Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 2.80 Billion |

| Market Size (2026) | USD 2.9 Billion |

| Market Size (2031) | USD 4.20 Billion |

| Growth Rate (2026 - 2031) | 7.40% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Malaysia Motor Insurance Market Analysis by Mordor Intelligence

The Malaysia Motor Insurance Market size in terms of gross written premiums value was valued at USD 2.80 billion in 2025 and is estimated to grow from USD 2.9 billion in 2026 to reach USD 4.20 billion by 2031, at a CAGR of 7.40% during the forecast period (2026-2031).

Expansion in the Malaysian motor insurance market is supported by risk-based pricing momentum under detariffication, which is encouraging product differentiation and better alignment of premiums with exposure. Digital road tax and licensing, together with API-based validation, have streamlined renewals and increased the utility of online channels for policy issuance and road tax bundling. Electric vehicle adoption is forcing underwriters to refine coverage for batteries, charging equipment, and specialized repairs, which is reshaping product design and claims operations, including EV-focused covers from leading carriers. Despite premium growth, underwriting pressure persists, as motor remained the backbone of general insurance, with a 42.8% share of industry premiums in the first half of 2025, yet posted a 102.2% combined ratio due to higher accident frequency and parts inflation[1]General Insurance Association of Malaysia, “Malaysia’s General Insurance Industry Posts 4.0% Growth,” PIAM, piam.org.my. The expansion of service tax on financial services to 8% from July 1, 2025, and earlier changes to taxable scope have further raised costs borne by policyholders and claims supply chains, making affordability and product mix management central to growth execution.

Key Report Takeaways

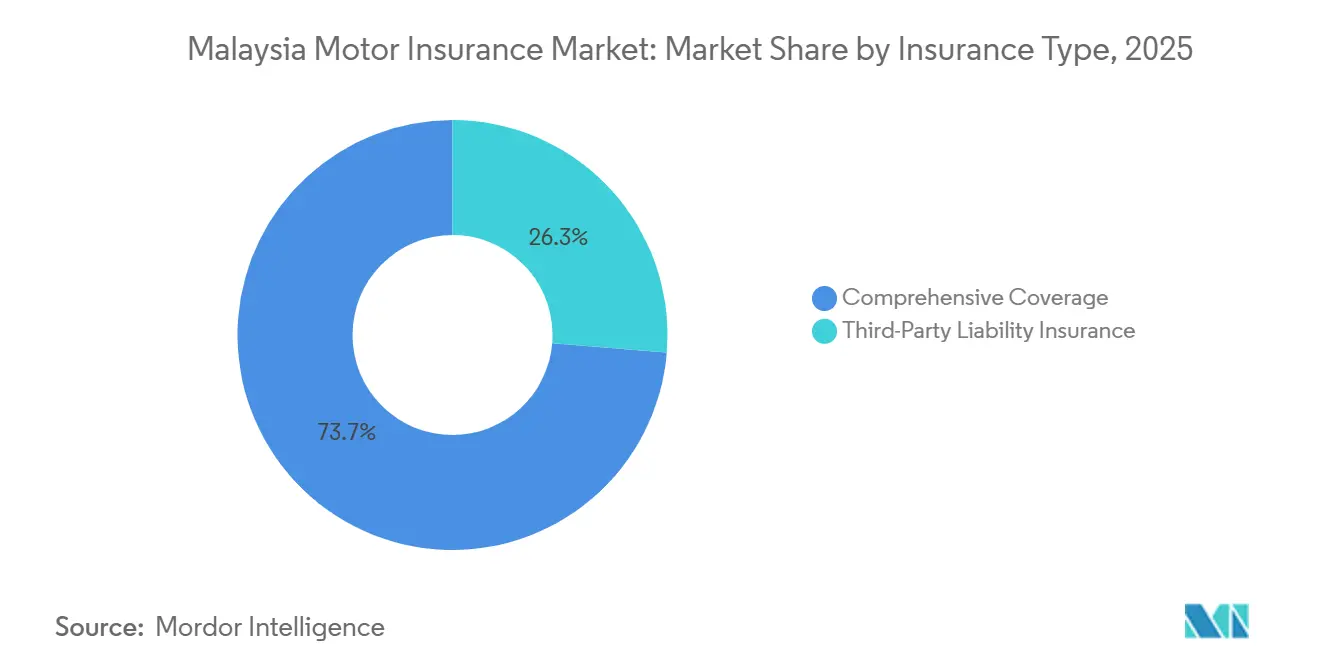

- By insurance type, comprehensive coverage led with 73.7% revenue share in 2025, while comprehensive with add-ons is forecast to expand at a 6.1% CAGR through 2031.

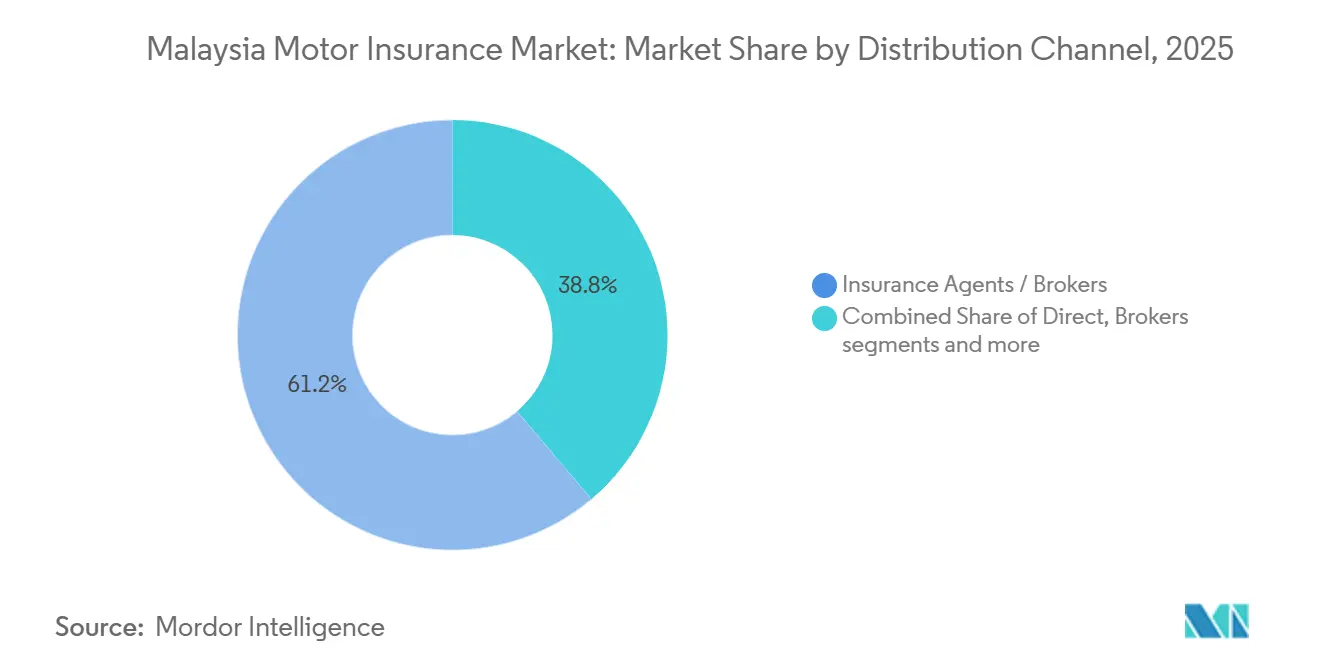

- By distribution channel, insurance agents and brokers held 61.2% of the Malaysian motor insurance market share in 2025, while online and digital channels are projected to record the highest CAGR at 13.4% through 2031.

- By vehicle type, passenger vehicles accounted for 74.4% of the Malaysia motor insurance market size in 2025, and commercial and light commercial vehicles are projected to advance at an 8.0% CAGR through 2031.

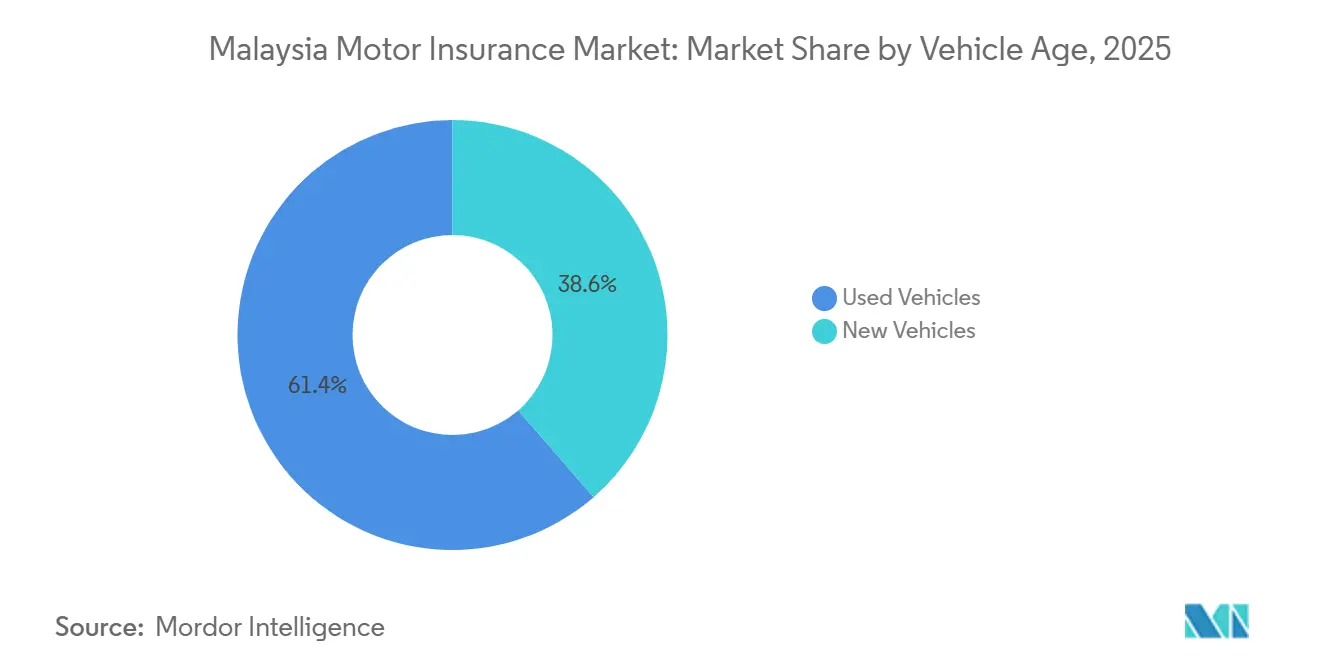

- By vehicle age, used vehicles held 61.4% share in 2025, while new vehicles are forecast to grow at a 7.1% CAGR through 2031.

- By geography, Peninsular Malaysia represented 84.4% of premiums in 2025, while Sabah and Sarawak are projected to grow at a 6.5% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Malaysia Motor Insurance Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Phased detariffication enabling risk-based pricing and new add-ons | +1.8% | National, with early gains in Klang Valley, Penang, Johor Bahru | Medium term (2-4 years) |

| EV uptake and EV-specific motor cover enhancements | +1.2% | Urban core, with spill-over to suburban Selangor | Medium term (2-4 years) |

| Digital direct and DITO licensing catalyzing online renewals and embedded flows | +1.5% | National, skewed toward Peninsular Malaysia's smartphone-enabled demographics | Short term (≤ 2 years) |

| Recovery in vehicle sales and higher insured values boost premiums | +1.1% | National, with stronger contribution from Peninsular Malaysia | Short term (≤ 2 years) |

| JPJ digital road tax/licence and API-driven renewal journeys reduce friction | +0.9% | National, leveraging MyJPJ adoption | Short term (≤ 2 years) |

| OEM/dealer insurance programs bundling at point-of-sale | +0.9% | National, concentrated at franchise dealerships for major brands | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Post-tariff liberalization accelerates product innovation & risk-based pricing

Malaysia’s shift to a liberalized tariff regime, initiated in 2016 and expanded in 2017, continues to enable premium setting based on granular risk profiles that consider driver demographics, vehicle safety technology, and localized perils like flood or theft exposure[2]Bank Negara Malaysia, “Liberalisation of Motor Insurance,” Bank Negara Malaysia, bnm.gov.my. This flexibility has unlocked product innovation, with market leaders offering usage-linked savings and expanded special-perils options that reflect the risk segmentation made possible by detariffication. Add-on covers for compassionate flood relief, towing, windscreen, and e-hailing endorsements have become more common, reinforcing attach rates within comprehensive policies and supporting value migration in the Malaysian motor insurance market. The regulator has complemented liberalization with consumer protection and governance expectations, including policy rules that reinforce pricing fairness and oversight of automated decision-making in underwriting workflows. These measures are material because underwriting performance has been under pressure, with motor posting a 102.2% combined ratio in first-half 2025, which underscores the need for data-driven pricing and superior risk selection to protect margins as competition intensifies. The result is a more dynamic Malaysian motor insurance market in which carriers that operationalize telematics, behavioral analytics, and transparent add-on portfolios are better positioned to gain profitable share.

EV Uptake and EV-Specific Motor Cover Enhancements

Rising EV penetration has introduced new underwriting and claims considerations, especially around high-voltage batteries, specialized repair capacity, and charging-related risks that differ from internal combustion vehicles, pushing insurers to adjust premium relativities and coverage terms in the Malaysian motor insurance market. Product design now frequently includes protection for home wall chargers, portable charging cables, and liabilities associated with home and public charging events, alongside enhanced special-perils language for water ingress or electrical damage. As EV ownership expands in urban centers, carriers have started to formalize EV-ready panel networks to shorten repair cycles and control parts and labor costs that can be escalated for high-voltage systems. These EV measures are increasingly integrated into comprehensive-with-add-ons bundles, which are among the fastest-growing policy configurations in the Malaysian motor insurance market. As the EV ecosystem matures, players with robust claims protocols, vetted repair partners, and clear coverage for EV-specific components are likely to see stronger retention and cross-sell performance. The broader implication is that specialized EV propositions will remain a differentiator for customer acquisition in urban corridors where early adoption is concentrated.

Digital Direct and DITO Licensing Catalyzing Online Renewals and Embedded Flows

Regulatory movement toward licensing digital insurers and takaful operators has signaled support for technology-led models that operate with simplified front ends, modern cores, and embedded distribution in adjacencies, a trend that dovetails with the digital transformation of motor purchase and renewal journeys. The digitization of road tax and licensing, supported by API-based validation of active insurance, has reduced renewal friction and set the stage for end-to-end online flows that tie insurance issuance to road tax processing for both cars and motorcycles. Government-linked service platforms and private operators have further eased access to online renewals, payment options, and document delivery, which helps extend reach to digital-first consumers across Peninsular Malaysia. Incumbents have upgraded self-service portals to support digital issuance, recurring payments, and multi-rail transactions, directly competing with aggregators by closing user-experience gaps. As a result, online and aggregator channels are forecast to scale quickly, with online and digital distribution projected to grow at 13.4% CAGR to 2031 in the Malaysian motor insurance market. Embedded partnerships in banking and commerce ecosystems reinforce this trajectory by placing motor coverage at the point of need and simplifying recurring renewals.

Recovery in Vehicle Sales and Higher Insured Values Boost Premiums

Premium growth has been supported by higher insured values and model mix shifts, with more SUVs and higher-spec vehicles entering the on-road fleet, which lifts average sums insured for comprehensive covers in the Malaysian motor insurance market. In the first half of 2025, motor contributed an additional MYR 283 million (USD 69.82 million) in premiums, and industry commentary highlighted stronger EV and hybrid adoption as one of the drivers of premium flows alongside a steady recovery in new registrations. Financing-linked requirements also sustain comprehensive attach rates for new vehicles, reinforcing the dominance of comprehensive coverage in overall premium composition. Bancassurance and dealer channels contribute to this momentum by bundling coverage into delivery and loan processes, thereby streamlining onboarding and securing year-one policy capture. As these growth factors compound, comprehensive coverage is projected to maintain its leadership, with comprehensive with add-ons rising faster than base comprehensive due to climate- and usage-led add-on adoption. This dynamic supports the medium-term premium outlook while intensifying the need for disciplined underwriting to manage loss ratios as exposure shifts toward higher-value vehicles.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Repair and bodily injury claims inflation pressuring combined ratios | -1.4% | National, with acute pressure in urban corridors due to higher accident density | Short term (≤ 2 years) |

| Service tax hike to 8% dampening affordability and upsell | -0.8% | National, affecting all policyholders and claims settlements | Short term (≤ 2 years) |

| Low flood add-on take-up amid intensifying monsoon risk | -0.5% | Kelantan, Terengganu, Pahang, Johor, with episodic impact in Klang Valley | Medium term (2-4 years) |

| Operating cost controls capping intermediary remuneration and rebates | -0.4% | National, particularly affecting agent and broker networks in Peninsular Malaysia | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Repair and Bodily Injury Claims Inflation Pressuring Combined Ratios

Motor underwriting losses remained evident in first-half 2025, when the segment posted a 102.2% combined ratio as inflation in spare parts and higher accident frequencies weighed on results. Imported electronics and sensor-heavy components have contributed to cost escalation, while elevated bodily injury awards increased third-party liabilities and reserves across the Malaysian motor insurance market. To curb leakage and improve outcomes, industry and regulators introduced measures such as the Insurers and Takaful Operators-Repairers Code of Conduct and promoted digitalization around police reporting to address fraud and expedite claims. Insurers are also modernizing claims through direct repair programs, roadside assistance ecosystems, and digital tools that streamline triage and repair routing for motor claims. These operational responses are aimed at containing repair bills, reducing cycle times, and improving customer satisfaction while protecting portfolio loss ratios. Even so, sustained inflation and accident density in urban corridors suggest continued pressure that requires disciplined pricing and enhanced cost controls across the Malaysian motor insurance market.

Service Tax Hike to 8% Dampening Affordability and Upsell

The expansion of service tax on financial services to 8% from July 1, 2025, increased the tax burden on commission- or fee-based insurance services, resulting in higher outlays for policyholders and higher claims settlement costs when workshops pass the tax on parts and labor. For a MYR 2,000 (USD 493.48) motor premium, this change increases the service tax from MYR 120 (USD 29.60) at 6% to MYR 160 (USD 39.48) at 8%, a MYR 40 (USD 9.87) increase that can discourage discretionary add-ons among price-sensitive customers[3]Royal Malaysian Customs Department, “Guide on Financial Services Version 2,” Royal Malaysian Customs Department, mysst.customs.gov.my Source: CIMB Bank,. Industry associations advocated targeted relief, including exemptions for certain group covers to sustain protection levels for employees, which highlights the push to manage affordability alongside fiscal policy changes. In response, incumbents have tightened underwriting and leaned into direct and digital channels that can eliminate intermediary commissions, helping offset tax-driven price pressure for end customers. Selected carriers have also sustained healthy ratios through product and portfolio discipline, demonstrating that operating execution can cushion tax headwinds in the Malaysian motor insurance market. Over the short term, the 8% levy remains a headwind for upsell, particularly for betterment waivers and elective accessories that are not mission-critical to coverage adequacy.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Insurance Type: Comprehensive Add-Ons Lead Long-Term Value Migration

Comprehensive coverage held a 73.7% share in 2025 within the Malaysian motor insurance market, anchored by financing-linked requirements and strong attach rates for own-damage protection. Within this umbrella, comprehensive-with-add-ons is projected to grow at a 6.1% CAGR through 2031 as policyholders expand protection to include special perils, windscreen, and e-hailing endorsements that reflect evolving mobility patterns and climate risk. The emphasis on configurable add-ons allows carriers to tailor premiums to risk and value preferences under detariffication, which is a core pillar of product strategy across the Malaysia motor insurance industry. Leading providers market distinct add-on combinations, including compassionate flood relief, towing, roadside assistance, and accessories protection that address pain points often exposed during monsoon seasons. Usage-linked propositions such as cashback for lower mileage complement these add-ons, providing tangible savings to low-risk drivers while reinforcing retention among urban cohorts.

Third-party liability fulfills legal compliance for older vehicles and cost-conscious owners but faces persistent pressure from elevated bodily injury awards, which can increase loadings and narrow price differentials versus basic comprehensive covers. As a result, product teams are pairing pricing discipline with education on the risk of asset loss under third-party-only policies, nudging migration toward comprehensive plans as vehicle values and repair complexity rise. Expanded availability of EV-focused features within comprehensive products further differentiates value, especially for owners seeking charger and battery-related protection alongside standard benefits. Over time, comprehensive-with-add-ons is set to anchor margin defense due to higher premium capture and cross-sell headroom, while third-party-only portfolios require tighter claims governance to avoid adverse selection in the Malaysia motor insurance market.

By Distribution Channel: Aggregators and Embedded Platforms Disrupt Agent Dominance

Agents and brokers accounted for 61.2% of channel share in 2025, reflecting deep relationships and nationwide reach, while online and digital distribution in the Malaysia motor insurance market is forecast to rise at a 13.4% CAGR through 2031 as consumers seek transparent comparisons and instant issuance. Direct channels run by carriers continue to gain traction, with self-service purchase and renewal supported by diverse payment rails, automated reminders, and digital documentation that reduce friction versus offline pathways. Bancassurance has reinforced its position through long-tenor partnerships, such as exclusive arrangements formed post-mergers that unlock cross-sell at branch and digital fronts. Embedded distribution via financial super-apps and internet banking portals is also expanding, placing motor protection in the same workflow as vehicle financing and payments.

Aggregators and comparison portals have grown their presence alongside direct carrier sites, lowering search costs for buyers who prioritize price, coverage clarity, and speed. As digital road tax and licensing became mainstream, platforms and carriers integrated insurance validation into renewal sequences, tightening compliance and improving on-time renewals for both car and motorcycle owners. For incumbents, the strategic response has centered on omnichannel, keeping agents central for advice-led sales while building carrier-owned digital storefronts and curated bancassurance journeys that match aggregator convenience. In this setup, the Malaysia motor insurance industry is likely to see channel mix shifts as online and embedded options scale faster from a smaller base without fully displacing agents in complex or bundle-oriented sales.

By Vehicle Type: Commercial and Light Commercial Vehicles Benefit from E-Commerce Logistics Boom

Passenger vehicles led with 74.4% of premiums in 2025, while commercial and light commercial vehicles are projected to expand at an 8.0% CAGR through 2031 as delivery fleets and small business usage patterns become more formalized in the Malaysia motor insurance market. Product designs for vans and pickups often include load-related conditions, driver restrictions, and telematics options that help monitor usage intensity and promote safer driving. As businesses prioritize uptime, direct repair networks and courtesy vehicle programs have become differentiators for commercial users that cannot afford prolonged downtime. Carriers have also introduced tiered packages for commercial owners, spanning comprehensive, third-party fire and theft, and third-party covers, aligned to asset value and operating budgets. EV adoption among light commercial fleets is beginning to inform underwriting standards for batteries and charging assets, echoing developments in the private EV segment.

Two-wheelers, which include motorcycles used for commuting and last-mile delivery, remain a significant subsegment where affordable comprehensive options and special-perils add-ons can help manage flood exposure and theft risk. Insurers are investing in mobile-first journeys to simplify bike policy purchase and claims, mirroring digital trends in car insurance. For heavier commercial vehicles, compulsory excesses and stricter underwriting are common due to higher repair costs and liability exposure, prompting closer alignment between risk management practices and pricing. Telematics that monitor mileage, routes, braking, and speeding can support better pricing and claims management for mixed fleets, helping carriers and clients align incentives on safety. As these practices mature, commercial and light commercial segments are expected to outpace the overall market, supported by data-driven underwriting and service-level commitments that focus on business continuity in the Malaysia motor insurance market.

By Vehicle Age: New Vehicles Capitalize on OEM Bundling and Higher Financing Attach Rates

Used vehicles represented 61.4% of premiums in 2025, while new vehicles are projected to grow faster at 7.1% CAGR through 2031 as OEM programs and financing mandates sustain comprehensive attach rates in the Malaysian motor insurance market. Dealer programs at major brands standardize comprehensive coverage at delivery, which improves experience and retention by eliminating post-purchase friction on insurance selection. As new vehicles now carry advanced driver assistance features and higher electronics content, own-damage severity and repair complexity justify comprehensive coverage that is configured with windscreen, special-perils, and accessory protection. EV-ready add-ons are increasingly bundled at origination, ensuring charger and cable coverage is present from day one for eligible models. Over time, these OEM and finance-linked pathways will continue to consolidate new-vehicle capture for carriers with strong showroom integration.

For older vehicles, price sensitivity and depreciation drive a gradual transition toward third-party or basic comprehensive cover, which requires careful claims management to maintain profitability. To expand addressable reach, some carriers highlight online rebates and simplified digital journeys that reduce operating costs and maintain affordability for aging vehicle cohorts. Digital self-service for renewals and policy administration helps limit lapses among used-vehicle owners by providing convenient reminders and easy payment choices. Across both new and used segments, embedded and digital channels continue to gain traction by combining issuance with adjacent activities like financing, banking, or road tax renewal, which improves on-time policy maintenance in the Malaysia motor insurance industry.

Geography Analysis

Peninsular Malaysia accounted for 84.4% of premiums in 2025, while Sabah and Sarawak are projected to grow at 6.5% CAGR through 2031 as road connectivity improves and household incomes rise, broadening the addressable base for comprehensive protection in the Malaysian motor insurance market. Peninsular’s leadership reflects both population density and the concentration of distribution infrastructure that supports digital-first journeys and bank-linked channels. Digitized road tax renewal and integrated insurance validation now underpin smoother customer experiences across Peninsular states, which reinforces online purchase and renewal behavior. As urban centers see more EVs and high-spec vehicles, comprehensive-with-add-ons continues to deepen its share due to coverage needs aligned with technology-rich models.

In East Malaysia, the opportunity is defined by catch-up growth and the formalization of distribution networks that can serve smaller urban centers and towns. As federal and state projects improve travel times and open new corridors, agent networks and bancassurance partners can capture first-time and upgrade buyers seeking comprehensive protection for newer vehicles. Motor remains a key lever for customer acquisition and cross-sell, particularly when paired with digital self-service that reduces branch dependency and aligns with mobile usage patterns. Strengthening workshop networks and clear service-level agreements for claims can help carriers bridge perceived service gaps in less dense geographies. Over the forecast, Sabah and Sarawak’s contribution rises as comprehensive adoption and attach rates increase, supporting balanced growth for the Malaysian motor insurance market.

Flood exposure is a cross-cutting theme, with East Coast states facing seasonal monsoon risk and urban flash floods occasionally disrupting Klang Valley and other conurbations. Industry outreach and repairer protocols aim to curb fraud, expedite claims, and enhance safety, which supports confidence in special-perils add-ons for both private cars and two-wheelers. Carriers that market clear flood coverage language and simplified claims support are better positioned to convert awareness into stable add-on adoption. This, combined with digitalized road tax and licensing, underpins steady renewal discipline nationally and favors players with mobile-led experiences. As distribution strengthens in East Malaysia and digital journeys continue to scale in Peninsular states, the geographic mix should remain anchored in the west while delivering above-market growth in the east for the Malaysian motor insurance market.

Competitive Landscape

The Malaysia motor insurance market is moderately fragmented, with Liberty General Insurance Berhad, Allianz General Insurance Company, and Etiqa among the leaders; Allianz held a 14.9% share in Q1 2025, while Liberty became the largest auto insurer following its merger with AmGeneral and a long-term bancassurance tie-up. Scale advantages have enabled multi-brand, multi-channel strategies that combine agency networks with carrier-owned digital channels and exclusive bank partnerships. Regulatory expectations on fair treatment, governance, and transparency have sharpened focus on algorithmic pricing oversight and consumer outcomes in a fully detariffed environment. With underwriting pressure still evident, players are balancing growth in comprehensive with improvements in claims cost control and repairer collaboration to sustain healthy ratios.

Service innovation has become a differentiator. Allianz’s digital self-service and assistance ecosystem streamlines policy management, claims, and roadside support, while its EV Shield signals category leadership in emerging vehicle technologies. Etiqa emphasizes direct digital journeys and online rebates that sharpen price competitiveness and convenience for renewals and new purchases. Tokio Marine has enhanced digital motor purchase and policy management flows, expanding user choice in how and where to engage. Carriers are also tightening workshop and repairer programs and investing in data-driven claims operations that can reduce cycle times and leakage. These moves address recurring pain points in claims and servicing, which influence retention and cross-sell potential across segments in the Malaysia motor insurance market.

Strategic partnerships continue to shape distribution. Liberty’s post-merger portfolio spans agency, bancassurance, and dealer programs across major automakers and premium brands, which embeds motor coverage at the point of sale. Banks integrate motor propositions within digital financial journeys that bundle financing, payments, and insurance, improving attach rates and user experience. As online and embedded pathways scale, incumbents are prioritizing omnichannel orchestration to preserve agent-led advisory while capturing digital growth. Over the forecast period, technology readiness in pricing, claims, and distribution is likely to be the central axis that separates sustained share gainers from laggards in the Malaysia motor insurance market.

Malaysia Motor Insurance Industry Leaders

Etiqa Malaysia

Allianz Malaysia

Zurich Malaysia

Liberty General / Kurnia

MSIG Insurance

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: Liberty General Insurance Berhad organized the Many Colours of Malaysia Campaign from August 28 to September 30, 2025, offering new and existing customers who purchase or renew eligible motor insurance products a chance to win weekly consolation prizes and grand prizes based on creative postings, thereby amplifying brand visibility across Liberty, Kurnia, and AmAssurance portfolios post-merger.

- May 2025: Allianz Malaysia Berhad Group reported strong Q1 2025 results with insurance revenue of MYR 1.53 billion (USD 0.38 billion) and gross written premiums of MYR 2.01 billion (USD 0.50 billion), while Allianz General Insurance Company (Malaysia) Berhad posted Q1 2025 GWP of MYR 978.0 million (USD 241.31 million) and profit before tax of MYR 159.7 million (USD 39.4 million), maintaining market leadership with a 14.9% market share through strong motor and commercial business growth and an improved combined ratio of 85.8%, while also granting a one-time no-claim discount waiver and extending MYR 2,500 (USD 616.86) cash relief under the Allianz We Care campaign to eligible motor policyholders affected by the Putra Heights gas pipeline explosion.

- April 2025: Tokio Marine Insurans Malaysia Berhad launched comprehensive motor insurance products “Tokio Marine AutoPro” and “Tokio Marine BikePro” with digital purchasing via its website and introduced the MyTokioApp for policy management with features including instant coverage, quick claims, unlimited towing within Malaysia, and optional add-ons including special perils and cover for private electric chargers and charging cables.

- March 2025: Bank Negara Malaysia enforced its revised Fair Treatment of Financial Consumers policy, mandating AI governance and stricter service-level tracking in motor underwriting, compelling all insurers and takaful operators to tighten algorithmic pricing transparency and claims-handling protocols to ensure fairness and accountability in risk assessment and premium determination.

Malaysia Motor Insurance Market Report Scope

A motor insurance policy is a mandatory policy issued by an insurance company as part of the prevention of public liability to protect the general public from any accident that might take place on the road.

The Malaysian Motor Insurance Market is segmented by Insurance Type (Third Party Liability and Comprehensive) and by Distribution Channel (Agents, Brokers, Banks, Online, and Other Distribution Channels). The report offers market size and forecast values for the Malaysia Motor Insurance Market in USD million for the above segments.

By Insurance Type

| Third-Party Liability Insurance |

| Comprehensive Coverage |

By Distribution Channel

| Insurance Agents / Brokers |

| Direct Sales |

| Bancassurance |

| Embedded / Platform Partnerships |

| Aggregators & Comparison Portals |

By Vehicle Type

| Passenger Cars |

| Two-Wheelers |

| Light Commercial Vehicles |

| Medium & Heavy Commercial Vehicles |

By Vehicle Age

| New Vehicles |

| Used Vehicles |

By Geography

| Peninsular Malaysia |

| Sabah |

| Sarawak |

| By Insurance Type | Third-Party Liability Insurance |

| Comprehensive Coverage | |

| By Distribution Channel | Insurance Agents / Brokers |

| Direct Sales | |

| Bancassurance | |

| Embedded / Platform Partnerships | |

| Aggregators & Comparison Portals | |

| By Vehicle Type | Passenger Cars |

| Two-Wheelers | |

| Light Commercial Vehicles | |

| Medium & Heavy Commercial Vehicles | |

| By Vehicle Age | New Vehicles |

| Used Vehicles | |

| By Geography | Peninsular Malaysia |

| Sabah | |

| Sarawak |

Key Questions Answered in the Report

What is the size and growth outlook for the Malaysia motor insurance market through 2031

The Malaysia motor insurance market size is USD 2.8 billion in 2025 and is forecast to reach USD 4.2 billion by 2031 at a 7.4% CAGR during 2026-2031.

Which product and customer segments are set to grow fastest by 2031 in Malaysia motor insurance

Comprehensive-with-add-ons is projected to grow at 6.1% CAGR, commercial and light commercial vehicles at 8.0%, and new vehicles at 7.1% through 2031.

Which distribution channels will gain the most ground in the Malaysia motor insurance market

Agents and brokers held 61.2% in 2025, while online and digital channels are projected to grow at 13.4% CAGR to 2031. Digital road tax integration supports end-to-end online renewals that link policy issuance with road tax processing.

How are detariffication and digital insurer licensing changing pricing and competition in Malaysia

Detariffication allows risk-based pricing that reflects driver, vehicle, and location factors, which enables more precise premiums and product variety. Bank Negara Malaysias digital insurer and takaful agenda supports tech-led models that scale embedded and direct distribution.

What are the main profitability headwinds leaders should plan for in 2026

Motor posted a 102.2% combined ratio in first-half 2025 as accident frequency and repair costs stayed elevated. The 8% service tax on financial services raises costs for customers and supply chains, which pressures upsell and retention.

How does growing EV adoption affect products and claims in the Malaysia motor insurance market

Leading carriers now bundle coverage for batteries, home chargers, public charging liability, and roadside assistance tailored to EV use. EV-ready repair networks and product features like dedicated EV add-ons help manage severity and improve customer confidence.

Page last updated on: