Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

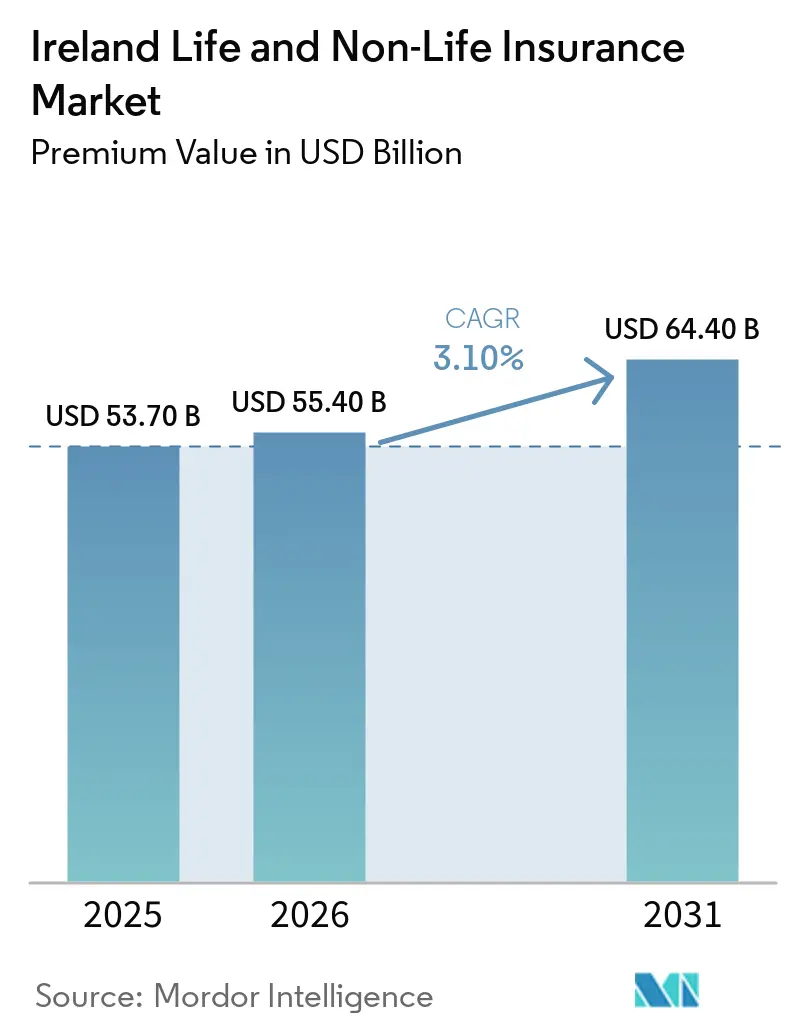

| Base Year Market Size (2025) | USD 53.70 Billion |

| Market Size (2026) | USD 55.40 Billion |

| Market Size (2031) | USD 64.40 Billion |

| Growth Rate (2026 - 2031) | 3.10% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Ireland Life and Non-Life Insurance Market Analysis by Mordor Intelligence

The Ireland Life And Non-Life Insurance Market size in terms of premium value is projected to expand from USD 53.70 billion in 2025 and USD 55.40 billion in 2026 to USD 64.40 billion by 2031, registering a CAGR of 3.10% between 2026 to 2031.

Growth aligns with structural shifts as MyFutureFund auto-enrollment begins to channel fresh contributions into long-term savings and group pensions from January 2026, strengthening life and retirement lines in the Irish life and non-life insurance market. Casualty pricing capacity benefits from the ongoing implementation of Personal Injuries Guidelines, which have reduced non-litigated injury awards and improved settlement consistency across motor and liability. Private health continues to underpin non-life momentum as penetration remained high in 2024 and average premiums rose, supporting written premium growth despite medical inflation pressures. Property and liability underwriters adjust to tighter reinsurance terms after Storm Éowyn set a new national insured loss record in January 2025, reshaping capacity and pricing for flood and wind-exposed risks in the Irish life and non-life insurance market. Conduct and distribution continue to evolve under the Individual Accountability Framework and the Consumer Protection Code 2025, which elevate governance standards and encourage digital-first customer journeys[1]Central Bank of Ireland, “Individual Accountability Framework,” Central Bank of Ireland, centralbank.ie.

Key Report Takeaways

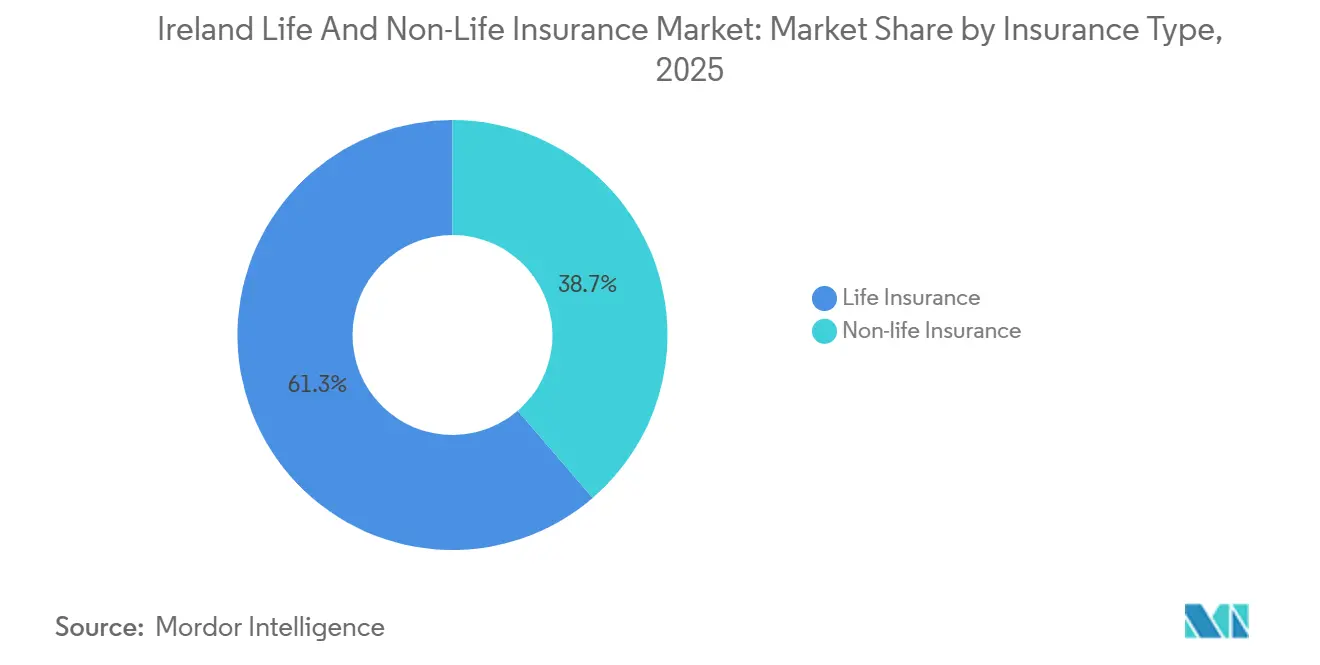

- By insurance type, life led the Ireland life and non-life insurance market with 61.3% share in 2025, while health is the fastest growing segment with a 5.5% CAGR through 2031.

- By customer segment, retail led the Ireland life and non-life insurance market with 58.6% share in 2025, while retail is advancing at a 3.9% CAGR through 2031.

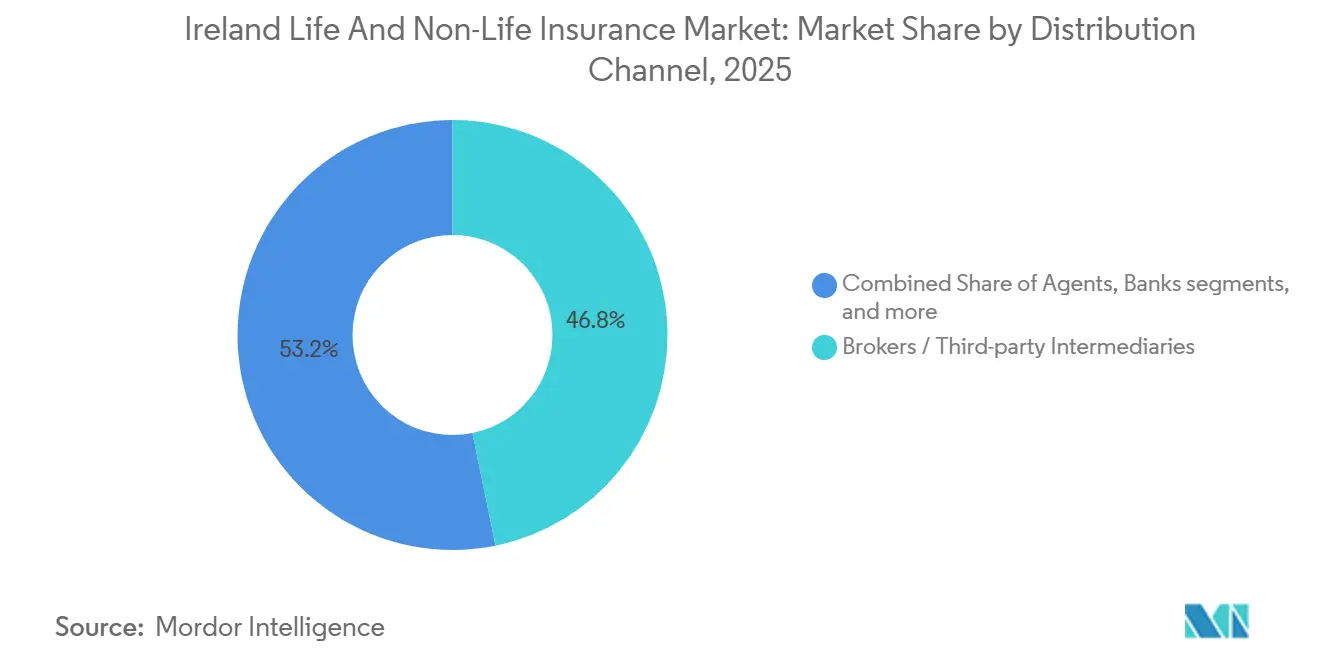

- By distribution channel, brokers held 46.8% of the Ireland life and non-life insurance market in 2025, while direct sales is the fastest growing channel at a 6.2% CAGR supported by digital-first compliance and switching provisions under CPC 2025.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Ireland Life and Non-Life Insurance Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Auto-Enrollment (MyFutureFund) Expands Long-Term Savings and Group Pensions/Life Cover | +0.8% | National, with early gains in urban employment hubs Dublin, Cork, Galway | Medium term (2-4 years) |

| Private Health Penetration and Premium Growth Sustain Non-Life Health GWP | +0.9% | National, elevated in high-income cohorts and corporate group schemes | Short term (≤ 2 years) |

| Personal Injuries Guidelines Lower Non-Litigated Costs, Stabilizing Motor/Liability Capacity | +0.6% | National, strongest effect in motor and employers/public liability | Medium term (2-4 years) |

| Insurance-Specific Inflation Lifts Written Premiums | +0.5% | National | Short term (≤ 2 years) |

| CPC 2025 Modernizes Conduct, Boosting Trust, Switching, and Digital Uptake | +0.3% | National | Long term (≥ 4 years) |

| NCID Transparency Deepens Pricing Sophistication and Attracts Capacity | +0.2% | National | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Auto-Enrollment MyFutureFund From 2026 Expands Long-Term Savings Inflows And Group Pensions Or Life Cover

MyFutureFund went live on January 1, 2026, and began onboarding large cohorts of private sector workers who previously lacked employer-backed pensions. Early activity brought 763,000 employees and 104,000 employers into the system within the first six weeks and accumulated more than EUR 60 million in contributions, which sets a durable channel for life and pension products. Eligibility parameters focus the intake on workers aged 23 to 60 with annual earnings above EUR 20,000 and no existing occupational pension, addressing a documented coverage gap. The contribution schedule starts at 1.5% each from employee and employer with a 0.5% state top-up, and steps up to a combined rate that is designed to strengthen long-horizon savings balances. Governance obligations under the Individual Accountability Framework raise the standard of oversight for auto-enrollment administration, with senior executives required to evidence reasonable steps. These features increase compliance certainty and support confidence in how auto-enrollment will shape flows in the Irish life and non-life insurance market.

Private Health Insurance Penetration And Premium Expansion Sustain Non-Life Health GWP

Private health coverage reached 2.52 million insured people by the end of 2024, and average premiums increased to EUR 1,740, indicating a firm willingness to retain cover despite affordability concerns. The over 65 cohort pays more on average than under 65s due to higher utilization patterns in orthopedic and cardiac care, which shapes benefit design and product positioning[2]Health Insurance Authority, “Health Insurance in Ireland, Market Report 2024,” Health Insurance Authority, hia.ie. Community rating and lifetime cover rules maintain access while requiring insurers to manage cost pressures through network management and pathway redesign. Day-case and outpatient pathways continue to expand, which helps optimize hospital capacity while improving turnaround. These health dynamics sustain a visible growth outperformance within non-life relative to the broader Ireland life and non-life insurance market. Insurers continue to show that pricing and benefit changes can track medical inflation within the remit of regulatory transparency requirements.

Personal Injuries Guidelines Reduce Non Litigated Injury Claim Costs, Stabilizing Motor And Liability Pricing Capacity

The Personal Injuries Guidelines have become the default reference for non-litigated injury claims and have reduced award levels for direct and Injuries Resolution Board settlements. In motor, the Central Bank’s 2024 report shows average injury claim costs per policy below the pre-pandemic baseline, even as damage costs increased due to supply chain and wage effects. The time and cost gap between litigated and non-litigated settlements remains wide, but the rising use of guidelines in settlements outside courts has a stabilizing effect on expected losses. Respondent consent to IRB assessments has improved while claimant acceptance has been slower, which caps the Board’s throughput but still delivers legal cost savings. The Department of Enterprise’s commissioned work highlights that Irish awards remain higher than those in England and Wales for minor soft tissue injuries, which leaves some residual pressure on reserve adequacy. Even so, the guidelines framework supports steadier rating in motor and liability within the Ireland life and non-life insurance market.

CPC 2025 Modernizes Conduct Rules, Boosting Trust, Switching, And Digital Uptake

The Consumer Protection Code 2025 concludes a multi-year review and takes effect on March 24, 2026, for insurers and intermediaries, with provisions that fit digital-first journeys and clearer disclosures[3]DAC Beachcroft, “Consumer Protection Code 2025: A Cultural Shift for Insurers,” DAC Beachcroft, dacbeachcroft.com. The Code extends pre-renewal notice periods for non-life switching, introduces opt-in auto-renewals for specific ancillary products, and limits unsolicited contact after online quote requests. By lifting transparency and reducing friction in switching, the Code creates more contestable renewal books and encourages investments in self-service and online advice. The policy wording and disclosure templates promote clear value comparisons, which support more frequent re-shopping across commoditized lines. As insurers adapt, direct channels gain share in simple products while intermediated advice repositions toward complex corporate and protection needs. These features reinforce digital adoption and improve customer choice across the Ireland life and non-life insurance market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Reinsurance Terms Tighten on Storm/Flood Risk, Pressuring Property Capacity and Pricing | -0.4% | National, elevated exposure in coastal and flood-prone regions | Short term (≤ 2 years) |

| Litigation Dominance in Injury Claims Delays Guideline Benefits | -0.3% | National | Medium term (2-4 years) |

| Differential Pricing Ban Compresses Renewal Pricing Levers in Motor/Home | -0.2% | National | Medium term (2-4 years) |

| IAF/SEAR and CPC 2025 Compliance Raises Operating Complexity and Cost-to-Serve | -0.1% | National | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Reinsurance Cost Or Terms Tighten On Storms And Flood Risk, Pressuring Property Capacity And Pricing

Storm Éowyn marked the costliest weather event in Irish insurance history in January 2025 and reset expectations for property catastrophe frequency and severity. As models incorporate stronger storm signals, reinsurers have tightened treaty structures through higher retentions and more aggregative protections, which push tail risk back to primary carriers. This dynamic reduces available capacity in flood-exposed and coastal zones and encourages primary carriers to adjust deductibles and underwriting appetite. The Central Bank has noted reserve movements in non-life that reflect both catastrophe experience and inflation adjustments, which heighten earnings volatility. Carriers with disciplined underwriting and program structures maintain advantages, but the overall supply of catastrophe capacity remains sensitive to global capital allocation trends. These reinsurance conditions weigh on property pricing and availability within the Ireland life and non-life insurance market.

Litigation Remains Dominant Channel For Injury Costs, Delaying Full Benefits Of The Guidelines

While award levels declined for non-litigated injury cases under the guidelines, a significant share of claims proceeds through litigation, which extends timelines and raises legal cost shares. Comparative analysis from the Department of Enterprise shows Irish soft tissue awards exceed England and Wales benchmarks, and legal costs in litigated pathways remain material. The gap in average total costs between litigated and direct or IRB settlements continues to dilute the full gain from award reductions. The Judicial Council has considered adjustments that, if enacted, could recalibrate guideline levels, adding further uncertainty to reserve planning. The IRB aims to improve claimant acceptance and accelerate throughput, which could curb litigation reliance over its 2025 to 2029 plan period[4]The Law Society of Ireland, “Judges Propose 16.7% Rise in PI Damages,” The Law Society of Ireland, lawsociety.ie. Until then, litigation predominance constrains the speed at which guideline savings flow through to pricing across the Irish life and non-life insurance market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Insurance Type: Life Cushions Margins While Health Surges On Medical Inflation

Life maintained leadership with a 61.3% share in 2025, and health is the fastest rising component with 5.5% CAGR, as premium levels and penetration supported non-life growth relative to the overall Irish life and non-life insurance market. The Ireland life and non-life insurance market share leadership of life reflects stable contributions in group pensions and individual protection, supported by employer schemes and growing awareness from auto-enrollment communications. Standard Life’s 2024 research highlights knowledge gaps in retirement products that insurers and advisors must bridge as auto-enrolled workers transition into more active plan management. As contributions escalate under the MyFutureFund schedule, unit-linked flows and annuity or ARF pathways see more consistent demand, which stabilizes life balance sheets. On the non-life side, health benefits from higher day case pathways and clinic access that support earlier intervention and more predictable claims. These shifts underpin segment resilience in the Ireland life and non-life insurance industry.

Motor and liability dynamics reflect the benefits of the Personal Injuries Guidelines on injury costs, even as damage severities rose with wage and parts pressures in 2024. Property underwriting must adapt to tighter catastrophe structures after Storm Éowyn, which makes flood mapping, deductibles, and resilience measures more material to pricing and coverage availability. Health insurers deploy product innovation including rapid-access clinics and targeted benefits that respond to chronic and outpatient needs, which can help balance hospital pressures. In life, bank-tied and digital advice channels gather more applicants and use simplified onboarding to convert awareness into funded policies. These patterns, together with consistent regulator disclosures via NCID and Solvency reporting, support steady risk selection and capital allocation in the Ireland life and non-life insurance market.

By Customer Segment: Retail Dominates As Corporate Buyers Exploit NCID Transparency

Retail customers held a 58.6% premium share in 2025 and grew at a 3.9% annual rate as reforms and switching improved value capture for households within the Ireland life and non-life insurance market. Motor, a retail bellwether, saw average written premiums rise in 2024 while injury claim costs per policy remained below pre-pandemic averages due to guideline effects. Transparency from the NCID keeps carriers in close competition on rating and claims performance, which helps sustain affordability gains for repeat renewals. The differential pricing ban has eliminated so-called price walking at second renewal for household and motor, which reduces loyalty penalties and strengthens competitive discipline. CPC 2025 extends notice periods for switching and restricts certain follow-up practices, which improves retail switching ease across commoditized lines. Health remains a key retail anchor as age-related utilization and coverage tiers shape benefit mix and consumer decisions, with the Health Insurance Authority tracking premium and enrollment changes. Auto-enrollment brings new savers into pensions, which creates opportunities to attach life protection and income protection cover over time.

Corporate buyers leverage NCID benchmarking to negotiate structures and premiums in liability and property, emphasizing deductibles and multi-year program certainty where possible. Group health continues to support workforce access to diagnostic and outpatient care, with insurers broadening clinic access and preventive programs to optimize costs. Property and liability placements reflect greater climate and catastrophe focus after Storm Éowyn, particularly for coastal and flood-exposed sites where insurers apply tighter terms. Corporate functions face higher governance burdens under IAF and SEAR, which insurers address with compliance support and training, embedded into renewal engagements. These retail and corporate patterns together shape distribution volume and product design in the Ireland life and non-life insurance industry and continue to move the portfolio toward clearer price quality comparisons.

By Distribution Channel: Brokers Hold Share Yet Direct Sales Accelerate Via Digital Platforms

Brokers retained a 46.8% share in 2025, while direct sales are the fastest-growing channel on a 6.2% trajectory as digital quoting and consent requirements reshape engagement models across the Irish life and non-life insurance market. CPC 2025 makes opt-in auto-renewals mandatory for certain ancillary covers and limits unsolicited outreach after online quotes, which strengthens the case for self-service journeys. Banks and tied agent channels remain relevant for protection products, especially when paired with mortgage and savings conversations that naturally introduce life and income cover. Insurers have raised digital submission rates for new business through advisor portals and customer onboarding tools, which shortens time to bind and reduces administrative friction. Brokers respond by focusing on complex commercial placements and risk engineering, where advice and market navigation add the most value. These changes continue to redistribute volumes within the Ireland life and non-life insurance market while preserving the need for advice in higher complexity risks.

Direct carriers emphasize end-to-end digital claims handling and straight-through processing, which benefits commoditized lines such as motor and household. Intermediated players deploy analytics to target retention and cross-sell, and to improve renewal conversations with NCID-referenced loss experience. Across both models, compliance readiness for IAF and CPC 2025 has become a differentiator in customer trust and operational resilience. The Ireland life and non-life insurance market continues to shift toward transparent pricing and product disclosure, which encourages channel competition on service and quality rather than inertia.

Geography Analysis

Regional variation in the Ireland life and non-life insurance market remains limited by the country’s compact geography and centralized regulation, but distribution patterns and claims experience differ across urban and rural areas. Dublin hosts many corporate headquarters and higher-income households, which concentrate group pensions and private health activity and underpin steady life and health flows. Standard Life’s 2024 research shows that retirement readiness varies across regions, with differences in financial and emotional preparedness that influence pensions and protection take-up. Health penetration is strongest where private hospital access and employer group schemes are dense, which reinforces non-life growth in metropolitan areas. Storm Éowyn highlighted coastal and western exposures through record wind gusts and widespread infrastructure disruption, which continues to inform pricing and underwriting focus in property. NCID disclosures and conduct standards apply uniformly nationwide and promote consistent market behavior across counties.

Outside Dublin, Leinster markets reflect higher pension savviness but also pressure from housing and childcare costs, which can defer discretionary cover decisions even at higher incomes. Munster benefits from resilient health infrastructure and targeted clinic expansions that increase access to day case and diagnostic services and help manage utilization. Connacht and Ulster exhibit lower congestion and different driving patterns, which can influence motor frequency trends relative to urban centers, while exposure to Atlantic wind events remains a key property consideration. Across regions, conduct reforms including differential pricing rules and extended renewal notices to support switching and reinforce price quality alignment for households.

The Ireland life and non-life insurance market continues to converge around consistent product standards while regional marketing and service models adapt to local needs. In urban centers, direct channels and digital advice gain traction as online comparison and consent rules reduce friction in switching and renewals. In less urbanized counties, agents and brokers keep a strong presence, where in-person advice remains preferred for farm, SME, and complex risks. Health insurers extend virtual care and clinic access to reduce geographic differences in specialist access and to manage chronic conditions. Pensions and protection are likely to show more even growth across regions as MyFutureFund normalizes contributions and creates a broader base of savers over time.

Competitive Landscape

The Ireland life and non-life insurance market is anchored by international groups and strong domestic incumbents that invest in digital platforms, analytics, and product innovation to compete on service and capital strength. Irish Life and New Ireland have advanced digital onboarding and advisor portals, which raise straight through processing rates and improve time to issue. Health insurers expand value propositions with clinic networks, rapid diagnostics, and preventive benefits that address outpatient demand and chronic pathways. Aviva’s commercial lines initiatives introduce property resilience cover for storm and flood, including mass timber propositions and energy efficiency rebuilding features, which align with corporate sustainability plans. RSA’s rebrand to Intact clarifies a unified operating identity across the region and underscores capacity in commercial and specialty classes.

Strategy execution emphasizes governance, customer trust, and speed. IAF implementation sets clear accountability expectations for senior executives, which leads carriers to upgrade conduct controls and documentation standards. CPC 2025 provisions encourage a more transparent customer experience, which in turn supports investments in self-service portals and in clearer product disclosures. On the commercial side, analytics and geospatial tools support property risk selection and pricing discipline in a tighter reinsurance environment shaped by Storm Éowyn. Across these initiatives, the Ireland life and non-life insurance market continues to reward disciplined underwriting, digital claims experiences, and credible sustainability enhancements in product wording.

New entrants and cross-border players extend competition in pensions and protection. Allianz Global Life received regulatory approval to offer PRSA and ARF products and is positioning for rollovers and contributions as auto-enrollment matures. Irish Life Health reported expanded day-to-day claims and new benefits in its 2024 SFCR, signaling a focus on outpatient and preventive pathways to manage medical inflation. AXA’s strategic plan highlights group-wide data and AI deployment for pricing, claims, and fraud controls, which feeds into Irish operations through shared platforms and methods. Together, these moves emphasize the scale benefits of multinational platforms while leaving space for domestic specialization in farm, SME, and regionally nuanced risks in the Ireland life and non-life insurance market.

Ireland Life and Non-Life Insurance Industry Leaders

Irish Life Group

Zurich Insurance plc (Ireland)

Aviva Life & Pensions Ireland

New Ireland Assurance

Royal London Ireland

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: MyFutureFund, Ireland’s auto-enrollment retirement savings system, launched with 763,000 employees and 104,000 employers enrolled in the first six weeks and over EUR 60 million in contributions, with the National Automatic Retirement Savings Authority overseeing delivery.

- October 2025: The Department of Enterprise, Trade and Employment released a comparative report on soft tissue injury awards and launched the IRB 2025 to 2029 strategy, underscoring remaining cost gaps with England and Wales while targeting greater settlement efficiency.

- July 2025: Allianz Global Life received approval to offer PRSA and ARF products to Irish consumers, expanding competition in pensions and retirement income.

- June 2025: Aviva GCS launched a unified Real Estate and Construction practice in the UK and Ireland with new resilient repair and mass timber features that speak to corporate sustainability plans and catastrophe resilience.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the Irish life and non-life insurance market as the gross written premiums collected by licensed insurers on protection, savings-linked, pension, and annuity contracts together with motor, property, health, liability, travel, marine, and other general lines where the underlying risk is situated in the Republic of Ireland. We count individual as well as group policies, and we value them at the point premiums are written.

We exclude cross-border reinsurance business that Irish-domiciled carriers book for foreign risks; we do not include captives or offshore special purpose vehicles.

Segmentation Overview

- By Insurance Type

- Life Insurance

- Non-Life Insurance

- Motor Insurance

- Health Insurance

- Property Insurance

- Liability Insurance

- Other Insurance

- By Customer Segment

- Retail

- Corporate

- By Distribution Channel

- Brokers

- Agents

- Banks

- Direct Sales

- Other Channels

Detailed Research Methodology and Data Validation

Primary Research

We then interviewed underwriting heads, broker association officers, and insurtech executives across Dublin, Cork, and Galway. Their firsthand views on loss-ratio shifts, digital uptake, and the forthcoming auto-enrollment pension scheme validated assumptions and filled information gaps that desk work alone could not close.

Desk Research

We began by extracting quarterly premium and balance-sheet series from the Central Bank of Ireland, macro indicators from the Central Statistics Office, and population-age projections from Eurostat. Insurance Europe yearbooks, EIOPA Solvency II disclosures, and IAIS Global Insurance Market Reports supplied trend data on product mix, solvency, and claims severity.

Company financials from D&B Hoovers, news runs on Dow Jones Factiva, parliamentary papers, and trade-body briefs helped us verify carrier splits, regulatory milestones, and distribution-channel shifts. These references illustrate the range of secondary inputs; many additional public and proprietary sources informed data collection, cross-checks, and clarifications.

Market-Sizing & Forecasting

Our model starts with a top-down reconstruction of gross written premiums reported by the Central Bank and distributes them across life and non-life lines before applying coverage-specific penetration ratios confirmed in primary calls. Supplier roll-ups of sampled average premiums multiplied by policy counts act as a bottom-up reasonableness check. Key drivers, including new car registrations, private health expenditure per capita, disposable household income, population aged sixty-five plus, and annual dwelling completions, feed a multivariate regression that projects demand through the forecast period. Scenario analysis then adjusts for macro shocks, and any data gaps are bridged by extrapolating known carrier portfolios using mean growth.

Data Validation & Update Cycle

We run outputs through anomaly scans and peer review, after which senior analysts sign off. Models refresh once each year, with interim updates whenever material events trigger a new round of respondent outreach.

Why Mordor's Ireland Life & Non-Life Insurance Baseline Earns Reliance

We observe that published market values often diverge because analysts draw boundaries differently, refresh data at uneven intervals, or convert currencies on separate dates. Mordor's disciplined scope selection, annual refresh, and dual validation steps reduce those distortions and give buyers a dependable starting point.

Key gap drivers include whether pension-style life contracts are counted, how digital premiums are projected, and the depth of carrier sampling we apply.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 53.71 B (2025) | Mordor Intelligence | - |

| USD 40.33 B (2024) | Global Consultancy A | Excludes pension-linked life products and applies conservative digital-channel growth |

| USD 35.92 B (2024) | Market Research Boutique B | Relies mainly on public filings and omits group life premiums |

Taken together, the comparison shows we deliver a balanced, transparent baseline that traces every figure to clear variables and repeatable checks, giving decision-makers greater confidence.

Key Questions Answered in the Report

What is the projected size and growth of the Ireland life and non-life insurance market by 2031?

The Ireland life and non-life insurance market size is projected to reach USD 64.4 billion by 2031, expanding at a 3.1% CAGR from 2026 to 2031.

How will auto-enrollment through MyFutureFund influence insurers in Ireland?

MyFutureFund started in January 2026 and is channeling new contributions into long-term pensions, which strengthens life segments and creates cross-sell opportunities in protection products.

What impact have the Personal Injuries Guidelines had on motor and liability lines?

The guidelines have reduced non-litigated award levels and helped stabilize injury claims costs per policy, although litigation still drives higher costs and longer timelines.

Which distribution channels are growing fastest in the Ireland life and non-life insurance market?

Direct sales is the fastest growing channel as CPC 2025 promotes digital-first engagement, while brokers retain share in complex placements.

How did Storm Éowyn change underwriting and reinsurance dynamics?

The storm set a national record for insured losses in January 2025 and led reinsurers to tighten terms on flood and wind exposures, which influences pricing and capacity.

What are regulators prioritizing for insurers in 2026?

The Individual Accountability Framework and the Consumer Protection Code 2025 are top priorities, requiring stronger governance and clearer, digital-friendly customer protections.

Page last updated on: