Lupus Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 5.33 Billion |

| Market Size (2031) | USD 8.54 Billion |

| Growth Rate (2026 - 2031) | 9.88% CAGR |

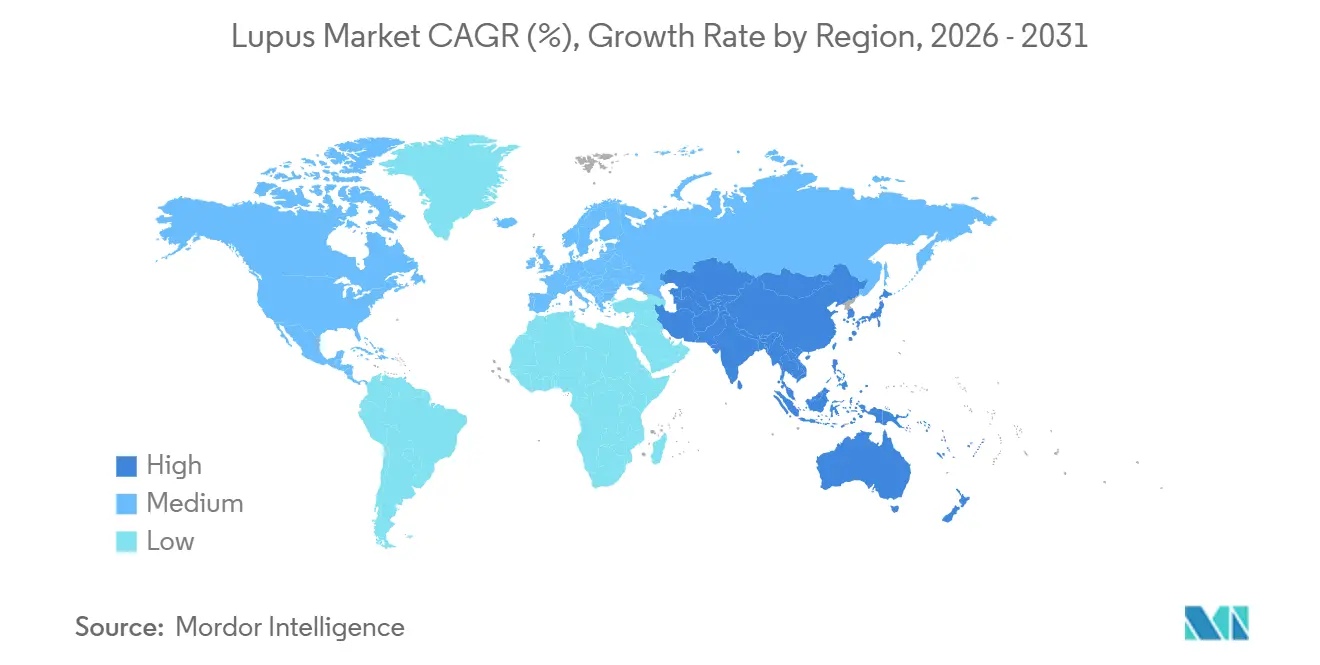

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Lupus Market Analysis by Mordor Intelligence

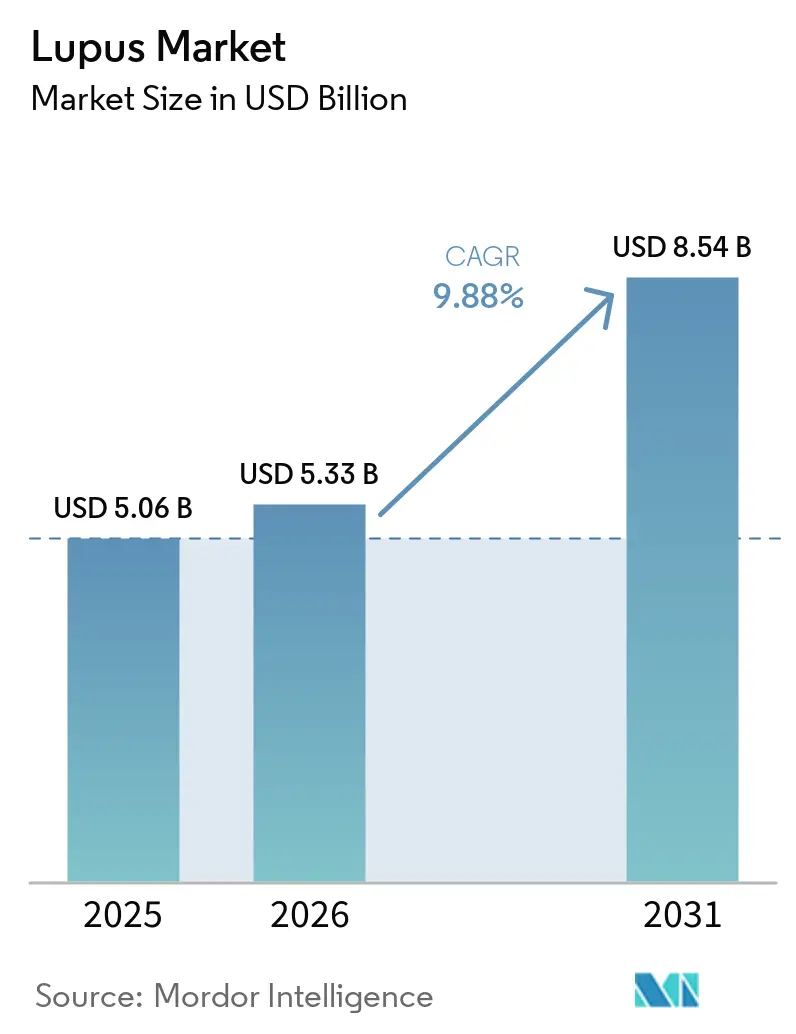

The Lupus Market size is projected to be USD 5.06 billion in 2025, USD 5.33 billion in 2026, and reach USD 8.54 billion by 2031, growing at a CAGR of 9.88% from 2026 to 2031.

The lupus market is transitioning from broad immunosuppression to precision biologics, focusing on organ protection and earlier intervention for complex cases. The FDA's approval of obinutuzumab for lupus nephritis in October 2025 marked a pivotal shift, ending years of limited innovation in advanced lupus therapies. The 2025 American College of Rheumatology guidelines further encouraged earlier use of immunosuppressants, both conventional and biologic, while promoting a stronger steroid-sparing approach, driving significant changes in prescribing patterns. Expanded reimbursements, improved specialty diagnostics, and self-administration options are enhancing access to advanced therapies, reducing reliance on hospital-based infusion settings. The market remains moderately concentrated in branded biologics, while a fragmented base of generic therapies continues to exert pricing pressure across various treatment lines.

Key Report Takeaways

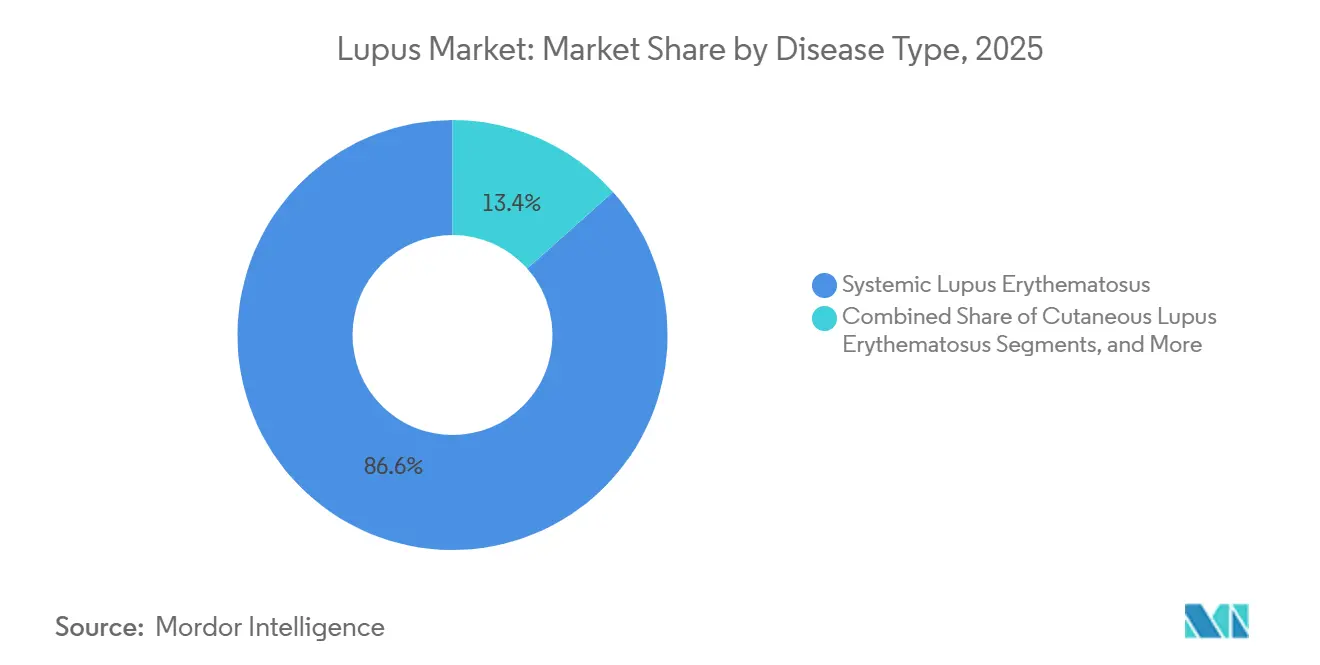

- By disease type, systemic lupus erythematosus held 86.58% of the segment in 2025, and the cutaneous lupus erythematosus segment remained the fastest-expanding subtype with a CAGR of 10.93% from 2026 to 2031.

- By treatment and diagnosis segment, the treatment segment held 70.22% of the segment in 2025, and is projected to grow at a 11.28% CAGR from 2026 to 2031.

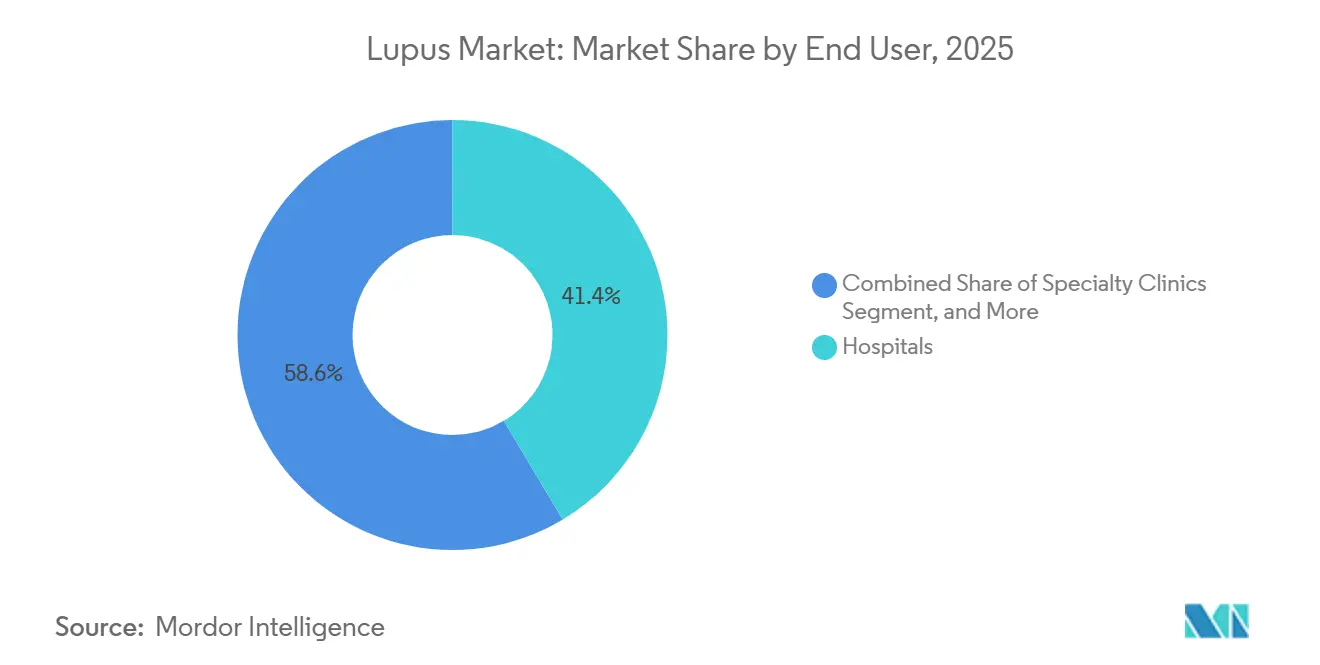

- By end user, hospitals held 41.43% of the segment in 2025, while home care settings are projected to expand at a 11.87% CAGR from 2026 to 2031.

- By geography, North America held 59.44% of the lupus market in 2025, while Asia-Pacific is projected to expand at an 11.89% CAGR from 2026 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Lupus Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Rising prevalence and earlier lupus detection | +1.8% | Global, with high impact in North America, Europe, and East Asia | Short term (≤ 2 years) |

| Shift toward targeted biologics and steroid-sparing treatment | +2.1% | North America and EU core, with spillover to APAC and GCC | Medium term (2-4 years) |

| Reimbursement expansion for specialty lupus diagnostics and therapeutics | +1.3% | US, Canada, Germany, Japan, China pilot cities | Medium term (2-4 years) |

| Rising demand for home-based administration and self-injection devices | +0.8% | North America, EU, Australia | Short term (≤ 2 years) |

| Biomarker-driven flare prediction and precision monitoring | +0.7% | North America, EU, Japan, South Korea | Long term (≥ 4 years) |

| Pipeline expansion in lupus nephritis and refractory SLE | +1.5% | Global, with regulatory acceleration in the US, EU, and China | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence and Earlier Lupus Detection

As testing access improves, clinicians are diagnosing lupus earlier, increasing the number of patients entering treatment before irreversible organ damage occurs. Underdiagnosis remains a challenge in regions like South and Southeast Asia, Sub-Saharan Africa, and Latin America, but advancements in testing infrastructure are expected to address this issue. Tools such as serum Raman spectroscopy and deep-learning classifiers are expediting confirmation processes, reducing delays between symptom onset and treatment. Electronic health record dashboards are also helping providers close follow-up gaps, further supporting market growth by expanding the treated population.

Shift Toward Targeted Biologics and Steroid-Sparing Treatment

The lupus market is shifting towards targeted biologics and reduced steroid use, driven by updated 2025 treatment guidelines emphasizing early biologic initiation. This trend is increasing demand for therapies like belimumab, anifrolumab, and voclosporin. China's 2025 guideline update expanded biologic adoption and introduced JAK inhibitors, reflecting broader global acceptance. Real-world evidence shows biomarker-guided telitacicept achieves higher response rates and greater corticosteroid reduction compared to standard treatments, making advanced therapies more defensible to payers by reducing complications.[1]Otsuka Pharmaceutical, “Otsuka Receives Approval in Japan for Lupkynis as a Treatment for Lupus Nephritis,” Otsuka Pharmaceutical, otsuka.co.jp

Reimbursement Expansion for Specialty Lupus Diagnostics and Therapeutics

Reimbursement policies are driving growth in the lupus market by improving access to high-cost therapies. In the U.S., the 2025 Medicare Part D out-of-pocket cap and USD 2,000 annual drug cost limit have reduced financial barriers, enhancing treatment adherence.[2]American College of Rheumatology, “2025 American College of Rheumatology Guideline for the Treatment of Systemic Lupus Erythematosus,” Contentstack Hosted Guideline Text, assets.contentstack.io Japan's approval and commercial launch of voclosporin for lupus nephritis in 2024 expanded access to this newer therapy. In Canada, the recommendation to reimburse obinutuzumab under specific cost conditions highlights a shift towards outcome-based reimbursement, focusing on measurable renal and systemic responses rather than upfront costs.

Rising Demand for Home-Based Administration and Self-Injection Devices

The lupus market is adapting to increased demand for self-administration options. AstraZeneca's approval of the Saphnelo Pen in the U.S. and EU reduces reliance on infusion centers, benefiting patients in underserved areas. Evidence from 2025 supports home-based therapeutic models as cost-effective and safe alternatives to hospital infusions. GSK's approval of the Benlysta autoinjector for pediatric lupus nephritis further expands homecare options, signaling a gradual shift in care delivery from hospitals to specialty clinics and home settings.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| High lifetime treatment cost and access barriers | -1.7% | Global, most acute in lower-income APAC markets, Latin America, and MEA | Medium term (2-4 years) |

| Diagnostic heterogeneity and delayed disease confirmation | -0.9% | Global, particularly South and Southeast Asia and Sub-Saharan Africa | Long term (≥ 4 years) |

| Infection risk and long-term safety concerns with immunosuppressants | -0.6% | North America and EU, where pharmacovigilance burden shapes prescribing | Medium term (2-4 years) |

| Slow clinical translation and narrow trial success rates | -0.7% | Global, affecting the investment cycle broadly | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Lifetime Treatment Cost and Access Barriers

High treatment costs continue to restrict the lupus market, despite strong clinical evidence supporting advanced therapies. In the U.S., annual biologic therapy costs often exceed USD 30,000. A 2025 analysis showed that 15.4% of patients faced financial instability, 8.2% encountered transportation challenges, and 12% lacked insurance coverage. Strict prior authorization requirements for agents like Saphnelo and belimumab delay treatment until earlier therapies fail or organ involvement worsens.[3]Frontiers Editorial Office, “BAFF/APRIL Expression-Guided Telitacicept Therapy Demonstrates Superior Efficacy in SLE Patients, A Real-World Comparative Study,” Frontiers in Medicine, frontiersin.org In emerging markets, maintaining standard treatments like hydroxychloroquine and corticosteroids remains difficult without insurance or regular specialist access. Reimbursement alone cannot drive uptake if monitoring infrastructure and specialist availability are inadequate.

Diagnostic Heterogeneity and Delayed Disease Confirmation

The lupus market is constrained by the lack of a definitive test for SLE across all patient groups. Current diagnostics rely on antinuclear antibody positivity, clinical criteria, and renal biopsies in nephritis cases, leading to slower and inconsistent diagnoses compared to diseases with clear biomarker thresholds. Delays often result in advanced organ injury, limiting treatment options. A 2025 study in Italy revealed that 85% of patients relied on corticosteroids, while only 26% accessed biologic DMARDs. Until point-of-care biomarker tools gain broader regulatory acceptance, diagnostic inconsistencies will continue to hinder early adoption of biologics in the lupus market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Disease Type: Systemic Lupus Drives Biologic Spend

In 2025, systemic lupus erythematosus (SLE) accounted for 86.58% of the lupus market, establishing itself as the primary focus for treatment and diagnosis. This dominance is due to SLE's extensive organ involvement, including renal, cardiac, neuropsychiatric, and mucocutaneous systems, which necessitate intensive treatment and complex follow-ups. The 2025 Chinese guidelines for SLE endorsed biologics and JAK inhibitors, marking a shift toward long-term remission and organ protection. SLE patients are more likely to adopt high-value drug regimens and require frequent monitoring, driving market growth.

Cutaneous lupus erythematosus remains a smaller segment with the highest CAGR of 10.93% from 2026 to 2031, primarily managed through dermatology with topical treatments and lower systemic drug intensity. However, its strategic importance is growing as companies target immune responses aligned with skin-dominant disease biology. Drug-induced and neonatal lupus, while commercially limited, contribute to diagnostic activities and specialist consultations. The push for multidisciplinary care across rheumatology, dermatology, nephrology, and mental health broadens the scope for identifying and managing these subtypes, supporting future demand even in smaller categories.

By Treatment and Diagnosis: Biologics Lead Revenue While Immunosuppressants Grow Fastest

Treatment type held 70.22% of the lupus treatment market in 2025, reflecting its revenue dominance despite limited patient use. Their premium position stems from strong pricing, specialized application in severe cases, and focus on active lupus nephritis and refractory SLE. Roche reported a 46.4% complete renal response rate for obinutuzumab combined with standard therapy, compared to 33.1% for standard therapy alone, validating the high spending on biologics. A small group of high-acuity patients drives significant spending due to the high costs of advanced therapies.

The treatment type segment is projected to grow at a 11.28% CAGR from 2026 to 2031, making it the fastest-growing treatment category. Voclosporin has revitalized this class with its modern profile and broader regulatory approvals, including its 2024 launch in Japan. Mycophenolate mofetil and tacrolimus are increasingly used in combination regimens under steroid-minimization guidelines. Antimalarial drugs remain foundational in SLE care, while antihypertensives manage cardiovascular complications. Corticosteroid reliance is gradually decreasing as the market shifts toward safer long-term options.

Moreover, essential tests such as ANA, anti-dsDNA, complement C3 and C4, and urinalysis are critical for diagnosis and follow-up. Their widespread clinical use ensures stable and recurring revenue across care settings. The adoption of multianalyte panels is increasing revenue per patient encounter as clinicians prefer comprehensive testing bundles over isolated markers. Multimodal MRI parameters have demonstrated their ability to detect cerebrovascular changes in neuropsychiatric SLE, offering capabilities beyond serology. Contrast-enhanced ultrasound is gaining traction as a non-invasive tool for differentiating proliferative from non-proliferative lupus nephritis, reducing reliance on kidney biopsies. While biopsy remains the gold standard for nephritis classification, its share is expected to decline as non-invasive methods gain acceptance, expanding diagnostic activity in previously limited settings.

By End User: Hospitals Remain Largest While Specialty Clinics Gain Ground

Hospitals accounted for 41.43% of the lupus market share in 2025, driven by the complexity of infusion therapy, nephrology co-management, and intensive monitoring for severe cases. Their dominance is tied to the management of lupus nephritis, inpatient relapse treatments, and advanced therapy escalations. A 2025 study highlighted that 55.4% of SLE patients experienced hospitalization for various reasons, with 33.4% hospitalized for SLE relapses, reinforcing hospitals' central role in acute care.

Homecare settings are projected to grow at a 11.87% CAGR from 2026 to 2031, making them the fastest-growing end-user segment. Payers are increasingly favoring outpatient administration, supported by subcutaneous options for anifrolumab and belimumab. GSK’s 2025 initiative emphasized investments in community-based systems to support decentralized care and improve patient adherence. Homecare settings are gaining relevance for self-injections and pediatric use, while diagnostic labs maintain steady demand. Although hospitals remain the primary revenue center, growth is shifting toward cost-effective outpatient and home-based care settings.

Geography Analysis

In 2025, North America led the lupus market with a 59.44% share, driven by a high density of rheumatology and nephrology specialists, early access to new therapies, and broader reimbursement options compared to other markets. The 2025 ACR guideline and Medicare Part D reform expanded access to biologics, reducing out-of-pocket costs for patients. The U.S. approval of the Saphnelo Pen in April 2026 reduced dependence on infusion centers and improved adherence in community rheumatology settings. In Canada, reimbursement support for obinutuzumab in active lupus nephritis enhanced access to advanced therapies.

Europe remained the second-largest regional contributor to the lupus market, with Germany, the UK, and France generating the highest revenue. The approval of subcutaneous anifrolumab in December 2025 strengthened competition by addressing delivery disadvantages compared to other biologics. The region is also set to benefit from obinutuzumab expansion as regulatory reviews progress, supported by strong late-stage nephritis and broader SLE data. Western Europe leads in biologic access, while Central and Eastern Europe face slower adoption due to inconsistent reimbursement systems.

Asia-Pacific is the fastest-growing region in the lupus market, projected to grow at an 11.89% CAGR from 2026 to 2031. China and Japan drive growth with large patient populations, faster regulatory approvals, and improved specialty access. Japan’s approval and launch of voclosporin for lupus nephritis set a precedent for premium therapy adoption. China’s 2025 treatment guideline update supports broader biologic use and formalized prescribing in major hospitals. India, South Korea, and Australia contribute to growth, while South America and the Middle East and Africa remain early-stage markets, limited by infrastructure and high out-of-pocket costs.

Competitive Landscape

In the lupus market, GSK, AstraZeneca, and Roche (or Genentech) dominate the branded biologic tier. GSK, leveraging its established Benlysta franchise, has broadened its reach by introducing self-administration and targeting pediatric lupus nephritis. AstraZeneca, with its Saphnelo Pen, has enhanced the flexibility of anifrolumab's administration, positioning the company to compete beyond traditional infusion-centered care. Roche and Genentech intensified the competition by securing approval for obinutuzumab in lupus nephritis and subsequently pushing for a wider SLE expansion, bolstered by robust Phase 3 ALLEGORY data. These strategic maneuvers highlight a shift among leading players in the lupus market, emphasizing a focus on indication breadth, organ-specific responses, and convenient delivery over mere first-mover advantages.

While the upper echelons of the lupus market see a concentration of innovative players, the landscape below is notably fragmented. Companies like Teva, Hikma, Dr. Reddy’s, Lupin, Aurobindo, Sun Pharma, and Zydus Lifesciences supply generic treatments such as hydroxychloroquine, methylprednisolone, and mycophenolate mofetil. Here, competition hinges more on pricing, consistent manufacturing, and robust distribution rather than clinical differentiation. This fragmentation, despite a few companies leading in premium biologics, ensures the lupus market doesn't tilt towards high concentration. It also underscores that in many countries, formulary decisions still weigh branded innovations against established, cost-effective standard regimens.

The lupus market is witnessing a diversification in strategic maneuvers. In April 2026, Genentech sought broader SLE application for obinutuzumab, citing a 76.7% SRI-4 response at 52 weeks, outpacing the 53.5% placebo response, potentially solidifying its foothold beyond nephritis. Meanwhile, Aurinia bolstered its lupus nephritis pipeline in March 2026, striking a deal to acquire Kezar Life Sciences at USD 6.955 per share, complemented by a contingent value right. The forthcoming competition in the lupus arena will hinge on companies' abilities to merge strong efficacy with user-friendly administration, enhanced safety monitoring, and demonstrable value for payers.

Lupus Industry Leaders

GSK plc

AstraZeneca plc

Bristol-Myers Squibb Company

Novartis AG

Pfizer Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: AstraZeneca received FDA approval for the Saphnelo Pen, a once-weekly subcutaneous autoinjector for SLE, based on Phase 3 TULIP-SC data. This is the first self-administered option for anifrolumab, enhancing patient access beyond infusion centers.

- April 2026: The FDA accepted Genentech's sBLA for Gazyva to expand its use in SLE, supported by Phase 3 ALLEGORY data showing a 76.7% SRI-4 response compared to 53.5% with placebo. A decision is expected by December 2026, with an EMA filing also submitted.

- March 2026: Aurinia Pharmaceuticals announced the acquisition of Kezar Life Sciences for USD 6.955 per share plus a contingent value right, adding zetomipzomib, a selective immunoproteasome inhibitor, to its lupus nephritis pipeline.

- October 2025: Roche secured FDA approval for Gazyva (or Gazyvaro) for lupus nephritis, supported by REGENCY Phase 3 data showing a 46.4% complete renal response with obinutuzumab plus standard therapy versus 33.1% with standard therapy alone.

Global Lupus Market Report Scope

As per the scope of the report, lupus is a chronic autoimmune disease in which the body's immune system mistakenly attacks healthy tissues and organs. This causes widespread inflammation that can damage the skin, joints, blood vessels, kidneys, lungs, and heart.

The lupus market is segmented by disease type, treatment and diagnosis, end-user, and geography. By disease type, the market includes systemic lupus erythematosus, cutaneous lupus erythematosus, and others. By treatment and diagnosis, the treatment market is segmented into corticosteroids, immunosuppressive drugs, biologic drugs, antimalarial drugs, antihypertensive drugs, and other treatment types, and the diagnosis market is categorized into laboratory tests, biopsy, imaging tests, and other diagnostic methods. By end-user, the market is segmented into hospitals, specialty clinics, homecare settings, and diagnostic laboratories. By geography, the market is analyzed across North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the market sizes and forecasts in terms of value (USD) for the above segments.

| Systemic Lupus Erythematosus |

| Cutaneous Lupus Erythematosus |

| Others |

| Treatment Type | Corticosteroids |

| Immunosuppressive Drugs | |

| Biologic Drugs | |

| Antimalarial Drugs | |

| Antihypertensive Drugs | |

| Other Treatment Types | |

| Diagnosis | Laboratory Tests |

| Biopsy | |

| Imaging Tests | |

| Other Diagnostic Methods |

| Hospitals |

| Specialty Clinics |

| Homecare Settings |

| Diagnostic Laboratories |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Disease Type | Systemic Lupus Erythematosus | |

| Cutaneous Lupus Erythematosus | ||

| Others | ||

| By Treatment and Diagnosis | Treatment Type | Corticosteroids |

| Immunosuppressive Drugs | ||

| Biologic Drugs | ||

| Antimalarial Drugs | ||

| Antihypertensive Drugs | ||

| Other Treatment Types | ||

| Diagnosis | Laboratory Tests | |

| Biopsy | ||

| Imaging Tests | ||

| Other Diagnostic Methods | ||

| By End User | Hospitals | |

| Specialty Clinics | ||

| Homecare Settings | ||

| Diagnostic Laboratories | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of the lupus market in 2026?

The lupus market is valued at USD 5.33 billion in 2026 and is projected to reach USD 8.54 billion by 2031, with a CAGR of 9.88% over the forecast period.

Which disease type contributes the most revenue in lupus treatment?

Systemic lupus erythematosus leads disease type demand and held 86.58% of the segment in 2025 because it involves multi-organ disease and higher treatment complexity.

Which treatment and diagnostic segment is growing the fastest in lupus management?

Treatment type are the fastest-growing category, with a projected 11.28% CAGR from 2026 to 2031 as non-invasive monitoring tools gain acceptance.

Which end-user setting dominates lupus care today?

Hospitals remain the leading end-user setting, with 41.43% of the segment in 2025, because infusion therapy, nephrology support, and relapse management still require hospital infrastructure.

Which region is expanding the fastest for lupus therapies?

Asia-Pacific is the fastest-growing region, with an 11.89% CAGR from 2026 to 2031, supported by a large patient base, regulatory momentum, and expanding specialty-care access.

Page last updated on: