Transverse Myelitis Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 0.8 Billion |

| Market Size (2031) | USD 1.01 Billion |

| Growth Rate (2026 - 2031) | 4.85% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

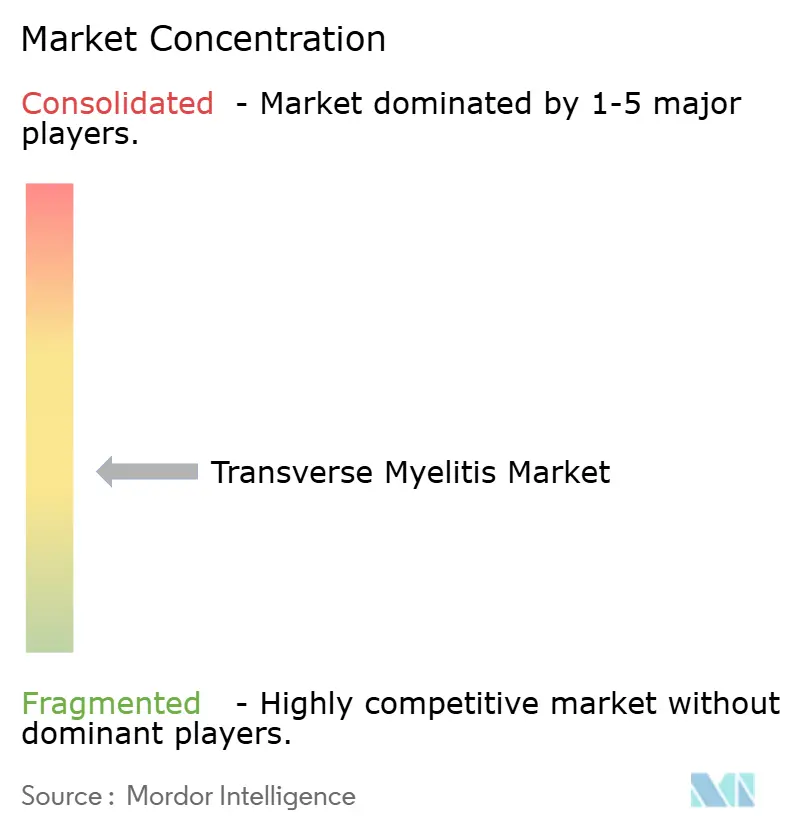

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Transverse Myelitis Market Analysis by Mordor Intelligence

The Transverse Myelitis Market size is expected to grow from USD 0.76 billion in 2025 to USD 0.8 billion in 2026 and is forecast to reach USD 1.01 billion by 2031 at 4.85% CAGR over 2026-2031.

The market is expanding even without a therapy approved specifically for transverse myelitis because care spending is spread across MRI, cerebrospinal fluid testing, antibody panels, acute steroids, plasma exchange, biologic maintenance borrowed from NMOSD practice, and long rehabilitation needs. The transverse myelitis market also benefits from faster use of cell-based AQP4-IgG and MOG-IgG testing, which improves etiologic classification and moves more patients into defined treatment pathways. Wider clinical interest in GFAP and neurofilament markers is increasing attention on objective measurement of neuroinflammatory injury, even though routine use remains selective and not yet fully standardized. Reimbursement remains a practical constraint in the transverse myelitis market because biologic access often depends on serostatus confirmation, which gives diagnostic platforms a direct role in whether higher-value treatment revenue can be realized. The transverse myelitis market also carries a durable post-acute spending tail because incomplete recovery, disability management, and structured rehabilitation keep patients in care long after the first inflammatory episode has passed.

Key Report Takeaways

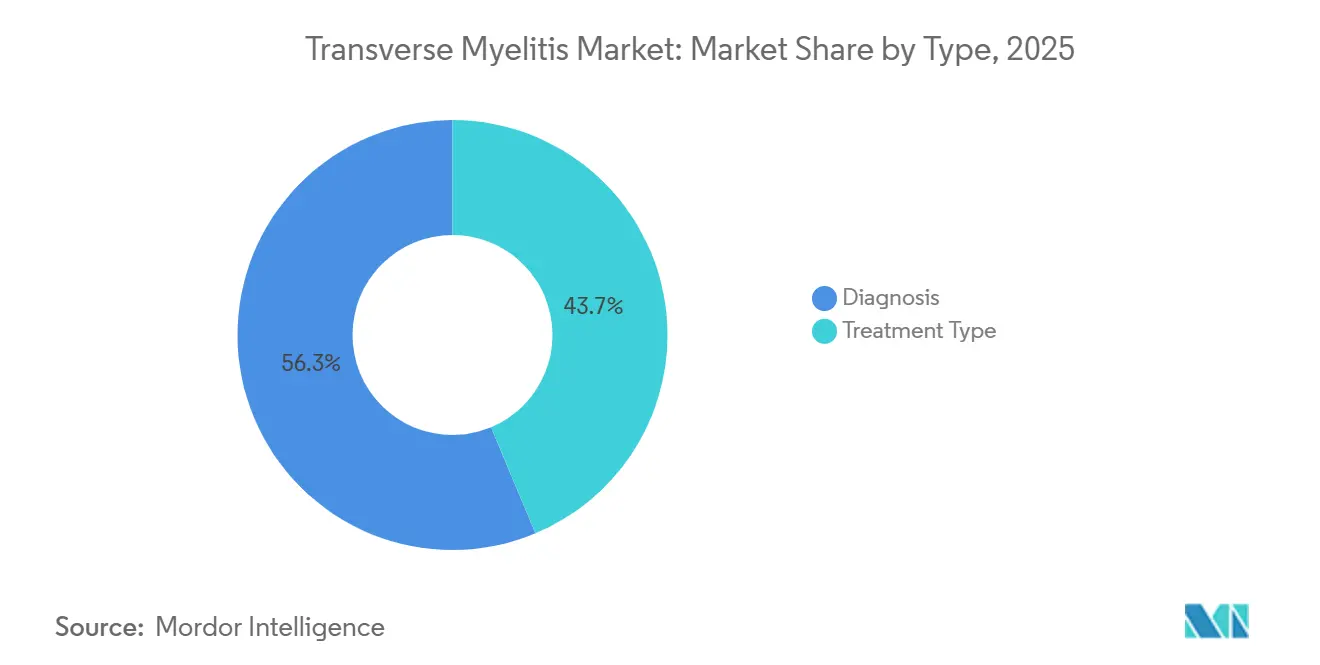

- By type, diagnosis held 56.31% of transverse myelitis market share in 2025, while treatment type is forecast to expand at 7.38% CAGR through 2031.

- By etiology, idiopathic transverse myelitis accounted for 40.24% share in 2025, while autoimmune disease-associated transverse myelitis is projected to record the fastest CAGR at 8.52% through 2031.

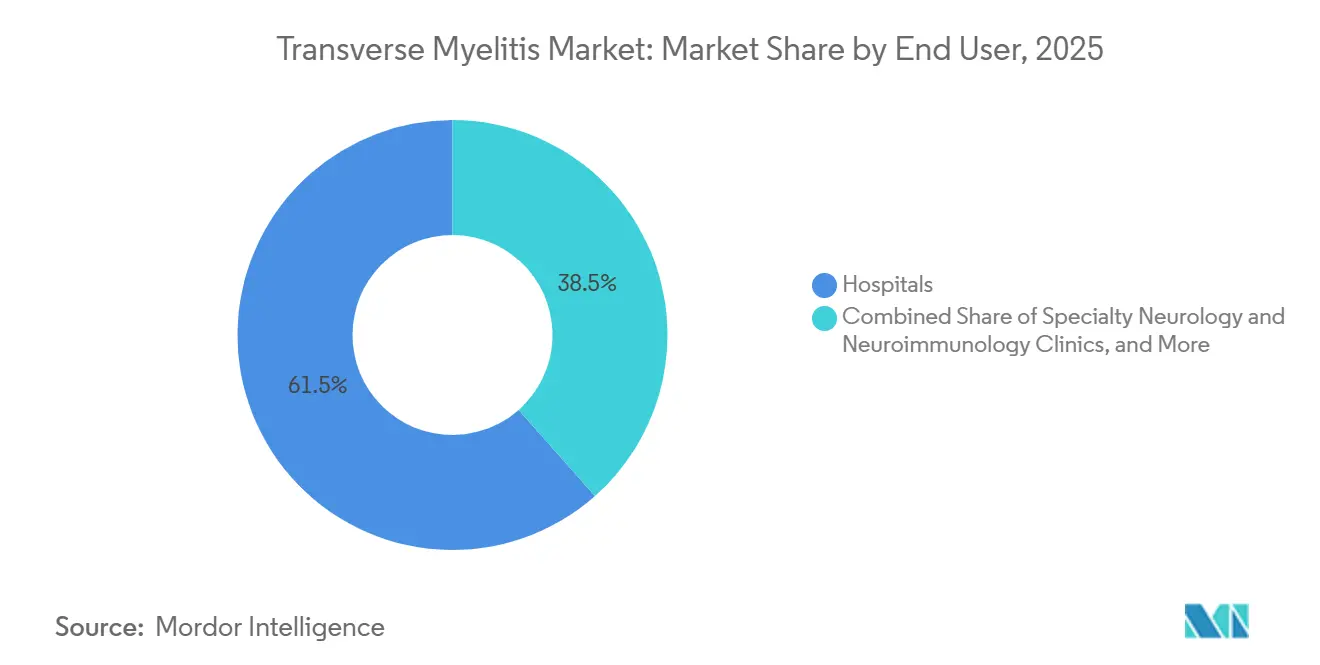

- By end user, hospitals accounted for 61.52% share of the transverse myelitis market size in 2025, while home care settings are projected to grow at 8.25% CAGR through 2031.

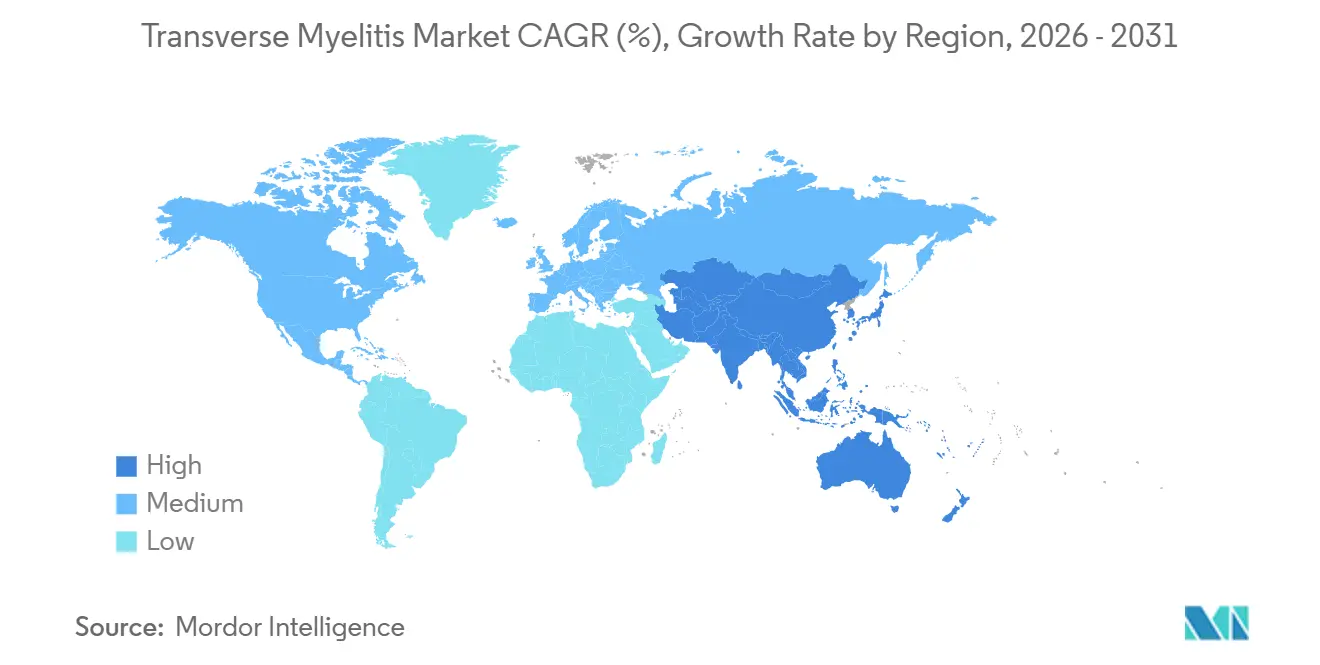

- By geography, North America held 39.24% share of the transverse myelitis market size in 2025, while Asia-Pacific is expected to advance at 7.83% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Transverse Myelitis Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Faster MRI, CSF, and antibody workups | +1.1% | Global, with concentrated gains in North America and Western Europe | Short term (≤ 2 years) |

| TM-adjacent biologic adoption from NMOSD and MOGAD | +1.4% | North America, EU, Japan | Medium term (2-4 years) |

| Expansion of specialist neuroimmunology centers | +0.5% | North America, APAC core, including Japan, China, and India | Medium term (2-4 years) |

| Long-tail rehabilitation demand | +0.4% | Global, with highest intensity in North America and Europe | Long term (≥ 4 years) |

| GFAP and NfL workflow commercialization | +0.5% | North America and EU, with spillover into APAC | Short term (≤ 2 years) |

| Tele-neuroimmunology and home-infusion access | +0.3% | North America, EU, and urban APAC | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Faster MRI, CSF, and Antibody Workups Compress Diagnostic Timelines

The transverse myelitis market is gaining from faster diagnostic workflows because MRI, CSF studies, and antibody testing are moving patients into defined care pathways sooner. High-field spinal MRI with gadolinium and STIR sequences remains central to distinguishing shorter inflammatory lesions from longitudinally extensive disease that points toward NMOSD or MOGAD. MENACTRIMS guidance published in 2026 formally favored cell-based assay testing over ELISA for AQP4-IgG, citing 76.7% sensitivity for CBA versus 47% for ELISA and specificity that can reach 100% for CBA. That shift matters commercially in the transverse myelitis market because better antibody resolution reduces the pool of poorly defined cases and increases the share of patients who can be classified into autoimmune or demyelinating subtypes. It also strengthens the link between laboratory capability and downstream treatment access because diagnosis is no longer only an entry step, but a direct gate for the therapies physicians are able to use in routine practice. Faster diagnostic cycles therefore support both volume and value in the transverse myelitis market, especially in tertiary neurology systems where testing and treatment decisions are closely integrated.

TM-Adjacent Biologic Adoption from NMOSD and MOGAD Reshapes Treatment Economics

The market has no dedicated approved drug for the core indication, yet treatment economics are being reshaped by NMOSD biologics that now influence care for seropositive patients. Current NMOSD practice includes eculizumab, ravulizumab, inebilizumab, and satralizumab for AQP4-IgG-positive disease, and these agents have changed expectations for relapse prevention in patients whose transverse myelitis presentation falls inside that serologic framework. The German multicenter cohort showed that rituximab and azathioprine remained the dominant real-world choices, while newly approved therapies rose to 12.3% of treatment episodes by 2022 and kept gaining relevance. That pattern supports a higher-value tier inside the transverse myelitis market because confirmed seropositive patients can move from generic acute management into longer-duration biologic maintenance pathways. MOGAD remains less settled because no disease-specific approval exists and current evidence for IL-6 targeting is still based on small or observational datasets, but the direction of travel is clear. As serostatus testing becomes more routine, the transverse myelitis market is likely to see a larger share of episodes managed under defined neuroimmunology protocols rather than broad idiopathic labels.

GFAP and NfL Workflow Commercialization Converts Inflammation Events into Structured Diagnostic Activity

The transverse myelitis market is also being shaped by growing interest in serum GFAP and neurofilament markers as measurable signs of astrocyte injury and axonal damage. Clinical guideline and review literature show that GFAP and neurofilament signals are increasingly relevant in NMOSD-related workups, even though routine use remains selective and clinical interpretation still requires context. BioDrugs noted that serum GFAP is promising as a disease activity marker in NMOSD and that detection often depends on highly sensitive Simoa-based testing, which keeps this part of the workflow concentrated in advanced laboratory settings. The practical result for the transverse myelitis market is that biomarker testing is adding another layer to the diagnostic pathway, especially when clinicians want stronger objective support for inflammatory activity or treatment monitoring. This does not replace MRI or antibody panels, but it does widen the role of laboratory medicine in neurology workups and follow-up care. Over time, that keeps the transverse myelitis market more connected to precision diagnostics and specialized testing infrastructure than symptom-led management alone would suggest.

Tele-Neuroimmunology and Home-Infusion Access Shift Site of Care

The market is seeing a gradual site-of-care shift as virtual specialist access and home-based administration models expand beyond major academic centers. Indiana University School of Medicine reported the development of Indiana’s first pediatric neuroimmunology clinic in 2026, reducing the need for families to travel out of state for specialized autoimmune neurology care. CHLA already combines infusion care, plasmapheresis access, virtual visits, rehabilitation, and multidisciplinary coordination in one neuroimmunology service model, which shows how provider systems are reorganizing delivery around continuity rather than a single acute episode. That matters in the transverse myelitis market because home-friendly biologic options and remote monitoring shift a growing share of ongoing care away from hospital infusion centers and toward specialty pharmacy and home-support channels[1]Children’s Hospital Los Angeles, “Neuroimmunology and Neuroinflammation Treatments,” Children’s Hospital Los Angeles, chla.org. The home care segment’s stronger growth rate fits this care redesign, especially where monthly self-injection and virtual follow-up reduce the burden of recurrent hospital visits. As a result, the transverse myelitis market is becoming more distributed across care settings, even while acute rescue care remains hospital-centered.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| No TM-specific approved therapies | -0.8% | Global | Long term (≥ 4 years) |

| High biologic, PLEX, and rehab costs | -0.6% | Global, most acute in lower-income APAC, MEA, and South America | Medium term (2-4 years) |

| PLEX capacity bottlenecks | -0.3% | North America and EU, especially tertiary hospital settings | Short term (≤ 2 years) |

| Diagnostic gray zones across TM, NMOSD, MOGAD, and GFAP astrocytopathy | -0.4% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

No TM-Specific Approved Therapies Sustains a Reimbursement Gray Zone

The market still faces a structural ceiling because no FDA-approved or EMA-approved therapy exists specifically for transverse myelitis as a standalone indication. Standard acute care still relies on high-dose intravenous methylprednisolone, with plasma exchange used early for severe or steroid-refractory attacks, while long-term biologic treatment is usually tied to NMOSD serostatus rather than to a pure TM label. That leaves a large commercial divide inside the transverse myelitis market because patients with confirmed AQP4-IgG positivity can access premium treatment pathways, while seronegative or unresolved cases often remain in lower-value steroid and supportive care tracks. The diagnostic burden is also heavier in cases that overlap with MOGAD, systemic autoimmune disease, or other inflammatory myelopathies, since treatment decisions depend on excluding close mimics with enough confidence. Until either TM-specific trials succeed or biomarker-defined indications widen further, the transverse myelitis market will continue to under-convert disease burden into treatment revenue.

High Biologic, PLEX, and Rehabilitation Costs Constrain Market Penetration

The transverse myelitis market is also limited by the high cost profile of specialty biologics, repeated rescue procedures, and long rehabilitation needs, even though the underlying clinical need remains strong. Frontiers in Immunology showed that late-onset NMOSD patients received more intensive acute treatment, including higher steroid exposure and more apheresis, yet still had worse recovery and faster disability accumulation than younger patients. That weakens the economic case for broad escalation when payers are already selective and when outcomes do not improve in a straight line with spending intensity. Rehabilitation adds another layer because case literature shows that recovery can require months or years of structured therapy, gait retraining, assistive support, and specialist follow-up after the acute episode. In lower-resource settings, this pushes the transverse myelitis market toward diagnostics and acute management first, while full access to long-duration biologic maintenance and advanced rehab remains uneven.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Diagnostics Lead on Volume While Treatment Expands on Value

Diagnosis accounted for 56.31% of transverse myelitis market share in 2025, which reflects how every suspected case moves through imaging, CSF analysis, and laboratory testing before treatment direction becomes clear. MRI remains the core tool because spinal cord lesion length, distribution, and contrast behavior help separate short-segment inflammatory events from longitudinally extensive disease that is more suggestive of NMOSD or MOGAD. CSF workups also remain central because pleocytosis, oligoclonal bands, IgG index, and infection exclusion still shape the clinical picture and the differential diagnosis. Within diagnostics, the fastest operational change has come from higher use of AQP4-IgG and MOG-IgG cell-based assays, which move care away from a syndromic label and toward a more actionable disease framework[2]Bassem Yamout et al., “Consensus Recommendations for the Diagnosis and Treatment of Neuromyelitis Optica Spectrum Disorders,” CNS Drugs, menactrims.org. The transverse myelitis industry therefore remains volume-led on the diagnostic side because each new or relapsing patient generates repeat testing demand across different stages of care.

Treatment type remains smaller, but it is projected to grow at 7.38% CAGR from 2026 to 2031 as the highest-value layer of the transverse myelitis market gains more structure around relapse prevention. Acute care still centers on intravenous steroids first and plasma exchange or IVIG when escalation is needed, especially in severe or poorly responsive myelitis. Maintenance treatment is where revenue intensity rises because rituximab, azathioprine, and newer NMOSD biologics expand use when antibody-confirmed patients need ongoing relapse control. Rehabilitation and symptom management also belong inside the treatment segment because persistent gait, bladder, pain, spasticity, and sexual dysfunction needs keep spending active beyond the acute inflammatory event. This mix keeps the transverse myelitis market balanced between high-volume diagnosis and high-value therapy, with the latter expected to grow faster as classification improves.

By Etiology: Idiopathic Cases Stay Large While Autoimmune Classification Gains Ground

Idiopathic transverse myelitis held 40.24% share in 2025, which shows that a large part of the transverse myelitis market still begins with cases that cannot be fully assigned to a confirmed cause at first presentation. That position is consistent with medical reference and guideline literature showing that transverse myelitis remains a heterogeneous syndrome that overlaps with multiple inflammatory, infectious, autoimmune, and neoplastic processes. These idiopathic cases often stay in lower-value care pathways because treatment focuses on corticosteroids, rescue plasma exchange, monitoring, and supportive care rather than automatic access to targeted maintenance biologics. The size of this segment therefore reflects unresolved diagnostic complexity more than it reflects premium revenue per patient. In the transverse myelitis market, that makes idiopathic volume important for service demand, but less powerful for value expansion than serology-linked subtypes.

Autoimmune disease-associated transverse myelitis is projected to grow at 8.52% CAGR through 2031, which makes it the fastest-rising etiologic segment as co-testing becomes more systematic. MENACTRIMS guidance specifically recommends active exclusion of systemic autoimmune disease in LETM presentations, including conditions such as Sjögren syndrome, lupus, Behçet disease, and GFAP astrocytopathy. Demyelinating disease-associated cases carry the highest revenue potential because AQP4-IgG-positive NMOSD and some MOGAD presentations open a clearer path to chronic immunotherapy and specialist follow-up. Post-infectious cases keep episodic treatment demand relevant, while rare paraneoplastic cases connect the transverse myelitis market to broader antibody-panel and oncology workups described in clinical references. The overall etiology mix is therefore shifting slowly from broad idiopathic labeling toward more defined autoimmune and demyelinating classifications, which is one of the clearest structural changes in the transverse myelitis market.

By End User: Hospitals Hold the Core While Home Care Builds Momentum

Hospitals held 61.52% share of the transverse myelitis market size in 2025 because the acute phase still depends on emergency imaging, lumbar puncture capacity, intravenous steroids, and access to plasma exchange. This concentration also reflects the severity of some cervical or longitudinally extensive presentations, where respiratory compromise, rapid weakness progression, or severe autonomic dysfunction require close inpatient monitoring. Specialty neurology and neuroimmunology clinics support the outpatient side of the transverse myelitis market by handling biologic initiation, surveillance, multidisciplinary follow-up, and repeat decision-making after relapses. Diagnostic centers also keep a steady role because antibody testing, follow-up MRI, and selected biomarker workups create recurring demand beyond the first hospital admission. That is why the hospital segment remains dominant even as parts of longitudinal care begin to shift elsewhere.

Home care settings are projected to grow at 8.25% CAGR through 2031, making them the fastest-rising end-user channel in the transverse myelitis market. The main reason is that self-injected or lower-touch maintenance therapy, tele-neuroimmunology follow-up, and home-supported coordination are reducing the need for every chronic encounter to return to a hospital campus. Rehabilitation centers remain structurally important because prolonged recovery can involve gait training, assistive technologies, bladder care, electrical stimulation, and long supervision after the acute attack. The CHLA model shows how infusion care, plasmapheresis, rehabilitation, virtual visits, and second opinions can sit within an integrated provider network rather than in a single department. As a result, the transverse myelitis market is keeping hospitals at the center of acute revenue while gradually shifting more chronic management into distributed care settings.

Geography Analysis

North America held 39.24% share of the transverse myelitis market size in 2025, and the region remains the leading revenue contributor because specialist neuroimmunology care, advanced MRI access, and broad antibody testing infrastructure are already well established. The United States anchors this position through dense tertiary neurology networks and earlier adoption of structured NMOSD treatment algorithms that influence seropositive transverse myelitis management. Acute care is also easier to coordinate in the region because MRI, CSF studies, infusion support, and plasma exchange are more likely to sit within the same hospital ecosystem. Provider-level examples such as CHLA show how the transverse myelitis market in North America is supported by integrated programs that connect infusion services, plasmapheresis, rehabilitation, virtual care, and transition planning. These factors keep North America ahead on both diagnosis intensity and high-value maintenance therapy adoption.

Europe is the second-largest regional cluster in the transverse myelitis market, although reimbursement and treatment access still vary by country. Germany and the United Kingdom remain important reference points because real-world evidence from 19 German centers showed rituximab at the center of practice, while newer approved biologics were steadily increasing their share of treatment episodes. France, Italy, and Spain add volume through academic neurology networks and access to EMA-recognized neuroimmunology therapies reflected in regional guidance. Eastern and Southern Europe still show diagnostic undercount, and the Bulgarian NMOSD consensus highlights the need for stronger epidemiologic visibility rather than suggesting low true disease burden[3]I. Milanov and S. Ivanova, “National Consensus on the Diagnosis and Treatment of Neuromyelitis Optica Spectrum Disorders,” Bulgarian Society of Neurology, nevrologiabg.com.

Asia-Pacific is the fastest-growing region in the transverse myelitis market, with a projected CAGR of 7.83% from 2026 to 2031. Japan stands out because the female-to-male ratio in AQP4-IgG seropositive NMOSD can reach 10 to 1, which points to a strong pool of patients relevant to NMOSD-associated transverse myelitis care. Chugai’s position around satralizumab also reinforces Japan’s commercial role in this treatment space through local development and brand presence. China and India are expanding diagnostic capacity through hospital modernization, but India still faces practical challenges in MOG-IgG testing accuracy and interpretation, especially when fixed assays are used without enough phenotype and MRI correlation. The Middle East and Africa remain earlier-stage contributors, while South America is building from academic participation and broader immunotherapy awareness, so growth there is present but still constrained by uneven access to advanced diagnostics, biologics, and rehabilitation.

Competitive Landscape

The transverse myelitis market is moderately fragmented because no single company controls the full care chain, and competition is split across diagnostics, biologics, plasma exchange systems, and rehabilitation-related services. That structure means leadership is layered rather than unified, with one group of companies strongest in imaging and laboratory workups, another in relapse prevention biologics, and a different set in apheresis support. In biologics, Alexion and AstraZeneca, Amgen through the Uplizna franchise, and Roche, Genentech, and Chugai through satralizumab compete around the highest-value seropositive patient pool shaped by NMOSD practice. Real-world evidence still shows rituximab and azathioprine as the practical base of care in many settings, which means premium products must compete not only with each other, but also with entrenched lower-cost standards. This keeps pricing power in check and gives the transverse myelitis market a more contested treatment layer than a simple orphan-drug narrative would imply.

A second competitive front in the transverse myelitis market sits in diagnostics, where clinical utility and assay quality can decide whether patients reach higher-value maintenance therapy at all. MENACTRIMS and other clinical sources reinforce the importance of cell-based assays for AQP4-IgG and MOG-IgG, which supports specialist laboratories and high-confidence testing providers over less sensitive formats. Biomarker-focused players also benefit from this trend because serum GFAP and neurofilament testing are adding another layer to differential diagnosis and disease monitoring, even if use remains selective. A third front is forming around MOGAD, where no approved therapy exists and IL-6 targeting remains one of the most watched future areas according to published reviews. This creates a clear white space that could alter the competitive map if future trials translate into approved labels for relapse prevention in MOGAD-related transverse myelitis pathways.

Company and provider actions already show how competition is being built through capability expansion rather than through one single product launch. Fresenius Kabi submitted a 510(k) notification in 2024 for Aurora Xi software with a new adaptive nomogram and then expanded deployment across BioLife Plasma centers in 2025, showing continued investment around plasmapheresis efficiency and system performance. Chugai’s commercial role around satralizumab in Japan remains another important strategic position because regional brand strength matters in a specialist disease area with concentrated prescriber influence. CHLA and Indiana University also show that provider competition matters in the transverse myelitis market because care networks that combine neuroimmunology expertise, infusion support, rehabilitation, and virtual access can capture more of the patient pathway than stand-alone departments. Taken together, these moves keep the transverse myelitis market competitive, specialized, and only moderately concentrated.

Transverse Myelitis Industry Leaders

F. Hoffmann-La Roche AG

Alexion Pharmaceuticals

Amgen

CSL Behring

Grifols

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Openwater, an open-source medical technology company, partnered with the Sharma Lab to develop portable, hospital-grade devices. Their research focuses on improving spasticity, neuropathic pain, bowel and bladder function, walking impairments from transverse myelitis, and essential tremors.

- April 2026: The Phase 3 METEOROID trial showed the IL-6 blocker satralizumab reduces MOGAD relapses by 68%, with quick results and placebo-like safety. The trial ended after 28 relapses, defined as optic neuritis, transverse myelitis, or brain attack with MRI-confirmed T2 lesions.

Global Transverse Myelitis Market Report Scope

As per the scope of the report, transverse myelitis is a neurological condition characterized by inflammation of the spinal cord. This inflammation can damage or destroy myelin, the protective covering of nerve fibers, leading to symptoms such as weakness, sensory disturbances, and sometimes paralysis, depending on the severity and location of the inflammation.

The segmentation of the transverse myelitis market is categorized by type, etiology, end user, and geography. By type, the market is divided into diagnosis, which includes MRI, lumbar puncture/CSF analysis, and blood tests and antibody testing, and treatment type, which comprises acute pharmacotherapy, acute rescue procedures, maintenance and relapse-prevention therapies, rehabilitation therapies, and symptom management. By etiology, the market is segmented into idiopathic transverse myelitis, post-infectious transverse myelitis, autoimmune disease-associated transverse myelitis, demyelinating disease-associated transverse myelitis, and paraneoplastic transverse myelitis. By end user, the segmentation includes hospitals, specialty neurology and neuroimmunology clinics, rehabilitation centers, home care settings, and diagnostic centers. By geography, the market is analyzed across North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. For each segment, the market size and forecast are provided in terms of value (USD).

| Diagnosis | MRI |

| Lumbar Puncture / CSF Analysis | |

| Blood Tests and Antibody Testing | |

| Treatment Type | Acute Pharmacotherapy |

| Acute Rescue Procedures | |

| Maintenance and Relapse-Prevention Therapies | |

| Rehabilitation Therapies | |

| Symptom Management |

| Idiopathic Transverse Myelitis |

| Post-infectious Transverse Myelitis |

| Autoimmune Disease-associated Transverse Myelitis |

| Demyelinating Disease-associated Transverse Myelitis |

| Paraneoplastic Transverse Myelitis |

| Hospitals |

| Specialty Neurology and Neuroimmunology Clinics |

| Rehabilitation Centers |

| Home Care Settings |

| Diagnostic Centers |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Type | Diagnosis | MRI |

| Lumbar Puncture / CSF Analysis | ||

| Blood Tests and Antibody Testing | ||

| Treatment Type | Acute Pharmacotherapy | |

| Acute Rescue Procedures | ||

| Maintenance and Relapse-Prevention Therapies | ||

| Rehabilitation Therapies | ||

| Symptom Management | ||

| By Etiology | Idiopathic Transverse Myelitis | |

| Post-infectious Transverse Myelitis | ||

| Autoimmune Disease-associated Transverse Myelitis | ||

| Demyelinating Disease-associated Transverse Myelitis | ||

| Paraneoplastic Transverse Myelitis | ||

| By End User | Hospitals | |

| Specialty Neurology and Neuroimmunology Clinics | ||

| Rehabilitation Centers | ||

| Home Care Settings | ||

| Diagnostic Centers | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the expected growth outlook for transverse myelitis market?

The transverse myelitis market size was valued at USD 0.76 billion in 2025 and estimated to grow from USD 0.80 billion in 2026 to reach USD 1.01 billion by 2031, at a CAGR of 4.85% during the forecast period 2026 to 2031.

Why does diagnosis account for the largest share of spending?

Diagnosis led with 56.31% share in 2025 because MRI, CSF studies, and antibody testing are required across nearly every suspected case before treatment can be tailored.

Which part of care is growing the fastest?

Treatment type is the fastest-growing segment with a 7.38% CAGR through 2031 because biologic maintenance, relapse prevention, and long-term symptom management raise value per patient.

Why are hospitals still the main end-user setting?

Hospitals held 61.52% share in 2025 because acute care often needs urgent MRI, lumbar puncture, intravenous steroids, and plasma exchange in one setting.

Which region offers the strongest near-term expansion opportunity?

Asia-Pacific is projected to grow fastest at 7.83% CAGR through 2031, supported by stronger diagnostic capacity and a favorable NMOSD-linked patient profile in Japan.

What is the biggest commercial constraint for this field?

The largest constraint is the lack of a therapy approved specifically for transverse myelitis, which keeps reimbursement tied to serostatus and limits broad access to high-value biologic treatment.

Page last updated on: