherlands | Long term (≥ 4 years) |

Source: Mordor Intelligence

Prevalence of chronic diseases and an aging European population

Europe’s over-65 cohort is on track to jump from 21% in 2023 to 29% by 2050, translating into millions more oncology, cardiology, and musculoskeletal scans each year.[1]Source: OECD, “Health at a Glance Europe 2024,” OECD Publishing, oecd.org Cancer incidence already exceeds 4.47 million new cases annually, with Northern and Western countries detecting disease earlier thanks to organized screening. Hospitals respond by prioritizing multipurpose scanners that handle high daily volumes yet deliver sub-millimetric resolution. Vendors cater to this surge with wider bore MRI and low-dose CT lines that preserve image quality for frail patients. Chronic disease management programs also drive sustained outpatient imaging referrals, re-orienting procurement toward scalable, cloud-connected systems that streamline image sharing among referring physicians.

Continuous technology innovation in imaging

Photon-counting CT provides up to four-fold higher spatial resolution and significantly lower radiation dose than conventional detectors, winning early adopters at sites such as San Raffaele Hospital in Italy. AI-aided reconstruction on Siemens Healthineers’ Helium-free MRI platform cuts exam times by 30%, enabling more scans per day and easing scheduling backlogs. France earmarked EUR 1.5 billion for healthcare AI, and early pilots show a 28% improvement in tumor detection with AI-assisted mammography. These breakthroughs spark modality replacement even in budget-tight environments because operational savings offset frontline price premiums. Vendors complement hardware with subscription-based AI suites that automate repetitive tasks and support remote reading.

Rising healthcare infrastructure investment and hospital modernization programs

Germany’s Hospital Future Act injects more than EUR 4 billion into digital upgrades across 1,624 hospitals, with imaging IT and scanner fleets ranking among the top spending categories. Value partnerships, such as the 12-year EUR 55 million agreement between Siemens Healthineers and University Hospital Nantes, bundle multiple CT, MRI, and ultrasound units with service and staff-training commitments. Capital programs aim to shrink wait lists and elevate diagnostic standards, prompting large multiyear tenders that reward suppliers able to integrate imaging chains into hospital enterprise platforms. Modernization also positions facilities to qualify for future outcome-based reimbursement models that depend on accurate, timely diagnostics.

Growing adoption of minimally invasive, image-guided procedures across specialties

Surgeons and interventional radiologists increasingly rely on live imaging to navigate catheters, ablation probes, and robotic tools, reducing patient trauma and length of stay. Evidence from lumbar spine interventions shows minimally invasive image-guided treatments lower operating room time and post-operative complications compared with open surgery. Nuclear medicine leverages diagnostic scans to personalize therapies, typified by the French reimbursement green light for 177Lu-PSMA prostate cancer treatment that pairs PET imaging with targeted radiopharmaceuticals. The procedural shift accelerates demand for hybrid operating suites equipped with high-resolution fluoroscopy, cone-beam CT, and ultrasound systems capable of real-time fusion imaging.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capital and total-cost-of-ownership for advanced imaging equipment | -1.1% | Small hospitals, emerging EU | Medium term (2-4 years) |

| Persistent shortage of radiologists and imaging technologists | -0.8% | UK, Germany, France | Long term (≥ 4 years) |

| Stringent EU regulatory landscape prolonging approvals | -0.6% | EU-wide | Medium term (2-4 years) |

| Uncertainty in reimbursement policies within public healthcare systems | -0.4% | Germany, France, Italy, Spain | Long term (≥ 4 years) |

Source: Mordor Intelligence

High capital and total-cost-of-ownership for advanced imaging equipment

Photon-counting CT and 3 T MRI units can top USD 1 million apiece, while annual service contracts often equal 10% of purchase price. EU MDR compliance adds incremental pre-market expenditure exceeding USD 50,000 for Class III devices and can lengthen time-to-market, delaying revenue realization for manufacturers and limiting early access for providers.[2]Source: EuroDev, “The Cost of Obtaining EU MDR Certification,” eurodev.com Smaller clinics struggle to justify such outlays under fixed reimbursement, potentially widening geographic gaps in care.

Persistent shortage of radiologists and imaging technologists

United Kingdom surveys show 75% of imaging departments operating with unfilled consultant posts, forcing reliance on locum staff and teleradiology outsourcing. Across Europe, technologist vacancy rates climbed to 18.1% in 2024 from 6.2% three years earlier, inflating labor costs and elongating patient queues. AI triage tools and remote reading networks help mitigate pressure yet cannot fully replace experienced personnel for complex procedures.

Segment Analysis

By Modality: MRI momentum reshapes diagnostic priorities

X-ray retained the largest slice of the Europe diagnostic imaging equipment market at 35.41% in 2024, anchored by ubiquitous use in trauma and primary care. That dominance is stable through mid-term forecasts, but MRI’s 7.46% CAGR represents the fastest lane, supported by helium-free magnet technology that removes bulk cryogen logistics and trims lifecycle emissions. Photon-counting CT shipments also accelerate thanks to oncology staging protocols demanding finer lesion characterization. Ultrasound remains indispensable in cardiac, obstetric, and point-of-care settings; 80% of Belgian emergency departments already use portable scanners for bedside triage. Nuclear imaging slots into theranostic regimens, while digital mammography enjoys AI decision support that lifts cancer detection sensitivity.

MRI’s share growth reshapes vendor R&D budgets toward advanced coils, motion correction, and compressed sensing. X-ray manufacturers counter by integrating AI fracture detection and dual-energy functionality. CT suppliers bundle dose-tracking dashboards to satisfy tightening radiation governance. Segment players that deliver comprehensive modality ecosystems—hardware, software, and service—capture recurring revenue themes and deepen account stickiness within the Europe diagnostic imaging equipment market.

Note: Segment shares of all individual segments available upon report purchase

By Portability: mobility bridges access gaps

Fixed systems still represent 79.21% of installed base and remain indispensable for high-throughput oncology and trauma centers. These suites house ceiling-suspended detectors, 64-slice CT, and 3 T MRI that anchor multidisciplinary hubs. Yet shifting care models favor agile solutions, propelling mobile and handheld systems at 7.12% CAGR. The Europe diagnostic imaging equipment market size for portable ultrasound is projected to climb above USD 1.2 billion by 2030 as general practitioners and paramedics adopt pocket devices that expedite triage in ambulances and rural clinics. Chipiron’s USD 17 million funding to engineer compact MRI underlines investor belief in mobility’s disruptive potential.

Mobile CT and C-arms also align with surgical suite expansion and trauma resuscitation bays that demand rapid imaging without patient transfer. Vendors refine battery life, wireless data transfer, and antimicrobial casings to support infection-control protocols. Meanwhile, leasing firms offer pay-per-scan models that remove upfront capital hurdles, especially for small hospitals, and fuel broader diffusion across the Europe diagnostic imaging equipment market.

By Application: cardiology presses oncology’s leadership

Oncology retained a 25.31% revenue share in 2024 as cancer screening programs and precision radiotherapy planning rely on multi-modality assessments. However, cardiology posts the quickest climb at 6.82% CAGR through improved CT-based coronary evaluation and stress MRI protocols. The Europe diagnostic imaging equipment market share for cardiac imaging is set to expand as 45-minute comprehensive scans replace multiple standalone tests, heightening throughput efficiency. Neurology benefits from AI-assisted stroke triage projects like the EUR 26.9 million UMBRELLA consortium that supplies real-time decision support. Orthopedics exploits cone-beam CT and metal artifact reduction software to refine implant planning.

Cross-specialty demand diversifies product roadmaps. Oncology-focused advances in spectral CT spill into cardiology plaque analysis, while high-frame-rate ultrasound designed for electrophysiology also serves pediatric clinics. Vendors that leverage modular platforms to address overlapping clinical protocols gain cost advantages and shorten development cycles within the Europe diagnostic imaging equipment market.

Note: Segment shares of all individual segments available upon report purchase

By End User: Independent imaging centers scale up

Hospitals commanded 71.18% of spending in 2024 owing to broad case mixes and emergency care, yet diagnostic imaging centers post a 7.95% CAGR as they provide faster appointments and transparent pricing. Private capital owns up to 20% of French outpatient imaging practices, injecting funds for scanner upgrades and expansion into neighboring countries. The Europe diagnostic imaging equipment market size allocated to these centers is forecast to substantially grow by 2030 because value-based insurers steer non-acute exams away from costlier hospital settings. Evidia’s merger creates a 100-plus site network that negotiates volume discounts on multi-year equipment contracts.

Academic institutions and contract research organizations also ramp imaging budgets to support clinical trials for personalized therapies, while mobile fleets provide overflow capacity during refurbishment projects. End-user diversity pushes vendors to craft flexible financing, uptime guarantees, and AI-driven fleet management dashboards to attract long-term service revenue from the Europe diagnostic imaging equipment market.

Geography Analysis

Germany dominated the market by acquiring a market share of 28.69% in 2024; it further dominates procurement thanks to industrial depth and clinical research density. France is projected to grow at the fastest CAGR rate of 5.86% from 2025 to 2030. France follows with its EUR 7.5 billion Health Innovation Plan that earmarks EUR 2.4 billion for digital applications, including AI-ready imaging archives. Partnerships such as Philips-Evidia installations in Uppsala position Nordic private clinics at the forefront of sustainable MRI fleet renewal.

The UK struggles with radiologist deficits that stretch reading times, prompting aggressive teleradiology outsourcing and AI prioritization in the national imaging strategy. Spain and Italy deploy mobile multi-screening buses to reach rural populations and cut carbon footprints by 97%. The Netherlands and Denmark enjoy near-universal enterprise PACS adoption and lead in cloud image exchange, providing fertile ground for AI start-ups that integrate with national health identifiers. Central and Eastern European states lag in scanner density but post double-digit growth as EU structural funds subsidize equipment upgrades.

Cross-border data regulations spur interest in federated AI that trains algorithms locally without sharing patient images, supporting compliant innovation adoption across the Europe diagnostic imaging equipment market. Vendors that tailor financing models and service networks to local reimbursement schemes better capture demand diversity.

Competitive Landscape

Siemens Healthineers, Philips, and GE HealthCare collectively are key players within the Europe diagnostic imaging equipment market, which points to moderate concentration. Siemens registered 7.6% imaging revenue growth in Q1 2025, propelled by photon-counting CT rollouts and helium-free Magnetom Flow MRI that slashes helium use by 99%.[3]Source: Siemens Healthineers, “Siemens Healthineers Reports Strong Q1 2025 Results,” siemens-healthineers.com

Second-tier firms such as Canon, Fujifilm, and Esaote push niche ultrasound and fluoroscopy innovations, often bundling AI modules and remote service portals. United Imaging clinches public tenders with cost-competitive high-end CT and MRI, challenging incumbents in price-sensitive procurements. Private equity-backed imaging chains negotiate enterprise-wide purchase agreements, prompting manufacturers to develop fleet-wide total-cost-of-ownership dashboards and uptime guarantees.

Sustainability credentials emerge as a differentiator because hospitals factor energy use and helium conservation into tender scoring. Vendors diversify revenue into managed services where fixed periodic payments cover equipment, software, and workforce training, aligning with hospital OPEX preferences and locking in decade-long relationships within the Europe diagnostic imaging equipment market.

Europe Diagnostic Imaging Equipment Industry Leaders

-

FUJIFILM Holdings Corporation

-

Siemens Healthineers AG

-

GE HealthCare

-

Koninklijke Philips N.V.

-

Canon Medical Systems Corporation

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- February 2025: Philips partnered with Evidia to install Ambition BlueSeal MRI and CT 5300 Premium at Aleris Elisabeth Hospital, the first private Swedish clinic to deploy the platform Philips.

- November 2024: Bracco invested USD 86 million in a new Swiss facility to triple production of ultrasound contrast agents Radiology Business.

- August 2024: CVC DIF agreed to acquire mobile imaging firm medneo UK, reflecting sustained investor interest in flexible service models Medical Device Network.

- July 2024: Duke Street acquired Agito Medical from Philips, expanding rental fleets across 10 countries Radiology Business.

Europe Diagnostic Imaging Equipment Market Report Scope

As per the scope of the report, the diagnostic imaging equipment market covers a wide array of medical devices used for diagnostic purposes. It has a vast range of applications in the oncological, orthopedic, gastro, and gynecological fields.

| By Modality | MRI | < 1.5 T | |

| 1.5–3 T | |||

| > 3 T | |||

| CT | ≤ 16-slice | ||

| 64-slice | |||

| ≥ 128-slice & photon-counting | |||

| Ultrasound | 2-D | ||

| 3-D/4-D | |||

| Hand-held & POCUS | |||

| X-ray | Analog | ||

| Digital (DDR/DR) | |||

| Nuclear Imaging | PET | ||

| SPECT | |||

| Fluoroscopy and C-arms | |||

| Mammography | |||

| By Portability | Fixed Systems | ||

| Mobile and Hand-held Systems | |||

| By Application | Cardiology | ||

| Oncology | |||

| Neurology | |||

| Orthopedics | |||

| Gastroenterology | |||

| Women’s Health & OB-GYN | |||

| Other Applications | |||

| By End User | Hospitals | ||

| Diagnostic Imaging Centers | |||

| Other End Users | |||

| By Country | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

By Modality

| MRI | < 1.5 T |

| 1.5–3 T | |

| > 3 T | |

| CT | ≤ 16-slice |

| 64-slice | |

| ≥ 128-slice & photon-counting | |

| Ultrasound | 2-D |

| 3-D/4-D | |

| Hand-held & POCUS | |

| X-ray | Analog |

| Digital (DDR/DR) | |

| Nuclear Imaging | PET |

| SPECT | |

| Fluoroscopy and C-arms | |

| Mammography |

By Portability

| Fixed Systems |

| Mobile and Hand-held Systems |

By Application

| Cardiology |

| Oncology |

| Neurology |

| Orthopedics |

| Gastroenterology |

| Women’s Health & OB-GYN |

| Other Applications |

By End User

| Hospitals |

| Diagnostic Imaging Centers |

| Other End Users |

By Country

| Germany |

| United Kingdom |

| France |

| Italy |

| Spain |

| Rest of Europe |

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

Which diagnostic imaging technologies are European hospitals prioritizing for replacement cycles?

Hospitals are chiefly replacing legacy CT and MRI scanners with photon-counting CT and helium-free MRI platforms because these systems cut radiation dose, lower helium use, and integrate seamlessly with AI software for faster reads.

How are sustainability goals influencing imaging equipment tenders in Europe?

Green procurement criteria now award points for low-energy gantries, circular-economy refurbishment programs, and scanners that eliminate consumables such as liquid helium, giving eco-designed systems a clear competitive edge.

What role does AI play in easing Europe’s radiologist shortage?

AI tools are increasingly used for triage, automated measurements, and quality checks, enabling overburdened radiology teams to focus on complex cases while keeping report turnaround times within clinical guidelines.

Why are private equity firms investing heavily in European imaging centers?

Outpatient imaging chains deliver predictable cash flow, benefit from technology upgrades that boost scan throughput, and are well-positioned to capture referrals as payers steer non-urgent exams away from high-cost hospital sites.

How is the shift toward minimally invasive procedures shaping equipment specifications?

Interventionalists demand hybrid rooms with real-time 3D imaging, low-dose fluoroscopy, and fusion software, prompting vendors to bundle high-resolution C-arms with navigation and robotics interfaces.

What barriers still limit advanced imaging adoption in smaller European facilities?

High total-cost-of-ownership, complex EU MDR compliance processes, and limited access to trained technologists continue to delay procurement of cutting-edge modalities in many rural and community hospitals.