Systemic Lupus Erythematosus Drugs Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

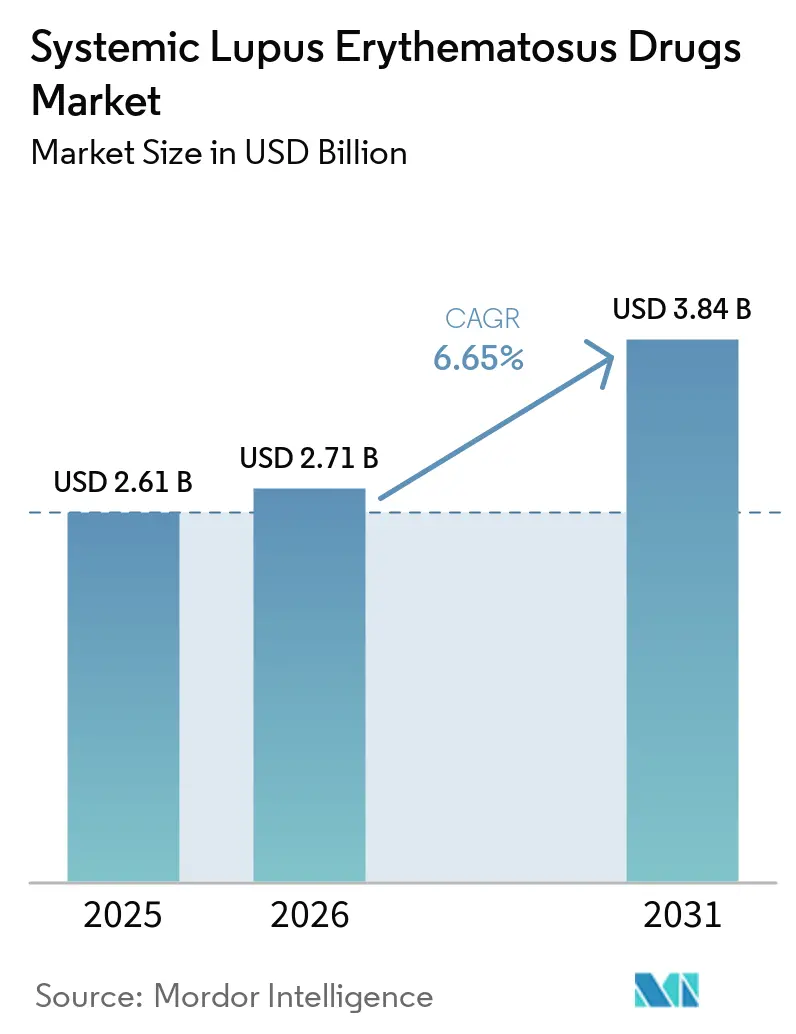

| Market Size (2026) | USD 2.71 Billion |

| Market Size (2031) | USD 3.84 Billion |

| Growth Rate (2026 - 2031) | 6.65% CAGR |

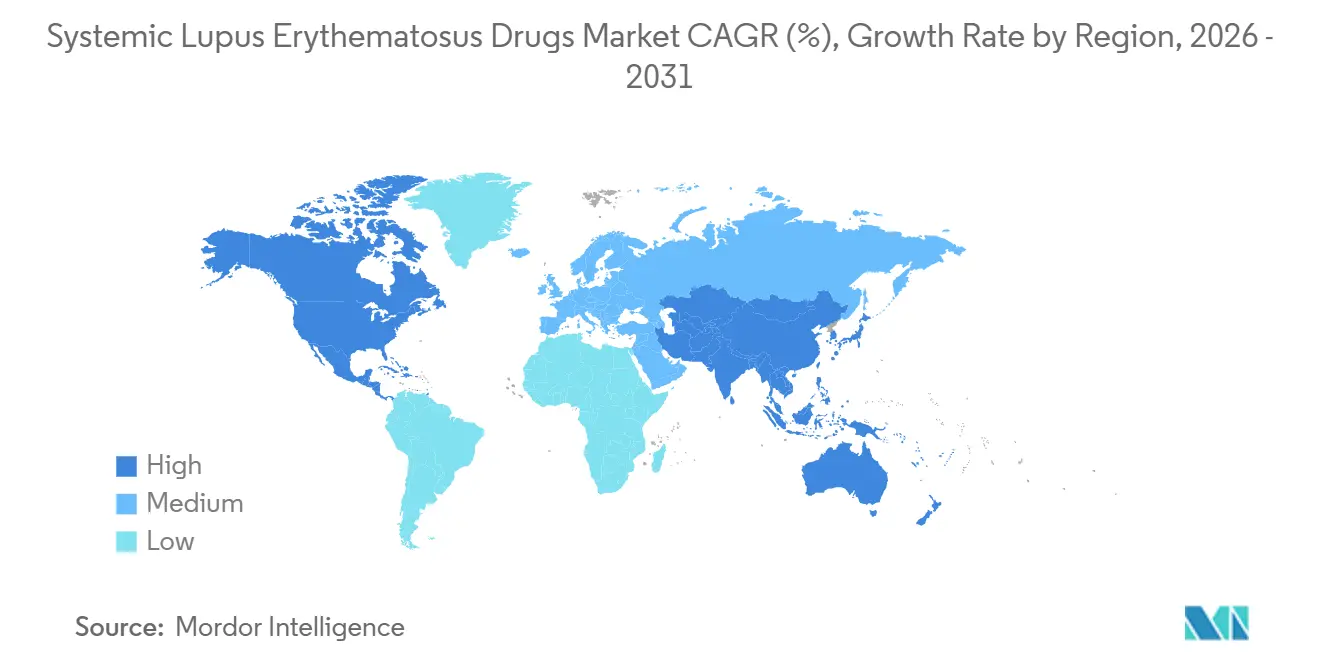

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Systemic Lupus Erythematosus Drugs Market Analysis by Mordor Intelligence

The Systemic Lupus Erythematosus Drugs Market size is expected to increase from USD 2.61 billion in 2025 to USD 2.71 billion in 2026 and reach USD 3.84 billion by 2031, growing at a CAGR of 6.65% over 2026-2031.

Growth is fueled by the maturation of precision-medicine diagnostics, accelerated biologic approvals, and the first wave of cell-based therapeutics that directly modulate disease drivers. Regulatory agencies are expanding the use of breakthrough and fast-track pathways, compressing development timelines, and incentivizing early-stage investments. Venture capital inflows topped USD 500 million in 2024 for autoimmune platforms, while global manufacturing expansions exceeding USD 8 billion signal long-term confidence in complex biologics and cell therapies. Companion-diagnostic adoption is simultaneously expanding the eligible patient pool and refining treatment selection, reinforcing a virtuous cycle of value-based reimbursement.

Key Report Takeaways

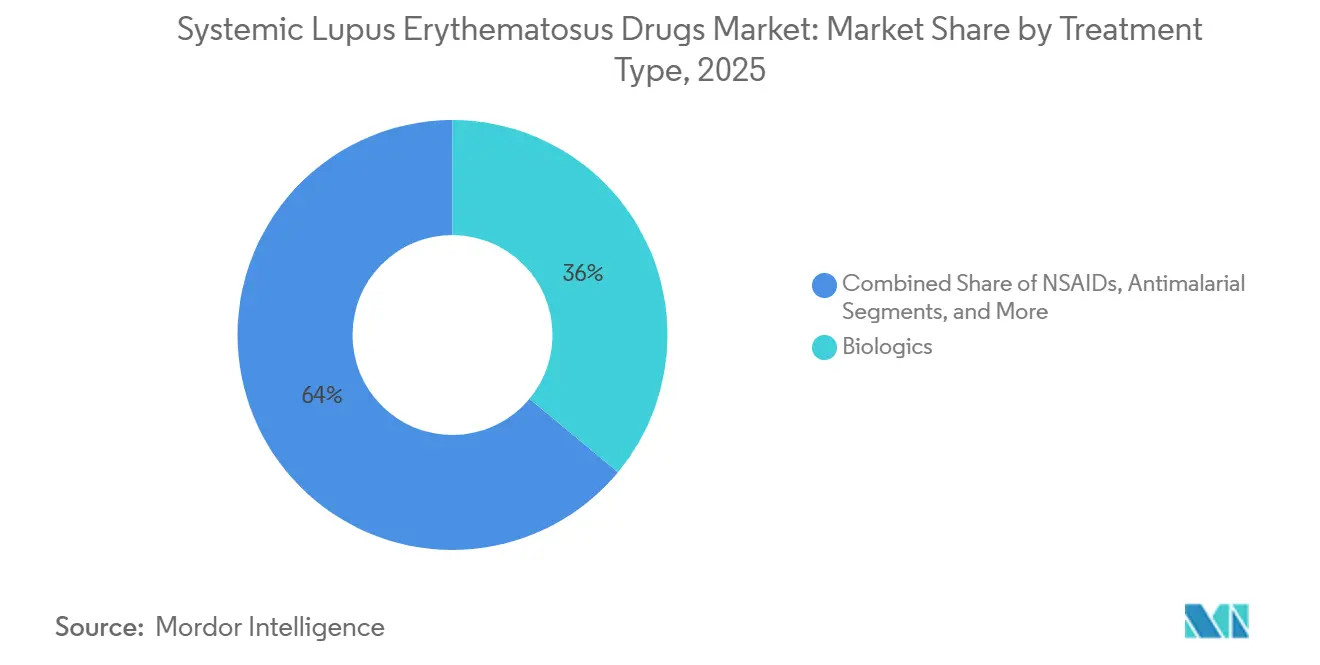

- By treatment type, biologics accounted for 36.02% of the systemic lupus erythematosus drugs market in 2025; stem-cell and gene-based therapies are forecast to grow at a 9.41% CAGR through 2031.

- By route of administration, intravenous formats held 58.10% share of the systemic lupus erythematosus drugs market in 2025, while subcutaneous delivery is projected to expand at a 10.15% CAGR to 2031.

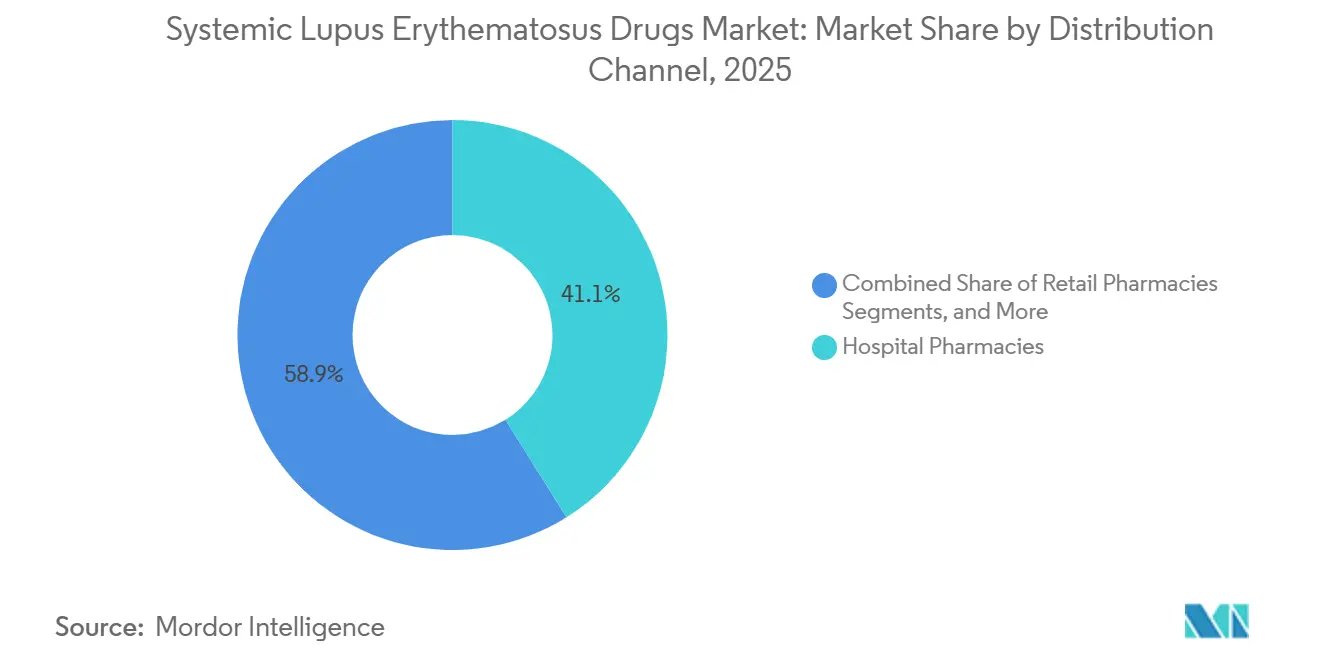

- By distribution channel, hospital pharmacies captured 41.05% of revenue in 2025, and online pharmacies are poised to grow at an 10.78% CAGR through 2031.

- By geography, North America led with 43.20% systemic lupus erythematosus drugs market share in 2025; Asia-Pacific is the fastest-growing region at a 8.72% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Systemic Lupus Erythematosus Drugs Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Rising Prevalence & Earlier Diagnosis of SLE | 1.20% | Global, with concentrated impact in North America & Europe | Medium term (2-4 years) |

| Rapid Approvals of Novel Biologics | 0.80% | North America & EU primary, spill-over to APAC | Short term (≤ 2 years) |

| Expansion of Companion-Diagnostic Biomarkers | 0.60% | Global, with early adoption in US & Germany | Medium term (2-4 years) |

| Tele-Rheumatology Boosting Access in Underserved Areas | 0.50% | APAC core, expanding to Latin America & MEA | Long term (≥ 4 years) |

| Venture Funding Surge for Autoimmune Biotech Platforms | 0.40% | North America & EU, with emerging activity in China | Short term (≤ 2 years) |

| Favorable Orphan-Drug & Fast-Track Designations | 0.30% | US primary, with EMA parallel pathways | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence and Earlier Diagnosis

Commercial biomarker panels detecting T-cell autoantibodies and cell-bound complement activation products (CB-CAPs) have moved lupus detection into an earlier therapeutic window. Medicare reimbursement of USD 840.65 per test for the AVISE panel in 2025 underscores payer support for molecular tools that enlarge the treatable cohort.[1]Exagen Medical Policy Team, “AVISE Lupus Test Coverage,” Arkansas Blue Cross and Blue Shield, arkansasbluecross.com Predictive assays like AMPEL’s LuGENE enable clinicians to alter therapy before clinical deterioration, directly expanding demand for targeted treatments across the systemic lupus erythematosus drugs market.

Rapid Approvals of Novel Biologics

The FDA’s acceptance of obinutuzumab’s supplemental application for lupus nephritis with an October 2025 decision timeline exemplifies the agency’s accelerated review posture.[2]Jared Kaltwasser, “Obinutuzumab in Lupus Nephritis,” HCPLive, hcplive.com Phase III data showed a 46.4% complete renal response versus 33.1% for standard care, establishing a new benchmark. Parallel fast-track designations for allogeneic CAR-T candidates from Adicet Bio and Sana Biotechnology further highlight momentum, positioning next-generation modalities to reshape competitive dynamics within the systemic lupus erythematosus drugs market.

Expansion of Companion-Diagnostic Biomarkers

Anti-C1q antibodies, Acute Flare Risk scoring, and AI-driven analytics are guiding biologic selection and dosage optimization. Cell-bound complement assays produce real-time disease-activity data, enabling therapy adjustments before irreversible organ injury occurs. Demonstrable outcome improvements justify premium pricing and facilitate reimbursement, reinforcing sustained uptake across the systemic lupus erythematosus drugs market.

Tele-Rheumatology Boosting Access

Digital health platforms now deliver specialist consultations to rural and underserved communities, reducing visit latency and improving monitoring frequency. Wearable sensors integrate fatigue, joint-motion, and activity data into rheumatology dashboards, supporting timely medication adjustments. Studies during the COVID-19 transition confirmed parity in disease-activity control between teleconsultations and in-person visits, validating the modality and expanding the addressable population for advanced therapies.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| High Therapy Cost & Reimbursement Hurdles | -0.90% | Global, with varying intensity by healthcare system | Long term (≥ 4 years) |

| Safety Concerns: Infection & Malignancy Risks | -0.70% | Global, with heightened scrutiny in regulated markets | Medium term (2-4 years) |

| Cold-Chain Complexity for mAbs & Cell Therapies | -0.50% | Global, with greater impact in emerging markets | Medium term (2-4 years) |

| Physician Inertia Toward Switching from Legacy Steroids | -0.40% | Global, with higher impact in traditional healthcare systems | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Therapy Cost and Reimbursement Hurdles

Despite Medicare’s USD 2,000 annual out-of-pocket cap for Part D in 2025, cumulative drug costs remain prohibitive for many patients. Payers demand real-world evidence and health-economic analyses before approving high-priced biologics, imposing step-therapy barriers that slow adoption. Biosimilar launches add marginal price pressure but have yet to meaningfully erode branded utilization in the systemic lupus erythematosus drugs market.

Safety Concerns: Infection and Malignancy Risks

Immunosuppressive profiles of biologics heighten susceptibility to infections such as herpes-zoster reactivation, noted in post-marketing surveillance of type I interferon inhibitors. CAR-T candidates introduce cytokine-release and autoimmune-complication risks requiring specialized management. Limited long-term safety data amplifies physician caution, tempering near-term penetration of novel therapies across the systemic lupus erythematosus drugs market.[3]Research Team, “Tele-rheumatology Outcomes,” Lupus Research Alliance, lupusresearch.org

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Treatment Type: Biologics Lead While Gene Therapies Surge

The systemic lupus erythematosus drugs market size for biologics translated to 36.02% of total sales in 2025. GSK’s Benlysta maintained double-digit growth, buoyed by expanded indications and an autoinjector format approved in 2024. Stem-cell and gene-based therapies, though nascent, hold the fastest growth outlook at a 9.41% CAGR as curative intent resonates with payers and patients.

Multiple CAR-T assets secured fast-track or orphan-drug status in 2024-2025, reflecting regulator confidence and investor appetite. Immunosuppressants and DMARDs remain clinical mainstays that enable steroid tapering, yet guideline updates from the American College of Rheumatology prioritize steroid minimization, indirectly boosting biologic adoption. Manufacturing scale-up globally points to a durable rise in demand across the systemic lupus erythematosus drugs market.

By Route of Administration: Subcutaneous Gains on IV Dominance

Intravenous delivery generated the majority of systemic lupus erythematosus drugs market revenue, corresponding to a 58.10% share in 2025. However, the systemic lupus erythematosus drugs market size linked to subcutaneous formats is expanding at a 10.15% CAGR through 2031. Patient-managed autoinjectors reduce clinic visits, cut infusion-center bottlenecks, and improve adherence. GSK’s pediatric Benlysta autoinjector and AstraZeneca’s late-stage subcutaneous anifrolumab illustrate the shift.

Cold-chain challenges and infusion-chair capacity constraints favor home-based administration, while device innovation from wearable pumps to needle-free injectors further erodes IV dominance. Oral routes remain limited to antimalarials and legacy immunosuppressants. Yet, ongoing formulation research targets oral delivery of smaller antibody fragments that could unlock new convenience thresholds within the systemic lupus erythematosus drugs market.

By Distribution Channel: Online Pharmacies Disrupt Traditional Models

Hospital pharmacies retained 41.05% channel share in 2025, benefiting from integrated care and access to complex infusion products. Online pharmacies, however, are scaling at an 10.78% CAGR, propelled by privacy, convenience, and specialty-pharmacy partnerships. AI-driven prior-authorization engines deployed by carriers such as Blue Shield of California have halved average approval times for specialty drugs, accelerating uptake.

Retail chains confront margin compression and operational complexity, prompting alliances with specialty distributors. Direct-to-patient cold-chain solutions, real-time temperature tracking, and at-home nursing support underpin the structural migration toward digital channels. These capabilities position e-pharmacies to capture an incremental share of high-value therapies in the systemic lupus erythematosus drugs market.

Geography Analysis

North America generated 43.20% of systemic lupus erythematosus drugs market revenue in 2025, supported by comprehensive insurance coverage, robust clinical-trial infrastructure and rapid uptake of FDA-designated breakthrough therapies. Implementation of the USD 2,000 Part D out-of-pocket ceiling in 2025 further reduces access barriers, while value-based contracting aligns payer incentives with outcome improvements. Canada’s evolving pan-Canadian Pharmaceutical Alliance negotiations shape pricing corridors, whereas Mexico’s Seguro Popular reforms introduce incremental reimbursement headroom.

Asia-Pacific is advancing at a 8.72% CAGR, the highest regional trajectory in the systemic lupus erythematosus drugs market. Japan approved voclosporin (LUPKYNIS) for lupus nephritis in 2024, creating precedent for accelerated filings of novel agents. China’s National Medical Products Administration adopted conditional approvals for domestic biologics such as telitacicept, while pilot reimbursement programs in Beijing and Shanghai subsidize targeted therapies. Australia listed anifrolumab on the Pharmaceutical Benefits Scheme in 2024, improving affordability and catalyzing market expansion. India and South Korea leverage expanding specialty-care networks and rising autoimmune-disease awareness to unlock latent demand.

Europe remains pivotal, anchored by established health-technology-assessment frameworks and stable reimbursement pathways. Germany’s early-benefit assessments embed real-world evidence requirements that reward durable efficacy, while the United Kingdom’s post-Brexit regulatory landscape continues to parallel EMA standards. Southern-European markets negotiate centralized tenders that temper price-growth but secure broad access. Real-world registries across France and Italy inform adaptive guidelines that integrate companion-diagnostic data, reinforcing precision-medicine adoption in the systemic lupus erythematosus drugs market.

Competitive Landscape

Competition is intensifying as legacy leaders confront disruptive modalities and precision medicine displaces empirical treatment selection. GSK, AstraZeneca, and Roche leverage deep commercial infrastructures to defend share, but biotech entrants capitalize on platform technologies that span multiple autoimmune indications. Sanofi’s USD 1.9 billion acquisition of Dren Bio’s DR-0201 underscores Big Pharma's appetite for differentiated mechanisms. GSK’s USD 300 million purchase of CMG1A46 extends its franchise beyond Benlysta.

Regulatory enthusiasm for cell therapies invites new competitors ranging from Adicet Bio to Sana Biotechnology, each targeting refractory systemic lupus with allogeneic CAR-T constructs. Manufacturing sophistication emerges as a competitive moat as players invest in viral-vector capacity, closed-system cell-processing, and GMP-compliant plasmid supply. Digital-health integration differentiates offerings: AstraZeneca’s partnership with a wearable biosensor firm captures patient-reported outcomes, while Roche embeds AI dosing calculators into its patient-support ecosystem. Collectively, these strategies elevate the systemic lupus erythematosus drugs market’s innovation bar and compress product life cycles.

White-space opportunities persist in underserved geographies and in companion-diagnostic co-development. Companies aligning drug and diagnostic launches secure reimbursement faster and obtain premium pricing. Tele-rheumatology alliances also become a strategic lever, extending specialist reach and embedding pharmaceutical brands in longitudinal care pathways. The October 2025 decision on obinutuzumab could re-rank market incumbents if favorable, setting a new efficacy baseline. Overall, competitive dynamics favor players that combine modality depth, digital-health fluency, and manufacturing agility within the systemic lupus erythematosus drugs market.

Systemic Lupus Erythematosus Drugs Industry Leaders

Eli Lilly and Company

Novartis AG

Viatris Inc.

GSK Plc

ImmuPharma

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Johnson & Johnson announced that the U.S. Food and Drug Administration (FDA) has granted Fast Track designation to nipocalimaba as a potential treatment for adults with systemic lupus erythematosus (SLE), a severe autoantibody-driven disease affecting approximately 3 to 5 million people worldwide.

- March 2025: The FDA accepted Roche's supplemental Biologics License Application for Gazyva (obinutuzumab) in lupus nephritis, with a decision expected by October 2025, based on Phase III REGENCY trial results showing 46.4% complete renal response versus 33.1% with standard therapy alone.

- February 2025: Adicet Bio received FDA Fast Track designation for ADI-001, an allogeneic gamma delta CAR-T cell therapy, for refractory systemic lupus erythematosus with extrarenal involvement, marking the second Fast Track designation for this investigational therapy.

Global Systemic Lupus Erythematosus Drugs Market Report Scope

As per the scope of the report, systemic lupus erythematosus (SLE) drugs are medications designed to manage chronic autoimmune inflammation, reduce flares, and prevent organ damage. Key treatments include hydroxychloroquine (foundational antimalarial), corticosteroids (like prednisone) for inflammation, and immunosuppressants (like mycophenolate, azathioprine, methotrexate) for severe cases. Recent FDA-approved biologics include belimumab and anifrolumab.

The systemic lupus erythematosus drugs market is segmented by treatment type, route of administration, distribution channel, and geography. By treatment type, the market includes Non-Steroidal Anti-Inflammatory Drugs (NSAIDs), antimalarials, corticosteroids, immunosuppressants/DMARDs, biologics, and stem-cell & gene-based therapies. By route of administration, the market is segmented into oral, intravenous, and subcutaneous. By distribution channel, the market is categorized into hospital pharmacies, retail pharmacies, and online pharmacies. By geography, the market is analyzed across North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the market sizes and forecasts in terms of value (USD) for the above segments.

| Non-Steroidal Anti-Inflammatory Drugs (NSAIDs) |

| Antimalarials |

| Corticosteroids |

| Immunosuppressants / DMARDs |

| Biologics |

| Stem-cell & Gene-based Therapies |

| Oral |

| Intravenous |

| Subcutaneous |

| Hospital Pharmacies |

| Retail Pharmacies |

| Online Pharmacies |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Treatment Type | Non-Steroidal Anti-Inflammatory Drugs (NSAIDs) | |

| Antimalarials | ||

| Corticosteroids | ||

| Immunosuppressants / DMARDs | ||

| Biologics | ||

| Stem-cell & Gene-based Therapies | ||

| By Route of Administration | Oral | |

| Intravenous | ||

| Subcutaneous | ||

| By Distribution Channel | Hospital Pharmacies | |

| Retail Pharmacies | ||

| Online Pharmacies | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current size of the systemic lupus erythematosus drugs market?

The market generated USD 2.71 billion in 2026 and is on track to reach USD 3.84 billion by 2031.

Which treatment segment holds the largest share?

Biologics led with 36.02% of revenue in 2025, anchored by products such as Benlysta.

Which region is growing fastest?

Asia-Pacific shows the highest growth, expanding at a 8.72% CAGR through 2031, driven by regulatory harmonization and rising healthcare investment.

What are the main growth drivers?

Earlier diagnosis through advanced biomarkers, rapid biologic approvals, and tele-rheumatology that broadens specialty care access are pivotal drivers.

Why are subcutaneous formulations gaining traction?

They enable home administration, reduce infusion-center dependency, and align with patient-centric care, resulting in a projected 10.15% CAGR for subcutaneous delivery.

Page last updated on: