Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

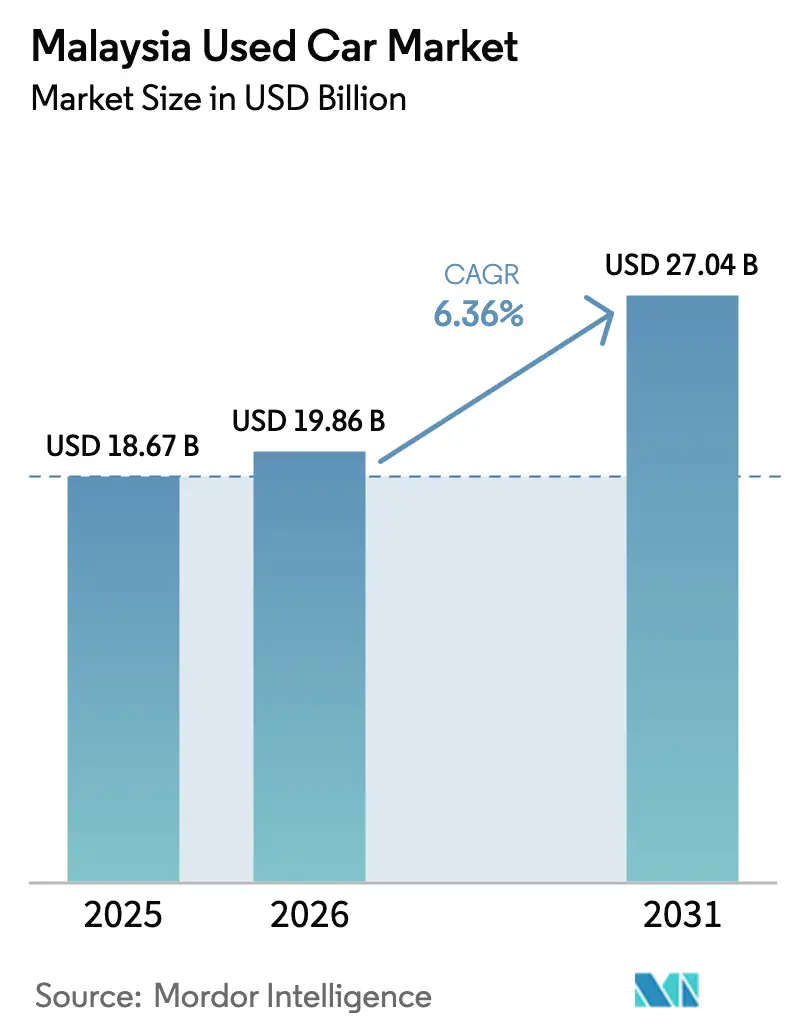

| Base Year Market Size (2025) | USD 18.67 Billion |

| Market Size (2026) | USD 19.86 Billion |

| Market Size (2031) | USD 27.04 Billion |

| Growth Rate (2026 - 2031) | 6.36% CAGR |

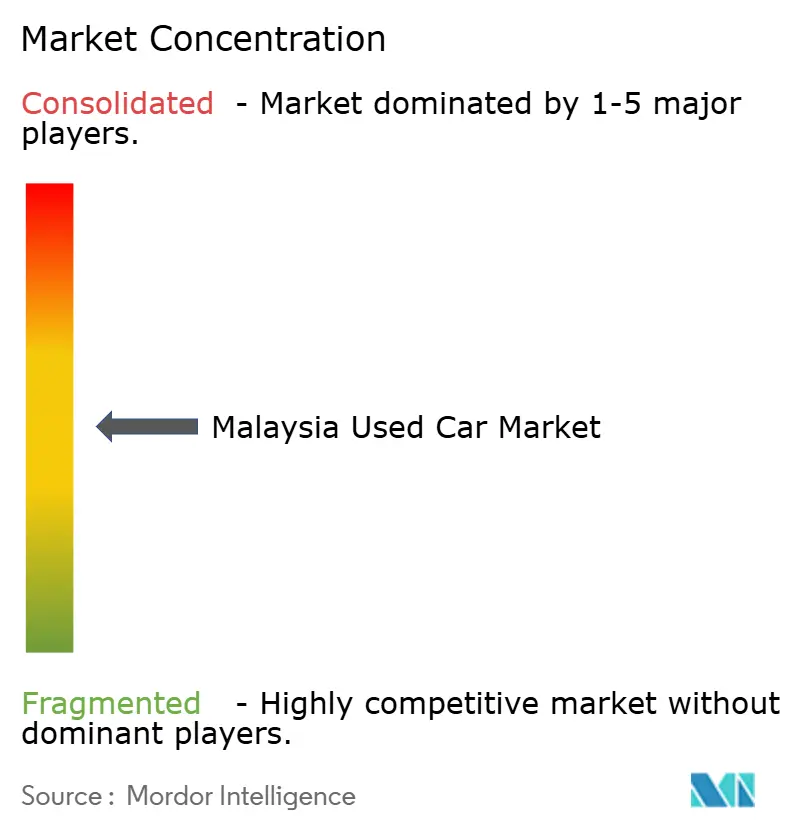

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Malaysia Used Car Market Analysis by Mordor Intelligence

The Malaysia Used Car Market size was valued at USD 18.67 billion in 2025 and estimated to grow from USD 19.86 billion in 2026 to reach USD 27.04 billion by 2031, at a CAGR of 6.36% during the forecast period (2026-2031). Robust household spending, strategic sales-tax exemptions and the National Automotive Policy’s gradual import liberalization underpin demand further enlarged the future supply of pre-owned vehicles. SUV demand is accelerating as buyers look for elevated driving positions suited to mixed traffic and seasonal flooding, while battery-electric models gain traction on the back of expanding charging infrastructure.

Key Report Takeaways

- By vehicle type, sedans led with 37.68% revenue share in 2025, whereas SUVs are poised for a 7.03% CAGR to 2031.

- By vendor type, the unorganised channel held 62.54% of the Malaysia used car market share in 2025, while organised players are advancing at a 6.47% CAGR through 2031.

- By fuel type, petrol vehicles accounted for 75.92% share of the Malaysia used car market size in 2025; battery-electric vehicles represent the fastest growth at 7.15% CAGR.

- By vehicle age, the 3-5 year bracket secured 40.74% share, and the 0-2 year cohort is expanding at 6.7% CAGR.

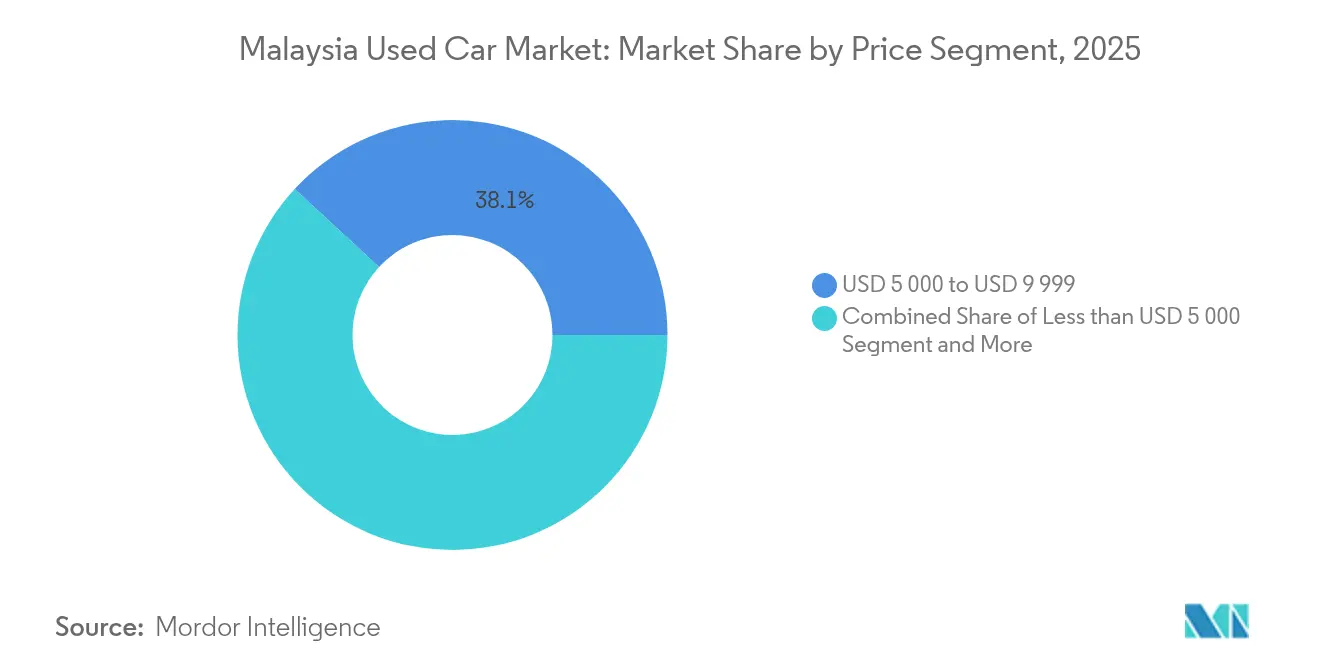

- By price segment, USD 5,000-9,999 cars captured 38.12% share, while the USD 30,000+ tier is set for 6.31% CAGR.

- By sales channel, offline dealerships retained 50.66% share, yet online channels are accelerating at 6.61% CAGR.

- By ownership, multi-owner cars commanded 61.72% share; first-owner resales register a 6.19% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Malaysia Used Car Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating New-Car Prices | +1.8% | National, strongest in middle-income segments | Short term (≤ 2 years) |

| Digital Retail Platform Expansion | +1.5% | National, early gains in Klang Valley, Penang, Johor | Medium term (2-4 years) |

| Diverse Selection Among Models | +1.2% | National, with concentration in urban centers | Medium term (2-4 years) |

| Integrated Financing and Insurance | +0.9% | National, with premium uptake in metropolitan areas | Long term (≥ 4 years) |

| OEM-Backed CPO Programs | +0.6% | National, concentrated in urban dealership networks | Medium term (2-4 years) |

| Telematics-Enabled Transparency | +0.5% | National, early adoption in premium segments | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Escalating New-Car Prices

New-vehicle sticker prices climbed during 2024 and are expected to rise another 8-20% once excise duty reforms are activated in 2026, pushing many middle-income families toward the USD 5,000–9,999 used segment that already commands 38.74% share. Persistent inflation and a weak ringgit inflate import costs, keeping the price gap wide. The differential supports steady inventory turnover for local brands such as Perodua and Proton that provide ample supply and affordable parts.

Digital Retail Platform Expansion

CARSOME processes more than 100,000 vehicles a year through its AI-driven 175-point inspection regime, delivering roughly USD 1 billion in revenue and setting new quality benchmarks.[1]“AI-Driven Inspection Standards,” CARSOME, carsome.my Partnerships with Google Cloud allow real-time pricing and customer-experience optimization, while traditional lots now add virtual showrooms to defend market share. The online channel’s 6.73% CAGR shows that Malaysian shoppers increasingly begin their journey with a mobile search even though many still insist on a last-mile physical inspection.

Diverse Selection Among Models

Malaysia’s 9 million-unit passenger-car parc supplies a deep bench of models across every budget, supported by 658 licensed dealers nationwide. Popular Perodua and Proton variants account for approximately 60% of new sales, assuring robust residual values in the secondary market. EV choice is widening as the locally branded Proton e.MAS 7 logged 2,716 registrations in its first four months of deliveries, starting in January 2025.

Integrated Financing & Insurance

Maybank extends up to 90% financing for used vehicles with tenors of nine years, while fixed Islamic products such as Murabahah Vehicle Term Financing-i cater to Shariah-compliant buyers at competitive 3% rates.[2]“Automobile Financing Programme,” Maybank, maybank.com EV packages offer interest rates as low as 1.75% plus charging credits, smoothing ownership costs and supporting the organised vendors’ 6.56% expansion as professional dealers integrate financing into the checkout funnel.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Counterfeit/Illegally Imported Vehicles | -0.8% | National, concentrated in border regions | Short term (≤ 2 years) |

| EV Residual-Value Uncertainty | -0.7% | National, strongest impact in premium EV segments | Medium term (2-4 years) |

| Fragmented Inspection Standards | -0.6% | National, varying by state implementation | Medium term (2-4 years) |

| Limited Aftermarket Warranty | -0.4% | National, particularly affecting unorganised vendors | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Counterfeit / Illegally Imported Vehicles

The end of the Open Approved Permit model and fresh Vehicle Entry Permit fines of RM300 for Singapore-registered cars entering Malaysia underscore tighter border controls. The crackdown lifts compliance costs in the short run but ultimately shields legitimate dealers, encouraging customers to gravitate toward organised lots with verifiable documentation.

Fragmented Inspection Standards

SIRIM QAS’s 4R2S certification is harmonising repair, reuse, recycle and remanufacture practices nationwide, nudging smaller operators to adopt structured quality checks.[3]“4R2S Certification Scheme,” SIRIM QAS International, sirim-qas.com.my Platforms offering warranties and standardised 175-point diagnostics already benefit from differentiated trust, signalling a medium-term industry shift toward clear inspection benchmarks.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Vehicle Type: SUVs Drive Premium Shift

Sedans maintained the largest 37.68% slice of the Malaysia used car market in 2025, though SUVs are forecast to post a 7.03% CAGR, outpacing every other body style. The SUV uptrend stems from elevated driving positions, better flood clearance and fresh supply from Proton X70 lease returns. CARSOME reports that SUV transactions command higher average selling prices, boosting per-unit profitability even while unit volumes are still catching sedans.

The Malaysia used car market size for SUVs is projected to grow exponentially by 2031, while hatchbacks retain strong entry-level resonance because of low running costs. Multi-Purpose Vehicles continue serving large families and ride-hailing operators that value flexible seating. Dealers stocking diversified SUV trims position themselves ahead of the demand curve as infrastructure projects lengthen urban commutes.

By Vendor Type: Organised Players Gain Ground

Unorganised yards still control 62.54% of the Malaysia used car market share, but organised operators are growing faster at 6.47% CAGR due to warranty coverage and digital service layers. Consumers are willing to pay modest premiums for certified inspections that reduce risk and provide after-sales peace of mind.

The Malaysia used car market size attributable to organised vendors as CARSOME expands to increase its inspection centres and Carro introduces instant online valuations. Sime Darby’s purchase of UMW Holdings integrates Toyota and Perodua pre-owned programs under a single banner, signalling deeper consolidation ahead.

By Fuel Type: Electric Transition Accelerates

Petrol cars commanded 75.92% of 2025 transactions, yet battery-electric units are charting the fastest 7.15% trajectory on incentives and charging rollouts. Diesel remains the province of logistics fleets, whereas hybrids deliver a transitional option for drivers worried about range.

Malaysia used car market size for xEVs is projected to triple between 2026 and 2031 as charging points climb to 10,000 and tax holidays stay intact through 2025. Dealers are beginning to train technicians in high-voltage servicing to capture the residual-value opportunity once the first wave of mass-market EVs enters secondary circulation.

By Vehicle Age: Premium Fresh Inventory Emerges

Cars aged 3-5 years controlled 40.74% of 2025 turnover, the sweet spot where modern safety tech meets attractive price drops. Nearly-new 0-2 year vehicles, buoyed by early lease returns, form the quickest-growing slice at 6.7% CAGR, signalling a tightening ownership cycle as buyers trade sooner.

Should policymakers introduce a 10-year age cap-a proposal supported by surveyed motorists-older inventory would exit faster, accelerating demand for younger stock. Dealers focused on cars under five years old record faster inventory turns and stronger lender support.

By Price Segment: Value Tier Dominates Transactions

The USD 5,000-9,999 bracket held 38.12% of spending in 2025, mirroring Malaysia’s middle-income demographics. Luxury tastes, however, are climbing: the USD 30,000+ band is set to advance 6.31% CAGR as higher wages and attractive financing broaden premium affordability.

Malaysia used car market size for premium tiers is forecasted to grow exponentially by 2031, led by European marques whose residual values benefit from certified pre-owned warranties. Banks offering up to 90% financing facilitate upward migration across price tiers.

By Sales Channel: Digital Integration Reshapes Retail

Offline showrooms still secure 50.66% of 2025 deals, but online pathways are expanding at 6.61% CAGR as buyers combine smartphone research with doorstep delivery. Classified portals funnel traffic to both independent dealers and OEM-run certified stores, blurring the line between digital and physical touchpoints.

The Malaysia used car industry continues to witness hybrid models: CARSOME’s e-commerce storefront synchronises with physical inspection hubs, while Sime Motors’ EV NEXT specialises in second-hand electric vehicles sold predominantly online. Auction houses digitise bidding to widen participation beyond metropolitan lots.

By Ownership: Multi-Owner Vehicles Drive Volume

Multi-owner cars represented 61.72% of 2025 handovers as depreciation curves make later ownership stints more affordable. Single-owner units are widening at 6.19% CAGR since more fleet lessees and professionals rotate vehicles within three years.

Transparent digital histories build buyer trust in single-owner listings, enabling higher price realisations. Organised dealers capture the premium by guaranteeing mileage authenticity and bundling after-sales coverage.

Geography Analysis

The Klang Valley, comprising Kuala Lumpur and Selangor, anchors roughly half of national pre-owned transactions, benefiting from dense population, higher incomes and robust digital platform penetration. Southern Johor enjoys spill-over demand from the Johor-Singapore Special Economic Zone, where cross-border commuters target Malaysian registrations to avoid Singapore’s higher fees. Penang’s industrial base supports steady mid-tier demand, while Sabah and Sarawak favour pickups and SUVs tailored to rural terrain.

CARSOME and Carro extend inspection centres in Penang, Johor Bahru and Melaka to match regional opportunities. Dealers noting eastern Malaysia’s appetite for utility vehicles adjust inventory accordingly, transporting units via coastal shipping to contain logistics costs.

Highway upgrades such as the Pan Borneo network reduce travel time, stimulating vehicle turnover as remote districts gain easier access to urban dealerships. The government’s 10,000-station charging goal concentrates initial EV infrastructure in key corridors, guiding early secondary-market EV demand toward urban hubs.

Competitive Landscape

Market concentration is moderate, Sime Darby’s USD 0.84 billion purchase of UMW Holdings fused Toyota and Perodua pre-owned programs under a single roof, solidifying a multibrand champion.[4]“Completion of UMW Holdings Acquisition,” Sime Darby Berhad, simedarby.com Digital disruptor CARSOME commands a USD 1.3 billion valuation and processes more than 100,000 cars yearly, leveraging AI pricing and 175-point inspections to build consumer trust. Unorganised lots remain fragmented yet dominant in volume, but face rising compliance and financing barriers favoring tech-enabled, capital-rich competitors.

Strategic focus converges on data analytics, warranty bundles, and regional expansion. Sime Motors launched EV NEXT, Malaysia’s first dedicated used EV dealership, while Carro rebranded from MyTukar and rolled out instant online valuations to shorten the sell-to-cash cycle. The December 2024 MIDA-DRB-HICOM-Geely memorandum signals future Chinese capital inflows that could reshape supply chains and certified pre-owned networks.

Players investing in predictive pricing, battery health assessment, and omnichannel experiences are best placed to defend margins as the Malaysian used car market becomes more transparent and price-efficient.

Malaysia Used Car Industry Leaders

Mudah.my Sdn Bhd

CARSOME Sdn Bhd

myTukar Sdn Bhd

Sime Darby Auto Selection

UMW Toyota Motor

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: PROTON partnered with Continental Malaysia to introduce tyre replacement at 60 outlets, bundled with a one-year road-hazard warranty.

- April 2025: CARSOME entered a multi-year Google Cloud collaboration to scale AI-driven pricing and customer-service automation.

- December 2024: Proton launched the e.MAS 7 electric vehicle, one of Malaysia’s first locally badged EVs.

Malaysia Used Car Market Report Scope

used car, a pre-owned vehicle, or a second-hand car is a vehicle that has previously had one or more retail owners. Used cars are sold through various outlets, including franchises and independent car dealers, rental car companies, buy-here-pay-here dealerships, leasing offices, auctions, and private-party sales.

The Malaysian used car market is segmented by vendor type, fuel type, body type, and sales channel. By vendor type, the market is segmented into organized and unorganized. By fuel type, the market is segmented into petrol, diesel, and other fuel types. By body type, the market is segmented into hatchbacks, sedans, and sports utility vehicles (SUVs) and multi-purpose vehicles (MPVs). By sales channel, the market is segmented into online and offline. For each segment, market sizing and forecast are performed on the basis of value (USD).

By Vehicle Type

| Hatchbacks |

| Sedans |

| Sport-Utility Vehicles (SUVs) |

| Multi-Purpose Vehicles (MPVs) |

| Others (convertibles, coupes, crossovers, sports cars) |

By Vendor Type

| Organised |

| Unorganised |

By Fuel Type

| Petrol |

| Diesel |

| Hybrid (HEV & PHEV) |

| Battery-Electric (BEV) |

| LPG / CNG / Others |

By Vehicle Age

| 0 – 2 Years |

| 3 – 5 Years |

| 6 – 8 Years |

| 9 – 12 Years |

| More than 12 Years |

By Price Segment

| Less than USD 5 000 |

| USD 5 000 – USD 9 999 |

| USD 10 000 – USD 14 999 |

| USD 15 000 – USD 19 999 |

| USD 20 000 – USD 29 999 |

| More than or equal to USD 30 000 |

By Sales Channel

| Online | Digital Classified Portals |

| Pure-play e-Retailers | |

| OEM-Certified Online Stores | |

| Offline | OEM-Franchised Dealers |

| Multi-brand Independent Dealers | |

| Physical Auction Houses |

By Ownership

| First-owner Resale |

| Multi-owner |

| By Vehicle Type | Hatchbacks | |

| Sedans | ||

| Sport-Utility Vehicles (SUVs) | ||

| Multi-Purpose Vehicles (MPVs) | ||

| Others (convertibles, coupes, crossovers, sports cars) | ||

| By Vendor Type | Organised | |

| Unorganised | ||

| By Fuel Type | Petrol | |

| Diesel | ||

| Hybrid (HEV & PHEV) | ||

| Battery-Electric (BEV) | ||

| LPG / CNG / Others | ||

| By Vehicle Age | 0 – 2 Years | |

| 3 – 5 Years | ||

| 6 – 8 Years | ||

| 9 – 12 Years | ||

| More than 12 Years | ||

| By Price Segment | Less than USD 5 000 | |

| USD 5 000 – USD 9 999 | ||

| USD 10 000 – USD 14 999 | ||

| USD 15 000 – USD 19 999 | ||

| USD 20 000 – USD 29 999 | ||

| More than or equal to USD 30 000 | ||

| By Sales Channel | Online | Digital Classified Portals |

| Pure-play e-Retailers | ||

| OEM-Certified Online Stores | ||

| Offline | OEM-Franchised Dealers | |

| Multi-brand Independent Dealers | ||

| Physical Auction Houses | ||

| By Ownership | First-owner Resale | |

| Multi-owner | ||

Key Questions Answered in the Report

What is the current size of the Malaysia used car market in 2026?

The Malaysia used car market reached USD 19.86 billion in 2026 and is projected to exceed USD 27.04 billion by 2031.

Which vehicle type is growing the fastest in the Malaysia used car market?

SUVs are the fastest-expanding segment with a forecast 7.03% CAGR through 2031, driven by demand for higher driving positions and better flood resilience.

How rapidly are online sales channels growing?

Online channels are expanding at a 6.61% CAGR, outpacing offline outlets as buyers embrace digital inspections, financing and doorstep delivery services.

What share do organised dealers hold versus unorganised vendors?

Unorganised vendors still control 62.54% of transactions, but organised dealers are gaining ground quickly due to warranties, financing partnerships and digital platforms.

How significant is the electric vehicle segment in the Malaysia used car industry?

Battery-electric cars currently account for a small base but are charting a 7.15% CAGR, supported by government incentives and a target of 10,000 public charging points by 2025.

Will potential excise-duty reforms affect used car demand?

Yes. Planned excise changes could lift new-car prices by up to 20%, likely pushing more consumers toward pre-owned options and sustaining used-market growth in the near term.

Page last updated on: