Diabetic Footwear Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

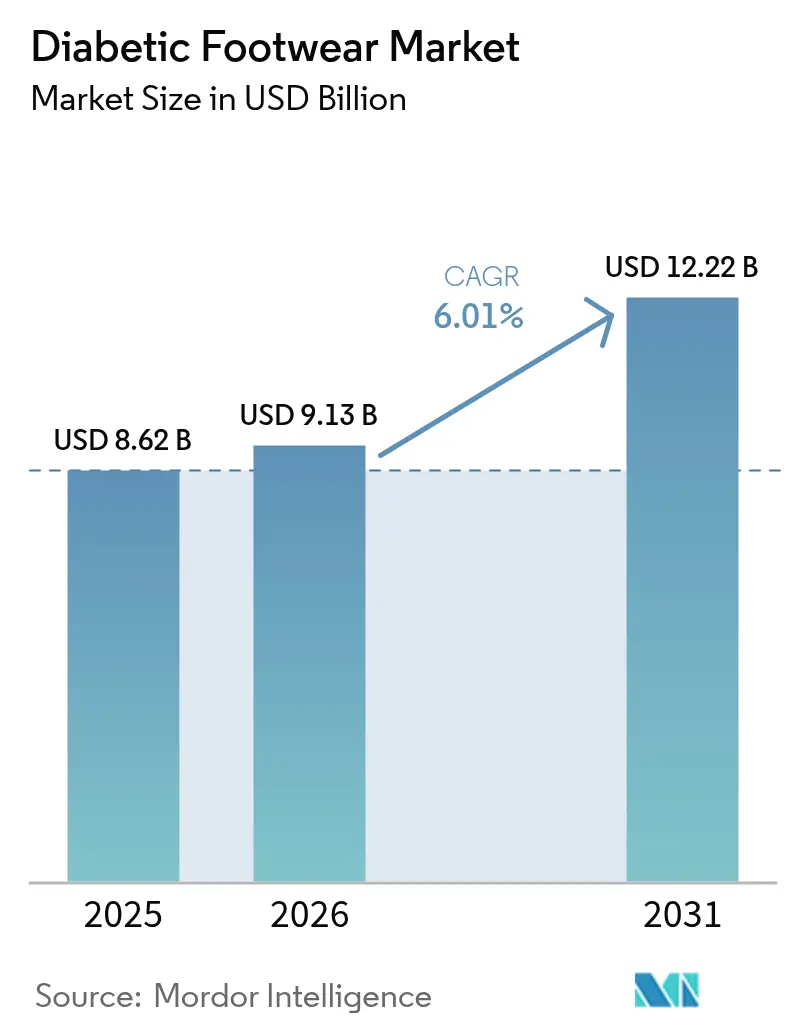

| Market Size (2026) | USD 9.13 Billion |

| Market Size (2031) | USD 12.22 Billion |

| Growth Rate (2026 - 2031) | 6.01% CAGR |

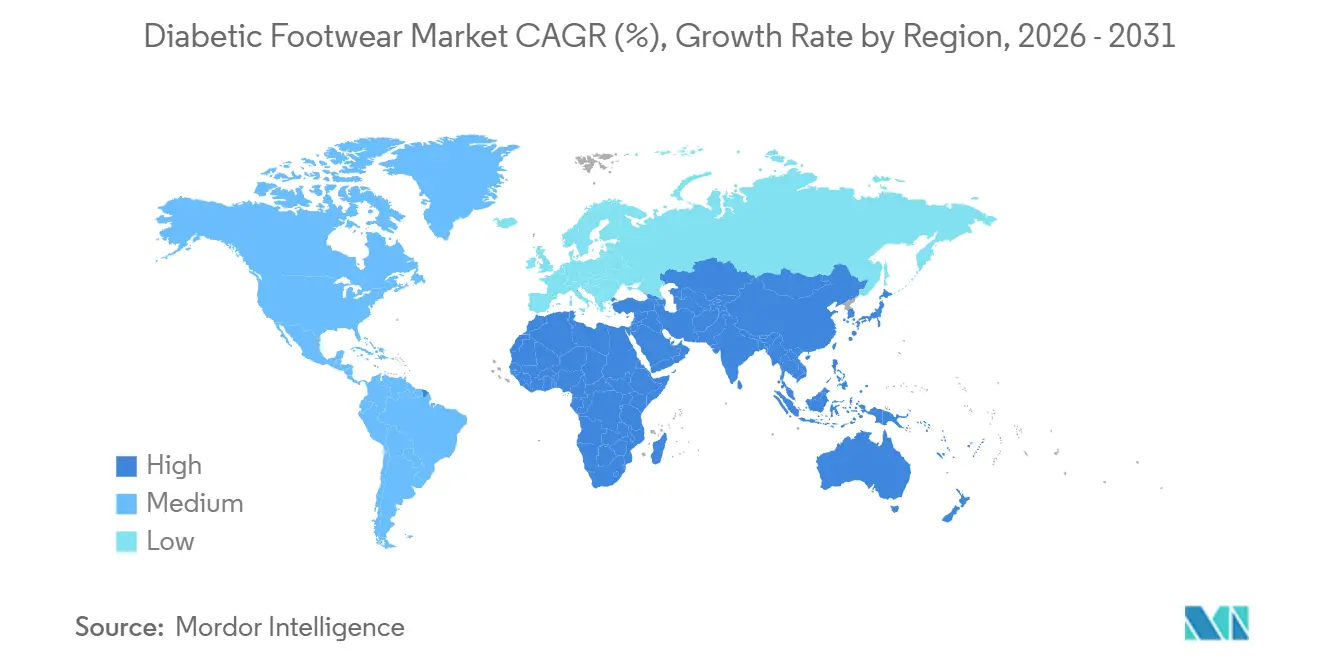

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Diabetic Footwear Market Analysis by Mordor Intelligence

The Diabetic Footwear Market size is projected to be USD 8.62 billion in 2025, USD 9.13 billion in 2026, and reach USD 12.22 billion by 2031, growing at a CAGR of 6.01% from 2026 to 2031. The Diabetic footwear market is expanding as rising diabetes prevalence converges with rapid population aging, broader reimbursement, and the commercial rollout of 3D foot-scanning that enables mass-customized fits. North American payers continue to anchor demand by updating Medicare A5500 fee schedules, while Asia-Pacific growth benefits from India’s and China’s growing senior cohorts and policy pilots that reimburse functional footwear. Suppliers increasingly differentiate through biomechanical engineering, such as rocker-bottom outsoles and cyclic pressure-offloading insoles, rather than basic depth or width adjustments. However, premium retail prices and a widening counterfeit channel in online marketplaces temper near-term uptake, especially across price-sensitive emerging regions.

Key Report Takeaways

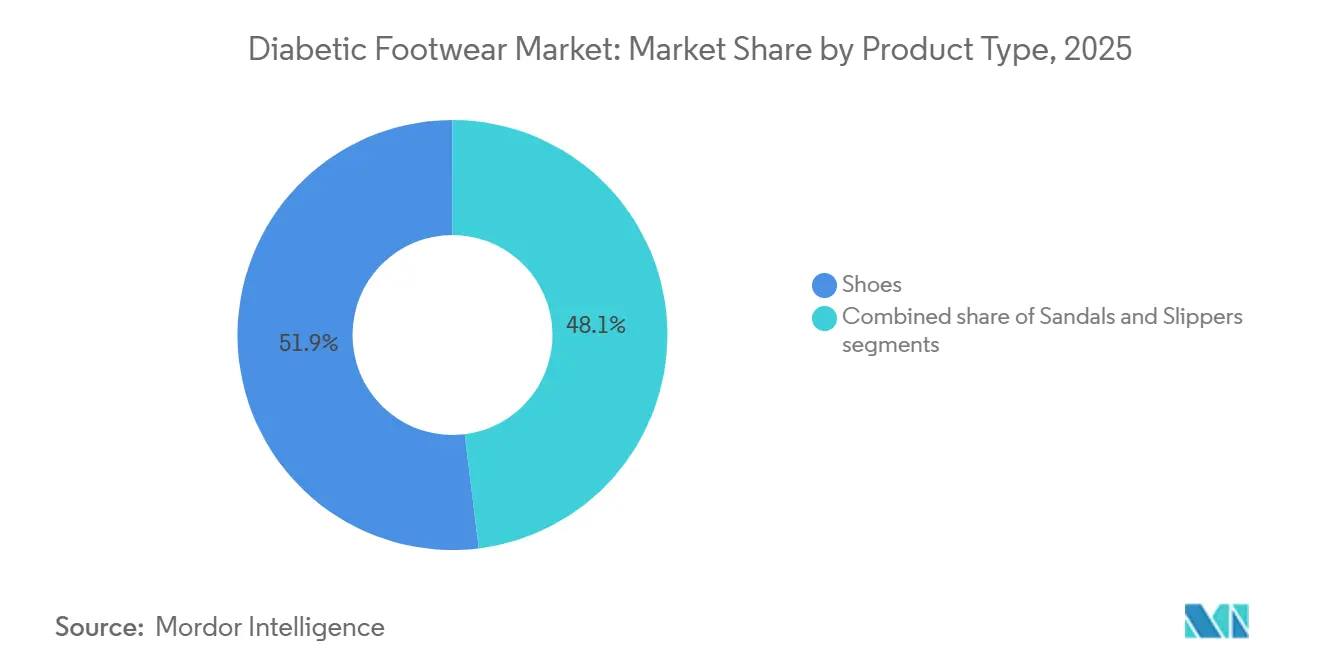

- By product type, enclosed shoes led with 51.94% of the diabetic footwear market share in 2025, while sandals are forecast to post a 7.05% CAGR through 2031.

- By end user, men accounted for 56.13% revenue in 2025, whereas the women’s segment is projected to advance at a 6.60% CAGR to 2031.

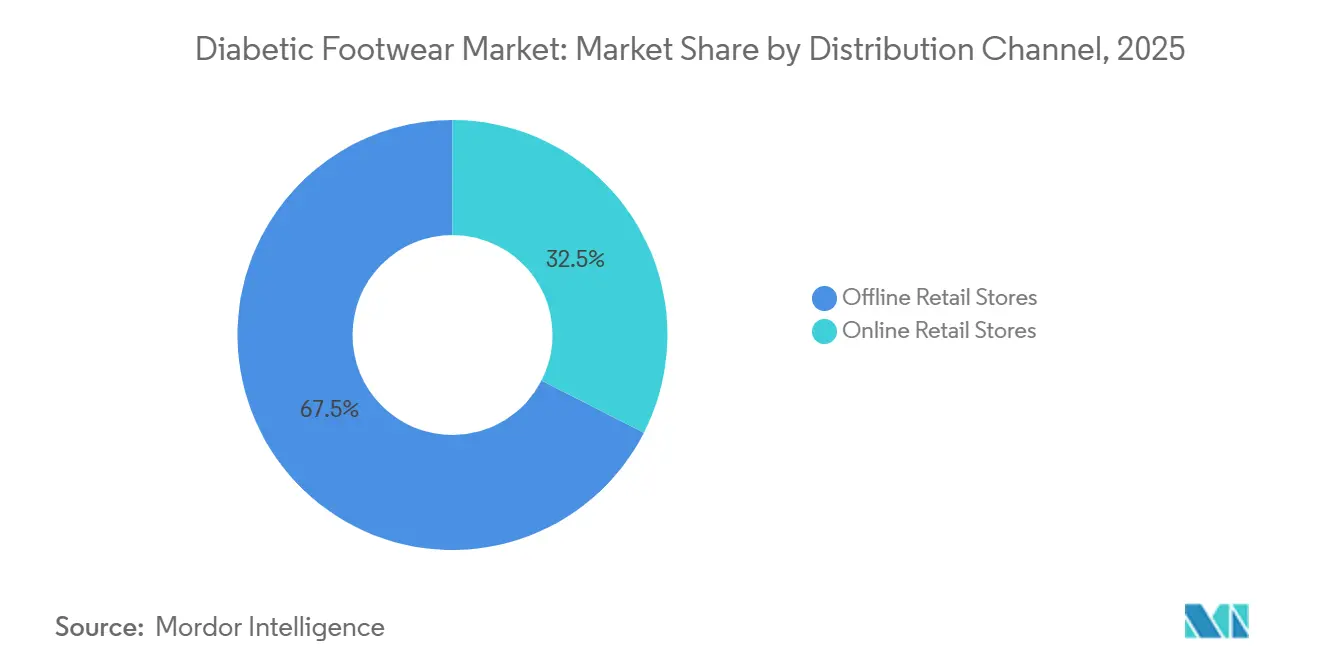

- By distribution channel, offline retail held 67.49% share of the diabetic footwear market size in 2025, and online platforms are expected to climb at a 7.12% CAGR over 2026-2031.

- By geography, North America captured 39.24% revenue in 2025, while Asia-Pacific is set to expand at a 7.90% CAGR through the forecast window.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Diabetic Footwear Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing global prevalence of diabetes | +1.2% | Global, with highest intensity in Asia-Pacific (India, China) and Middle East | Long term (≥ 4 years) |

| Heightened awareness of diabetic foot complications and preventive care | +0.7% | North America, Europe, Australia; expanding to urban Asia-Pacific | Medium term (2-4 years) |

| Integration of podiatry-led preventive care into mainstream healthcare systems | +0.9% | North America, Europe, Australia; pilot programs in Japan | Medium term (2-4 years) |

| Rapid expansion of the aging population worldwide | +0.8% | Global, with pronounced effect in Japan, Europe, North America | Long term (≥ 4 years) |

| Adoption of mass customization through 3D scanning and additive manufacturing | +1.1% | North America and European Union core, expanding to Asia-Pacific and Latin America | Medium term (2-4 years) |

| Gradual introduction of reimbursement coverage in emerging economies | +0.6% | Asia-Pacific (India, China, Southeast Asia), Latin America, Middle East and Africa | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Increasing global prevalence of diabetes

The increasing prevalence of diabetes worldwide is driving demand for diabetic footwear, with the International Diabetes Federation (2025) reporting that 11.1% of the global adult population, 589 million individuals, or 1 in 9 adults, are living with the condition [1]Source: International Diabetes Federation, "Facts and Figures," idf.org. Alarmingly, over 40% remain undiagnosed, elevating the risk of complications such as neuropathy and foot ulcers. This highlights the critical need for preventive care solutions, including specialized footwear that reduces pressure points, enhances circulation, and prevents injuries. Rising diabetes cases, fueled by urbanization, aging populations, and sedentary lifestyles, are contributing to a growing incidence of diabetic foot conditions, prompting healthcare systems and consumers to prioritize early intervention products over reactive treatments. Medically engineered footwear is gaining traction across developed and emerging regions, supported by awareness campaigns and clinical guidelines that emphasize foot care as a vital component of diabetes management. Brands like Dr. Comfort are addressing this demand by offering therapeutic footwear with features such as extra depth, protective interiors, and biomechanical support tailored for diabetic patients. Furthermore, the large undiagnosed population sustains latent demand, as many consumers enter the market only after complications arise, ensuring long-term growth. These factors collectively strengthen the diabetic footwear market by expanding the addressable patient base and driving the adoption of preventive solutions.

Heightened awareness of diabetic foot complications and preventive care

Rising awareness of diabetic foot complications and the importance of preventive care is reshaping demand dynamics, as education on risks such as neuropathy, ulcers, and infections drives both patients and healthcare providers to prioritize early intervention over reactive treatment. This trend is particularly significant for the large undiagnosed diabetic population, where informed individuals are more likely to adopt protective footwear before severe symptoms develop, fueling growth in the preventive care segment. Clinical recommendations and podiatrist-led guidance increasingly highlight the need for specialized footwear with features such as pressure redistribution, seamless interiors, and orthotic support, influencing consumer preferences toward medically designed shoes. The growing prominence of therapeutic footwear brands, such as Orthofeet, reflects this shift, with products engineered to reduce pressure points, improve circulation, and prevent irritation, key factors in mitigating diabetic foot complications. Awareness campaigns, digital health platforms, and retail pharmacists are further promoting preventive foot care, encouraging a transition from generic comfort footwear to clinically validated diabetic solutions, and reinforcing premiumization trends. Additionally, the integration of comfort, style, and medical functionality is reducing the stigma associated with orthopedic shoes, driving adoption among younger and more active diabetic populations. This convergence of medical awareness, preventive healthcare focus, and product innovation is sustaining demand growth in the diabetic footwear market.

Rapid expansion of the aging population worldwide

The aging population worldwide is driving significant demand for diabetic footwear, with United Nations data showing the share of individuals aged 65 and above nearly doubling from 5.5% in 1974 to 10.3% in 2024 and projected to reach 20.7% by 2074 [2]Source: United Nations Population Fund, "Ageing," unfpa.org. This demographic shift correlates with increased diabetes prevalence and age-related complications, such as reduced circulation, neuropathy, and foot ulcers, expanding the consumer base for therapeutic footwear. As longevity rises and fertility rates decline, a larger portion of the population requires continuous medical and preventive care, fueling demand for products that combine comfort with clinical functionality. This trend has integrated geriatric care with consumer health products, positioning diabetic footwear as a daily-use necessity rather than a niche medical device. Older consumers, prone to mobility challenges and chronic conditions, seek footwear offering enhanced cushioning, stability, and pressure offloading, driving product innovation. Companies like Apex Foot Health Industries are addressing these needs with orthopedic and diabetic footwear featuring extra-depth designs and accommodative insoles for age-related foot issues. Additionally, healthcare systems emphasizing aging-in-place and preventive care are boosting demand across institutional and retail channels. The convergence of an aging population and chronic disease prevalence establishes diabetic footwear as a critical component of eldercare and chronic disease management.

Adoption of mass customization through 3D scanning and additive manufacturing

Mass customization, driven by advancements in 3D scanning and additive manufacturing, is enabling the creation of highly personalized diabetic footwear solutions. By leveraging digital foot scanning and gait analysis, manufacturers can capture precise biomechanical data to produce customized footwear and orthotic components that address individual foot morphology, pressure distribution, and gait abnormalities. This approach ensures optimal fit, reduces the risk of ulcers and pressure injuries, and aligns with the broader healthcare trend of precision medicine, which focuses on preventive care tailored to individuals. Additive manufacturing supports on-demand production with minimal inventory, faster turnaround times, and reduced material waste, making mass customization commercially viable and accessible to patients. Companies like Aetrex utilize extensive networks of in-store foot scanners and 3D printing technologies to deliver custom orthotics within days, while platforms such as Phits (Materialise) employ dynamic gait analysis and 3D printing to enhance comfort and therapeutic effectiveness. The ability to fine-tune parameters like cushioning zones, arch support, and material density ensures diabetic patients receive footwear that actively mitigates complications. Additionally, decentralized production models enabled by additive manufacturing are improving localized, clinic-based fabrication, enhancing patient access in both developed and emerging markets, and redefining supply chains and value propositions.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Premium pricing of medically certified diabetic footwear | -0.6% | Emerging markets in Asia-Pacific, South America, Middle East and Africa; rural areas globally | Short term (≤ 2 years) |

| Rising presence of counterfeit and substandard products in price-sensitive markets | -0.5% | Global, concentrated in China, India, Southeast Asia, Sub-Saharan Africa | Short term (≤ 2 years) |

| Lack of harmonized global prescription and clinical guidelines | -0.4% | Global, particularly affecting cross-border trade and emerging markets | Medium term (2-4 years) |

| Dependence on specialized therapeutic materials and cushioning foams within supply chains | -0.3% | Global, with supply chain concentration in Asia-Pacific | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Premium pricing of medically certified diabetic footwear

The premium pricing of medically certified diabetic footwear poses a significant challenge for market adoption. These products, designed with advanced materials, biomechanical features, and regulatory compliance, incur higher production and certification costs, which are passed on to consumers. This issue is particularly pronounced in low- and middle-income countries, home to approximately 6.56 billion people or 74% of the global population in 2024, as per the World Bank, where affordability constraints drive demand toward lower-cost or non-medical alternatives [3]Source: World Bank Group, "Low and Middle Income," data.worldbank.org . Despite growing awareness of diabetic foot complications, price sensitivity among a large portion of the target population creates a gap between medical needs and product adoption. Premium footwear, offering benefits such as pressure redistribution, extra depth, and orthotic compatibility, is often priced significantly higher than regular footwear, limiting its reach in emerging markets. For instance, brands like Drew Shoe provide medically certified diabetic shoes with advanced features, but their specialized construction and compliance requirements result in premium pricing. This barrier is further exacerbated in regions lacking insurance coverage or reimbursement frameworks, where out-of-pocket healthcare spending dominates. Many patients delay or avoid purchasing diabetic footwear until complications worsen, undermining preventive care and early-stage market growth. While some manufacturers are introducing cost-optimized variants, balancing affordability with medical efficacy remains a persistent challenge, particularly in price-sensitive markets.

Rising presence of counterfeit and substandard products in price-sensitive markets

The presence of counterfeit and substandard products in price-sensitive markets remains a significant restraint, as the influx of low-cost imitations undermines product efficacy, patient safety, and brand credibility. In emerging economies and online marketplaces, counterfeit diabetic footwear is often marketed with misleading medical claims but lacks essential features such as pressure-relief insoles, seamless interiors, and proper cushioning, exposing patients to higher risks of ulcers and complications. Affordability constraints further exacerbate this issue, as cost-conscious consumers, already hesitant due to premium pricing, opt for cheaper alternatives, perpetuating the circulation of substandard products and weakening demand for certified solutions. The expansion of e-commerce and informal retail channels has increased the visibility and accessibility of counterfeit products, making it difficult for consumers to distinguish between medically approved and imitation footwear. This erosion of consumer trust impacts purchasing decisions and compels hospitals and clinicians to recommend only verified suppliers, limiting market access for smaller or newer brands. Established players, such as Podartis, face indirect competition from counterfeit products that imitate design aesthetics without delivering therapeutic benefits, diluting brand value and market share. Counterfeit products contribute to revenue losses and reduced market penetration for legitimate manufacturers, creating a fragmented market where inconsistent quality hampers standardization and slows the adoption of preventive healthcare solutions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Enclosed Shoes Dominate, Sandals Surge on Ventilation Demand

Enclosed shoes hold the largest share in the diabetic footwear market, accounting for 51.94% of the projected 2025 revenue. Their versatility across various climates, workplace environments, and formal settings makes them a preferred choice for daily wear. Additionally, they align with reimbursement frameworks such as Medicare A5500 codes for depth-inlay designs, significantly enhancing affordability and adoption among eligible patients. Features like reinforced soles, extra depth, and orthotic compatibility further establish enclosed shoes as the most clinically preferred option for long-term diabetic foot management, particularly in developed healthcare systems. Brands like Propet exemplify this leadership by offering Medicare-approved diabetic shoes that combine therapeutic design with everyday usability. Innovation in this segment is increasingly focused on biomechanical engineering to redistribute pressure and reduce tissue stress, advancing beyond basic fit accommodations.

Sandals represent the fastest-growing segment, with a projected CAGR of 7.05% through 2031, outpacing the overall market by 104 basis points. This growth is driven by clinical recognition of their benefits for post-ulcer healing and high-risk foot conditions, offering enhanced ventilation and reduced friction that enclosed shoes cannot fully provide. Companies like DARCO International are capitalizing on this trend by developing therapeutic sandals and post-operative footwear designed to offload pressure and improve airflow. This shift highlights the growing emphasis on clinical performance in product differentiation.

By End User: Men Lead, Women Accelerate on Gender-Specific Design

The male demographic holds the largest share in the diabetic footwear market, accounting for 56.13% of the projected demand by 2025. This is primarily due to the higher prevalence of diabetes among men aged 45 to 64 and their greater adoption of medical-grade footwear for occupational safety and mobility needs. Workplace norms in industrial and service sectors, where protective and supportive footwear is standard, facilitate a seamless transition to diabetic-specific shoes. Durable, enclosed footwear designed for prolonged wear remains in steady demand, with brands like Dunlop Protective Footwear offering work-oriented designs that combine safety features with ergonomic support. This alignment between product utility and occupational requirements continues to drive demand among male users, particularly in working-age populations with higher disease incidence.

The women’s segment is expected to grow at a faster rate of 6.60% through 2031, driven by increasing recognition of gender-specific biomechanics. Historically, diabetic footwear designs relied on male-oriented lasts with minimal adjustments, overlooking women’s narrower heels, higher arches, and wider forefoot profiles. Brands like KURU Footwear are addressing these needs with anatomically precise solutions, including heel-cupping technology, tapered heel counters, and seam-free linings. However, socioeconomic and cultural factors, particularly in emerging markets, limit adoption as women often deprioritize personal healthcare spending. Improved awareness, accessibility, and gender-specific innovations are expected to transform this segment into a high-growth area, reshaping market dynamics.

By Distribution Channel: Offline Resilience Meets Online Surge

Offline retail accounts for 67.49% of the projected 2025 revenue in diabetic footwear distribution, driven by the critical need for in-person evaluations. Proper fitting, gait analysis, and compliance with Medicare documentation, which often requires clinician signatures, make offline channels indispensable. Podiatric clinics, specialty footwear retailers, and durable medical equipment suppliers provide tactile assessments, immediate adjustments, and professional guidance that cannot be fully replicated online. These services ensure therapeutic efficacy and enhance patient confidence. Brands such as Orthofeet leverage offline channels to deliver personalized consultations, custom fittings, and on-site demonstrations, fostering trust and adherence to prescribed footwear.

Online retail is experiencing rapid growth, with a projected CAGR of 7.12% through 2031. This expansion is supported by advancements in virtual fitting technologies, the adoption of telemedicine, and direct-to-consumer models that reduce intermediary costs. Platforms like Aetrex utilize over 12,000 3D foot scanners to create digital foot models, enabling accurate remote ordering through e-commerce sites. The post-pandemic acceptance of telemedicine-generated prescriptions under Medicare has further legitimized online purchases. Additionally, direct-to-consumer brands bypass distributor markups, offering competitive pricing and convenience. The integration of these technological advancements with shifting consumer preferences is gradually creating a hybrid retail landscape, balancing offline dominance with online convenience while maintaining clinical reliability.

Geography Analysis

North America holds the largest share of the diabetic footwear market, contributing 39.24% of the projected 2025 revenue. This dominance is driven by Medicare’s A5500–A5514 reimbursement codes and an updated Centers for Medicare and Medicaid Services fee schedule, which increased coverage for depth-inlay shoes, ensuring sustained support for eligible beneficiaries. The United States features a dense network of podiatric clinics and durable medical equipment suppliers. Companies like Aetrex have implemented thousands of 3D foot scanners across clinical and retail locations to enhance fitting accuracy and compliance. High per-capita healthcare spending and a well-established reimbursement framework provide a stable revenue base, though growth is constrained by market saturation and limited new patient inflows due to aging demographics.

The Asia-Pacific region represents the fastest-growing market, with a forecasted CAGR of 7.90% through 2031. Growth is supported by the International Diabetes Federation’s (IDF) projection that India will reach 134 million diabetic patients by 2045, while China already exceeds 140 million cases. Similarly, National insurance programs, such as Japan’s functional footwear coverage and Australia’s Department of Veterans’ Affairs and Enable NSW initiatives, are improving access to therapeutic footwear by addressing financial barriers. Brands offering regionally adapted solutions that combine comfort, preventive features, and regulatory compliance are well-positioned to capture the expanding addressable population in this region.

Europe benefits from established national health systems and reimbursement mechanisms that stabilize demand for diabetic footwear. In contrast, South America and the Middle East and Africa (MEA) face challenges such as infrastructure gaps, a limited podiatric workforce, and affordability constraints. However, rising diabetes prevalence and urbanization are gradually expanding the consumer base in these regions. International brands like DARCO International are increasingly partnering with local distributors and clinics to improve accessibility and awareness, signaling a gradual strengthening of market penetration despite systemic challenges.

Competitive Landscape

Aetrex holds a significant share in the diabetic footwear market, leveraging its deployment of 12,000 foot scanners globally and over 50 million completed scans. This extensive data repository provides a competitive advantage, supporting machine-learning algorithms that refine last designs, predict fit accuracy, and enhance product effectiveness. These capabilities result in higher patient satisfaction and increased repeat adoption. Furthermore, Aetrex integrates connected health platforms to link footwear performance with patient outcomes, aligning with payers’ growing focus on value-based care rather than product volume.

Other prominent companies, including Orthofeet, DJO Global’s Dr. Comfort, and DARCO International, employ strategies such as vertical integration, proprietary scanning technologies, and Medicare billing expertise to maintain their market positions. These approaches enable them to align product offerings with clinical requirements, regulatory compliance, and patient-specific customization needs. By addressing these critical factors, these companies strengthen their competitive positioning and foster customer loyalty in a moderately fragmented market.

Traditional manufacturers without advanced digital capabilities face increasing pressure to innovate as the competitive landscape rewards companies that combine clinical validation with technological sophistication. Orthofeet is responding by introducing digitally informed design and customer support systems, while DARCO and Dr. Comfort emphasize orthotic compatibility and durable construction. The convergence of data-driven customization, reimbursement alignment, and connected health solutions is reshaping the market. Sustained leadership in the diabetic footwear market increasingly depends on the ability to integrate technology with therapeutic efficacy, reflecting the evolving priorities of both patients and payers.

Diabetic Footwear Industry Leaders

-

Aetrex Worldwide Inc.

-

DJO Global Inc. (Dr. Comfort)

-

Orthofeet Inc.

-

DARCO International Inc.

-

Drew Shoe Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: Carbon Meditek partnered with DiabeticShoe.in as an authorized dealer, aiming to enhance the availability of diabetic and orthopedic footwear across India. This collaboration enabled Carbon Meditek to offer premium diabetic shoes, orthopedic sandals, and diabetic socks from DiabeticShoe.in to its expanding customer base, improving accessibility for individuals managing diabetes and mobility-related issues.

- July 2025: SHOEMART, a family footwear retailer operated by Landmark Group, introduced a diabetic footwear line under its comfort brand, Le Confort. This launch was part of a collaboration with the Al Jalila Foundation, the philanthropic arm of Dubai Health. The Le Confort Diabetic Shoes were designed to emphasize comfort and support, featuring wide toe boxes for swollen feet, breathable materials, memory foam insoles, and slip-resistant soles.

- June 2024: FootSecure, a healthcare startup specializing in podiatric medicine and wound care, launched a custom footwear manufacturing unit in Bengaluru with support from the Karnataka Institute of Endocrinology and Research. It introduced six models, including four for women and two for men, priced from Rs 2000. Customizations included the outer sole, midsole, insole, and uppers, addressing conditions such as foot pain, diabetes, arthritis, congenital foot disorders, post-accident deformities, and post-surgical anomalies. The facility had a production capacity of up to 300 pairs of custom offloading footwear per day.

Global Diabetic Footwear Market Report Scope

Diabetic Footwear is specifically designed for the diabetic population as a preventive measure for foot care and offering comfort. The scope of the diabetic footwear market includes segmentation based on product type, end-user, distribution channel, and geography. The market is segmented by type into shoes, sandals, and slippers. By the end-user, the market is segmented into men and women. Furthermore, on the basis of the distribution channel, the market is segmented into offline and online retail stores. Lastly, the report covers geographical insights into the major regions, including North America, Europe, Asia-Pacific, and Rest of the World. The market sizing has been done in value terms in USD for all the abovementioned segments.

| Shoes |

| Sandals |

| Slippers |

| Men |

| Women |

| Offline Retail Stores |

| Online Retail Stores |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Rest of Middle East and Africa |

| By Product Type | Shoes | |

| Sandals | ||

| Slippers | ||

| By End User | Men | |

| Women | ||

| By Distribution Channel | Offline Retail Stores | |

| Online Retail Stores | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the projected value of the Diabetic footwear market by 2031?

The market is expected to reach USD 12.22 billion by 2031.

Which product category is growing faster than the overall market?

Sandals are forecast to advance at a 7.05% CAGR through 2031, outpacing overall growth.

Why is Asia-Pacific the fastest-growing region?

High diabetes prevalence in India and China, combined with emerging reimbursement schemes, drives a 7.90% regional CAGR.

What are the main challenges limiting adoption in emerging markets?

Premium pricing and a surge of counterfeit, substandard products remain key obstacles.

Page last updated on: