Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

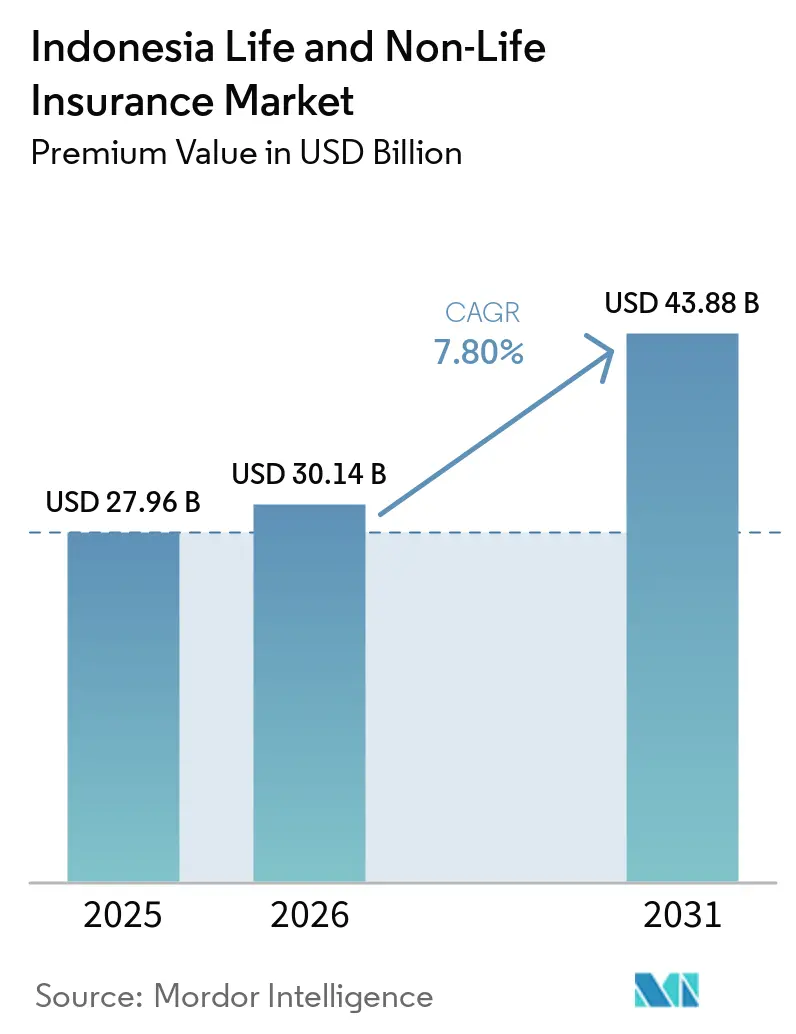

| Base Year Market Size (2025) | USD 27.96 Billion |

| Market Size (2026) | USD 30.14 Billion |

| Market Size (2031) | USD 43.88 Billion |

| Growth Rate (2026 - 2031) | 7.80% CAGR |

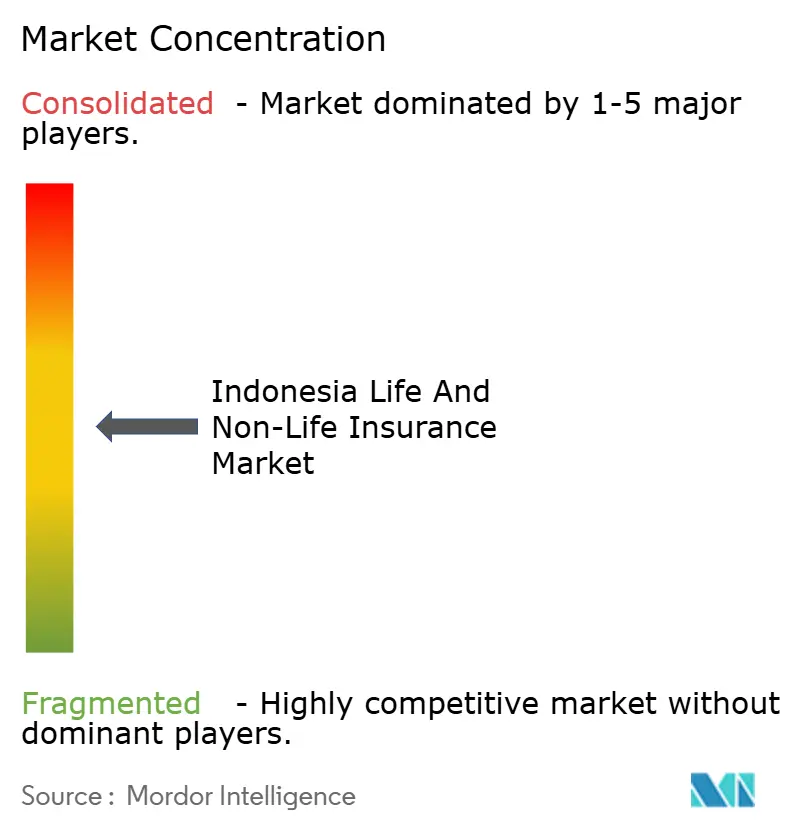

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Indonesia Life and Non-Life Insurance Market Analysis by Mordor Intelligence

The Indonesia Life And Non-Life Insurance Market size in terms of premium value was valued at USD 27.96 billion in 2025 and is estimated to grow from USD 30.14 billion in 2026 to reach USD 43.88 billion by 2031, at a CAGR of 7.80% during the forecast period (2026-2031).

The Indonesian life and non-life insurance market benefits from regulatory reforms that fully formalize digital distribution, strengthen prudential standards, and, in 2022, adopt IFRS 17, which enhances reporting quality and pricing discipline. Penetration remains structurally low even as reforms gather pace, which keeps long-term growth headroom intact relative to regional peers. The growth trajectory surpasses the historical CAGR of the late 2010s and early 2020s as modernization of distribution and oversight supports healthier premium expansion in 2026. OJK’s 2025 deployment of the Indonesia Insurance Agents Database and the Indonesia Insurance Policies Database improves agent verification and policy-level transparency, which reduces mis-selling risk and supports consumer confidence across the Indonesian life and non-life insurance market. The regulatory stance remains focused on prudential resilience, digital governance, and consumer protection as the Indonesian life and non-life insurance market scales beyond major urban centers in 2026.

Key Report Takeaways

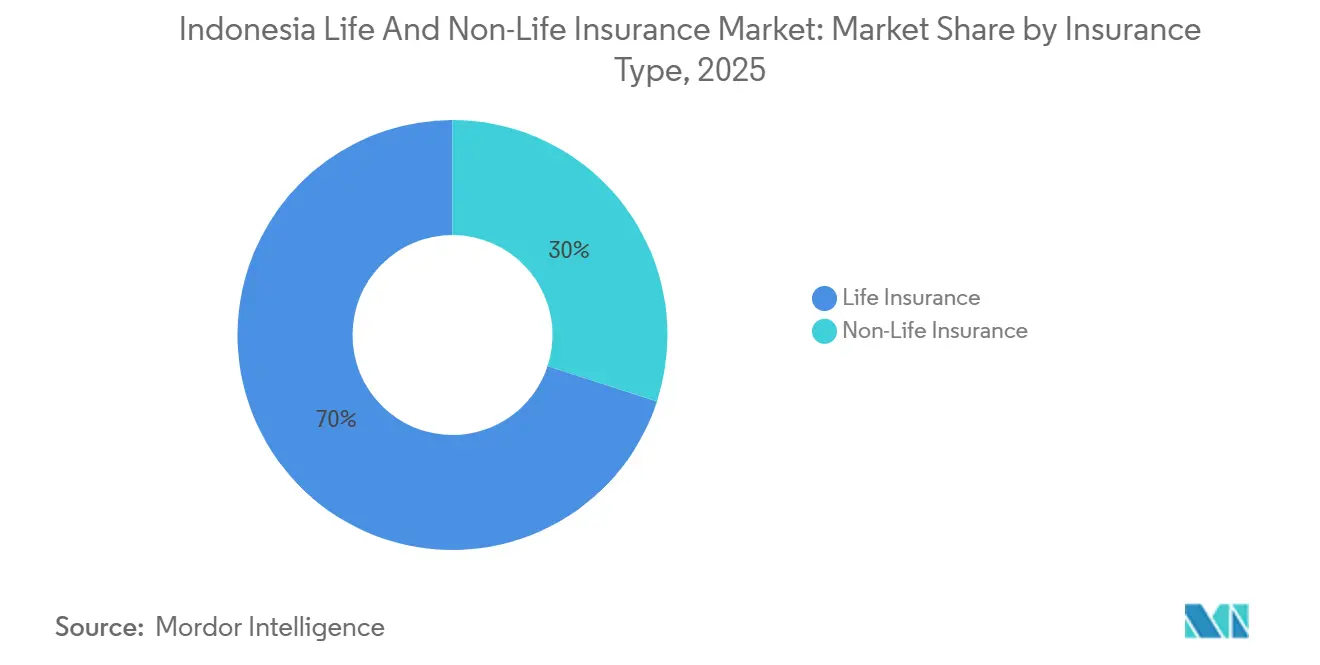

- By insurance type, life insurance led with 70% of the Indonesian life & non-life insurance market size in 2025, while non-life is projected to expand at an 11% CAGR from 2026 to 2031.

- By distribution channel, banks captured 33% of the Indonesian life & non-life insurance market size in 2025, while other channels are forecasted to grow at a 16% CAGR through 2031.

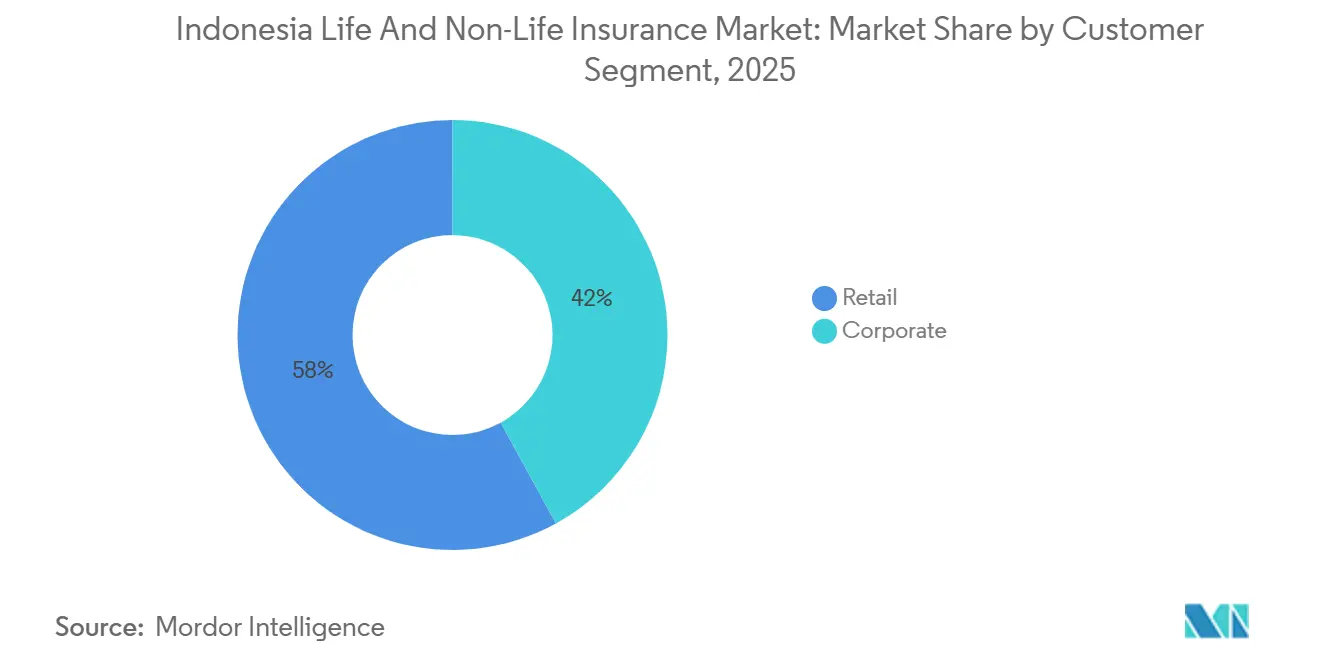

- By customer segment, retail accounted for 58% of the Indonesian life & non-life insurance market size in 2025 and is projected to record a 9% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Indonesia Life and Non-Life Insurance Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Digital Bancassurance Adoption Surging Post-OJK POJK No 38/2020 | +1.8% | National, with early gains in Jakarta, Surabaya, Bandung | Short term (≤ 2 years) |

| Mandatory BPJS Reforms Spurring Supplemental Health Policies | +1.3% | National, particularly in urban centres with formal employment | Medium term (2-4 years) |

| Climate-Induced Catastrophe Risk Elevating Property Cover Demand | +1.5% | National (Ring of Fire), highest impact in Jakarta, Java, Sumatra | Long term (≥ 4 years) |

| Syariah Finance Boom Catalyzing Takaful Product Uptake Outside Java | +1.2% | National, with a concentration in Sulawesi, Kalimantan, and Sumatra | Medium term (2-4 years) |

| PAYDI (Investment-Linked) Regulation Unlocking Unit-Linked Growth | +0.9% | National, urban middle class | Medium term (2-4 years) |

| E-commerce & Ride-Hailing Micro-insurance Expanding Risk Pools | +1.1% | National, particularly urban Java, and emerging secondary cities | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Digital Bancassurance Adoption Surging Post-OJK POJK No 38/2020

OJK’s modernization of distribution rules enabled product sales and servicing through electronic systems under an approval regime that requires registration as an electronic system provider and robust IT risk management, catalyzing a structural shift toward digital bancassurance in 2026. Partnerships illustrate the scale of this shift, including Prudential’s long-term bancassurance agreement with Bank Syariah Indonesia in late 2024, which opened access to a large syariah customer base for life and protection products in 2025[1]Prudential plc, “Prudential expands in ASEAN region via a strategic partnership with Bank Syariah Indonesia,” Prudential plc, prudentialplc.com. OJK’s June 2025 launch of the Indonesia Insurance Agents Database and the Indonesia Insurance Policies Database strengthens agent identity verification and policy-level oversight, which reduces mis-selling and improves complaint handling as volumes rise across the Indonesian life and non-life insurance market. IFRS 17 adoption requires more granular digital reporting, which supports profitability analytics and product mix optimization for bancassurance-led portfolios in 2026. Together, these changes are reducing friction across sales and service while deepening bank-insurer integration in the Indonesian life and non-life insurance markets.

Mandatory BPJS Reforms Spurring Supplemental Health Policies

The transition to standardized inpatient benefits under KRIS eliminates class-based differentiation in public coverage, which is motivating employers to adopt supplemental policies to maintain benefit competitiveness in 2026. Policy deliberations on co-payment structures have focused on sustainability and consumer protection as the regulator coordinates timelines and operating standards for health cover in the private system. Health-related premiums rose sharply in late 2024, which reflected rising demand for supplemental cover that complements the public scheme and employee benefit strategies. The scale of Badan Penyelenggara Jaminan Sosial (BPJS) assets highlights the footprint of public programs and the opportunity for add-on coverage as households move up the income curve and employers refine health benefits. These dynamics expand the insured base and reinforce premium growth within the Indonesian life and non-life insurance market.

Climate-Induced Catastrophe Risk Elevating Property Cover Demand

Indonesia’s multi-hazard exposure to seismic, volcanic, and extreme weather events continues to heighten risk awareness among corporates and households, underpinning demand for property, engineering, and catastrophe solutions in 2026. Coastal flood risk in Jakarta and subsidence pressures remain prominent, shaping demand for both traditional indemnity products and parametric concepts aligned with resilience planning[2]Otoritas Jasa Keuangan, “OJK Launches Database of Indonesia Insurance Agents and Indonesia Insurance Policies,” Otoritas Jasa Keuangan, ojk.go.id. General insurance premiums and the property line’s share rose into late 2024, supported by risk-transfer needs among corporations and SMEs following repeated large events. Public risk-financing tools, including pooled disaster funds and state asset insurance, provide a backstop and complement private coverage as authorities scale disaster-risk financing strategies. These conditions sustain growth in property-related lines and increase the relevance of catastrophe protection within the Indonesian life and non-life insurance market.

Syariah Finance Boom Catalyzing Takaful Product Uptake Outside Java

OJK’s roadmap mandates spin-offs of takaful windows into standalone entities by end-2026, which is raising organizational focus and product development in syariah lines across regions in 2026. A long-term bancassurance partnership between Prudential and Bank Syariah Indonesia expanded access to millions of customers and diversified distribution toward syariah-focused segments. New syariah entity build-outs and product launches have supported underwriting scale and asset growth, including the formation and expansion of dedicated syariah operations that reported rising assets and claims capacity in 2025. OJK targets faster premium growth outside Java, aligning with syariah demand in Sumatra, Kalimantan, and Sulawesi, and leveraging digital channels to compress distribution costs. This expansion broadens the risk pool and strengthens segment relevance within the Indonesian life and non-life insurance market.

Restraints Impact Analysis*

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Low Insurance Literacy in Eastern Provinces | -0.8% | National, concentrated in Papua, Maluku, and Nusa Tenggara | Long term (≥ 4 years) |

| POJK 14/2020 Solvency Hikes Pressuring Small Domestic Carriers | -1.1% | National | Medium term (2-4 years) |

| Motor Claims Fraud & Data-Quality Gaps Eroding Margins | -0.7% | National, particularly urban Java | Short term (≤ 2 years) |

| IDR Volatility Complicating ALM & Capital Buffers | -0.6% | National | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Low Insurance Literacy in Eastern Provinces

OJK and Statistics Indonesia are fielding the 2025 National Survey of Financial Literacy and Inclusion to update provincial indicators and guide targeted interventions where inclusion and literacy gaps persist[3]Otoritas Jasa Keuangan, “OJK Joins Hands with Statistics Indonesia to Conduct the National Survey of Financial Literacy and Inclusion 2025,” Otoritas Jasa Keuangan, ojk.go.id. UNDP’s inclusive insurance diagnostic highlights systemic gaps that expose households to unsuitable offerings and limit adoption in remote areas, which weakens the underlying demand for protection. A documented digital divide reduces the effectiveness of online education and enrolment, underscoring the need for omnichannel outreach and infrastructure improvements to lift take-up in outer regions. OJK’s agent database and policy registry raise conduct standards and enhance traceability, supporting consumer safeguards as the Indonesian life and non-life insurance market extends into less familiar segments. Until literacy improves, adoption will face headwinds in selected provinces of the Indonesian life and non-life insurance market.

IDR Volatility Complicating ALM & Capital Buffers

Historical evidence links rupiah depreciation with declines in equity values, which feed through to insurer portfolios and capital adequacy through asset valuation and credit conditions that affect corporate borrowers. OJK investment rules require life insurers to hold significant domestic government bonds, which stabilize cash flows but reduce natural currency matching for foreign exposures in certain products. Indonesia’s reinsurance balance has a net outward component, which can increase foreign-currency settlement needs following large events and magnify currency risk during periods of stress. IFRS 17 is sharpening ALM practices by clarifying profit drivers, encouraging closer matching and reinsurance strategies in the Indonesian life and non-life insurance markets. Currency and interest-rate volatility, therefore, remain structural constraints in selected books within the Indonesian life and non-life insurance market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Insurance Type: Balanced Maturation, Intensifying Non-Life Momentum

Life insurance held 70% in 2025, anchoring the Indonesian life and non-life insurance market with traditional protection products regaining ground under tighter conduct and disclosure standards for investment-linked business. A late-2024 rebound in bank-led unit-linked flows showed that revised governance can coexist with healthier demand, especially when partners strengthen advice journeys and disclosure quality. Elevated solvency buffers reported by OJK in 2025 support pricing and product redesign as IFRS 17 improves attribution of profit and risk across portfolios. Property, motor, and credit lines maintained relevance on the general side as enterprises recalibrate risk-transfer needs following repeated extreme events and higher awareness of asset exposures. This remix of protection and investment features is improving product resilience within the Indonesian life and non-life insurance market as 2026 unfolds.

Non-life is projected to be the fastest-growing segment, with a 11% CAGR from 2026 to 2031, as climate risk, health add-ons, and corporate risk-transfer needs lift demand beyond traditional motor lines. Property remains central in 2026, given hazard profiles and the growing awareness of risk financing in corporate and SME segments, backed by state disaster programs that complement private cover. Employers are increasing supplemental health protection after KRIS standardization, which raises the relevance of A&H within general books alongside accident and employer-focused offerings. IFRS 17 continues to refine pricing and reserve calibration across life and non-life, which should support steadier margins as insurers expand beyond legacy lines in the Indonesian life and non-life insurance market. These changes are guiding more data-driven underwriting and capital allocation across the Indonesian life and non-life insurance industry in 2026.

By Distribution Channel: Bancassurance Anchors, But Digital-First Challengers Accelerate

Banks captured 33% of distribution in 2025, as bancassurance remained the core engine of life premium flows, with combined branch and digital journeys tailored to customer risk tolerance. Life premium concentration in bank channels reflects structured advice, product tiering, and improved disclosure that aligns with OJK’s conduct expectations and IFRS 17 reporting in 2026. Prudential’s partnership with Bank Syariah Indonesia demonstrates how bank networks can unlock new customer segments and deepen syariah distribution to expand protection reach in 2026. OJK’s agent and policy databases, launched in mid-2025, help verify agent identity via QR codes and enable monthly policy reporting, thereby strengthening channel integrity and trust in the Indonesian life and non-life insurance market. These assets support hybrid bank-digital models that improve cross-sell, persistency, and service touchpoints across the Indonesian life and non-life insurance market.

Other channels are projected to grow at a 16% CAGR through 2031 as OJK’s digital service framework permits fully online underwriting and claims for approved products, provided system registration and staffing requirements are met. Embedded protection, mobile-first purchasing, and API-based partner distribution continue to expand reach in urban and secondary cities in 2026. Agent roles are shifting toward advice in complex cases, while digital identity checks and conduct rules reduce mis-selling and enhance supervisory oversight across the Indonesian life and non-life insurance market. IFRS 17 supports a channel mix shift toward metrics that emphasize value and persistency rather than headline premiums, which is improving product-channel fit in 2026. These channel dynamics signal continued convergence of bank-led and digital-first models in the Indonesian life and non-life insurance market.

By Customer Segment: Retail Commands, Yet Commercial/SME White Space Beckons

Retail customers accounted for 58% in 2025, making retail the anchor of the Indonesian life and non-life insurance market, as smoother digital buying journeys and rising financial literacy lift demand in 2026. Employer demand for supplemental health coverage is rising with KRIS implementation, which places a premium on easy-to-understand benefits and transparent claims for households. OJK’s supervision underscores consumer protection and conduct standards as coverage expands through digital channels and advisory models in 2026. Insurers are simplifying retail offerings to meet non-face-to-face distribution rules and to improve service in apps and partner platforms, thereby deepening reach into underinsured demographics across the Indonesian life and non-life insurance markets. Microinsurance remains a bridge for underserved segments, and UN analysis confirms a large latent demand that digital channels can unlock.

Corporate customers account for the residual share through group life, property, liability, and credit-related offerings, while OJK prioritizes risk-sharing improvements and governance across credit and guarantee lines relevant to SMEs. The social insurance system continues to expand coverage and assets, which opens complementary opportunities for employers and affinity groups to add protection in 2026. UNDP’s diagnostic stresses that inclusive insurance requires fit-for-purpose product design and claims processes to succeed outside major cities, which informs commercial product development for SMEs. IFRS 17 improves segment-level profitability analysis and encourages careful repricing and risk selection across both retail and corporate books in the Indonesian life and non-life insurance market. As disciplines tighten, cross-selling to SME owners and retail employees can drive deeper penetration of coverage in the Indonesian life and non-life insurance market.

Geography Analysis

Indonesia’s USD 30.14 billion premium pool in 2026 is concentrated in Java due to higher financial inclusion and dense bank networks that favour bancassurance, while OJK’s priorities support diversification into outer islands. The Indonesian life and non-life insurance market is positioned to benefit from road-mapped interventions that target faster growth beyond Java by leveraging digital distribution and inclusive insurance instruments. OJK’s agent and policy databases improve agent verification and policy-level transparency, which helps extend trusted distribution into secondary cities and rural districts across the Indonesian life and non-life insurance market. These digital assets encourage new product pilots and embedded partnerships that can tailor protection to local purchasing power and risk profiles as 2026 progresses. Collectively, these moves support a more balanced regional contribution to the Indonesian life and non-life insurance market over time.

Java’s risk intensity, dense urbanization, and infrastructure concentration keep property and A&H purchasing elevated, as hazard exposure underwrites a strong case for catastrophe-aligned products and risk-management services. Beyond Java, OJK’s spin-off mandate for syariah windows feeds a new generation of dedicated carriers and products targeted to local preferences, especially in Sumatra, Kalimantan, and Sulawesi, where uptake is rising. UNDP’s inclusive insurance work stresses practical claims processes, accessible premiums, and fit-for-purpose features to improve adoption outside major cities, which helps guide product development across the Indonesian life and non-life insurance market. The public disaster-risk financing architecture provides a backstop to private insurance, improving overall resilience in hazard-prone provinces in 2026. These elements continue to strengthen the foundation for diversified regional growth in the Indonesian life and non-life insurance market.

In the Eastern Provinces, infrastructure gaps and physical distance from financial service points constrain traditional channels, which validates OJK’s emphasis on digital governance, agent identity verification, and conduct standards to protect consumers as coverage expands. As data quality and agent oversight improve, mis-selling and claims friction can decline, which supports higher confidence among first-time buyers and underserved segments in 2026. Regulatory backing for parametric and other innovative risk-transfer tools supports agricultural and climate-sensitive regions, aligning risk solutions to local hazards and livelihoods. The Indonesian life and non-life insurance market is therefore set to broaden coverage beyond Java as digital readiness and targeted product design improve in 2026. Continued collaboration among regulators, carriers, and public programs will be central to unlocking sustainable geographic expansion in the Indonesian life and non-life insurance market.

Competitive Landscape

The market is moderately concentrated, with large life carriers holding a substantial share, but the top five across the combined Indonesian life and non-life insurance market do not approach the dominance implied by higher threshold bands.

OJK’s phased equity requirements through 2028 are accelerating consolidation discussions, especially among smaller firms that face higher compliance costs and need stronger capital bases under IFRS 17. The digital regulatory framework that permits fully non-face-to-face journeys is reshaping competitive dynamics by reducing distribution friction and enabling embedded models across large platforms in 2026. Data and conduct reforms, including agent verification and policy-level reporting, reinforce trust and reduce mis-selling risk as channels scale in the Indonesian life and non-life insurance market. IFRS 17 adoption continues to improve performance measurement, pricing, and capital planning, which supports more disciplined competition in 2026.

Distribution moves highlight the centrality of bancassurance and the rising importance of syariah. Prudential’s long-term collaboration with Bank Syariah Indonesia deepened distribution into large syariah customer bases and diversified beyond agency, which enhanced reach for traditional and hybrid products in 2025 and into 2026. Product development and unit-linked governance improvements supported a rebound in bank-led sales for leading carriers, aided by tighter disclosure and risk-profiling standards. On the technology front, Tokio Marine Indonesia introduced AI-enabled tools, real-time production tracking for agents, and new auto packages, signalling a drive to differentiate through agent productivity and digital service in 2025 and 2026. These distribution and technology strategies shape how incumbents defend their share and expand into new customer segments within the Indonesian life and non-life insurance market. As channel convergence progresses, advisory quality and consumer protection remain key competitive levers across the Indonesian life and non-life insurance market.

M&A and portfolio shaping continue to influence competitive positioning. Manulife’s agreement to acquire Schroders Indonesia aims to expand asset management capabilities in the country, which can support investment-linked product competitiveness and broader wealth solutions linked to protection[4]Manulife Investment Management, “Manulife Wealth & Asset Management to Acquire Schroders Indonesia,” Manulife Investment Management, manulifeim.com.hk. OJK’s actions to resolve distressed institutions, including the revocation of the Jiwasraya license in January 2025, underscore a consumer-first approach and a willingness to enforce prudential discipline when remediation fails. Regulatory focus on health product governance, data infrastructure, and ALM under IFRS 17 points to further standard setting across pricing and risk transfer in 2026. These moves collectively point to a more resilient competitive environment as the Indonesian life and non-life insurance market scales under tighter conduct and capital rules. Strategic partnerships, product remodelling, and disciplined ALM are likely to remain central themes in 2026 across the Indonesian life and non-life insurance market.

Indonesia Life and Non-Life Insurance Industry Leaders

PT Prudential Life Assurance

PT AIA Financial

PT Manulife Indonesia

PT Allianz Life Indonesia

PT AXA Financial Indonesia

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Hanwha General Insurance acquired a 61.5% stake in Indonesia’s PT Lippo General Insurance Tbk, consolidating its position in Southeast Asia. The acquisition, valued at 82.3 billion won (USD 57 million), strengthens Hanwha’s international insurance operations.

- September 2025: Manulife Wealth and Asset Management signed an agreement to acquire 100% of PT Schroder Investment Management Indonesia, which is expected to create a combined AUM of approximately USD 10.9 billion when closed, subject to regulatory approvals.

- July 2025: Manulife Indonesia launched Manulife PRIME (Protection Optimum Elite), a new life protection solution designed for liquid and valuable legacy planning, distributed through Bank DBS Indonesia branches with premium financing facilities available; the product addresses the complexities of cross-generational wealth transfer amid Indonesia's projected USD 83.5 trillion wealth transfer by 2048.

- February 2025: PT Asuransi Allianz Life Indonesia and PT Bank HSBC Indonesia launched Premier Plan Assurance, a new unit-linked life product for premier clients with features that include 100% premium allocation to investment funds from the first policy year and a persistency bonus.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study treats the Indonesia insurance market as the annual gross written premiums generated by licensed life and general (non-life) insurers, converted to U.S. dollars at yearly average rupiah rates.

Policies written offshore, captive reinsurance, and micro-takaful schemes under IDR 50 million are excluded to keep the scope comparable with OJK disclosure standards.

Segmentation Overview

- By Insurance Type

- Life Insurance

- Non-Life Insurance

- Motor Insurance

- Health Insurance

- Property Insurance

- Liability Insurance

- Other Insurance

- By Customer Segment

- Retail

- Corporate

- By Distribution Channel

- Brokers/Agents

- Banks

- Direct Sales

- Other Channels

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interview underwriting managers, bancassurance heads, insurtech founders, and actuarial consultants across Jakarta, Surabaya, and Medan.

These conversations clarify retention levels, average ticket sizes, and emerging risks (for example, mandatory motor TPL proposals) that raw desk data cannot capture alone. This allows us to stress-test early assumptions before numbers are frozen.

Desk Research

We start by collecting headline premium totals, solvency ratios, and line-of-business splits from tier-1 regulators such as OJK's monthly industry updates and its quarterly Financial Sector Development reports, which anchor the 2024 baseline at IDR 336.65 trillion premiums. Macro context is built from Statistics Indonesia household-income tables, Bank Indonesia interest-rate releases, World Bank penetration studies, and regional trade-association white papers. Company 10-Ks, investor decks, and reputable press help us trace product pricing shifts and channel share moves. Where needed, analysts tap D&B Hoovers for carrier financials and Dow Jones Factiva for deal flow and M&A cues. This list is illustrative; many additional open and paid sources are referenced during data validation.

Market-Sizing & Forecasting

We apply a top-down premium pool reconstruction using official life versus general splits. We then verify totals with selective bottom-up checks such as sampled motor-policy counts x average premium and health loss-ratio back-solves. Key drivers fed into the model include household disposable income, vehicle sales, property completions, medical inflation, and regulator-mandated minimum equity thresholds. A multivariate regression links these variables to historical premium growth and generates the base forecast, which is subsequently adjusted through scenario analysis for currency swings and catastrophic loss cycles. Data gaps in niche lines are bridged by weighted averages of peer disclosures and expert quotes, flagged for later refresh.

Data Validation & Update Cycle

Outputs go through three layers: automated anomaly flags, senior-analyst peer review, and a final lead-author sign-off.

We re-contact sources if variance exceeds preset bands and refresh the model annually, with interim updates triggered by material events such as cap-requirement changes or natural-disaster losses.

Why Mordor's Indonesia Life & Non-Life Insurance Industry Size and Share Research with Trends and Analysis (Segments, Regions) Baseline Deserves Trust

Published estimates frequently diverge because firms pick different premium definitions, currency conversions, or forecast windows.

One global consultancy cites a USD 51 billion 2024 market, inflating totals by folding in offshore reinsurance and pension-like products. A boutique provider quotes only USD 37.22 million for 2025 after limiting coverage to select digital channels. Our disciplined scope, OJK-anchored baseline, and yearly refresh cadence position Mordor's USD 25.53 billion 2025 figure as a balanced decision-making starting point.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 25.53 bn (2025) | Mordor Intelligence | - |

| USD 51 bn (2024) | Regional Consultancy A | Includes offshore covers and pension savings, uses aggressive FX assumptions |

| USD 0.04 bn (2025) | Industry Analysis B | Tracks only digital direct premiums, excludes agency and bancassurance pools |

In sum, by rooting forecasts in regulator data, validating inputs with field intelligence, and disclosing clear inclusions and exclusions, we provide a transparent, repeatable baseline that managers can rely on with confidence.

Key Questions Answered in the Report

What is the size and growth outlook for the Indonesian life and non-life insurance market in 2026 and beyond?

The Indonesian life and non-life insurance market size is USD 30.14 billion in 2026, with a forecast of USD 43.88 billion by 2031 at a 7.80% CAGR. This outlook reflects regulatory modernization, digital channel expansion, and improved data governance across carriers.

Which segment leads by insurance type within the Indonesian life and non-life insurance market?

Life led with 70% in 2025, while non-life is projected to be the fastest-growing segment at an 11% CAGR from 2026 to 2031 as climate and health-related cover gains momentum.

How are channels evolving in the Indonesian life and non-life insurance market?

Banks held 33% of distribution in 2025, and other channels are set to grow quickly thanks to OJK rules that enable fully digital, non-face-to-face underwriting and claims for approved products, backed by agent and policy databases that improve trust.

What regulatory changes most affect 2026 strategies in the Indonesian life and non-life insurance market?

IFRS 17 reporting, OJK's digital distribution approvals, and phased equity requirements are shaping product design, pricing discipline, and consolidation paths that influence 2026 strategies across carriers.

Where are the most promising geographic growth avenues within the Indonesian life and non-life insurance market?

OJK targets faster premium growth outside Java by leveraging digital channels and syariah spin-offs, with Sumatra, Kalimantan, and Sulawesi positioned for stronger uptake as distribution costs fall and tailored products expand.

Page last updated on: