DNS, DHCP, And IPAM Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

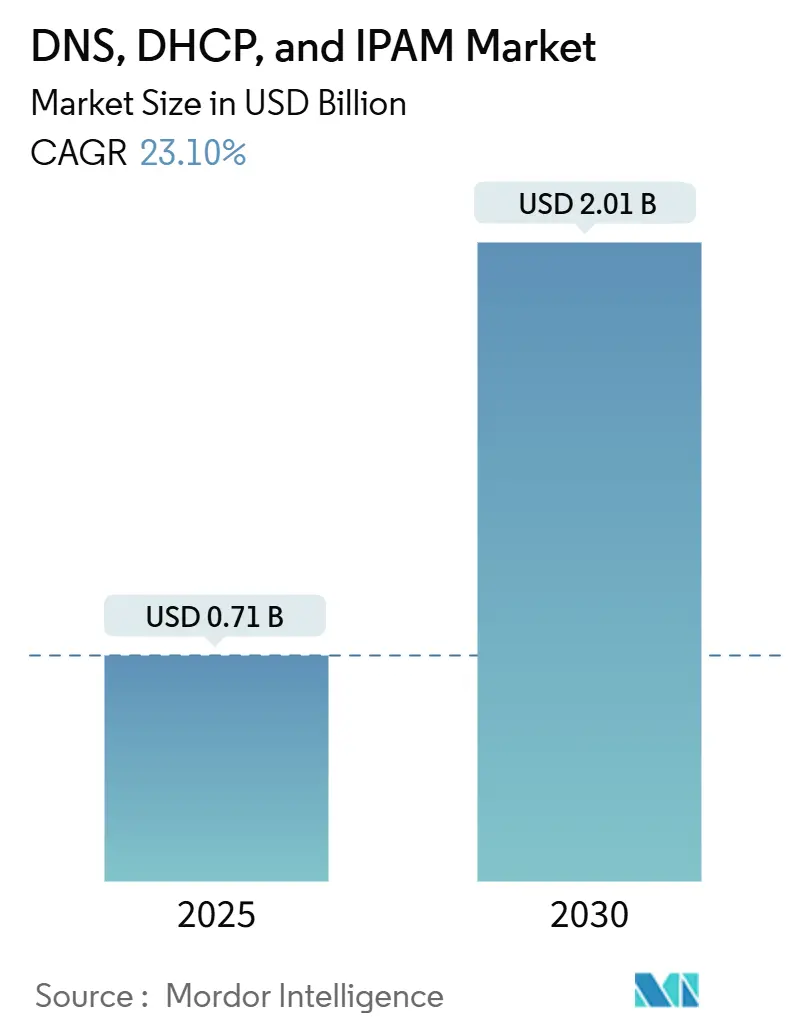

| Market Size (2025) | USD 0.71 Billion |

| Market Size (2030) | USD 2.01 Billion |

| Growth Rate (2025 - 2030) | 23.10% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

DNS, DHCP, And IPAM Market Analysis by Mordor Intelligence

The DNS, DHCP, and IPAM market size stands at USD 0.71 billion in 2025 and is forecast to reach USD 2.01 billion by 2030, reflecting a 23.1% CAGR through the period. The expansion aligns with soaring endpoint counts, multi-cloud adoption, and an upswing in DNS-focused cyber-attacks that collectively strain traditional network tools. Vendors gain momentum by embedding threat-intelligence feeds, API-first automation, and cloud-native delivery that simplify roll-outs for both global enterprises and first-time SME buyers. Early movers also benefit from regulatory tailwinds-GDPR, NIS2, and evolving U.S. sector mandates—that require granular IP address audit trails. Meanwhile, managed DDI services climb because organizations face talent gaps in scripting, DevOps, and DNS security and therefore outsource day-to-day operations to specialists. Competition intensifies as public-cloud providers bundle DNS resolution and IPAM add-ons, prompting pure-play suppliers to differentiate on multi-cloud neutrality, AI analytics, and zero-touch edge deployment features.

Key Report Takeaways

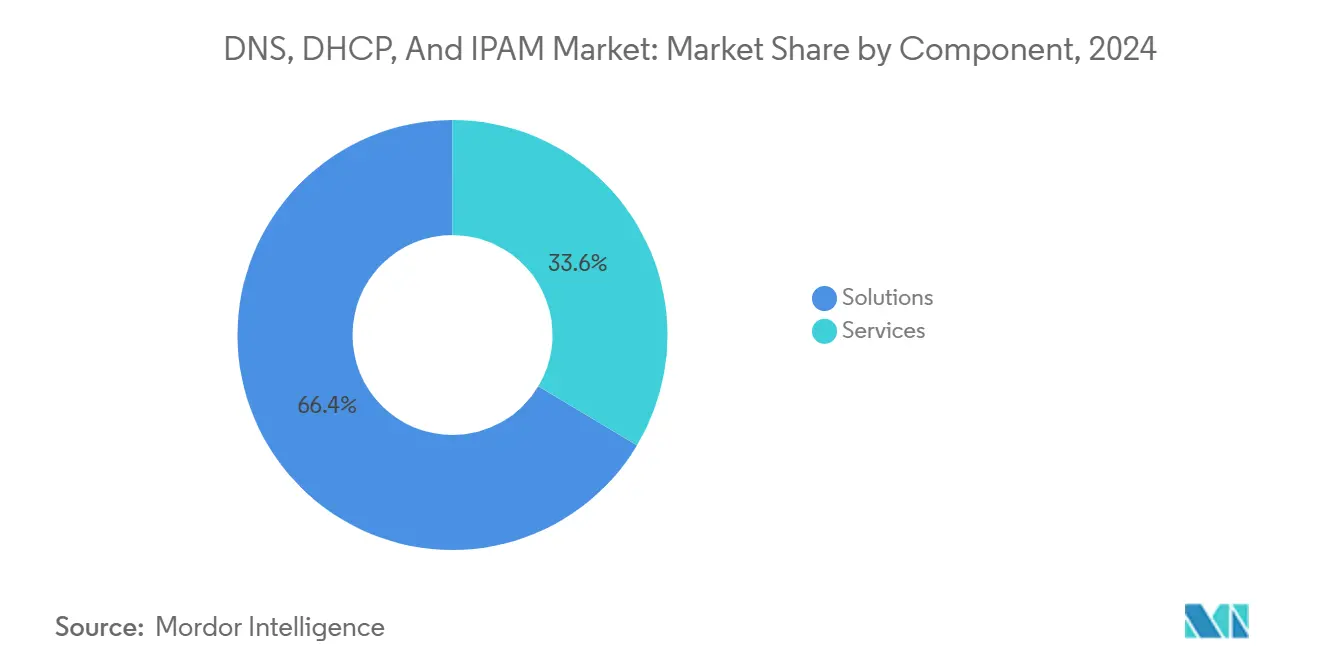

- By component, solutions held 66.43% of the DNS, DHCP, and IPAM market share in 2024, while services recorded the fastest CAGR at 24.56% through 2030.

- By deployment model, on-premise installations accounted for 53.26% of the DNS, DHCP, and IPAM market size in 2024; cloud deployment is projected to compound at a 24.89% CAGR to 2030.

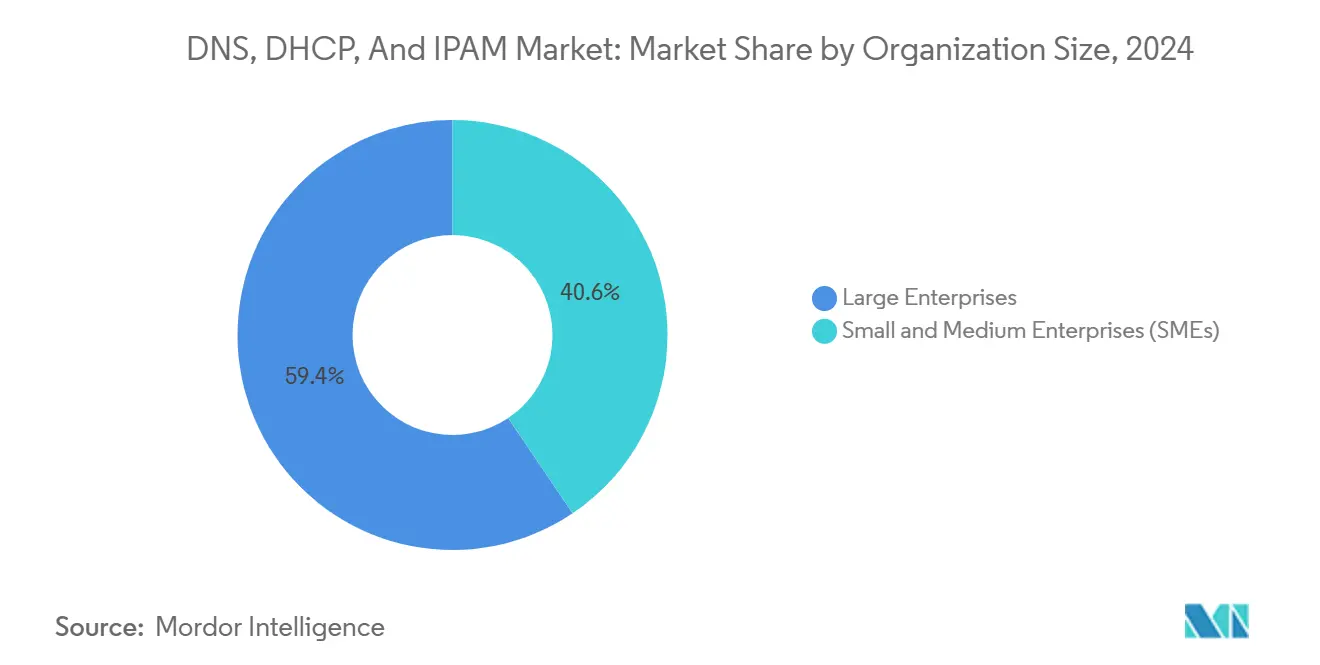

- By organization size, large enterprises captured 59.43% revenue share in 2024; SMEs exhibit the highest growth at 24.97% CAGR through 2030.

- By end-user industry, telecom and IT led with 27.94% revenue share in 2024, whereas manufacturing is forecast to expand at 23.67% CAGR to 2030.

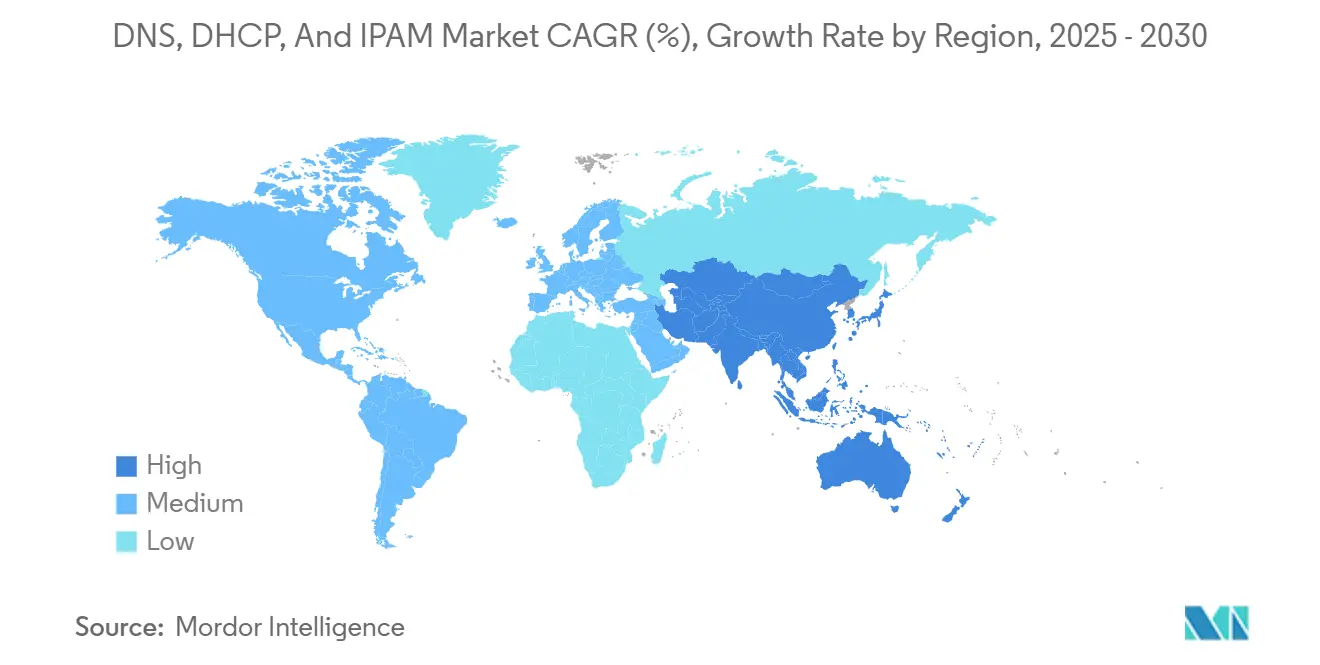

- By geography, North America commanded 36.82% revenue share in 2024, and Asia-Pacific is advancing at 23.94% CAGR through 2030.

Global DNS, DHCP, And IPAM Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Proliferation of IoT-connected endpoints expanding IP pools | +4.2% | Global; Asia-Pacific manufacturing, North America smart-city pilots | Medium term (2-4 years) |

| Escalating DNS-based cyber-attacks pushing security-driven DDI adoption | +3.8% | North America and EU; Asia-Pacific finance emerging | Short term (≤ 2 years) |

| Hybrid/multi-cloud complexity requiring centralized IP visibility | +3.5% | Global; enterprise-dense regions | Medium term (2-4 years) |

| Compliance mandates for address-level audit trails | +2.9% | EU primary; North America secondary; Asia-Pacific emerging | Long term (≥ 4 years) |

| DevOps shift toward Infrastructure-as-Code integrating DDI APIs | +2.7% | North America and EU tech hubs | Short term (≤ 2 years) |

| 5G edge and private-network rollouts demanding ultra-low-latency DDI | +2.1% | Asia-Pacific manufacturing, North America telecom, EU industrial | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

IoT Endpoint Proliferation Drives IP Address Pool Expansion

Manufacturers deploying smart-factory programs report device densities of up to 1 million sensors per 5G cell, a scale that renders static IP spreadsheets obsolete. [1]TRANSFORMA INSIGHTS, “Mobile Private Networks,” transformainsights.com Dynamic DHCP orchestration and automated IPAM discovery shorten device-inventory collection time by 90% once rolled into modern DDI suites. IPv6 momentum climbs because IPv4 exhaustion cannot satisfy these volumes, especially inside smart-city and Industry 4.0 footprints.

DNS-Based Cyber-Attacks Accelerate Security-Focused Adoption

Campaigns such as “Revolver Rabbit” registered more than 500,000 rogue domains at a cost exceeding USD 1 million to sidestep perimeter tools. [2]INFOBLOX, “Revolver Rabbit’s Million-Dollar Masquerade,” infoblox.com Enterprises integrating DNS telemetry into DDI platforms detect threats an average of 63 days earlier and block 77% more malware callbacks than stand-alone firewalls. Heightened vigilance around state-orchestrated exploits like “Muddling Meerkat” cements DNS security as a board-level concern.

Hybrid-Cloud Complexity Demands Centralized Visibility

Organizations migrating thousands of apps and petabyte-scale data sets to AWS and Azure save 22% in cloud expenses when they unify IP address tracking and policy synchronization under one DDI plane. Cloud-native workloads spin up and down within seconds, and only API-driven discovery maintains accurate mappings between ephemeral addresses and business services.

DevOps Integration Through Infrastructure-as-Code

Roughly 97% of mature multi-cloud enterprises embed Terraform or Ansible modules that call DDI APIs for automated DNS record creation and scope allocation, trimming manual handoffs and cutting network-provisioning labor by 19%. Container clusters also rely on the same hooks for real-time service discovery across nodes.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront cost of appliance-centric DDI platforms | −2.8% | Global; SME adoption hit hardest | Short term (≤ 2 years) |

| Shortage of advanced DDI skillsets among NetOps teams | −2.1% | Global; acute in Asia-Pacific and emerging markets | Medium term (2-4 years) |

| Budget competition with broader cybersecurity priorities | −1.7% | North America and EU enterprises | Short term (≤ 2 years) |

| Data-sovereignty concerns slowing cloud DDI uptake | −1.4% | EU and regulated sectors worldwide | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Upfront Costs Limit Appliance-Based Deployments

Enterprise-grade appliances often start near USD 50,000 and climb to USD 200,000 once feature bundles and redundant hardware are factored in, a hurdle that squeezes IT budgets already skewed toward security spending increases. Subscription-based cloud DDI lowers entry points to roughly USD 150 per instance per month, prompting appliance vendors to revisit pricing and financing models. [3]DIGITAL MARKETPLACE, “Cloud Managed DDI and Network Security,” applytosupply.digitalmarketplace.service.gov.uk

DDI Skills Shortage Constrains Roll-Out Velocity

Roughly 69% of Asia-Pacific firms admit insufficient training in SD-WAN and multi-cloud networking, both prerequisites for advanced DDI. Consequently, organizations lean on managed services to handle scripting, policy orchestration, and threat-feed tuning, an arrangement that inflates services demand yet risks longer lead times.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Gain Ground on Complexity

Solutions dominated revenue at 66.43% in 2024, yet the services segment is racing ahead with a 24.56% CAGR. The DNS, DHCP, and IPAM market size attributable to managed offerings is projected to more than triple by 2030, underscoring buyer reliance on third-party expertise for integration, threat-intel tuning, and DevOps enablement. Enterprises cite rapid onboarding-one retailer completed a full migration in 3 weeks-as proof that external teams shorten time-to-value.

Continuous optimization also needs to favor outsourced models. Security feed updates, API version alignment, and compliance reporting occur on a rolling basis, and internal staff shortages make 24×7 coverage untenable. Providers bundle SLAs, periodic audits, and remediation guidance, converting what was historically a capital expense into a predictable operations expenditure-an accounting shift many CFOs prefer.

By Deployment Model: Cloud Installations Accelerate

On-premise systems retained a narrow lead at 53.26% in 2024, but cloud is expanding at 24.89% CAGR. The DNS, DHCP, and IPAM market share for SaaS deployments will overtake appliances before 2028 as enterprises prize global reach, elastic capacity, and auto-patching features native to hosted options. Unified planes also simplify distributed policy administration across AWS, Azure, and Google Cloud by abstracting each provider’s proprietary DNS constructs into common API calls.

Hybrid blueprints dominate transition roadmaps. Critical authoritative zones or regulated workloads stay local, while non-sensitive DHCP and IPAM functions float to SaaS nodes. Early adopters report a 334% ROI based on lower maintenance labor and downtime reduction once patch cycles move from quarterly to continuous.

By Organization Size: SMEs Surge on Subscription Pricing

Large enterprises held 59.43% of 2024 turnover, driven by global WAN footprints that demand multi-site orchestration. Even so, SMEs are set to grow at 24.97% CAGR, fueled by cloud-first IT stacks and pay-as-you-go billing that erase six-figure entry hurdles. The DNS, DHCP, and IPAM market size for firms with under 1,000 employees is forecast to more than double by 2030, a pace not seen in prior refresh cycles.

SaaS DDI packages bundle templates, wizards, and pre-built threat feeds that require minimal training, allowing lean IT teams to stand up authoritative DNS zones in hours rather than weeks. Case studies show mid-market companies slicing ticket resolution time from 15 minutes to 1 minute after migrating to cloud-native consoles.

By End-User Industry: Manufacturing Fastest Riser

Telecom and IT led 2024 revenue at 27.94%, reflecting the sectors’ intrinsic dependency on reliable network naming and addressing. Manufacturing, however, is advancing at 23.67% CAGR as Industry 4.0 drives sensor sprawl, edge analytics, and private 5G. The DNS, DHCP, and IPAM market size tied to factory automation is poised to expand as every robot, conveyor, and quality-inspection camera requires secure, low-latency IP provisioning.

Smart-factory blueprints count on deterministic DNS resolution for dynamic workloads, from machine-learning inference at the line edge to automated guided vehicles roaming across Wi-Fi and cellular. Studies show that manufacturers integrating DDI with plant-floor MES systems experience tangible yield gains owing to faster fault isolation and device-lifecycle tracking.

Geography Analysis

North America posted a 36.82% revenue share in 2024 and retains leadership through deep compliance regimes and early hybrid-cloud adoption. Highly regulated verticals earmark larger budgets for DNS threat shielding and granular IP logging, dovetailing with managed DDI uptake. DevOps culture is also mature, making API-driven provisioning nearly standard practice.

Europe expands under the weight of GDPR and the forthcoming NIS2 directive. Data-sovereignty mandates make dual-deployment strategies popular: authoritative servers remain in-country while SaaS IPAM provides visibility across subsidiaries. Vendors offering EU-hosted control planes and automatic audit exports are well-positioned.

Asia-Pacific is the fastest climber at 23.94% CAGR, propelled by manufacturing digitization in China, Japan, and South Korea, as well as widespread SD-WAN rollouts across service providers. More than 97% of regional enterprises either plan or pilot SD-WAN, each instance requiring centralized DNS policy orchestration. Low-touch SaaS and regional data centers help mitigate skill shortages, ensuring quick onboarding even for SMEs.

Middle East and Africa and South America remain emerging but promising. Government digitization programs, burgeoning fintech ecosystems, and investments in hyperscale data centers bolster baseline demand. Cloud-hosted DDI sidesteps capital outlays and accelerates compliance with nascent regional regulations.

Competitive Landscape

Market concentration is moderate: Infoblox commands roughly 50% global share, yet challenger heat rises as hyperscalers embed native DNS and IPAM APIs. Incumbents answer with ecosystem integrators-over 20 certified connectors into Microsoft, Splunk, and HashiCorp stacks-strengthening platform stickiness.

Acquisition routes expand scope: BlueCat’s 2024 purchase of LiveAction folds performance telemetry into its core offer, marrying visibility with address orchestration. Edge-centric innovators such as Celona push 5G LAN supernetting to satisfy ultra-low-latency requirements inside private cellular setups.

Overall, leadership favors suppliers fusing threat-intel, zero-touch automation, and vendor-agnostic cloud control. Those unable to pivot from appliance licensing to SaaS subscriptions risk ceding ground as recurring revenue already tops 90% of sales for market frontrunners.

DNS, DHCP, And IPAM Industry Leaders

Infoblox Inc.

BlueCat Networks Inc.

EfficientIP SAS

Cygna Labs Corp.

Alcatel-Lucent Enterprise International SAS

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Digi International reported USD 120 million ARR on IoT connectivity, signaling robust managed DDI demand.

- December 2024: Cisco detailed Private 5G integration paths with Umbrella DNS and Identity Services Engine.

- October 2024: BlueCat agreed to acquire LiveAction, enlarging its footprint to performance monitoring.

- September 2024: Infoblox rolled out Universal DDI Suite that unifies core services with automation and threat intelligence.

Global DNS, DHCP, And IPAM Market Report Scope

| Solutions |

| Services |

| On-premise |

| Cloud |

| Hybrid |

| Large Enterprises |

| Small and Medium Enterprises (SMEs) |

| Telecom and IT |

| Banking, Financial Services and Insurance (BFSI) |

| Government and Public Sector |

| Retail and E-commerce |

| Manufacturing |

| Other |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| By Component | Solutions | ||

| Services | |||

| By Deployment Model | On-premise | ||

| Cloud | |||

| Hybrid | |||

| By Organization Size | Large Enterprises | ||

| Small and Medium Enterprises (SMEs) | |||

| By End-User Industry | Telecom and IT | ||

| Banking, Financial Services and Insurance (BFSI) | |||

| Government and Public Sector | |||

| Retail and E-commerce | |||

| Manufacturing | |||

| Other | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

Key Questions Answered in the Report

What is the projected value of the DNS, DHCP, and IPAM market in 2030?

The market is forecast to reach USD 2.01 billion by 2030, expanding at a 23.1% CAGR.

Which component segment shows the fastest growth?

Services are advancing at 24.56% CAGR as organizations outsource implementation and operations.

Why are SMEs adopting DDI platforms rapidly?

Subscription-based cloud offerings remove high upfront costs and simplify deployment, enabling 24.97% CAGR growth among SMEs.

Which region is growing the quickest?

Asia-Pacific is rising at 23.94% CAGR, driven by manufacturing digitization and SD-WAN rollouts.

How do DNS-based cyber-attacks influence DDI spending?

Rising domain-generation exploits push enterprises to integrate security-centric DDI, improving malware detection by 77%.

What is the chief competitive threat to legacy appliance vendors?

Bundled DNS and IPAM services from public-cloud providers are pressuring appliance vendors to pivot toward SaaS and AI-assisted automation.

Page last updated on: