Electronic Nose Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

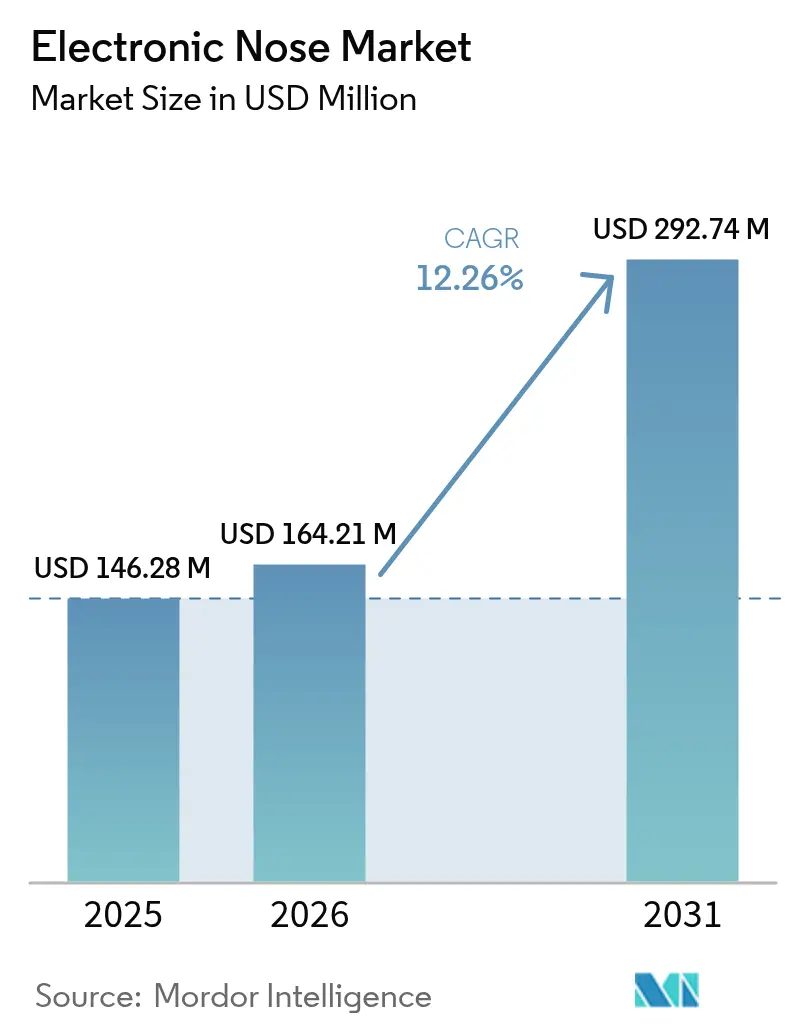

| Market Size (2026) | USD 164.21 Million |

| Market Size (2031) | USD 292.74 Million |

| Growth Rate (2026 - 2031) | 12.26% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Electronic Nose Market Analysis by Mordor Intelligence

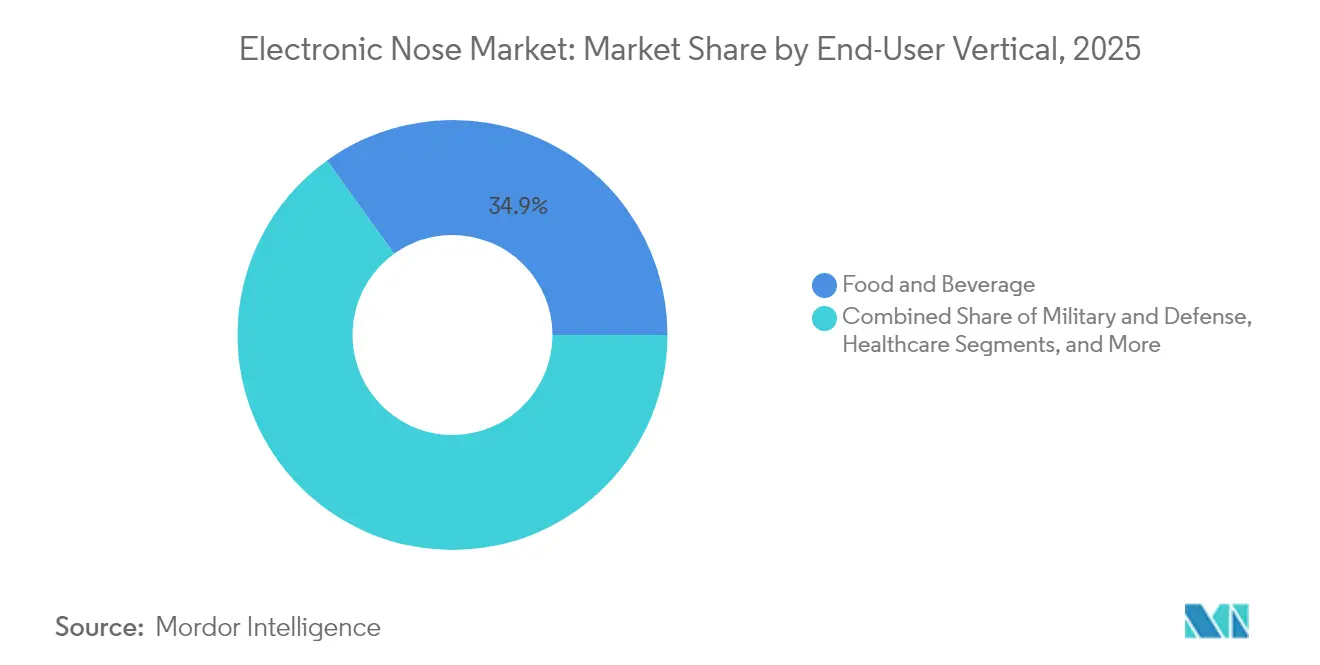

The electronic nose market size is expected to grow from USD 146.28 million in 2025 to USD 164.21 million in 2026 and is forecast to reach USD 292.74 million by 2031 at 12.26% CAGR over 2026-2031. Strong momentum arises from miniaturized MEMS sensor arrays, neuromorphic AI algorithms, and increasing deployment across healthcare, food safety, and environmental monitoring. High-speed odor detection now matches mammalian olfaction with millisecond response times, making the technology viable for real-time diagnostics. North America holds a 30.5% electronic nose market share in 2024 on the back of supportive regulatory frameworks for breath diagnostics. Meanwhile, the Asia-Pacific is the fastest-growing region at 14.0% CAGR, fueled by quality control demands in manufacturing and agriculture. Across end-user verticals, food and beverage commands 35.3% revenue while healthcare shows the highest 13.6% CAGR, driven by validated breath-based disease tests.

Key Report Takeaways

- By end-user vertical, food and beverage led with 34.92% revenue share in 2025, while healthcare is projected to advance at a 13.42% CAGR through 2031.

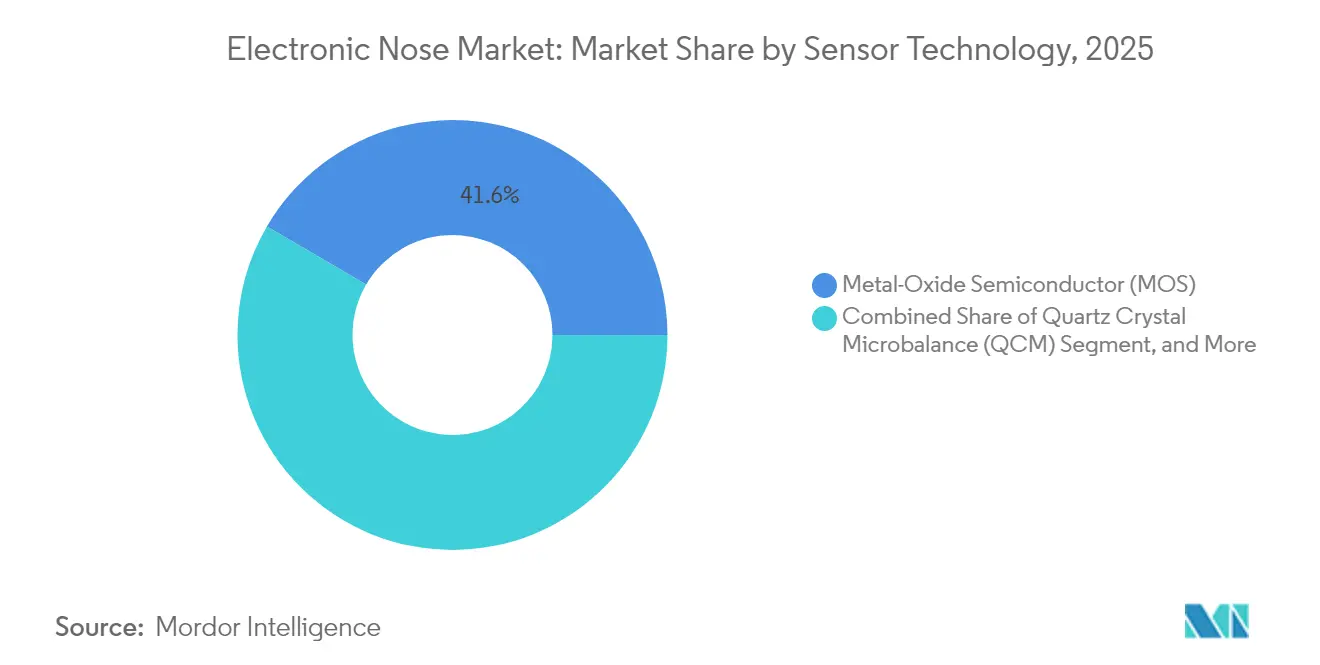

- By sensor technology, metal-oxide semiconductor arrays captured 41.58% of the electronic nose market share in 2025; field asymmetric ion mobility spectrometry is forecast to expand at a 13.68% CAGR to 2031.

- By application, quality control and shelf-life prediction accounted for a 32.18% share of the electronic nose market size in 2025, and disease diagnosis is moving forward at a 13.95% CAGR through 2031.

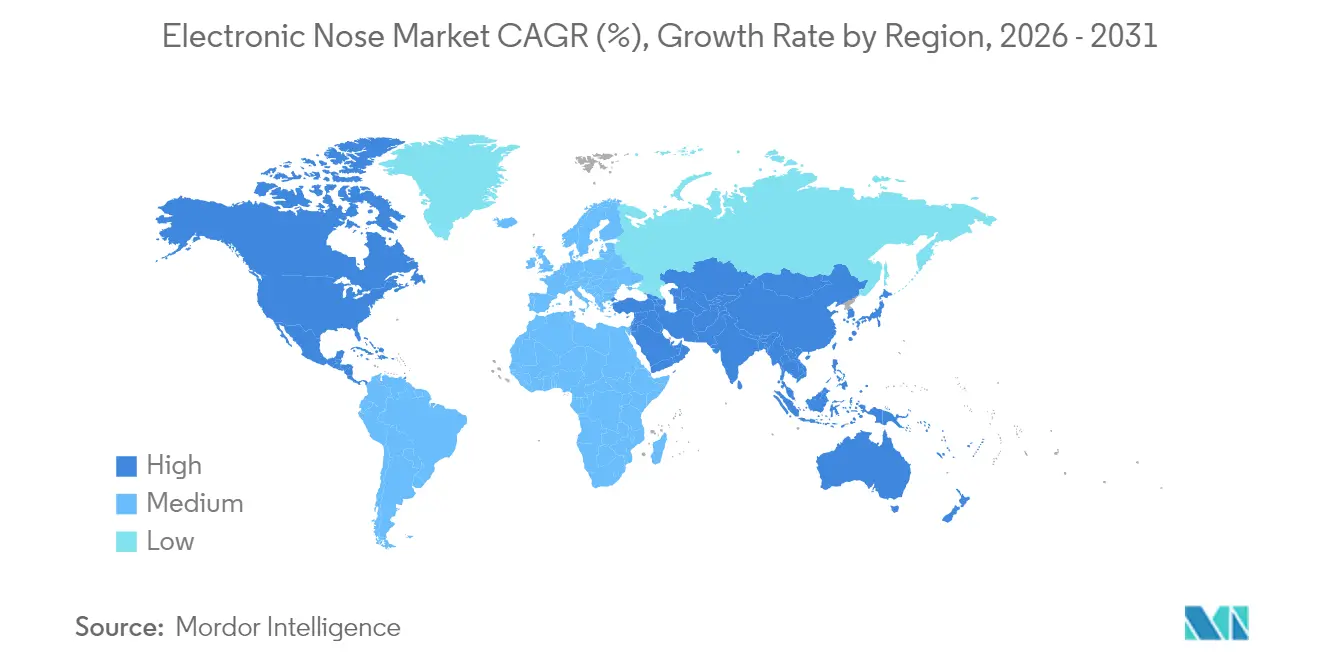

- By geography, North America held 30.12% revenue in 2025, whereas Asia-Pacific is tracking a 13.72% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Electronic Nose Market Trends and Insights

Driver Imapct Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Rapid miniaturization and cost decline of MEMS sensor arrays | +2.1% | Global (manufacturing centred in Asia-Pacific) | Medium term (2-4 years) |

| Integration of neuromorphic AI for real-time pattern recognition | +1.8% | North America and Europe leadership; Asia-Pacific adoption rising | Long term (≥ 4 years) |

| Heightened bio-security mandates in Agri-exporting nations | +1.4% | Global with focus on top exporters | Short term (≤ 2 years) |

| VOC-based disease diagnostics gaining regulatory fast-track | +1.7% | North America and Europe; global expansion | Medium term (2-4 years) |

| Odor-as-a-service platforms unlocking recurring revenue | +1.2% | Early uptake in developed markets | Long term (≥ 4 years) |

| Edge-to-cloud analytics lowering total cost of ownership | +1.5% | Global IoT environments | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid Miniaturization and Cost Decline of MEMS Sensor Arrays

MEMS-based systems now fit on credit-card footprints while maintaining >95% detection accuracy. Standardized semiconductor packaging and expanded wafer fabs in China, South Korea, and Taiwan have shaved 40-60% off unit costs since 2022. Tungsten-trioxide nanorod heaters enable 0.5–1 s identification, far outpacing legacy 10–30 s platforms.[1]Source: Nannan Zhang, “Smart E-Nose Uses Self-Heating Temperature Modulation,” phys.orgDuty-cycling strategies cut power draw to 160 µW at 250 °C, opening battery-operated and wearable use cases. The net result: entry barriers fall and the electronic nose market penetrates consumer electronics, telehealth, and smart-home ecosystems.

Integration of Neuromorphic AI for Real-Time Pattern Recognition

Spiking neural networks modeled on the mammalian olfactory bulb accomplish >97% classification accuracy with <16 ms latency on 1 mW ASICs.[2]Source: Anup Vanarse et al., “Application of Brain-Inspired Spiking Neural Networks,” mdpi.com Large-language-model extensions fuse chemical signatures with contextual metadata, sharpening selectivity for overlapping VOC profiles. Edge implementations trim cloud traffic, critical for hazardous-gas alerts in mining and process plants. Online active-learning loops counter sensor drift, keeping long-term accuracy above 90% without manual recalibration. These breakthroughs underpin the next wave of autonomous odor-analysis devices across defense, healthcare, and industrial safety.

Heightened Bio-security Mandates in Agri-Exporting Nations

Washington’s FY 2025 Chemical and Biological Defense Program budgets USD 1.66 billion toward advanced detection technologies.[3]Source: Office of the Under Secretary of Defense, “FY 2025 Justification Book,” defense.gov Electronic nose systems detect bark-beetle infestations at 95% accuracy, preventing multimillion-dollar timber losses in Europe and North America. Grain-storage operators deploy VOC sensors to isolate insect outbreaks and optimize fumigation timing. Export certificates in China, Brazil, and Australia increasingly require continuous olfactory monitoring to avoid trade disruptions. Integration with satellite crop-health data yields holistic bio-security dashboards, expanding the electronic nose market in smart-agriculture ecosystems.

VOC-Based Disease Diagnostics Gaining Regulatory Fast-Track

The FDA’s emergency authorizations for COVID-19 breath tests established precedent for expedited VOC-diagnostic approvals.[4]Source: Carrie Arnold, “Diagnostics to Take Your Breath Away,” nature.com Clinical trials on >10,000 patients achieved 93-98% accuracy in lung-cancer detection via breath, equaling gold-standard imaging. The NIOX platform’s clearance for asthma therapy monitoring further signals regulator openness to non-invasive olfactory tools. Governments in the EU, Japan, and Israel draft specific performance benchmarks, cutting time-to-market for medical device makers. Healthcare providers see cost reductions and patient-experience benefits, spurring hospital adoption and driving electronic nose market growth.

Restraints Impact Analysis*

| RESTRAINTS | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Sensor drift and calibration complexity in harsh environments | -1.9% | Global | Short term (≤ 2 years) |

| Data-privacy concerns for breath-biopsy health records | -1.3% | North America and Europe | Medium term (2-4 years) |

| Absence of harmonised global odour emission standards | -2.2% | Global | Long term (≥ 4 years) |

| Limited battery life in portable e-nose devices | -2.5% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Sensor Drift and Calibration Complexity in Harsh Environments

Metal-oxide sensors exhibit pronounced baseline drift under humidity and temperature swings, forcing quarterly recalibration that inflates operating costs.[5]Source: Anil Kumar, “Correction Model for Metal Oxide Sensor Drift,” ncbi.nlm.nih.gov Seven-year field studies confirm performance erosion necessitating sensor replacement in refinery stacks and landfills. Wavelet-decomposition and machine-learning compensation reach 100% identification over one-year horizons but demand embedded computing power, raising the bill of materials. While one-class drift schemes cut calibration samples by 70%, they still rely on controlled training cycles. Industries requiring 24/7 uptime, such as petrochemical processing, view these maintenance burdens as adoption barriers.

Data-Privacy Concerns for Breath-Biopsy Health Records

Breath analysis outputs are classified as protected health information under HIPAA and GDPR, obligating encryption, consent tracing, and localized data storage. Hospital CIOs cite integration challenges with electronic medical record systems that were never designed for high-frequency chemical fingerprints. Cross-border data flows complicate clinical trials for multinational device makers, adding legal overhead. Cybersecurity audits now form part of procurement checklists, elongating sales cycles. These factors temper short-term healthcare deployments, although emerging privacy-preserving federated-learning frameworks promise relief.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By End-user Vertical: Healthcare Drives Future Growth

Healthcare is projected to post a 13.42% CAGR through 2031. Breath-based oncology screening and asthma-monitoring devices drive demand, supported by favorable reimbursement pilots in the United States and Germany. Food and beverage remains the largest vertical, leveraging e-noses for meat freshness, wine oxidation, and dairy adulteration checks. Adoption spreads from processing plants to quick-service restaurants, integrating cloud dashboards for daily product audits.

Military, defense, and homeland security made up 9.05% revenue in 2025, propelled by toxic-gas detection requirements within NATO and Asia-Pacific defense modernization. Waste-management operators deploy odor sensors to comply with landfill emission caps in EU member states. Industrial safety and HVAC companies embed arrays in ventilation systems for 24/7 CO₂ and VOC tracking, reducing sick-building complaints. Overall, healthcare’s elevated CAGR positions it to eclipse food and beverage revenue post-2030.

By Sensor Technology: FAIMS Challenges MOS Dominance

Metal-oxide arrays held a 41.58% electronic nose market share in 2025 on account of proven reliability and sub-USD 1 per die pricing. Hybrid stacks incorporating tin-oxide and zinc-oxide nanoparticles deliver ppb-level sensitivity for formaldehyde and ammonia monitoring. Field asymmetric ion mobility spectrometry clocks a 13.68% CAGR as laboratories adopt it for high-selectivity breath diagnostics and explosive detection.

Quartz crystal microbalance sensors dominate moisture-sensitive applications like pharmaceutical blister-pack integrity, while conducting polymers attract wearables designers due to room-temperature operation. Emerging optical and photo-ionization detectors serve refinery and offshore platforms where intrinsic safety is mandatory. Machine-learning-driven sensor fusion tightens classification accuracy to 99% in complex odor matrices, reinforcing FAIMS' appeal in precision medicine.

By Application: Disease Diagnosis Transforms Market Dynamics

Quality control and shelf-life prediction 32.18% of the electronic nose market size in 2025, serving meat, dairy, spirits, and cosmetics producers. Cloud-based dashboards enable real-time pass/fail flags that sync with MES systems. Disease diagnosis, currently 10.62% of revenue, will expand at a 13.95% CAGR as clinical validation stacks up for lung cancer, COPD, and cystic fibrosis.

Hazardous-gas detection remains a core industrial safety segment with 11.67% revenue, fueled by stricter methane-emissions rules in North America and Europe. Indoor-air-quality monitoring benefits from the post-pandemic emphasis on ventilation and workplace wellness. Research and academic testing increase steadily as universities secure grants to explore VOC biomarkers for Alzheimer’s and sepsis.

Geography Analysis

North America generated 30.12% of the electronic nose market, underpinned by NIH grants and early FDA clearances for breath diagnostics. Defense and homeland-security spending on chemical-threat detection further stimulates demand. Academic-industry collaborations at institutions such as Stanford and MIT accelerate new-product pipelines.

Asia-Pacific is projected to clock the fastest 13.72% CAGR as China, Japan, and India digitize food-supply chains and smart-factory lines. Semiconductor manufacturing hubs in Taiwan and South Korea offer cost-effective fabs for MEMS die, lowering regional ASPs. Local start-ups in Shenzhen and Bengaluru use edge AI to tailor low-cost modules for curry freshness, rice-wine quality, and urban air pollution use cases.

Europe is sustained by EN 13725:2022 odor-emission enforcement that obliges industrial sites to deploy continuous monitoring. The region’s agri-exporters integrate e-noses in bio-security protocols to protect trade with the Middle East and Asia. In South America and the Middle East, and Africa, the demand for electronic nose is driven by agricultural export inspection and oil-and-gas methane detection respectively, albeit from a lower base.

Competitive Landscape

Market fragmentation remains moderate: the top five vendors. MSA Safety fortified its position with the USD 200 million takeover of M&C TechGroup, bolstering process-gas analytics. Owlstone Medical secured USD 2.3 million from the Cystic Fibrosis Foundation to accelerate breath-based pathogen tests, highlighting investor appetite for niche healthcare platforms.

SICK transferred 800 employees to a joint venture with Endress+Hauser to leverage shared gas-analysis IP for refinery and chemical customers. Envirosuite drew a USD 10 million minority stake from Hitachi Construction Machinery to merge odor-monitoring with ESG mining platforms. Sensirion’s methane-monitor partnerships with Intero – The Sniffers and Sensible EDP demonstrate targeted vertical solutions.

Start-ups such as Plasmion and Aryballe specialize in FAIMS and silicon photonics, respectively, pursuing OEM licensing rather than end-product sales. Large tech firms experiment with odor sensing for mixed-reality and autonomous-vehicle cabins, though still at research and development stages. Overall, value migrates toward software analytics and application-specific customization rather than commodity hardware.

Electronic Nose Industry Leaders

Alpha MOS SA

Owlstone Medical Ltd .

Airsense Analytics GmbH

Aryballe Technologies SAS

Envirosuite Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: MSA Safety completed the USD 200 million acquisition of M&C TechGroup, expanding its industrial gas-analysis suite.

- April 2025: Owlstone Medical secured up to USD 2.3 million from the Cystic Fibrosis Foundation for breath-based Pseudomonas detection.

- January 2025: Hitachi Construction Machinery invested USD 10 million (AUD 15.1 million) in Envirosuite, forming an ESG-focused mining alliance.

- November 2024: Sensirion Connected Solutions partnered with Intero – The Sniffers on methane-emissions monitoring in oil and gas.

Global Electronic Nose Market Report Scope

An electronic nose, a sophisticated device, can detect odors with greater efficacy than the human sense of smell. At its core, it features a mechanism designed for chemical detection. This intelligent sensing apparatus employs a selective array of overlapping gas sensors complemented by a pattern recognition component. The market is defined by the revenue generated by the sales of electronic nose devices globally.

The electronic nose market is segmented by end-user vertical (military and defense, healthcare, food and beverage, waste management (environmental monitoring), and other end-user verticals) and by geography (North America, Europe, Asia-Pacific, and the rest of the World). The market sizes and forecasts are provided in terms of value in USD for all the above segments.

| Military and Defence |

| Healthcare |

| Food and Beverage |

| Waste Management (Environmental Monitoring) |

| Industrial Safety and HVAC |

| Metal-Oxide Semiconductor (MOS) |

| Quartz Crystal Microbalance (QCM) |

| Field Asymmetric Ion Mobility Spectrometry (FAIMS) |

| Conducting Polymer |

| Optical and Photo-Ionisation |

| Disease Diagnosis (Breath Analysis) |

| Quality Control and Shelf-life Prediction |

| Hazardous Gas Detection |

| Indoor Air Quality Monitoring |

| Research and Academic Testing |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| South-East Asia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| By End-user Vertical | Military and Defence | ||

| Healthcare | |||

| Food and Beverage | |||

| Waste Management (Environmental Monitoring) | |||

| Industrial Safety and HVAC | |||

| By Sensor Technology | Metal-Oxide Semiconductor (MOS) | ||

| Quartz Crystal Microbalance (QCM) | |||

| Field Asymmetric Ion Mobility Spectrometry (FAIMS) | |||

| Conducting Polymer | |||

| Optical and Photo-Ionisation | |||

| By Application | Disease Diagnosis (Breath Analysis) | ||

| Quality Control and Shelf-life Prediction | |||

| Hazardous Gas Detection | |||

| Indoor Air Quality Monitoring | |||

| Research and Academic Testing | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| South-East Asia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

How large is the electronic nose market in 2026?

The electronic nose market size stands at USD 164.21 million in 2026.

What CAGR is projected for electronic nose solutions to 2031?

A 12.26% CAGR is forecast from 2026 to 2031.

Which region shows the fastest uptake of electronic nose systems?

Asia-Pacific is growing fastest at 13.72% CAGR due to manufacturing and agricultural applications.

Which sensor technology is gaining on MOS arrays?

Field asymmetric ion mobility spectrometry is advancing at a 13.68% CAGR, challenging MOS dominance.

Page last updated on: