Domain Name System Firewall Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

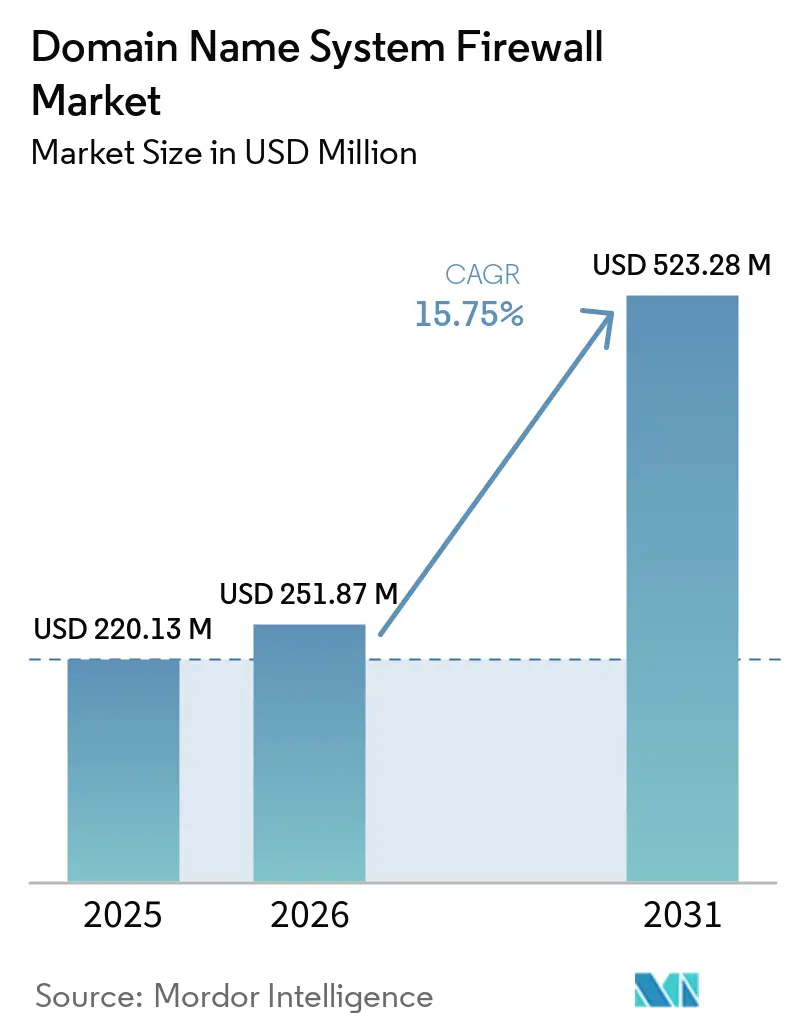

| Market Size (2026) | USD 251.87 Million |

| Market Size (2031) | USD 523.28 Million |

| Growth Rate (2026 - 2031) | 15.75% CAGR |

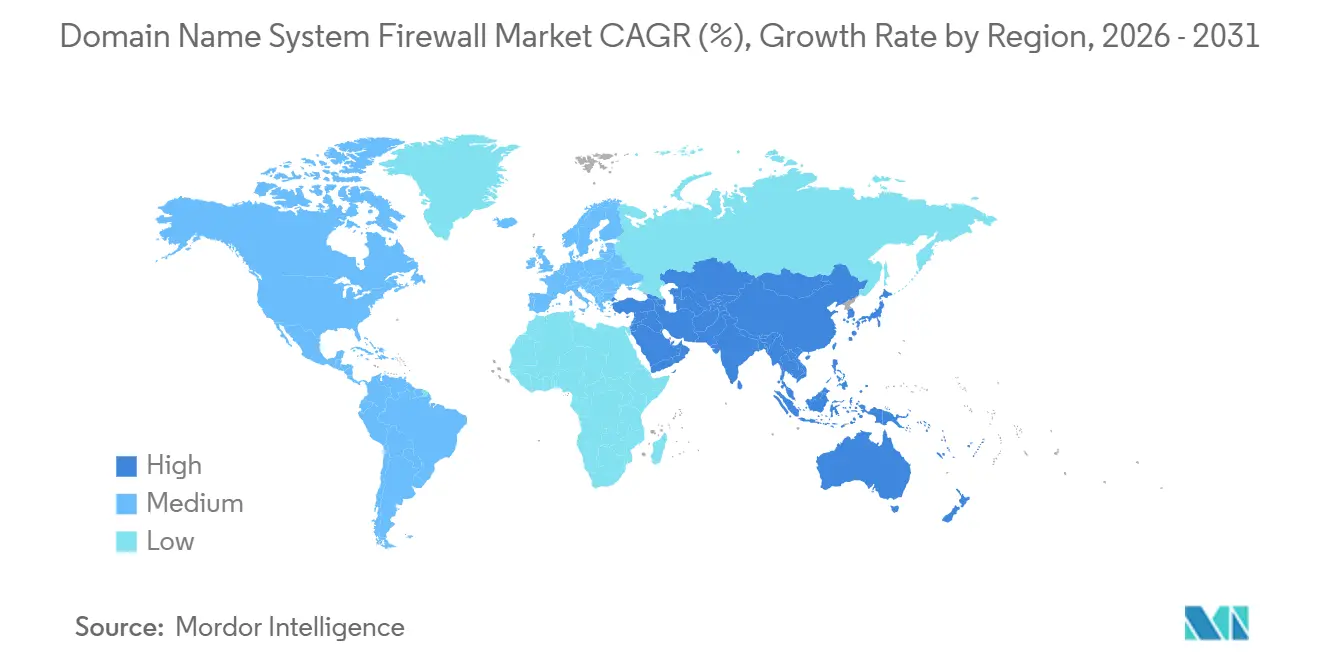

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Domain Name System Firewall Market Analysis by Mordor Intelligence

The Domain Name System Firewall market size was valued at USD 220.13 million in 2025 and estimated to grow from USD 251.87 million in 2026 to reach USD 523.28 million by 2031, at a CAGR of 15.75% during the forecast period (2026-2031). The rapid lift in spending mirrors the migration from passive DNS logging to active, policy-based blocking at the resolver and authoritative tiers. Encrypted DNS protocols, chiefly DNS over HTTPS and DNS over TLS, now cloak query contents from legacy inspection tools, so enterprises are embedding threat intelligence directly into name-server software to keep visibility alive. Telecom carriers are turning their recursive footprints into managed security revenue streams, while hyperscale cloud providers fold DNS firewalls into secure access service edge offerings to defend workloads moving among data centers, public clouds, and edge sites. Against this backdrop, performance concerns in latency-sensitive verticals such as high-frequency trading and clinical imaging are steering many buyers toward hybrid deployment patterns that let on-premises resolvers coexist with cloud orchestration.

Key Report Takeaways

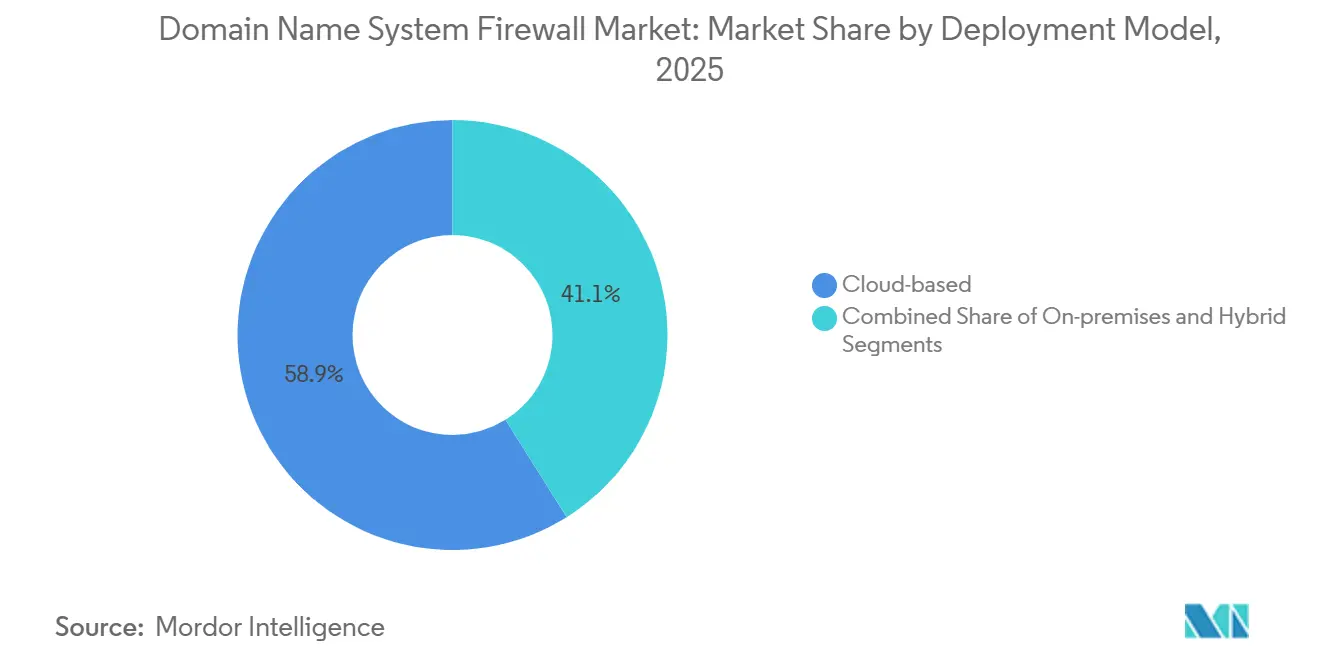

- By deployment model, cloud-based options led with a 58.91% revenue share in 2025; hybrid configurations are projected to advance at a 16.43% CAGR through 2031.

- By DNS server type, recursive resolver firewalls held 38.45% of the Domain Name System Firewall market share in 2025; authoritative variants are forecast to expand at a 15.95% CAGR over 2026-2031.

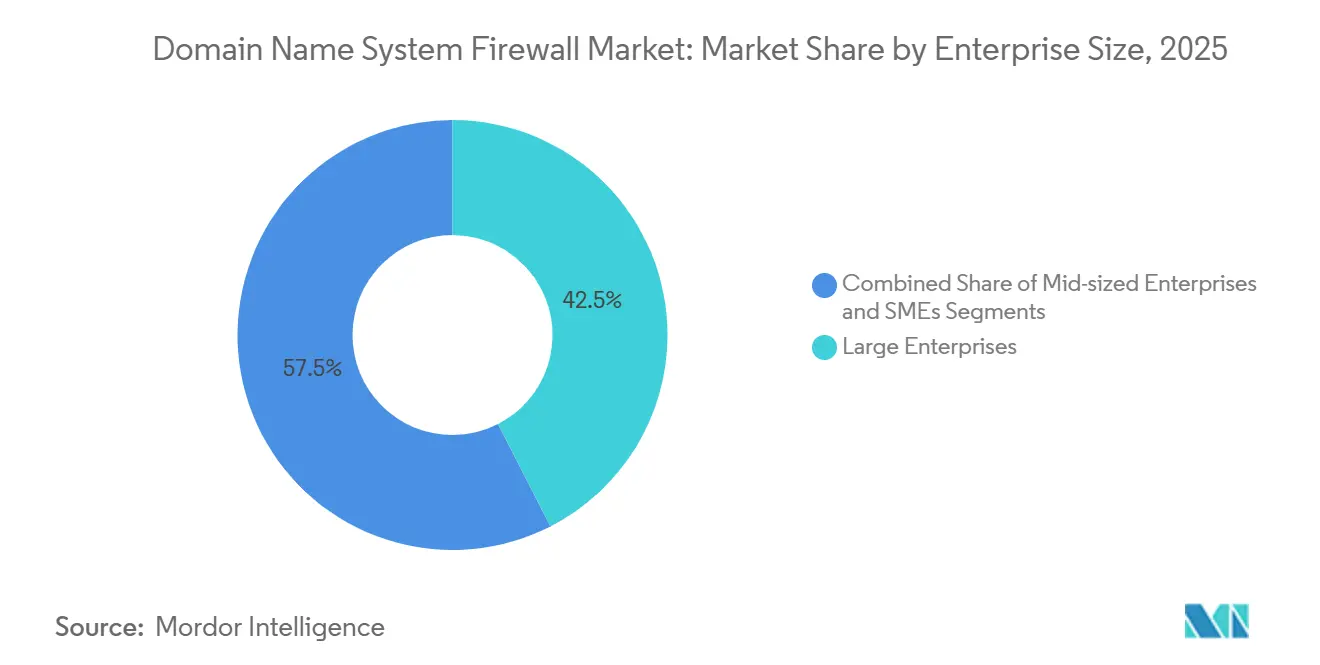

- By enterprise size, large enterprises accounted for 42.45% of spending in 2025; SMEs are poised to grow at a 16.21% CAGR to 2031.

- By industry vertical, BFSI deployments captured 25.46% of 2025 revenue; healthcare and life sciences are expected to climb at a 16.11% CAGR during the forecast horizon.

- By geography, North America dominated with a 42.56% contribution in 2025; Asia-Pacific is projected to post the fastest trajectory at a 15.92% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Domain Name System Firewall Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing DNS-Layer Attacks Driving Mandatory Security Investments | +3.2% | Global, strongest in North America and Europe | Short term (≤ 2 years) |

| Rapid Migration to Multi-Cloud and Hybrid IT Architectures | +2.8% | North America and Europe core, expanding into Asia-Pacific hubs | Medium term (2-4 years) |

| Regulatory Mandates for Zero-Trust and Secure Access Service Edge Frameworks | +2.5% | Europe, North America, Asia-Pacific | Medium term (2-4 years) |

| Growing Use of DNS Tunneling for Command-and-Control in Edge IoT Fleets | +2.1% | Global, early uptake in manufacturing and logistics | Long term (≥ 4 years) |

| Rise of Everything over HTTPS Accelerating Encrypted DNS Adoption | +1.9% | Global, led by enterprise segments in North America and Europe | Medium term (2-4 years) |

| Telecom Operators Monetizing DNS Threat-Intelligence Feeds to Enterprises | +1.6% | North America, Europe, Middle East telecom markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Increasing DNS-Layer Attacks Driving Mandatory Security Investments

High-volume reconnaissance, phishing, and distributed denial-of-service assaults are shifting corporate security budgets toward resolver-centric countermeasures. A joint advisory from the U.S. Cybersecurity and Infrastructure Security Agency and the National Security Agency in March 2025 flagged “fast flux” domain rotation that hides attacker infrastructure behind constantly changing IP addresses, rendering static blocklists obsolete. The technique gained urgency after the Federal Bureau of Investigation dismantled a Russian botnet that hijacked more than one million small-office routers in early 2024, illustrating how ubiquitous DNS traffic can be weaponized.[1]Federal Bureau of Investigation, “FBI Disrupts Russian Botnet,” FBI.gov Infoblox’s 2025 DNS Threat Report logged a 37% rise in tunneling events, confirming that adversaries now view DNS as a low-friction command-and-control pathway. Board-level cyber-risk discussions increasingly treat protective DNS as a prerequisite for cyber-insurance underwriting, compressing procurement cycles from years to quarters.

Rapid Migration to Multi-Cloud and Hybrid IT Architectures

Enterprises juggling workloads across Amazon Web Services, Microsoft Azure, Google Cloud, and colocation sites struggle to keep consistent domain policies. IBM’s NS1 Connect white paper documented that financial firms maintain at least two external DNS providers to eliminate single points of failure, a practice vindicated when a major platform suffered a six-hour recursive outage in mid-2024.[2]IBM, “NS1 Connect Multi-Provider DNS Architecture,” IBM.com Performance-critical apps, from algorithmic trading to real-time patient telemetry, still depend on local resolvers, so organizations favor hybrid designs that blend on-premises appliances with cloud orchestration. Cisco addressed those latency and sovereignty concerns in April 2026 by rolling out localized DNS firewall appliances for Gulf Cooperation Council markets while tying them back to its Umbrella cloud layer for a unified policy push. The architectural sprawl fuels demand for management consoles that broadcast threat feeds and response-policy zones across disparate resolver instances in near real time. Vendors that can automate this federation without degrading query performance are winning disproportionate wallet share.

Regulatory Mandates for Zero-Trust and Secure Access Service Edge Frameworks

Compliance is no longer a checkbox exercise in Europe or North America. The Digital Operational Resilience Act, live since January 2025, obliges EU financial entities to log and analyze DNS traffic as part of ICT risk management.[3]European Commission, “The NIS2 Directive,” Digital-strategy.ec.europa.eu Simultaneously, the U.S. Cybersecurity and Infrastructure Security Agency earmarked USD 24.7 million in fiscal 2025 to widen its Protective DNS program, offering threat-fed recursive services to federal agencies and critical infrastructure operators. Japan’s February 2026 DNSSEC guideline, authored by the Ministry of Internal Affairs and Communications, ratchets up cryptographic validation expectations for hospitals and utilities. These statutes penalize non-compliance with fines and reputational harm, accelerating budget approvals for resolver-level defenses. Consequently, solution providers that map feature roadmaps directly to zero-trust and SASE frameworks see faster sales cycles and lower churn.

Growing Use of DNS Tunneling for Command-and-Control in Edge IoT Fleets

Industrial environments now attach millions of sensors and programmable logic controllers to IP networks, yet outbound DNS gets little scrutiny. Researchers uncovered the “Dohdoor” backdoor in 2024, which sneaks commands through DNS over HTTPS to circumvent firewall rules. A 2025 campaign dubbed ZipLine siphoned manufacturing blueprints before detonating ransomware in plant control systems, relying on tunneled DNS to skirt perimeter monitoring. Vendors such as Robustel reacted by baking DNS firewalls into cellular routers that sit at edge gateways, blocking anomalous query bursts before they traverse the WAN. Secure64’s LineGuard appliance applies cryptographic validation and rate limiting at the protocol layer, making large-scale amplification and tunneling infeasible. As 5G private networks extend IoT reach, resolver-side inspection is emerging as the only scalable counter to covert DNS channels.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Replacement Cost for Legacy Recursive Servers in Large Incumbents | -1.8% | Global, acute in North America and Europe | Medium term (2-4 years) |

| Lack of Skilled DNS Security Professionals | -1.3% | Global, acute in Asia-Pacific and Middle East emerging markets | Long term (≥ 4 years) |

| Performance Trade-Offs with Encrypted DNS over Satellite Back-Haul Links | -0.9% | Remote and maritime deployments worldwide | Long term (≥ 4 years) |

| Fragmentation of National Root-Server Policies in Sovereign Clouds | -0.7% | China, Russia, Middle East sovereign-cloud zones | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Replacement Cost for Legacy Recursive Servers in Large Incumbents

Financial and telecom giants that standardized on open-source resolvers such as BIND face capital outlays topping USD 500,000 when migrating to commercial firewalls. Geographic clusters built for redundancy house hundreds of anycast nodes that cannot simply be “forklifted” into new hardware. NIST’s Special Publication 800-81 Revision 3 cautions that retrofitting DNSSEC and response-policy zones can drag on for 12–18 months in brownfield environments.[4]National Institute of Standards and Technology, “SP 800-81 Rev 3,” Nist.gov During the transition window, teams must dual-maintain old and new infrastructure, inflating labor costs and elongating change-control windows. The budgetary shock is especially acute in manufacturing and retail, where thin operating margins leave minimal headroom for seven-figure security projects.

Lack of Skilled DNS Security Professionals

Running a resolver-level defense stack demands a rare blend of network engineering and threat-intel analysis. The Internet Society’s 2025 report flagged that many operators cannot interpret DNSSEC failures or tune response-policy zones, leaving default configurations unoptimized. While managed service providers fill gaps in North America and Europe, enterprises subject to audit restrictions, such as banking or defense, prefer in-house talent. Emerging markets face an even wider deficit; Malaysia’s April 2026 DNSSEC workshop drew more than 300 attendees, yet it still covers only a fraction of the personnel needed for nationwide rollouts. Until university curricula elevate DNS security to core coursework, skill scarcity will temper adoption velocity despite growing executive awareness.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment Model: Hybrid Gains as Latency Trumps Cloud Economics

Hybrid setups accounted for a material slice of 2025 spending and are growing at 16.43% CAGR, outpacing the broader Domain Name System Firewall market. Organizations first gravitated to cloud-based firewalls for quick wins, 58.91% of outlays in 2025, but discovered that added query hops inflate latency by 10-20 milliseconds, an unacceptable drag on trading algorithms and clinical imaging systems. Consequently, buyers now mesh lightweight on-premises resolvers with cloud orchestration to retain sub-millisecond response while centralizing policy control. EfficientIP’s 2025 survey found that 62% of firms above 10,000 employees already run such dual architectures, and NIS2 resilience mandates reinforce the trend. The Domain Name System Firewall market size benefits because buyers procure both subscriptions and appliance hardware instead of choosing one or the other.

A second growth lever is sovereign-cloud regulation. Saudi Arabia’s Salam Secure DNS keeps all logs within national borders while still accepting threat-feed pushes from vendor clouds, providing a playbook for other Gulf markets. Cloudflare Gateway illustrates the opposite end of the spectrum: more than 15,000 enterprises without legacy gear leaped straight into pure cloud DNS in 2025. Still, as edge sites proliferate, caching forwarders will remain indispensable for branch offices where bandwidth is scarce. Whether orchestrated centrally or run stand-alone, resolver diversity is now a compliance requirement rather than an architectural preference.

By DNS Server Type: Authoritative Firewalls Rise as SaaS Providers Harden Infrastructure

Recursive resolver engines remained the workhorse in 2025, controlling 38.45% of the Domain Name System Firewall market share because every endpoint query begins there. Yet authoritative-layer defenses are climbing at a 15.95% CAGR, propelled by SaaS vendors and CDNs fending off terabit-scale reflection floods. Akamai logged a 71% spike in such assaults during 1H 2025, forcing operators to deploy rate limiting and DNSSEC validation at the zone apex. New architectural blueprints now recommend pairing resolver and authoritative filters in a shared policy mesh, moving the Domain Name System Firewall market closer to a unified control-plane vision.

VeriSign’s daily query load of 183 billion illustrates the throughput requirement that authoritative engines must satisfy without false positives. Neustar and F5 have responded with machine-learning classifiers that flag anomalous volume bursts or geo anomalies in sub-second intervals. The Internet Engineering Task Force’s draft Protective DNS framework further cements feature parity guidelines, ensuring vendor differentiation skews toward analytics depth rather than basic block-and-allow lists. With SaaS adoption still climbing, authoritative firewalls should preserve their growth premium well into the next decade even as recursive spending stays robust.

By Enterprise Size: SMEs Adopt as MSPs Bundle DNS Filtering

Large enterprises generated 42.45% of 2025 billings, reflecting sprawling multi-cloud estates that demand dedicated DNS security operations centers. However, the steepest slope sits with SMEs, whose 16.21% CAGR eclipses the headline Domain Name System Firewall market rate. Low-touch managed service bundles under USD 10 per employee remove deployment friction, putting resolver-level protection within reach of cash-constrained IT teams. DNSFilter reported in 2025 that nearly 7 in 10 customers employ fewer than 500 workers, confirming bottom-up momentum.

Mid-sized firms, often migrating from on-premises BIND clusters, weigh capital avoidance against data-residency concerns. Cisco Umbrella’s 2025 poll showed 74% of that cohort valuing identity-provider integration above all else, nudging roadmaps toward SAML and OAuth compatibility. At the top end, Fortune 500 banks lean on Infoblox BloxOne to fuse DNS telemetry with XDR platforms, automating device isolation when malicious lookups spike. The upshot is layered purchasing behavior: SMEs consume resolver security as a utility, midsized buyers chase ease of integration, and large enterprises insist on API-rich analytics pipelines that feed SIEM dashboards.

By Industry Vertical: Healthcare Surges on HIPAA Compliance Pressure

BFSI entities retained supremacy in 2025 with a 25.46% slice of revenue, a position undergirded by fraud-prevention mandates in DORA and Payment Card Industry guidelines. Yet healthcare is scripting the most aggressive climb, charting a 16.11% CAGR that beats the underlying Domain Name System Firewall market size expansion. February 2026 ushered in a revised HIPAA Security Rule obligating DNS-layer anomaly detection within 240 days, forcing hospitals, insurers, and medical device makers to accelerate purchase orders.

Clinical environments pose distinct hurdles: many imaging scanners and infusion pumps run antiquated OS builds that cannot host endpoint agents. Resolver-centric controls, therefore, offer the only scalable shield against domain-spoofing and ransomware callback traffic. Vendors like Vigilbase now package asset discovery, IoT risk scoring, and DNS firewalling into unified portals that satisfy both biomedical engineers and compliance officers. Elsewhere, retailers pivot to resolver filtering to meet PCI DSS v4.0 network-monitoring clauses, and manufacturers deploy edge-ready appliances to stop designs from leaking through tunneled DNS.

Geography Analysis

North America generated 42.56% of 2025 receipts after the U.S. Protective DNS initiative funneled threat-fed resolver services into 101 federal agencies. Mature cyber budgets, plus proximity to hyperscale clouds and managed security innovators, keep the region ahead on absolute spend. Canada’s Center for Cyber Security echoed the push in 2025 by advising provincial health systems to harden recursive infrastructure, and Mexico’s regulators compelled banks to monitor DNS following 2024 hijacking incidents.

Asia-Pacific, tracking a 15.92% CAGR, tops the velocity charts. Japan earmarked JPY 4.93 billion (USD 33 million) for university and utility resolver rollouts, while India’s CERT-In processed 2.944 million incidents in 2025 and doubled down on an AI-driven malicious-domain detection grid. South Korea’s KISA plugged EU and U.S. threat intel into its 2025 monitoring stack, illustrating growing cross-regional data sharing. Across ASEAN, ICANN’s regional plan boosted DNSSEC workshops, accelerating public-sector adoption.

Europe’s trajectory is shaped by NIS2 and DORA, which pull DNS into the core of supply-chain audits. Germany’s BSI, the U.K.’s National Cyber Security Center, and sovereign-cloud initiatives in Saudi Arabia and the UAE reinforce the view that resolver policy is now as strategic as firewall policy. Africa and South America still lag in spending, but managed security providers are introducing pay-as-you-go resolver protection that may compress the gap over the next five years.

Competitive Landscape

Infoblox, Cisco, and Akamai lead a moderate-concentration field, leveraging deep customer footprints in DDI, networking, and content delivery to upsell resolver protection suites. Cloudflare and Zscaler use single-pane dashboards to fold DNS firewalls into broader secure access service edge arsenals, winning greenfield cloud-native deals where legacy appliances never existed. Palo Alto Networks marches down the same path, embedding DNS policies into next-generation firewalls so customers avoid overlay products.

Telecom operators have emerged as disruptors. AT&T monetizes carrier-grade resolvers via its Dynamic Defense tiers, bundling curated threat feeds and compliance dashboards. European and Middle Eastern telcos replicate the model, incentivized by privacy regulations that favor domestic data residency. Privacy-first nonprofits such as Quad9 carve a niche among GDPR-sensitive enterprises, pledging never to monetize query logs.

Standardization also reshapes rivalry. The IETF’s Protective DNS draft harmonizes response-policy zone syntax and telemetry export formats, flattening feature disparities and intensifying competition on price and analytics quality. Huawei seizes momentum in Asia-Pacific and the Gulf by baking DNS firewall functions into router silicon, sidestepping procurement objections tied to appliance sprawl. Meanwhile, Secure64, Neustar, and EfficientIP focus on industrial and sovereign-cloud deployments where deterministic latency and locality are contractual must-haves.

Domain Name System Firewall Industry Leaders

Infoblox Inc.

Cloudflare, Inc.

Cisco Systems, Inc.

Akamai Technologies, Inc.

BlueCat Networks, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Cisco Systems introduced a Sovereign Critical Infrastructure portfolio that pairs localized DNS firewall appliances for Saudi Arabia and Gulf markets with its Umbrella cloud service, targeting National Cybersecurity Authority compliance.

- April 2026: India’s CERT-In issued an advisory on AI-driven attacks that leverage domain-generation algorithms, urging critical infrastructure operators to deploy machine-learning-ready DNS firewalls and reinforcing the nation’s 6-hour breach-notification rule.

- April 2026: Malaysia’s MYNIC and the National Cyber Security Agency hosted a DNSSEC training program for 300+ government and critical-infrastructure staff, advancing the country’s quantum-resilient DNS agenda.

- February 2026: JPNIC published a DNSSEC guideline prepared by Japan’s Ministry of Internal Affairs and Communications, accelerating cryptographic validation across critical infrastructure.

Global Domain Name System Firewall Market Report Scope

| On-premises |

| Cloud-based |

| Hybrid |

| Recursive Resolver Firewall |

| Authoritative DNS Firewall |

| Caching Forwarder Firewall |

| Large Enterprises (≥1,000 employees) |

| Mid-sized Enterprises (100–999 employees) |

| SMEs (<100 employees) |

| BFSI |

| IT and Telecommunications |

| Government and Defense |

| Healthcare and Lifesciences |

| Retail and e-Commerce |

| Manufacturing |

| Other Industry Vertical |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| ASEAN | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of the Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Deployment Model | On-premises | ||

| Cloud-based | |||

| Hybrid | |||

| By DNS Server Type | Recursive Resolver Firewall | ||

| Authoritative DNS Firewall | |||

| Caching Forwarder Firewall | |||

| By Enterprise Size | Large Enterprises (≥1,000 employees) | ||

| Mid-sized Enterprises (100–999 employees) | |||

| SMEs (<100 employees) | |||

| By Industry Vertical | BFSI | ||

| IT and Telecommunications | |||

| Government and Defense | |||

| Healthcare and Lifesciences | |||

| Retail and e-Commerce | |||

| Manufacturing | |||

| Other Industry Vertical | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| ASEAN | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of the Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current Domain Name System Firewall market size and how fast is it growing?

The Domain Name System Firewall market size stood at USD 251.87 million in 2026 and is projected to reach USD 523.28 million by 2031, reflecting a 15.75% CAGR over 2026-2031.

Which deployment model is gaining traction among enterprises?

Hybrid configurations that blend on-premises resolvers with cloud orchestration are expanding at a 16.43% CAGR as they balance latency and centralized policy control.

Why are healthcare organizations accelerating DNS firewall adoption?

A revised HIPAA Security Rule effective February 2026 mandates DNS-layer logging and anomaly detection, pushing hospitals and insurers to upgrade resolver defenses within a 240-day compliance window.

Which region is the fastest-growing market for DNS firewalls?

Asia-Pacific leads with a projected 15.92% CAGR through 2031, buoyed by large-scale initiatives in Japan and India that subsidize protective DNS services for critical infrastructure.

How are telecom operators influencing competitive dynamics?

Carriers such as AT&T now bundle resolver-level threat intelligence into managed security packages, monetizing their DNS infrastructure and squeezing margins for standalone appliance vendors.

What is the biggest barrier to widespread DNS firewall deployment?

The shortage of skilled DNS-security professionals, especially in emerging markets, hampers implementation despite rising executive awareness and regulatory pressure.

Page last updated on: