Thailand OOH And DOOH Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

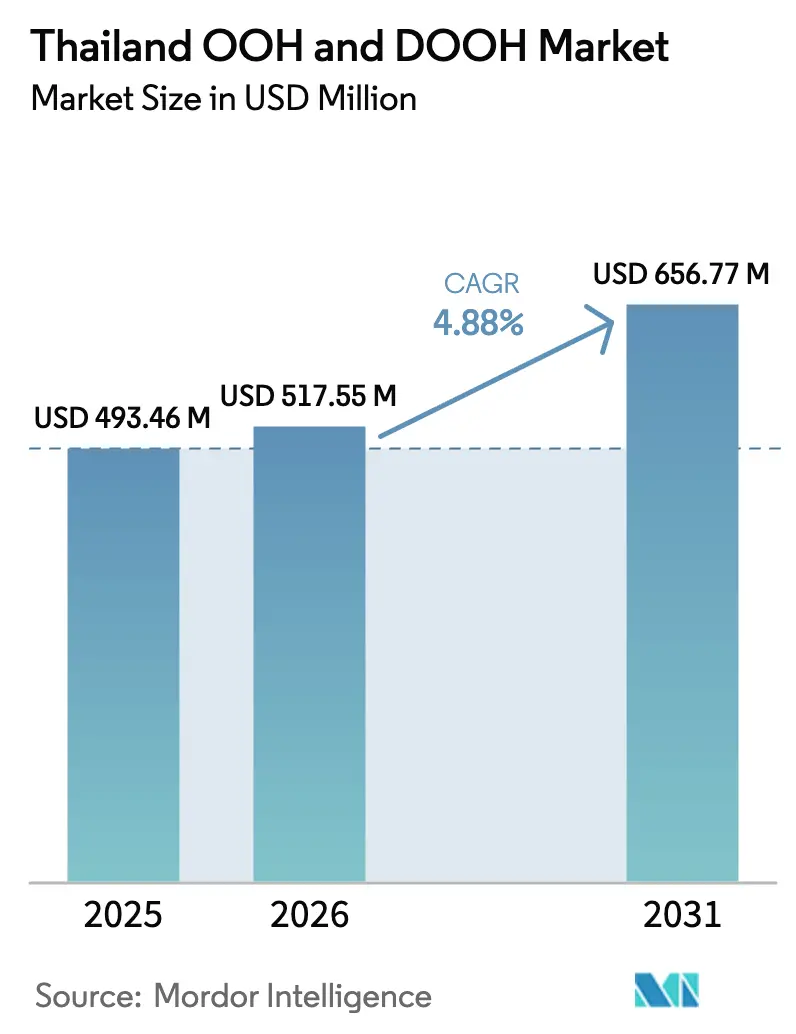

| Base Year Market Size (2025) | USD 493.46 Million |

| Market Size (2026) | USD 517.55 Million |

| Market Size (2031) | USD 656.77 Million |

| Growth Rate (2026 - 2031) | 4.88% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Thailand OOH And DOOH Market Analysis by Mordor Intelligence

The Thailand out-of-home advertising market size in 2026 is estimated at USD 517.55 million, growing from 2025 value of USD 493.46 million with 2031 projections showing USD 656.77 million, growing at 4.88% CAGR over 2026-2031. Constant passenger growth at upgraded airports, smart-city funding that accelerates digital conversions, and record tourism inflows are keeping demand resilient even as media budgets tighten elsewhere. Programmatic digital OOH, expanding 12% each year, is redefining price benchmarks in premium transit zones, while mixed-use real-estate projects in secondary provinces bring street-furniture formats to audiences once reachable only in Bangkok. Brands are also allocating more spend to place-based screens inside shopping centers to leverage longer dwell times and newly available data integrations. At the same time, fragmented media ownership, limited third-party auditing, and content-approval delays continue to limit the pace at which national campaigns scale and optimize. Yet the overall competitive intensity is encouraging technology partnerships that improve buying efficiency, suggesting further upside for the Thailand out-of-home advertising market during the outlook period.

Key Report Takeaways

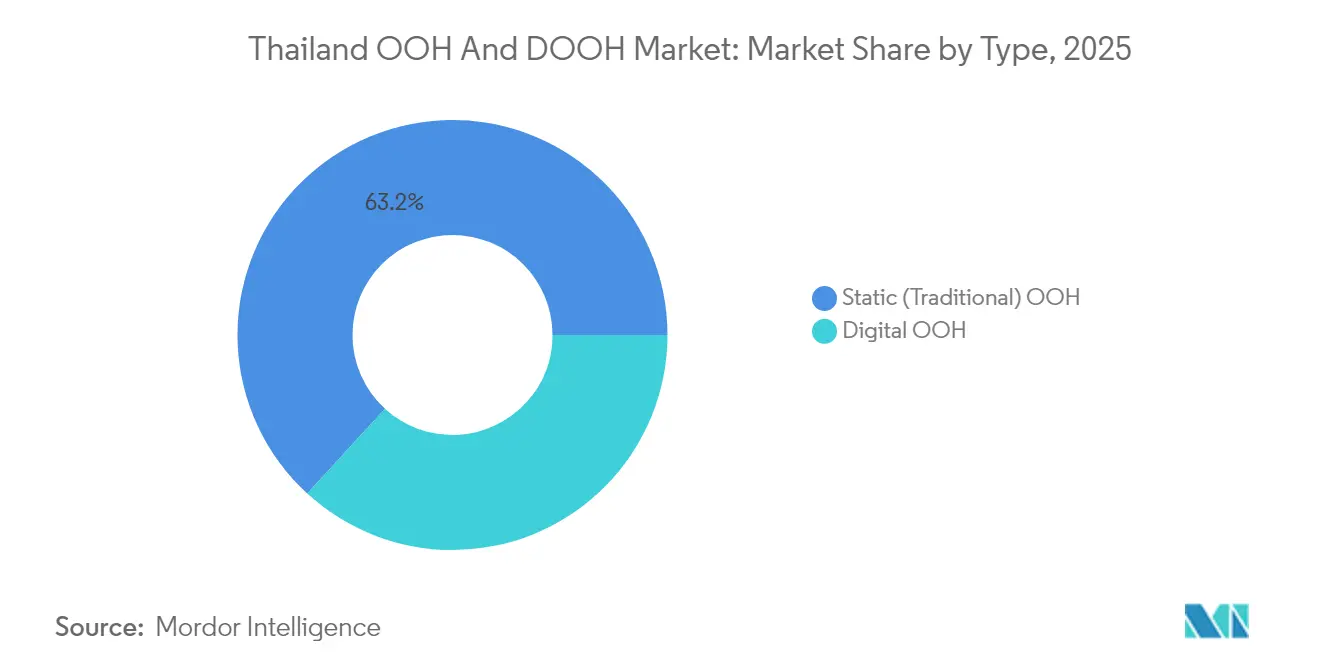

- By type, static OOH led with 63.20% of Thailand out-of-home advertising market share in 2025, whereas programmatic OOH is projected to grow at a 11.2% CAGR through 2031.

- By format, billboards commanded 41.10% revenue share in 2025; place-based media is forecast to expand at an 8.28% CAGR between 2026-2031.

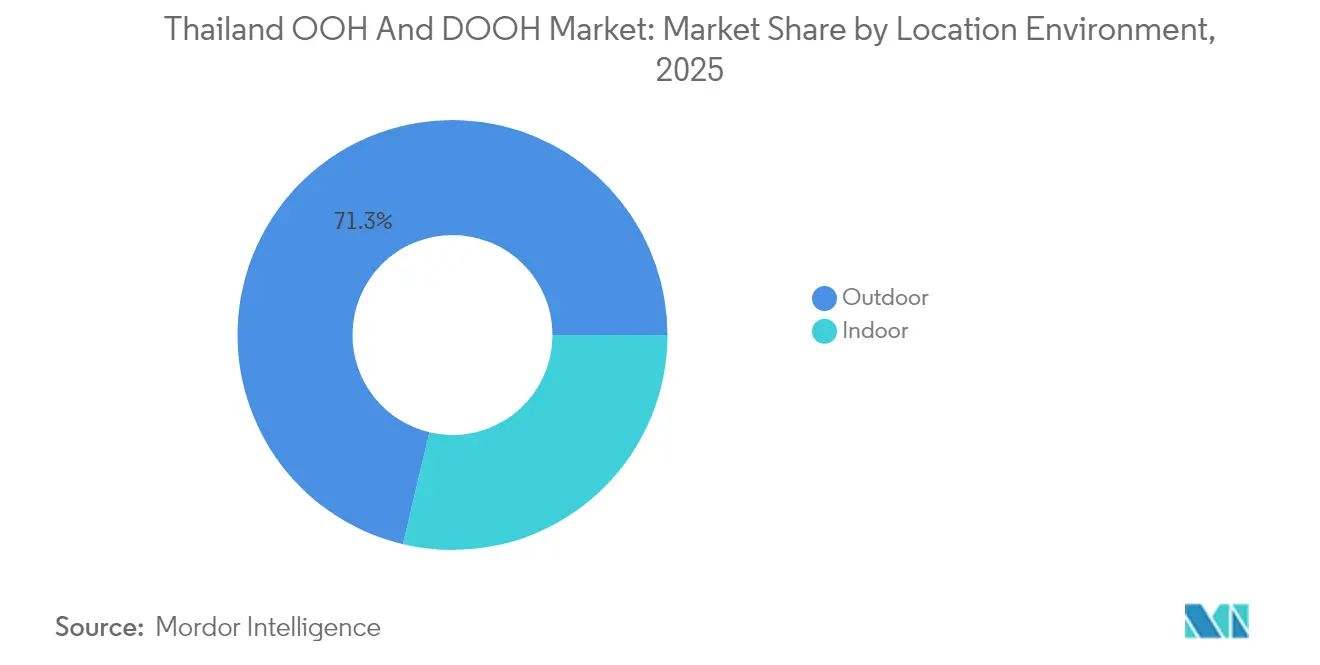

- By location environment, outdoor formats accounted for a 71.30% share of the Thailand out-of-home advertising market size in 2025, while indoor formats are advancing at a 6.52% CAGR to 2031.

- By end-user vertical, retail & FMCG held 26.60% of market revenue in 2025; healthcare & pharma is the fastest growing vertical at a 7.55% CAGR over the same period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Thailand OOH And DOOH Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance Impact | Timeline |

|---|---|---|---|

| Ongoing shift to digital OOH via smart-city projects | +1.8% | National, early uptake in Bangkok, Chiang Mai, Phuket | Medium term (2-4 years) |

| De-congestion of Bangkok airports expanding premium transit inventory | +0.9% | Bangkok metro, spillover to regional hubs | Medium term (2-4 years) |

| Retail-centric mixed-use megaprojects adding high-footfall street furniture | +0.7% | Urban centers nationwide | Short term (≤ 2 years) |

| Tourism-led GDP strategy lifting location-based media budgets | +1.2% | Bangkok, Phuket, Chiang Mai, Krabi, Samui | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Ongoing shift to digital OOH via smart-city projects

Program funding under Thailand’s national smart-city framework is converting static panels into networked digital screens across mass-transit stations, arterial roads, and municipal facilities. Media owners monetize the upgrades through dynamic pricing and daypart scheduling, giving advertisers flexible creative rotations that shorten purchase cycles and improve message relevance vistarmedia [1]Vistar Media, “Vistar Media Expands into Thailand as Part of APAC Growth,” vistarmedia.com . These capabilities are attracting multinational brands that require near-real-time optimization, propelling programmatic supply by 139,000 additional venues in 2024. Over the outlook period, interoperability with city-wide IoT infrastructure is expected to elevate measurement accuracy and reduce perceived risk, reinforcing the Thailand out-of-home advertising market as a performance-oriented channel.

De-congestion of Bangkok airports expanding premium transit inventory

A USD 2.8 billion plan to lift Suvarnabhumi capacity to 150 million passengers and parallel upgrades at Don Mueang, Phuket, and Chiang Mai extend advertiser reach to diverse traveler cohorts bangkokpost [2]Bangkok Post, “Suvarnabhumi Boosts Passenger Target to 150 Million with New Runway,” bangkokpost.com. New high-dwell digital gateways, such as the third runway concourse, enable contextual messaging tied to departure destinations and time bands. CPMs remain three to four times higher than roadside billboards, yet brands accept the premium because audience density and data-feed integrations support strong upper-funnel lift. JCDecaux’s global airport model positions the firm to secure long-term concessions, ensuring consistent quality and technical standards across Thailand’s transit network jcdecaux [3] JCDecaux, “Q3 2024 Revenue: Continued Growth in Digital,” jcdecaux.com .

Retail-centric mixed-use megaprojects adding high-footfall street furniture

Central Pattana’s THB 4.5 billion Central Krabi build and the THB 10 billion transformation of Bangkok sites are designed as “Centers of District,” merging retail, residential, and hospitality flows into a single commercial spine centralpattana. Developers embed digital kiosks, large-format LEDs, and experiential zones into the master plan, giving media owners avenues to upsell daypart-based dynamic inventory. As similar projects proliferate in secondary cities, advertisers gain lower-CPM access to affluent audiences outside the capital, broadening the Thailand out-of-home advertising market footprint.

Tourism-led GDP strategy lifting location-based media budgets

Tourism-led GDP Government aims to welcome 40 million foreign arrivals in 2025, surpassing pre-pandemic highs, by accelerating airport, cruise-terminal, and hospitality projects bangkokpost. Brands targeting high-spending tourists are ramping place-based campaigns inside duty-free zones, piers, and heritage districts, resulting in an 8.6% CAGR for place-based media. Campaigns often align with gastronomy events or cultural festivals championed by the Tourism Authority, ensuring local resonance. The influx of international audiences is anticipated to sustain impression volumes even during domestic spending fluctuations, undergirding long-run revenue visibility for the Thailand out-of-home advertising market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented media-owner landscape raising coordination cost | -0.8% | Nationwide | Long term (≥ 4 years) |

| Limited third-party impression auditing eroding confidence | -1.1% | Nationwide | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Fragmented media-owner landscape raising coordination cost

The market contains numerous small operators with divergent rate cards, file-format standards, and maintenance practices. National advertisers therefore juggle multiple insertion orders, synchronize technical specs, and pay duplicated agency fees, which amplifies campaign overhead and dilutes ROI. While major holding-company agencies are investing in proprietary buying hubs to streamline workflows, the associated platform fees can offset efficiency gains. Until consolidation progresses, the Thailand out-of-home advertising industry will remain encumbered by elevated transaction friction.

Limited third-party impression auditing eroding confidence

Unstandardized footfall and vehicle-traffic metrics hinder cross-channel comparison and undermine post-campaign reporting credibility. High-priced airport and mall screens face particular scrutiny because buyers have minimal independent verification that contracted impression guarantees were met. Some media owners trial computer-vision counting, yet adoption is uneven, leading to a patchwork of methodologies that confuse planners. Unless an industry-wide audience-measurement body emerges, budget growth into the Thailand out-of-home advertising market may lag the medium’s proven brand-building efficacy.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Digital Momentum Redefines Asset Allocation

Static displays retained 63.20% revenue leadership in 2025, benefiting from sunk hardware costs and entrenched landlord contracts. Even so, programmatic formats are scaling quickly at a 11.2% CAGR through 2031 as smart-city grants lower capex barriers for screen replacement. This divergence shows how media owners now allocate upgrade capital to high-yield transit corridors while leaving lower-footfall districts static until depreciation cycles conclude. Vistar Media’s 2024 entry, with 139,000 new programmatic sites, signals rising liquidity for data-driven buys that shorten booking lead times vistarmedia.

Digitization also elevates creative flexibility, allowing advertisers to switch content by hour, weather, or traveler origin. Premium airport walkways, for instance, can rotate bilingual messaging tied to destination gates. As a result, the Thailand out-of-home advertising market size for programmatic is projected to widen its share steadily, even if static boards continue to blanket suburban roadways for cost efficiency. In this context, scale operators differentiate by offering unified trading APIs that consolidate both static and digital inventory under one contract.

By Format: Place-Based Screens Challenge Billboard Primacy

Billboards produced 41.10% of 2025 revenue, using large canvases along expressways and city arteries to reinforce brand equity. Yet place-based screens within malls, supermarkets, and entertainment complexes are advancing at an 8.28% CAGR, reflecting post-pandemic foot traffic rebounds and longer dwell times. Central Pattana’s THB 15 billion pipeline will unlock additional indoor impressions at Central Bangna, Central Pinklao, and Central Chaengwattana, each configured for omnichannel shopper journeys centralpattana.

Advertisers value these controlled environments because they combine audio capability, mobile-data retargeting, and purchase-pressure proximity. The Thailand out-of-home advertising market share for place-based formats is therefore forecast to expand, though roadside billboards will remain vital for mass reach. Transit media inside concourses and along the BTS Silom line supplements both, creating a layered format mix that aligns with funnel position and creative weight.

By Location Environment: Indoor Networks Gain Headroom

Outdoor assets held 71.30% of market revenue in 2025 thanks to Thailand’s year-round visibility and extensive road network. Nonetheless, indoor environments are growing 6.52% annually as malls, airports, and mixed-use towers install high-resolution LEDs and interactive kiosks. Central Pattana posted THB 46,790 million retail revenue in 2023, an increase of 26%, underscoring tenant demand that supports advertising tenancy fees centralpattana.

These controlled climates mitigate weather risk and enable rich-media formats unsuitable for roadside deployment. Brands leverage proximity to point of sale by integrating QR codes and NFC triggers, creating closed-loop attribution unavailable on highways. As the number of high-footfall indoor panels rises, the Thailand out-of-home advertising market size attributed to enclosed venues is expected to inch upward, though street-level reach will still dominate national campaign planning.

By End-User Vertical: Healthcare Gains Share Amid Regulatory Openness

Retail & FMCG spent the most on OOH in 2025, accounting for 26.60% of revenue, as proximity messaging lifts in-store sales. The healthcare & pharma sector, however, shows the highest momentum with a 7.55% CAGR, buoyed by greater public health awareness and comparatively flexible Thai regulations on pharmaceutical promotion. Multilingual campaigns around vaccination drives and wellness tourism benefit from OOH’s credibility in both urban commute paths and hospital campuses.

Automotive brands remain heavy buyers, often pairing 3D billboard creatives with test-drive QR codes. An innovative program by Flare and Toyota Tsusho places wrap-around ads on private vehicles, creating a moving extension of conventional sites toyota-tsusho. BFSI and technology advertisers round out spending, valuing trust signals from premium street furniture. Overall, the Thailand out-of-home advertising industry continues to diversify its client base, thereby smoothing cyclical exposure to any single category.

Geography Analysis

Bangkok anchors the Thailand out-of-home advertising market through dense population, high GDP per capita, and an expanding mass-transit network. The 35.9 kilometer MRT Orange Line, with 28 stations, broadens commuter touchpoints across east-west corridors mrta. Simultaneously, capacity uplifts at Suvarnabhumi and Don Mueang airports add premium inventory with prolonged exposure times, supporting higher CPMs bangkokpost.

Phuket, Chiang Mai, and Krabi attract tourism-centric spend as government targets drive arrivals beyond 40 million by 2025. Phuket International’s THB 6 billion terminal expansion will double capacity to 12 million annual passengers, giving advertisers fresh canvas for luxury campaigns bangkokpost. The Central Krabi complex scheduled for 2026 completion adds indoor networks aligned with beach-resort itineraries centralpattana.

Eastern Economic Corridor provinces such as Rayong and Chonburi gain importance due to the U-Tapao Airport and Eastern Airport City project, which is slated to function as Bangkok’s third international gateway by 2029 eec. Advertisers enjoy lower CPMs while accessing a manufacturing workforce and emerging leisure travelers. These shifts collectively reduce geographic concentration risk, helping the Thailand out-of-home advertising market sustain balanced growth across multiple metropolitan clusters.

Competitive Landscape

The competitive field features international concessionaires and domestic conglomerates. JCDecaux Thailand leverages global airport contracts and digital expertise to control premium concourse screens, reporting a 17.8% year-over-year rise in DOOH revenue in Q3 2024 jcdecaux. VGI PCL, backed by BTS Group, continues to integrate media with sky-train operations under its “MOVE, MIX, MATCH” strategy that packages transit, data, and payment solutions btsgroup [4]BTS Group, “Media Business 3M Strategy Presentation,” btsgroup.co.th. Plan B Media PCL fortifies sports and event assets, driving cross-channel tie-ins.

Technology outsiders are reshaping purchase behavior. Vistar Media opened a Bangkok office in 2024, scaling programmatic demand and closing gaps between digital budgets and street-level screens vistarmedia. Hivestack pursues similar supply-side integrations, sharpening real-time bidding pipes. Meanwhile, Flare’s mobile wrap approach enlarges supply without costly fixed assets, pressuring legacy owners to innovate toyota-tsusho.

Competitive intensity is driving selective mergers and revenue-share renegotiations to secure long-term site control, particularly for high-footfall transit corridors. The need to finance LED conversions and measurement tech favors scale players, suggesting moderate consolidation over the forecast window. Nonetheless, niche local firms retain strong landlord relationships, ensuring that the Thailand out-of-home advertising market stays only semi-consolidated.

Thailand OOH And DOOH Industry Leaders

VGI PCL

Plan B Media PCL

JCDecaux Thailand Ltd.

Clear Channel Outdoor Thailand

Hivestack Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Central Pattana announced a THB 4.5 billion (USD 0.14 billion) mixed-use development in Krabi and a THB 10 billion transformation of Bangna, Pinklao, and Chaengwattana sites, broadening high-footfall OOH opportunities.

- November 2024: JCDecaux posted Q3 2024 adjusted revenue of EUR 948.2 million (USD 1111.43 million), with DOOH contributing 38.5%, reflecting ongoing digital acceleration.

- October 2024: Makro and GroupM introduced the Makro Retail Media Network, targeting THB 2 billion in in-store advertising budgets.

- October 2024: Thaicom, INVIDI, and PSI launched addressable TV advertising with plans to extend the capability to OOH screens.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Mordor Intelligence defines Thailand's out-of-home (OOH) and digital out-of-home (DOOH) market as the gross media spend booked on static billboards, street furniture, transit assets, and place-based digital screens that carry paid advertising messages, whether sold programmatically or by fixed tenancy, within Thailand's borders.

Scope Exclusion: Agency service fees and physical production or installation costs sit outside this valuation.

Segmentation Overview

- By Type

- Static (Traditional) OOH

- Digital OOH

- Programmatic OOH

- Other Digital Types

- By Format

- Billboard

- Transit

- Airports

- Other Transit (Bus, MRT, BTS)

- Street Furniture

- Place-Based Media

- By Location Environment

- Indoor

- Outdoor

- By End-User Vertical

- Retail and FMCG

- Automotive

- BFSI

- Healthcare and Pharma

- Others

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed media-owner executives, agency trading-desk leads, retail-mall asset managers, and outdoor-measurement specialists across Bangkok, Chiang Mai, Phuket, and secondary provinces to verify screen counts, secondage pricing, and occupancy shifts flagged by desk findings.

Desk Research

We began by mining Thai Customs broadcast-equipment imports, the National Economic and Social Development Council's quarterly ad-spend tables, and industry briefs from the Media Agency Association of Thailand. These were cross-referenced with audience data issued by the Advertising Association of Thailand, airport traffic tallies from Airports of Thailand, and MRT ridership released by the Bangkok Mass Transit System. To enrich financial context, our team screened company filings in D&B Hoovers and news flows captured in Dow Jones Factiva. The sources listed illustrate, not exhaust, the secondary evidence base consulted.

Market-Sizing & Forecasting

A top-down model starts with net advertising expenditure reported by official bodies, which is then split by medium and converted to OOH share using five-year averages. We corroborate totals with bottom-up spot checks, billboard inventory roll-ups, and sampled average spend per panel multiplied by occupancy. Key drivers embedded in the model include installed digital screen stock, airport and MRT passenger volumes, inbound tourist arrivals, CPM inflation, and smart-city screen mandates. These variables feed a multivariate regression and scenario-analysis module that projects value through 2030. Provincial gaps are bridged through GDP weightings.

Data Validation & Update Cycle

Outputs pass a three-layer review: algorithmic outlier scans, peer-analyst audits, and final practice-head sign-off. Models refresh annually; interim recalculations trigger when regulatory caps, major tender awards, or currency swings above 10% occur, ensuring clients always receive the latest vetted view.

Why Mordor's Thailand OOH And DOOH Baseline Commands Reliability

Published estimates often diverge because firms differ on what counts as spend, how they treat digital loop frequency, and the cadence of refresh.

Key Gap Drivers: Some providers fold creative production into market value, others include screen-hardware sales, and a few project only DOOH impressions without subtracting barter inventory, leading to inflation or under-capture versus Mordor's net-spend focus.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 493.46 M (2025) | Mordor Intelligence | |

| USD 520 M (2024) | Regional Consultancy A | Uses broader base year and converts gross rate-card spend without discount normalization |

| USD 4.8 B (2025) | Sector Specialist B | Counts only DOOH and adds hardware plus service revenue, inflating size |

These comparisons show that Mordor's disciplined scope, dual-angle modeling, and yearly refresh supply a balanced, transparent baseline that decision-makers can trace back to measurable Thai advertising variables.

Key Questions Answered in the Report

What is the current size of the Thailand out-of-home advertising market?

The market is valued at USD 517.55 million in 2026 and is forecast to reach USD 656.77 million by 2031 at a 4.88% CAGR.

Which segment is growing fastest within the Thailand out-of-home advertising market?

Programmatic digital OOH is expanding 11.2% annually, more than double the overall market rate.

How do airport expansions influence OOH revenue in Thailand?

Capacity upgrades at Suvarnabhumi, Don Mueang, Phuket, and Chiang Mai introduce high-dwell digital sites that command premium CPMs, lifting transit OOH revenue potential.

Why are mixed-use developments important to advertisers?

Projects like Central Krabi integrate retail, residential, and hospitality activities, generating captive audiences and new digital street-furniture inventory.

Page last updated on: