Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

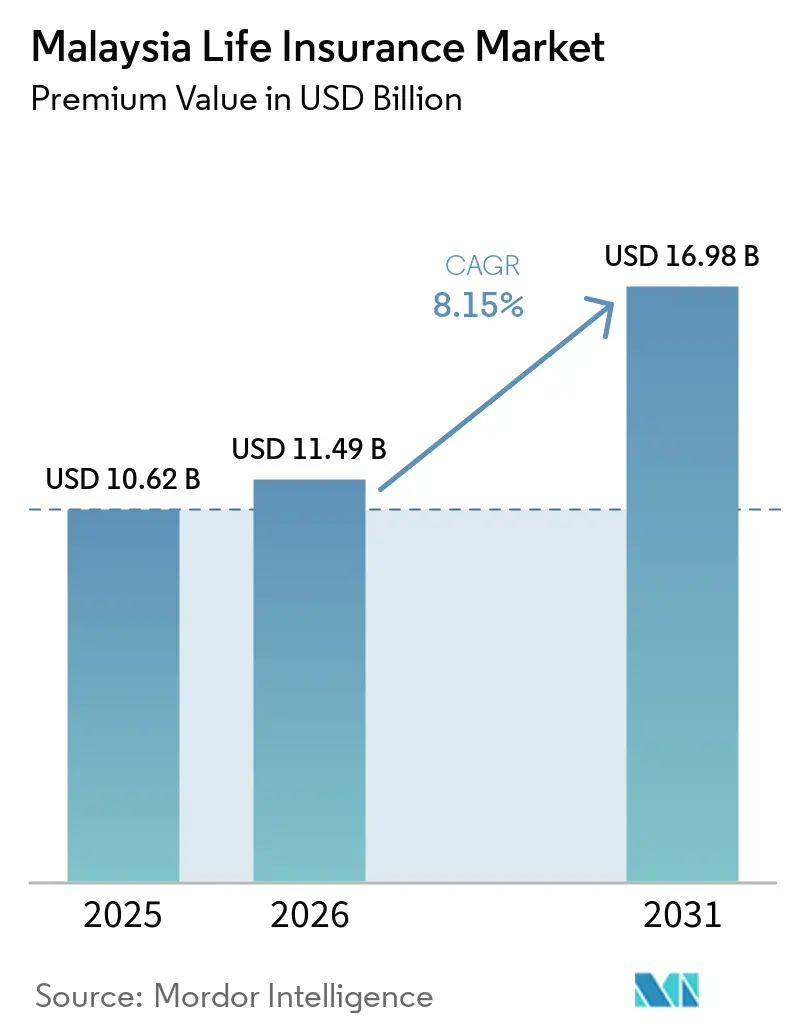

| Base Year Market Size (2025) | USD 10.62 Billion |

| Market Size (2026) | USD 11.49 Billion |

| Market Size (2031) | USD 16.98 Billion |

| Growth Rate (2026 - 2031) | 8.15% CAGR |

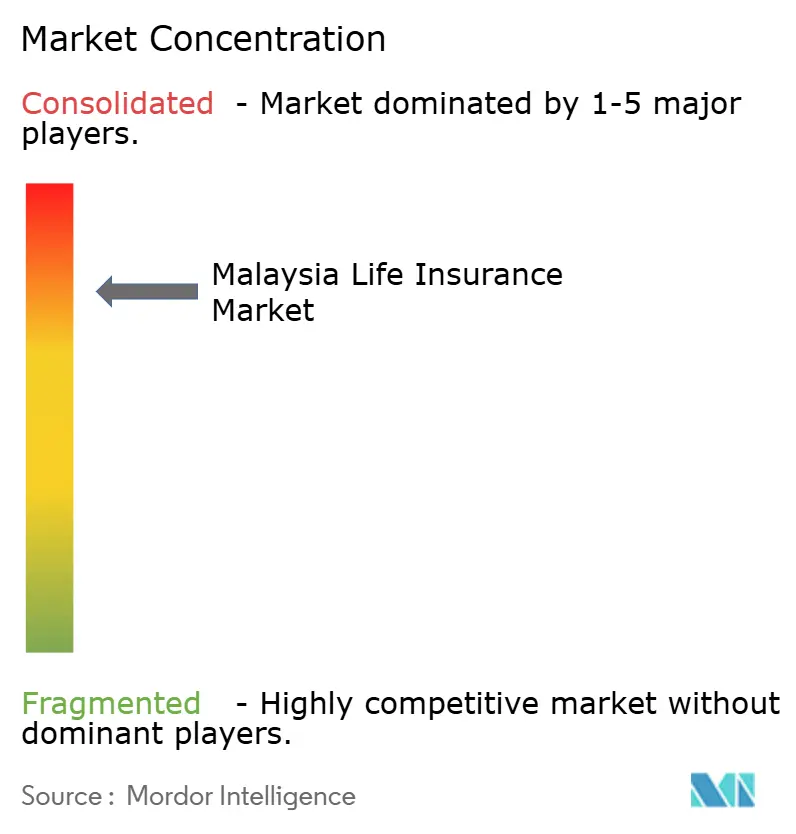

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Malaysia Life Insurance Market Analysis by Mordor Intelligence

The Malaysia Life Insurance Market size in terms of premium value was valued at USD 10.62 billion in 2025 and is estimated to grow from USD 11.49 billion in 2026 to reach USD 16.98 billion by 2031, at a CAGR of 8.15% during the forecast period (2026-2031).

The Malaysia life insurance market benefits from Bank Negara Malaysia’s (BNM) RBC-2 capital regime and digital-sandbox policies, which strengthen solvency while lowering barriers for tech-led entrants[1]Bank Negara Malaysia, “Annual Report 2024,” bnm.gov.my. An aging society, citizens 65 years and older already form 8.1% of the population, feeds sustained demand for retirement-linked cover, while a 68.9% working-age cohort drives volume in protection and investment-linked offerings[2]Ministry of Health Malaysia, “Malaysia Health Statistics 2024,” moh.gov.my. Premium growth is also buoyed by generous tax incentives that now allow up to RM4,000 relief on medical and education policies, plus continued deductions for Private Retirement Scheme (PRS) contributions. Intense competition spurs consolidation: Great Eastern’s RM1.121 billion purchase of AmMetLife channels illustrates how established players hunt scale advantages in the Malaysia life insurance market

Key Report Takeaways

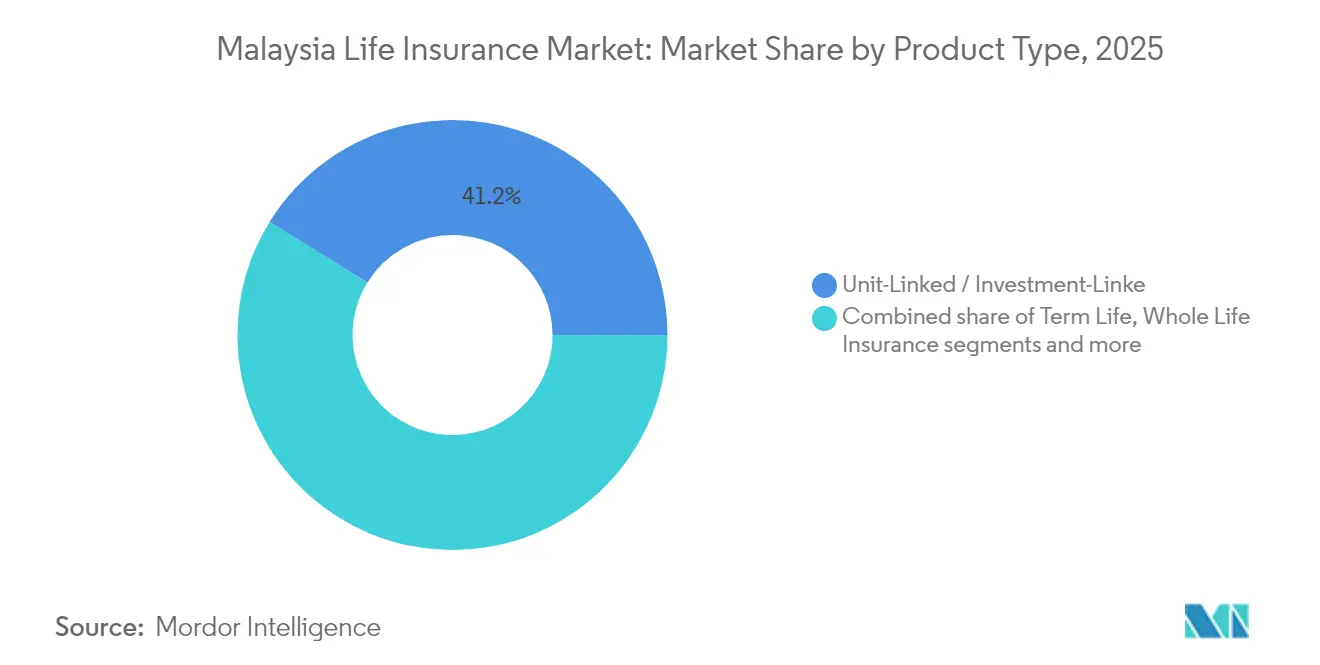

- By product type, unit-linked and investment-linked policies captured 41.20% of the Malaysia life insurance market share in 2025

- By product type, annuity insurance is projected to expand at a 9.52% CAGR through 2031

- By distribution channel, agents commanded a 50.85% share of the Malaysia life insurance market size in 2025

- By distribution channel, online marketplaces record the highest projected CAGR at 10.29% to 2031.

- By premium type, regular-premium business accounted for 68.10% of the Malaysia life insurance market size in 2025.

- By customer age group, the 45-64 cohort is advancing at a 9.22% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Malaysia Life Insurance Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising middle-class disposable income & insurance penetration | +1.5% | Klang Valley, Johor, Penang | Medium term (2-4 years) |

| Tax incentives on life-insurance premiums | +1.2% | Urban centers nationwide | Short term (≤ 2 years) |

| Growth of Shariah-compliant takaful life products | +0.8% | Rural and conservative regions | Long term (≥ 4 years) |

| EPF withdrawals into approved annuity products | +1.1% | Pre-retirees nationwide | Medium term (2-4 years) |

| Digital channels after BNM sandbox expansion | +0.9% | Urban then tier-2 cities | Short term (≤ 2 years) |

| Biometric underwriting cuts issue time | +0.7% | Led by tier-1 insurers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Middle-Class Disposable Income & Insurance Penetration

Malaysia’s middle class is expanding alongside a 2.1% annual population growth rate and a life expectancy of 74.0 years, generating a larger addressable base for the Malaysia life insurance market. The Employees Provident Fund (EPF) delivered a 6.30% dividend for 2024, reinforcing consumer confidence to allocate more income toward protection and savings policies. Penetration remains modest at roughly 5% of GDP, leaving sizeable headroom as incomes climb. Urban clusters such as Klang Valley post above-average wages, accelerating uptake of investment-linked covers that blend protection and wealth creation. Compared with mature markets facing shrinking workforces, Malaysia’s demographic profile underpins medium-term premium expansion in the Malaysia life insurance market.

Tax Incentives on Life-Insurance Premiums

Budget 2025 raised tax relief ceilings on medical and education policies from RM3,000 to RM4,000, directly lowering the effective cost of ownership[3]Ministry of Finance, “Budget 2025 Speech,” malaysiabudget.gov.my. Extended PRS incentives until 2030 reinforce demand for retirement-focused solutions such as annuities. These measures coincide with BNM’s consumer-protection guidance, boosting trust and encouraging innovation. International evidence shows similar fiscal levers can produce two-to-three-fold jumps in new-business premiums when households rush to optimize tax savings. The alignment of tax and regulatory policy, therefore, magnifies growth momentum for the Malaysia life insurance market.

Growth of Shariah-Compliant Takaful Life Products

BNM’s January 2024 policy on hajah and darurah clarified Shariah standards, reducing compliance uncertainty for takaful operators. Malaysia’s stature as an Islamic finance hub provides in-house expertise that accelerates product design for investment-linked takaful plans, now moving beyond simple term coverage. Family takaful premiums at Maybank jumped 74.6% year-over-year, signalling mainstream acceptance[4]Maybank Investor Relations, “2024 Full-Year Results,” maybank.com. Rural regions with higher Muslim populations prefer Shariah-compliant solutions, expanding geographic reach. Cross-border spillover into Muslim-majority neighbors may also lift exportable capabilities, broadening addressable volumes for the Malaysia life insurance market.

EPF Withdrawals into Approved Annuity Products

The EPF framework lets members channel lump-sum balances into approved annuity plans, transforming one-time withdrawals into guaranteed retirement income. A growing 65+ cohort, already 8.1% of citizens, faces longevity risk that annuities uniquely hedge. Female life expectancy at 76.6 years versus 71.8 years for males underscores the need for gender-sensitive pricing. The quasi-mandatory nature of EPF-linked annuities trims distribution costs, giving insurers efficient entry into the pre-retiree segment. As a result, annuities are set to be the fastest-growing line in the Malaysia life insurance market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Low financial literacy & product complexity | -0.6% | Rural segments nationwide | Long term (≥ 4 years) |

| Prolonged low-interest-rate environment | -0.4% | All insurers nationwide | Medium term (2-4 years) |

| Capital requirement hikes under RBC-2 | -0.5% | Smaller insurers nationwide | Short term (≤ 2 years) |

| Competition from Private Retirement Schemes | -0.3% | Urban professional segments | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Low Financial Literacy & Product Complexity

The National Strategy for Financial Literacy flagged persistent gaps in understanding investment-linked and annuity mechanics, a hurdle that lowers uptake for advanced solutions. PIDM behavioral studies show many buyers focus on headline premiums rather than long-term value, leading to underinsurance and policy lapses. Complexity triggers decision paralysis, particularly in rural populations with limited adviser access despite rising digital reach. Sustained, multi-year education is needed before literacy gains materially expand the Malaysia life insurance market.

Prolonged Low-Interest-Rate Environment

Subdued yields squeeze spreads on legacy guaranteed policies, forcing insurers to bolster capital or reprice products. Savings-oriented covers become less attractive than market-linked alternatives when returns lag, pressuring overall premium growth. Smaller firms lacking diversified asset strategies face higher solvency risk. While investment-linked business is insulated from guarantee strains, weak fund performance can still erode customer appetite. Persistently low rates, therefore, shave 0.4 percentage points from the overall CAGR for the Malaysia life insurance market..

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Unit-Linked Leads as Annuities Accelerate

In 2025, unit-linked and investment-linked covers commanded a 41.20% share of Malaysia's life insurance market, underscoring a strong consumer preference for these flexible protection and investment solutions. These products offer policyholders the ability to combine insurance coverage with investment opportunities, making them particularly attractive in a market where financial planning and wealth accumulation are gaining importance. Meanwhile, annuities surged ahead with a robust 9.52% CAGR, driven by channels like EPF withdrawals and growing concerns over longevity risks. The increasing life expectancy of Malaysia's population has further amplified the demand for annuities, as individuals seek financial security during retirement.

The appeal of unit-linked products, with their transparency and fund-switching options, resonates particularly with younger urban buyers who value flexibility and control over their investments. While conservative savers continue to favor whole-life policies for their guarantees in a low-rate environment, the tightening spreads are squeezing profitability for insurers. Whole-life policies remain a staple for risk-averse consumers, but insurers are facing challenges in maintaining margins due to the prevailing economic conditions. As buyers pivot towards higher-yield options, endowments are witnessing a decline in popularity, with many consumers opting for products that offer better returns and align with their financial goals. Health-linked riders are grappling with rising costs, highlighted by Great Eastern's average claims soaring to RM8,760, leading to a market-wide repricing in Malaysia's life insurance sector. The increasing healthcare costs and inflationary pressures are compelling insurers to reassess their pricing strategies to ensure sustainability while meeting policyholder needs.

By Distribution Channel: Agents Stay Central While Online Soars

In 2025, agents maintained a dominant 50.85% share of Malaysia's life insurance market, highlighting the significance of relational selling in navigating complex products. This dominance reflects the trust and personalized service that agents provide, which remains critical in a market where consumers often seek guidance for intricate insurance decisions. Meanwhile, online marketplaces are on a growth trajectory, boasting a 10.29% CAGR, resonating with the self-directed research tendencies of today's digital-native consumers. These platforms cater to the growing demand for convenience and transparency, enabling customers to compare policies and make informed decisions independently.

In the first half of 2024, bancassurance partnerships, notably the AIA–Public Bank alliance, propelled VONB by 18%, underscoring the influential role of banking channels. Such alliances leverage the extensive customer base and trust associated with banks, making them a powerful distribution channel for life insurance products. Specialized brokers are now addressing niche corporate needs and high-sum-assured cases, offering tailored solutions that cater to specific client requirements. The landscape is evolving: hybrid models are emerging, with agents increasingly equipped with digital tools to enhance efficiency and customer engagement. For instance, 90% of Prudential’s Malaysian agents now use PRUForce for e-submission, streamlining processes and improving service delivery. Multichannel engagement strategies are expected to play a pivotal role in shaping customer acquisition approaches across the Malaysia life insurance market, ensuring that insurers can meet diverse consumer preferences effectively.

By Premium Type: Regular Flows Dominate as Single Lump Sums Rise

In 2025, regular premiums accounted for 68.10% of Malaysia's life insurance market, aligning with the monthly income cycles of salaried workers. This dominance highlights the preference for consistent, recurring payment structures among policyholders. Meanwhile, the smaller single-premium segment is on a rapid ascent, growing at a rate of 10.11%. This surge is driven by retirees tapping into their EPF lump sums and affluent savers opting for immediate coverage, reflecting a shift in consumer behavior toward one-time, high-value investments in life insurance products.

Digital platforms are streamlining the process for single-premium issuances, leading to an uptick in larger-ticket transactions conducted online. These platforms reduce administrative friction, making it easier for consumers to purchase policies and for insurers to process them efficiently. Maybank’s Etiqa demonstrated balanced growth, with regular-premium new business increasing by 17.3%, while single-premium sales benefited from a 38.4% surge in NAP. This dual growth underscores the adaptability of insurers in catering to diverse customer needs. The coexistence of stable recurring flows from regular premiums and high-value one-time deposits from single premiums supports diversified cash-flow resilience for Malaysia's life insurance market. This balance ensures that the market remains robust, catering to both long-term policyholders and those seeking immediate financial protection.

By Customer Age Group: Working-Age Core Tilts Toward Pre-Retirement

In 2025, the 25-44 age group accounted for 45.60% of total premiums, solidifying its role as the backbone of Malaysia's life insurance market. However, the 45-64 age bracket is on a rapid ascent, projected to grow at a 9.22% CAGR through 2031, driven by peak wealth accumulation and heightened retirement planning. This growth reflects a shift in consumer priorities, as individuals in this age group increasingly focus on securing financial stability for their retirement years. The rising disposable income and awareness about financial planning in this demographic are further fueling the demand for life insurance products.

Younger individuals often depend on insurance covers bought by their parents or through employer group plans. These segments typically prioritize affordability and basic coverage, which are often provided through group policies. However, as this demographic matures, there is potential for increased adoption of individual policies tailored to their evolving needs. As the population ages, there's a rising demand for immediate annuities and long-term care riders, catering to the needs of retirees seeking financial security and healthcare support. Additionally, with women generally outliving men, there's a pressing need for pricing adjustments, particularly for retirement income products tailored to female policyholders. Gender-specific longevity gaps are prompting insurers to develop actuarially sound pricing models to address these disparities effectively. By 2030, pre-retirees are expected to significantly influence the product mix within the Malaysia life insurance market, driving innovation and diversification in offerings to meet evolving consumer demands.

Geography Analysis

Klang Valley, Johor, and Penang dominate premium pools owing to higher incomes and concentrated financial infrastructure, creating a natural stronghold for complex investment-linked solutions in the Malaysia life insurance market. These regions benefit from a well-established network of financial institutions and a higher penetration of financial literacy, which supports the adoption of sophisticated insurance products. Rural districts, on the other hand, lean toward basic term products due to lower literacy levels and a scarcity of advisers. However, the expansion of 4G coverage is gradually improving digital outreach, enabling insurers to tap into these underserved areas more effectively.

East Malaysia, including Sabah and Sarawak, presents fresh growth opportunities driven by improving connectivity and employment growth in commodity-based industries. Despite these prospects, insurers face challenges such as high distribution and compliance costs, which hinder market penetration. In Kelantan and Terengganu, the preference for Islamic finance has spurred the adoption of takaful products, providing an advantage to operators with expertise in Shariah-compliant solutions. This trend underscores the importance of tailoring offerings to align with regional preferences and cultural nuances.

Urban centers, characterized by older demographics, are witnessing increased demand for annuity and healthcare riders, reflecting the aging population's need for retirement and medical security. Conversely, younger populations in emerging economic corridors prioritize income-replacement protection, highlighting the diverse needs across different age groups. Additionally, cross-border commuters traveling to Singapore seek portable coverage options, prompting insurers to adapt their products to include overseas medical networks and other cross-border benefits. To sustain balanced growth in the Malaysia life insurance market, insurers must strategically calibrate their propositions to address the unique demands and challenges of each region.

Competitive Landscape

Multinational subsidiaries and major domestic groups predominantly shape the Malaysia life insurance market, which showcases a moderate concentration. The recent RM1.121 billion acquisition of AmMetLife by Great Eastern not only amplifies its scale but also broadens its distribution reach, highlighting a trend of active consolidation. AIA Malaysia's consistent eight-year reign at the top of the MDRT agent rankings emphasizes the advantage of a high-caliber advisory force. This dominance reflects the growing importance of skilled advisory networks in driving customer acquisition and retention in a competitive market.

Technological prowess sets incumbents apart: Prudential's PRUForce achieved a 49% boost in lead conversion, while AIA's digital enhancements propelled Premier Agency's VONB by 7%. These advancements underline the critical role of technology in improving operational efficiency and enhancing customer experiences. Meanwhile, smaller insurers grapple with the stringent RBC-2 capital requirements, positioning them as potential acquisition targets. The inability to meet these regulatory demands could lead to further consolidation, reshaping the competitive landscape.

Untapped avenues like rural micro-insurance and SME employee benefits present lucrative prospects, especially with the success of digital, cost-effective models. These segments remain underpenetrated, offering significant growth potential for insurers willing to innovate and adapt. While BNM's DITO framework opens doors for new tech players in the Malaysia life insurance market, it also enforces stringent solvency requirements, striking a balance between fostering innovation and safeguarding consumer interests. This framework is expected to encourage healthy competition while ensuring market stability, ultimately benefiting policyholders and driving long-term growth in the sector.

Malaysia Life Insurance Industry Leaders

Great Eastern Life Assurance (Malaysia) Berhad

AIA Bhd.

Prudential Assurance Malaysia Berhad

Etiqa Life Insurance Berhad

Allianz Life Insurance Malaysia Berhad

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Generali Malaysia rolled out BNM-approved repricing options for SmartCare Optimum, including higher deductibles and reinstatement offers to cushion medical inflation.

- November 2024: Great Eastern General Malaysia provided interim medical repricing relief with dedicated hotlines and surrender reinstatement pathways.

- August 2024: AIA Group reported USD 183 million VONB in Malaysia, up 14% year over year, with a 64.2% margin driven by protection sales.

- August 2024: Prudential plc recognized a 49% non-controlling interest in its Malaysia conventional unit after a Federal Court ruling, clarifying dividend flows and group embedded-value allocation.

Malaysia Life Insurance Market Report Scope

Life and annuity insurance refers to a financial product that features a predetermined periodic payout amount until the death of the annuity owner or annuitant.

Life and annuity insurance is one of the most widely demanded products as people adopt digitalization. The Malaysian life and annuity insurance market is segmented by product type (conventional, investment-linked, and annuities), by user type (individual and group), and by distribution channel (direct, brokers, banks, online, and other distribution channels). The report offers market size and forecasts for the Malaysia Life and Annuity Insurance Market in terms of volume (number of products) and value (USD million) for all the above segments.

By Product Type (Value)

| Term Life Insurance |

| Whole Life Insurance |

| Endowment Insurance |

| Unit-Linked / Investment-Linked |

| Annuity Insurance |

| Other Types |

By Distribution Channel (Value)

| Agents |

| Brokers |

| Banks |

| Direct to Consumer |

| Online Marketplaces |

By Premium Type (Value)

| Regular Premium |

| Single Premium |

By Customer Age Group (Value)

| 0–24 Years |

| 25–44 Years |

| 45–64 Years |

| 65 Years & Above |

| By Product Type (Value) | Term Life Insurance |

| Whole Life Insurance | |

| Endowment Insurance | |

| Unit-Linked / Investment-Linked | |

| Annuity Insurance | |

| Other Types | |

| By Distribution Channel (Value) | Agents |

| Brokers | |

| Banks | |

| Direct to Consumer | |

| Online Marketplaces | |

| By Premium Type (Value) | Regular Premium |

| Single Premium | |

| By Customer Age Group (Value) | 0–24 Years |

| 25–44 Years | |

| 45–64 Years | |

| 65 Years & Above |

Key Questions Answered in the Report

What is the projected premium value for Malaysia life insurance by 2031?

The Malaysia life insurance market is forecast to reach USD 16.98 billion by 2031.

How fast will premiums grow over the forecast period?

Aggregate premiums are expected to rise at an 8.15% CAGR between 2026 and 2031.

Which product category is expanding the quickest?

Annuity policies lead growth, posting a 9.52% forecast CAGR through 2031.

Are digital channels overtaking agents in new policy sales?

Agents still command 50.85% of premiums, yet online marketplaces record a 10.29% growth pace, the fastest among all channels.

What regulatory shift most benefits digital insurers?

Bank Negara Malaysia’s Digital Insurers and Takaful Operators (DITO) framework provides a structured pathway for full-stack digital entrants.

How concentrated is insurer market power?

The top five providers control a little over half of total premiums, reflecting moderate concentration.

Page last updated on: