Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Historical Data Period | 2020 - 2024 |

| Market Size (2026) | USD 0.91 Trillion |

| Market Size (2031) | USD 1.42 Trillion |

| Growth Rate (2026 - 2031) | 9.30% CAGR |

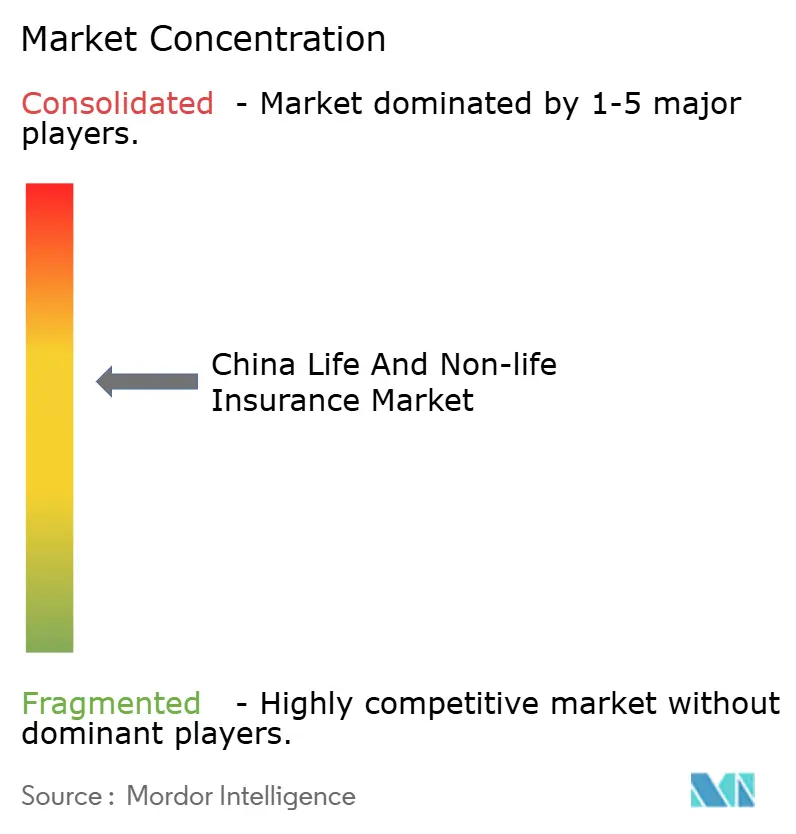

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

China Life And Non-life Insurance Market Analysis by Mordor Intelligence

The China life and non-life insurance market reached USD 0.91 trillion in 2026 and is projected to expand to USD 1.42 trillion by 2031, reflecting a 9.3% CAGR, indicating the China life and non-life insurance market size will continue to expand at a steady clip through the forecast period. This acceleration aligns with structural drivers such as an aging population, continued urbanization, and rapid digitalization that improve product design, distribution efficiency, and underwriting precision, supported by sector solvency that remains well above regulatory floors. Rising claims and benefits during 2025, higher new policy counts, and growing sector assets confirm robust operating momentum across life and non-life lines. Adoption of large language models in production has shifted from pilots to scaled use in customer service, underwriting, and claims, with insurers reporting notable efficiency gains that compress cycle times and lower unit costs. Policy initiatives to strengthen capital markets participation and data infrastructure further enable broader product innovation in the China life and non-life insurance market.

Key Report Takeaways

- By insurance type, life insurance led with 56% revenue share of the China life and no-life insurance market size in 2025, while non-life is forecast to expand at an 11.60% CAGR through 2031.

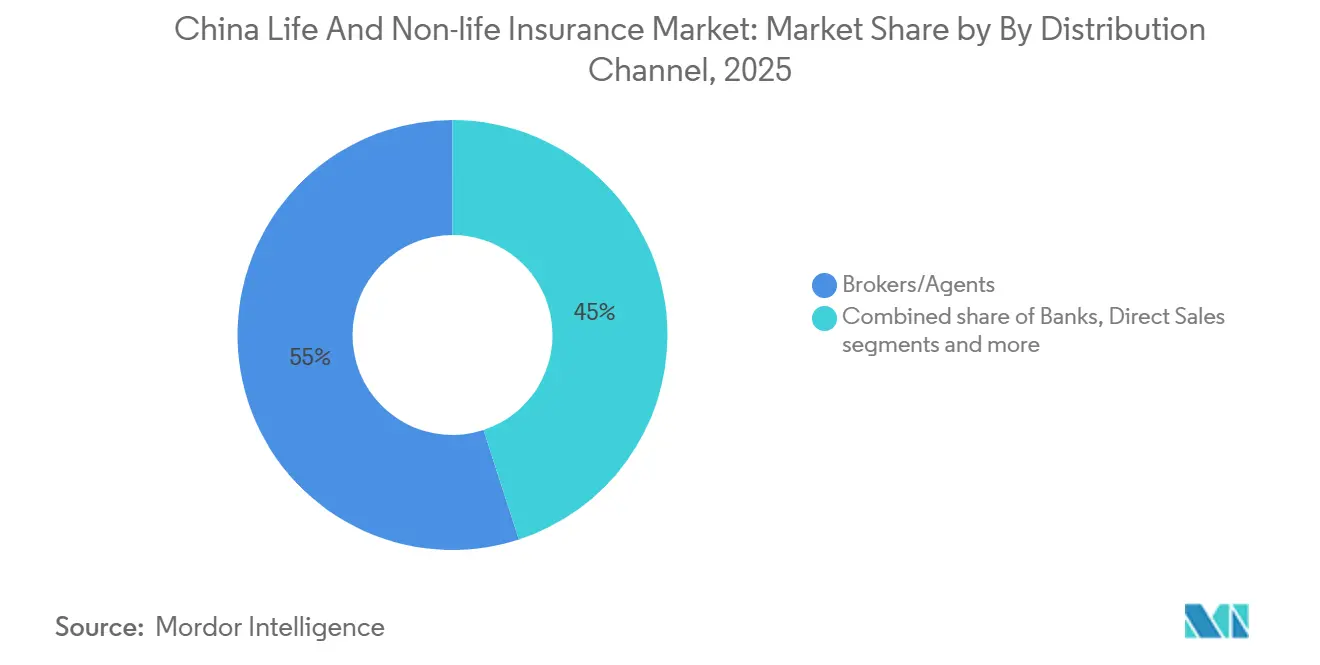

- By distribution channel, brokers and agents held 55% of the China life and non-life insurance market share in 2025, while other channels are projected to record the highest growth at a 12.40% CAGR through 2031.

- By customer segment, the retail segment accounted for a 68% share of the China life and non-life insurance market size in 2025 and is advancing at a 10.80% CAGR through 2031.

- China life and non-life insurance market is dominated by a few large insurers, but meaningful market share remains available for mid-sized and specialized players to compete and grow.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

China Life And Non-life Insurance Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising disposable incomes and middle-class expansion | +2.1% | National, concentrated in tier-1 and tier-2 cities | Medium term (2-4 years) |

| An aging population is driving life, retirement, annuity, and health demand | +2.5% | National, particularly acute in eastern provinces | Long term (≥ 4 years) |

| Elevated post-pandemic risk awareness | +1.3% | Global, with urban China leading adoption | Short term (≤ 2 years) |

| Urbanization and penetration into underserved markets | +1.6% | Rural and tier-3/4 cities, western regions | Medium term (2-4 years) |

| Policy support, regulatory reforms, and financial inclusion | +1.2% | National | Long term (≥ 4 years) |

| Digitalization, insurtech adoption, and advanced analytics | +1.8% | National, with early gains in Shanghai, Beijing, Guangdong | Short to medium term |

| Source: Mordor Intelligence | |||

Rising Disposable Incomes and Middle-Class Expansion Boosting Demand

Steady gains in household disposable income and ongoing efforts to broaden the social safety net are expanding demand for protection and savings products, particularly among urban middle-income consumers. Basic medical insurance coverage remained near-universal in 2025, providing a foundation for private insurers to design complementary health and critical illness offerings that enhance financial protection for households. Life insurers increased new business value through stronger execution in bancassurance and higher-margin product mixes, reflecting how rising wealth translates into more sophisticated demand across risk and savings needs. Regulatory measures have strengthened product suitability and sales practices, supporting consumer trust and channel productivity as the China life and non-life insurance market scales. As customer profiles diversify, large incumbents are using multi-channel models to reach both affluent and mass segments while keeping unit costs in check through digital onboarding and straight-through processing. Sector-wide momentum in policy issuance and premium income during 2025 supports the view that rising incomes are translating into product uptake across life, health, and accident lines in the China life and non-life insurance market.

Aging Population Driving Growth in Life, Retirement, Annuity, and Health Insurance Products

An aging demographic profile is reshaping product design and reserve strategies, with long-term care, annuity, and health riders gaining traction as insurers adapt underwriting and pricing to longevity risks. Long-term care programs and enhanced medical coverage at the national level provide an anchor for commercial solutions that address out-of-pocket risks for older adults, spurring private demand for riders and supplemental coverage. Commercial pension and health insurance reserves expanded during the 14th Five-Year Plan, reflecting the deeper role private capital plays in retirement security and chronic disease protection[1]National Financial Regulatory Administration, “Press Conferences on ‘Delivering High-Quality Results under the 14th Five-Year Plan’,” National Financial Regulatory Administration, nfra.gov.cn. Insurers have invested in senior ecosystems that blend finance and services, including retirement communities and health management platforms that improve persistency and customer lifetime value. These “insurance plus” models integrate screening, chronic disease management, and residential care into policy structures, creating service-led differentiation that supports margin resilience. The demographic tailwind remains most pronounced in eastern provinces, although the China life and non-life insurance market is seeing broader national adoption as underwriting for senior cohorts expands.

Elevated Post-Pandemic Risk Awareness Increasing Uptake of Health, Life, and Accident Covers

Heightened awareness of health and mortality risks since the pandemic period has reinforced demand for health, life, and accident covers, particularly among urban professionals. Regulatory initiatives to encourage commercial coverage of innovative therapies that sit outside public reimbursement create new product categories for private health insurers and expand potential coverage scopes. Digital-first carriers and incumbents have scaled automation in underwriting and claims, which reduces the friction of purchase and service while improving risk selection. China’s largest digital-native players report significant throughput on core AI platforms, supporting both customer service and straight-through policy issuance at scale in the China life and non-life insurance market. The combination of rising claims activity, broadening product scope, and higher automation rates indicates that risk awareness is translating into sustained premium growth across health-linked lines. As these products mature, cross-selling into longer-duration life and annuity products strengthens multi-line engagement and retention.

Urbanization and Expansion into Underpenetrated Urban and Rural Insurance Markets

Urbanization continues to support premium growth in inland and lower-tier cities as population shifts and infrastructure investment raise insurance awareness and purchasing power. Leading foreign-invested and joint-venture carriers have expanded into new provincial markets, adding millions of addressable customers and diversifying beyond saturated coastal metros. Large domestic incumbents are deepening agricultural, property, and liability coverage in rural areas, using extensive branch networks and partnerships to distribute protection where physical risk remains elevated. Catastrophe and agricultural schemes improve income stability and support insurance adoption among rural households, creating on-ramps for broader coverage over time in the China life and non-life insurance market. These efforts help reduce geographic concentration risk for carriers while raising penetration in markets where distribution density and product awareness had lagged. The result is a more balanced national footprint with premium growth that increasingly reflects contributions from central and western regions.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Macroeconomic uncertainty and income pressure | -0.9% | National, export-heavy provinces are more exposed | Short to medium term |

| Low interest rates and investment volatility | -0.7% | National | Medium term (2-4 years) |

| Stricter solvency, capital, and conduct regulations | -0.4% | National | Long term (≥ 4 years) |

| Regulatory limits on guaranteed products and motor pricing controls | -0.5% | National, motor insurance constraints in tier-1 cities | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Macroeconomic Uncertainty and Income Pressure Limiting Insurance Affordability and Demand

Macroeconomic headwinds from property sector stress, softer external demand, and cautious household sentiment can slow premium growth in discretionary lines and pressure agent-driven sales models. Government funding allocations for healthcare security in 2026 reflect a recognition that public support must complement private coverage capacity where affordability is strained. Large incumbents are tilting toward longer-duration regular premium products that stabilize income and improve persistency in a slower-growth environment. New policy issuance and total sector assets still expanded in 2025, although renewal momentum in certain cohorts moderated, consistent with pressure on middle and lower-middle household budgets. Sales force rationalization continued through 2024 and into 2025 as carriers focused on productivity, digital onboarding, and compliance to support sustainable growth. The overall effect is resilient but more selective growth in the China life and non-life insurance market as carriers prioritize quality over volume.

Low Interest Rates and Investment Volatility Weighing on Life Insurer Profitability.

Persistently low government bond yields compress asset returns and narrow spreads on legacy guaranteed blocks, increasing the importance of asset-liability duration matching and product repricing. Mortality table updates and assumption changes have influenced pricing and reserving, with some carriers indicating lower long-term investment return assumptions that weigh on reported new business value. Regulators launched a pilot in 2025 that allows gold investments by insurance funds, signaling openness to diversified instruments that can manage rate risk. Leading carriers increased allocations to long-duration government bonds and launched private funds to access strategic sectors, healthcare, and infrastructure as part of refined portfolio construction. Investment income improved for several large incumbents in 2024 and 2025 as equity markets recovered, although structural yield headwinds remain a concern for life profitability. The mix shift toward participating, protection-oriented, and asset-backed solutions helps balance margin risk while supporting the China life and non-life insurance market through the rate cycle.

Segment Analysis

By Insurance Type: Non-Life Segment Gains Momentum Amid NEV and Digitalization Catalysts

Life insurance accounted for a 56% share in 2025 while non-life is projected to expand at 11.60% through 2031, indicating that the China life and non-life insurance market size has scope to rebalance as property and liability lines accelerate. This divergence reflects growing uptake of health and accident policies from digital channels and the scale-up of newer categories within motor and liability lines. Property-casualty carriers report strong throughput in motor and health-related short-duration products, with rural and agricultural lines playing a stabilization role in regional portfolios. Leading carriers strengthened underwriting, pricing, and service models with AI and data-led tools to improve combined ratios even as volumes rise. Sustained improvements in claims handling and fraud detection, alongside regulatory initiatives to refine pricing discipline, support non-life profitability as the China life and non-life insurance market continues to expand.

Life franchises are increasingly diversified, with higher-margin protection and participating products improving new business value despite rate headwinds. Large incumbents reported growth in new business value, supported by enhanced agent productivity and improved bancassurance execution that increases access to mass affluent customers. The non-life segment benefited from scale in motor and evolving risk management practices powered by telematics, analytics, and faster claims resolution. Property-casualty leaders deployed targeted strategies in agriculture and catastrophe schemes that reinforce social resilience and household income stability, which in turn support broader insurance adoption. The interplay of life and non-life growth vectors contributes to balanced expansion in the China life and non-life insurance market.

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Customer Segment: Retail Dominance Reflects Middle-Class Aspiration and Digital Onboarding

Retail customers held a 68% share in 2025 and are projected to grow at 10.80% through 2031, which means the retail component of the China life and non-life insurance market size is set to expand faster than corporate lines through the forecast horizon. Retail scale is supported by life policies, health covers, and personal accident products that have benefited from better suitability processes and digital self-service adoption. Large incumbents report high retention among multi-product households and growing use of app-based services that standardize onboarding and claims settlement. As straight-through processing rates rise and tele-underwriting matures, retail conversion improves without proportional expansion of agent headcount, which supports distribution cost control in the China life and non-life insurance industry. The corporate segment remains important for group health, property, and liability covers, where risk engineering and ESG-linked services differentiate offerings.

The multi-line model is expanding as carriers bundle wellness, eldercare, and financial planning services that elevate engagement and persistency. Health and senior care ecosystems are now material contributors to value of new business at leading groups, and they strengthen cross-sell potential into annuity and critical illness. Corporate clients are adopting value-added services such as risk monitoring and sustainability-linked risk solutions as they navigate operational and regulatory demands. These dynamics keep retail in a leadership position while allowing corporate to deepen strategic relationships with insurers that go beyond risk transfer. Together, they create a stable base for the China life and non-life insurance market through the cycle.

By Distribution Channel: Direct and Digital Channels Disrupt Traditional Broker-Agent Models

Brokers and agents captured a 55% share of premiums in 2025, while other channels that include direct digital platforms and bancassurance are projected to expand at a 12.40% growth rate through 2031, suggesting the China life and non-life insurance market size from digital and direct channels will rise faster than traditional agency. Agent productivity continues to improve at leading carriers due to AI-supported training and lead prioritization, even as headcounts adjust to quality standards. Bancassurance has seen a resurgence as insurers and banks refine partnerships, focus on higher-value products, and align incentives around service and compliance. Direct-to-consumer platforms scale standardized products and enable rapid iteration where risk data and customer behavior insights can be quickly integrated into pricing. The result is a more balanced omnichannel landscape that increases access and reduces friction for customers in the China life and non-life insurance market.

Digital onboarding and self-service improve time-to-issue and reduce errors, which enhances customer experience and compliance outcomes. App ecosystems at large incumbents enable underwriting and policy administration with high automation rates that support stable service levels at scale. As online channels gain share, insurers are investing in analytics, experimentation, and user experience design that translates into higher conversion and retention. Banks deepen relationships by positioning protection and retirement solutions within broader wealth management journeys, which lifts the value of new business contribution from bancassurance at several large groups. Over time, the distribution mix will reflect a larger contribution from direct digital and bank partners, while agency remains central to complex life sales in the China life and non-life insurance market.

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

Geography Analysis

Eastern coastal provinces, including Guangdong, Zhejiang, Shanghai, and Beijing, continue to anchor a majority share of national premiums in 2025, supported by concentrated wealth, dense distribution, and strong digital infrastructure. Capital markets activity associated with insurer funds also clusters around Shanghai and Shenzhen, reinforcing the financial and technology ecosystems that support product design and investment strategies. Major illness insurance and long-term care programs reached large portions of the population by 2025, with pilot programs more prevalent in affluent municipalities before broader rollout. Together, these factors favor complex life products, critical illness coverage, and cyber liability solutions in tier-1 cities as household financial planning sophistication rises in the China life and non-life insurance market. Regulatory communication in 2025 confirmed strong sector solvency and growing reserves that support long-duration guarantees. The geographic pattern underscores the role of coastal hubs in setting benchmarks for product sophistication and service standards.

Central and western regions such as Sichuan, Chongqing, Henan, Hubei, Anhui, Hunan, and Shaanxi are recording faster growth from lower bases as urbanization and industrial upgrading expand middle-income cohorts. New regional expansions by multinational carriers are adding material addressable populations and increasing competitive intensity in these provinces. Larger domestic incumbents broadened agricultural and catastrophe programs that stabilize household income and encourage insurance adoption in rural areas as infrastructure and supply chains develop. The China life and non-life insurance market is therefore seeing a steady rise in inland premium contribution as distribution networks penetrate and product awareness improves. Provincial capitals with technology and manufacturing clusters are seeing stronger demand for comprehensive protection and wealth-linked life offerings. This rebalancing supports a more even growth profile across regions during 2026 and beyond.

Southern clusters such as the Greater Bay Area remain important for innovation and cross-border finance, and they influence product development and risk management practices nationwide. The regulatory action plan in 2025 to support Shanghai as an international financial center and the sector’s strong solvency and asset growth emphasize the system’s readiness to integrate further with capital markets. The China life and non-life insurance market benefits from these initiatives as carriers access deeper investment opportunities and reinsurance capacity, which in turn support product guarantees and pricing stability. The combination of coastal sophistication and inland catch-up suggests premium growth will moderate in mature hubs while accelerating in underpenetrated markets. The evolving geographic footprint increases the role of regional ecosystems in shaping distribution, product, and service priorities through 2031. These dynamics help the China life and non-life insurance market balance growth with risk across macro and demographic cycles.

Competitive Landscape

Market concentration is moderate, with top incumbents in life and property-casualty capturing significant, but not dominant, combined shares, which leaves room for mid-tier and specialized players. China Life reported sharp profit growth in 2024 with rising embedded value and total assets, underscoring balance sheet strength to support long-duration protection and pension products[2]China Life Insurance Company Limited, “2024 Annual Report,” HKEXnews, hkexnews.hk. Ping An delivered higher investment yields and growth in new business value from life and health, as well as improved underwriting performance in property-casualty. PICC Group maintained leadership in property-casualty premiums and underwriting profitability, supported by data and AI tools embedded in claims management[3]PICC Property and Casualty, “2024 Annual Results PICC P&C,” PICC P&C, property.picc.com. These characteristics combine to define a competitive field where scale, omnichannel reach, and technology maturity are decisive in the China life and non-life insurance market.

Strategy has tilted toward ecosystems and service integration. Ping An’s integrated finance with health and senior care focus increases multi-product penetration and reinforces retention across a near 250 million customer base while AI service representatives process a large majority of service volumes[4]Ping An Insurance, “Audited Results for the Year Ended 31 December 2024,” HKEXnews, hkexnews.hk. China Life and CPIC continue to expand senior care and wellness-linked services that wrap around life policies and extend engagement beyond claims, which supports persistency and cross-sell. Property-casualty leaders leverage risk engineering, telematics, and analytics to improve loss ratios in motor and to calibrate pricing in health and liability lines as data breadth improves. Together, these moves reflect a competitive shift toward outcome-based service promises that strengthen customer lifetime value in the China life and non-life insurance market.

Mid-tier and specialized carriers are scaling digital distribution and automation to close cost gaps and to address niche risks. ZhongAn’s automation of underwriting and bot-enabled service demonstrates how cloud-native models deliver underwriting scale and speed without a large physical network. AIA continues to expand selective provincial footprints and sustain high margins through a premier agency model, targeting affluent customer cohorts with comprehensive protection and wealth solutions. Reinsurance capacity is reinforced by China Re’s designation as an internationally active insurance group, which deepens oversight and global integration that benefits the broader China life and non-life insurance market. These examples illustrate how differentiation now rides on digital execution, geographic precision, and balance sheet strength.

China Life And Non-life Insurance Industry Leaders

People’s Insurance Co. of China (PICC)

China Life Insurance Co. Ltd.

Ping An Insurance (Group) Co. of China Ltd.

China Pacific Insurance (CPIC)

New China Life Insurance Co.

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- June 2025: NFRA designated China Reinsurance Group as an Internationally Active Insurance Group, reinforcing oversight of systemically important carriers.

- February 2025: NFRA launched a pilot program that permits gold investment by insurance funds to enhance asset-liability management and manage rate risk

- June 2025: New China Life Insurance Company Ltd completed the acquisition of a 5.45 % equity interest in Bank of Hangzhou Co. Ltd, purchasing approximately 329.6 million shares as part of a broader strategic diversification of its investment portfolio.

- November 2025: New China Life Insurance launched its “Xinhua-Kang” health management services brand and the “Kanghu Wuyou” care insurance product, marking a shift toward an integrated “insurance + health services” ecosystem offering end-to-end health management solutions.

China Life And Non-life Insurance Market Report Scope

The life and non-life insurance market encompasses life insurance products, which offer long-term financial protection and savings, and non-life insurance products, which address short-term risks, including health, property, motor, and liability losses.

The China Life and Non-Life Insurance Market Report is Segmented by Insurance Type (Life Insurance, Non-Life Insurance(Motor, Health, Property, Liability, and More)), by Customer Segment (Retail, Corporate), and by Distribution Channel (Brokers/Agents, Banks, Direct Sales, Other Channels). The Market Forecasts are Provided in Terms of Value.

By Insurance Type

| Life Insurance | |

| Non-Life Insurance | Motor Insurance |

| Health Insurance | |

| Property Insurance | |

| Liability Insurance | |

| Other Insurance |

By Customer Segment

| Retail |

| Corporate |

By Distribution Channel

| Brokers/Agents |

| Banks |

| Direct Sales |

| Other Channels |

| By Insurance Type | Life Insurance | |

| Non-Life Insurance | Motor Insurance | |

| Health Insurance | ||

| Property Insurance | ||

| Liability Insurance | ||

| Other Insurance | ||

| By Customer Segment | Retail | |

| Corporate | ||

| By Distribution Channel | Brokers/Agents | |

| Banks | ||

| Direct Sales | ||

| Other Channels | ||

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the current size and growth outlook for the China life and non-life insurance market?

The sector stands at USD 0.91 trillion in 2026 and is projected to reach USD 1.42 trillion by 2031 at a 9.3% CAGR, supported by demographic shifts, urbanization, and digitalization.

Which segments are expanding fastest within China’s life and non-life space?

Non-life lines are forecast to be the fastest with an 11.60% growth rate through 2031, while retail customers and other digital channels are also growing strongly at 10.80% and 12.40%, respectively.

How are solvency and capital conditions shaping the China life and non-life insurance market?

Sector solvency remains well above regulatory floors, and 2025 technical adjustments reduced risk factors for long-term equity holdings, supporting patient capital deployment.

What is driving digital adoption among Chinese insurers?

Over 60% of insurers have at least one LLM-based application in production, and app-based automation in underwriting and policy administration is improving efficiency and customer experience.

How is aging influencing product demand in China?

Aging is raising demand for long-term care, annuity, and health riders, with insurers integrating senior care and wellness services to strengthen engagement and persistency.

Which regions are most influential in shaping growth patterns?

Coastal hubs anchor premium share and product sophistication, while central and western provinces are growing faster from lower bases as urbanization and distribution density rise.