Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

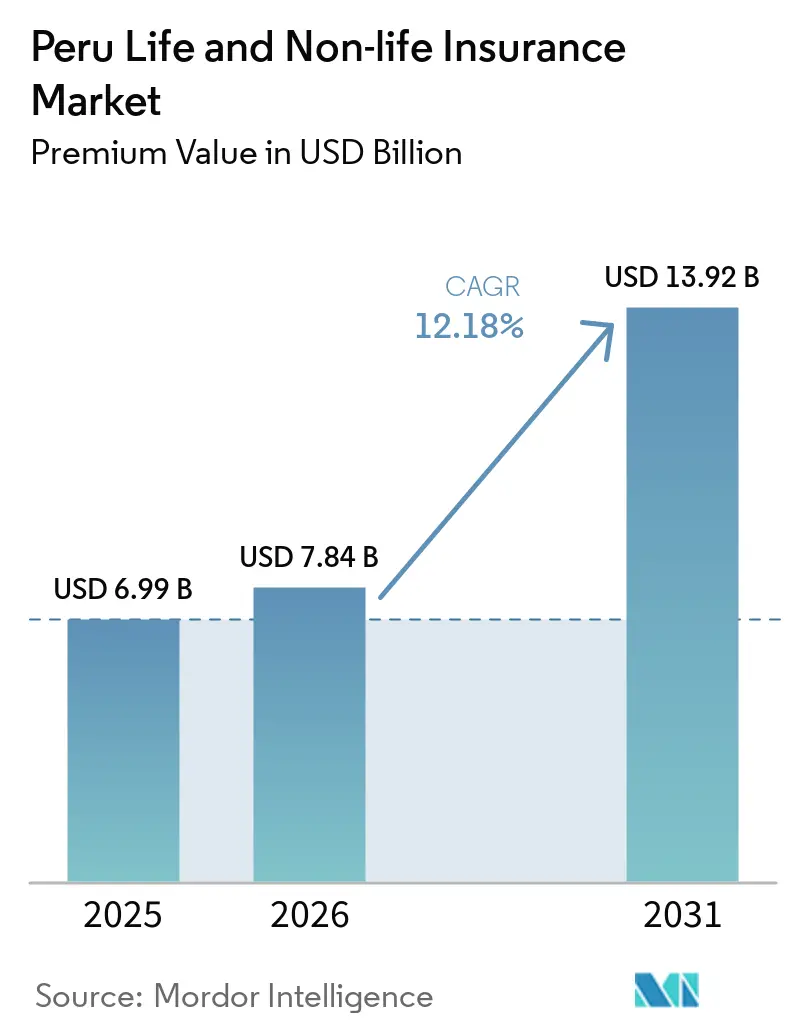

| Base Year Market Size (2025) | USD 6.99 Billion |

| Market Size (2026) | USD 7.84 Billion |

| Market Size (2031) | USD 13.92 Billion |

| Growth Rate (2026 - 2031) | 12.18% CAGR |

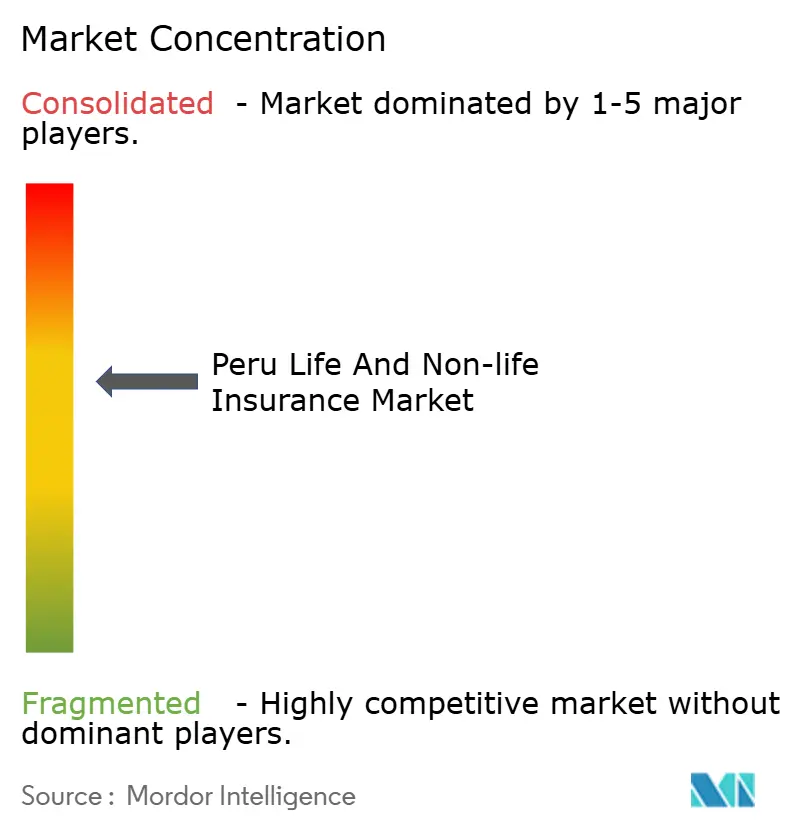

| Market Concentration | Medium |

Major Players.webp) *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Peru Life and Non-life Insurance Market Analysis by Mordor Intelligence

The Peru Life And Non-life Insurance Market size in terms of premium value is expected to increase from USD 6.99 billion in 2025 to USD 7.84 billion in 2026 and reach USD 13.92 billion by 2031, growing at a CAGR of 12.18% over 2026-2031.

Accelerating economic momentum, including the Ministry of Economy and Finance’s 4% GDP growth projection for 2025, underpins rising disposable income and expanding insurance uptake across personal and commercial lines. Non-life products continue to dominate because of compulsory SOAT motor cover, large-scale commercial activities in mining and agribusiness, and a supportive regulatory push for climate-risk analysis. Life insurance gains speed on the back of the 2024 pension reform that broadens annuity eligibility and raises retirement ages, while digital channels lower acquisition costs and improve product visibility. Collectively, these forces position the Peru life and non-life insurance market as one of Latin America’s fastest-growing protection ecosystems.

Key Report Takeaways

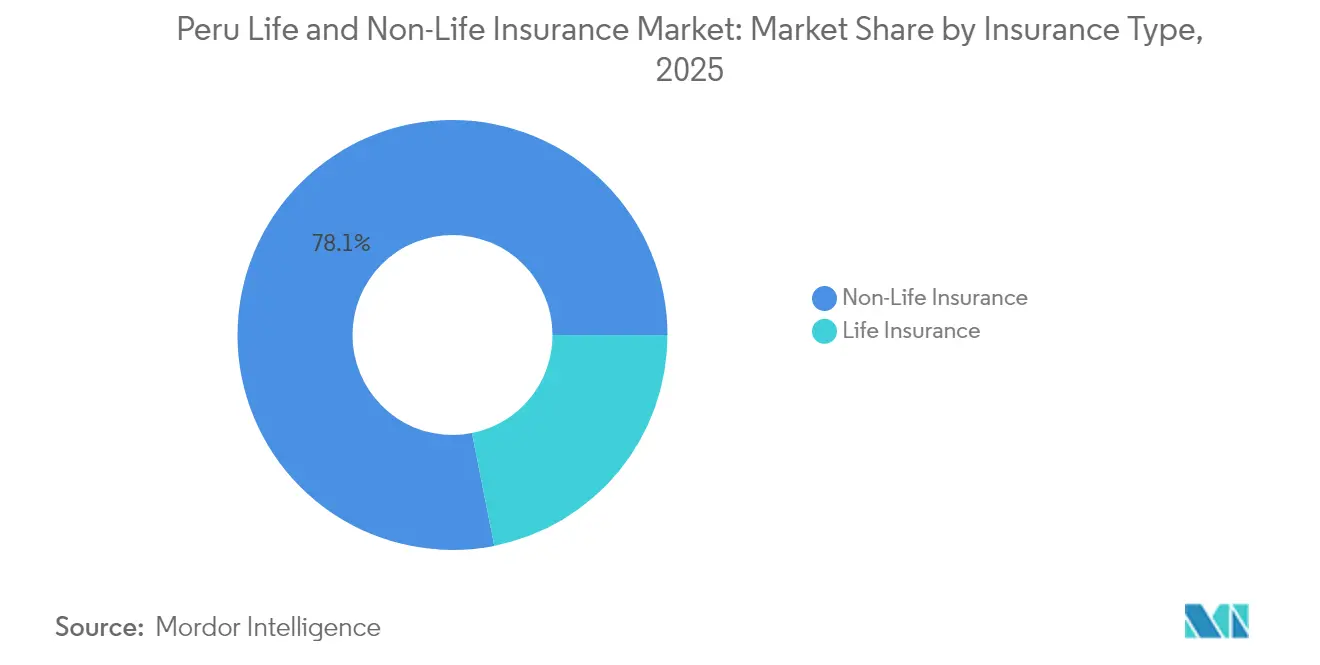

- By insurance type, non-life lines led with 78.12% of the Peru life and non-life insurance market share in 2025; life products are forecast to expand at an 11.42% CAGR through 2031.

- By distribution channel, bancassurance held 37.65% of the Peru life and non-life insurance market size in 2025, whereas direct online and InsurTech platforms are projected to post a 12.31% CAGR to 2031.

- By end user, individual consumers accounted for 59.05% of the Peru life and non-life insurance market size in 2025, while SMEs represent the fastest-growing segment at an 8.37% CAGR.

- By premium type, renewals captured 57.18% of the Peru life and non-life insurance market size in 2025; new business premiums are expanding at an 8.28% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Peru Life and Non-life Insurance Market Trends and Insights

Drivers Impact Analysis*

| Driver | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising middle-class income & insurance awareness | +2.8% | National; strongest in Highlands and major urban centers | Medium term (2-4 years) |

| Expansion of bancassurance partnerships | +2.1% | National; coastal regions and Lima cluster | Short term (≤ 2 years) |

| Mandatory SOAT motor cover & vehicle-parc growth | +1.9% | Nationwide | Short term (≤ 2 years) |

| Rapid InsurTech & digital-channel adoption | +2.3% | Urban hubs and secondary cities | Medium term (2-4 years) |

| Climate-resilient agriculture spurring crop covers | +1.2% | Highlands and agricultural regions | Long term (≥ 4 years) |

| Pension-system reform boosting annuity demand | +1.4% | National, with urban concentration | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Middle-Class Income & Insurance Awareness

Steady GDP growth and declining poverty continue to buoy the Peru life and non-life insurance market[1]Ministerio de Economía y Finanzas, “Marco Macroeconómico Multianual 2025-2028,” mef.gob.pe. Rising wages broaden consumers’ capacity to purchase voluntary covers, while public outreach after 2023 seismic events heightened risk perception and spurred demand for property and personal accident lines. Government-led connectivity programs lifted household internet penetration to 73% in 2024, improving access to online comparison tools and financial education portals. Public health coverage through SIS now reaches 97% of residents, showcasing how supportive policy can accelerate penetration. Insurers, led by the national association APESEG, have intensified educational campaigns that highlight earthquake and climate-related protection gaps, translating awareness into policy conversions.

Expansion of Bancassurance Partnerships

Banks remain central to the Peru life and non-life insurance market because customers already trust their institutions for savings and credit products. The 2025 divestment of CrediScotia to a multinational lender is set to unlock upgraded digital banking stacks and new cross-sell journeys. Mortgage, credit-card and micro-loan bundling strategies continue to push insurance attachment rates higher, supported by consumer-protection mandates from the Superintendencia de Banca, Seguros y AFP (SBS). Cost advantages also help: digital-first banks operate efficiency ratios near 30%, giving them latitude to price embedded covers competitively and still meet margin targets. As a result, bancassurance remains a benchmark channel even while digital-only outlets proliferate.

Mandatory SOAT Motor Cover & Vehicle-Parc Growth

Peru’s updated vehicle-registration decree of December 2024 requires RFID-enabled license plates for all M1 units, simplifying enforcement of SOAT compliance[2]Ministerio de Transportes y Comunicaciones, “Decreto Supremo 021-2024-MTC,” mtc.gob.pe. A parallel surge in new vehicle sales—supported by accessible credit lines—expands the non-life premium pool. Commercial fleets that service 13 newly certified agricultural export corridors face stricter verification requirements and now purchase multi-line policies that combine liability, cargo, and telematics-enabled risk-management modules. Digital verification APIs shorten policy issuance to minutes, cutting administrative overhead for both insurers and end users. Together, these measures sustain high renewal rates and attract tech vendors keen to integrate real-time compliance checks.

Rapid InsurTech & Digital-Channel Adoption

An expanding FinTech ecosystem, home to more than 230 formally registered start-ups, accelerates experimentation in parametric weather cover, on-demand logistics insurance, and fully digital life onboarding. Investment rounds support open-architecture platforms that partner with incumbent carriers, allowing real-time quotation and automated claims. The SBS’s sandbox regime grants provisional operating approvals, enabling product pilots without excessive upfront capital requirements. With mobile data prices falling and e-wallet penetration widening, insurers report double-digit growth in direct online submissions, especially among under-40 consumers. For incumbents, co-innovation with InsurTechs now represents a strategic path to defend market share against nimble entrants.

Restraints Impact Analysis*

| Restraint | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High informality & low insurance literacy | -2.1% | National; pronounced in rural districts | Long term (≥ 4 years) |

| Cultural risk-aversion to property insurance | -1.3% | Highlands and traditional communities | Medium term (2-4 years) |

| Catastrophe-driven reinsurance cost inflation | -1.6% | National, with higher impact in disaster-prone regions | Medium term (2-4 years) |

| Slow healthcare reform curbing private health uptake | -0.9% | National, particularly affecting urban middle class | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Informality & Low Insurance Literacy

Roughly two-thirds of Peru’s workforce operates outside the formal economy, limiting pay-slip-linked and employer-sponsored coverage growth[3] International Monetary Fund, “Peru: 2024 Article IV Consultation,” imf.org . Low banking penetration—only 38% of adults hold an account—further restricts automatic premium debits. Although the digital-ID program “Cuenta DNI” is expanding basic financial access, rural areas still lean on cash transactions. Insurers respond by launching simplified micro-policies distributed through agricultural cooperatives, yet premium collection remains complex. Sustained progress needs broader structural reform, stronger consumer protection enforcement, and continuous financial-literacy outreach that translates online exposure into actionable coverage decisions.

Cultural Risk-Aversion to Property Insurance

In many mountain and coastal communities, informal mutual-aid arrangements substitute for formal insurance. Post-disaster relief often arrives in the form of government grants, reinforcing expectations of state intervention rather than private-sector solutions. Recent earthquakes that triggered public funeral-expense coverage under SIS illustrate this dynamic. Community-based adaptation projects supported by USAID and local NGOs are raising awareness of holistic resilience planning, but converting that awareness into policy uptake is an incremental process. Insurers increasingly pilot micro-property covers delivered through trusted local organizations to bridge the cultural gap while respecting established risk-sharing traditions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Insurance Type: Non-Life Dominance, Life Accelerating

Non-life products generated 78.12% of the Peru life and non-life insurance market size in 2025, anchored by mandatory SOAT, mining liability, and cargo lines. Motor cover benefits directly from RFID-plate reforms, while marine and transit policies gain scale through new agricultural export nodes. Health insurance receives momentum from updated essential health regulations that now include mental health diagnoses. Life insurance, although smaller, is on a steep 11.42% CAGR through 2031. Pension reform Law 32123 ushers in mandatory system entry at age 18 and lengthens contribution spans, driving demand for annuities and credit-linked life products. Leading carriers are modernizing underwriting with e-medical declarations, trimming issuance times from weeks to hours. Higher embedded-policy penetration in consumer finance is expected to narrow the non-life gap by decade-end.

Life cover growth further capitalizes on rising middle-class aspirations for inter-generational wealth transfer. Flexible premium holidays, micro-ticket life, and unit-linked arrangements appeal to young professionals wary of long-term commitments. Digital robo-advice tools, often co-branded with banks, help customers simulate retirement-income scenarios, strengthening engagement. Meanwhile, property and casualty insurers seek diversification by partnering with health-maintenance organizations to pilot hybrid protection-plus-prevention bundles that leverage telemedicine and wellness apps. These strategies enhance cross-sell potential and protect incumbents from single-line margin compression as competitive intensity climbs.

By Distribution Channel: Bancassurance Leads Yet Digital Surges

Bancassurance controlled 37.65% of the Peru life and non-life insurance market in 2025, leveraging bank branch footprints, data-driven cross-sell engines, and regulatory alignment around consumer-protection disclosures. The model benefits from integrated credit-life requirements in mortgage, auto, and SME loans, lifting attachment rates. However, direct online and InsurTech platforms are accelerating at a 12.31% CAGR, fueled by user-friendly interfaces, transparent pricing, and instant policy issuance. Digital wallets and e-commerce giants now embed micro-covers at checkout, converting first-time buyers at scale.

Agency and broker networks pivot toward advisory roles, focusing on complex commercial risks, employee-benefit schemes, and high-sum-assured life products. They increasingly rely on customer-relationship portals and API connectivity to maintain relevance in a self-service age. Retail affinity channels—telecom, supermarket, and fuel station tie-ups—offer in-person convenience and installment payments. Across all channels, omnichannel servicing becomes non-negotiable: chatbots handle low-complexity queries, while human agents concentrate on claims advocacy and cross-line planning. Such hybrid models aim to preserve the sector-leading renewal ratio that underpins profitability.

By End User: Individual Strength, SME Momentum

Individual policyholders represented 59.05% of the Peru life and non-life insurance market size in 2025, mainly through motor, personal accident, and micro-life products. Digital KYC and biometric verification have streamlined onboarding, lowering abandonment rates among young adults who value immediacy. Mass-market education programs reinforce the link between financial stability and insurance, further normalizing routine premium payments. Yet SMEs constitute the fastest-growing cohort, posting an 8.37% CAGR as business formalization accelerates.

Family farms and small processors—classified as SMEs—receive targeted crop, equipment, and liability packages designed for seasonal cash flows. Construction and services firms benefit from the 2024 expansion of mandatory workers’ compensation coverage from 200 to 270 activities, broadening the addressable employer pool. Larger corporations already buy sophisticated multi-line programs that integrate cyber, environmental, and business-interruption covers. To capture SME potential while preserving underwriting discipline, carriers deploy AI-driven risk-scoring models that combine tax-registration data with telematics and satellite imagery for property verification.

By Premium Type: Renewal-Driven Stability with New-Business Lift

Renewals accounted for 57.18% of the Peru life and non-life insurance market size in 2025, indicating satisfactory claims-handling and service levels. Automatic debit arrangements, loyalty bonuses, and no-claim discounts sustain persistency, especially in motor and health lines. From a working-capital perspective, renewals provide predictable cash flows that support capital adequacy ratios and fuel investment in digital modernization. New-business premiums, advancing at an 8.28% CAGR, reflect mandatory-cover expansions and the success of direct-to-consumer mobile apps.

Players emphasize straight-through processing, aiming to reduce underwriting touchpoints by half within three years. MAPFRE’s three-year strategic plan targets 6% compound revenue growth, underpinned by a nationwide mobile-training unit that promotes workplace safety and reduces loss ratios. Meanwhile, parametric crop protection continues to pilot in highland farming cooperatives, using weather-station triggers to deliver payouts within days, a feature popular among farmers accustomed to lengthy claims cycles.

Geography Analysis

Highlands provinces headline the geographic split, delivering the largest premium share and the highest regional CAGR. Rural road upgrades and 4G rollout have brought banking correspondents to secondary towns, significantly easing premium collection and claims servicing. Additionally, public-private irrigation projects stabilize crop yields, making weather-indexed covers more actuarially viable and encouraging farmer participation. Mining expansions continue to demand comprehensive property damage and business-interruption placements, with insurers leveraging satellite monitoring to improve underwriting accuracy. Growing domestic tourism also stimulates travel and accident covers, adding incremental premium streams that compound the region’s dominant position.

Costa zones, anchored by Lima, contributed to premium posting mid-single-digit growth. Regulators adopt tighter solvency and cybersecurity standards, prompting carriers to enhance capital buffers and invest in fraud-detection analytics. Earthquake shocks in 2024 renewed corporate interest in multi-hazard property policies, while upgraded port facilities amplify cargo throughput and associated marine cover. Lima’s concentration of IT-services firms drives demand for professional-indemnity and cyber-liability policies, areas where global reinsurers provide capacity and technical support. Despite slower top-line expansion than the Highlands, the Costa maintains higher average premium per policy, sustaining profitability.

The Selva (Amazon) region, though with the smallest share in premium, expands at high single digits as sustainable timber and ecotourism gain traction. Development agencies back micro-insurance pilots that bundle life, accident and weather benefits within community savings groups. Remote-sensing technologies assist insurers in mapping flood-prone zones, allowing tailored flood-parametric solutions that align payout triggers with river-gauge readings. Over the forecast horizon, improved transport links and renewable-energy projects are expected to draw larger commercial accounts, progressively elevating the region’s weight in the Peru life and non-life insurance market.

Competitive Landscape

Incumbents Rimac, Pacífico, and MAPFRE jointly hold a near-majority share, but competitive equilibrium is shifting as technology lowers entry barriers. Rimac pioneers broker-specific plans that offer flexible commission matrices, helping independent intermediaries defend value amid digital self-service growth. Pacífico leverages its hospital network to integrate preventive-care services into health policies, differentiating on wellness outcomes rather than pure indemnity. MAPFRE deploys AI-driven claims triage and the country’s first mobile risk-prevention unit, cutting workplace-accident response times.

More than 230 InsurTechs now operate locally, ranging from parametric crop-cover providers to usage-based motor start-ups. Zuru Logistics, for instance, supplies on-demand freight insurance backed by established carriers, showcasing a partnership path rather than outright disruption. Foreign insurers view Peru as a regional hub, attracted by transparent regulation and high digital adoption. Reinsurers offer facultative capacity to support catastrophe-exposed lines, while local capital-market reforms allow insurers to match long-duration liabilities with infrastructure bonds, improving asset–liability management.

Regulatory modernization continues apace. Resolution 1233-2023 obliges all insurers to embed climate-risk stress testing in ORSA reports, favoring firms with sophisticated analytics stacks. A proposed national cybersecurity task force aims to standardize data-security protocols, indirectly raising compliance hurdles for smaller players. Meanwhile, consumer-protection norms push transparent disclosure and simplified wording, raising service benchmarks across the board. In this environment, scale alone is no longer sufficient; data agility, partner ecosystems and customer-experience excellence have become decisive competitive levers.

Peru Life and Non-life Insurance Industry Leaders

Rimac

Pacifico Seguros

La Positiva

Mapfre Peru

Interseguro

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: SBS raised the maximum coverage level for Peru’s Deposit Insurance Fund to reinforce consumer confidence and sector stability.

- May 2025: La Positiva extended its telemedicine platform across all individual and group health plans, deepening digital-care integration.

- May 2025: MAPFRE launched the country’s first mobile training unit that uses virtual-reality simulators to reduce workplace-accident risk.

- May 2025: Scotiabank Peru agreed to sell 100% of CrediScotia to Banco Santander, reshaping bancassurance alliances and digital-bank reach.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the Peruvian life and non-life insurance market as every new policy, measured in gross written premiums, that transfers mortality, morbidity, property, liability, or motor risk from individuals or organizations to licensed insurers operating under the SBS regulatory framework. According to Mordor Intelligence, this universe encompasses direct insurers, captives, and InsurTech carriers selling primary cover across retail and commercial lines.

Scope Exclusion: The model intentionally omits inward reinsurance treaties, self-insurance pools, and brokerage or TPA service revenues.

Segmentation Overview

- By Insurance Type

- Life Insurance

- Individual

- Group

- Non-Life Insurance

- Motor

- Property & Fire

- Marine & Cargo

- Health

- Personal Accident

- Agricultural

- Life Insurance

- By Distribution Channel

- Direct (Insurer Sales)

- Agency / Brokers

- Bancassurance

- Digital / Online

- Affinity & Retail Partnerships

- By End User

- Individuals

- SMEs

- Large Corporates

- By Premium Type

- New Business Premium

- Renewal Premium

- By Region

- Costa

- Highlands

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts conduct semi-structured calls with underwriters, bancassurance heads, digital brokers, and product regulators across Lima, Arequipa, and Trujillo. These conversations validate distribution weights, average premium per policy, and uptake of mandatory SOAT cover while revealing early shifts in micro-insurance and pension annuities.

Desk Research

We start with regulatory filings from Peru's Superintendencia de Banca, Seguros y AFP, premium statistics from the Central Reserve Bank of Peru, and household surveys from INEI, which anchor historic premium pools. Macro drivers come from IMF WEO, World Bank, and UN DESA. Trade association updates from APESEG, catastrophe loss data from DesInventar, and policy insights from OECD Insurance Outlook broaden context. Paid databases such as D&B Hoovers and Dow Jones Factiva help us parse company splits and news flow. This list is illustrative; many other public records and subscription sources feed our desk work.

A second pass reconciles currency conversions, one-off catastrophe impacts, and policy rule changes before the numbers move to modeling.

Market-Sizing & Forecasting

The baseline is built through a top-down reconstruction of gross written premiums by line, adjusted for retention ratios and policy lapses, which are then cross-checked through sampled average premium-times-policies bottom-up rolls. Key variables include vehicle parc growth, household disposable income, mortgage origination, life expectancy, inflation, and digital channel penetration. A multivariate regression projects each variable to 2030, and scenario analysis tests shocks such as El Niño-driven catastrophe losses or pension reform delays. Gaps in bottom-up data, for example, informal micro-policies, are bridged with calibrated factors derived from expert interviews.

Data Validation & Update Cycle

Outputs face anomaly scans, variance checks against peer country norms, and a two-level analyst review. Reports refresh every twelve months, with interim updates triggered by regulatory changes or events exceeding a preset premium-impact threshold.

Why Mordor's Peru Life & Non-Life Insurance Baseline Earns Confidence

Published estimates rarely match because firms differ on policy classes, currency timing, and refresh cadence. Our disciplined scope, annual refresh, and dual-track model keep the baseline consistent and transparent.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 6.99 B (2025) | Mordor Intelligence | - |

| USD 5.50 B (2024) | Global Consultancy A | Uses regional growth multipliers, limited channel coverage, narrower data year |

| USD 6.08 B (2024) | Industry Monitor B | Reports net premiums and includes inward reinsurance, omits micro-policy segment |

| USD 2.60 B (2023) | Trade Journal C | Tracks non-life only and an older base year, excludes life and annuities |

The comparison shows that scope breadth, data year alignment, and validation steps strongly influence headline values. Mordor Intelligence anchors its figure in regulator-verified premiums, cross-checks with field insight, and updates promptly, giving decision-makers a balanced, reproducible baseline.

Key Questions Answered in the Report

What is the current size of the Peru life and non-life insurance market?

The Peru life and non-life insurance market size reached USD 7.84 billion in 2026 and is projected to grow to USD 13.92 billion by 2031.

Which segment holds the largest share within the market?

Non-life insurance accounts for 78.12% of the Peru life and non-life insurance market share, mainly due to mandatory motor and commercial covers.

How fast is life insurance growing in Peru?

Life insurance premiums are forecast to post an 11.42% CAGR through 2031, supported by pension reform and rising household incomes

Why is bancassurance important in Peru?

Bancassurance controls 37.65% of the Peru life and non-life insurance market, leveraging existing banking relationships to embed protection products into loans and savings accounts.

Page last updated on: