Lyophilization Equipment And Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

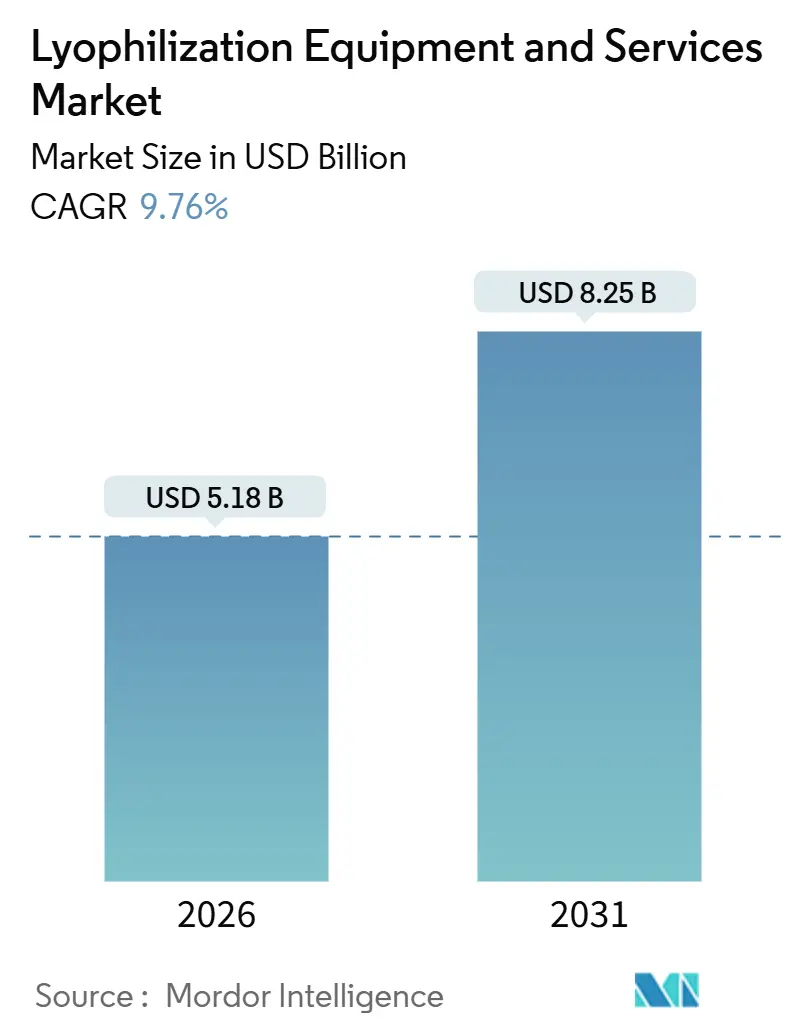

| Market Size (2026) | USD 5.18 Billion |

| Market Size (2031) | USD 8.25 Billion |

| Growth Rate (2026 - 2031) | 9.76% CAGR |

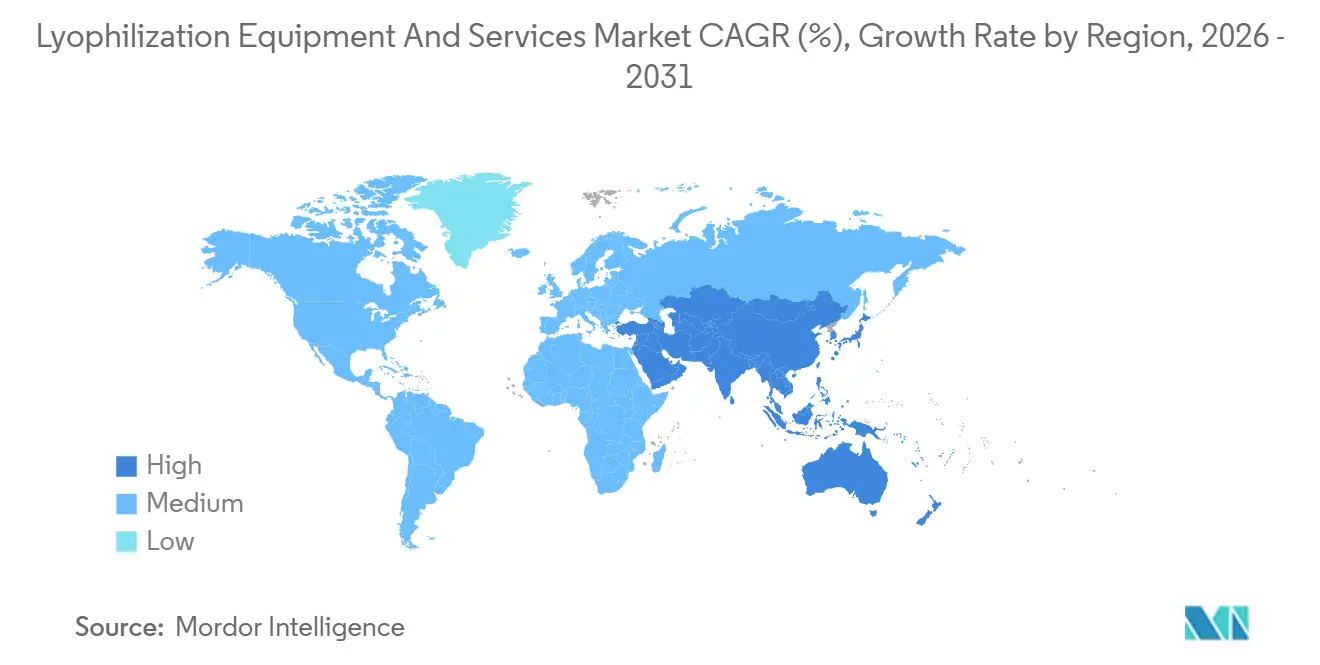

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Lyophilization Equipment And Services Market Analysis by Mordor Intelligence

The Lyophilization Equipment And Services Market size is estimated at USD 5.18 billion in 2026, and is expected to reach USD 8.25 billion by 2031, at a CAGR of 9.76% during the forecast period (2026-2031).

This growth outlook reflects the pharmaceutical sector’s shift toward biologics that require freeze-drying to maintain potency, the increase in contract manufacturing investments, and consistent demand from food processors seeking shelf-stable formats. Equipment suppliers are responding with natural-refrigerant systems and energy-saving cycles to comply with the European Union’s F-gas reduction mandate and corporate net-zero pledges. At the same time, contract development and manufacturing organizations (CDMOs) have announced more than USD 500 million of new capacity since 2024, reinforcing an ecosystem in which smaller sponsors rely on outsourced expertise rather than owning dryers outright. These themes collectively underpin a robust expansion path for the lyophilization equipment and services market.

Key Report Takeaways

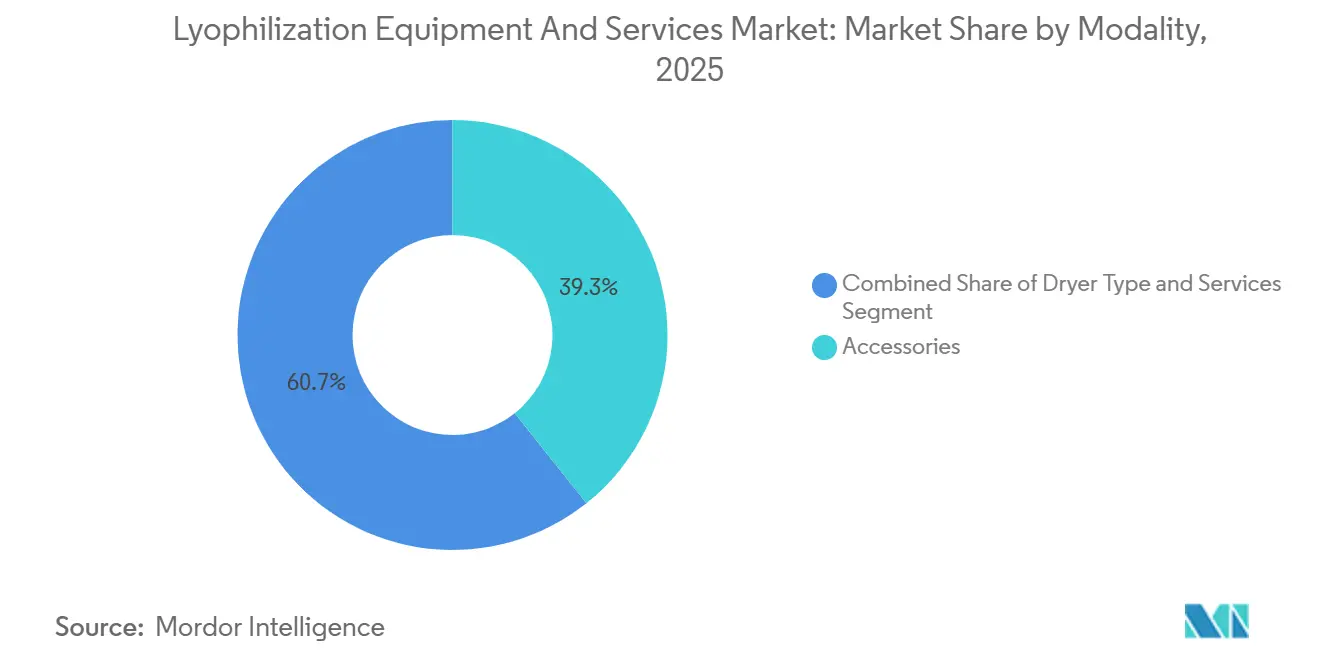

- By modality, accessories captured 39.28% revenue share of the lyophilization equipment market in 2025 while services are forecast to expand at a 10.29% CAGR through 2031.

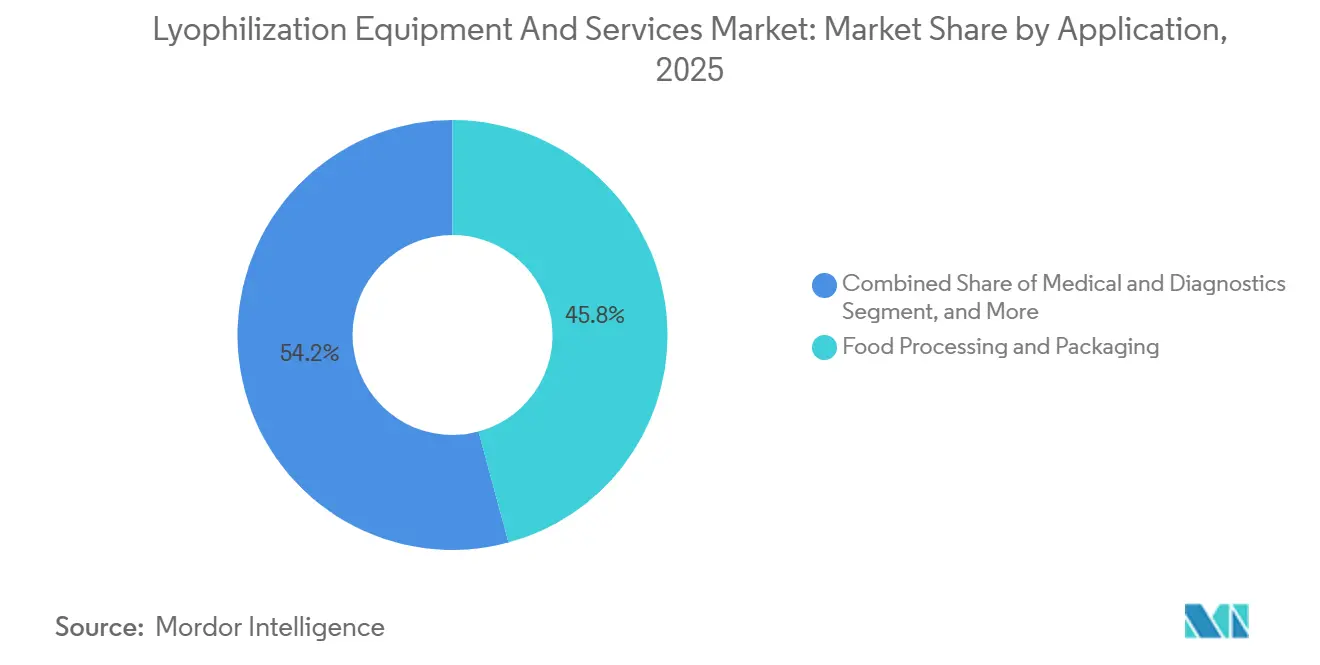

- By application, food processing accounted for 45.83% of the lyophilization equipment market size in 2025; medical and diagnostics is projected to advance at an 11.21% CAGR to 2031.

- By geography, North America held 36.86% of the lyophilization equipment market share in 2025, whereas Asia-Pacific is poised to grow at a 13.19% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Lyophilization Equipment And Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Demand for Lyophilized Biologics & Injectables | +2.8% | Global, concentrated in North America & EU | Medium term (2-4 years) |

| Expansion of Contract Lyophilization (CMO/CDMO) Capacity | +2.1% | North America, APAC core with spillover to EU | Short term (≤ 2 years) |

| Advances in High-Capacity Continuous & Microwave-Assisted Freeze-Drying | +1.5% | North America & EU early adopters, APAC followers | Long term (≥ 4 years) |

| Cold-Chain-Independent Vaccine Distribution Initiatives | +1.3% | Sub-Saharan Africa, South Asia, Latin America | Medium term (2-4 years) |

| Sustainability Incentives for Energy-Efficient Lyophilizers | +1.2% | EU primary, North America secondary | Short term (≤ 2 years) |

| Personalised-Medicine Micro-Batch Requirements | +0.9% | North America & EU, limited APAC uptake | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Lyophilized Biologics & Injectables

Monoclonal antibodies, vaccines, and antibody-drug conjugates accounted for 68% of FDA biologics approvals in 2025, and most relied on freeze-drying to ensure multi-year room-temperature stability.[1]U.S. Food and Drug Administration, “Biologics Approvals 2025,” fda.gov Patent expiries accelerated biosimilar launches: Trastuzumab biosimilar Bisintex gained European approval in December 2024, and adalimumab biosimilars captured a 42% U.S. share by mid-2025, each emulating the originator's stability with lyophilized vials.[2]European Medicines Agency, “Human Medicines Highlights 2024,” ema.europa.eu Next-generation allogeneic CAR-T platforms are evaluating dry formats to avoid liquid-nitrogen logistics, potentially expanding required capacity by 15%-20% if commercialized at scale. Moderna disclosed pilot sugar-glass drying for mRNA vaccines in its 2024 10-K, signaling that nucleic-acid modalities may also pivot to freeze-drying. These pipelines directly swell order books for the lyophilization equipment and services market.

Expansion of Contract Lyophilization Capacity

CDMOs have outpaced in-house investments three-to-one since 2024, a pattern underscored by Samsung Biologics’ Plant 5 build in Incheon and Lonza’s eight-dryer expansion at Visp in 2025.[3]Samsung Biologics, “Plant 5 Ground-Breaking Press Release,” samsungbiologics.com Vetter’s EUR 150 million project in Ravensburg added a high-speed line for pre-filled syringes, which command premium prices because aseptic freeze-drying prevents moisture ingress. Outsourcing eases capital burdens for start-ups yet concentrates know-how within a handful of service providers, reinforcing end-to-end offerings that now underpin a sizable share of the lyophilization equipment and services market.

Advances in High-Capacity Continuous & Microwave-Assisted Freeze-Drying

A University of Connecticut pilot demonstrated a belt-based continuous dryer that trimmed residence time from 48 hours to 12 hours for monoclonal antibodies while achieving 98% moisture removal. Regulatory pathways remain nascent because the FDA has not issued dedicated guidance; however, equipment vendors are preemptively patenting hybrid microwave-vacuum designs, such as IMA’s 2025 filing, to capture a first-mover advantage once standards mature. Commercial uptake, therefore, hinges on validation frameworks yet promises to raise throughput and reshape the lyophilization equipment and services market by 2028.

Cold-Chain-Independent Vaccine Distribution Initiatives

The World Health Organization updated its controlled-temperature-chain guidance in 2024, allowing lyophilized vaccines to withstand temperatures of up to 40°C for up to five days. Gavi earmarked USD 1.2 billion in 2025 to source such thermostable doses for 73 low-income nations. In response, the Serum Institute of India increased its Pune capacity by 40% and Biological E commissioned a new line in Hyderabad, both targeting WHO pre-qualification for heat-stable vaccines. Facility upgrades in emerging regions, therefore, enlarge the addressable base for the lyophilization equipment and services market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Capital & Maintenance Costs of Freeze-Dryers | -1.4% | Global, acute in emerging APAC markets | Short term (≤ 2 years) |

| Adoption of Alternative Drying Methods | -0.8% | North America & EU for heat-stable compounds | Medium term (2-4 years) |

| Tightening Fluorinated-Refrigerant Regulations | -0.6% | EU primary, North America secondary | Short term (≤ 2 years) |

| Shortage of PAT-Skilled Freeze-Drying Operators | -0.5% | Global, most severe in APAC | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Capital & Maintenance Costs of Freeze-Dryers

A 100 m² industrial tray dryer lists at USD 3 million to USD 5 million, and maintenance contracts consume up to 12% of the capital cost annually. Facility integration can add 30% due to HVAC and clean-room retrofits, as demonstrated by a 2024 Charleston project that spent USD 1.2 million on a single installation. Import tariffs of 15%-25% in India and Brazil elevate landed prices. At the same time, sparse local service networks increase downtime, prompting small firms to turn to CDMOs and limiting direct purchases in the lyophilization equipment and services market.

Adoption of Alternative Drying Methods

Spray drying accounts for roughly 18% of pharmaceutical drying tasks in 2026, being favored for heat-stable compounds and vaccines where reconstitution speed is secondary. GEA’s PHARMA-SD platform completes four-hour cycles, slashing production cost 60% for suitable formulations. Supercritical CO₂ and low-temperature vacuum drying nibble an additional share, especially for diagnostic enzymes. While these alternatives rarely match freeze-drying for biologic stability, they impose pricing pressure and incremental share loss on the lyophilization equipment and services market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Modality: Services Outpace Equipment as Outsourcing Deepens

Services generated the fastest growth in 2026 and are on track to post a 10.29% CAGR to 2031 as sponsors reallocate budgets from ownership to per-batch outsourcing. Accessories accounted for 39.28% of revenue in 2025, driven by a sizable installed base that requires vacuum pumps, SIP/CIP modules, and control upgrades. Lonza charges USD 150,000-USD 250,000 to validate a freeze-drying cycle, which is far less than the USD 3 million-USD 5 million required for an in-house dryer, encouraging smaller clients to outsource. CDMOs operating three dryers at 90% utilization achieve vial costs 40%-50% lower than single-dryer plants running at 60%, a structural advantage that expands the lyophilization equipment and services market through service revenues.

Tray-style systems retain the majority of equipment sales due to their flexibility across vial formats, while manifold units focus on personalized medicine. Rotary dryers claim premium niches where 10%-15% faster cycles offset 30% higher prices. Accessories demand remains linked to Process Analytical Technology (PAT) retrofits; adding tunable diode laser sensors can cut cycle development time by 30% and deliver a payback within two years for high-volume users.

By Application: Medical Diagnostics Surge as Point-of-Care Testing Expands

Food processing and packaging contributed 45.83% of revenue in 2025, due to products such as instant coffee, freeze-dried fruit, and premium pet food; however, its growth is slowing in developed regions as consumers shift to fresh alternatives. Medical and diagnostics applications are set to climb at an 11.21% CAGR to 2031, underpinned by point-of-care test growth of 18% in 2025. Lyophilized primers in Abbott’s Alinity m RESP assay remain stable 24 months at 25°C, eliminating cold-chain costs that once captured 20% of per-test expenses. Pharmaceutical and biotech companies benefit from the development of antibody-drug conjugates and potential mRNA vaccines, yet rising biosimilar competition pressures their margins. Other segments, cosmetics, nutraceuticals, and industrial enzymes, represent a fragmented 8%-10% share with modest visibility.

Geography Analysis

North America generated 36.86% of global revenue in 2025, driven by over 2,000 industrial dryers operating under FDA regulations. PCI Pharma Services completed a USD 100 million expansion of its New Hampshire plant in 2024, adding 12 dryers. Expansion at Charleston brought four additional units online. Although high labor and electricity costs temper new purchases, frequent retrofits for PAT compliance keep accessories and services buoyant. Canada’s smaller base and Mexico’s early-stage biosimilar capacity add incremental volume, with Lonza studying a Monterrey site for near-shored manufacturing in 2025.

The Asia-Pacific region is the fastest-growing, projected to post a 13.19% CAGR through 2031. WuXi Biologics commissioned three new suites in 2024 to serve export clients, leveraging 40%-50% lower production costs. The Serum Institute and Biological E each expanded their lines to supply thermostable vaccines, underscoring the pull of vaccine manufacturing on the lyophilization equipment and services market. Tofflon boosted exports by 47% in 2025 by pricing tray dryers 25%-30% below those of its Western peers, although limited FDA penetration persists. Australia and South Korea contribute modestly, while operator-skill gaps across China and India constrain ramp-ups, underscoring the demand for validated, turnkey capacity.

Europe maintained roughly 28% of revenue in 2025, led by Germany, Italy, France, the United Kingdom, and Spain. Industrial electricity prices in Germany averaged EUR 0.22 per kWh in 2025, nearly triple the U.S. rates, eroding the economics for energy-intensive dryers. Compliance with the EU’s F-gas cuts incurs retrofit costs, yet major CDMOs remain committed. For instance, Recipharm invested EUR 3.7 million in Italy in 2024, and Vetter spent EUR 150 million in Ravensburg the same year. Nonetheless, European equipment shipments slipped 6% in 2025 as some projects migrated to lower-cost Asia-Pacific hubs.

South America and Middle East & Africa together form a sub-scale share below 15%, driven by Brazil’s pharmaceutical investments and South Africa’s vaccine ambitions. Infrastructure gaps and import duties dampen growth, though Gavi-funded vaccine rollouts could spur incremental demand, extending the global footprint of the lyophilization equipment and services market.

Competitive Landscape

The top five suppliers, GEA Group, IMA S.p.A., Thermo Fisher Scientific, SP Industries, and Azbil Telstar, accounted for a significant share of equipment revenue in 2025. Each exploits installed-base lock-in through service contracts and modular upgrades. GEA’s ECO Mode retrofit, which sells for USD 400,000-USD 600,000, extends legacy dryer life while reducing energy use. In contrast, IMA’s 2024 PAT sensor bundle, which trims cycle-development times by up to 40%, enhances throughput for high-volume sites. Thermo Fisher leverages a broad catalog of consumables to cross-sell accessories, and SP Industries emphasizes turnkey validation packages.

Chinese challenger Tofflon deepened its international penetration with a 47% surge in exports in 2025, supported by pricing 25%-30% below Western equivalents. Despite cost appeal, FDA-regulated buyers still cite concerns over validation support and after-sales service, capping near-term share gains. White-space opportunities revolve around micro-batch and continuous drying platforms; Lonza and Catalent charge premium vial pricing for autologous CAR-T intermediates processed in manifold and rotary dryers, while academic-industry partnerships pursue continuous systems that could quadruple hourly throughput once regulatory paths are defined.

Operator skill shortages present a bottleneck. Facilities in Asia-Pacific retain fewer certified PAT technicians, prompting sponsors to outsource to CDMOs offering bundled expertise. This dependency tilts negotiating leverage toward service providers, although it also introduces concentration risk for drug developers if capacity becomes tight during pandemic-scale vaccine surges. Overall, competitive dynamics remain balanced between scale leaders and agile regional entrants, shaping an evolving lyophilization equipment and services market.

Lyophilization Equipment And Services Industry Leaders

Azbil Corporation

Labconco Corporation

Optima Packaging Group Gmbh

GEA Group Aktiengesellschaft

Martin Christ Gefriertrocknungsanlagen GmbH

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Cytiva and Argonaut Manufacturing Services signed a contract manufacturing agreement to expand reagent stabilization and lyophilization capacity for diagnostic assay developers, aiming to cut cold-chain logistics and lower carbon footprints.

- January 2025: Purdue University formed an academic-industry consortium with Eli Lilly and Merck to accelerate advanced aseptic processing technologies, including next-generation lyophilization platforms.

- July 2024: GEA, a leading global supplier of systems and components for the food, beverage, and pharmaceutical sectors, has implemented significant changes to enhance the sustainability of pharmaceutical freeze-drying. At ACHEMA 2024 in Frankfurt/Main, GEA showcased its latest advancements in freeze-drying technology, aimed at optimizing production processes, minimizing environmental impact, and conserving energy.

- February 2024: Optima Group launched its filling, isolator, and lyophilization equipment technologies at the Interphex 2024 conference. These technologies included turnkey filling solutions with freeze-dryer and isolator technology.

Global Lyophilization Equipment And Services Market Report Scope

As per the scope of the report, lyophilization is a freeze-drying process that removes water from a product after it is frozen and placed under a vacuum. This is in contrast to dehydration by most conventional methods that make water evaporate using heat.

The lyophilization equipment and services market is segmented by modality, application, and geography. By modality, the segment is further divided into dryer type, accessories, and services. The application segment is further segmented into food processing and packaging, pharmaceutical and biotech manufacturing, and other applications. The geography segment is further bifurcated into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The market report also covers the estimated market sizes and trends for 17 different countries across major regions globally.

The report offers the value (in USD) for the above segments.

| Dryer Type | Tray-style Freeze Dryers |

| Manifold Freeze Dryers | |

| Rotary Freeze Dryers | |

| Vacuum Freeze Dryers | |

| Accessories | Vacuum Systems |

| CIP / SIP Systems | |

| Loading & Unloading Systems | |

| Control & Monitoring Modules | |

| Services | Process & Cycle Development |

| Contract Manufacturing / Bulk Lyophilization | |

| Maintenance & Validation |

| Pharmaceutical & Biotech Manufacturing |

| Food Processing & Packaging |

| Medical & Diagnostics |

| Other Applications |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Modality | Dryer Type | Tray-style Freeze Dryers |

| Manifold Freeze Dryers | ||

| Rotary Freeze Dryers | ||

| Vacuum Freeze Dryers | ||

| Accessories | Vacuum Systems | |

| CIP / SIP Systems | ||

| Loading & Unloading Systems | ||

| Control & Monitoring Modules | ||

| Services | Process & Cycle Development | |

| Contract Manufacturing / Bulk Lyophilization | ||

| Maintenance & Validation | ||

| By Application | Pharmaceutical & Biotech Manufacturing | |

| Food Processing & Packaging | ||

| Medical & Diagnostics | ||

| Other Applications | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large is the lyophilization equipment and services market today?

The market generated USD 5.18 billion in 2026 and is projected to reach USD 8.25 billion by 2031, growing at a 9.76% CAGR.

Which segment is growing fastest within lyophilization?

Contract services lead, expanding at a 10.29% CAGR as sponsors outsource cycle development and batch production.

Why is Asia-Pacific drawing new investments?

Lower labor and utility costs, along with expanding biosimilar and vaccine production, underpin a 13.19% regional CAGR to 2031.

How are sustainability rules affecting equipment design?

EU energy-efficiency and F-gas mandates drive the adoption of natural-refrigerant dryers and energy-saving cycles that cut energy use by 20% or more.

What technologies could disrupt traditional batch dryers?

Continuous belt dryers and hybrid microwave-vacuum systems promise 50%-75% faster cycles once regulatory guidance matures.

Page last updated on: