Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

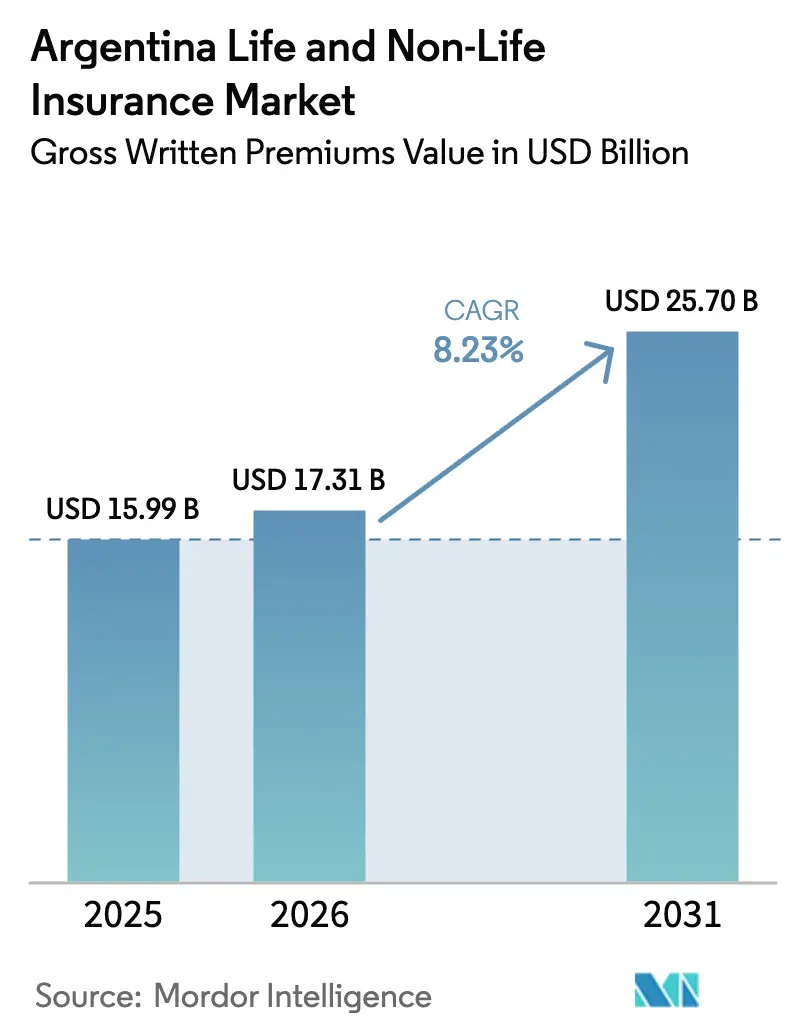

| Base Year Market Size (2025) | USD 15.99 Billion |

| Market Size (2026) | USD 17.31 Billion |

| Market Size (2031) | USD 25.70 Billion |

| Growth Rate (2026 - 2031) | 8.23% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Argentina Life And Non-Life Insurance Market Analysis by Mordor Intelligence

The Argentina Life And Non-Life Insurance Market size in terms of gross written premiums value is projected to expand from USD 15.99 billion in 2025 and USD 17.31 billion in 2026 to USD 25.70 billion by 2031, registering a CAGR of 8.23% between 2026 to 2031.

The Argentina life and non-life insurance market operates under active regulatory supervision and is navigating disinflation in 2026 after a sharp CPI deceleration through late 2025, which supports a gradual improvement in pricing stability for multi-year covers. Capital adequacy reforms and reserve methodology changes remain an important driver of prudential resilience in the Argentina life and non-life insurance market, while the shift to automatic product authorization shortens time to market for new offerings. Distribution is still led by brokers and agents, and the Argentina life and non-life insurance market is adding scale in digital channels as customer onboarding and claims workflows digitize at pace. Market concentration is moderately low, and top-tier insurers are positioned to consolidate share under the new solvency thresholds in the Argentina life and non-life insurance market.

Key Report Takeaways

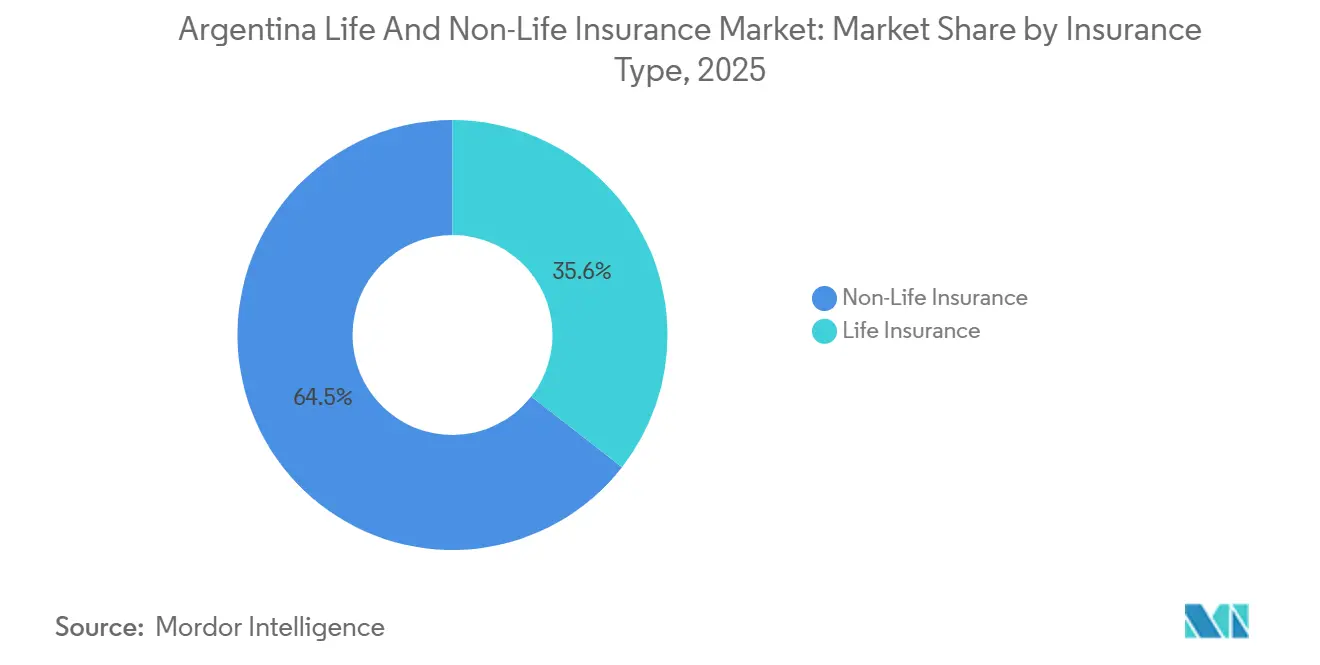

- By product line, non-life insurance led with 64.45% share of Argentina life and non-life insurance market size in 2025, and is projected as the fastest-growing line at a 14.2% CAGR through 2031.

- By distribution channel, brokers and agents held 55.30% of Argentina life and non-life insurance market size in 2025, and digital channels are expected to record the highest projected CAGR at 12.5% through 2031.

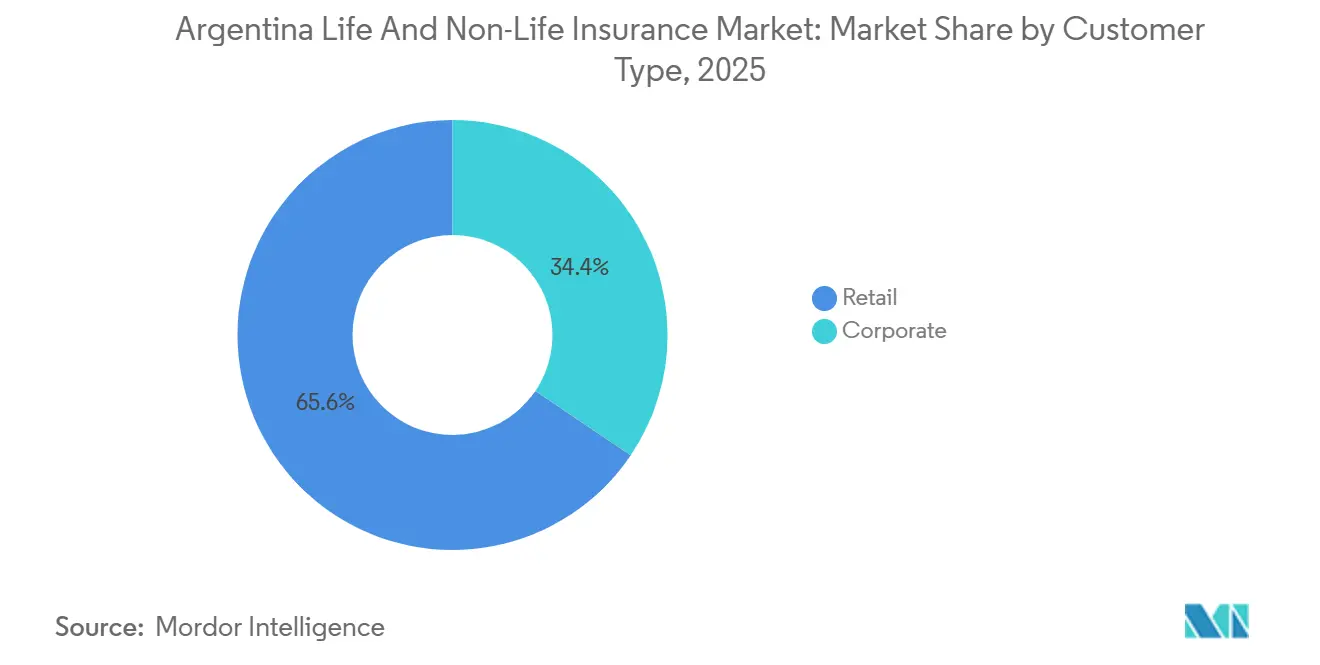

- By customer type, retail accounted for 65.56% of Argentina life and non-life insurance market size in 2025, and SMEs are projected to expand at a 10.8% CAGR between 2026 and 2031.

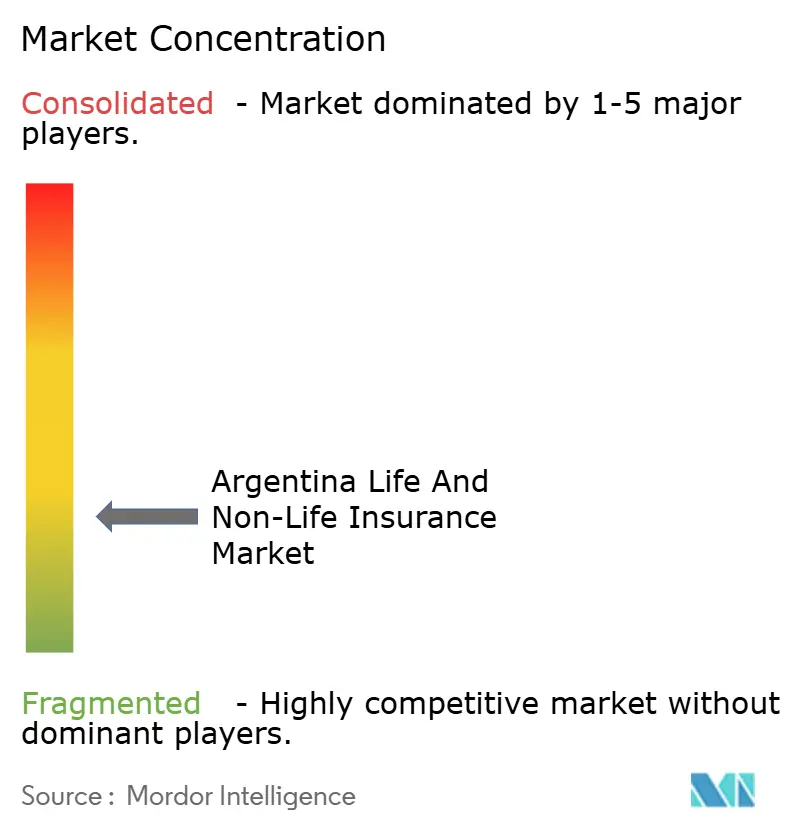

- Among companies, the top five insurers commanded a combined 35% share of Argentina life and non-life insurance market in 2025.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Argentina Life And Non-Life Insurance Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Low insurance penetration and catch-up potential | +1.8% | Nationwide | Long term (≥ 4 years) |

| Strong regulatory framework and active SSN supervision | +1.2% | Nationwide | Medium term (2-4 years) |

| Insurance as long-term capital for investment and infrastructure | +0.8% | Nationwide, project corridors | Long term (≥ 4 years) |

| Growing risk awareness in health and catastrophe exposures | +1.0% | Nationwide, agricultural provinces | Medium term (2-4 years) |

| Consumer protection and contract transparency | +0.6% | Nationwide | Medium term (2-4 years) |

| Innovation, parametric, and inflation-adjusted covers | +1.1% | Nationwide, agro belts and major urban centers | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Low Insurance Penetration and Large Catch-Up Potential

Insurance penetration stood near 3.5% of GDP in 2025, which placed the Argentina life and non-life insurance market below regional benchmarks and indicates a meaningful long-term expansion runway as macro conditions stabilize and real incomes recover[1]Asociación Argentina de Compañías de Seguros, “Informes y Estadísticas del Mercado,” AACS, aacs.org.ar. The depth of financial intermediation also remained low, with private sector credit at 10.6% of GDP in March 2025, and this supports the case that rising formalization can unlock new premium pools for the market as credit and savings products deepen across the cycle[2]Banco Central de la República Argentina, “Informe de Estabilidad Financiera,” BCRA, bcra.gob.ar. Beyond these structural indicators, disinflation extending into 2026 reduces policy limit erosion and enhances product relevance for households and SMEs, supporting more sustainable premium growth. Improving macro conditions, alongside OECD projections of renewed economic momentum, provide a favorable environment for commercial insurance demand as businesses expand assets and employment, lifting uptake across property, liability, and workers’ compensation lines. At the same time, greater use of digital distribution and claims processing lowers onboarding frictions and strengthens underwriting quality, enabling broader adoption of voluntary covers. Together, these factors point to a multi-year catch-up phase in which historically low coverage across life, health, property, and agricultural insurance can gradually converge toward regional norms as stability becomes entrenched.

Strong Regulatory Framework And Active Supervision By SSN

The SSN’s law-based supervisory mandate and the RGAA framework provide clear authority for prudential oversight, conduct rules, and market transparency, which in turn strengthens confidence in the Argentina life and non-life insurance market. The reform cycle since 2024 has centered on solvency, operational deregulation, and transparency, with key resolutions overhauling capital thresholds and allowing automatic plan authorization to shorten product launch cycles in the market. The unified minimum capital based on UVA for direct insurers and local reinsurers simplifies capital structure management and reduces fragmentation by line of business, which can support diversification strategies across the market. The open data portal and the “Tu Tablero Asegurador” dashboard enhance disclosure on solvency, claims ratios, and financial indicators, enabling buyers and distributors to compare options across the market. New reserve methodology for IBNR and pending claims aligns with actuarial techniques and inflation updates, which supports reserve adequacy as litigation flows evolve. Reporting deadlines and electronic systems for mediated and judicial claims strengthen supervisory monitoring, which promotes discipline across carriers.

Use of Insurance To Promote Long-Term Investment And Infrastructure

Insurers serve as core institutional investors, holding a portfolio near 5% of GDP in 2024, and this positions the Argentina life and non-life insurance market as a channel for long-dated capital formation that can finance infrastructure and productive projects. Portfolio composition at the end of 2023 showed broad use of inflation-linked government securities and mutual funds alongside corporate bonds, which helps align assets with inflation-indexed liabilities within the market. Regulatory constraints require that locally registered carriers hold investments and cash equivalents in Argentina, which concentrates exposure domestically while channeling savings into the local economy. Allocation requirements to SMEs support productive sector financing where bank credit depth remains limited, and this can strengthen the customer base for commercial covers[3]Insurance Europe, “Argentina Foreign Exchange Controls and Insurance Market,” Insurance Europe, insuranceeurope.eu. Broader reforms in investment rules have expanded the use of closed-end funds and sub-sovereign instruments, which enable insurers to diversify within domestic limits and match liability profiles in the market. Inflation-linked units such as CER and UVA published by the central bank provide technical tools for liability matching, which is important for longer-duration lines in the market.

Growing Risk Awareness Including Health And Catastrophe Risks

Health-related price dynamics raised awareness of out-of-pocket exposure and accelerated demand for supplemental protection in 2025, as regulated health system prices posted strong year-over-year gains and households prioritized financial safeguards. Employers increasingly use group health and group life to differentiate compensation packages as formal employment conditions improve, which supports premium growth. Climate variability and extreme weather events have drawn attention to parametric solutions that trigger on objective indices and pay quickly, which opens a path for drought and flood coverage innovations in the market. UNDP diagnostics have highlighted gaps in disaster risk finance and microinsurance penetration, and the inclusive insurance agenda can expand access for vulnerable groups. Property owners are reviewing sums insured due to rising replacement costs, which helps address legacy underinsurance risks. Reserve reforms that use longer claims histories for long-tail lines acknowledge evolving litigation patterns and support stability in the Argentina life and non-life insurance market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Chronic high inflation and currency instability | -1.5% | Nationwide | Short term (≤ 2 years) |

| Risk of underinsurance and outdated coverage limits | -0.9% | Nationwide | Short term (≤ 2 years) |

| Macroeconomic and sovereign risk pressures on insurers’ balance sheets | -1.2% | Nationwide | Medium term (2-4 years) |

| Regulatory and operating complexity with frequent rule changes | -0.8% | Nationwide | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Chronic High Inflation And Currency Instability

Persistent inflation has impaired premium adequacy and reserve dynamics, and the CPI path that fell to 31.4% year over year by November 2025 followed a peak period that strained underwriting results in the market. Pricing models faced difficulty as medical costs, vehicle prices, and legal expenses moved at different rates, which weakened the predictive value of historical loss ratios. Exchange rate volatility raised the local currency cost of reinsurance and foreign obligations, and the official wholesale rate stood near ARS 1,469.61 per USD in early January 2026, which affected payables and recoveries across the market[4]Banco Central de la República Argentina, “Principales Variables,” BCRA, bcra.gob.ar. Control liberalization in April 2025 eased settlement timelines for cross-border reinsurance, although counterparties still weigh policy risk when assessing commitments. Domestic investment rules require local asset allocation for carriers, which constrains hard currency diversification and links balance sheets to local inflation cycles. In this environment, underinsurance becomes a direct consequence of inflation, and policyholders often need limit adjustments to maintain real protection in the Argentina life and non-life insurance market.

Macroeconomic And Sovereign Risk Pressures On Insurers’ Balance Sheets

Insurers hold a large share of portfolios in sovereign securities and mutual funds that themselves hold government bonds, which creates correlated exposure to public finance shifts in the Argentina life and non-life insurance market. Sovereign spread volatility transmits to insurance asset valuations and solvency ratios, and this pressure can coincide with higher reserve needs when inflation expectations rise. The economy contracted in 2024, then returned to growth in 2025 and 2026 in OECD projections, and that cycle shaped demand for commercial lines and capital budgets across the market. Quasi-fiscal dynamics have been under adjustment, yet the legacy structure of central bank liabilities and their conversion to Treasury instruments means refinancing risk remains a factor for financial markets that insurers depend on in the Argentina life and non-life insurance market. Restrictions that require local investment for carriers limit the ability to hedge external shocks with offshore assets, and this reinforces exposure to domestic macro cycles. Regulatory changes have allowed amortization of reserve increases over set periods, and such provisions helped manage the transition to new methodologies without immediate solvency strain in the market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Line: Non-life remains dominant with motor as the anchor

Non-life insurance contributed 64.45% of premiums in 2025. Motor insurance led total premiums in 2025, and it captured the largest share within non-life, which continued to anchor the Argentina life and non-life insurance market as mass risk coverage with compulsory foundations. Health coverage has been the fastest-growing line on a forward basis, and the Argentina life and non-life insurance market is seeing accelerated interest in products that address medical cost volatility and employer benefits demand. The market has also seen a steady focus on liability and property covers, as business asset bases shift with the investment cycle and require more precise risk transfer. Parametric products for agriculture and catastrophe events are gaining traction and complement traditional indemnity structures. The share held by motor aligns with Argentina’s large vehicle fleet and mandatory third-party liability, and this supports a stable premium foundation across cycles.

Motor held a significant share of total premiums in 2025, which highlights the centrality of mobility risks. Health is positioned as the fastest-expanding line as regulated health system prices and household expectations sustain demand, and the non-life insurance market size is projected to expand at a 14.2% CAGR between 2026 and 2031. Property and liability growth aligns with investment activity, and this adds diversity to non-life premium sources in the Argentina life and non-life insurance market. Life covers remain a smaller share than regional peers, yet benefit from improved consumer protection and solvency clarity, and these reforms strengthen trust in the Argentina life and non-life insurance market. New index-linked and foreign currency-eligible contracts broaden design choices and help maintain coverage relevance through inflation cycles in the Argentina life and non-life insurance market.

By Distribution Channel: Intermediation dominated by brokers, digital gains momentum

Brokers and agents commanded 55.30% of distribution in 2025, and this intermediation model remains the principal route to market for carriers operating in the market. Bancassurance and direct channels provide complementary reach across retail and SME segments, and the industry continues to evolve as digital workflows improve quote issuance and policy servicing. The market is adopting advanced onboarding tools that reduce cycle times, which helps close coverage gaps and supports better policy persistence. Regulatory measures for digital transparency and opt-out processes increase consumer confidence and aid channel diversification in the market.

Digital distribution is expected to be the fastest-growing route, and the market size for digital issuance and servicing is projected to expand at a 12.5% CAGR through 2031 as carriers scale analytics and self-service platforms. Brokers remain essential for complex commercial risks and tailored coverage, and this preserves an advisory-led core in the market. Direct channels reduce acquisition costs where products are simple and standardized, which benefits retail conversions. Bancassurance grows with credit expansion and cross-selling in retail and SME portfolios, and this adds distribution diversity to the Argentina life and non-life insurance market. Combined, this channel mix supports resilience and reach in the Argentina life and non-life insurance industry.

By Customer Type: Retail anchors demand, SMEs drive incremental growth

Retail customers accounted for 65.56% in 2025, and this underscores the central role of households in driving premium flows in the market. The SME segment is the fastest-growing customer group on a forward basis, and this reflects formalization and increased adoption of commercial covers for credit and investment recovery. Employers are prioritizing group health and group life benefits to attract talent, which supports retail-linked growth. Property and liability needs expand as SMEs add assets and employees, and this broadens the product footprint in the market.

Retail’s share highlights the weight of personal lines and mandatory covers in the Argentina life and non-life insurance market share. The SME segment is projected to grow at a 10.8% CAGR through 2031, and the market size for SME-targeted solutions is expected to rise with equipment, fleet, and employee-related risks. As underwriting models gain more data and pricing balance improves in a disinflationary setting, conversion rates can lift in both retail and commercial books. Consumer protection and financial disclosure reforms elevate trust, and that benefits multi-year retention across segments. Together, retail depth and SME momentum form the dual growth engines.

Geography Analysis

In 2026, market activity in Argentina's life and non-life insurance sector remains concentrated in economically vibrant provinces, with the Buenos Aires metropolitan area serving as the focal point. This distribution mirrors national GDP trends and formal employment densities. By mid-2025, Argentina's population approached 46.39 million, with major urban centers driving demand for property, motor, health, and group insurance covers. Provinces with higher per capita incomes enjoy broader insurance awareness and a diverse product mix. In contrast, rural areas, often tied to agriculture, are increasingly turning to parametric and weather-linked insurance solutions. As macroeconomic stability strengthens, there is a notable expansion of SMEs in interior provinces, leading to a broader uptake of insurance products.

Regional insurance activity is closely tied to employment rates and household financial health. In Q3 2025, an unemployment rate of 6.6% underscored stable labor market conditions, bolstering employer benefits. Investments in provincial infrastructure are diversifying premium pools, extending beyond Argentina's core urban corridors. A 2025 shift in the exchange rate regime facilitated smoother cross-border settlements for reinsurance, bolstering placements for catastrophe and large commercial risks. Local investment regulations ensure that insurance portfolios remain within Argentina, tying premium-funded savings to domestic development across provinces.

Regional differences influence both claims patterns and product preferences. Agricultural provinces lean towards weather risk tools, while urban centers show a preference for liability and health insurance. Multilateral assessments have highlighted disaster risk financing gaps, suggesting that municipal and provincial programs could harness parametric designs to bolster resilience in flood-prone regions. Nationwide consumer protection measures standardize key contract terms, helping to bridge regional disparities in buyer confidence. As disinflation takes hold, real-term affordability improves, paving the way for broader adoption of voluntary insurance policies across the country.

Competitive Landscape

In mid-2025, Argentina boasted a diverse institutional base for its life and non-life insurance market, with 189 entities authorized by the SSN. These included a mix of patrimonial and mixed insurers, life companies, retirement providers, ART carriers, and public transport mutual entities. By 2024, the top five groups commanded a notable market share, indicating a moderately low concentration in the sector. As 2026 approached, leading carriers were honing in on solvency strength, reserve adequacy, and cost discipline. With reserve recalibration and inflation normalization on the horizon, active balance sheet and pricing management became paramount. Concurrently, regulators emphasized transparency and standardized disclosures, intensifying competition based on product clarity, service quality, and claims performance.

Reforms linking capital requirements to UVA thresholds established a clear solvency baseline. With compliance deadlines set for mid-2026, operators were urged to optimize capital, consider mergers in cases of suboptimal scale, and rationalize their portfolios. The move towards automatic plan authorization empowered both established players and newcomers to swiftly innovate in product design. This shift heightened competitive intensity and fostered a trend towards modular covers. Local investment mandates ensured that assets remained within domestic markets, influencing asset allocation strategies crucial for spread income and duration matching. Brokers and agents continued to dominate distribution, with partnerships for digital onboarding and claims automation gaining traction.

In 2026, major carriers converged on reserve methodology changes, electronic reporting for litigated and mediated claims, and refined IBNR rules. Mastery in these technical areas became the distinguishing factor for market leaders. While health and group life segments emerged as key growth areas, motor and property portfolios demanded vigilance, especially concerning inflation indexation and parts cost dynamics. Following FX liberalization, international channels for reinsurance payments saw marked improvement, bolstering treaty stability for catastrophe and large industrial risks. In summary, the competitive landscape of 2026 was shaped by factors like solvency readiness, the pace of product refreshes, and channel execution.

Argentina Life And Non-Life Insurance Industry Leaders

Federación Patronal Seguros

Grupo Sancor Seguros

La Segunda Cooperativa de Seguros

Nación Seguros S.A.

Provincia ART S.A.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: FX control liberalization adjusted timelines for reinsurance outward payments and improved cross-border settlements for admitted placements

- July 2025: Resolution RESOL-2025-287-APN-SSN introduced strengthened reserve methodologies for pending claims, mediations, and IBNR by branch with inflation updates

- April 2025: Life Seguros and Life Group (formerly Prudential Seguros) completed a merger approved by the Superintendencia de Seguros de la Nación, consolidating over 5.9 million policies and expanding leadership in the local market.

- December 2025: Barbados-based reinsurer Active Capital Reinsurance Ltd. (Active Re) received regulatory approval to operate as an admitted reinsurer in Argentina, marking a new market entry for specialized reinsurance capacity

Argentina Life And Non-Life Insurance Market Report Scope

Life insurance provides a lump sum of the sum assured at maturity or in case of the policyholder's death. Non-life insurance policies offer financial protection to a person for health issues or losses due to damage to an asset.

The Argentina Life and Non-Life Insurance Market is segmented by Insurance Type (life Insurance, Non-Life Insurance (motor, Health, Property, and Other Non-Life Insurances), by Customer Segment (Retail and Corporate), and by Distribution Channel (Brokers/Agents, Banks, Direct, and Other Channels). The report offers market size and forecasts for Argentina's Life and non-life Insurance Market in value (USD) for all the above segments.

By Insurance Type

| Life Insurance | |

| Non-Life Insurance | Motor Insurance |

| Health Insurance | |

| Property Insurance | |

| Liability Insurance | |

| Other Insurance |

By Customer Segment

| Retail |

| Corporate |

By Distribution Channel

| Brokers/Agents |

| Banks |

| Direct Sales |

| Other Channels |

| By Insurance Type | Life Insurance | |

| Non-Life Insurance | Motor Insurance | |

| Health Insurance | ||

| Property Insurance | ||

| Liability Insurance | ||

| Other Insurance | ||

| By Customer Segment | Retail | |

| Corporate | ||

| By Distribution Channel | Brokers/Agents | |

| Banks | ||

| Direct Sales | ||

| Other Channels | ||

Key Questions Answered in the Report

What is the current size and growth outlook for the Argentina insurance market?

The Argentina insurance market size is USD 17.31 billion in 2026 and is projected to reach USD 25.70 billion by 2031 at an 8.23% CAGR.

Which segment leads premium contribution in the Argentina insurance market?

Non-life leads with 64.45% of 2025 premiums, supported by compulsory motor and workers’ compensation, property, and health-related covers.

How are regulations shaping the Argentina insurance market in 2026?

Reforms implemented in 2025 streamlined product approvals, unified capital floors, and improved reporting standards, supporting faster innovation and more predictable oversight.

What distribution channels are growing fastest in the Argentina insurance market?

Other channels that include embedded and direct digital are forecast to grow at a 12.5% CAGR through 2031, while bancassurance reports high digital issuance and broad reach.

Where are the strongest geographic growth drivers within Argentina?

Buenos Aires remains dominant by premium share, while Neuquén and the Northwest provinces are expanding with energy and mining projects that require specialized insurance.

What underwriting challenges remain in the Argentina insurance market?

Elevated claims severity in motor, sovereign-exposure volatility, and underinsurance from inflation continue to pressure results, making repricing, claims efficiency, and valuation discipline critical.

Page last updated on: